165

Canterbury Regional Economic Development Strategy 2009

Canterbury Regional

Economic

Development Strategy

2009

2

Contents

Section 1 Canterbury Regional Profile and Economic Outlook

Section 2 Vision and Objectives

Section 3 Implementation Plan

Section 4 Exemplar Projects

3

Canterbury Regional Profile

and Economic Outlook

4

Acknowledgements

This project was funded by New Zealand Trade and Enterprise through the Canterbury Economic Development Co. The authors Paul Dalziel and Caroline Saunders AERU Research Unit, Lincoln University are particularly grateful to Heather Warwick (Enterprise North Canterbury), Lesley Symington and Barbara Bately (Selwyn District Council), Rob Brawley (Enterprise Ashburton) and Wendy Smith and Andrea Miller (Aoraki Development Trust) for helping us identify key sectors in their respective districts. We are also particularly grateful to John Reid (Te Rūnanga o Ngāi Tahu) for briefing us on approaches to economic development within Ngāi Tahu. We thank Simon Markham and Mary Sparrow (Waimakariri District Council), John McPhail (Kaikoura District Councillor) and Annie Paterson (Kaikoura District Council) for feedback through Heather Warwick on economic development in North Canterbury. We thank Rachel Pugh for comments on economic development in the Selwyn District. We are grateful for helpful comments from participants in two meetings hosted by the Canterbury Development Corporation: Justin Andrist, Toni Browne, Blair Cottam, Chris Hyland, Trish Leddy, Larry Podmore, Simon Worthington (all CDC), Adam Naiman (Christchurch City Council) and Richard Simmonds (Christchurch City Holdings Ltd). We thank staff from the Christchurch offices of New Zealand Trade and Enterprise who provided us with written or verbal background material: Stephen Bryant, David Grant, Mark Hazeldine, Cate Hlavac, David Lough, Maureen Manson and Irvine Paulin. We pay tribute to our former AERU colleague, Meike Guenther, for her outstanding work in collecting data and preparing the Economic Base Reports that provided the foundations for this Canterbury Regional Profile and Economic Outlook.

iii

Contents

Acknowledgements ii

Contents iii

List of Tables iv

List of Figures v

Preface vii

1. Introduction 1

2. Producing from the Land 5

3. The People of Canterbury 15

4. The Canterbury Labour Force 21

5 The Canterbury Economy 29

6. Key Sectors in Canterbury 37

7. Economic Infrastructure in Canterbury 43

8. Economic Outlook 57

References 69

iv

List of Tables

2.1 Agriculture Land Use in Canterbury, 2002 and 2007 8

2.2 Farm Types in Canterbury, 2002 and 2007 9

2.3 Livestock in Canterbury, 2002 and 2007 10

2.4 Selected Crops in Canterbury, 2002 and 2007 11

2.5 Canterbury/Waipara Grape Varieties, 2008 13

3.1 Usually Resident Population in Canterbury, 2001 and 2006 15

3.2 Projected Population in Canterbury, 2006 and 2031 17

3.3 Age Distribution in Canterbury, 2001 and 2006 18

3.4 Highest Attainment of Canterbury School Leavers, 2007 20

4.1 Highest Education Attainments of Working Age Population, 2006 24

4.2 Total Personal Incomes of Working Age Population, 2005/06 25

4.3 Occupations of Employed People, 2006 26

5.1 Estimated GDP for Canterbury, 2007 31

5.2 Shift-Share Analysis of Canterbury Employment, 2001-2006 36

6.1 Annual Guest Nights in Canterbury, 2004-2008 40

7.1 Overview of Canterbury Transport Infrastructure, 2006/07 46

7.2 Canterbury Regional Land Transport Strategy Targets 47

7.3 Household Access to Telecommunications, 2001 and 2006 49

8.1 Forecasts of Trading Partners’ Economic Growth 58

8.2 Composition of the Property and Business Services Sector 61

v

List of Figures

The Canterbury Region x

1.1 Canterbury Regional Strategic Land Transport Network 3

2.1 Land-Use Capability Classes in Canterbury 6

2.2 Vineyard Production Areas of New Zealand, 2008 12

2.3 Canterbury/Waipara Grape Varieties, 2008 13

3.1 Canterbury Projected Median Age, 1996-2031 19

4.1 Canterbury Working Age Population and Labour Force, 1988-2008 21

4.2 Canterbury and New Zealand Participation Rates, 1988-2008 22

4.3 Canterbury and New Zealand Unemployment Rates, 1988-2008 22

5.1 New Zealand Real Per Capita GDP, 1969/70-2007/08 29

5.2 Canterbury and New Zealand Industry Employment Shares, 2006 33

5.3 Canterbury and New Zealand Increase in Employment, 2006 33

5.4 Extra Employees Not Explained by National Trends, 2001-2006 35

6.1 The South Island Clusters Identified By NZTE, 2002 38

6.2 Annual Guest Nights in Canterbury, 2001-2008 41

6.3 Forecasts of Total Visits to Canterbury, 2008-2014 42

7.1 Passenger Movements at Christchurch International Airport, 1999-2008 43

7.2 Cargo Movements at Christchurch International Airport, 1999-2008 44

7.3 Cargo Movements at Port of Lyttelton, 1999-2008 45

7.4 Cargo Movements at PrimePort Timaru, 1999-2008 45

7.5 Urban/Rural Use of Dial-Up and Broadband Technologies, 2006 50

7.6 Canterbury Water Resource Zones 52

7.7 Average Seasonal Variation of Future Water Demand Scenario 53

7.8 Stylised Regional Innovation System 55

vi

List of Figures (Continued)

8.1 Actual and Projected Economic Growth, New Zealand, 2006-2012 57

8.2 Actual and Projected Unemployment, New Zealand, 2006 2012 59

8.3 New Zealand United States Exchange Rate, 1999-2008 60

8.4 New Zealand’s Economic Structure in Four Segments 64

vii

Preface

E te whenua, e takoto nei, tēnā koe.

E Aoraki, e ngā maunga o tēnei motu, tēnā koutou.

E ngā awa, e ngā moana, e ngā mahinga kai, tēnā koutou.

E Te Moana-nui-a-Kiwa, tēnā koe.

E ngā Papatipu Rūnanga o Ngāi Tahu whānui, tēnā koutou.

Kei te mihi māua ki ngā taonga o Waitaha, Ngāti Māmoe me Ngāi Tahu.

E ngā tāngata kua nau mai no ngā hau e whā ki tēnei wāhi, tēnā koutou.

Tēnā koutou, tēnā koutou, kia ora tatou katoa.

The authors of this report are very pleased to begin by greeting the land, the mountains, the rivers, the lakes, the gathering places of food and the ocean of Canterbury. We are very pleased to acknowledge the region’s tāngata whenua and to pay tribute to the treasured heritage of Waitaha, Ngāti Māmoe and Ngāi Tahu. We are very pleased to greet all the peoples who have come to this region from the four corners of the world. Greetings, greetings, may we all live in good health.

In November 2008, the AERU Research Unit at Lincoln University (working in close partnership with the economic development agencies of North Canterbury, Christchurch City, Selwyn, Ashburton and South Canterbury) was commissioned to update the Canterbury Regional Economic Development Strategy (CREDS) that was first prepared in 2000 and then revised in 2005. This report completes the first stage of our work, in which we present a snapshot of the region’s economic profile and outlook.

Any regional economic development strategy must build on the strengths of its existing businesses and industries. In New Zealand, the policy focus is on firms who export, since other firms are constrained by the size of New Zealand’s relatively small domestic market. Consequently, our intention in this report is to assess Canterbury’s strengths and opportunities for export-based economic development, based on the region’s social, economic, environmental and cultural resources. The data analysed in the chapters that follow provide important foundations for the design of an updated economic development strategy, which is the next step in our work.

viii

In presenting this first report, the authors acknowledge the work that was done for CREDS 2000 and CREDS 2005, particularly by the Canterbury Development Corporation (which was responsible for coordinating the writing of those two strategic documents). Our own work seeks to build on those earlier documents and follows their example in many important ways.

CREDS 2000 sought to identify regional issues grouped under five major headings: economy; education and skills; social; environment; and attitude. A number of priorities were chosen for each heading, and then each priority was fleshed out with a series of action areas and measures of success. The result was a very comprehensive spreadsheet of goals, priorities, action areas and measures of success, but the review of the strategy in 2005 came to the view that ‘while a significant number of projects and activities resulted from the 2000 strategy, the document and its action framework suffered from being too high-level in its focus’.

Consequently, CREDS 2005 sought to complement a high-level ‘top-down’ strategic approach with a sub-regional ‘bottom-up’ focus on local issues within the constituent territorial authorities of Canterbury. This was timely since the regional, city and district councils were engaged in preparing Long Term Council Community Plans (LTCCPs) under the recently reformed Local Government Act 2002. CREDS 2005 identified ten major regional issues and opportunities, and supplemented this regional analysis with stand-alone strategic plans at the district or city level for North Canterbury, Christchurch, Banks Peninsula, Selwyn, Ashburton and South Canterbury.

During our consultations for the preparation of this CREDS update, the authors were told that the projects identified in the district-level strategic plans have generally been completed, and that CREDS 2005 had provided a valuable impetus to those projects. There is a general perception that CREDS 2005 was less successful in initiating regional-level initiatives. That perception was validated by examining the CREDS website at the end of 2008, which stated without further detail that ‘the local Government and key stakeholders in CREDS are currently working on the development of several transformational regional and local projects as identified in the strategic plan, all determined by our vision and mission of transforming Canterbury into a world-class regional economy founded on innovation, diversity and sustainability’.

ix

Important regional initiatives have taken place within Canterbury since 2005. Different partnerships of central and local government bodies have begun strategic work programmes related to the region’s economic development; for example, the Greater Christchurch Urban Development Strategy, the Canterbury Regional Land Transport Strategy 2008 - 2018, Stages 2 and 3 of the Canterbury Strategic Water Study and the Canterbury Labour Market Strategy. Further, in February 2009 all of Canterbury’s territorial authorities published renewed Long Term Council Community Plans in draft.

Against this background, the team responsible for updating CREDS is focusing on identifying strategic region-wide initiatives for fostering regional economic development, taking into account the various regional and local strategies already in existence. The update process is following Regional Economic Development Strategy Guidelines published as a web-based resource by the Ministry of Economic Development in October 2008 (see www.med.govt.nz/strategy-development/). These guidelines recommend research at an early stage of the process to gather relevant data that will help identify the region’s positioning in the national economy and its key regional drivers of economic development. This report presents the results of this stage of our work.

The authors are particularly grateful to our former colleague, Meike Guenther, for her outstanding work in collating data on the local and regional economies of Canterbury. This resulted in five Economic Base Reports for North Canterbury, Christchurch City, Selwyn, Ashburton and South Canterbury, as well as a separate report for the Canterbury region as a whole. These reports were discussed in draft with our partner economic development agencies before the final reports were prepared.

The Canterbury Regional Profile and Economic Outlook presented here is based on those final reports. It is written for a general audience with the aim of synthesising relevant data to highlight important features of the Canterbury regional economy. These features will be taken into account in the next step of the project, which involves preparing an updated regional economic development strategy.

Paul Dalziel Caroline Saunders (30 March 2009)

x

The Canterbury Region

Source: Morgan et al. (2002, p. 8).

1

1. Introduction

The Canterbury region covers 4.8 million hectares in the middle of the South Island of New Zealand. To the east, the Canterbury coastline extends along the Pacific Ocean, from Kekerengu Point in the north to the Waitaki River in the south. The Canterbury Plains extend westwards to the Southern Alps, overseen by Aoraki/Mt Cook, the tallest mountain in Australasia (3754 metres).

Eighteen major rivers flow across the plains to the sea: Clarence (Waiau-Toa), Conway (Tūtae Putaputa), Waiau, Hurunui, Waipara, Kowai, Ashley (Rakahuri), Waimakariri, Selwyn (Waikirikiri), Rakaia, Ashburton (Hakatere), Hinds (Hekeato), Rangitata, Orari, Opihi, Pareora, Waihao and Waitaki. Nearly 90 per cent of the Canterbury area is covered by pastoral grasses, tussock, scrub or bare land, with another 8 per cent devoted to forests.

