48

Trusted commercial intelligencewww.woodmac.com

Carbon’s impact on crude oil -stormy seas for petrochemicals?

November 2016

Trusted commercial intelligencewww.woodmac.com

3

Agenda

1. Energy, oil and carbon - Is the crude oil juggernaut turning?

2. Petrochemicals – Addressing the uncertainties

Trusted commercial intelligencewww.woodmac.com

4

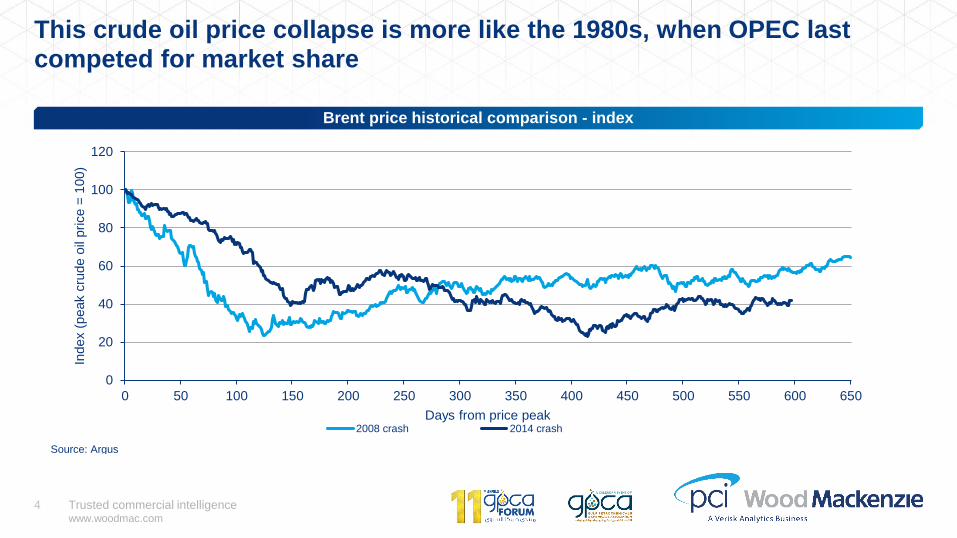

This crude oil price collapse is more like the 1980s, when OPEC last competed for market share

Brent price historical comparison - index

0

20

40

60

80

100

120

0 50 100 150 200 250 300 350 400 450 500 550 600 650

Index (

peak c

rude o

il price =

100)

Days from price peak2008 crash 2014 crash

Source: Argus

Trusted commercial intelligencewww.woodmac.com

5

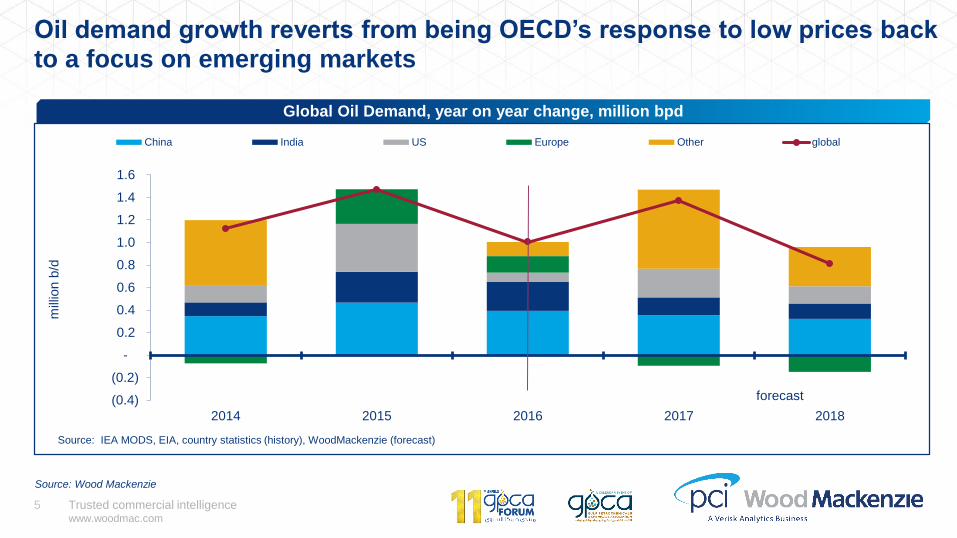

Oil demand growth reverts from being OECD’s response to low prices back to a focus on emerging markets

Global Oil Demand, year on year change, million bpd

Source: Wood Mackenzie

(0.4)

(0.2)

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2014 2015 2016 2017 2018

mill

ion b

/d

China India US Europe Other global

forecast

Source: IEA MODS, EIA, country statistics (history), WoodMackenzie (forecast)

Trusted commercial intelligencewww.woodmac.com

6

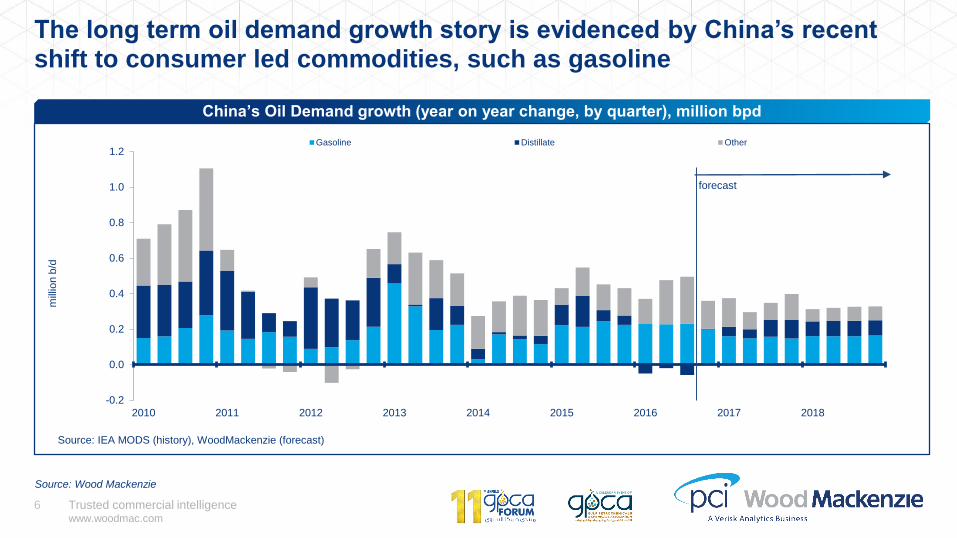

The long term oil demand growth story is evidenced by China’s recent shift to consumer led commodities, such as gasoline

China’s Oil Demand growth (year on year change, by quarter), million bpd

Source: Wood Mackenzie

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

2010 2011 2012 2013 2014 2015 2016 2017 2018

mill

ion b

/d

Gasoline Distillate Other

forecast

Source: IEA MODS (history), WoodMackenzie (forecast)

Trusted commercial intelligencewww.woodmac.com

7

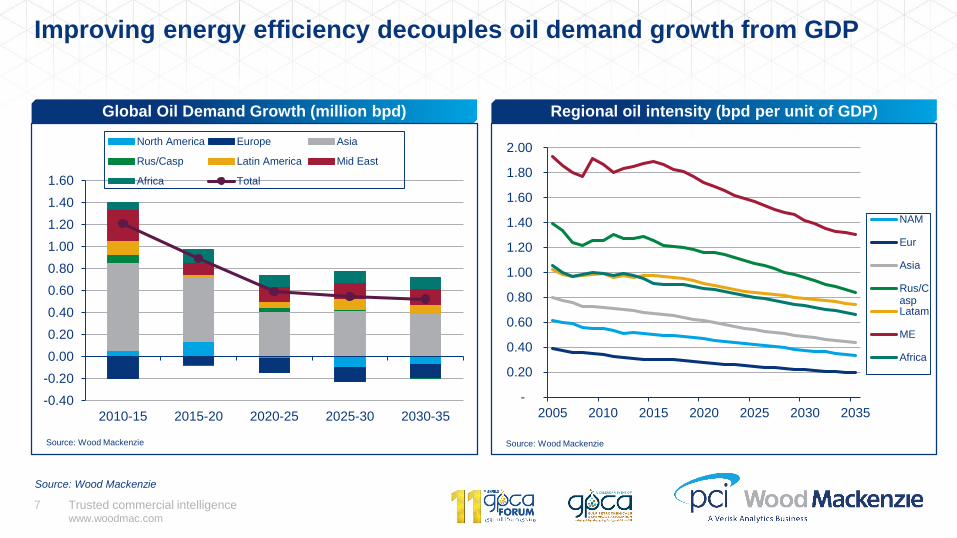

Improving energy efficiency decouples oil demand growth from GDP

Source: Wood Mackenzie

Global Oil Demand Growth (million bpd) Regional oil intensity (bpd per unit of GDP)

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2010-15 2015-20 2020-25 2025-30 2030-35

