24

Canadian Oil and Gas Outlook In association with: April 2011 www.mergermarket.com

Canadian Oil and Gas Outlook

In association with:

April 2011w

ww

.mergerm

arket.com

ContentsExecutive Summary 3

Methodology 3

Overview 4

Cross-border outlook 9

Targeted industry forecast 12

Strategies 15

Market movers 18

About Blakes 22

About mergermarket 23

Canadian Oil & Gas Outlook

3www.mergermarket.com

Blake, Cassels & Graydon LLP is pleased to present this Canadian Oil and Gas Outlook, published in association with mergermarket. Based on a series of interviews with over 100 executives and investment bankers focused on the Canadian oil and gas market, this report provides a detailed analysis of key challenges, opportunities and developments in the sector.

Oil and gas M&A activity in Canada is set for a steady increase in the next 12 months. Seventy-nine percent of respondents expect deal volume to increase during this period, and 71% expect the same of average deal values, driven by improved economic conditions, commodity price stabilization, an influx of Asian buyers and a host of other forces.

Respondents are split over the future of oil prices. While the majority (58%) do not expect them to change dramatically, 40% predict further increases, which are likely to drive increased M&A activity. Conversely, natural gas companies, particularly smaller firms struggling with debt and liquidity issues, may face pressure to sell if gas prices continue to lag in the months ahead. Indeed, respondents throughout this survey consistently stress the importance of low gas prices in driving M&A.

China’s need for natural resources is keeping its firms acquisitive, which is illustrated by the results in which 56% of respondents

expect most cross-border deals involving Canadian oil and gas to come from the Asia-Pacific region; the US follows with 34%. In regards to outbound activity, Canadian acquirers are expected to focus primarily in the US and Latin America by 41% and 38% of respondents, respectively.

When asked to consider the factors that will shape the oil and gas industry in the next decade, respondents stress the importance of North American energy independence initiatives, which translates into the development of the region’s shale gas industry, sustainable energy resources, and new technologies including hydraulic fracturing. The emergence of unconventional production methods reducing North America’s reliance on overseas sourcing is reflected across the industry. “Shale gas has completely changed the market,” one respondent comments.

Additionally, respondents are optimistic that the sector will be insulated from external factors. Sustainability and climate change initiatives, for example, are not expected to affect the Canadian oil and gas M&A market in the near-term, nor are regulatory developments linked to the Gulf of Mexico oil spill in the US.The following pages offer insight into the issues and expectations for the upcoming year in the Canadian oil and gas industry. We hope you find this study both informative and useful and as always, we welcome your feedback.

Executive Summary

MethodologyIn the fourth quarter of 2010, Blake, Cassels & Graydon LLP commissioned mergermarket to interview over 100 corporate executives and investment bankers with recent Canadian oil and gas M&A experience to gain insight into the trends and drivers for the market segment over the next 12 months. All respondents are anonymous and results are presented in aggregate.

Canadian Oil & Gas Outlook

4 www.mergermarket.com

What do you expect to happen to the total volume of oil & gas M&A transactions in Canada over the next 12 months?

What do you expect to happen to the total value of oil & gas M&A transactions in Canada over the next 12 months?

The energy sector continues to drive the Canadian M&A market, representing one-quarter of total deal volume and 37% of aggregate M&A deal value in 2010, according to mergermarket data. This is not expected to change in the foreseeable future. The overwhelming majority of respondents (79%) expect to see an increase in the volume of oil & gas M&A in Canada over the next 12 months. Many respondents point to economic recovery as a key driver of M&A during this period, citing improved financing markets and companies’ renewed appetite for acquisitions. “Business cycles and conditions seem to be improving. Beyond the business climate, consumers are in a better position now, and energy consumption is increasing as a result,” says one oil & gas executive. Respondents also believe oil & gas M&A will be driven largely by cash-rich foreign investors, consolidation in specific industry subsectors and low natural gas prices. These and other factors are examined in more detail throughout this report.

Increased deal volume over the next 12 months will likely be accompanied by higher deal values. The large majority of respondents (70%) expect to see an increase in the value of M&A transactions involving Canadian oil & gas companies over the next 12 months, especially in rapidly developing segments of the market. Many respondents point to shale gas as an area where assets are commanding high valuations, and others say the same of the oil sands industry: “Sellers of oil and gas assets, primarily Alberta oil sands assets, are starting to get good value for the development risk of long term oil projects,” says one executive. Meanwhile, another executive explains of the broader business environment: “The world realizes that Canada is business friendly, has quality public equity markets and access to natural resources. This should create premium pricing for deals.”

Overview

Increase significantly

Increase

Remain the same

Decrease

Decrease

Remain the same

Increase

Increase significantly

8%

71%

17%

4%

Increase significantly

Increase

Remain the same

Decrease

Decrease

Remain the same

Increase

Increase significantly

5%

65%

23%

7%

GlobAl EnErGy M&A DEAls

VAluE in uSD M nO. Of DEAlS

2010 411,165 951

2009 290,734 762

2008 287,897 892

2007 511,737 1,043

The global M&A drivers of stable, increasing oil prices, low interest rates and improving costs of capital, when combined with the Canadian unconventional opportunities for acquiring significant reserves via oil sands, shale gas and tight oil plays, will result in a busy 2011.”Dallas Droppo, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

5www.mergermarket.com

Increase

Decrease

Remain the same

<$15m

$15m - $50m

$50m - $100m

$100m - $250m

$250m - $500m

$500m - $1bn

>$1bn

Do you expect private equity funds’ involvement in the oil and gas sector over the next 12 months to:

In which value range do you expect to see the highest volume of Canadian oil & gas M&A transactions over the next 12 months?

