97

Capital Markets Day 1 February 2018

Capital Markets Day 1 February 2018

Agenda

Business overview - Jane Aikman

Hull and East Yorkshire - Cathy Phillips

National Network Services - Iain Shearman

BREAK

Enterprise - Stephen Long

Investment in core assets and capabilities - Sean Royce and Jane Aikman

Summary - Jane Aikman

Wine and canapes

Business overview Jane Aikman

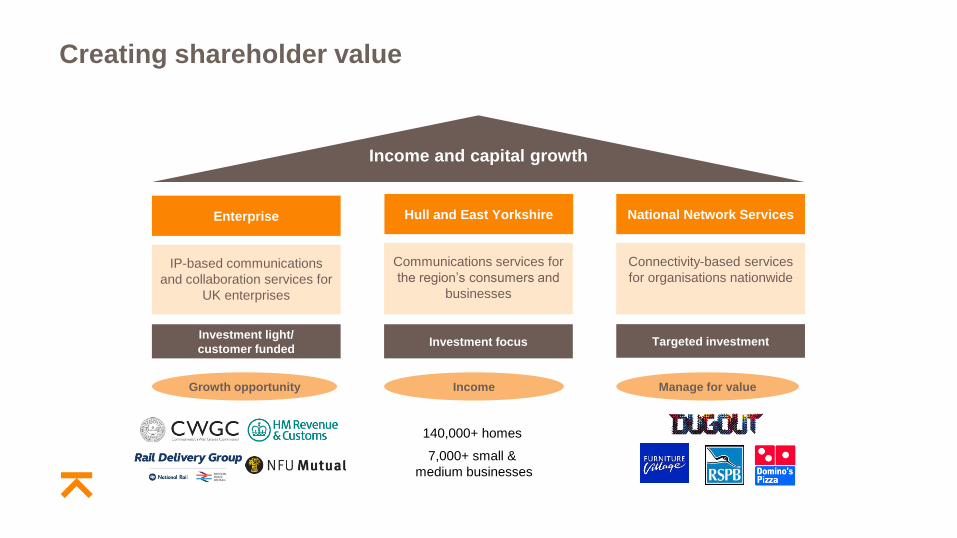

Investment focus Targeted investment Investment light/

customer funded

Income and capital growth

Hull and East Yorkshire Enterprise National Network Services

Communications services for

the region’s consumers and

businesses

Connectivity-based services

for organisations nationwide

IP-based communications

and collaboration services for

UK enterprises

Growth opportunity Manage for value Income

Creating shareholder value

140,000+ homes

7,000+ small &

medium businesses

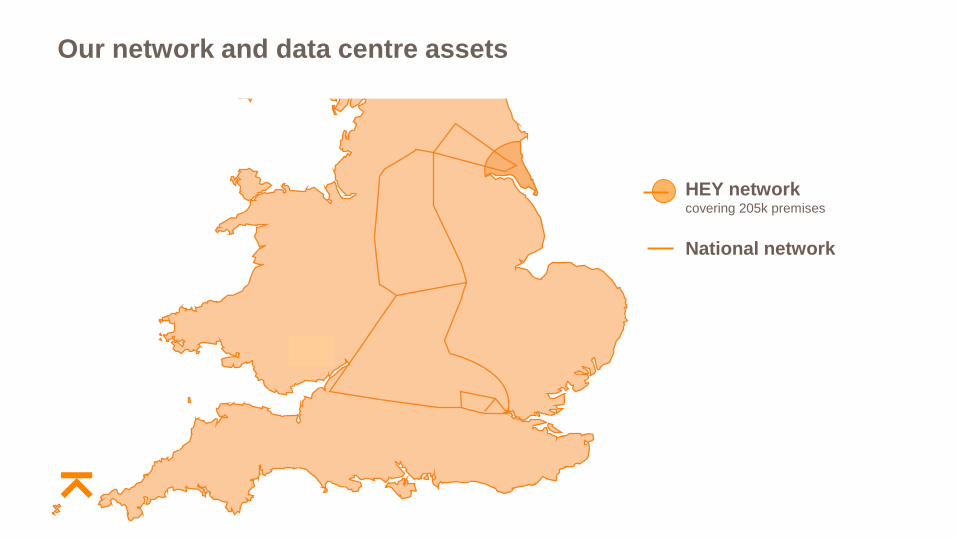

Our network and data centre assets

HEY network covering 205k premises

Our network and data centre assets

HEY network covering 205k premises

National network

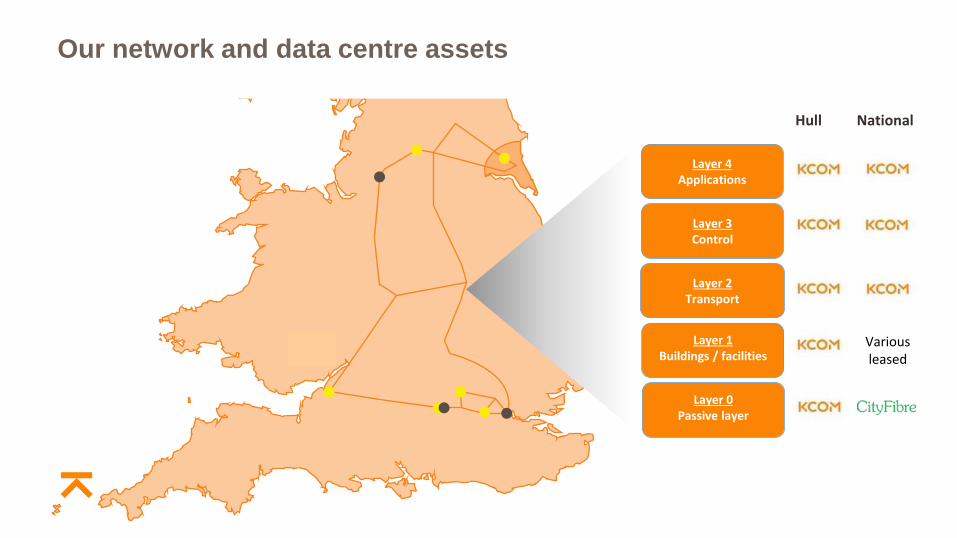

Our network and data centre assets

HEY network covering 205k premises

KCOM’s own Private Cloud (e.g. leased data centres capacity)

National network

Our network and data centre assets

HEY network covering 205k premises

KCOM’s own Private Cloud (e.g. leased data centres capacity)

Access to Public Cloud (eg. AWS, Azure)