North America Europe Asia

Rus/Casp Latin America Mid East

Africa Total

Source: Wood Mackenzie

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

2005 2010 2015 2020 2025 2030 2035

NAM

Eur

Asia

Rus/CaspLatam

ME

Africa

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

8

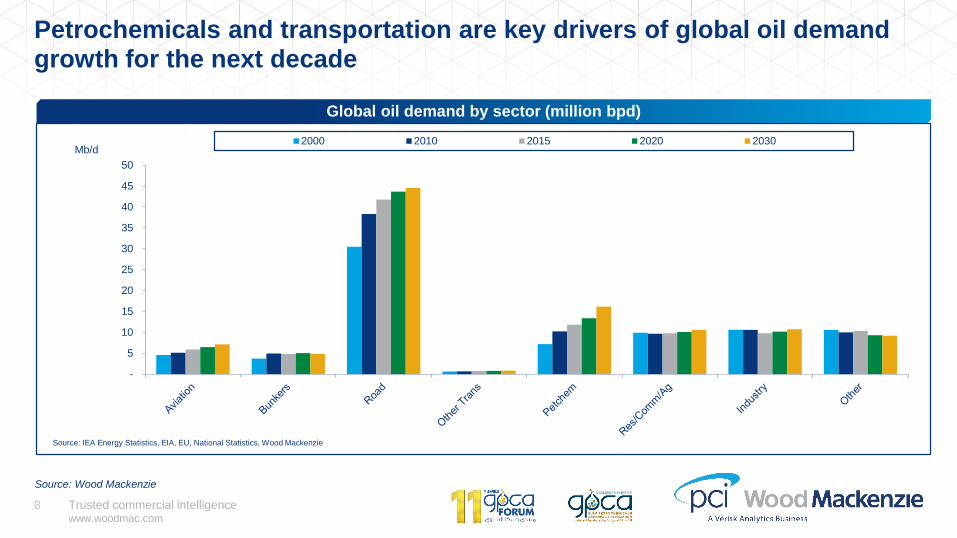

Petrochemicals and transportation are key drivers of global oil demand growth for the next decade

Global oil demand by sector (million bpd)

Source: Wood Mackenzie

-

5

10

15

20

25

30

35

40

45

50

Mb/d2000 2010 2015 2020 2030

Source: IEA Energy Statistics, EIA, EU, National Statistics, Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

9

Upstream capex has fallen significantly since mid 2014, which is leading to a re-balancing of the oil market

Global Upstream Capex Outlook Global change in supply/demand (million bpd)

Source: Wood Mackenzie

0.0 1.0 2.0 3.0 4.0

Supply

Demand

2015

2016

2017

2018

0

100

200

300

400

500

600

700

800

2014 2015 2016 2017 2018 2019 2020

Cap

ex

in

ve

stm

en

t (U

S$ b

illi

on

s)

E&A Spend

US L48

Technical

Probable development

Under development

Onstream

Pre-oil price collapse outlook

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

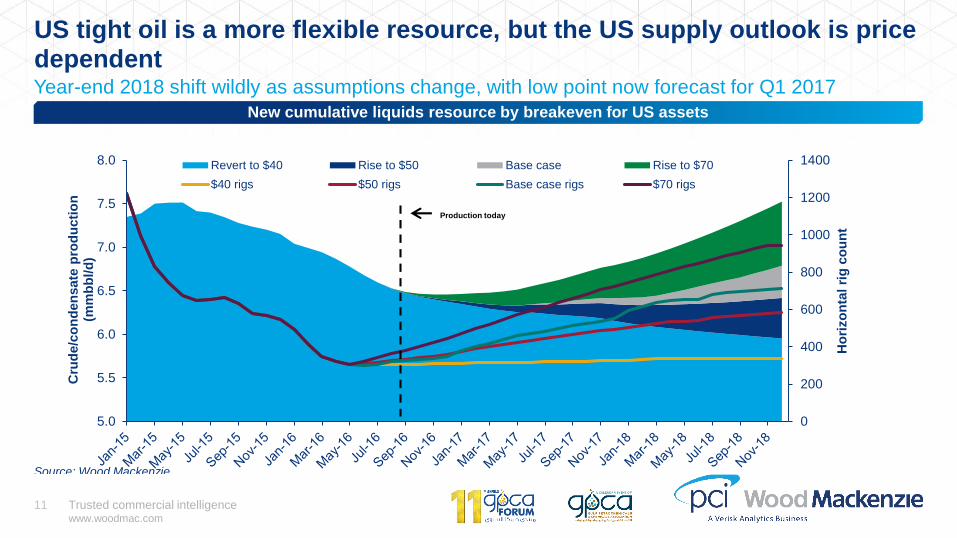

11

US tight oil is a more flexible resource, but the US supply outlook is price dependentYear-end 2018 shift wildly as assumptions change, with low point now forecast for Q1 2017

0

200

400

600

800

1000

1200

1400

5.0

5.5

6.0

6.5

7.0

7.5

8.0

Ho

rizo

nta

l ri

g c

ou

nt

Cru

de/c

on

den

sate

pro

du

cti

on

(m

mb

bl/

d)

Revert to $40 Rise to $50 Base case Rise to $70

$40 rigs $50 rigs Base case rigs $70 rigs

Source: Wood Mackenzie

New cumulative liquids resource by breakeven for US assets

Production today

Trusted commercial intelligencewww.woodmac.com

12

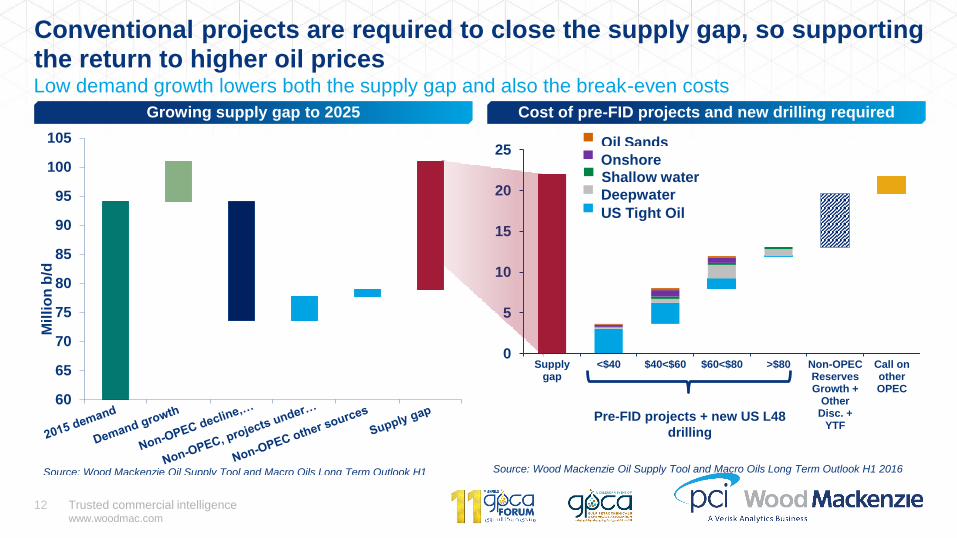

0

5

10

15

20

25

Supplygap

<$40 $40<$60 $60<$80 >$80 Non-OPECReservesGrowth +

OtherDisc. +

YTF

Call onotherOPEC

Oil Sands

Onshore

Shallow water

Deepwater

US Tight Oil

Source: Wood Mackenzie Oil Supply Tool and Macro Oils Long Term Outlook H1 2016

Pre-FID projects + new US L48

drilling

Growing supply gap to 2025 Cost of pre-FID projects and new drilling required

Conventional projects are required to close the supply gap, so supporting the return to higher oil prices

60

65

70

75

80

85

90

95

100

105

Mil

lio

n b

/d

Source: Wood Mackenzie Oil Supply Tool and Macro Oils Long Term Outlook H1

2016

Low demand growth lowers both the supply gap and also the break-even costs

Trusted commercial intelligencewww.woodmac.com

13

0

50

100

150

200

250

300

350

400

200

5

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

202

5

mm

tpa

H1 2016 H1 2015

0

50

100

150

200

250

300

350

400

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

202

5

mm

tpa

Operational New Other

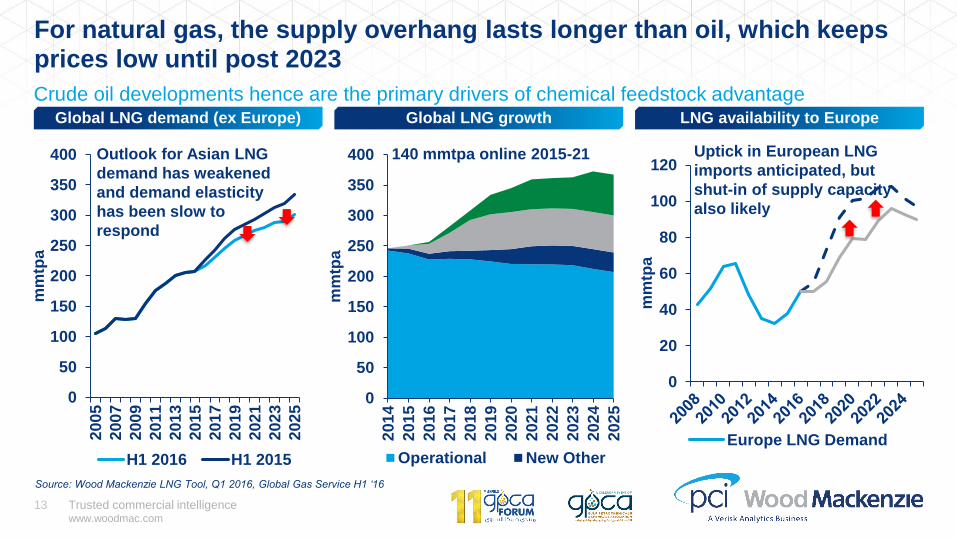

For natural gas, the supply overhang lasts longer than oil, which keeps prices low until post 2023

Source: Wood Mackenzie LNG Tool, Q1 2016, Global Gas Service H1 ‘16

0

20

40

60

80

100

120

mm

tpa

Europe LNG Demand

Outlook for Asian LNG

demand has weakened

and demand elasticity

has been slow to

respond

140 mmtpa online 2015-21 Uptick in European LNG

imports anticipated, but

shut-in of supply capacity

also likely

Global LNG growthGlobal LNG demand (ex Europe) LNG availability to Europe

Crude oil developments hence are the primary drivers of chemical feedstock advantage