More than half of respondents expect private equity firms to become increasingly active players in the Canadian oil & gas sector over the next 12 months. There is certainly room for growth in buyout and exit volume after a quiet period for financial buyers. In 2010, the Canadian energy sector saw 10 private equity related deals (including buy-and-builds) worth a reported US$1.95bn. Still, respondents are optimistic in their outlook for private equity deals going forward citing large amounts of capital, the improving economy and low valuations. An investment banker captures this sentiment by explaining: “Private equity involvement will continue to increase – there is strong value in the sector and it offers better returns than other asset groups.”

Recent deals may provide insight into the direction private equity firms will take in the upcoming year. In one of the largest private equity related deals of 2010, Northern Blizzard Resources Inc., an acquisition vehicle of US-based private equity firms Natural Gas Partners and Riverstone Holdings, acquired the heavy oil assets of Canada-based Nexen Inc. for US$940m in the second quarter of 2010. In the third quarter, Advent International, the US-based private equity firm, announced it would acquire Canadian oilfield services company BOS Solutions for an undisclosed amount.

Respondents are divided when it comes to average M&A deal sizes over the next 12 months but, overall, respondents tend to favor the mid-market range. A likely result of many senior E&Ps acquiring junior E&Ps [see page 7], 29% of respondents expect most deals in the Canadian oil & gas sector to range between US$50m and US$100m in value, and one-quarter of respondents expect deal values to fall between US$100m and US$250m.

While respondents generally agree that deal values are set to rise, they do acknowledge that this may not be the case for all corners of the oil & gas sector. Further emphasizing that deal values will be dictated by industry-specific conditions, an investment banker describes the unique situation of natural gas companies: “There is going to be a lot more consolidation among companies that are stretched on their credit facilities. This will allow for reasonably cheap acquisitions.”

Remain the same

Decrease

Increase

3%

51%

46%

>$1bn

$500m-$1bn

$250m-$500m

$100m-$250m

$50m-$100m

$15m-$50m

>$15m

24%

1%1% 7%

29%

25%

13%

Canadian Oil & Gas Outlook

6 www.mergermarket.com

Increase significantly

Increase

Remain the same

Decrease

Decrease significantly

What do you expect to happen to Canadian oil & gas company valuations over the next 12 months?

The majority of respondents (61%) expect the valuation climate to become more favorable for Canadian oil & gas companies over the next 12 months. Valuations will be linked directly to commodity prices, and also to the financial health of the companies, says one respondent: “There is a lot of liquidity and transparency in Canadian companies, which is attractive to buyers.” Market sentiment and recent deal flow will also play a role. An executive explains that valuations will improve “due to land grabs in the past 12 to 24 months and new horizontal drilling opportunities.” Still, 14% of respondents expect valuations to decrease, and an investment banker in this group cites low gas prices as an important downward force: “Gas prices are very low. Demand is down, but production is continuously increasing, leading to a decrease in valuations.” Another banker reiterates: “Oil might be volatile but gas is really suffering.”

Decrease significantly

Decrease

Remain the same

Increase

Increase significantly

60%

26%

8%

5% 1%

Increase

Decrease

Remain the same

What do you expect to happen to the price of oil and gas in the next 12 months?

Respondents generally expect oil and natural gas prices, a key determinant of oil & gas asset values, to remain stable in the next six to 12 months. Following on from years of extreme volatility in oil prices, bankers and executives alike are optimistic that price swings will be kept at bay for the foreseeable future.

The forecast is slightly more conservative for natural gas. One-fifth of respondents foresee a decrease in natural gas prices in the next six to 12 month period, compared to an almost negligible minority expecting the same for oil. This reflects some respondents’ serious misgivings about gas prices, as noted in the previous question.

0

20%

40%

60%

80%

100%

Natural gasOil

Per

cent

age

of r

espo

nden

ts

40%28%

20%

52%

2%

58%

Canadian Oil & Gas Outlook

7www.mergermarket.com

Senior E&P

Junior E&P

Trusts

Oilfield services companies

Which of the following will be most acquisitive in Canada over the next 12 months?

Most oil & gas M&A activity in the upcoming 12 months will come from the industry’s major players, according to 52% of respondents who expect the most active buyers in Canada to be senior E&P companies. Junior E&Ps and trusts are identified by 27% and 15% of respondents, respectively, while a very small proportion of respondents expect oilfield services businesses to be the most active acquirers. Respondents’ outlook for senior E&Ps is not necessarily surprising given that these parties tend to have easier access to financing than most other companies, not to mention a more diverse mix of businesses and product offerings.

While corporations are widely expected to be more acquisitive than trusts in the next 12 months, it should be noted that some of the most active corporate acquirers could in fact be recently-converted income trusts. This does indeed appear to be the case for some of Canada’s major trusts, including Penn West Energy Trust and Just Energy Income Fund, both of which have implemented aggressive growth strategies with their conversions from trusts to corporations [see page 16 for further analysis of income trust tax legislation]. Similarly, Enerplus Resource Fund, which in early 2011 completed its corporate conversion, agreed to acquire additional land at its Bakken lands, as well as other shale plays in West Virginia and Maryland in the second half of 2010.

Oilfield services companies

Trusts

Junior E&P

Senior E&P52%

27%

15%

6%

Which of the following will be the most common target in Canada over the next 12 months?

Unsurprisingly, the large majority of respondents (71%) expect junior E&Ps to be the most common target this year. Looking at respondent commentary, there is a sense that junior E&P targets, especially those operating in the natural gas industry, will continue to generate a significant amount of distressed M&A activity in the upcoming 12 months as juniors facing cost pressures consider selling off assets or selling themselves to larger strategic buyers. An investment banker based in Canada predicts that the difficult situation facing gas companies will result in M&A: “Gas exports are lacking. Gas companies will consolidate to increase cash flow for resource plays.”