National network

Our network and data centre assets

Layer 4 Applications

Layer 3 Control

Layer 2 Transport

Layer 1

Buildings / facilities

Layer 0 Passive layer

Various leased

Hull National

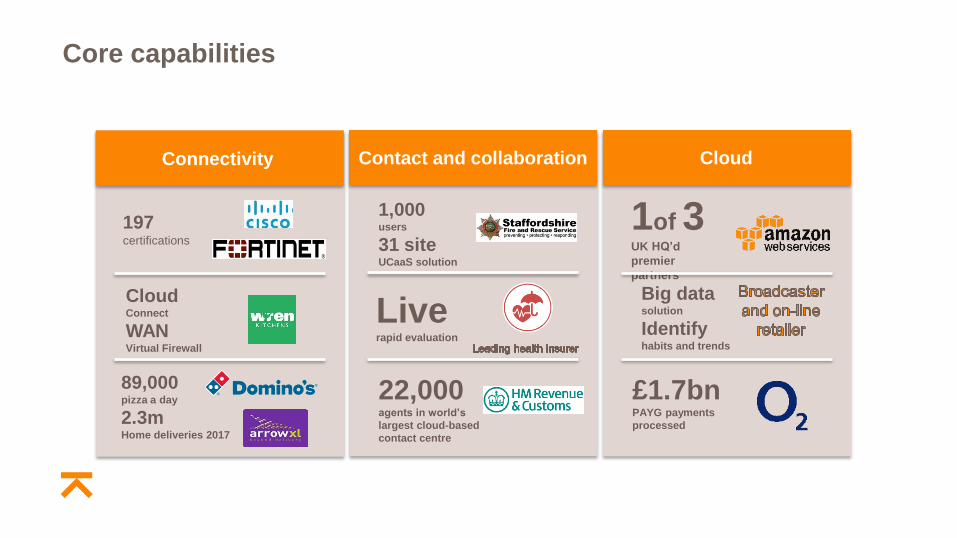

Core capabilities

> Connectivity capability

> Contact and collaboration

> Cloud professional services

> Partner and vendor relationships

> Project delivery

> Service delivery

> Customer service

Investment to improve

scalability, efficiency and

to support the strategy

Connectivity capability

Virtualised Hybrid Connectivity

DSL MPLS 3G/4G Ethernet Optical

Cloud

Connect

Private

Cloud

Programmable

Dev ops Orchestration

Secure

Virtual firewall

Policy Management

Connectivity capability

Our people, expertise and

heritage Robust proven delivery

and support processes

In-depth customer

visibility and control

• Managed 1,000 cloud

instances

• Award winning billing and

reporting capability

• Management tools

• Over 50 national WAN

customers

• 129,000 broadband customers

• 190 Cisco certifications

• 7 Fortigate certifications

• ITIL accredited

• ISO9001

• First to deliver Cisco UK WAN

optimisation

• First UK PSN deliveries

Customer first…….

> We put in front of the customer the technical team that will design, build, and support and deliver the solution proposed

> We are able to be flexible and bespoke elements of customer solution at pace

> We map our values with customer values so we support their business goals

…….increasing the level of customer intimacy

Contact and collaboration

capability

> Building on our Telco heritage and

connectivity capabilities

> Combined with our knowledge in customer

experience

> We have successfully designed, installed and

managing the largest contact centre in Europe

for HMRC

> We have a strong omni-channel proposition

> Cisco gold partner status

> Small number of competitors

> Currently achieving 15-20% of the market of

contact centres over 500 seats in private

cloud*

* Sources: KCOM internal analysis; Proprietary research,

Cairneagle 2017; “UK contact Centres 2018-2022, the State of the

Industry”, ContactBabel; “RPA state of the Market”, Everest.

Contact and collaboration - strength in partner relationships

Cisco Cisco Cisco eGain Verint

Calabrio

Cisco Collaboration

Partner of the Year

EMEAR 2015

Cisco Cloud Contact

Centre Partner of the

Year EMEAR 2014

eGain World Partner

award for 2015

Verint Best New

Partner for EMEA

2015

Eco system built on Best of Breed Partners

Corporate Telephony Unified Comms Contact Centre Workforce Optimisation CRM Web

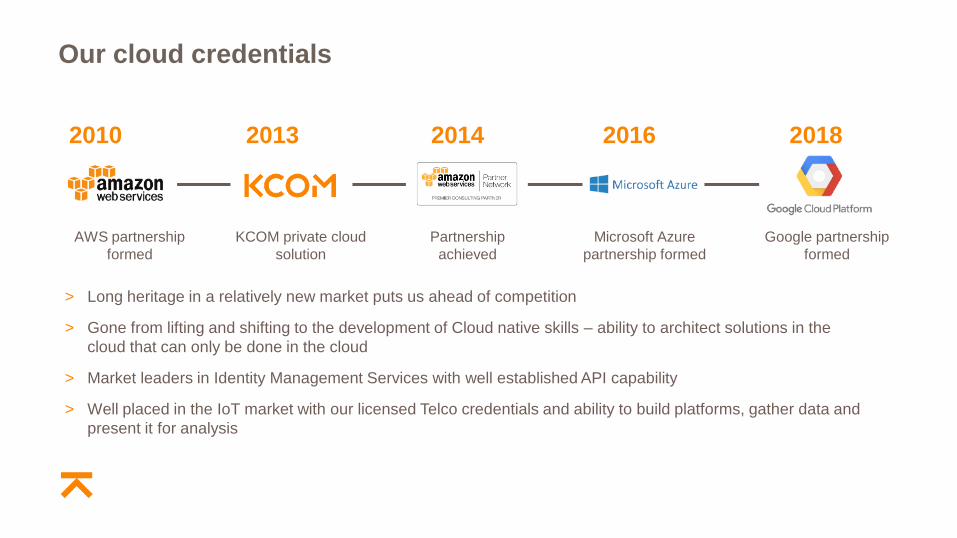

Our cloud credentials

2010 2013 2014 2018

Partnership

achieved

AWS partnership

formed

KCOM private cloud

solution

Microsoft Azure

partnership formed

2016

Google partnership

formed

> Long heritage in a relatively new market puts us ahead of competition

> Gone from lifting and shifting to the development of Cloud native skills – ability to architect solutions in the

cloud that can only be done in the cloud

> Market leaders in Identity Management Services with well established API capability

> Well placed in the IoT market with our licensed Telco credentials and ability to build platforms, gather data and

present it for analysis

Core capabilities

1of 3

UK HQ’d

premier

partners

Cloud

Big data solution

Identify habits and trends

£1.7bn PAYG payments

processed

Contact and collaboration

1,000 users

31 site UCaaS solution

Live rapid evaluation

22,000 agents in world’s

largest cloud-based

contact centre

197 certifications

Connectivity

Cloud Connect

WAN Virtual Firewall

89,000 pizza a day

2.3m Home deliveries 2017

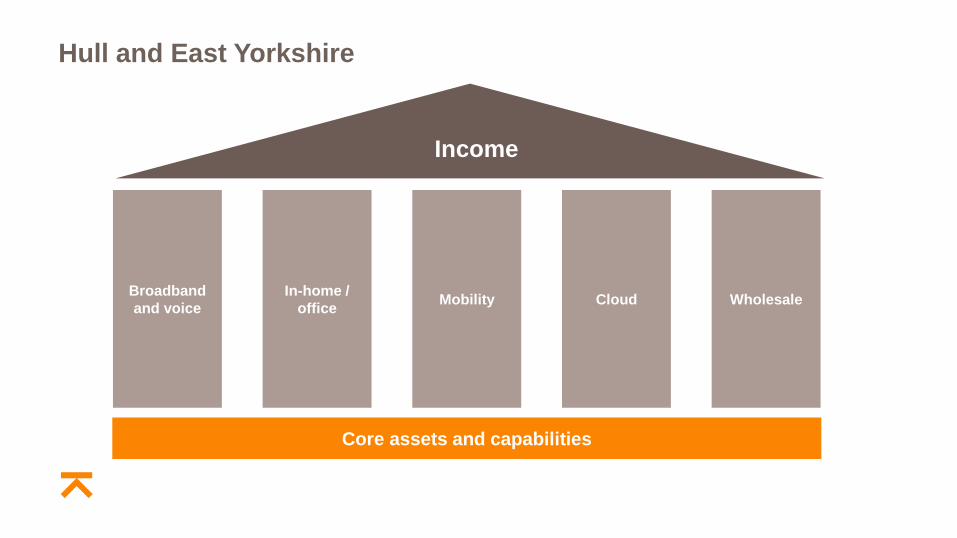

Hull and East Yorkshire Cathy Phillips

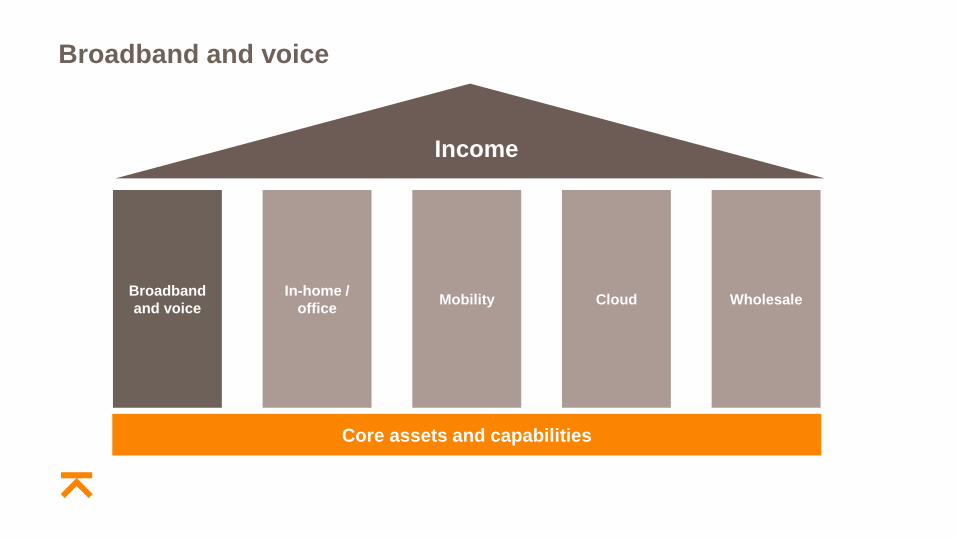

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

Hull and East Yorkshire

EYE

OLA

HCC

East Yorkshire Expansion

6k Consumer customers (27%)