Trusted commercial intelligencewww.woodmac.com

14

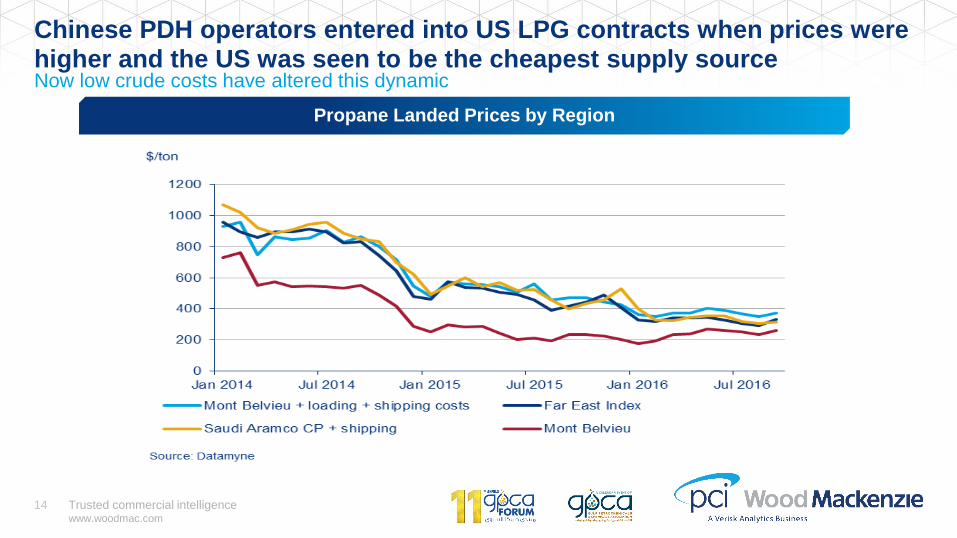

Chinese PDH operators entered into US LPG contracts when prices were higher and the US was seen to be the cheapest supply sourceNow low crude costs have altered this dynamic

Propane Landed Prices by Region

Trusted commercial intelligencewww.woodmac.com

15

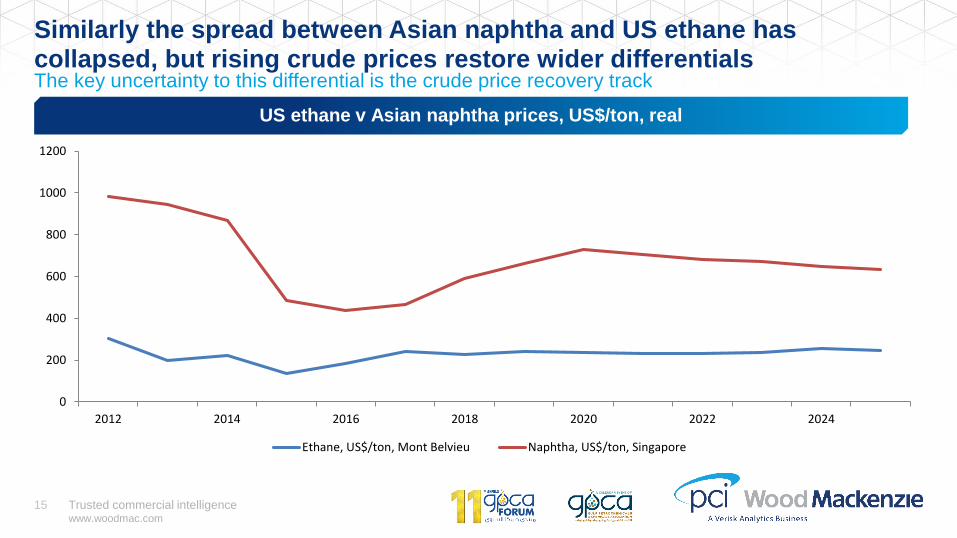

Similarly the spread between Asian naphtha and US ethane has collapsed, but rising crude prices restore wider differentialsThe key uncertainty to this differential is the crude price recovery track

US ethane v Asian naphtha prices, US$/ton, real

0

200

400

600

800

1000

1200

2012 2014 2016 2018 2020 2022 2024

Ethane, US$/ton, Mont Belvieu Naphtha, US$/ton, Singapore

Trusted commercial intelligencewww.woodmac.com

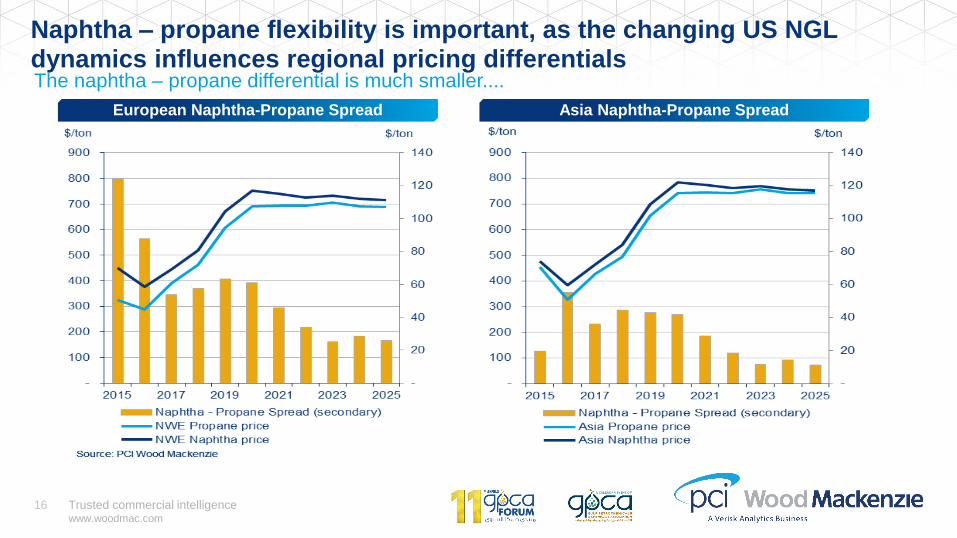

16

Naphtha – propane flexibility is important, as the changing US NGL dynamics influences regional pricing differentials

European Naphtha-Propane Spread Asia Naphtha-Propane Spread

The naphtha – propane differential is much smaller....

Trusted commercial intelligencewww.woodmac.com

17

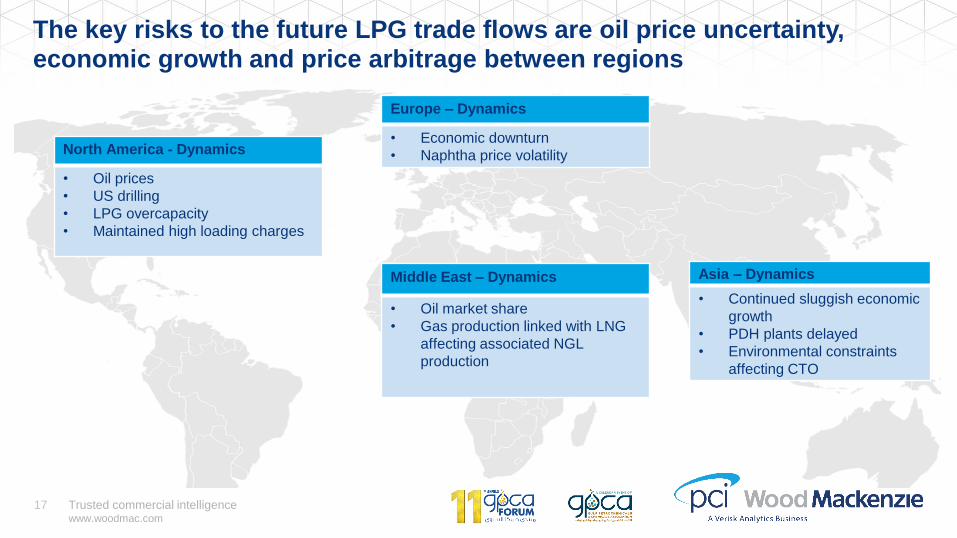

The key risks to the future LPG trade flows are oil price uncertainty, economic growth and price arbitrage between regions

North America - Dynamics

• Oil prices

• US drilling

• LPG overcapacity

• Maintained high loading charges

Europe – Dynamics

• Economic downturn

• Naphtha price volatility

Middle East – Dynamics

• Oil market share

• Gas production linked with LNG

affecting associated NGL

production

Asia – Dynamics

• Continued sluggish economic

growth

• PDH plants delayed

• Environmental constraints

affecting CTO

Trusted commercial intelligencewww.woodmac.com

18

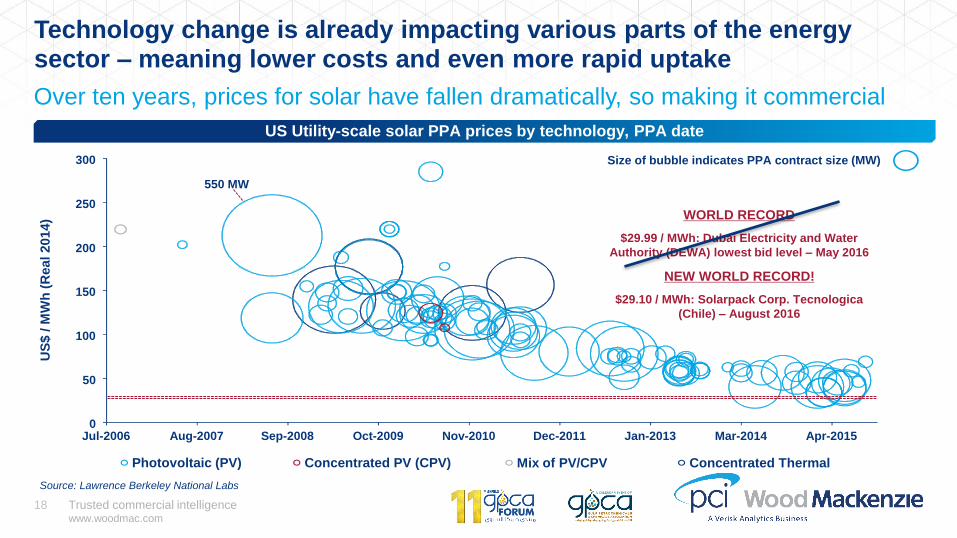

Technology change is already impacting various parts of the energy sector – meaning lower costs and even more rapid uptake