Trusts

Oilfield services companies

Senior E&P

Junior E&P

71%

14%

8%

7%

Junior E&P

Senior E&P

Oilfield services companies

Trusts

Canadian Oil & Gas Outlook

8 www.mergermarket.com

0%

20%

40%

60%

80%

100%

Legislation related to

environmental or alternative energy issues

Legislation related

to income trust taxation

Recent large-cap

consolidation

Debt or liquidity issues

Valuation climate

Oil prices

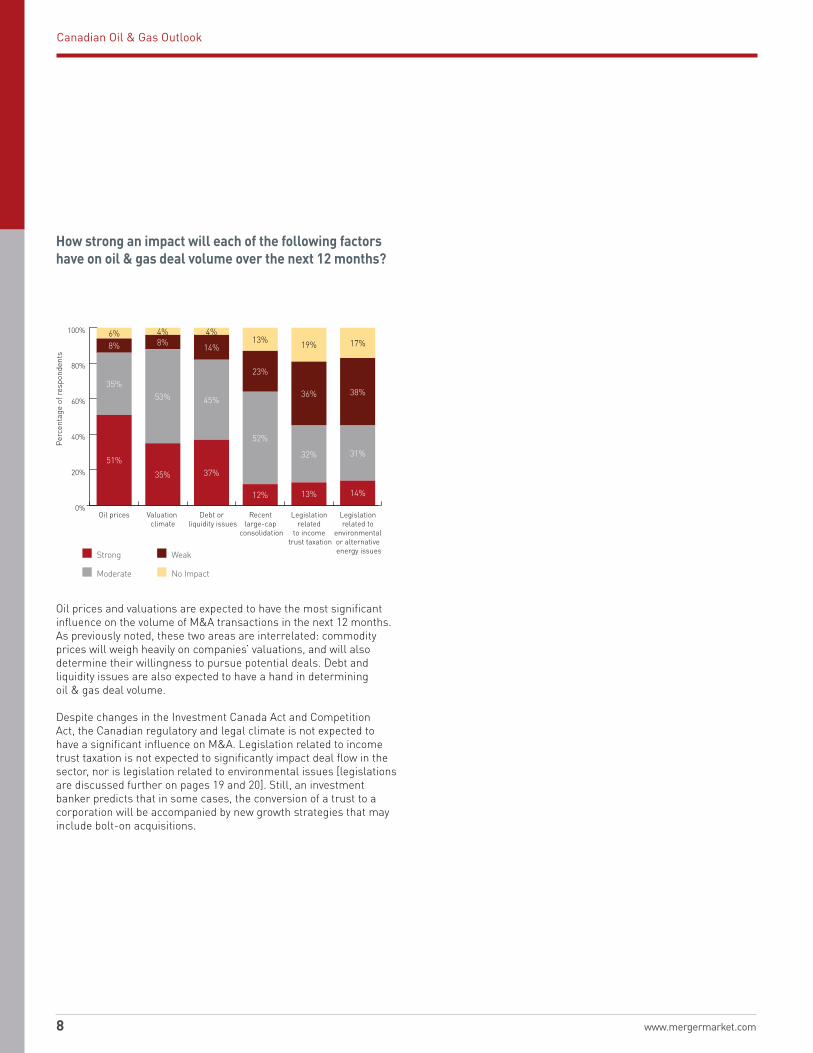

How strong an impact will each of the following factors have on oil & gas deal volume over the next 12 months?

Oil prices and valuations are expected to have the most significant influence on the volume of M&A transactions in the next 12 months. As previously noted, these two areas are interrelated: commodity prices will weigh heavily on companies’ valuations, and will also determine their willingness to pursue potential deals. Debt and liquidity issues are also expected to have a hand in determining oil & gas deal volume.

Despite changes in the Investment Canada Act and Competition Act, the Canadian regulatory and legal climate is not expected to have a significant influence on M&A. Legislation related to income trust taxation is not expected to significantly impact deal flow in the sector, nor is legislation related to environmental issues [legislations are discussed further on pages 19 and 20]. Still, an investment banker predicts that in some cases, the conversion of a trust to a corporation will be accompanied by new growth strategies that may include bolt-on acquisitions.

Strong

Moderate

Weak

No Impact

Per

cent

age

of r

espo

nden

ts

51%

35% 37%

12%

52%

23%

13%

13% 14%

31%

38%

17%

32%

36%

19%

45%

14%

4%

53%

8%4%

35%

8%6%

Canadian Oil & Gas Outlook

9www.mergermarket.com

Cross-border outlook

In which of the following countries or regions do you expect Canadian oil & gas companies to be the most acquisitive over the next 12 months?

Looking at regional trends in M&A activity, the US and Latin America emerge as the top two most attractive regions for Canadian acquirers over the next 12 months. This may be attributed to the increasing importance of US shale plays, which continue to attract foreign investors to the US.

In Latin America, energy M&A has indeed proved substantial in recent months, with 54 deals worth a reported US$35.68bn announced in 2010 in South and Central America. The largest foreign oil & gas deal by a Canadian company during this period, a US$1.75bn acquisition of BP Exploration Company in Colombia by the Canada-based Talisman Energy, highlights the importance of Latin America.

Which of the following countries or regions do you expect to be most acquisitive in the Canadian oil & gas sector over the next 12 months?

More than half of respondents expect most inbound M&A in Canada to come from the Asia-Pacific region, followed by over one-third of respondents who expect US-based acquirers to be most active. In the previous edition of this study both the US and Europe surpassed Asia in respondents’ expectations for inbound foreign buyers. A respondent provides some insight into the factors that make Chinese buyers favorable: “China needs almost all natural resources and has the cash available to make investments. Also, they are willing to take minority positions, keeping management teams in place. This helps to close deals.”

In 2010, Canadian firms were frequent targets of buyers from the Asia-Pacific region. China was involved in three deals totaling a reported US$5.87bn, including the US$4.65bn sale of a 9.03% interest in Syncrude Canada to China-based Sinopec International Petroleum Exploration and Production Corporation (Sinopec). In the fourth quarter of 2010, other countries from the region got involved: Thailand-based PTT Exploration and Production agreed to pay US$2.28bn for Canada-based oil sands project Statoil and Harvest Operations Corporation, a wholly owned subsidiary of Korea National Corporation, acquired Hunt Oil Company of Canada and Hunt Oil Alberta for US$545m.