0.4k Business customers* (18%)

City of Hull Boundary

81k Consumer customers (69%)

5.8k Business customers* (89%)

Original Licensed Area

Outer

52k Consumer customers (87%)

4.3k Business customers* (93%)

With differing demographics, competitors, opportunities and regulation

* Via direct and indirect channels

Our HEY market – three distinct areas

Our HEY market – Consumer competition

EYE

OLA

HCC

* Via direct and indirect channels

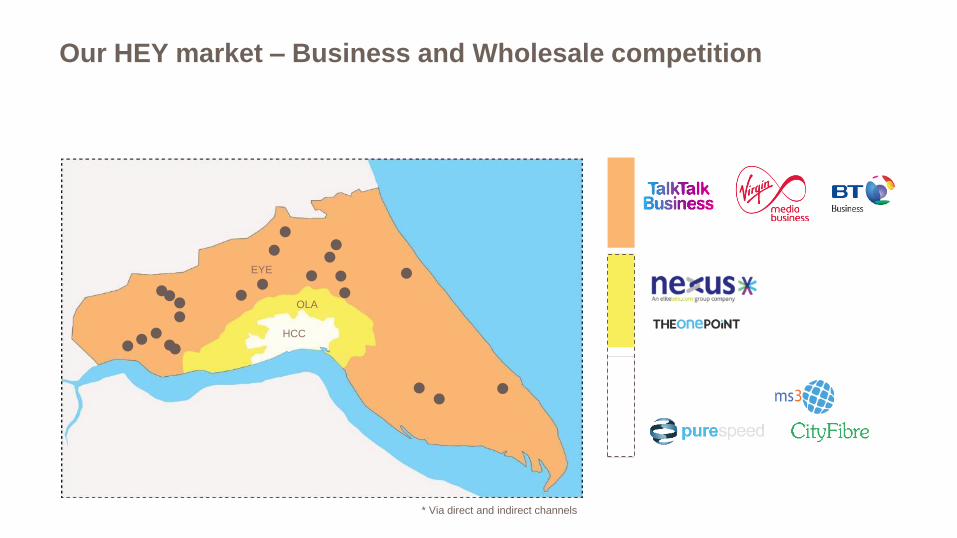

Our HEY market – Business and Wholesale competition

EYE

OLA

HCC

* Via direct and indirect channels

Don’t use Mobile

(cost) Outside home Mobile

(choice) Fixed basic Fixed

typical

Fixed

savvy

The Service Proposition Model

Our Internet User groups

shape the need

Our Customer Charter

forms the guidelines for

everything we do

End to end propositions

built around customer

need – One Size will

not fit all

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

Broadband and voice

Broadband and Voice

> Consistent year-on-year HEY Consumer revenue growth

> Mix change away from fixed voice revenues to broadband ISP and data revenues

> Growth underpinned by broadband acquisition and fibre conversion

£0.0

£10.0

£20.0

£30.0

£40.0

£50.0

£60.0

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Re

ven

ue

(£m

)

Other Revenue (£m)

Total Broadband Revenue (£m)

Voice Only Revenue (inc calls) (£m)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

Pe

ne

trat

ion

rat

e (

%)

Bro

adb

and

Cu

sto

me

r s

(No

)

Fibre Connections ADSL Connections BB Penetration of Customers

Broadband and Voice leveraging our fibre network and services to deliver profitable growth

Lightstream roll out Performance and reliability

Driving customer connections through our

superior infrastructure offering faster

and more reliable service

Personalise our portfolio and offering

flexibility as customers can choose their

speeds and data usage as they need

Flexible Portfolio Monetise usage of broadband

speeds and data

A broadband portfolio that allows flexibility

as customers can self-serve e.g. upgrading

speed

Bundled Services Tailored options

Current Next Future

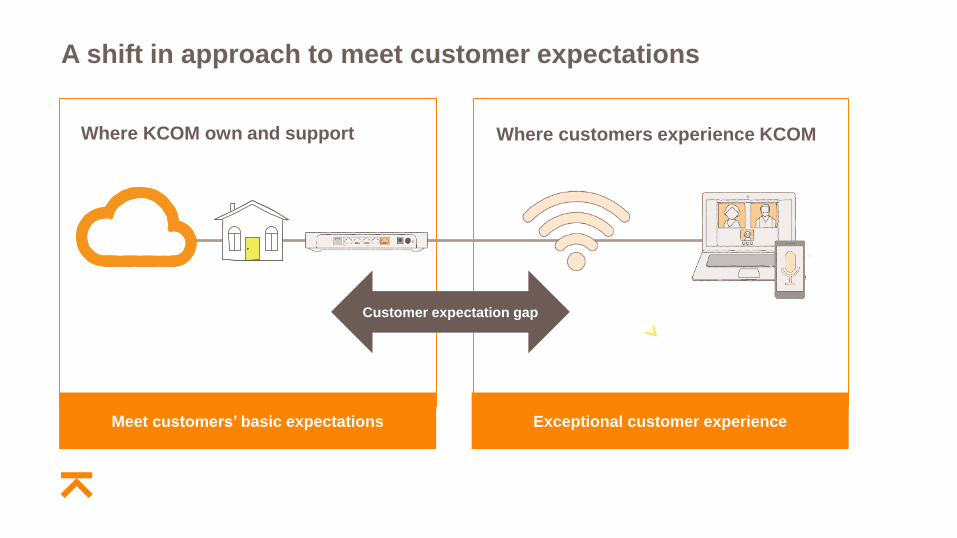

A shift in approach to meet customer expectations

Meet customers’ basic expectations

Customer expectation gap

Where KCOM own and support Where customers experience KCOM

Exceptional customer experience

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

In-home / office

In-Home Proposition To support broadband growth and increase customer satisfaction

In-home Improve Wi-Fi connectivity

in and around the home

Enhance the in-home customer

experience through improved

onboarding and proactive support

services such as:

> Wi-Fi health checks

> Remedial solutions

> Priority service options

Support the use of more devices and

offer safety, management and control

of the online world through:

> Improved parental controls

> Anti-virus software

> Wi-Fi device control app

> Discounts

Optimisation Flexibility and control

Enable Support customers to

do more online

Support the use of more internet

enabled devices:

> Laptops, tablets, mobiles, games

> OTT services

> Smart home products

Current Next Future

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

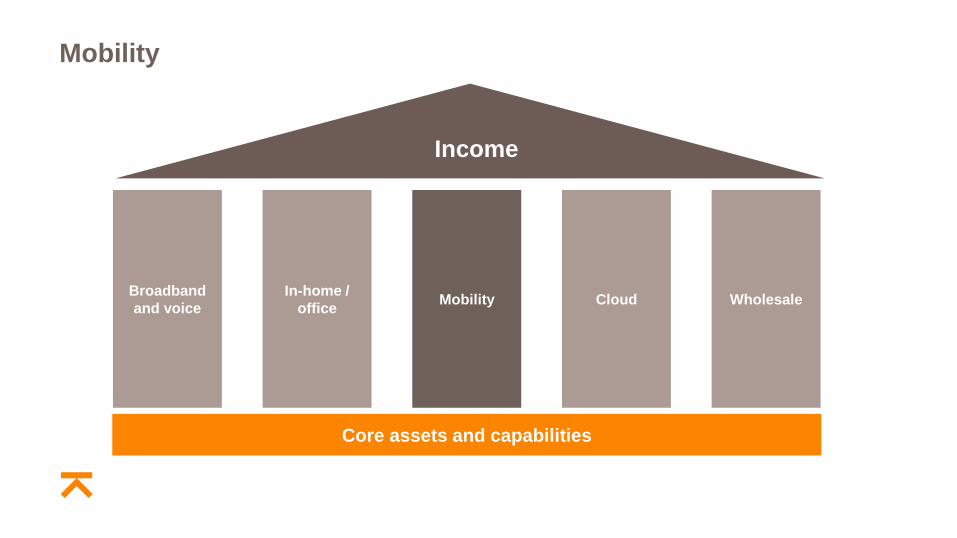

Mobility

Mobility proposition To acquire new customers, drive share of wallet and leverage our fibre asset

to provide a unique proposition

> Capture both fixed and mobile data

in and out of the home/office

> Leverage our fixed asset and

offload mobile data

> Become a leader in our local market

Expand offering Strategic: consolidate Fixed and mobile

convergence

> Re-iterate the customer journeys

to address all core segments and

start developing leadership

position

> Enhanced MVNO capability that

allows KCOM to truly differentiate

itself in the market place

> Innovative commercials that blur

the boundaries between fixed and

mobile data

Current Next Future

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

Cloud

Voice and contact Business apps Networking and security

> Maximise opportunity with KCOM’s

current business cloud telephony

and VoIP solution, evolving

cloud-based call management and

PCI capabilities

> Evolve KCOM’s relationship with

Microsoft to drive uptake of O365

and the wider portfolio and identify

other suitable business apps

> Deliver KCOM’s managed Wi-Fi

and network security propositions

(Meraki). Enable secure hybrid

inter-cloud working

Cloud Propositions To meet change in customer behaviours and increase share of wallet

Current Next Future

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

Wholesale

Wholesale propositions Be the partner of choice with a range of access products that deliver best value

> Deliver growth through revised

Ethernet pricing and introduction of

fibre access. Driving large capacity

1 GIG and 10 GIG as standard

> Provide flexible branch network

solutions with easy enablement of

new services

> Leveraging our Software Defined

Networks developments, create

managed options that provide

innovative and compelling ways to

connect

Refresh Expand Manage

Current Next Future

Broadband

and voice

In-home /

office Cloud Mobility

Income

Wholesale

Core assets and capabilities

Hull and East Yorkshire

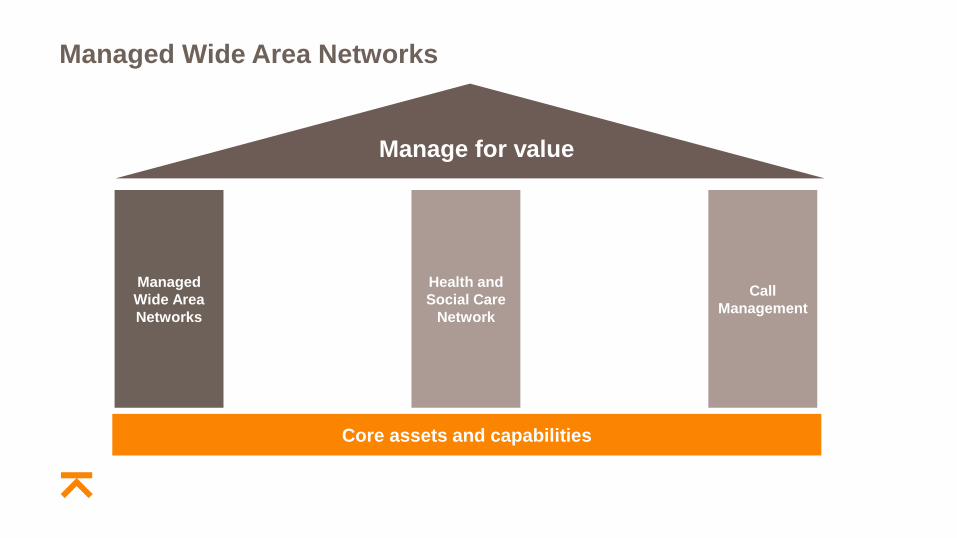

National Network Services Iain Shearman

Managed

Wide Area

Networks

Health and

Social Care

Network

Call

Management

Manage for value

Core assets and capabilities

National Network Services

NNS value of customer segments

500 (3%)

750 (3%)

20,000 (94%)

Customer numbers by segment

44%

31%

25%

Margin (£) contribution by segment

Grow

Maximise

Manage

Defining the NNS market – Segmentation approach

Grow Maximise Manage

Distributed

Government and

public funded

organisations,

both national and

regional bodies

Businesses

present across

several regions

and able to serve

a national market

Regional and

specialist

businesses

Lifestyle businesses

or those growing to

be established in

chosen market

Large-scale orgs

that provide

expertise in

adoption of IT and

managed services

Large businesses

that provide

managed ICT

Internationally, often

with own

infrastructure

Consumer, home

office and micro

businesses

Local, trusted

providers of network

products and

services

Large channel

partner with strong

brand presence

Need to embrace

modern working.

Aligned to

frameworks and

cost-conscious

Trusted advisor

who can deliver

increasingly

complex

connectivity and

cloud needs

Ability to own and

control customer

experience.

Seeking value and

great support

Technology advice

and enablement.

Like local

relationships

Strong market

proposition with

excellent service

management and

continual

improvement

Capability bridging

to fill in network

reach. Usage based

commercial models

Highly mobile

solutions, tech

education and

tailored solutions

with robust support

Reliable, simple

solutions that

support mobile

working. Want

immediate service

Multi-solution

supplier with ease of

doing business.

Price-led and need

to self-serve

Wh

o

Defi

nit

ion

N

eed

C

om

pe

titi

on

Multi Site

Orgs

Public

Sector

Service

Provider

Small

Connectors

SI &

BPO

Carrier &

DC

Commodity

Connector

Consumer

& SOHO

Reseller

What are we selling?

Iterating our national WAN

proposition with SDN/NFV capability

Developing our HSCN peering

capability

Call Management additional value

both direct and through the channel

Competitors

Why KCOM?

UK WAN market is large

WAN is critical to business proposition

delivery in key segments

Increased demand for agility and

flexibility to support cloud adoption

> Design and delivery approach

> Not tied to particular access network

> Market positioning – size and agility

> Core network investment – flexible by

design

46,000 Connections / 14000 sites to be

replaced by 2020

£42m per annum spend

NHS continuing digital enablement

of services

> Design and delivery approach

> Not tied to particular access network

> Sector references

> Framework positioning; RM1045 or

RM3825

Over 20B minutes per annum. 43% of call

routing in the cloud

Customers struggling to innovate due to

legacy environments and licence costs

Award winning solutions from KCOM

> Ease of implementation and change

> API availability

> Education programme for channel

partners

SI &

BPO

Multi Site

Orgs Public

Sector

Public

Sector

Multi Site

Orgs Service

Provider

Managed

Wide Area

Networks

Health and

Social Care

Network

Call

Management

Manage for value

Core assets and capabilities

Managed Wide Area Networks

Managed Wide Area Network

Cloud enabled Improving TCO

Software Defined A more agile network

> One single infrastructure

> Readily scalable

> Choice of carrier

> Simple deployment

Hybrid Enhanced IT resilience

> Adaptable policies and control

> Enhanced security

> Flexible bandwidth and access

> Improved use of IT resources

> Easy network orchestration

> Virtualised network services

> Integrated cloud consumption

> Optimised billing system

Advance our national WAN proposition with Software

Defined Network (SDN) / Network Function Virtualisation

(NFV) capability promoting growth across core target

segments

Current Next Future

Maximising life time customer value

Wires only

network

Cloud

connect

Professional

services

Managed

firewall

Colocation Call

management

Public cloud

Wren Kitchens overview

> Trusted partnership

> Fully resilient

> Journey to cloud

> Customer experience

“KCOM has just the right scale and capability

to support us through this growth period, but

perhaps more importantly balances this with

the flexibility and consultative approach we

need as we look to more than double the

size of our business.”