Over ten years, prices for solar have fallen dramatically, so making it commercial

US Utility-scale solar PPA prices by technology, PPA date

Source: Lawrence Berkeley National Labs

Size of bubble indicates PPA contract size (MW)

US

$ / M

Wh

(R

eal 2014)

Photovoltaic (PV) Concentrated PV (CPV) Mix of PV/CPV Concentrated Thermal

550 MW

0

50

100

150

200

250

300

Jul-2006 Aug-2007 Sep-2008 Oct-2009 Nov-2010 Dec-2011 Jan-2013 Mar-2014 Apr-2015

WORLD RECORD

$29.99 / MWh: Dubai Electricity and Water

Authority (DEWA) lowest bid level – May 2016

NEW WORLD RECORD!

$29.10 / MWh: Solarpack Corp. Tecnologica

(Chile) – August 2016

Trusted commercial intelligencewww.woodmac.com

19

0

5

10

15

20

2010 2015 2020 2025 2030 2035 2040 2045 2050

mb

/d

Africa China IndiaOther Asia Pacific Europe Middle EastNorth America Russia & Caspian South America

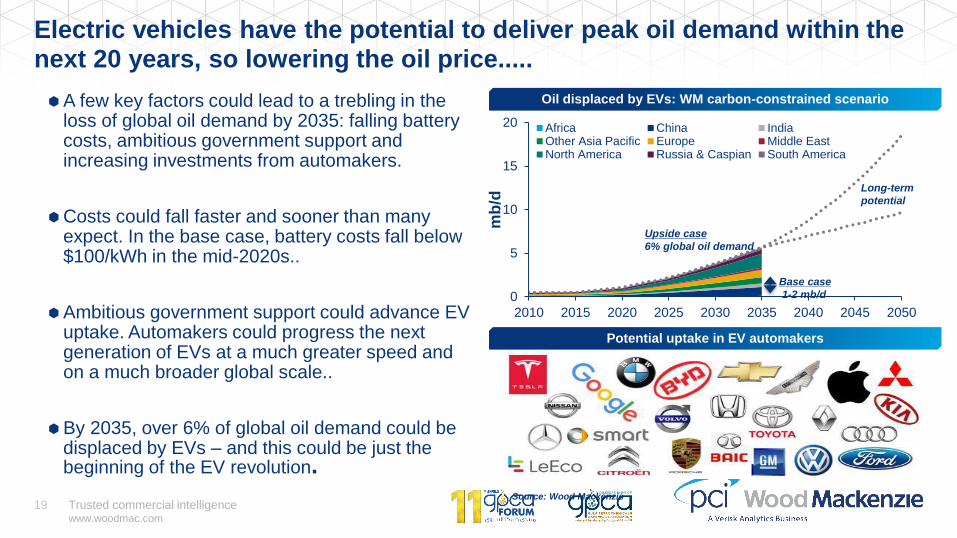

Electric vehicles have the potential to deliver peak oil demand within the next 20 years, so lowering the oil price.....

Oil displaced by EVs: WM carbon-constrained scenario

Source: Wood Mackenzie

Potential uptake in EV automakers

A few key factors could lead to a trebling in the loss of global oil demand by 2035: falling battery costs, ambitious government support and increasing investments from automakers.

Costs could fall faster and sooner than many expect. In the base case, battery costs fall below $100/kWh in the mid-2020s..

Ambitious government support could advance EV uptake. Automakers could progress the next generation of EVs at a much greater speed and on a much broader global scale..

By 2035, over 6% of global oil demand could be displaced by EVs – and this could be just the beginning of the EV revolution.

Base case

1-2 mb/d

Upside case

6% global oil demand

Long-term

potential

Trusted commercial intelligencewww.woodmac.com

20

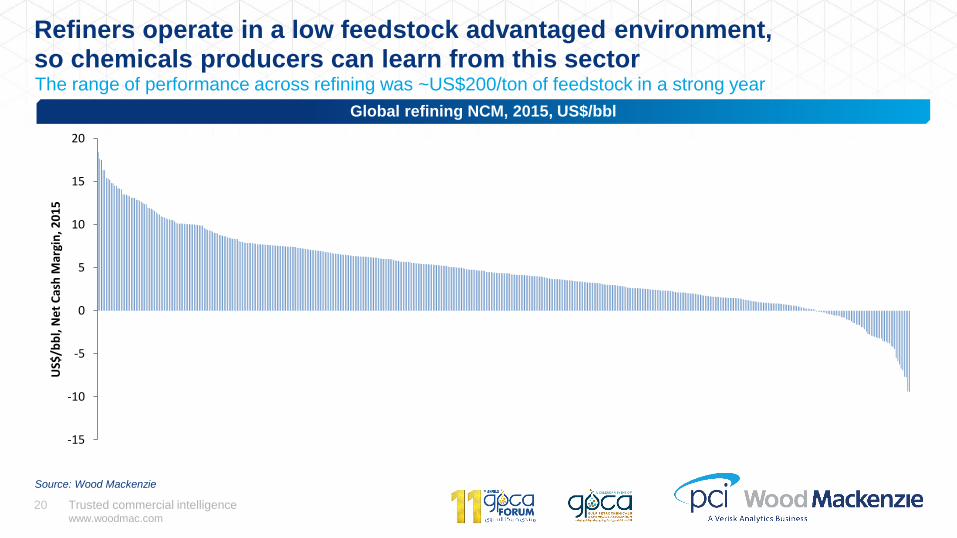

Refiners operate in a low feedstock advantaged environment, so chemicals producers can learn from this sector

Global refining NCM, 2015, US$/bbl

Source: Wood Mackenzie

-15

-10

-5

0

5

10

15

20

US$

/bb

l, N

et

Cas

h M

argi

n, 2

01

5

The range of performance across refining was ~US$200/ton of feedstock in a strong year

Trusted commercial intelligencewww.woodmac.com

21 Trusted commercial intelligencewww.woodmac.com

21

Success in a low oil world is driven by “efficiency” and “optionality”

Efficient operations

» Reliable operations essential, delivering high asset availability

» Low cost operations

» Maintenance is to be planned and effective

» Projects to be delivered “on time” and “on budget” and start up smoothly

Capture Value

» Asset flexibility to be maximised without undue capital cost

» Process advantaged/opportunity feedstocks through global procurement

» Global trading capabilities and effective logistics network are key to capture opportunities in product

markets

Reduced feedstock advantage requires efficient activities that capture value

Trusted commercial intelligencewww.woodmac.com

22

The crude oil juggernaut appears to be turning, but

slowly......

The significance of feedstock advantage will return to the

petrochemicals sector as oil price recovers

The return to a feedstock advantage is not guaranteed in

either the short term (weak demand growth) or the long

term (demand side technology revolution)

Refining has lived an environment of weak feedstock

advantage for many years and those who have adapted

have become successful.

The key success criteria are efficiency and optionality so:

Do things well

Capture value

Key

takeaways

Conclusions

Trusted commercial intelligencewww.woodmac.com

23

Agenda

1. Energy, oil and carbon - Is the crude oil juggernaut turning?

2. Petrochemicals – Addressing the uncertainties

Trusted commercial intelligencewww.woodmac.com

24

Agenda

The current competitive arena for olefins and aromatics

» Who are the winners and losers in an evolutionary world?

Amid economic fragility can chemical growth continue?