US

Latin America

Asia-Pacific

Middle East

North Africa

Europe

Europe

North Africa

Middle East

Asia-Pacific

Latin America

US

4%

6%

8%

3%

41%

38%

Europe

Latin America

US

Asia-Pacific

6%3%

57%34%

Asia-Pacific

US

Latin America

Europe

2010 lAtIn AMErICAn EnErGy

DEAls by Country

VOluME Of DEAlS

Brazil 24

Colombia 8

Mexico 6

Argentina 5

Chile 3

Guatemala 3

Peru 2

There has been a lot of press about foreign energy companies coming into Canada but there’s also a good story about Canadian companies participating in plays all over the world.”Mungo Hardwicke-brown, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

10 www.mergermarket.com

In the Asia-Pacific region, which of the following countries do you expect to generate the most significant M&A or joint venture (JV) activity with Canadian oil & gas companies over the next 12 months?

AsIA-PACIfIC MIDDlE EAst

Looking specifically at the Asia-Pacific region, China is overwhelmingly favored by respondents as the country that will be most actively involved in Canadian M&A and joint venture (JV) activity in the oil & gas sector over the next 12 months. China does indeed feature heavily in some of Canada’s most high-profile oil & gas transactions. The previously mentioned acquisition by ConocoPhillips of a 9.03% stake in Syncrude Canada’s joint venture with China-based Sinopec was the largest deal of 2010 in the Canadian energy sector. Another Chinese buyer, China Investment Corporation, a government sponsored sovereign wealth fund, acquired a 45% stake in the Alberta oil sands properties of Penn West Energy Trust for US$799m.

In the Middle East region, which of the following countries do you expect to generate the most significant M&A or joint venture (JV) activity with Canadian oil & gas companies over the next 12 months?

Focusing on the Middle East, nearly half of respondents identify the United Arab Emirates (UAE) as the most active country for cross-border M&A and JV transactions in the upcoming months, while slightly less than one-fifth of respondents identify Saudi Arabia. Shedding light on the drivers of cross-border activity in these markets, many respondents describe the UAE as especially open to doing deals with Canadian firms. One respondent describes UAE-based businesses as “long-term thinkers” in their approach to new projects while another respondent says the region’s business climate welcomes Canadian investors. The appeal of Saudi Arabia for cross-border deals, meanwhile, rests largely in its vast oil reserves and its firm understanding of the market’s dynamics. Kuwait and Qatar are also identified by 14% and 12% of respondents, respectively, and one respondent comments that “relations between Qatar and Canada have already been established.”

As is the case with Asia, many cross-border deals involving the Middle East feature government backed entities. Large sovereign wealth funds are cited frequently by respondents when discussing Middle Eastern involvement in cross-border Canadian oil & gas deals, and it is worth noting that not all of these deals are major, multi-billion dollar events. One example is the sale of certain assets owned by Canada-based Suncor Energy to TAQA North, a subsidiary of Abu Dhabi National Energy Company PJSC (TAQA), for US$280m.

China

Australia

India

Korea

Singapore

United Arab Emirates (UAE)

Saudi Arabia

Kuwait

Qatar

Kurdistan region

Bahrain

Singapore

Korea

India

Australia

China

6%

7%

3% 1%

83%

Bahrain

Kurdistan Region

Qatar

Kuwait

Saudi Arabia

United Arab Emirates (UAE)

5% 1%

49%

12%

14%

19%

Given China’s interest in Canadian resources, Canadian governments and companies should consider the best method for developing a bilateral, mutually beneficial and strategic relationship with China. We must be cognizant that Chinese companies view resources on a global scale and if Canada cannot respond to its needs other countries will.”Michael laffin, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

11www.mergermarket.com

How do you expect most cross-boarder JVs involving Canadian oil & gas companies to be structured over the next 12 months?

There is no clear consensus on the structure of cross-border JVs over the next 12 months, although more than half of respondents believe Canadian companies will be the dominant party in most of these deals. As previously noted, some of Canada’s largest deals have in fact been minority stake purchases, including the Sinopec and Syncrude Canada deal. Other cross-border deals have been split evenly, for example, the 50/50 JV agreement involving Penn West and Japan-based Mitsubishi, which acquired a diverse mix of Penn West assets including gas, land, facilities and infrastructure, in the third quarter of 2010.

What is the most significant challenge Canadian oil & gas companies face when contemplating a foreign transaction?

The majority of respondents (59%) cite political risk as the most challenging aspect of cross-border transactions, followed by close to one-quarter of respondents (23%) who say economic risks are most pressing. Respondents provide further insight into these and other issues, including fluctuating exchange rates and legal risks, with some respondents drawing from their experience in specific countries. An investment banker with experience in Eastern Europe reports complicated “jurisdictional and political regulations in foreign countries like Russia”, while another banker says of his experience in Latin America: “It boils down to how governments handle fiscal frameworks.”

Canadian companies will own more than 50%

Canadian companies will own less than 50%

Canadian companies will own less than 50%

Canadian companies will own more than 50%

56%

44%

Legal risk

Fluctuating exchange rates

Economic risk

Political risk

9%

9%

59%23%

Political risk

Economic risk

Fluctuating exchange rates

Legal risk

The impact of foreign energy companies entering Canada is affecting and will continue to affect our way of doing business. Given the increasing propensity of Canadian companies to transact with foreign companies and to seek transactions in foreign jurisdictions, it will be interesting to see if Canadian energy companies can exert a greater global impact over the next decade.”Michael laffin, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

12 www.mergermarket.com

Targeted industry forecast

Which of the following industry subsectors in Canada will see the most domestic M&A activity over the next 12 months?

