Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing. Greetings from FundsIndia! The annual exercise of presenting the national budget has come and gone. Our assessment is that this year’s document was an exercise in caution – not measuring up to the built-up hopes of the citizenry, but not falling short in terms of fiscal prudence. Coming as it did in an election year, Mr. Chidambaram has shown commendable restraint in terms of not yielding to political prerogatives at the expense of fiscal discipline. In hindsight, it is possible that there were unrealistic expectations from the budget this year. Given the state of the government’s finances as well as the state of global economy, the minister had little leeway in terms of mak- ing crowd-pleasing concessions in his presentation. However, what is disappointing is the lack of effort in addressing the genuine grievances of a tax-paying populace who are reeling under the effects of high inflation over several consecutive years. One could say that the docu- ment is more protective of the nation’s coffers than those of the common man. For FundsIndia investors, this budget brought in a couple of changes. Short-term investors in debt funds need to be aware of the raise in the dividend distribution tax (DDT) from 12.5% to 25%. Equity investors will be relieved by the reduction in securities transaction tax (STT) imposed at the time of redemption. Please refer to Vidya Bala’s opinion piece in our blog for more details about the impact. In this issue of the newsletter as well, you will find two articles – another essay by Vidya and an essay by Dhiren- dra Kumar, both looking at the budget from different perspectives. One of the few investor-friendly announcements in the budget was the expansion of the RGESS scheme – now available for tax benefit for three years as opposed to one year previously. If you are eligible and would like to save few more thousand rupees in taxes, please login to FundsIndia and let us help you with your RGESS investments. And, of course, this is the month of March, which means that it’s about time you completed your ELSS investments for getting the 80-C tax deduction for this year. If you have not already done it, the time is now! Happy Investing! The monthly newsletter from FundsIndia 06—Mar—2013 Volume 5, Issue 03 Inside this issue: Budget—an exer- cise in caution— Srikanth Meenakshi 1 The month ahead - Equity recommen- dations - B.Krishna Kumar 2 Budgets and the Markets —Vidya Bala 4 Financial Planning Education Series 6 Great Expecta- tions, But Few Achievements —Dhirendra Kumar 7 Budget – an exercise in caution Srikanth Meenakshi *Please note: Comprehensive financial planning is a fee based service

Transcript

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Greetings from FundsIndia!

The annual exercise of presenting the national budget has come and gone. Our assessment is that this year’s document was an exercise in caution – not measuring up to the built-up hopes of the citizenry, but not falling short in terms of fiscal prudence. Coming as it did in an election year, Mr. Chidambaram has shown commendable restraint in terms of not yielding to political prerogatives at the expense of fiscal discipline.

In hindsight, it is possible that there were unrealistic expectations from the budget this year. Given the state of the government’s finances as well as the state of global economy, the minister had little leeway in terms of mak-ing crowd-pleasing concessions in his presentation.

However, what is disappointing is the lack of effort in addressing the genuine grievances of a tax-paying populace who are reeling under the effects of high inflation over several consecutive years. One could say that the docu-ment is more protective of the nation’s coffers than those of the common man.

For FundsIndia investors, this budget brought in a couple of changes. Short-term investors in debt funds need to be aware of the raise in the dividend distribution tax (DDT) from 12.5% to 25%. Equity investors will be relieved by the reduction in securities transaction tax (STT) imposed at the time of redemption. Please refer to Vidya Bala’s opinion piece in our blog for more details about the impact.

In this issue of the newsletter as well, you will find two articles – another essay by Vidya and an essay by Dhiren-dra Kumar, both looking at the budget from different perspectives.

One of the few investor-friendly announcements in the budget was the expansion of the RGESS scheme – now available for tax benefit for three years as opposed to one year previously. If you are eligible and would like to save few more thousand rupees in taxes, please login to FundsIndia and let us help you with your RGESS investments.

And, of course, this is the month of March, which means that it’s about time you completed your ELSS investments for getting the 80-C tax deduction for this year. If you have not already done it, the time is now!

Happy Investing!