The first settlers in the region were Māori, beginning with the Waitaha tribes, followed by Ngāti Māmoe and then Ngāi Tahu. As successive migrations arrived, they defeated or intermingled with their predecessors, so that today Ngāi Tahu describe themselves as ‘the iwi comprised of Ngāi Tahu whānui; that is, the collective of the individuals who descend from the five primary hapū of Ngāi Tahu, Ngāti Māmoe and Waitaha, namely Kāti Kurī, Ngāti Irakehu, Kāti Huirapa, Ngāi Tūāhuriri and Ngāi Te Ruahikihiki’ (see the Ngāi Tahu website, www.ngaitahu.iwi.nz/About-Ngai-Tahu/).

An Act of Parliament set up Te Rūnanga o Ngāi Tahu (TRONT) in 1996, which is governed by elected representatives from 18 Papatipu Rūnanga throughout the South Island. Ten of these hold manawhenua over land within Canterbury: Te Rūnanga o Kaikōura; Te Ngāi Tuahuriri Rūnanga; Rapaki Rūnanga (Te Hapū o Ngāti Wheke); Te Rūnanga o Koukourarata; Wairewa Rūnanga; Te Rūnanga o Onuku; Taumutu Rūnanga; Te Rūnanga o Arowhenua; Te Rūnanga o Waihao; and Te Rūnanga o Moeraki.

The first wave of organised European migrations began in England with the formation of the Canterbury Association by John Godley and Edward Wakefield in 1848 and the arrival at Lyttelton of the Association’s first four ships in December 1850: the Charlotte Jane, the Randolph, the Sir George Seymour and the Cressy. Further vessels brought the number of European settlers in Canterbury to 3,000 by the end of 1851. In 1852, New Zealand was divided into six self-governing provinces, including Canterbury. These provincial governments were replaced by a national government on 1 November 1876, with local government devolved to 64 counties.

2

The system of local government in New Zealand has continued to change over the decades. Canterbury now has a Regional Council, known as Environment Canterbury, which covers territories governed by the Kaikoura District Council, the Hurunui District Council, the Waimakariri District Council, the Christchurch City Council, the Selwyn District Council, the Ashburton District Council, the Timaru District Council, the Waimate District Council and the Mackenzie District Council. The Environment Canterbury region also includes the western half of the Waitaki District Council.

The Canterbury region continues to attract migrants from around the world. In the 2006 census, 17.9 per cent of the normally resident Canterbury population who reported their place of birth were born outside New Zealand. The largest group were born in the United Kingdom and Ireland (6.7 per cent), followed by residents who had been born in Asia (4.7 per cent).

Figure 1.1 comes from Environment Canterbury’s (2008) Regional Land Transport Strategy. It shows the region’s strategic land transport network, and is a good representation of the integrated province. There are five main points of entry by land. From the north, State Highway One brings traffic from the top of the South Island through Marlborough into Canterbury and towards Kaikoura. To the west, three mountain passes provide access from the north-west (Lewis Pass), the west (Arthur’s Pass) and the south-west (Lindis Pass). From the south, State Highway One brings traffic from Oamaru in North Otago towards Timaru in South Canterbury.

The city of Christchurch lies at the centre of the network. Christchurch International Airport is the point of arrival into the province for many visitors from overseas and the rest of New Zealand; it recorded three million passenger arrivals in 2008. In the 2006 census, two-thirds of Canterbury’s normally resident population (521,832 people) lived in Christchurch City (348,435 people).

Canterbury offers a great diversity of cultural, recreational and sporting opportunities to visitors and residents alike. The city of Christchurch, the larger towns and the smaller villages of Canterbury are conscious of their heritage, which is interpreted in museums, galleries, festivals and events throughout the province. To give an example that reflects the region’s agricultural roots, in any given calendar year there are nineteen Agricultural and Pastoral (A&P) shows in Canterbury, organised in Amberley, Amuri (Rotherham), Ashburton, Banks Peninsula, Cheviot, Christchurch (the Royal New Zealand Show), Courtenay, Duvachelle, Ellesmere, Hawarden, Kaikoura, MacKenzie, Malvern, Mayfield, Methven, Oxford, Rangiora, Temuka and Geraldine, and Waimate.

3

Figure 1.1 Canterbury Regional Strategic Land Trans port Network

Source: Environment Canterbury (2008, p. 98).

4

The following chapters of this report provide data and analysis to describe important features of the Canterbury regional economy. Chapter 2 begins with production from the land. Chapter 3 presents data on the Canterbury population, mainly drawn New Zealand’s five yearly census and population projections, and Chapter 4 describes trends in the Canterbury labour force. Chapter 5 discusses the Canterbury economy, using standard industry classifications. For many purposes, the standard classifications are too broad, and so Chapter 6 discusses important industry clusters in the region, including tourism. Chapter 7 presents data on infrastructure in Canterbury, focusing on airports and seaports, land transport, telecommunications, water and innovation systems. Chapter 8 concludes the report with a discussion of the short-term outlook for the Canterbury economy in the context of recent national and international trends.

5

2. Producing from the Land

There is considerable diversity in land types within the Canterbury region (see Winterbourn, 2008, which is the source of the material in this paragraph). In the most straightforward classification, Jon Harding and Michael Winterbourn (1997) identify four ecoregions: the Southern Alps, the High Country, the East Coast Plains and Banks Peninsula. The Southern Alps ecoregion involves steep mountain terrain with no forest vegetation. The High Country ecoregion is characterised by less steep terrain on the eastern foothills of the Southern Alps. Parts of this ecoregion can support beech forest, exotic plantation forests, indigenous and introduced scrub and pasture grasses. The East Coast Plains extend from the Southern Alps foothills to the east coast of the South Island. This ecoregion is highly modified to support pastoral and other types of farming, as well as hosting the main urban settlements in Canterbury. Banks Peninsula is comprised of two deeply eroded volcanic craters, which has resulted in a distinctive ecoregion despite the similar climate to that on the East Coast Plains.

The Canterbury Regional Council has defined eight soil environment groups (Environment Canterbury, 2004). These are: (a) High country: moist mountain ranges; (b) High country: dry mountain ranges; (c) Inland basins and major river valleys; (d) Soft rock hill country and downs; (e) Hard rock hill country; (f) Kaikoura coastal zone; (g) Banks Peninsula; and (h) The Canterbury Plains. Maps of these groups can be found on pages 8-6 and 8-7 of the Council’s Proposed Natural Resources Regional Plan.

Kevin O’Connor and George Knox (2008) offer a different classification based on ten major land systems. This classification again recognises Banks Peninsular as a distinctive system, but divides the East Coast Plains into three land systems: the Hurunui Basin, the Canterbury Plains and the Timaru Downs. The Southern Alps and High Country are divided into six land systems: Hope-Kaikoura, Arrowsmith-Arthur’s, Heron-Porter, Aoraki, Mackenzie-Waitaki and Kohurau-Hunter. A map showing the ten major land systems can be found on page 865 of their book chapter.

A third classification is provided by Peter Newsome’s (1987) eight classes of land-use capabilities. Classes 1-4 are suitable for cultivation. Class 1 describes land that is good for multiple uses and has very little erosion risk; class 4 has severe limitations on what can be grown, requiring very careful land management. Classes 5-8 cover non-arable land. Classes 5 and 6 are good for forestry and pasture, Class 7 is very difficult for pasture but moderately suited for forestry, and Class 8 is not suitable for production.

6

Figure 2.1 presents a pie chart of the distribution of land-use capability classes in Canterbury, taken from a table prepared by Trevor Webb (2008) using Newsome’s categories. Given the presence of the Southern Alps in the west of the region, it is not surprising that nearly one-quarter (23 per cent) of the land in Canterbury is not suited for production and another 16 per cent is in Class 7.

Figure 2.1 Land-Use Capability Classes in Canterbur y

Classes 1-2

4%

Class 3

29%

Class 4

4%

Classes 5-6

24%

Class 7

16%

Class 8

23%

Source: Webb (2008, p. 116).

Note: The classes are ranked from the most versatile soils in Class 1 to non-productive land in Class 8.

More than a third of the land in Canterbury is arable (Classes 1 to 4), but only four per cent of the total land area is in the most versatile categories of Classes 1 and 2. Webb (2008, pp. 115) comments that half of this four per cent lies within a one hour commuting distance from Christchurch, so that there has been pressure on this resource from rising demand for lifestyle blocks. Environment Canterbury (1998, p. 87) has a policy objective to ‘minimise the irreversible effect of land use activities on land comprising versatile soils where such use would foreclose future land use options that benefit from being located on those soils, where it is practicable to so’.

7

Just over 60 per cent of Canterbury land is in land-use capability Classes 1 to 6, which is good for cultivation (Classes 1 to 3) or good for pasture and forestry (Classes 1 to 6). The quality of these soils has long been the basis of Canterbury’s land-based economy. Nevertheless, from the earliest migrations into the region, settlers have had to be innovative to produce from the land. Sir Tipene O’Regan (1989), for example, has explained how Ngāi Tahu settlers in the seventeenth century modified Māori culture to meet the rigours of the colder environment and a very different economy from their previous experience in the eastern North Island. The Waitangi Tribunal (1991, p. 843) has recorded that survival for the tribes depended on seasonal journeys to hunt and gather food from mahinga kai spread over wide territories.

Similarly, the vision of the Canterbury Association in 1848 was that the new English settlement would be based on an agriculture sector involving large numbers of yeoman farmers on relatively small blocks of land. Once the settlers arrived, they discovered this was impractical. The rules were soon changed to allow large properties for running sheep to produce wool for export to the United Kingdom. The decade after 1857 was a boom time for the pastoralists; at its height in 1867, annual wool exports from Canterbury were 11 million pounds, worth more than £600,000 (Rogers, 2007, p. 55).

Primary sector producers in Canterbury have access to a number of research organisations that offer expertise in raising land productivity while improving environmental outcomes. In particular, the Lincoln Resource is a group of companies and organisations involved in land-based research and its application in business, based in and around the Lincoln township in Selwyn. Partners include AgResearch, Crop and Food Research, the Foundation for Arable Research, Heinz Wattie’s, Lincoln University, Lincoln Ventures, Manaaki Whenua Landcare Research Ltd, PGG Wrightson Ltd and Selwyn District Council. This cluster involves more than 900 staff involved in a range of research, development, consulting, support and management roles. It is an important strategic asset for the ongoing improvement of land productivity in Canterbury.

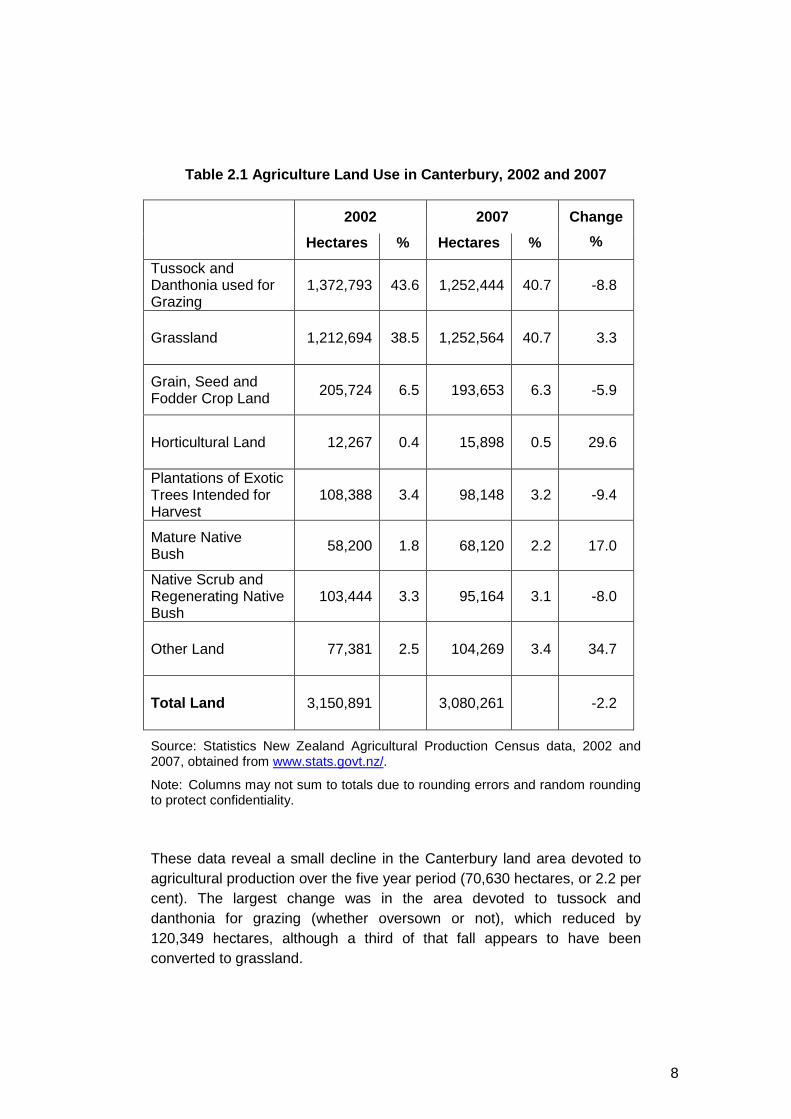

Statistics New Zealand in association with the Ministry of Agriculture and Forestry conducts a census of agricultural production in New Zealand every five years (www.stats.govt.nz/economy/primary-production/). The census provides statistics on animal farming (including sheep, beef and dairy cattle, and deer), crop growing (including grain and seed crops, fruit and vegetables, wine grapes and nursery plants) and forestry. Table 2.1 presents information on agricultural land use in Canterbury as recorded in the 2002 and the 2007 agricultural production censuses.