Natural gas and oil are identified as the top two subsectors for domestic M&A in the next 12 months, according to 36% and 32% of respondents, respectively, followed by oil sands. Most remaining respondents expect domestic deal volume to be highest in the oilfield services industry. In keeping with respondents’ feedback throughout this report, distressed gas prices will be an important driver of consolidation among smaller natural gas companies. Low prices could suit the needs of buyers and sellers alike and facilitate M&A, according to one respondent: “Natural gas is so low, so anybody with a long-term outlook will be picking up assets, and people with a short-term outlook will want to exit.” Respondents also point to the increasing demand for oil as a reason for consolidation in that subsector: “It’s the commodity of choice right now.”

Which of the following industry subsectors in Canada will see the most cross-border M&A activity over the next 12 months?

Similar to domestic M&A, cross-border M&A activity over the next 12 months will not necessarily be concentrated in any one industry subsector, but will instead span natural gas, oil and oil sands. These three subsectors emerge as the top three most active markets for domestic and cross-border M&A alike. Interestingly, while domestic natural gas M&A is expected to be on par with oil M&A, cross-border deal flow in the natural gas space will be much quieter.

Respondents’ outlook for cross-border activity in oilfield services also mirrors their domestic M&A forecast as a considerable 10% of respondents expect Canada’s oilfield services industry to see the most significant cross-border deal flow, due to what one respondent from this group calls “the greatest availability of targets” compared to all other subsectors. Cross-border activity in oilfield services is also likely to stem from foreign buyers’ appetite for the unique technology and know-how of Canadian firms. In an example from late 2010, Canada-based Flint Energy acquired the heavying hauling business of US-based Stallion Oilfield Services for US$36m. This acquisition is part of a strategy to strengthening its position in the shale gas fields market.

Natural gas

Oil

Oil sands

Oilfield services

Offshore

Alternative energy

Downstream

Oil

Oil sands

Natural gas

Oilfield services

Offshore

Alternative energy

Downstream

Downstream

Alternative energy

Offshore

Oilfield services

Oil sands

Oil

Natural gas

9%

5% 1% 1%

16%

32%

36%

Downstream

Alternative energy

Offshore

Oilfield services

Natural gas

Oil sands

Oil

10%

4% 1%1%

21%

29%

34%

There’s a tremendous amount of oil and gas operational expertise in Canada that is being exported all over the world.”Mungo Hardwicke-brown, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

13www.mergermarket.com

In which subsector will the valuation climate be most favorable for sellers over the next 12 months?

The subsectors that will see the most favorable valuations are the same subsectors that will see the most significant M&A. Sixty-one percent of respondents expect oil companies to see the most favorable valuations in the next 12 months, followed by oil sands and oilfield services companies. Judging from respondents’ comments throughout this report, it comes as little surprise that natural gas, offshore and alternative energy companies are expected to face a less favorable valuation climate. Indeed, respondents have consistently pointed out that low natural gas prices will put downward pressure on valuations. Offshore and non-conventional operations are both considered more costly to operate by many respondents, and these play types also face a great deal of uncertainty from a regulatory standpoint. One respondent explains: “The cost of harnessing renewable energy is very high, as compared to the fossil fuels.”

Which type of buyer will be more active in the oilfield services subsector over the next 12 months?

In the oilfield services space, strategic buyers are expected to be more acquisitive than financial buyers including private equity and venture capital firms. Should regulatory uncertainty and low gas prices continue to be an issue, strategic buyers are widely expected to be more active in taking advantage of low valuations than financial buyers who may be more concerned with the exit environment down the road.

Financial buyers do indeed appear to be in a protracted flat period, even though deal volume is rising on a global scale. Globally, private equity deals in the energy sector totaled 69 worth US$6.60bn in 2009 and in 2010 amounted to 111 deals worth US$12.20bn. Canadian private equity buyouts in the energy industry have been uncommon, however, amounting to only four private equity deals worth US$91m in 2010.

Oil

Oil sands

Oilfield services

Natural gas

Offshore

Alternative energy

Alternative energy

Offshore

Natural gas

Oilfield services

Oil sands

Oil

11%

9%

1%4%

14%61%

Strategic

Financial

78%

22% Financial

Strategic

Canadian Oil & Gas Outlook

14 www.mergermarket.com

What will be most important to buyers when evaluating oilfield services companies over the next 12 months?

Buyers’ appetite for oilfield services targets will be determined largely by the target’s technology and by prevailing market conditions, according to 38% of respondents each. Interestingly, margins and valuations are expected to be less relevant. On this issue, one executive draws attention to the growing importance of horizontal drilling and hydraulic fracturing technologies: “There is a huge demand for fracturing and advanced completion techniques. That is what’s driving a lot of companies’ success and their appeal to buyers.” Commenting on other important areas of the Canadian oil & gas landscape, respondents consistently point to shale and oil sands as areas that will require technological innovation to make extraction processes less labor intensive and more cost effective.

When do you expect most private equity exits to occur in the oilfield services subsector?

Respondents expect private equity firms to hold their oilfield services investments for at least the next year. Many buyout firms may still be waiting for more favorable market conditions, as a fair share of oilfield services buyouts were announced long before the financial crisis and extreme commodity price volatility took hold of the market. Notable deals announced include the US$262m buyout of Osum Oil Sands Corporation by a consortium involving US-based private equity firms Warburg Pincus and Blackstone Capital, and the US$2.5bn management buyout of CCS Income Trust backed by US-based private equity firm Kelso & Company, Vestar Capital Partners, GS Capital Partners and Canada-based private equity firm CAI Capital Partners III.

Technology

Market conditions

Margins

Valuation climate

Other

H1 2011

H2 2011

2012 or later

Georgraphy

Valuation climate

Margins

Market conditions

Technology

38%

8%

8%

8%

38%

2012 or later

H2 2011

H1 2011

H2 2010

41%

49%

10%

nOCs seeking to enhance their knowledge base and experience in cutting edge technologies relating to long reach horizontal drilling, pressure pumping and bitumen upgrading will continue to invest heavily in the Canadian oil & gas sector. nOCs will take the Canadian technology and use it at home or use it in countries where they have other investments.”Dallas Droppo, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

15www.mergermarket.com

Strategies

What will be the primary focus of senior E&P companies in Canada over the next 12 months?