Craig Douglas, CIO, Wren Kitchens

Managed

Wide Area

Networks

Health and

Social Care

Network

Call

Management

Manage for value

Core assets and capabilities

Health and Social Care Network (HSCN)

Health and Social Care Network

Connectivity Improved access

WAN integration HSCN as a ‘bolt-on’

Future A more agile network

> Core connectivity

> Compliance and efficiency

> Wider WAN development

> Hybrid integration

> Cloud integration

> Software Defined as a Service

Complete HSCN accreditation and build our health proposition

Current Next Future

Maximising life time customer value

Managed

WAN

HSCN

Connection

Security Wi-Fi Public Cloud

DELT shared services overview

> HSCN Stage 1 compliance created engagement

> WAN replacement urgently required

> RM1045 procurement

> Public Cloud agenda in near future

Professional

services

Application

Performance

Management

Customer independently sought

feedback from public sector peers

regarding “the KCOM experience”.

Recommendations received

help to secure business

Managed

Wide Area

Networks

Health and

Social Care

Network

Call

Management

Manage for value

Core assets and capabilities

Call Management

Call management

for direct channel

Evolve with value added

voice services

Support and educate

> Maximise NNS direct opportunity

through cross-sell of a call

management solution

> Utilise existing KCOM capability

and repurpose for the channel

> Evolve portfolio

> PCI Compliant Voice

> Voice biometrics capabilities

> Omni-channel offering

> Maximise existing direct and indirect

channel

> Further evolution with SIP delivery in

line with NGV programme

> Education programmes to grow

existing relationships and

maximise value

> Develop further support offerings

to assist direct customers and

partners with service enablement

and changes

Call Management

To maximise direct relationships

Current Next Future

Maximising life time customer value

Internet

connect Professional

services

DSL Wi-FI Call

management

Elite Telecom and Nexus overview

> Trusted partnership

> Portal and self management tools

> National relationship extends in to East Yorkshire

> Direct and Indirect sales model supported

“We genuinely enjoy working with

KCOM, they go the extra mile in terms

of service, technical support and

providing guidance around contracts.”

Rob Sims, CEO at Nexus

Managed

Wide Area

Networks

Health and

Social Care

Network

Call

Management

Manage for value

Core assets and capabilities

National Network Services

Break

Enterprise Stephen Long

Customer

Contact

Services

Enterprise

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Customer

Contact

Services

Customer contact services

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Contact Centre as a Service continues to grow, as organisations

put more focus on the customer journey

Source: Cairneagle 2017

0

100

200

300

400

500

600

2012 2016 2020

62%

61%

29%

27%

29%

12%

11%

10% CAGR

+14.3%

333

568

59%

CAGR

+19.6%

163

Small (<50)

Medium (50-500)

Large (>500)

Size of UK CCaaS Market (£m)

Market drivers and trends:

Contact Centre as a Service

> Customer experience is increasingly vital to

customer loyalty

> Consumers expect seamless communication

with organisations – via traditional and digital

channels

> Several UK businesses are re-shoring their

contact centres to take closer control of the

customer experience and journey

> More businesses are migrating to more flexible

Opex-based cloud platforms

> Omni-channel capabilities, underpinned by

intelligent automation and self service, can

reduce contact centre costs and improve

customer experience

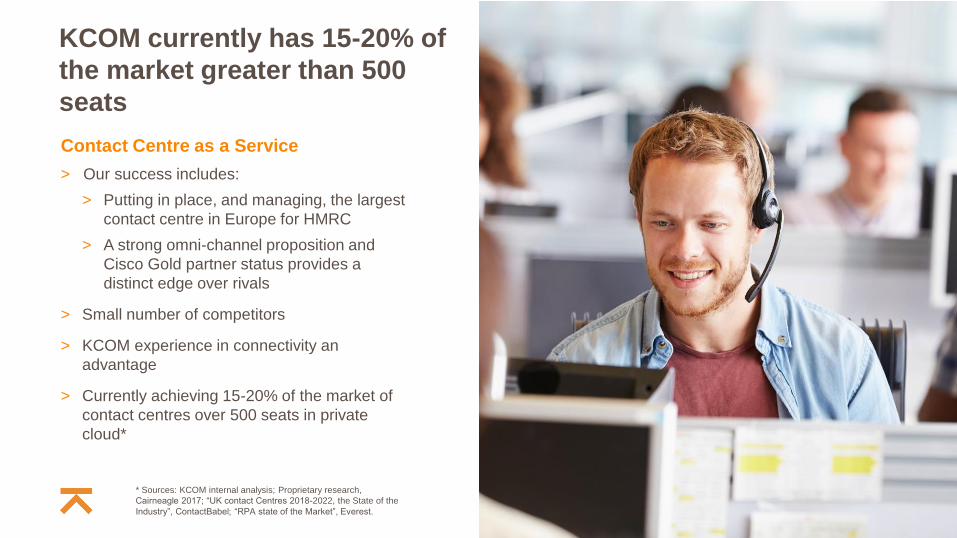

KCOM currently has 15-20% of

the market greater than 500

seats

Contact Centre as a Service

> Our success includes:

> Putting in place, and managing, the largest

contact centre in Europe for HMRC

> A strong omni-channel proposition and

Cisco Gold partner status provides a

distinct edge over rivals

> Small number of competitors

> KCOM experience in connectivity an

advantage

> Currently achieving 15-20% of the market of

contact centres over 500 seats in private

cloud*

* Sources: KCOM internal analysis; Proprietary research,

Cairneagle 2017; “UK contact Centres 2018-2022, the State of the

Industry”, ContactBabel; “RPA state of the Market”, Everest.

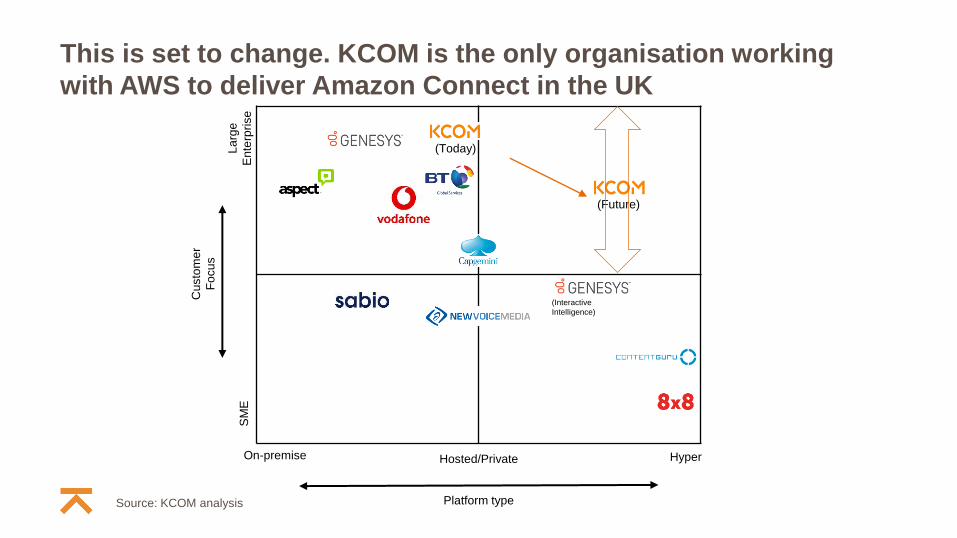

La

rge

En

terp

rise

S

ME

Custo

me

r

Fo

cu

s

Hosted/Private Hyper On-premise

(Today)