8

Table 2.1 Agriculture Land Use in Canterbury, 2002 and 2007

2002 2007

Hectares % Hectares %

Change

%

Tussock and Danthonia used for Grazing

1,372,793 43.6 1,252,444 40.7 -8.8

Grassland

1,212,694 38.5 1,252,564 40.7 3.3

Grain, Seed and Fodder Crop Land 205,724 6.5 193,653 6.3 -5.9

Horticultural Land

12,267 0.4 15,898 0.5 29.6

Plantations of Exotic Trees Intended for Harvest

108,388 3.4 98,148 3.2 -9.4

Mature Native Bush 58,200 1.8 68,120 2.2 17.0

Native Scrub and Regenerating Native Bush

103,444 3.3 95,164 3.1 -8.0

Other Land

77,381 2.5 104,269 3.4 34.7

Total Land

3,150,891 3,080,261 -2.2

Source: Statistics New Zealand Agricultural Production Census data, 2002 and 2007, obtained from www.stats.govt.nz/.

Note: Columns may not sum to totals due to rounding errors and random rounding to protect confidentiality.

These data reveal a small decline in the Canterbury land area devoted to agricultural production over the five year period (70,630 hectares, or 2.2 per cent). The largest change was in the area devoted to tussock and danthonia for grazing (whether oversown or not), which reduced by 120,349 hectares, although a third of that fall appears to have been converted to grassland.

9

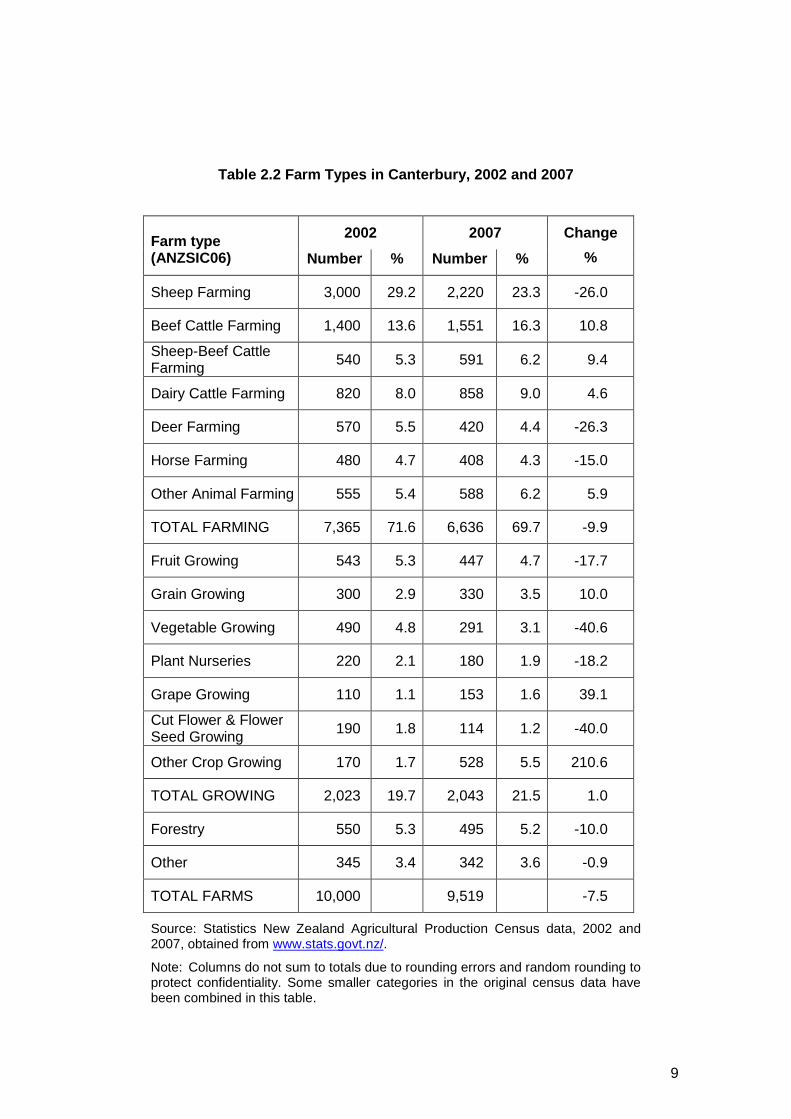

Table 2.2 Farm Types in Canterbury, 2002 and 2007

2002 2007 Farm type (ANZSIC06) Number % Number %

Change

%

Sheep Farming 3,000 29.2 2,220 23.3 -26.0

Beef Cattle Farming 1,400 13.6 1,551 16.3 10.8

Sheep-Beef Cattle Farming 540 5.3 591 6.2 9.4

Dairy Cattle Farming 820 8.0 858 9.0 4.6

Deer Farming 570 5.5 420 4.4 -26.3

Horse Farming 480 4.7 408 4.3 -15.0

Other Animal Farming 555 5.4 588 6.2 5.9

TOTAL FARMING 7,365 71.6 6,636 69.7 -9.9

Fruit Growing 543 5.3 447 4.7 -17.7

Grain Growing 300 2.9 330 3.5 10.0

Vegetable Growing 490 4.8 291 3.1 -40.6

Plant Nurseries 220 2.1 180 1.9 -18.2

Grape Growing 110 1.1 153 1.6 39.1

Cut Flower & Flower Seed Growing 190 1.8 114 1.2 -40.0

Other Crop Growing 170 1.7 528 5.5 210.6

TOTAL GROWING 2,023 19.7 2,043 21.5 1.0

Forestry 550 5.3 495 5.2 -10.0

Other 345 3.4 342 3.6 -0.9

TOTAL FARMS 10,000 9,519 -7.5

Source: Statistics New Zealand Agricultural Production Census data, 2002 and 2007, obtained from www.stats.govt.nz/.

Note: Columns do not sum to totals due to rounding errors and random rounding to protect confidentiality. Some smaller categories in the original census data have been combined in this table.

10

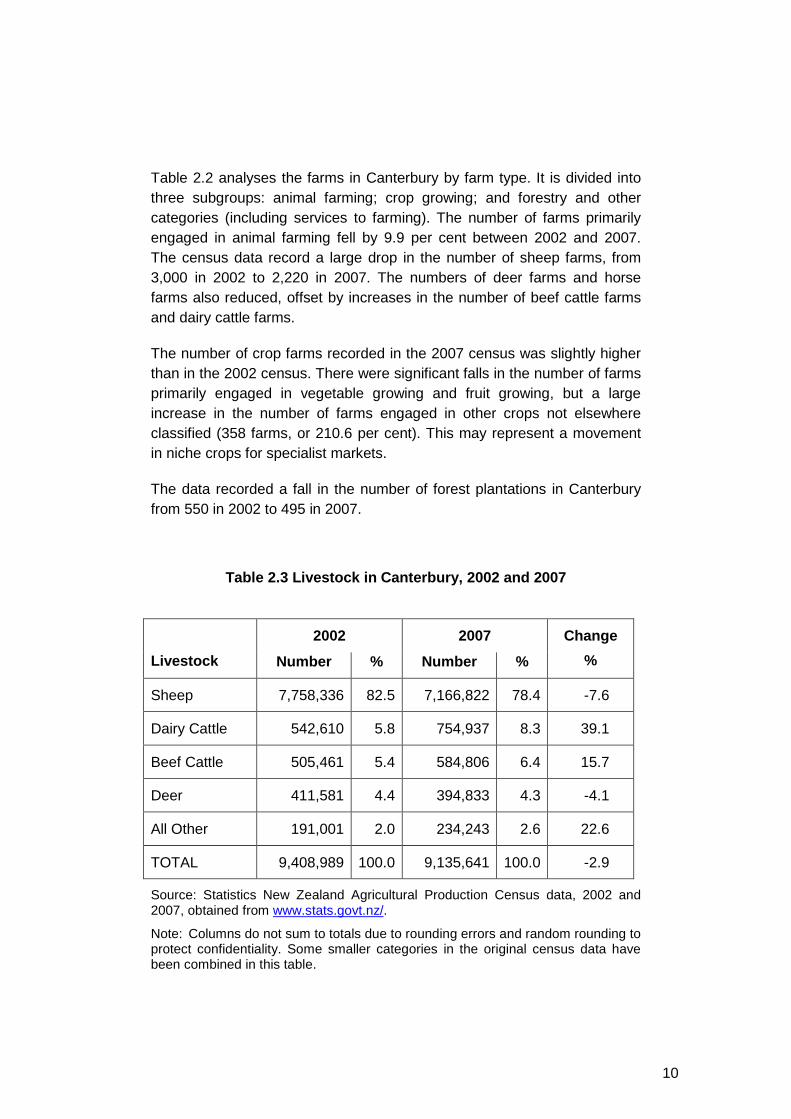

Table 2.2 analyses the farms in Canterbury by farm type. It is divided into three subgroups: animal farming; crop growing; and forestry and other categories (including services to farming). The number of farms primarily engaged in animal farming fell by 9.9 per cent between 2002 and 2007. The census data record a large drop in the number of sheep farms, from 3,000 in 2002 to 2,220 in 2007. The numbers of deer farms and horse farms also reduced, offset by increases in the number of beef cattle farms and dairy cattle farms.

The number of crop farms recorded in the 2007 census was slightly higher than in the 2002 census. There were significant falls in the number of farms primarily engaged in vegetable growing and fruit growing, but a large increase in the number of farms engaged in other crops not elsewhere classified (358 farms, or 210.6 per cent). This may represent a movement in niche crops for specialist markets.

The data recorded a fall in the number of forest plantations in Canterbury from 550 in 2002 to 495 in 2007.

Table 2.3 Livestock in Canterbury, 2002 and 2007

2002 2007

Livestock Number % Number %

Change

%

Sheep 7,758,336 82.5 7,166,822 78.4 -7.6

Dairy Cattle 542,610 5.8 754,937 8.3 39.1

Beef Cattle 505,461 5.4 584,806 6.4 15.7

Deer 411,581 4.4 394,833 4.3 -4.1

All Other 191,001 2.0 234,243 2.6 22.6

TOTAL 9,408,989 100.0 9,135,641 100.0 -2.9

Source: Statistics New Zealand Agricultural Production Census data, 2002 and 2007, obtained from www.stats.govt.nz/.

Note: Columns do not sum to totals due to rounding errors and random rounding to protect confidentiality. Some smaller categories in the original census data have been combined in this table.