T h e m o n t h l y n e w s l e t t e r f r o m F u n d s I n d i a

06—Mar—2013

Volume 5, Issue 03

Inside this issue:

Budget—an exer-c ise in caut ion—Sr ikanth Meenakshi

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Last month, we had highlighted and voiced concern on the apparent slowdown in momentum behind the rally in benchmark indices. The apprehension was not ill founded with the benchmark indices cracking sharply in the later half of February.

The Union Budget was behind us now and the stock market attention would now shift to the global developments and domestic macro-economic indicators. The food inflation is still high and there are hardly any signs of easing. The price of petrol has been hiked recently, which again would foster inflationary pressure.

Given this context, it remains to be seen if the Reserve Bank of India would be keen to cut interest rates any further in its forthcoming meeting scheduled later this month. On the current front, the US Dollar has started strengthening after a period of minor downtrend.

We expect the US Dollar to appreciate to Rs. 56-56.50 levels in the short-term. Given this backdrop, we are unable to comprehend the case for a strong rally in the stock market. On the global front, the compulsory spending cut would come into force in the US, unless the govern-ment takes some remedial measures. Any such forced cuts may result in a dry-up in liquidity and could have repercussions across various asset classes.

Technically too, there are signs to indicate that the index could seek lower levels. As mentioned last month, the index fell to the support zone of 5,650-5,700. In the process, the index has fallen below the crucial support level at 5,820, which is a significant sign of weakness.

We remain bearish on the Nifty and expect the slide to continue to 5,350-5,400 range. From an extremely short-term perspective, there would be a relief rally but we would view any such recovery as an exit opportunity.

Unless-term index scales above the resistance at 5,970, the path of least resistance would be on the way down. The index heavyweights such as Reliance Industries, ONGC, Hindustan Unilever and State Bank India look vulnerable and may act as a drag on the Nifty.

This month, we cover the outlook for a couple of stocks from the metals pack. After being range-bound for several weeks, the BSE Metals index cracked below the lower end of the range, which is a sign of weakness. The short-term outlook for the metals index as well as Tata Steel and Hin-dalco is bearish. We recommend investors to scale down exposures in these stocks.

Tata Steel has been an underperformer and its European operation seems to be a drag on the overall performance. As highlighted in the chart below, Tata Steel has fallen below crucial support level and appears headed to the next support at Rs.310-315 range.

While there could be a temporary respite to the sell-ing pressure around the Rs. 310-315 range, we expect the downward move to extend up to the lower blue line highlighted in the above chart at Rs.290-295. Shareholders may use any rally to pare exposures in the company.

Traders comfortable in the derivatives segment may consider short position on a rally, with a stop loss at Rs.362 for an eventual target of Rs.290, based on spot price.

Continued on page 4 . . .

Page 2 Volume 5, Issue 03

The month ahead - Equity recommendations B. Krishna Kumar

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

Hindalco is another company from the metals pack that has taken a pounding in the past few weeks. The short-term outlook is negative and we anticipate a fall to the major support at Rs.85-86 range.

Shareholders owning Hindalco may reduce exposures while those who are comfortable trading in the fu-tures segment may consider short positions on any pull back rally, with a stop loss at Rs.105 and a target of Rs. 86, basis spot price.

Mr. B. Krishna Kumar also hosts a weekly webinar that discusses the mar-ket outlook for the following week.

You can register for the webinar by clicking here:

https://www4.gotomeeting.com/register/927617871

Page 4 Volume 5, Issue 03

Budget and the markets Vidya Bala—Head - Mutual Fund Research at FundsIndia

Yet another budget and not much has changed except for the negative reaction in the stock market. What would the budget mean for your investments? Should you change your equity strategy or debt strategy? How does the Budget impact your other income, investments and spending?

Well, we may not be able to answer them all as it would mean predicting markets. But let us try to put things in perspective to aid your in-vestment decisions.

Equity market

The Sensex fell 290 points or 1.5 per cent on Budget day; clearly not too pleased with the proposals. An over-optimistic revenue receipt forecast and no conscious effort to cut expenditure does leave much to be said on the fiscal consolidation front.