Impact on trade flows as new capacity is commissioned

» Focus on China imports

» Impact on key exporting regions

Conclusions

Trusted commercial intelligencewww.woodmac.com

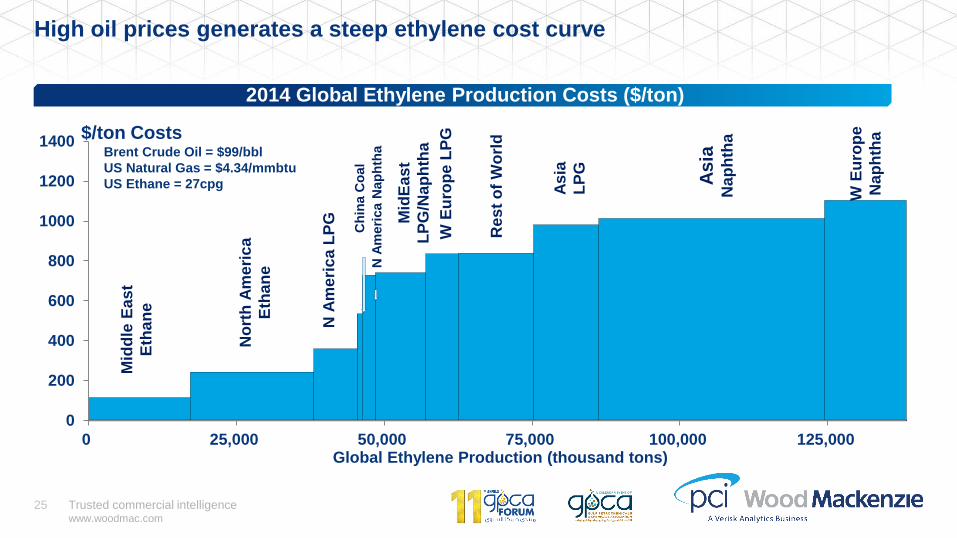

25

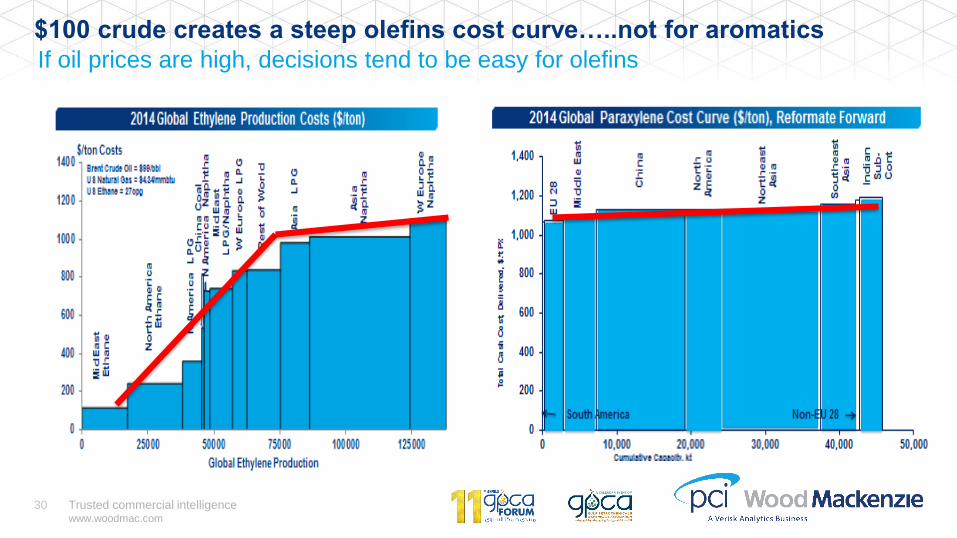

High oil prices generates a steep ethylene cost curve

2014 Global Ethylene Production Costs ($/ton)

0

200

400

600

800

1000

1200

1400

0 25,000 50,000 75,000 100,000 125,000Global Ethylene Production (thousand tons)

$/ton CostsBrent Crude Oil = $99/bbl

US Natural Gas = $4.34/mmbtu

US Ethane = 27cpg

Mid

dle

Ea

st

Eth

an

e

No

rth

Am

eri

ca

Eth

an

e

Mid

Ea

st

LP

G/N

ap

hth

a

Res

t o

fW

orl

d

As

ia

Nap

hth

a

WE

uro

pe

Nap

hth

a

N A

me

ric

a L

PG

Ch

ina C

oal

WE

uro

pe L

PG

As

ia

LP

G

N A

me

rica N

ap

hth

a

Trusted commercial intelligencewww.woodmac.com

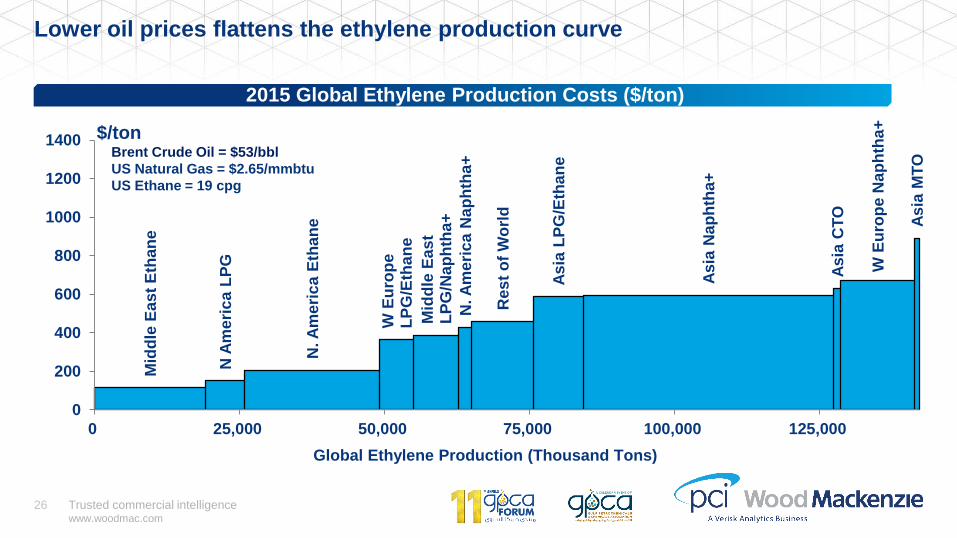

26

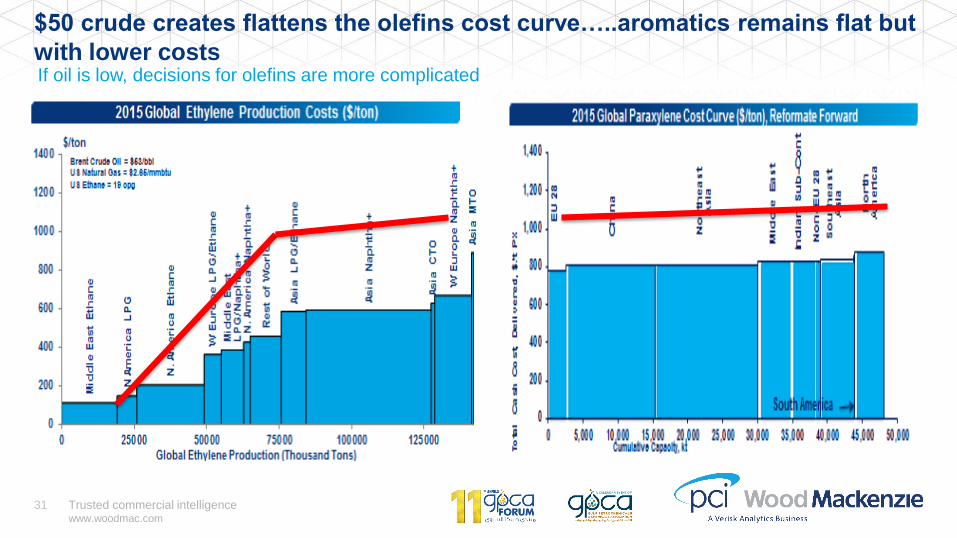

Lower oil prices flattens the ethylene production curve

2015 Global Ethylene Production Costs ($/ton)

Mid

dle

Ea

st

Eth

an

e

N A

me

ric

a L

PG

N. A

me

ric

a E

tha

ne

W E

uro

pe

L

PG

/Eth

an

e

Mid

dle

Ea

st

LP

G/N

ap

hth

a+

N. A

me

ric

a N

ap

hth

a+

Res

t o

f W

orl

d

As

ia L

PG

/Eth

an

e

As

ia N

ap

hth

a+

As

ia C

TO

W E

uro

pe N

ap

hth

a+

As

ia M

TO

0

200

400

600

800

1000

1200

1400

0 25,000 50,000 75,000 100,000 125,000

$/tonBrent Crude Oil = $53/bbl

US Natural Gas = $2.65/mmbtu

US Ethane = 19 cpg

Global Ethylene Production (Thousand Tons)

Trusted commercial intelligencewww.woodmac.com

27

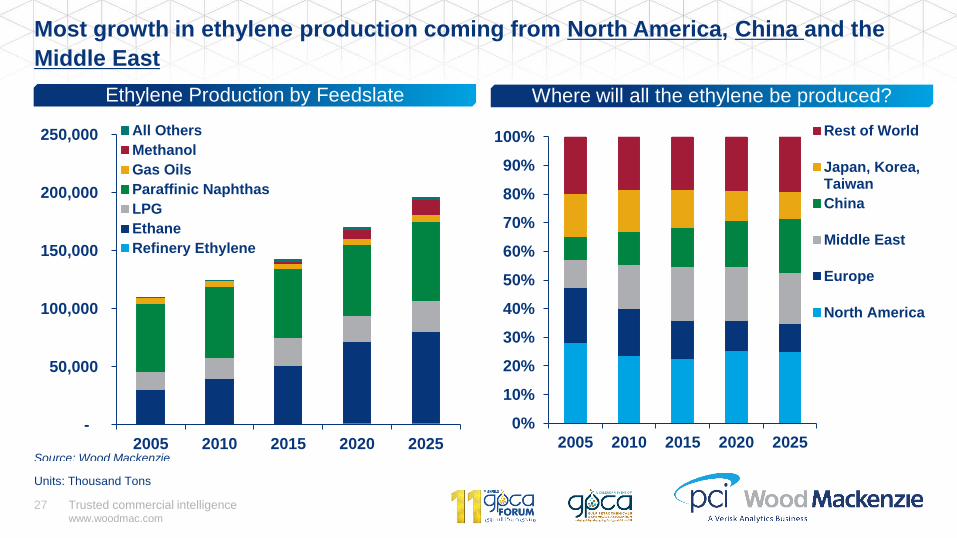

Most growth in ethylene production coming from North America, China and the

Middle East

Ethylene Production by Feedslate

-

50,000

100,000

150,000

200,000

250,000

2005 2010 2015 2020 2025

All Others

Methanol

Gas Oils

Paraffinic Naphthas

LPG

Ethane

Refinery Ethylene

Source: Wood Mackenzie

Where will all the ethylene be produced?