11

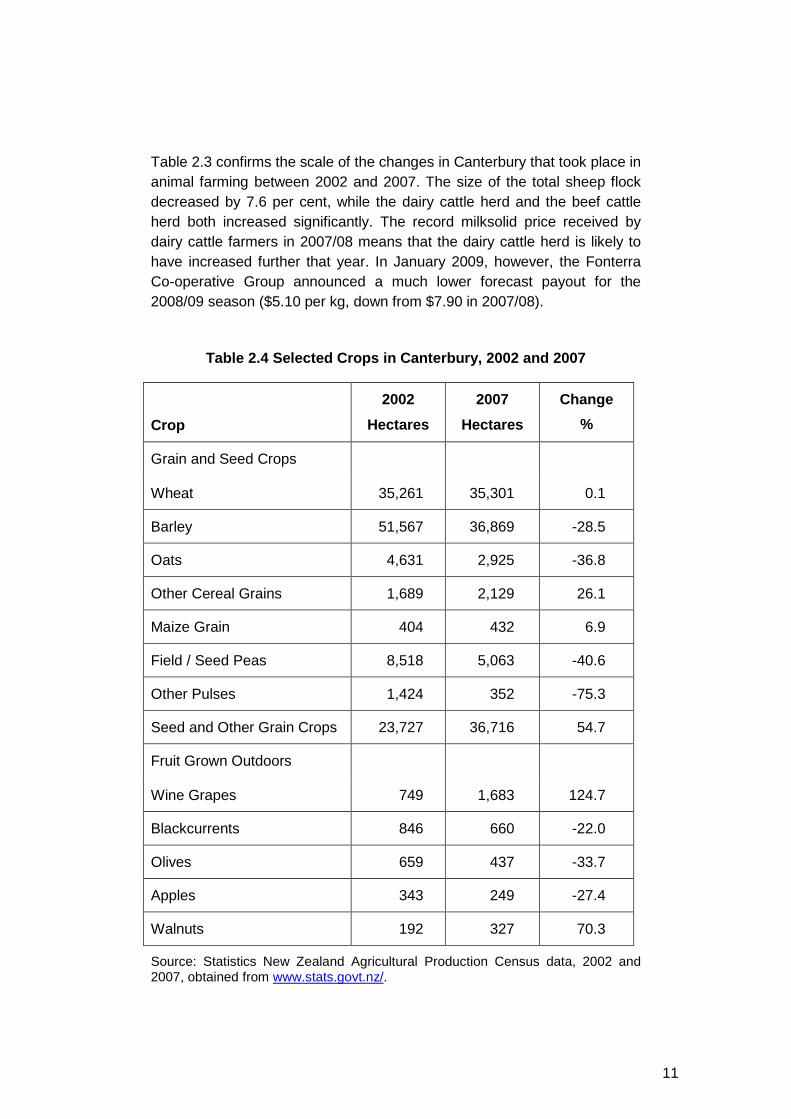

Table 2.3 confirms the scale of the changes in Canterbury that took place in animal farming between 2002 and 2007. The size of the total sheep flock decreased by 7.6 per cent, while the dairy cattle herd and the beef cattle herd both increased significantly. The record milksolid price received by dairy cattle farmers in 2007/08 means that the dairy cattle herd is likely to have increased further that year. In January 2009, however, the Fonterra Co-operative Group announced a much lower forecast payout for the 2008/09 season ($5.10 per kg, down from $7.90 in 2007/08).

Table 2.4 Selected Crops in Canterbury, 2002 and 20 07

Crop

2002

Hectares

2007

Hectares

Change

%

Grain and Seed Crops

Wheat 35,261 35,301 0.1

Barley 51,567 36,869 -28.5

Oats 4,631 2,925 -36.8

Other Cereal Grains 1,689 2,129 26.1

Maize Grain 404 432 6.9

Field / Seed Peas 8,518 5,063 -40.6

Other Pulses 1,424 352 -75.3

Seed and Other Grain Crops 23,727 36,716 54.7

Fruit Grown Outdoors

Wine Grapes 749 1,683 124.7

Blackcurrents 846 660 -22.0

Olives 659 437 -33.7

Apples 343 249 -27.4

Walnuts 192 327 70.3

Source: Statistics New Zealand Agricultural Production Census data, 2002 and 2007, obtained from www.stats.govt.nz/.

12

Table 2.4 presents 2002 and 2007 data for Canterbury hectares planted in selected crops. The top half of the table shows grain and seed crops, while the bottom half shows some outdoor fruit crops. There were significant falls in the area devoted to barley and oats, but a significant increase in seed and other grain crops. This last category is dominated by herbage seeds (statistics on this item were not collected separately in the 2002 census) and illustrates the responsiveness of farmers to shift towards a high value-added product in a reasonably short period.

The table shows that the area devoted to wine grapes more than doubled, from 749 hectares in June 2002 to 1,683 hectares in June 2007. This means that the Canterbury/Waipara region is now the fourth largest vineyard production area in New Zealand, as shown in Figure 2.2 below. Table 2.5 presents data on the grape varieties grown in the Canterbury/ Waipara region. More than four-fifths (82.1 per cent) of the vineyard areas are in Waipara, which has become an important wine-growing cluster in North Canterbury. Two-fifths of the Canterbury/Waipara wine area is devoted to Sauvignon Blanc grapes (see also Figure 2.3). Pinot Noir accounts for a further 24 per cent, with Chardonnay, Pinot Gris and Riesling being the other three significant varieties in the region.

Figure 2.2 Vineyard Production Areas of New Zealand , 2008

Marlborough

54%

Hawkes Bay

17%

Gisbourne

7%

Canterbury/

Waipara

6%

Otago

5%

Wairarapa/

Wellington

3%

Nelson

3%

Other

5%

Source: New Zealand Winegrowers (2008) Statistical Annual 2008, p. 4, obtained from www.nzwine.com/statistics/.

Note: Calculated from hectares in production. Auckland and Waikato/Bay of Plenty data have been combined with the Other and Unknown category in this chart.

13

Table 2.5 Canterbury/Waipara Grape Varieties, 2008

Crop

Waipara

Hectares

Canterbury

Hectares

Total

Hectares

Pinot Noir 300.0 119.8 419.8

Chardonnay 67.5 56.0 123.5

Pinot Gris 78.6 32.7 111.3

Riesling 279.4 50.5 329.9

Sauvignon Blanc 650.9 34.1 685.0

Other 45.9 16.4 62.3

Total 1422.3 309.5 1731.8

Source: New Zealand Winegrowers (2008) Statistical Annual 2008, pp. 23-24, obtained from www.nzwine.com/statistics/.

Figure 2.3 Canterbury/Waipara Grape Varieties, 2008

Pinot Noir

24%

Chardonnay

7%

Pinot Gris

6%

Riesling

6%

Sauvignon Blanc

40%

Other

3%

Source: New Zealand Winegrowers (2008) Statistical Annual 2008, pp. 23-24, obtained from www.nzwine.com/statistics/.

14

A well recognised characteristic of land production in Canterbury is the influence of water. Recent research by Arthur Grimes and Andrew Aitken (2008) on land in the Mackenzie District of Canterbury, for example, found that irrigated farms sell for up to 50 per cent more than similar non-irrigated farms. Water storage and related issues are considered in the infrastructure chapter of this report.

15

3. The People of Canterbury

The number of people recorded in the 2006 census as usually resident in Canterbury was 521,832. This was 13.0 per cent of the New Zealand usually resident population. It represented an increase of 8.4 per cent since the previous census in 2001, which was above the national rate of increase (7.8 per cent). Table 3.1 shows the distribution of the population among Christchurch City, the eight Districts and the half District of West Waitaki that make up the Canterbury region.

Table 3.1 Usually Resident Population in Canterbury , 2001 and 2006

2001 2006 City, Districts and Region Number % Number %

Change

%

Christchurch City 324,057 67.3 348,435 66.8 4.0

Kaikoura 3,483 0.7 3,621 0.7 6.0

Hurunui 9,885 2.1 10,476 2.0 7.5

Waimakariri 36,900 7.7 42,834 8.2 16.1

Selwyn 27,312 5.7 33,666 6.5 23.3

Ashburton 25,443 5.3 27,372 5.2 7.6

Timaru 41,967 8.7 42,867 8.2 2.1

Mackenzie 3,717 0.8 3,804 0.7 2.3

Waimate 7,101 1.5 7,206 1.4 1.5

West Waitaki 1,566 0.3 1,551 0.3 -1.0

Canterbury 481,431 521,832 8.4

Source: Statistics New Zealand Census of Population and Dwellings data, 2001 and 2006, obtained from www.stats.govt.nz/.

Note: The West Waitaki data is calculated as a residual to ensure that the sum of the numbers for the districts of Canterbury equals the numbers for the region.

16

Two features immediately stand out from Table 3.1. First, two-thirds of the Canterbury population reside in Christchurch City. Of these residents, just over 5,000 live on Banks Peninsula, but a further 11.8 per cent of the region’s population live in the four towns with more than 10,000 residents (Rangiora, 11,871; Kaiapoi, 12,946; Ashburton, 11,931; and Timaru, 24,694). Thus, more than three-quarters of people usually resident in Canterbury live in the region’s five largest urban settlements.

Second, the two Districts that are immediately outside Christchurch City (Waimakariri and Selwyn) had very high population growth over the five year period. The 23.3 per cent increase in Selwyn was the second highest growth by a New Zealand territorial authority between the 2001 census and the 2006 census (only the Queenstown-Lakes District had a higher growth rate), and the 16.1 per cent increase in Waimakariri was the fifth highest in the country. The population of Rolleston on the outskirts of Christchurch City almost doubled from 1,974 people to 3,822 people, an increase of 93.6 per cent. These increases meant that Christchurch City itself grew at the modest rate of 4.0 per cent over the five years. The growth rates in South Canterbury (Timaru, Mackenzie, Waimate and West Waitaki) were all below 2.5 per cent.

The expansion in the residential population within commuting distance of Christchurch City has led to a definition of the ‘Greater Christchurch’ urban area that includes the eastern parts of the Waimakariri and Selwyn Districts and the urban and some rural areas of Christchurch City (including the Lyttelton Harbour Basin). Environment Canterbury, the Christchurch City Council, the Waimakariri District Council, the Selwyn District Council and Transit New Zealand collaborated to produce the Greater Christchurch Urban Development Strategy and Action Plan 2007, referred to by the acronym UDS. This substantial 194 page document is intended to provide the primary strategic direction for the UDS area and to establish a basis for all organisations and the community to co-operatively manage growth.

Official projections of the region’s population growth for the next 25 years are reported in Table 3.2. The Selwyn and Waimakariri Districts are projected to grow at the fastest rate between 2006 and 2031, while the projections suggest that South Canterbury will lose population. Under the medium fertility, mortality and migration assumptions used to derive the data in Table 3.2, the combined share of Christchurch City, Waimakariri District and Selwyn District is projected to increase from 81.6 per cent in 2006 to 84.2 per cent in 2031, while the combined population of South Canterbury is projected to fall by 4.6 per cent over the twenty-five years.

17

Table 3.2 Projected Population in Canterbury, 2006 and 2031

2006 2031 City, Districts and Region Number % Number %

Change

%

Christchurch City 361,800 67.0 422,100 65.9 16.7

Kaikoura 3,700 0.7 3,900 0.6 5.4

Hurunui 10,800 2.0 12,600 2.0 16.7

Waimakariri 44,100 8.2 64,100 10.0 45.4

Selwyn 35,000 6.5 53,400 8.3 52.6

Ashburton 28,000 5.2 30,900 4.8 10.4

Timaru 43,800 8.1 42,300 6.6 -3.4

Mackenzie 3,900 0.7 3,800 0.6 -2.6

Waimate 7,400 1.4 6,400 1.0 -13.5

West Waitaki 1,500 0.3 1,500 0.2 0.0

Canterbury 540,000 641,000 18.7

Source: Statistics New Zealand Subnational Population Projections: 2006(base)-2031 data, 2006 and 2031, obtained from www.stats.govt.nz/.

Notes: Projections are for the 30th of June each year, involving medium assumptions about fertility, mortality and migration. The West Waitaki data is calculated as a residual to ensure that the sum of the numbers for the districts of Canterbury equals the numbers for the region.