(Interactive

Intelligence)

Source: KCOM analysis Platform type

Large telcos dominate in on-prem and hosted cloud

Hyper cloud solutions aren’t yet viable for enterprises

This is set to change. KCOM is the only organisation working

with AWS to deliver Amazon Connect in the UK

La

rge

En

terp

rise

S

ME

Custo

me

r

Fo

cu

s

Hosted/Private Hyper On-premise

(Today)

(Interactive

Intelligence)

Source: KCOM analysis Platform type

(Future)

A hyper cloud contact capability could grow KCOM’s

addressable market by £475m – or 1,110%

£69m

Addressable by KCOM

Today - 2017

£105m

250 seats +

Lower seat count as customers demand less voice

£184m

Hyper cloud

Adding hyper cloud capability: workplaces 2.0 and AWS Connect

£544m

Digital service

Forecast market for robotic automation

1,110%

Market

Growth

vs. 2017

Customer

Contact

Services

Cloud propositions

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Continuous market volatility and rising customer expectations are framing the business context

New buyers are making new technology investments to meet rising customer expectations and drive operational flexibility

Business processes are being re-built to address continuous change

Firms are working with different kinds of suppliers to build new classes of systems with modern architectures

Composable software assets become the accelerators for the digital business

Five trends drive a fast-changing world. Organisations need to

be agile to meet the expectations of customers

Old New

Source: Forrester, 2017

Gartner and Forrester see accelerating hyper cloud spend, with

global Platforms growth >100% to 2020

September 2016 February

2017

This is replicated in the UK, with spend doubling to £2.2 billion in

2020. Whitehall is an early adopter

Source: TechMarketView, 2018.

* IaaS: Infrastructure as a Service

PaaS: Platform as a Service

CAGR: +28%

2017-2020

0

0.5

1

1.5

2

2.5

3

3.5

2016 2017 2018 2019 2020

UK Cloud Professional Services Market Growth

£1.9bn

£1.5bn

£2.8bn

£3.3bn

CAGR: +21%

£2.3bn

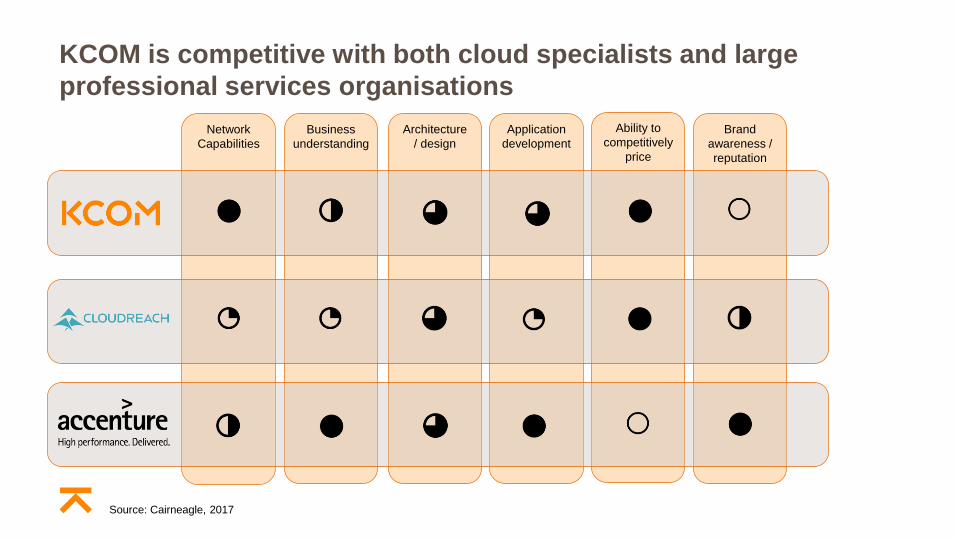

Network

Capabilities

Business

understanding

Architecture

/ design

Application

development

Ability to

competitively

price

Brand

awareness /

reputation

KCOM is competitive with both cloud specialists and large

professional services organisations

Source: Cairneagle, 2017

Customer

Contact

Services

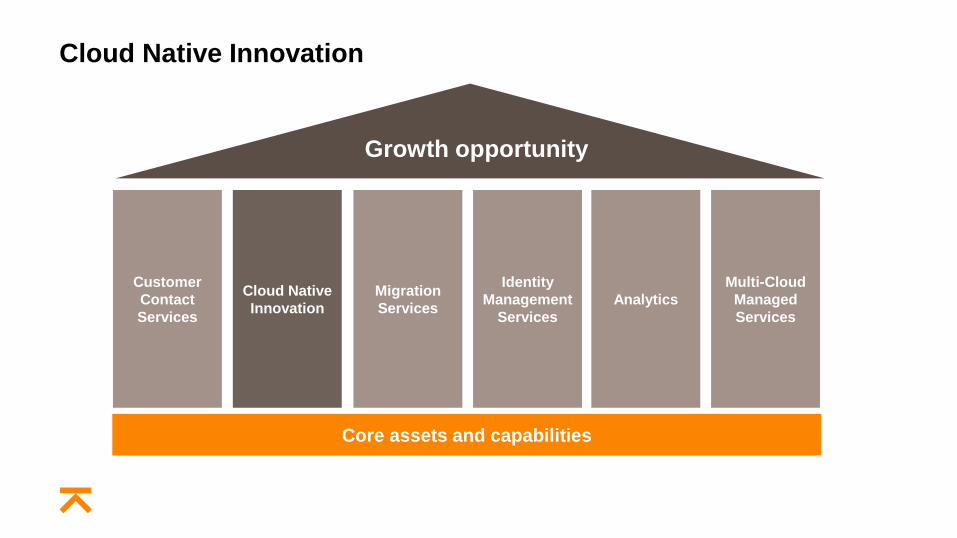

Cloud Native Innovation

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Our first cloud proposition, Cloud Native Innovation, uses advanced

features only available in hyper cloud

We help our customers re-imagine and create their future, using advanced cloud platform features

Source: www.computerworlduk.com

Strategy and Development

Microservices

Architecture

Cloud PaaS Services

TODAY

Our “Cloud Native” services develop applications (and the architecture behind them) using features only available in hyper cloud.

Often using server-less technology, this is faster, less costly, and far more flexible than traditional IT (including private cloud).

KCOM’s application knowledge and extensive cloud experience gives it a leading position in this market.

NEXT

> Bespoke “born-in-the-cloud”

applications and architecture

> Post-migration, re-architect

applications for greater

efficiency and features

FUTURE

> Templated solutions,

focused on industry

verticals, to drive scale

Customer

Contact

Services

Migration Services

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

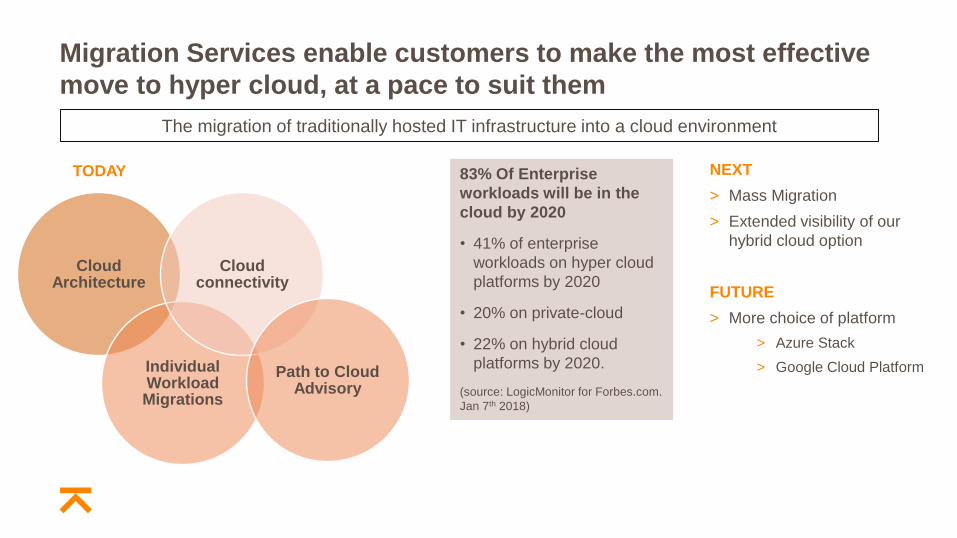

Migration Services enable customers to make the most effective

move to hyper cloud, at a pace to suit them

The migration of traditionally hosted IT infrastructure into a cloud environment

Cloud Architecture

Individual Workload Migrations

Cloud connectivity

Path to Cloud Advisory

TODAY 83% Of Enterprise

workloads will be in the

cloud by 2020

• 41% of enterprise

workloads on hyper cloud

platforms by 2020

• 20% on private-cloud

• 22% on hybrid cloud

platforms by 2020.