Units: Thousand Tons

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2010 2015 2020 2025

Rest of World

Japan, Korea,Taiwan

China

Middle East

Europe

North America

Trusted commercial intelligencewww.woodmac.com

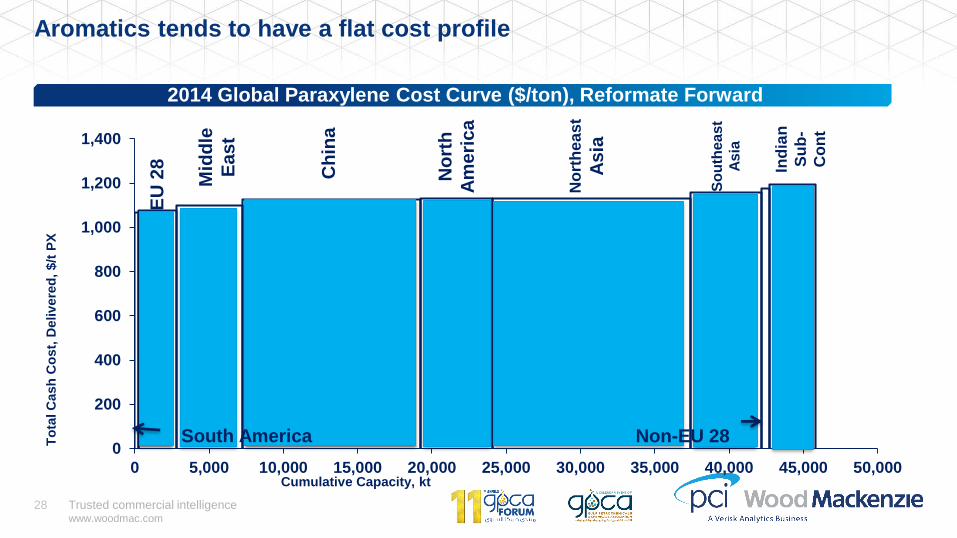

28

Aromatics tends to have a flat cost profile

2014 Global Paraxylene Cost Curve ($/ton), Reformate Forward

0

200

400

600

800

1,000

1,200

1,400

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

To

tal C

ash

Co

st,

Deliv

ere

d,

$/t

PX

Cumulative Capacity, kt

Mid

dle

East

No

rth

ea

st

As

ia

Ch

ina

Ind

ian

Su

b-

Co

nt

So

uth

ea

st

As

ia

No

rth

Am

eri

ca

EU

28

South America Non-EU 28

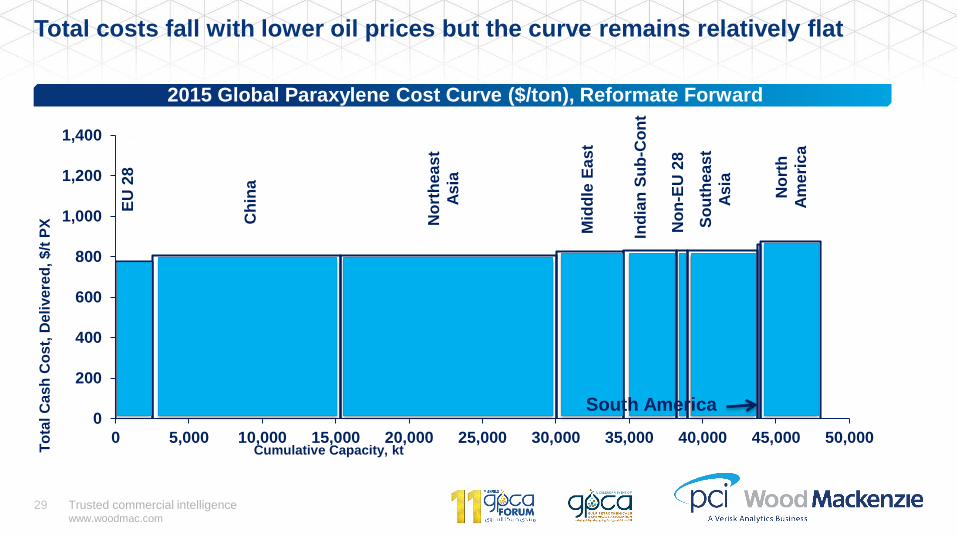

Trusted commercial intelligencewww.woodmac.com

29

0

200

400

600

800

1,000

1,200

1,400

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

To

tal C

ash

Co

st,

De

live

red

, $

/t P

X

Cumulative Capacity, kt

Mid

dle

Ea

st

No

rth

ea

st

As

ia

Ch

ina

Ind

ian

Su

b-C

on

t

No

n-E

U 2

8

So

uth

ea

st

As

ia

No

rth

Am

eri

ca

South America

Total costs fall with lower oil prices but the curve remains relatively flat

2015 Global Paraxylene Cost Curve ($/ton), Reformate Forward

EU

28

Trusted commercial intelligencewww.woodmac.com

30

$100 crude creates a steep olefins cost curve…..not for aromatics

If oil prices are high, decisions tend to be easy for olefins

Trusted commercial intelligencewww.woodmac.com

31

$50 crude creates flattens the olefins cost curve…..aromatics remains flat but

with lower costsIf oil is low, decisions for olefins are more complicated

Trusted commercial intelligencewww.woodmac.com

32

Agenda

The current competitive arena for olefins and aromatics

» Who are the winners and losers in an evolutionary world?

Amid economic fragility can chemical growth continue?

Impact on trade flows as new capacity is commissioned

» Focus on China imports

» Impact on key exporting regions

Conclusions

Trusted commercial intelligencewww.woodmac.com

33

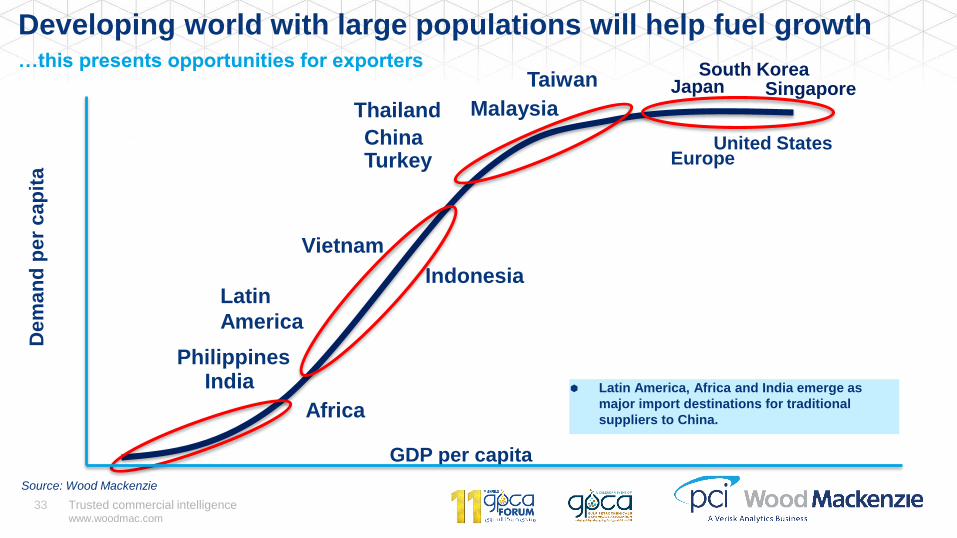

Developing world with large populations will help fuel growth…this presents opportunities for exporters

Dem

an

d p

er

ca

pit

a

Thailand

PhilippinesIndia

Vietnam

United StatesChinaEurope

SingaporeJapan

Indonesia

Malaysia

South KoreaTaiwan

Turkey

Africa

Latin

America

Latin America, Africa and India emerge as

major import destinations for traditional

suppliers to China.

Source: Wood Mackenzie

GDP per capita

Trusted commercial intelligencewww.woodmac.com

34

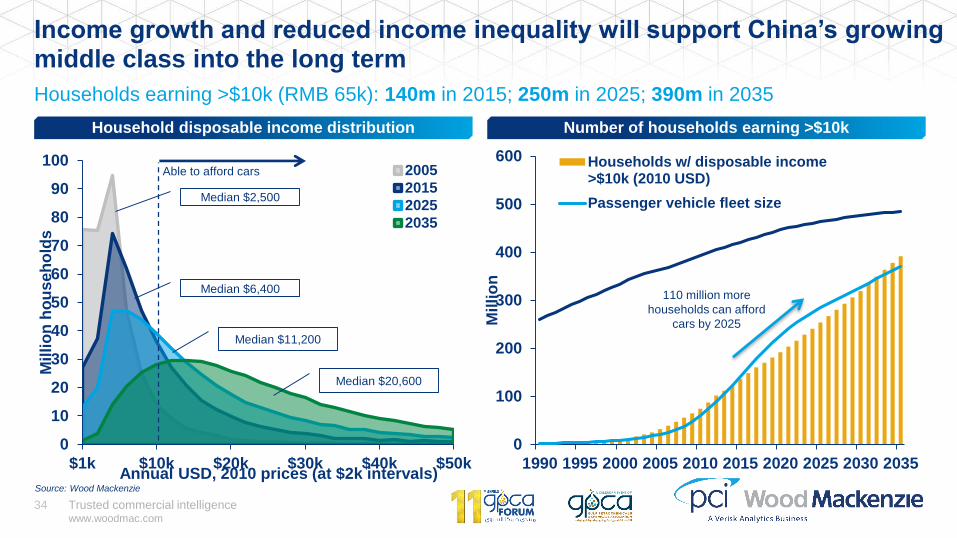

0

100

200

300

400

500

600

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Mil

lio

n

Households w/ disposable income>$10k (2010 USD)