Lack of any big-bang reforms in terms of promoting capital expenditure (except for investment allowance for 2 years), or improving the environment for project clearances and land acquisition, did not augur too well for capital goods and infrastructure stocks. That means the budget belied hopes of any quick turnaround in these sectors, after having lagged behind this long.

While not much has been done to trigger capital formation, overall rural spending budget is up, thanks to a number of social development allocation made in the budget. But allocation under the MNREGA scheme remains flat at Rs 33,000 crore.

While sectors such as IT and pharma remained neutral on budget day, banking stocks were beaten on fear of a liquidity crunch. This is because the budget has proposed a 12.5% increase in government borrowing to Rs 6.3 trillion. That means the government would suck plenty of credit available in the system, thus impacting the banks’ ability to get money at reasonable costs.

Overall, while you may have very little to cheer on the budget’s impact on equities, this could be the year for accumulating equities. It is years such as the current one, that will help you average costs if you have been running your SIPs. Here are a few dos and don’ts for your

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

equity investments:

· While infrastructure and capital good stocks may be available at low valuations, avoid taking focused bets on them through theme funds or direct equities simply based on budget proposals. Quite a few equity funds have started zeroing-in on stock specific select opportunities in this space, especially backed by low valuations. Hence, you may actually see some of your di-versified/value-based funds gradually increase exposure to select stocks in this space. That should suffice for you.

· Higher rural spending may spell better prospects for the consumer sector. But it is noteworthy that the Government’s pay

commission and MNREGA were key factors driving the consumption sector thus far. While consumer demand may continue, pay commission’s effect has waned and the proposed spending on MNREGA remains flat compared with last year.

· With the sharp run-up in stocks from the FMCG space, these companies may have to keep up with high earnings growth to

deliver returns. A number of you have wished to take exposure to this theme. Our suggestion would be that you do it through diversified funds rather than theme funds.

· Banking stocks were battered on tight liquidity conditions. But then it is worth noting that of the gross borrowings of Rs 6.5

trillion, Rs 50,000 crore is due to bond buyback by the government. The Government is planning to buyback bonds that are falling due in FY-15. If done in a prudent way, this could infuse liquidity to the said extent into the system. Hence, while there could be near-term pain, rate cuts and such liquidity infusion could ease the situation after a few months. Hence, do not panic if your funds are actually accumulating select stocks from this sector.

· Interestingly, mid-cap stocks (using BSE Midcap as the index) have fallen 12 per cent year to date. The budget has not done

much to spruce them up. · If you have seen your mid-cap funds under perform , don’t stop your SIPs. This could be the time to average their costs by

buying in to them steadily. · Overall, the pain of additional burden from surcharge, higher royalty (applicable for many MNCs) and lack of any meaningful

reforms could mean slower earnings growth in the near term. Hence, do not expect the kind of rally you saw in 2012. But if you are one scouting for value, then this could be the year to average your portfolio cost. Apart from SIPs, consider buying funds/index funds as lump sums on market falls of 5 per cent or more. You could also set up VIPs for this purpose to auto-mate it.

Debt market

The five-year and ten-year gilt yields closed 7 basis points higher to 7.87% and 8.9% respectively at the close of Budget day, after the government announced its borrowing programme. Clearly, the impending liquidity crunch drove the yields, dampening the sentiments of those who were betting on a price rally in this segment. What does this spell for your debt funds? It spells opportu-nities! Contrary to our belief that debt fund performance would become more sedate in the coming fiscal, the budget provides sufficient scope for some action on the debt side.

Strategy

Given the liquidity crunch that is likely to prevail over the next couple of months, short-term funds would be a good idea for in-vestors looking for investment avenues for about a year. It is noteworthy that 60-65% of government borrowings typically happen in the first half of the year. Hence, with rate cuts likely to have happened by that time, yields may ease up a bit, providing some opportunity in instruments with medium time frame. If you have not less than a time frame of 1.5-2 years, consider going for income funds/dynamic bond funds. Within this class, be aware of funds that also play on the credit risk. The latter is for more risky investors. Even if you wish to play the gilt game (not much steam left in it), consider using income funds that have some gilt exposure, than going for pure gilt funds. In all, expect yields of corporate and government bonds to be range-bound for a good part of the year. That means returns may not be much lower than last year.