(source: LogicMonitor for Forbes.com.

Jan 7th 2018)

NEXT

> Mass Migration

> Extended visibility of our

hybrid cloud option

FUTURE

> More choice of platform

> Azure Stack

> Google Cloud Platform

Customer

Contact

Services

Identity Management Services

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Centralised sign on for multiple and distributed systems. Identities and access rights stored centrally

and securely.

TODAY

Voice Biometrics

(Nuance)

Identity & Access

Management

(Forgerock)

Advisory Skills

Managed Services

We deploy Forgerock and Nuance

software, customised to meet the

needs of our customers, on either

private or hyper cloud platforms.

Our suite of Identity Management Services has protected customers

since 2013. Now in hyper cloud

NEXT

> A continuation of our services

today

> GDPR and Open banking will

accelerate demand

FUTURE

> Enhance AWS tools for

Identity and Access

Management with our own IP,

to offer a cloud native choice

to AWS customers

> Introduce a similar

Azure-based offering

Customer

Contact

Services

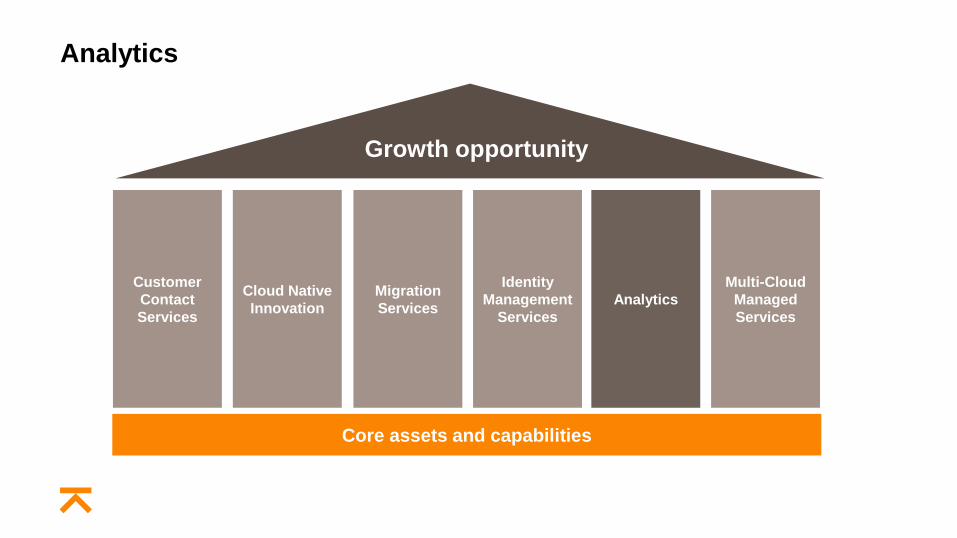

Analytics

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Building the hyper cloud platform architecture to turn complex data into business insights

Source: GrowthEnabler/Markets and Markets April 2017

Internet of Things UK market value c$4.7Bn

(3% of global IoT deals in 2016)

Source: CBI/Growth Enabler

Analytics and IoT are areas where our skills in handling huge

complexity comes into their own

> We create fast, agile and elastic compute

capabilities for the data scientists we

partner with, enabling them to analyse

vast quantities of complex data

Building the hyper cloud platform architecture to turn complex data into business insights

TODAY

Internet of Things projects

Large-scale Platform Analytics

Architecture

Analytics: our plans for the future include a toolkit to deliver scale,

and a Machine Learning offering

Early wins in media, retail, transport and

utilities

NEXT

> A Template Analytics Platform

toolkit will enable us to set up

standard tools in the cloud at

the press of a button

FUTURE

> Extend our offering to

incorporate Machine Learning

Customer

Contact

Services

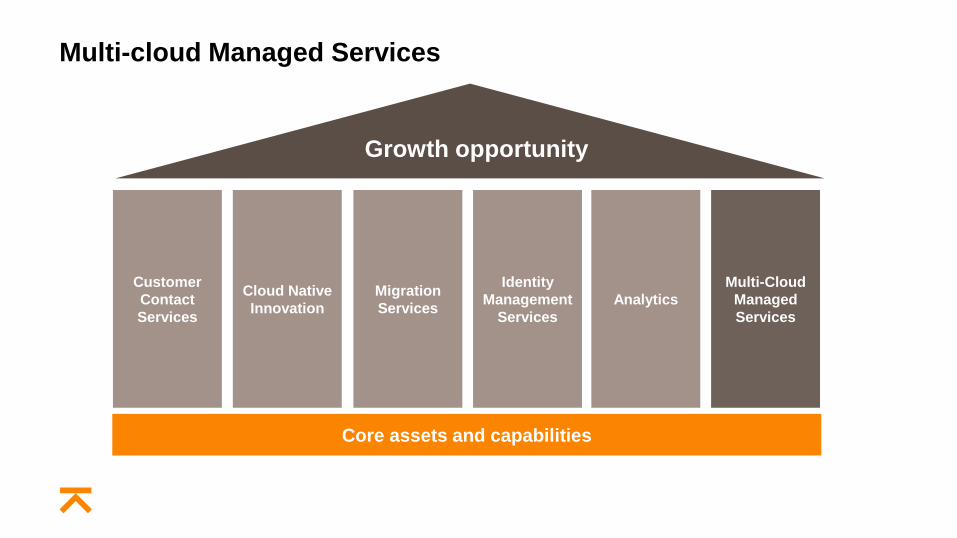

Multi-cloud Managed Services

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

We provide managed services for hyper cloud, multi-cloud, and hybrid environments

Sources: TechMarketView, 2016; Forrester, “Use Managed Cloud Services To Speed Transformation”, 2017

Break/fix support

24/7, 3 tier problem

management

ITIL certified,

ISO 20000 and 27000

Warranted end-to-end

TODAY

KCOM combines expertise in hyper cloud, private cloud, on-premise, and connectivity. Our service wrapper manages the new

complexities of legacy systems and multiple cloud environments, including AWS and Azure.