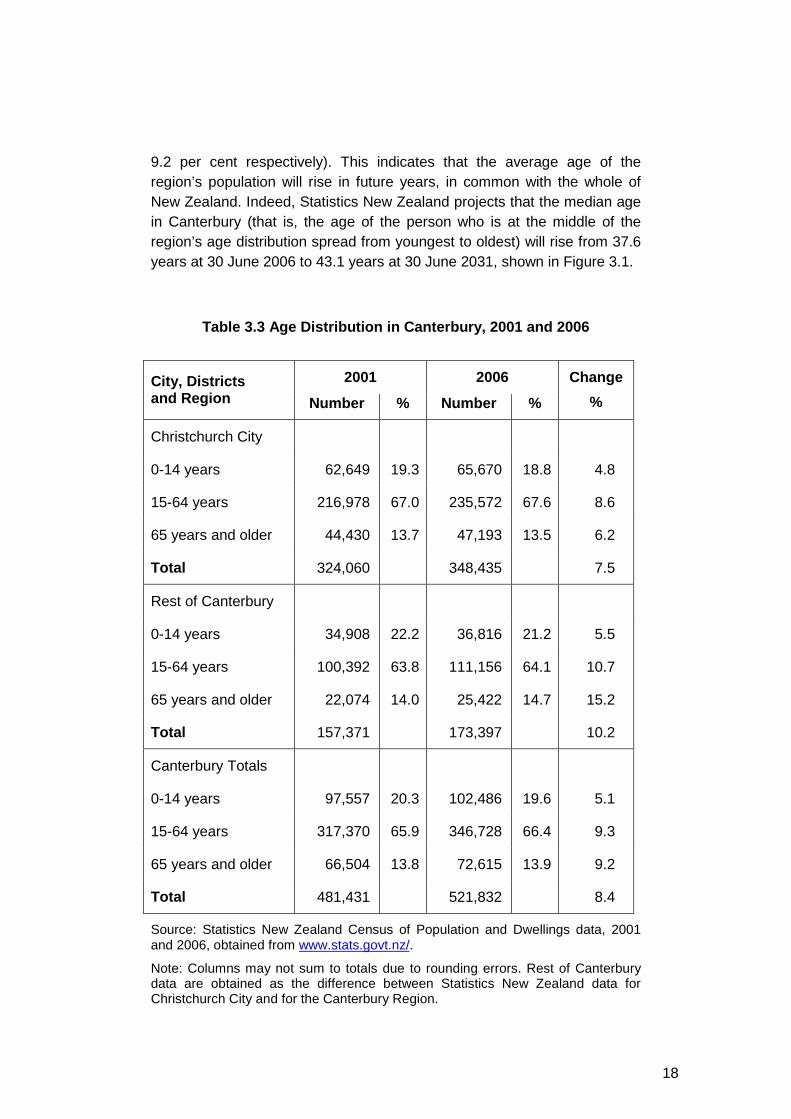

There are some important differences in the population dynamics of Christchurch City compared to the rest of Canterbury. These are presented in Table 3.3 on the next page, which shows the region’s age distribution for three age groups: 0-14 years, 15-64 years, and 65 years and above. The middle group approximates the region’s workforce. The first set of data is for Christchurch City; the second set is for the rest of Canterbury; and the third set contains the totals for the whole of Canterbury.

The first point to note from Table 3.3 is that the growth rate of the youngest age group in Canterbury (5.1 per cent for the five years from 2001 to 2006) is well below the growth rate of the two older age groups (9.3 per cent and

18

9.2 per cent respectively). This indicates that the average age of the region’s population will rise in future years, in common with the whole of New Zealand. Indeed, Statistics New Zealand projects that the median age in Canterbury (that is, the age of the person who is at the middle of the region’s age distribution spread from youngest to oldest) will rise from 37.6 years at 30 June 2006 to 43.1 years at 30 June 2031, shown in Figure 3.1.

Table 3.3 Age Distribution in Canterbury, 2001 and 2006

2001 2006 City, Districts and Region Number % Number %

Change

%

Christchurch City

0-14 years 62,649 19.3 65,670 18.8 4.8

15-64 years 216,978 67.0 235,572 67.6 8.6

65 years and older 44,430 13.7 47,193 13.5 6.2

Total 324,060 348,435 7.5

Rest of Canterbury

0-14 years 34,908 22.2 36,816 21.2 5.5

15-64 years 100,392 63.8 111,156 64.1 10.7

65 years and older 22,074 14.0 25,422 14.7 15.2

Total 157,371 173,397 10.2

Canterbury Totals

0-14 years 97,557 20.3 102,486 19.6 5.1

15-64 years 317,370 65.9 346,728 66.4 9.3

65 years and older 66,504 13.8 72,615 13.9 9.2

Total 481,431 521,832 8.4

Source: Statistics New Zealand Census of Population and Dwellings data, 2001 and 2006, obtained from www.stats.govt.nz/.

Note: Columns may not sum to totals due to rounding errors. Rest of Canterbury data are obtained as the difference between Statistics New Zealand data for Christchurch City and for the Canterbury Region.

19

Figure 3.1 Canterbury Projected Median Age, 1996-20 31

25

30

35

40

45

50

1996 2001 2006 2011 2016 2021 2026 2031

Years

As at 30 June

Source: Statistics New Zealand Subnational Population Projections: 2006(base)-2031 data, 2006 and 2031, obtained from www.stats.govt.nz/.

The second point to note from Table 3.3 is that the population of Christchurch City has been growing more slowly than the rest of the region (7.5 per cent, compared to 10.2 per cent for the rest of Canterbury), but has a greater share of its population in the working age group (15-64 years). In times of low unemployment, this is likely to imply labour shortages in the rural districts of Canterbury if there is a tendency for working age adults who do not have young or elderly dependents to move to the city.

Table 3.4 on the following page presents data on the education attainments of Canterbury school leavers in 2007, available at the Ministry of Education’s Education Counts website. It records 6,759 young people left Canterbury schools in 2007, 40 per cent of whom attained National Certificate of Educational Attainment (NCEA) Level 3 qualification or higher. The proportion attaining NCEA Level 1 or higher was 83.1 per cent, and the proportion qualifying for university entrance was 37.8 per cent. These figures are all better than the national averages recorded that year.

More than two-thirds of the school leavers came from Christchurch City schools (68.3 per cent). The table records some disparities between Christchurch City schools and schools in the rest of Canterbury, especially at the highest attainment levels. Thus, 41.4 per cent of school leavers from

20

Christchurch schools qualified for university entrance, but only 30.0 per cent from the rest of Canterbury. Similarly, 43.5 per cent of Christchurch school leavers attained an NCEA Level 3 qualification or higher, but only 32.4 per cent outside of Christchurch.

Table 3.4 Highest Attainment of Canterbury School L eavers, 2007

Highest Attainment Level Christchurch

City Rest of

Canterbury Canterbury

Totals

No. 2,010 695 2,705 NCEA Level 3 or higher

% 43.5 32.4 40.0

No. 538 217 755 Halfway to a Level 3 qualification % 11.7 10.1 11.2

No. 717 444 1,161 NCEA Level 2

% 15.5 20.7 17.2

No. 320 194 514 Halfway to a Level 2 qualification % 6.9 9.1 7.6

No. 278 206 484 NCEA Level 1

% 6.0 9.6 7.2

No. 335 170 505 Halfway to a Level 1 qualification % 7.3 7.9 7.5

No. 212 106 318 Less than halfway to a Level 1 qualification % 4.6 4.9 4.7

No. 207 110 317 Little or no formal attainment % 4.5 5.1 4.7

No. 4,617 2,142 6,759 Total School Leavers

% 100.0 100.0 100.0

No. 1911 642 2553 University Entrance Attainment % 41.4 30.0 37.8

Source: Ministry of Education School Leavers data, 2007, obtained from www.educationcounts.govt.nz/statistics/schooling/school_leavers2/school_leavers.

Notes: Rest of Canterbury data are obtained as the difference between Ministry of Education data for Christchurch City and for the Canterbury Region. Data excludes international and adult students. The final row (University Entrance Attainment) is already included in the Total School Leavers figures of the previous row. More precise definitions of the qualification levels can be found in the original database available at the above website.

21

4. The Canterbury Labour Force

New Zealand’s labour force statistics define the country’s working age population as those aged 15 and above. The solid line in Figure 4.1 shows the Canterbury region’s working age population over the last 20 years. The dotted line in the figure shows the number of people who were participating in the labour force each quarter. To be counted as part of the labour force, a person must be of working age, and must be either employed (including self-employed) for at least one hour a week or officially unemployed (by actively searching for employment and being available to start work immediately).

Figure 4.1 Canterbury Labour Force and Working Age Population, 1988-2008

0

100

200

300

400

500

600

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Thousands

Working Age Population

Labour Force

Source: Statistics New Zealand Household Labour Force Survey data, 1998-2008, obtained from www.stats.govt.nz/.

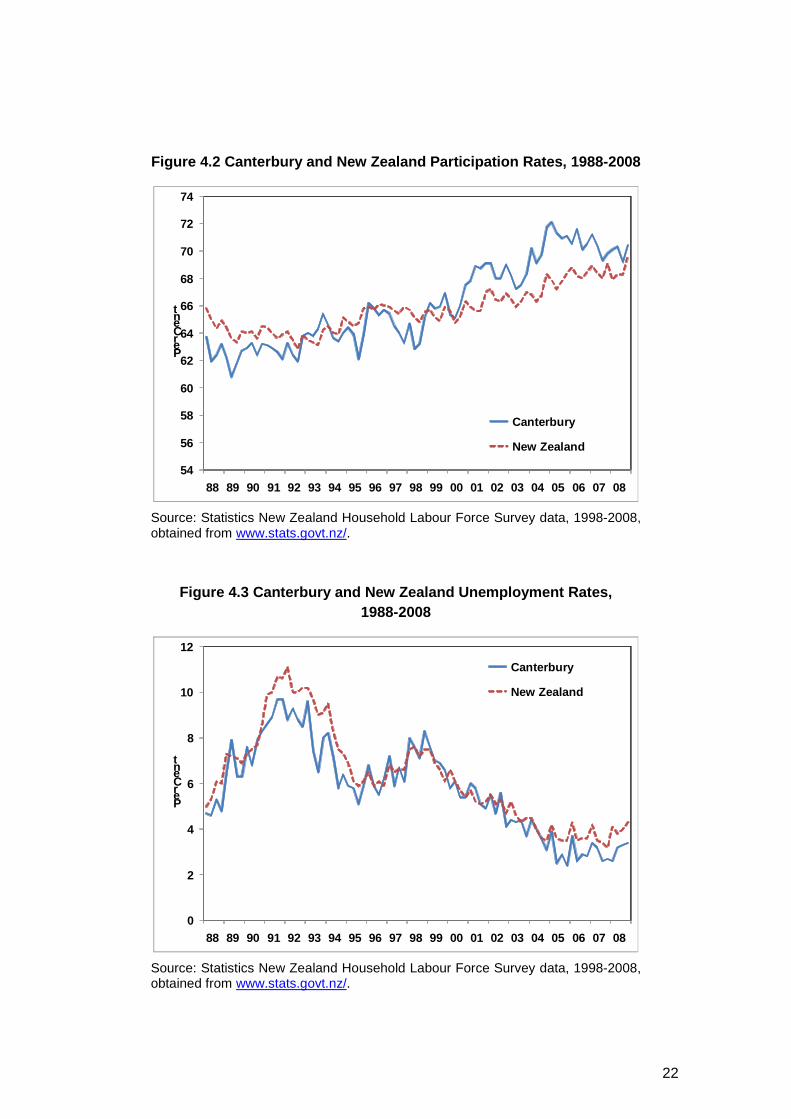

The ratio of the labour force to the working age population is known as the economy’s participation rate. The ratio of the number of people officially unemployed to the labour force is the economy’s unemployment rate. Figures 4.2 and 4.3 show for Canterbury and New Zealand the participation rates and the unemployment rates respectively over the same time period as Figure 4.1.

22

Figure 4.2 Canterbury and New Zealand Participation Rates, 1988-2008

54

56

58

60

62

64

66

68

70

72

74

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Per Cent

Canterbury

New Zealand

Source: Statistics New Zealand Household Labour Force Survey data, 1998-2008, obtained from www.stats.govt.nz/.

Figure 4.3 Canterbury and New Zealand Unemployment Rates, 1988-2008

0

2

4

6

8

10

12

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Per Cent

Canterbury

New Zealand

Source: Statistics New Zealand Household Labour Force Survey data, 1998-2008, obtained from www.stats.govt.nz/.

23

The Canterbury participation rate and the Canterbury unemployment rate track their national counterparts reasonably closely. In recent years, however, the Canterbury participation rate has been consistently higher than the New Zealand figure and the Canterbury unemployment rate has been consistently lower. This suggests that the Canterbury economy has made better use of its potential labour force than nationally, since a greater proportion of the local economy’s working age population participates in the labour force, and a greater proportion of that labour force is in employment.