Senior E&Ps, which are expected to be the most aggressive buyers in the Canadian oil & gas industry this year [see page 7], are expected to turn most of their attention to growth initiatives during this period. Forty-two percent of respondents say seniors will focus on making acquisitions over the next 12 months, while 36% of respondents expect seniors to focus on organic growth. Examples of acquisitive behavior in 2010 include Husky Energy’s acquisition of western Canada oil and gas properties from ExxonMobil Corporation, for US$852m as well as the natural gas assets in west central Alberta, Canada from Talisman Energy Inc. for US$427m. Similarly, PetroBakken Energy made three acquisitions in 2010 for a total deal value of US$983m.

What will be the primary focus of junior E&P companies in Canada over the next 12 months?

Respondents are somewhat divided in their outlook for junior E&P companies over the next 12 months. While most respondents believe juniors will be focused on growth, either organic growth (30%) or growth through acquisitions (19%), other respondents appear less optimistic. Approximately one-fifth of respondents say juniors will focus on restructuring or improving their balance sheets, and a comparable 18% of respondents say juniors will consider selling themselves or merging with another company.

This division is reflected in individual respondents’ feedback. One executive describes juniors as increasingly “entrepreneurial” and another states: “Smaller companies are typically the first movers. If sentiment is that the market turns up, they will move quickly to take advantage.” Similarly, an executive says: “A lot of juniors are looking forward to building a big base and growing into intermediates or seniors.” But there are also several respondents who believe most juniors are in distress. One respondent in this group says: “Junior E&P companies are facing pressure to sell, due to accumulated non-performing assets or high debt. It’s a question of survival, where companies are left with no other choice but to sell themselves.”

Growth through acquisitions

Organic growth

Growth through farm-in agreements

Asset sales

Restructuring or improving balance sheet

Sale or merger of company

Sale or merger of company

Restructuring or improving balance sheet

Asset sales

Growth through farm-in agreements

Organic growth

Growth through acquisitions

36%

42%8%

7%

5% 2%Asset sales

Growth through farm-in agreements

Sale or merger of company

Growth through acquisitions or partnerships

Restructuring or improving balance sheet

Organic growth

21%19%

30%

18%

7%

5%

Organic growth

Restructuring or improving balance sheet

Growth through acquisitions or partnerships

Sale or merger of company

Growth through farm-in agreements

Asset sale

Canadian Oil & Gas Outlook

16 www.mergermarket.com

How do you expect most oil & gas companies to obtain financing for new and existing projects over the next 12 months?

Debt financing will likely be the most widely used financing source for oil & gas projects over the next 12 months, according to 44% of respondents. Several investment bankers draw attention to the improved financing environment, which has allowed for large banks to come forward to finance new deals. Balance sheet financing and partnerships will also be key financing sources, according to 29% and 23% of respondents, respectively. Partnerships, and more specifically JVs, have been a prime focus for some of Canada’s largest oil companies. For example, Suncor Energy and Total E&P Canada announced a strategic partnership in late 2010 that aims to further develop oil sands in Alberta. EnCana and the China National Petroleum Corporation (CNPC) also announced a joint venture that will focus on the former’s shale gas plays - this partnership is currently being finalized. And this trend is set to continue with Husky Energy, the Canadian-based oil producer with a market cap of roughly US$22bn saying in 2010 that it would pursue JV opportunities to put its capital to work on attractive projects inside and outside of the country.

While deals will be largely dependent on debt, it is important to note that the availability of debt will vary somewhat according to borrowers’ size and market position. Major underwriters have been involved in some of the largest deals of 2010, including the US$1bn acquisition by Cresent Point of Shelter Bay Energy, backed by a syndicate of underwriters that included BMO Capital Markets, CIBC, Scotia Capital and TD Securities, among others.

Which of the following options will be the most attractive to income trusts ahead of 2011 tax legislation?

Approximately three-quarters of respondents (76%) expect income trusts to respond to tax legislation coming into effect in 2011 by converting to corporations before the 2012 deadline. Remaining respondents are somewhat evenly split between trusts becoming takeover targets, or remaining income trusts and maximizing their tax positions. Most trusts have followed the trend of converting to corporations, as many respondents point out that trusts can satisfy investors by converting to a company that yields high dividends. Trusts that are not in the financial positions to pay attractive dividends, however, are more likely to become takeover targets.

Convert to corporation

Become takeover target

Keep income trust structure and maximize tax position

Keep income trust structure and maximize tax position

Become takeover target

Convert to corporation

10%

14%

76%

0%

10%

20%

30%

40%

50%

IPOsEquity financingAsset salesPartnershipBalance sheetDebt financing

Per

cent

age

of r

espo

nden

ts

44%

29%23%

14% 12% 12%

Canadian Oil & Gas Outlook

17www.mergermarket.com

Which of the following factors will have the greatest influence on their decision?

Market conditions and the valuation climate are identified by 43% and 27% of respondents, respectively, as the top two factors influencing trusts’ strategies. Responses to the previous question confirm that most trusts will convert into corporations. One respondent notes that converting to a corporation is ideal for larger, established trusts: “Many income trusts have established themselves and taken on new operations, and will be looking to strengthen their operations further after converting to a corporation.” Gaining broader access to debt and equity capital markets, more certainty regarding governance issues and more flexibility cash flow management will also make early conversion ideal.

Market conditions

Valuation climate

Investor demand

Ability to absorb tax increase

Ability to absorb tax increase

Investor demand

Valuation climate

Market conditions

14%

16%

27%

43%

Canadian Oil & Gas Outlook

18 www.mergermarket.com

Market movers

Do you expect recent interest in renewable energy to impact oil & gas companies going forward?