Budget and you The budget does have some impact on your personal finances, your spending and your investment options. To know more, read our blog: http://www.fundsindia.com/blog/index.php/mutual-funds/budget-2013-10-measures-that-can-impact-you/1408/ Vidya Bala is the Head of Mutual Fund Research at FundsIndia. A chartered accountant by training, she was earlier with the Hindu Business Line’s research bureau, tracking mutual funds, stock markets and sectors for eight years. She writes for our monthly newsletter on topics including mutual fund, personal finance and equity markets. Vidya Bala can be reached at [email protected]

Page 5 Volume 5, Issue 03

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

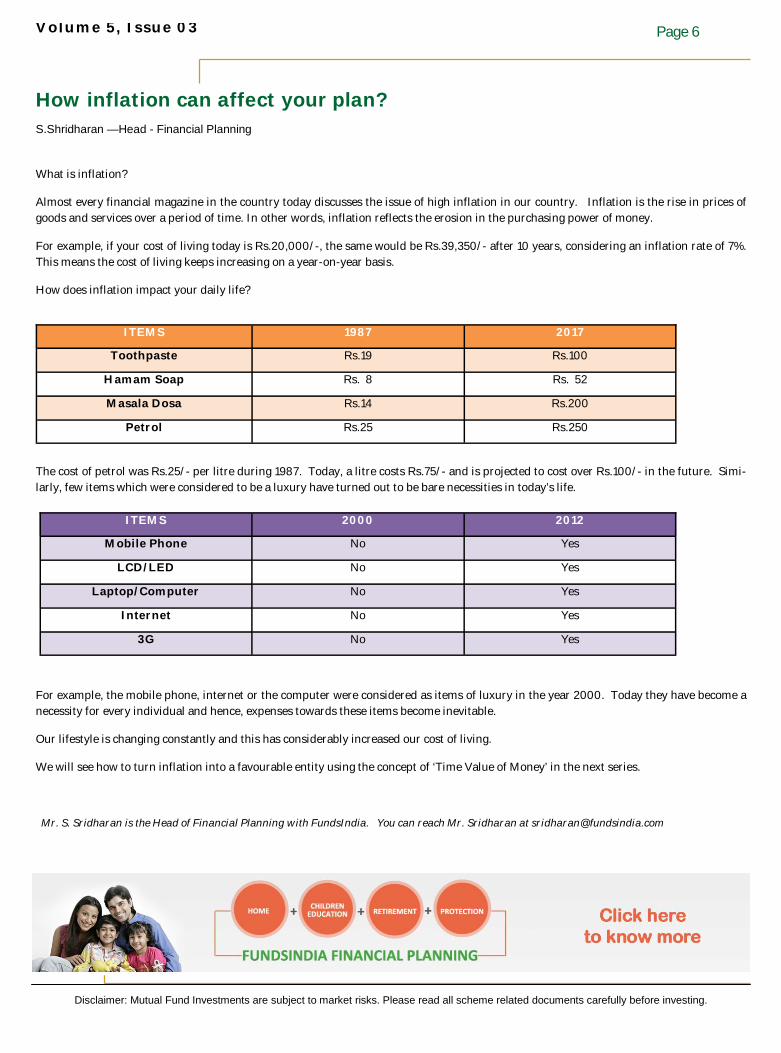

What is inflation?

Almost every financial magazine in the country today discusses the issue of high inflation in our country. Inflation is the rise in prices of goods and services over a period of time. In other words, inflation reflects the erosion in the purchasing power of money.

For example, if your cost of living today is Rs.20,000/-, the same would be Rs.39,350/- after 10 years, considering an inflation rate of 7%. This means the cost of living keeps increasing on a year-on-year basis.

How does inflation impact your daily life?

The cost of petrol was Rs.25/- per litre during 1987. Today, a litre costs Rs.75/- and is projected to cost over Rs.100/- in the future. Simi-larly, few items which were considered to be a luxury have turned out to be bare necessities in today’s life.