More information on the potential Canterbury labour force is available from census data, restricting attention to residents aged 15 years and over. An indication of available skills, for example, can be drawn from the distribution of highest qualifications among the working age population. The top half of Table 4.1 compares the qualifications of the Canterbury population with the qualifications of the national population. The distributions are similar, with Canterbury having a slightly larger proportion of residents with no formal qualifications and a slightly lower proportion with a Level 7 qualification or higher.

The bottom half of Table 4.1 makes a comparison between Christchurch City and the rest of Canterbury. For both working age populations, 60 per cent have a secondary school qualification, a Level 1-4 Certificate or a Level 5 or 6 Diploma as their highest education attainment. The distribution of the remaining 40 per cent is very different: Christchurch City has a much lower proportion with no formal qualification and a much higher proportion with a Level 7 qualification or higher.

Table 4.2 presents data on personal incomes for the year ending 31 March 2006 as reported in the 2006 census. Canterbury has a lower proportion than the national figures in the two highest income groups shown in the table ($40,001 or higher) and also has a lower proportion earning zero income or making a loss. Thus there is a greater concentration in the Canterbury population of people receiving income between $10,000 and $40,000.

A similar pattern can be seen in the comparison between Christchurch City and the rest of Canterbury. Christchurch City has a higher proportion with an annual personal income less than $10,000 or greater than $70,000, while the rest of Canterbury is more concentrated in the range $10,001 to $40,000.

24

Table 4.1 Highest Education Attainments of Working Age Population, 2006

Canterbury New Zealand

Number Per Cent Number Per Cent

No qualification 98,436 25.7 708,429 25.0

Qualification gained at secondary school 137,277 35.8 992,568 35.0

Level 1-4 Certificate gained post-school 54,555 14.2 415,221 14.7

Level 5-6 Diploma 38,058 9.9 268,365 9.5

Level 7 qualification and Bachelor degree 38,142 10.0 315,846 11.2

Postgraduate or research degree 16,746 4.4 131,934 4.7

Not elsewhere included 36,126 – 328,014 –

TOTAL 419,343 3,160,371

Christchurch City Rest of Canterbury

Number Per Cent Number Per Cent

No qualification 60,408 23.4 38,028 30.5

Qualification gained at secondary school 93,348 36.1 43,929 35.2

Level 1-4 Certificate gained post-school 35,490 13.7 19,065 15.3

Level 5-6 Diploma 25,836 10.0 12,222 9.8

Level 7 qualification and Bachelor degree 29,805 11.5 8,337 6.7

Postgraduate or research degree 13,476 5.2 3,270 2.6

Not elsewhere included 24,399 – 11,727 –

TOTAL 282,765 136,578

Source: Statistics New Zealand Census of Population and Dwellings data, 2001 and 2006, obtained from www.stats.govt.nz/.

Notes: Columns may not sum to totals due to rounding errors. Rest of Canterbury data are obtained as the difference between Statistics New Zealand data for Christchurch City and for the Canterbury Region. The ‘Not Elsewhere Included’ category includes highest qualification unidentifiable or not stated, and so has not been included in the calculation of percentages.

25

Table 4.2 Total Personal Incomes of Working Age Pop ulation, 2005/06

Canterbury New Zealand

Number Per Cent Number Per Cent

Zero or Loss 18,810 4.9 162,408 5.7

$1-$10,000 61,524 15.9 447,963 15.8

$10,001-$20,000 90,744 23.5 615,981 21.7

$20,001-$40,000 119,004 30.8 839,028 29.5

$40,001-$70,000 71,460 18.5 543,456 19.1

$70,001 or more 25,392 6.6 230,643 8.1

Not stated 32,412 – 320,889 –

TOTAL 419,343 3,160,371

Christchurch City Rest of Canterbury

Number Per Cent Number Per Cent

Zero or Loss 13,008 5.0 5,802 4.6

$1-$10,000 42,531 16.4 18,993 15.0

$10,001-$20,000 59,799 23.0 30,945 24.4

$20,001-$40,000 79,170 30.4 39,834 31.4

$40,001-$70,000 47,610 18.3 23,850 18.8

$70,001 or more 17,946 6.9 7,446 5.9

Not stated 22,695 – 9,717 –

TOTAL 282,762 136,581

Source: Statistics New Zealand Census of Population and Dwellings data, 2001 and 2006, obtained from www.stats.govt.nz/.

Notes: Columns may not sum to totals due to rounding errors. Rest of Canterbury data are obtained as the difference between Statistics New Zealand data for Christchurch City and for the Canterbury Region. The ‘Not Stated’ category has not been included in the calculation of percentages.

26

Table 4.3 Occupations of Employed People, 2006

Canterbury New Zealand

Number Per Cent Number Per Cent

Managers 43,611 17.1 340,530 18.2

Professionals 46,926 18.4 374,328 20.0

Technicians and trades workers 34,569 13.5 241,857 12.9

Community & personal service workers 23,088 9.0 156,471 8.4

Clerical and administrative workers 31,059 12.2 240,816 12.9

Sales workers 26,214 10.3 186,060 9.9

Machinery operators and drivers 17,169 6.7 114,324 6.1

Labourers 32,622 12.8 218,991 11.7

Christchurch City Rest of Canterbury

Number Per Cent Number Per Cent

Managers 25,185 14.9 18,426 21.2

Professionals 35,238 20.9 11,688 13.5

Technicians and trades workers 22,815 13.5 11,754 13.5

Community & personal service workers 16,026 9.5 7,062 8.1

Clerical and administrative workers 21,573 12.8 9,486 10.9

Sales workers 19,059 11.3 7,155 8.2

Machinery operators and drivers 10,992 6.5 6,177 7.1

Labourers 17,604 10.4 15,018 17.3

Source: Statistics New Zealand Census of Population and Dwellings data, 2001 and 2006, obtained from www.stats.govt.nz/.

Notes: Columns may not sum to totals due to rounding errors. Rest of Canterbury data are obtained as the difference between Statistics New Zealand data for Christchurch City and for the Canterbury Region. The table does not report the ‘Not Elsewhere Included’ category, which includes responses that were unidentifiable, outside scope or not stated.

27

Table 4.3 presents the distribution of occupations reported by residents in the 2006 census. Compared to the New Zealand distribution, there are smaller proportions of employed people in Canterbury working as managers or professionals, and a larger proportion working as labourers. Within the Canterbury economy, Christchurch City has considerably smaller proportions employed as managers and labourers compared to the rest of the region. The share of technicians and trades workers is 13.5 per cent in the city and in the rest of Canterbury, but Christchurch has a much larger proportion of people employed in professional occupations.

28

29

5. The Canterbury Economy

The Canterbury economy has undergone radical changes over the last forty years as successive governments adopted four different approaches to managing the national economy. The approaches are listed in Figure 5.1, which shows data on New Zealand’s real per capita gross domestic product (GDP) between 1969/70 and 2007/08. This statistic measures the market value of recorded production in New Zealand, excluding the impact of inflation on market values, divided by the number of people normally resident in the country. This figure is often used as an indicator of average economic well-being in the country, before taking into account factors such as income distribution or environmental degradation.

Figure 5.1 New Zealand Real Per Capita GDP, 1969/70 -2007/08

18,000

21,000

24,000

27,000

30,000

33,000

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

1999/2000 NZ$

Years Ending March

EconomicStagflation

EconomicReform

EconomicTransformation

EconomicTransition

Source: Statistics New Zealand National Accounts data, 1969/70-2007/08, obtained from www.stats.govt.nz/.

The graph divides New Zealand’s policy environment over the last 30 years into four periods. Following the first oil shock of 1973, New Zealand entered into a decade of rising unemployment and relatively high inflation, a phenomenon known as economic stagflation. Following the election of the fourth Labour government in July 1984, New Zealand embarked on a programme of extensive market-led economic reform. This proceeded in two waves; the first wave focused on macroeconomic stability and product market liberalisation, while the second wave (initiated by the National government elected in 1999) focused on welfare reform and labour market liberalisation.

30

The final policy change during the economic reforms was the passing of the Fiscal Responsibility Act in 1994. This was followed by a period of economic transition, as the reforms were bedded in but not extended. A change of government at the end of 1999 saw policymakers adopt a new term: ‘economic transformation’. This approach was reflected in the Growth and Innovation Framework, published by the government in 2002, and was given a further boost in two Cabinet papers outlining the government’s Economic Transformation Agenda in November 2006.

The transformation framework guided the central government’s economic development policies, and many initiatives at the regional level, in recent years. As recorded in Figure 5.1, it was a period of strong economic growth by New Zealand standards, with steady growth in real per capita gross domestic product since 1993, punctuated by the short recession associated with domestic drought and the South-East Asian currency crisis in 1998.

At the time of writing, New Zealand has again entered into a recession triggered by world events. In this case, a global financial crisis that started in the United States sub-prime mortgage market has severely constrained credit and consumer demand in all the major markets around the world. Although New Zealand’s own financial system has not been affected to the same extent as in other countries, the world-wide fall in equity prices and associated economic downturn also affects New Zealand consumers and producers. There is considerable uncertainty about the extent and likely length of the current recession.

Further, November 2008 saw a change of government in New Zealand, with the National Party entering into formal coalition with the Act Party, the Māori Party and the United Futures Party to obtain a strong majority in Parliament. This event has led to a review of economic strategy at the national level, as the new government implements its own policy framework for economic development. As in the past, the Canterbury regional economy will respond to national policy initiatives as well as to changes in the global marketplace.

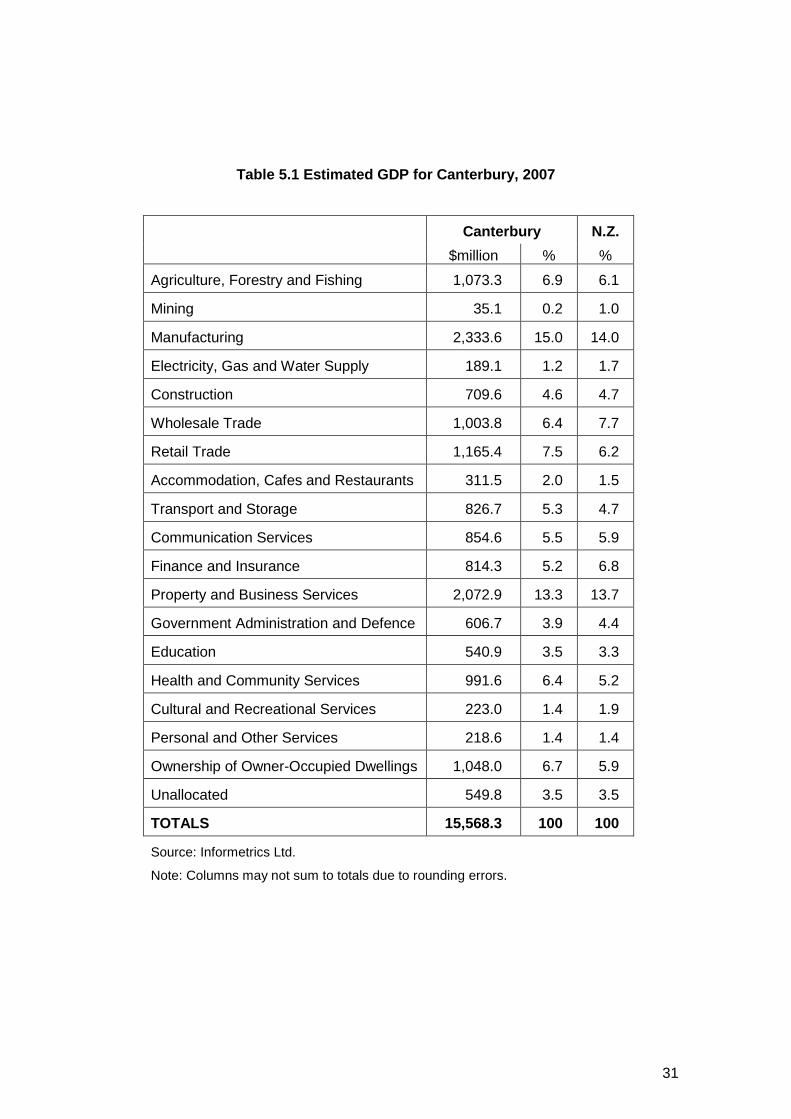

No official data exist for measuring regional gross domestic product, but a number of private institutions use advanced statistical techniques to provide reasonable estimates using standard classifications of industries. Table 5.1 presents data for the Canterbury region estimated by Infometrics Ltd for the 2007 calendar year, and compares the percentage share of each industry with the national percentage share (also estimated by Infometrics) in the same year.