Passenger vehicle fleet size

0

10

20

30

40

50

60

70

80

90

100

$1k $10k $20k $30k $40k $50k

Mil

lio

n h

ou

se

ho

lds

Annual USD, 2010 prices (at $2k intervals)

2005

2015

2025

2035

Income growth and reduced income inequality will support China’s growing middle class into the long term

Households earning >$10k (RMB 65k): 140m in 2015; 250m in 2025; 390m in 2035

Number of households earning >$10kHousehold disposable income distribution

Able to afford cars

110 million more

households can afford

cars by 2025

Median $2,500

Median $6,400

Median $11,200

Median $20,600

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

35

Longer term, China’s urban residential completions will be determined by its

demographic outlook and standard of living

China’s typical first-time buyers, 20-34 years old Annual increase in urban population

150

200

250

300

350

400

(mn

pe

rso

ns)

Source: Wood Mackenzie

-

5

10

15

20

25

30

2001 2006 2011 2016 2021 2026 2031

(mn

pe

rso

ns)

Source: Wood Mackenzie

This age cohort forms the bulk of first-time buyers – new graduates

moving to cities and couples getting married. It reached a second

peak of 335 million in 2015 and is projected to decline by 77 million in

the next 10 years, and another 24 million between 2025 to 2035

China’s rapid urbanisation fuelled a property

boom: 206m people moved into urban areas

between 2006-15. However, we expect

urbanisation to slow. We forecast urban

population to increase by 162m between 2016-

2025 and 95m between 2026-35

China implemented the one-

child policy in 1980

Property demand faces a double whammy from ageing population and slowing urbanisation

Trusted commercial intelligencewww.woodmac.com

36

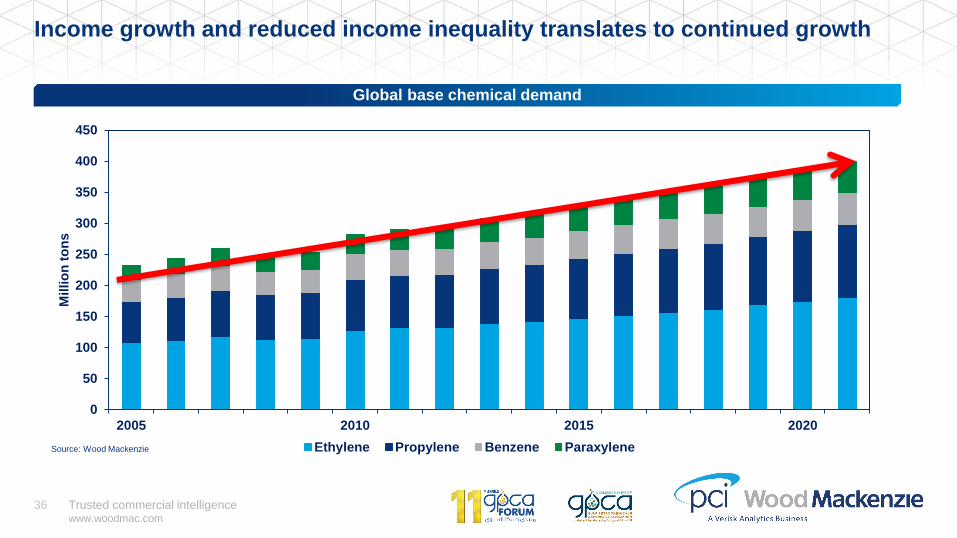

Income growth and reduced income inequality translates to continued growth

Global base chemical demand

0

50

100

150

200

250

300

350

400

450

2005 2010 2015 2020

Millio

n t

on

s

Ethylene Propylene Benzene ParaxyleneSource: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

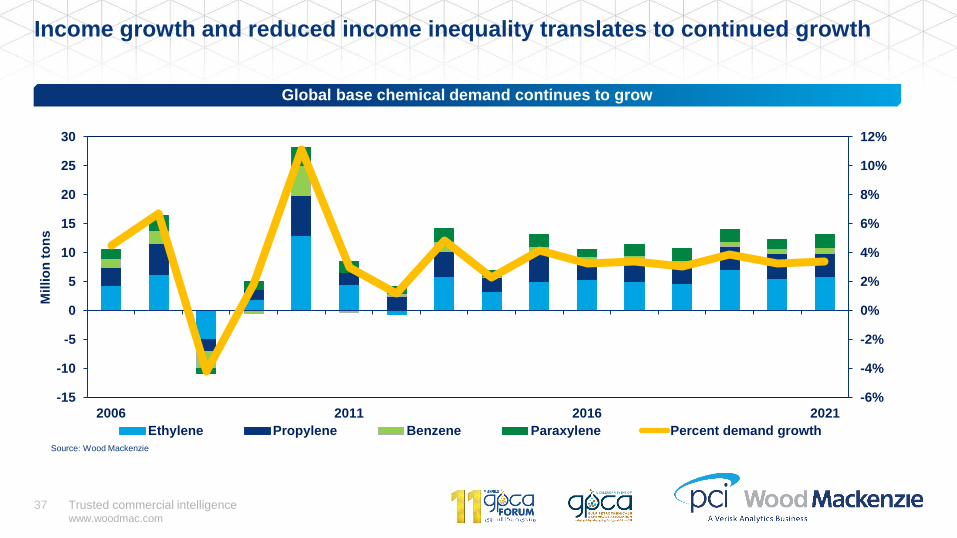

37

Income growth and reduced income inequality translates to continued growth

Global base chemical demand continues to grow

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

-15

-10

-5

0

5

10

15

20

25

30

2006 2011 2016 2021

Millio

n t

on

s

Ethylene Propylene Benzene Paraxylene Percent demand growth

Source: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

39

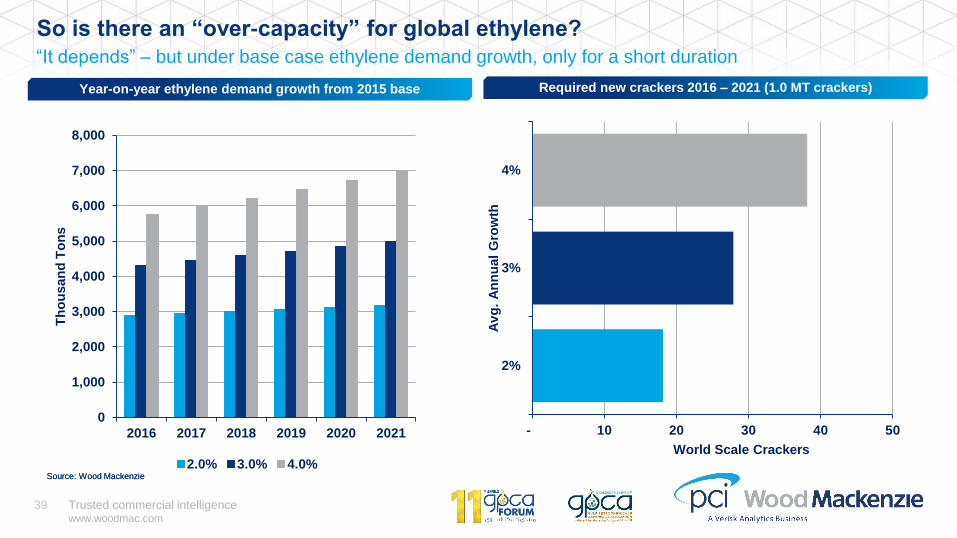

Year-on-year ethylene demand growth from 2015 base

“It depends” – but under base case ethylene demand growth, only for a short duration

So is there an “over-capacity” for global ethylene?

Required new crackers 2016 – 2021 (1.0 MT crackers)

- 10 20 30 40 50

2%

3%

4%

World Scale Crackers

Av

g.

An

nu

al

Gro

wth

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017 2018 2019 2020 2021

Th

ou

san

d T

on

s

2.0% 3.0% 4.0%Source: Wood MackenzieSource: Wood Mackenzie

Trusted commercial intelligencewww.woodmac.com

40

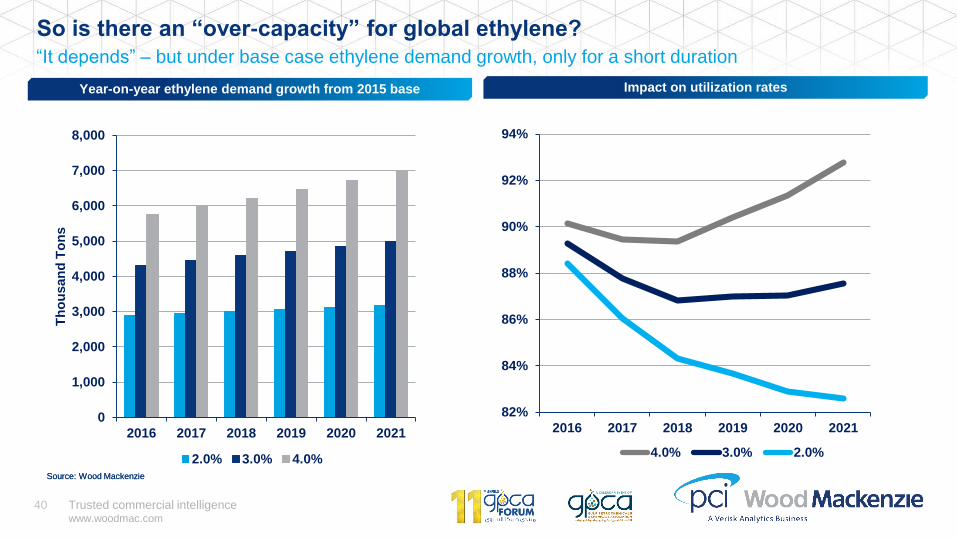

Year-on-year ethylene demand growth from 2015 base

“It depends” – but under base case ethylene demand growth, only for a short duration

So is there an “over-capacity” for global ethylene?