Climate change issues have brought the oil industry’s environmental impact under close scrutiny, and have led to a greater interest in developing alternative energy sources. Yet most respondents believe Canada’s oil & gas industry will remain unaffected by developments in the renewable energy space. Fifty-two percent of respondents believe heightened interest in renewable energy will have no impact on Canadian oil & gas businesses, while most remaining respondents believe the impact of renewables on the sector will be weak at best.

Respondents’ feedback on this issue is illuminated by their commentary, which tends to focus on practicality and cost issues. One respondent explains: “Most renewables will not be economical without serious government incentives. We have a three hundred year supply of non-renewable natural gas available at a relatively low cost, and relatively low carbon intensity.” Another respondent seconds this viewpoint by stating: “Natural gas is too cheap and too clean to not be seen as a legitimate green source of energy in the here and now.”

Do you expect climate change initiatives, including the American Clean Energy and security Act of 2009 (ACEs) in the us, to negatively affect oil & gas companies operating in Canada?

Looking more closely at specific developments related to renewable energy, approximately three-quarters of respondents say Canada’s oil & gas industry will not be affected by the American Clean Energy and Security Act of 2009 (ACES) and other climate change initiatives in the US. These respondents express a fair share of skepticism in their individual feedback, as they did in the previous question. One respondent explains: “Regulators are going to make a lot of noise. But they are not going to do anything because they still need oil and gas.” Other respondents believe costs will be a major factor, including one executive who says: “The clean energy initiative is a very costly affair against cheap crude oil. The ACES will be swept under the table. It will not have any impact on our oil & gas industry.”

Yes

No

No

Yes24%

76%

No

Slightly

Moderately

Significantly

Significantly

Moderately

Slightly

No

11%2%

35%

52%

Demand growth, continued oil price recovery and falling extraction and development costs will result in a renewal of project activity in 2011.”Chris Christopher, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

19www.mergermarket.com

Do you expect recent cross-boarder JV activity involving Canada and Asia to trigger increased foreign investment regulations or amendments to the Investment Canada Act over the next 12 to 24 months?

Do you expect to see regulation of offshore operations in Canada in the wake of the us Gulf Coast oil spill in 2010?

Recent cross-border deals between Canada and Asia are not expected to toughen regulation in the near future, 63% of respondents agree. Many comments cite the existing strength of Canada’s review panel who continually work with ongoing conditions. Other supportive arguments state Canada’s need to attract foreign investment, adding “the [tax] income is very welcome.”

While the recent blockage of BHP Billiton’s takeover of Canada’s Potash Corporation of Saskatchewan by the Canadian government may have raised concerns regarding foreign investment regulation, the situation appears to be more of an “isolated incident.”

Yes

No

No

Yes

37%

63%

There seems to be no clear consensus on the impact of the 2010 Gulf Coast oil spill on the Canadian regulatory environment, with 45% of respondents expecting increased offshore regulations and 55% of respondents expecting no material change. Regardless of whether the regulatory environment changes, respondents across the board seem to agree that uncertainty will be a major theme in the offshore market going forward. One respondent explains: “Valuations will fall to cover the cost of increased regulation, especially early on when there is more uncertainty about what specific regulations might be added and how these regulations will be enacted and enforced.” Another respondent says this period of uncertainty will be coupled with “a higher cost of operations and a longer cycle time for operating approvals” as well as depressed valuations for offshore assets.

No

Yes

45%

55%

Yes

No

u.S. government policy and decisions regarding the moratorium on offshore drilling in the Gulf, pipelines to the u.S. from Canada, oil from the Canadian oilsands, and the regulation of shale gas development, will have far reaching impacts on the Canadian oil industry.”Michael laffin, Partner, blake, Cassels & Graydon llP

“

Canadian Oil & Gas Outlook

20 www.mergermarket.com

over the past decade, what global event/issue do you think has had the greatest impact on the north American oil and gas industry?

Looking back on the past decade, respondents are somewhat divided as to the most influential factors in the North American oil & gas industry’s development. Commodity price volatility is cited by the largest proportion of respondents (41%), but 27% and 22% of respondents, respectively, believe the growth of emerging markets and the global financial crisis have been the two most powerful forces shaping the sector. Arguably, these factors do not exist in isolation as financial market disruption has played an important part in driving commodity price swings.

Going into more detail on these factors, respondents comment on erratic commodity prices having changed the framework of the energy industry. Price expectations are a big factor: at one point oil was at US$20 per barrel and it doesn’t look like this will ever be the case again making the new market volatility something to get used to. Another respondent acknowledges a shift in the industry’s most active players, referring to the “increasing power of nationalized oil companies and competition for scarce resources” as important features of the oil & gas industry landscape over the past ten years.

Which of the following do you believe will shape the north American oil and gas industry over the next decade?

Looking ahead to the next decade, 43% of respondents believe North American energy independence initiatives will be critical in shaping the region’s oil & gas industry. Expanding on this topic, respondents repeatedly stress the importance of shale gas and new technologies focused on horizontal multi-fractured drilling. One executive voices the widely held view that “shale gas has completely changed the market.” Feedback from other respondents suggests the shale gas industry will continue to mature going forward with improvements to extraction and distribution processes.

North American energy independence is expected to outweigh public sentiment, political developments and sustainability initiatives in determining the future of the oil & gas industry. But these forces are largely interrelated: many respondents acknowledge that the focus on North American energy independence has and will continue to be dictated by public sentiment and politics, and will likely be accompanied by sustainability initiatives aimed at tempering the region’s dependence on conventional oil. This promises to create a dynamic landscape for oil & gas companies going forward as companies in Canada and the broader North American region adjust to new realities.