31

Table 5.1 Estimated GDP for Canterbury, 2007

Canterbury N.Z.

$million % %

Agriculture, Forestry and Fishing 1,073.3 6.9 6.1

Mining 35.1 0.2 1.0

Manufacturing 2,333.6 15.0 14.0

Electricity, Gas and Water Supply 189.1 1.2 1.7

Construction 709.6 4.6 4.7

Wholesale Trade 1,003.8 6.4 7.7

Retail Trade 1,165.4 7.5 6.2

Accommodation, Cafes and Restaurants 311.5 2.0 1.5

Transport and Storage 826.7 5.3 4.7

Communication Services 854.6 5.5 5.9

Finance and Insurance 814.3 5.2 6.8

Property and Business Services 2,072.9 13.3 13.7

Government Administration and Defence 606.7 3.9 4.4

Education 540.9 3.5 3.3

Health and Community Services 991.6 6.4 5.2

Cultural and Recreational Services 223.0 1.4 1.9

Personal and Other Services 218.6 1.4 1.4

Ownership of Owner-Occupied Dwellings 1,048.0 6.7 5.9

Unallocated 549.8 3.5 3.5

TOTALS 15,568.3 100 100

Source: Informetrics Ltd.

Note: Columns may not sum to totals due to rounding errors.

32

Based on the data in Table 5.1, a feature of the Canterbury economy is its balanced industry structure, meaning that it is not too dissimilar from New Zealand’s national industry structure. The two largest sectors in Canterbury are manufacturing (15.0 per cent), and property and business services (13.3 per cent). These are followed by retail trade, agriculture, ownership of occupied dwellings and health and community services. This is similar to New Zealand national averages apart from being slightly higher by approximately one per cent in agriculture, manufacturing, retail, health and ownership of occupied dwellings and slightly lower in wholesale trade and finance and insurance.

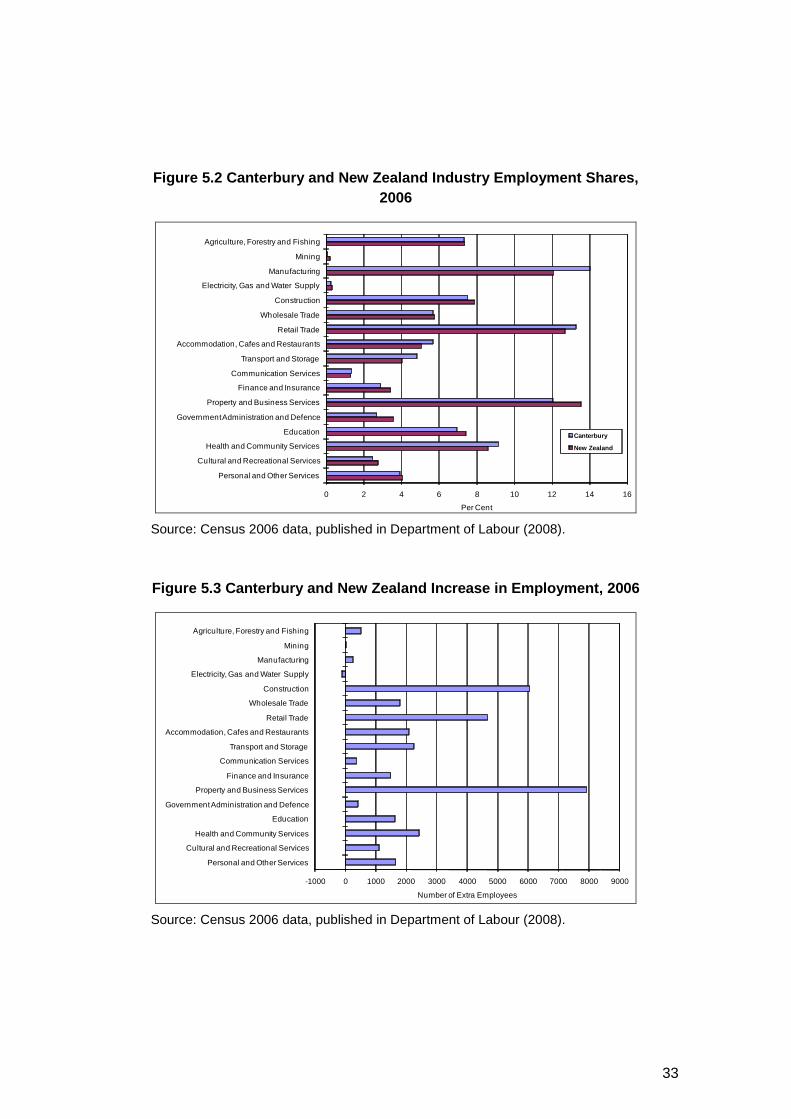

A commonly used source of official information to determine the importance of sectors in a regional economy is employment data, since these are readily obtained from the country’s five-yearly population census. Figure 5.2 shows census employment data for Canterbury, which reveal that the largest sector in the Canterbury region (measured by numbers in employment) is manufacturing, followed by retail trade, and then by property and business services. Between them, these three sectors account for nearly 40 per cent of the employment in Canterbury. The main difference between the Informetrics GDP data and these labour data is the relative ranking of the retail trade (reflecting relatively large employment per output in this sector).

The range of sectors and distribution of activity and employment in both the GDP data and the employment data suggest that the Canterbury economy is well diversified, and does not depend on a few sectors in the same way that the West Coast (for example) relies heavily on dairying, mining and tourism. This diversification means that the Canterbury economy is relatively resilient, since a downturn in one sector can be counter-balanced by ongoing strengths in other sectors.

Figure 5.3 uses the employment data to calculate the increase in number of people employed by sector between the 2001 census and the 2006 census. The largest increase by a considerable margin was in property and business services, followed by construction and then by retail trade. Thus, in terms of size and increased numbers of people in employment, the evidence is clear that the key sectors in Canterbury in recent years have been manufacturing, property and business services, retail trade, and construction.

33

Figure 5.2 Canterbury and New Zealand Industry Empl oyment Shares, 2006

0 2 4 6 8 10 12 14 16

Agriculture, Forestry and Fishing

Mining

Manufacturing

Electricity, Gas and Water Supply

Construction

Wholesale Trade

Retail Trade

Accommodation, Cafes and Restaurants

Transport and Storage

Communication Services

Finance and Insurance

Property and Business Services

Government Administration and Defence

Education

Health and Community Services

Cultural and Recreational Services

Personal and Other Services

Per Cent

Canterbury

New Zealand

Source: Census 2006 data, published in Department of Labour (2008).

Figure 5.3 Canterbury and New Zealand Increase in E mployment, 2006

-1000 0 1000 2000 3000 4000 5000 6000 7000 8000 9000

Agriculture, Forestry and Fishing

Mining

Manufacturing

Electricity, Gas and Water Supply

Construction

Wholesale Trade

Retail Trade

Accommodation, Cafes and Restaurants

Transport and Storage

Communication Services

Finance and Insurance

Property and Business Services

Government Administration and Defence

Education

Health and Community Services

Cultural and Recreational Services

Personal and Other Services

Number of Extra Employees Source: Census 2006 data, published in Department of Labour (2008).

34

Another tool often used by regional scientists to identify key sectors in a regional economy is shift-share analysis. This tool takes the increases in employment shown in Figure 5.3, and analyses how much of each sector’s increase can be explained by: (a) the national economy’s growth over the same period; (b) differences in the national growth rate of each sector; and (c) other regional factors that resulted in a different growth rate for the sector compared to the sector’s national average.

Table 5.2 presents a shift-share analysis of the Canterbury region’s employment increase between 2001 and 2006. The first column shows the total increase in employment in each sector (excluding the residual category of ‘not elsewhere included’ in the census data). This sums to 34,494 extra employees. The remaining three columns analyse how much of this increase can be explained by national trends (columns a and b) and other regional factors (column c, which is a residual calculation).

Between 2001 and 2006, census data recorded an increase of 15 per cent in the number of people employed nationally. Column (a) shows how much Canterbury employment in a sector would have grown by if the sector had increased its employment by this national average of 15 per cent. The sum of this column is 32,434, which is less than the actual figure of 34,494 actually achieved. This indicates that the Canterbury economy did better than the national average in creating employment over the five years.

At the national level, employment in some sectors grew by more than 15 per cent, and others by less than 15 per cent. The impact of this is presented in column (b), which shows how many extra people would have been employed in Canterbury if the sector in the region had grown at the national growth rate of the sector. A negative number means the sector grew by less than 15 per cent nationally. The sum of column (b) is -1,314. The minus sign indicates that Canterbury’s industry structure in 2001 was over-represented in sectors that grew relatively slowly at a national level between 2001 and 2006. Canterbury’s strong employment performance over this period was not due to a fortunate industry structure in 2001; rather the sectors did better on average in Canterbury than they did nationally.

This observation is confirmed in column (c), which is calculated by subtracting columns (a) and (b) from the figure in the first column. A positive value indicates that the sector did better in Canterbury than would be expected from the sector’s national performance, while a negative number indicates the local sector did not increase its employment by as great a percentage as nationally. The column (c) calculations are also presented in Figure 4.4.

35

Table 5.2 Shift-Share Analysis of Canterbury Employ ment, 2001-2006

Explained By:

Sector Total

Increase

(a) Total National Growth

(b) Sector National Growth

(c) Other Regional Factors

Agriculture, Forestry and Fishing

514 2,672 – 3,315 1,157

Mining 3 26 16 – 40

Manufacturing 251 5,212 – 4,854 – 107

Electricity, Gas and Water Supply

-108 109 – 94 – 123

Construction 6,053 1,935 3,652 466

Wholesale Trade 1,798 1,868 – 802 732

Retail Trade 4,661 4,291 – 73 442

Accomm., Cafes and Restaurants

2,089 1,820 395 – 125

Transport and Storage

2,254 1,470 – 136 920

Communication Services

364 445 – 289 208

Finance and Insurance

1,490 867 534 89

Property and Business Services

7,907 3,353 3,655 899

Government Admin. and Defence

409 945 – 133 – 403

Education 1,625 2,364 – 755 16

Health and Community Services

2,428 3,071 11 – 654

Cultural and Recreational Services

1,115 761 558 – 204

Personal and Other Services

1,641 1,224 316 101

TOTAL 34,494 32,434 – 1,314 3,374

Source: Census 2006 data, published in Department of Labour (2008).

36

Figure 5.4 Extra Employees Not Explained by Nationa l Trends, 2001-2006

-1000 -500 0 500 1000 1500

Agriculture, Forestry and Fishing

Mining

Manufacturing

Electricity, Gas and Water Supply

Construction

Wholesale Trade

Retail Trade

Accommodation, Cafes and Restaurants

Transport and Storage

Communication Services

Finance and Insurance

Property and Business Services

Government Administration and Defence

Education

Health and Community Services

Cultural and Recreational Services

Personal and Other Services

Number of Extra Employees Source: Column (c) of Table 4.2.

The stand-out sector in this shift-share analysis is agriculture, forestry and fishing. At the national level, employment in this sector fell by 3.5 per cent between 2001 and 2006. It increased by 2.8 per cent in Canterbury, resulting in 1,157 more people employed in agriculture, forestry and fishing than would have been expected from national trends.

Five other sectors contributed strongly to the region’s better than average performance: transport and storage; property and business services; wholesale trade; construction; and retail trade. Three of these have already been mentioned in previous paragraphs, but the relatively strong regional performance of the wholesale trade sector and of the transport and storage sector suggest that Canterbury may have increased in importance as a hub in business supply chains.

37

6. Key Sectors in Canterbury

From the analysis in Chapter 5, seven sectors might be considered key in Canterbury. Manufacturing is the largest sector in Canterbury, and has a greater share of total employment in Canterbury than is the case nationally. Property and Business Services had the largest increase in employment between 2001 and 2006, is the third largest employer in Canterbury, and grew much more strongly in Canterbury than would be expected from national trends. Retail Trade is the region’s third largest sector by GDP and second largest employer; it also grew more strongly than expected from national trends. Construction had the second largest increase in employment between 2001 and 2006, again above the national trend. Agriculture, Forestry and Fishing was the regional sector that provided the most extra jobs in Canterbury above the level that might be expected from national trends. Wholesale Trade, and also Transport and Storage, both performed better than national trends.