Multi-Cloud Managed Services is a proposition still in development,

but we already have the capabilities

NEXT

> Enhanced Services:

> Cost optimisation

> Technical Design Authority –

dedicated consultant resource

FUTURE

> Extend to Google and other cloud

environments

Customer

Contact

Services

Enterprise

Cloud Native

Innovation

Multi-Cloud

Managed

Services

Identity

Management

Services

Migration

Services

Growth opportunity

Analytics

Core assets and capabilities

Investment in core assets

and capabilities Sean Royce and Jane Aikman

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

Investment in network assets

Packaged

Capex

Contract term

Network

constrained

Physical

asset

Application based

Cloud

Subscription usage

Integrated

Opex

Old World

Network Service Provider New World

Experience Service Provider

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

Layer 4

Applications

Layer 3

Control

Layer 2

Transport

Layer 1

Buildings /

facilities

Layer 0

Passive layer

Original Network Layers

Intelligent Service Platforms

Data Networks

Voice Switching

DWDM Optical

Metro Optical and Access

Utilities and Facilities

Operation Support Systems

Buildings

Fibre Optic Cables

Duct and Chambers

14+1 exchange buildings in Hull and East Yorkshire. 90 leasehold, 1

Freehold, 15 Street Cabinets and 17 x 3rd Party Hosing Centres across UK

Fibre and copper access

Hull and East Yorkshire core and access network into 205k premises; CFH leased 2,200km

AC and DC Plant management, facilities contracts,

security, rates etc

Business Support Systems

Layer 4

Applications

Layer 3

Control

Layer 2

Transport

Layer 1

Buildings /

facilities

Layer 0

Passive layer

Billing CRM Orchestration

EM’s, IMS, NFV

Intelligent Service Platforms

Next Generation Voice (VOIP)

Service Creation Platform (IP Core)

Next Generation Transport (OTN)

Metro Optical and Access

Utilities and Facilities

Operation Support Systems

Buildings

Fibre Optic Cables

Duct and Chambers

Business Support Systems

Potential Fully Transformed KCOM Network Layers

Layer 2 (Transport) - Next Generation Transmission

KCOM’s own data centres

Access to public cloud

HEY FTTP network

Other KCOM NGT PoPsd

> Optical transport network - that rationalises 3 platforms into

1 and provides pipework for all applications

> SDN enabled - 5.6Tbs capable, and fully scalable

> Virtualized network operations - partitioning an

OTN-switched network into private network partitions provides

a dedicated set of network resources to each customer

> Flexible - customer driven connectivity and bandwidth

reservation, delivering faster service provisioning

> Dynamic infrastructure – makes network dynamic and

responsive making possible emerging services such as on-

demand/scheduled cloud interconnections

> Secure by design - ensures a high level of privacy and

security, designed with High Availability and individual QoS

Layer 3 (Control) - Service Creation Platform

London Bristol

Manchester

Hull

> New Cisco IP network - to manage and protect traffic and

customer data streams

> SDN enabled - Cisco 9912’s scalable to 12Tbs

> Replaces 3 x platforms - from ALU, Cisco and Ericsson

> Next Generation Core IP Switching Platform delivering:

> Advanced Layer 2 & 3 Switching and connectivity

> Core data services and enhanced WAN applications

> Enhanced Service protection

> Customer Authentication and Service Assurance

> Full management capability - to deliver NFV functionality

> QOS and policy control – enabled through Procera

Layer 3 (Control) - Next Generation Voice

Plan to transform the fixed line telephone network

M

D

F

O

D

F

System

X Conc

PON ONT

M

D

F

System

X Conc

O

D

F

VOIP PON ONT

O

D

F PON ONT

M

D

F

Gate

-way VOIP

Legacy

Hybrid

Gateway

Future

> By introducing a gateway that

emulates the existing voice

services, whether analogue or

digital, it allows the earlier

displacement of System X support

and power costs

> Otherwise we would have to migrate

all customers to the all optical future

model before the System X could be

displaced

> It becomes a cost effective interim

step in an uncertain environment

> Potential converged mobile

opportunity

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

Data Centre Strategy

> We currently have 10 data centre locations across the UK

> Consolidate to 3 data centres – over the course of a five year programme

> True geographic diversity and resilience - with sufficient capacity for customer/internal demand

> Power usage efficiency (PUE) – 50%-100% improvement

Reduced Unit Cost

and Operational

Simplification

Cloudification Opportunity

Network Services

• Transmission

• SCP

Cloud Services

• Virtualisation

• Compute

• Storage

Voice Services

• Workplaces

• ECT

• MetaSwitch

Bristol

Network Services

• Transmission

• SCP

Cloud Services

• Virtualisation

• Compute

• Storage

Voice Services

• Workplaces

• ECT

• MetaSwitch

Hull

Network Services

• Transmission

• SCP

Cloud Services

• Virtualisation

• Compute

• Storage

Voice Services

• Workplaces

• ECT

• MetaSwitch

London

Vodafone

BTW

Virgin

Media

AWS

MS Azure

TTB

Network Access

& Voice Interconnects

High Speed

Transmission and

Service Creation

Platform (SCP) Core

Low Latency Cloud

Interconnects

Key:

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

Service delivery - transformation

Network Managed Service

> Exit BTW managed service arrangement – from 1 April 2018

> Provision of low level design, build, monitoring and

maintenance functions by BTW, since 2009 to be in-sourced

with out-tasking explored where appropriate

> End-to-end accountability for service delivery – removal of

hand offs and areas of grey

> Significant capital and opex savings

> Benefit from scale operations within Hull and East Yorkshire

Customer Service Operations Centre

> Single ownership and accountability for level 1 and 2 technical support,

with all services catered for from one common operations centre

> Personalised, but standardised customer experience for all customers

> Single service desk and service Interface for any incident. 80% of

expertise in one place focused on the customer, with resolver groups

available for deeper technical issues

> Combined pool of technical resources across all technologies, giving

faster access to the right technical and support expertise in one place

> Best Practice (ITIL and Agile)

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

Project delivery - transformation

> Need to improve capability highlighted by the

issues with the complex software projects

> Strengthening of end-to-end project

governance including Project Assurance

Office – reach and independence

> Creation of a project management

professional community for coaching,

professional development and maintenance of

high standards

> Thorough assessment across entire function

to assess and upgrade capabilities and tools

> Upgrading our Agile capabilities to build a

sustainable offering and delivery technique

> Significant investment in skills and capabilities to

ensure this function is scalable, effective and able

to support the Enterprise strategy in particular

> This will be paid back by efficient and effective

delivery of our projects

71 current Enterprise projects in flight in addition to other capex projects across the business

Investment in core assets and capabilities

> Network transformation

> Data centre rationalisation

> Service delivery

> Project delivery

> Investment and cost reduction

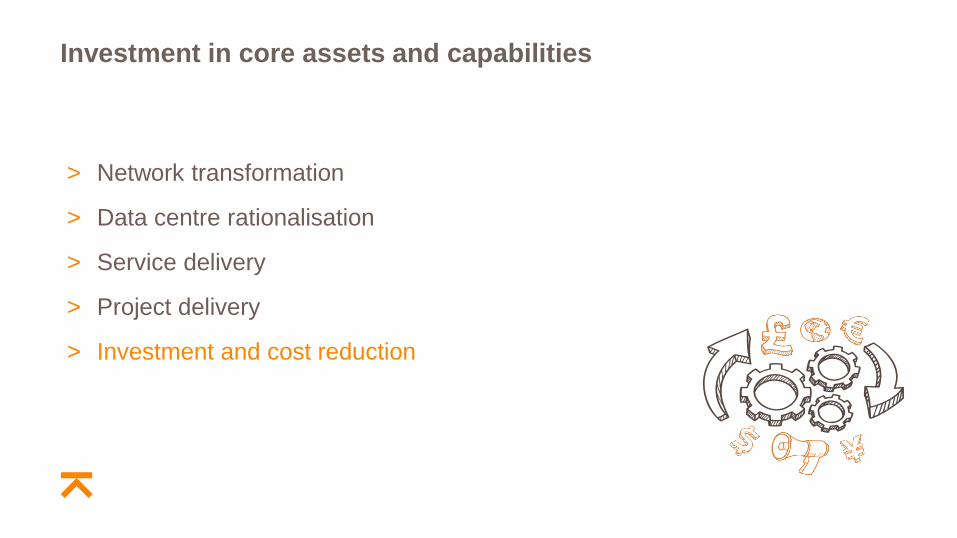

Capital investment driving opex and capex reductions

Significant cost reduction driven by investments in core assets and capabilities

Capex Opex and capex reductions

-

10

20

30

40

50

60

FY18 FY19 FY20 FY21 FY22

£m

BAU Fibre Deployment

Network Transformation Other Transformational Projects

-

1

2

3

4

5

6

7

8

9

FY18 FY19 FY20 FY21 FY22

£m

HEY Capex HEY Opex Enterprise Opex NNS Opex

Summary Jane Aikman

Agenda

Business overview

Hull and East Yorkshire

National Network Services

BREAK

Enterprise

Investment in core assets and capabilities

Summary

Wine and canapes

Thank you