North American energy indendence initiatives

Public sentiment

Political developments

Sustainability initiatives

Sustainability initiatives

Political developments

Public sentiment

North American energy independence initiatives

43%

20%

17%

20%

Commodity price volatility

Growth of emerging markets

Global financial crisis

Increased focus on climate change/ sustainability

Policitcal environment post- September 11, 2001

Political environment post-September 11, 2001

Increased focus on climate change/sustainability

Global financial crisis

Growth of emerging markets

Commodity price volatility

41%22%

8%2%

27%

The global economic recovery, coupled with rising energy demand and global competition for access to secure sources of energy, will continue to draw external investors into Canadian unconventional resource plays.”Chris Christopher, Partner, blake, Cassels & Graydon llP

“

MONTRÉAL OTTAWA TORONTO CALGARY VANCOUVER NEW YORK CHICAGO LONDON BAHRAIN AL-KHOBAR* BEIJING SHANGHAI* blakes.com

*Associated Office Blake, Cassels & Graydon LLP

Thank you to our clients for making us the busiest Canadian

M&A law firm, yet again.

Blakes is the #1 Canadian Firm in both Global and Canadian M&A rankings:

Our No. 1 rankings in mergermarket 2010 M&A league tables include:

No. 1 in Canada Announced Deals by deal value No. 1 Canadian firm in United States Announced Deals by deal value and count No. 1 Canadian firm in Americas Announced Deals by deal value and count No. 1 Canadian firm in Global Announced Deals by deal value and count No. 1 Canadian firm in Europe Announced Deals by deal value and count

Our No. 1 rankings on Bloomberg's 2010 M&A league tables include:

No. 1 in Canada Announced Deals by deal count No. 1 Canadian firm in United States Announced Deals by deal value and count No. 1 Canadian firm in Global Announced Deals by deal count No. 1 Canadian firm in Europe Announced Deals by deal count No. 1 Canadian firm in China Announced Deals by deal value

Our No. 1 rankings on Thomson Reuters 2010 M&A league tables include:

No. 1 in Any Canadian Involvement Announced Deals by deal count No. 1 Canadian firm in Any United States Involvement Announced Deals by deal value and count No. 1 Canadian firm in Worldwide Announced Deals by deal value and count No. 1 Canadian firm in Any European Involvement Announced Deals by deal value No. 1 Canadian firm in Any Chinese Involvement Announced Deals by deal value

In the past five years, Blakes has been involved in more than 750 public and private M&A transactions, with an aggregate dollar value in excess of US$900-billion. Among these are some of the largest and most complex Canadian and global energy-sector deals.

Canadian Oil & Gas Outlook

22 www.mergermarket.com

For more than 150 years, Blakes has proudly served many ofthe world’s leading businesses and organizations. The Firmhas built a reputation during that time as both a leader in thebusiness community and in the legal profession – leadership thatcontinues to be recognized to this day. Thanks to our clients andthe challenging legal work they generate, Blakes is recognizedas “Canada’s Law Firm of the Year” for 2010 by Who’s Who Legaland, for the third year running, as “Law Firm of the Year:Canada” in the PLC Which Lawyer? Awards. We also consistentlyrank as the top Canadian firm and one of the world’s top 10 firmson the mergermarket global M&A league tables.

Blakes has lawyers in offices in Canada, the United States,the United Kingdom, China, Bahrain, and Saudi Arabia. Servinga diverse international client base, our integrated office networkprovides clients with access to the Firm’s full spectrum ofcapabilities in virtually every area of business law. Whether anissue is local or multi-jurisdictional, practice-area specific orinterdisciplinary, Blakes handles transactions of all sizes andlevels of complexity. It is our culture and philosophy to workclosely with clients to understand all of their legal needs, and tokeep them apprised of legal developments that may affect them.We provide relevant legal services expertly, promptly and in acost-effective manner to assist clients in achieving theirbusiness objectives.

for further information about this report and investments in the north American region, please contact:

Chris ChristopherPartnerDir: +1 [email protected]

Dallas DroppoPartnerDir: +1 [email protected]

Mungo Hardwicke-brownPartnerDir: +1 [email protected]

Mike laffinPartnerDir: +1 [email protected]

for additional information about blakes, please contact:

Celia bobkinManager, Media & Public relationsTel: +1 [email protected]

brock GibsonChairTel: +1 [email protected]

www.blakes.com

About Blakes

Canadian Oil & Gas Outlook

23www.mergermarket.com

mergermarket

mergermarket is an unparalleled, independent Mergers &Acquisitions (M&A) proprietary intelligence tool. Unlike any otherservice of its kind, mergermarket provides a complete overview of the M&A market by offering both a forward-looking intelligencedatabase and an historical deals database, achieving realrevenues for mergermarket clients.

Contacts

For further inquiries regarding mergermarket or its publishingdivision, Remark, please contact:

Erik WickmanManaging Director, [email protected]: +1 212-686-3329

About mergermarket

DisclaimerThis publication contains general information and is not intended to be comprehensive nor to provide financial, investment, legal, tax or other professional advice or services. This publication is not a substitute for such professional advice or services, and it should not be acted on or relied upon or used as a basis for any investment or other decision or action that may affect you or your business. Before taking any such decision you should consult a suitably qualified professional adviser. Whilst reasonable effort has been made to ensure the accuracy of the information contained in this publication, this cannot be guaranteed and neither Mergermarket nor any of its subsidiaries nor any affiliate thereof or other related entity shall have any liability to any person or entity which relies on the information contained in this publication, including incidental or consequential damages arising from errors or omissions. Any such reliance is solely at the user’s risk.

remark, Part of the Mergermarket Group

www.mergermarket.com11 West 19th Street,2nd fl.New York, NY 10011USA

t: +1 212.686.5606f: +1 [email protected]

80 StrandLondon, WC2R 0RLUnited Kingdom

t: +44 (0)20 7059 6100f: +44 (0)20 7059 [email protected]

Suite 2001Grand Millennium Plaza181 Queen’s Road, CentralHong Kong

t: +852 2158 9700f: +852 2158 [email protected]