There are, however, weaknesses in this analysis. It does not distinguish exporting producers, and it relies on the standard industry classifications used by Statistics New Zealand. These categories are very broad (manufacturing, for example), and so further analysis is required to identify a region’s particular strengths in production. Further, a core export sector of economic activity might involve several industries in the standard classification. The most important example of this, which is recognised nationally and internationally, is the Tourism sector. Another example that is particular to Canterbury concerns the wide range of activities that take place in Christchurch because of the city’s long association with the exploration and scientific study of Antarctica (see, for example, the material at www.ccc.govt.nz/christchurch/antarcticconnections/).

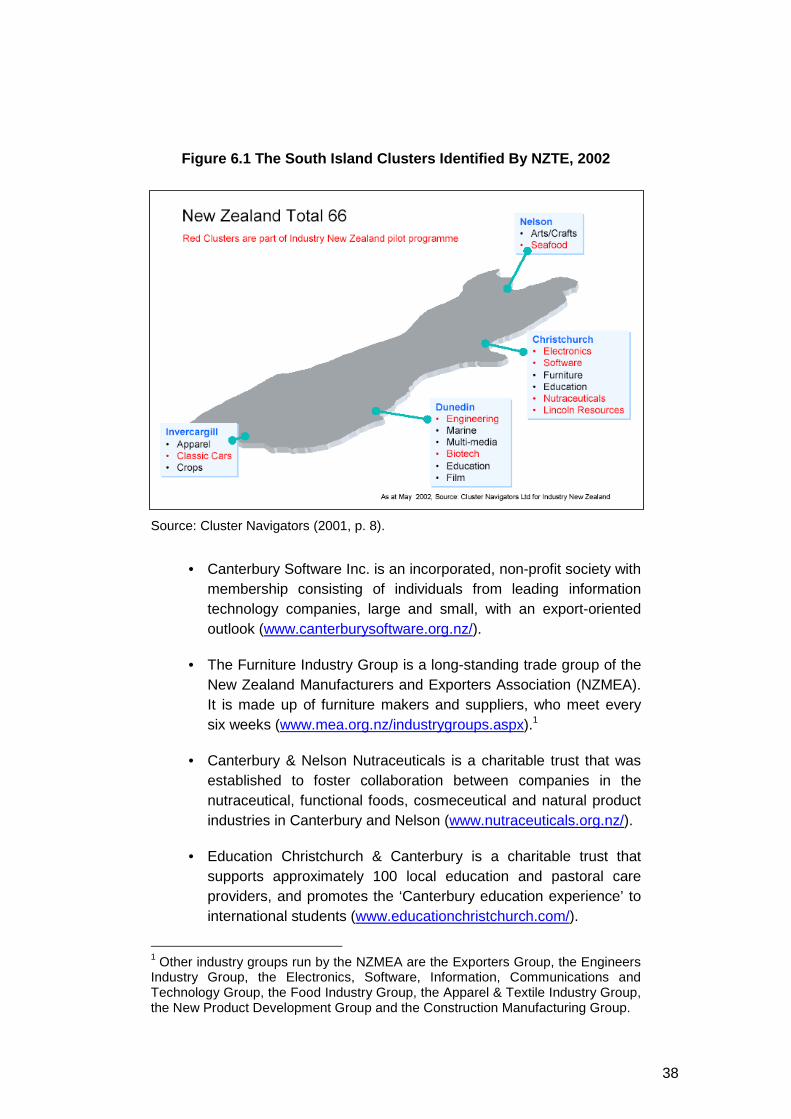

In July 2002, Industry New Zealand (now New Zealand Trade and Enterprise) published work by Ifor Ffowc-Williams and Guy Redding aimed at identifying industry clusters across New Zealand. Figure 6.1 shows the clusters identified for the South Island, six of which were in the Canterbury area: electronics, software, furniture, education, nutraceuticals and Lincoln resources. There have been a number of local and national policies aimed at strengthening these Canterbury clusters.

• Electronics South is an industry group representing approximately 200 electronics design, manufacturing and related companies. It is led by industry professionals and hosts the Connectivity event (see its website at www.electronicssouth.com/).

38

Figure 6.1 The South Island Clusters Identified By NZTE, 2002

Source: Cluster Navigators (2001, p. 8).

• Canterbury Software Inc. is an incorporated, non-profit society with membership consisting of individuals from leading information technology companies, large and small, with an export-oriented outlook (www.canterburysoftware.org.nz/).

• The Furniture Industry Group is a long-standing trade group of the New Zealand Manufacturers and Exporters Association (NZMEA). It is made up of furniture makers and suppliers, who meet every six weeks (www.mea.org.nz/industrygroups.aspx).1

• Canterbury & Nelson Nutraceuticals is a charitable trust that was established to foster collaboration between companies in the nutraceutical, functional foods, cosmeceutical and natural product industries in Canterbury and Nelson (www.nutraceuticals.org.nz/).

• Education Christchurch & Canterbury is a charitable trust that supports approximately 100 local education and pastoral care providers, and promotes the ‘Canterbury education experience’ to international students (www.educationchristchurch.com/).

1 Other industry groups run by the NZMEA are the Exporters Group, the Engineers Industry Group, the Electronics, Software, Information, Communications and Technology Group, the Food Industry Group, the Apparel & Textile Industry Group, the New Product Development Group and the Construction Manufacturing Group.

39

• The Lincoln Resource is a group of companies and organisations involved in land-based research and its application in business, located in and around the Lincoln township in the Selwyn District. It used to host a dedicated website for its profile, but no longer.

More recently, it has generally been recognised that the development of around 80 vineyards in Waipara has given rise to another significant cluster in the Canterbury region. Waipara Valley Winegrowers have created a website to promote the profile of this cluster (www.waiparawine.co.nz/). Its pages contain links to 24 wineries in the valley. The cluster is involved in a substantial research project led by Professor Steve Wratten to promote biodiversity and viticulture pest management through natural bio-control.

In the course of consultations for this report, a number of different sources suggested to the authors that there could be other (unidentified) clusters in Canterbury grouped loosely under the heading of ‘agricultural support industries’. The thought behind this suggestion is that Canterbury has more than 150 years experience exporting agricultural produce, and this has developed world-class expertise in support activities such as seed production, specialist engineering, irrigation systems and veterinary care. The suggestion is that the expertise and skills in these agricultural support industries might provide strong foundations for expansion into new areas of technology-based production.

Tourism is a special type of ‘cluster’ because it cuts across the standard industry classifications. This is recognised by Statistics New Zealand, which produces a Satellite Account to the National Accounts that provides data on tourism in New Zealand. These data are not available at the regional level, but Statistics New Zealand estimates that full-time equivalent employment (both direct and indirect) in New Zealand tourism increased nationally from 158,600 in 2001 to 178,700 in 2006 (Statistics New Zealand, 2008, Table 3, p. 8). This is an increase of 12.7 per cent, which is slightly less than the overall employment growth figure of 15 per cent used in Table 5.2 of the previous chapter.

The Canterbury region contains some of New Zealand’s international iconic tourist attractions. These include WhaleWatch Kaikoura, the Hanmer Springs Thermal Pools and Spa, the International Antarctic Centre in Christchurch, Akaroa Harbour, the Aoraki/Mount Cook National Park, the Mt Hutt Ski Area, and Lake Tekapo. This list illustrates the great diversity of visitor experiences available in Canterbury, from climbing the highest peak in Australasia to watching whales attracted by nutrients created by a 2km deep sea canyon just off the Kaikoura shore.

40

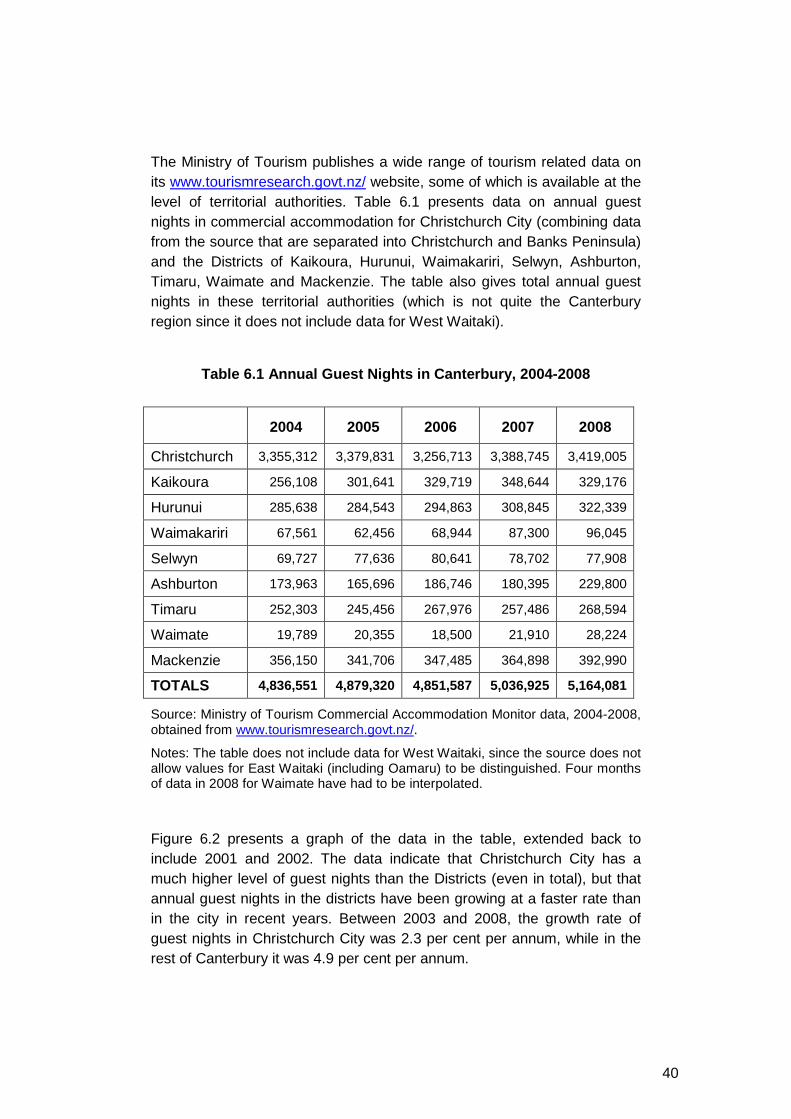

The Ministry of Tourism publishes a wide range of tourism related data on its www.tourismresearch.govt.nz/ website, some of which is available at the level of territorial authorities. Table 6.1 presents data on annual guest nights in commercial accommodation for Christchurch City (combining data from the source that are separated into Christchurch and Banks Peninsula) and the Districts of Kaikoura, Hurunui, Waimakariri, Selwyn, Ashburton, Timaru, Waimate and Mackenzie. The table also gives total annual guest nights in these territorial authorities (which is not quite the Canterbury region since it does not include data for West Waitaki).

Table 6.1 Annual Guest Nights in Canterbury, 2004-2 008

2004 2005 2006 2007 2008

Christchurch 3,355,312 3,379,831 3,256,713 3,388,745 3,419,005

Kaikoura 256,108 301,641 329,719 348,644 329,176

Hurunui 285,638 284,543 294,863 308,845 322,339

Waimakariri 67,561 62,456 68,944 87,300 96,045

Selwyn 69,727 77,636 80,641 78,702 77,908

Ashburton 173,963 165,696 186,746 180,395 229,800

Timaru 252,303 245,456 267,976 257,486 268,594

Waimate 19,789 20,355 18,500 21,910 28,224

Mackenzie 356,150 341,706 347,485 364,898 392,990

TOTALS 4,836,551 4,879,320 4,851,587 5,036,925 5,164,081

Source: Ministry of Tourism Commercial Accommodation Monitor data, 2004-2008, obtained from www.tourismresearch.govt.nz/.

Notes: The table does not include data for West Waitaki, since the source does not allow values for East Waitaki (including Oamaru) to be distinguished. Four months of data in 2008 for Waimate have had to be interpolated.