For example, the mobile phone, internet or the computer were considered as items of luxury in the year 2000. Today they have become a necessity for every individual and hence, expenses towards these items become inevitable.

Our lifestyle is changing constantly and this has considerably increased our cost of living.

We will see how to turn inflation into a favourable entity using the concept of ‘Time Value of Money’ in the next series.

Mr. S. Sridharan is the Head of Financial Planning with FundsIndia. You can reach Mr. Sridharan at [email protected]

ITEMS 1987 2017

Toothpaste Rs.19 Rs.100

Hamam Soap Rs. 8 Rs. 52

Masala Dosa Rs.14 Rs.200

Petrol Rs.25 Rs.250

ITEMS 2000 2012

Mobile Phone No Yes

LCD/LED No Yes

Laptop/Computer No Yes

Internet No Yes

3G No Yes

Page 6 Volume 5, Issue 03

How inflation can affect your plan? S.Shridharan —Head - Financial Planning

Disclaimer: Mutual Fund Investments are subject to market risks. Please read all scheme related documents carefully before investing.

As the dust settles on the Union Budget for 2013-14, the moral of the story is quite clear: if you don't want to be disappointed, then don't get your hopes too high. For a whole set of reasons, all of us—as savers, investors, busi-nessmen and analysts, had psyched ourselves into expecting something special. As budget day came nearer, we heard the phrase 'dream budget' more and more. There was supposed to be some magic wand that Mr. Chidambaram would wave and all would be well again.

It was always wishful thinking and has proven to be. However, from the perspective of personal finance, saving and investments, the budget has turned out to be a deep disappointment. There were a large number of quite reasonable expectations of simple measures that could have been taken but none of them have been. Somehow,

the powers seem quite unaware of the fact that the ordinary individual saver is in a deep crisis and we need a structural overhaul in savings to rescue the situation.

We are saving less, we are saving in the wrong things and we are getting less from our savings. The propensity to invest in equity and equity-backed mutual funds is decreasing, while at the same time, deposits, bonds and other fixed-income investments are earning less and less compared to the consumer inflation rate. The budget does nothing for any of this.

In the weeks leading up to the budget, there were definite indications from the finance ministry that either an enhancement to the Rs. 1 lakh limit for section 80C tax exemptions or some kind of a new pension-targeted saving scheme was in the works. None of that has materialised.

Instead, all we have is the extension of the Rajiv Gandhi Equity Savings Scheme (RGESS) from one to three years. Since it was first an-nounced in the last budget, it has been clear that while the RGESS has the germ of a good idea, it was needlessly complicated. And learning to deal with all the complexity was not much use because the scheme could be used only once in a lifetime and that too by those who had never invested in stocks before. Now, that single-use limit has been extended to three but all the other complexity remains. A lot of people in the finance ministry will admit that the scheme was announced in haste with the wrong targets in mind but somehow the government seems anchored to those faults instead of thinking afresh.

The other changes too haven't materialised. The section 80C limit of Rs. 1 lakh is now unchanged for more than a decade and its real value has declined sharply. Channeling long-term, retirement-oriented savings remains a pipe dream.

Instead of improvements, the budget creates a couple of new problems. One is the massive hike in dividend distribution tax. If you are an investor who gets dividends from your stock investments or your fixed-income mutual funds, the deduction at source will be 25 per cent, rather than the current 12.5 per cent. Those who depend on these sources for income will be hit hard. From being barely more than the base income tax rate, the dividend distribution rate has gone up close to the highest tax bracket.

One more potential issue is that the KYC norms for insurance have been made easier, but not for mutual funds. This is an odd move, given that most of what is sold as insurance are actually investment products. Hopefully, by the time the budget is passed, this will be fixed.

Syndicated from Value Research Online—Article can be viewed online here—http://www.valueresearchonline.com/story/h2_storyview.asp?str=101431

Page 7 Volume 5, Issue 03

Wealth India Financial Services Pvt. Ltd., H.M. Centre, Second Floor,