Impact on utilization rates

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017 2018 2019 2020 2021

Th

ou

san

d T

on

s

2.0% 3.0% 4.0%

Source: Wood MackenzieSource: Wood Mackenzie

82%

84%

86%

88%

90%

92%

94%

2016 2017 2018 2019 2020 2021

4.0% 3.0% 2.0%

Trusted commercial intelligencewww.woodmac.com

41

Agenda

The current competitive arena for olefins and aromatics

» Who are the winners and losers in an evolutionary world?

Amid economic fragility can chemical growth continue?

Impact on trade flows as new capacity is commissioned

» Focus on China imports

» Impact on key exporting regions

Conclusions

Trusted commercial intelligencewww.woodmac.com

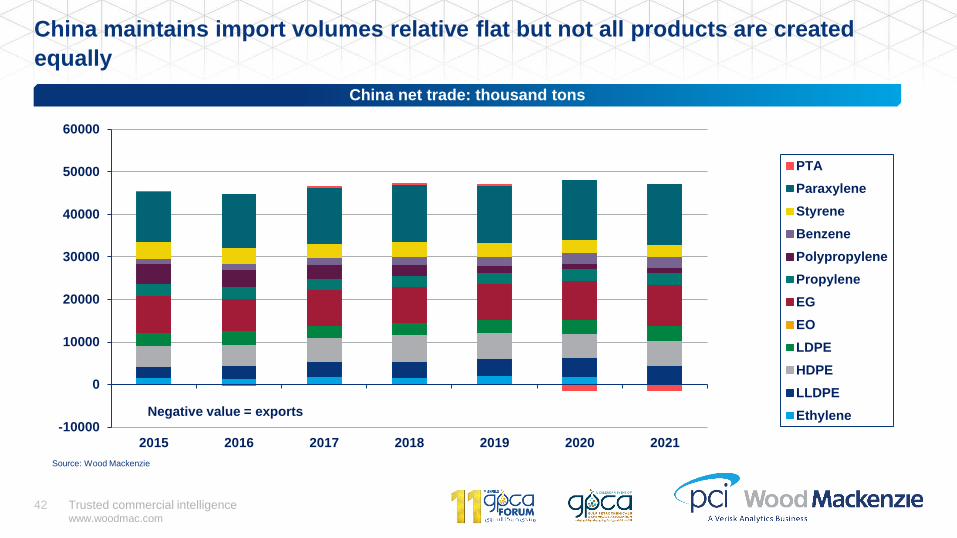

42

China maintains import volumes relative flat but not all products are created

equally

China net trade: thousand tons

-10000

0

10000

20000

30000

40000

50000

60000

2015 2016 2017 2018 2019 2020 2021

PTA

Paraxylene

Styrene

Benzene

Polypropylene

Propylene

EG

EO

LDPE

HDPE

LLDPE

Ethylene

Source: Wood Mackenzie

Negative value = exports

Trusted commercial intelligencewww.woodmac.com

43

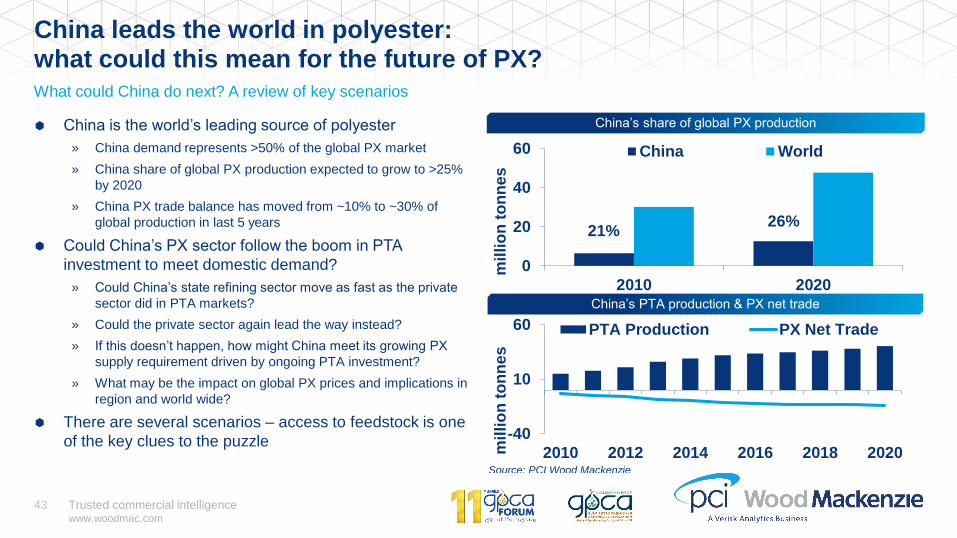

China leads the world in polyester: what could this mean for the future of PX?

China is the world’s leading source of polyester

» China demand represents >50% of the global PX market

» China share of global PX production expected to grow to >25%

by 2020

» China PX trade balance has moved from ~10% to ~30% of

global production in last 5 years

Could China’s PX sector follow the boom in PTA

investment to meet domestic demand?

» Could China’s state refining sector move as fast as the private

sector did in PTA markets?

» Could the private sector again lead the way instead?

» If this doesn’t happen, how might China meet its growing PX

supply requirement driven by ongoing PTA investment?

» What may be the impact on global PX prices and implications in

region and world wide?

There are several scenarios – access to feedstock is one

of the key clues to the puzzle

What could China do next? A review of key scenarios

0

20

40

60

2010 2020

mil

lio

n t

on

nes

China World

21%26%

China’s share of global PX production

-40

10

60

2010 2012 2014 2016 2018 2020mil

lio

n t

on

nes

PTA Production PX Net Trade

Source: PCI Wood Mackenzie

China’s PTA production & PX net trade

Trusted commercial intelligencewww.woodmac.com

44

Global base chemical trade flows – 2015, 2018, 2021China continues to dominate global trade/imports

Source: Wood MackenzieAll figures are in million tons

North America

Europe

Middle East

China

Rest of Asia

-50-40-30-20-10

010

2015 2018 2021

-50-40-30-20-10

010

2015 2018 2021

India-50-40-30-20-10

010

2015 2018 2021

-100

1020304050

2015 2018 2021

-100

1020304050

2015 2018 2021

-50-40-30-20-10

010

2015 2018 2021

Negative value = exports

Trusted commercial intelligencewww.woodmac.com

45

Agenda

The current competitive arena for olefins and aromatics

» Who are the winners and losers in an evolutionary world?

Amid economic fragility can chemical growth continue?

Impact on trade flows as new capacity is commissioned

» Focus on China imports

» Impact on key exporting regions

Conclusions

Trusted commercial intelligencewww.woodmac.com

46

Project execution: Critical success factors

Access to competitively priced feedstock

Project finance

Capital cost as low as possible using world-class technology

from an experienced licensor

Low energy costs and modern technology that fully

integrates energy recovery systems

Economies of scale

Access to a consuming market

Stable off take agreements

Strategic joint venture partner

Good local capability and skills to operate the plant ideally

with prior experience.

Top class project management to build and commission the

plant.

Environmental awareness

Trusted commercial intelligencewww.woodmac.com

47

In a low crude oil environment the task of project investment is the same but the margin for error is less

Easy voyage Little room for error

Which one would you rather captain? Do you have a choice?

Trusted commercial intelligencewww.woodmac.com

48

Lower oil prices flatten the olefins supply curve

complicating where to invest and which feedstock to utilize.

With forecast rising crude prices light olefins feedstocks

should enjoy advantaged costs.

Global chemical demand is expected to continue to grow

requiring extensive investments for years to come.

Global trade for most products will only rise to meet

growing demand.

Overall profitability of olefins-polyolefins chain is expected

to soften but with base case growth it will be a relatively

quick rebound.

China PX trade deficit is now 30% of global production

driving demand and trade. Extensive new capacity has yet

to be fully absorbed.

Key

takeaways

Conclusions

Trusted commercial intelligencewww.woodmac.com

49

Disclaimer

This presentation has been prepared by Wood Mackenzie Limited. The presentation is intended

solely for the benefit of attendees and its contents and conclusions are confidential and may not

be disclosed to any other persons or companies without Wood Mackenzie’s prior written

permission.

The information upon which this presentation comes from our own experience, knowledge and

databases. The opinions expressed in this report are those of Wood Mackenzie. They have been

arrived at following careful consideration and enquiry but we do not guarantee their fairness,

completeness or accuracy. The opinions, as of this date, are subject to change. We do not

accept any liability for your reliance upon them.

Strictly Private & Confidential

Wood Mackenzie™, a Verisk Analytics business, is a trusted source of commercial intelligence for the world's

natural resources sector. We empower clients to make better strategic decisions, providing objective analysis

and advice on assets, companies and markets. For more information visit: www.woodmac.com

WOOD MACKENZIE is a trade mark of Wood Mackenzie Limited and is the subject of trade mark registrations and/or applications in

the European Community, the USA and other countries around the world.

Europe +44 131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Website www.woodmac.com