83

INVESTOR PRESENTATION

INVESTOR PRESENTATION

DISCLAIMER

The communication may contain statements relating to futurebusiness developments, company’s performance and economicperformance that may constitute ‘forward looking statements’.p y gWhile these forward looking statements represent the company’sjudgments and future expectations, a number of factors could causeactual developments and results to differ materially fromexpectations. The company undertakes no obligation to publiclyrevise any forward-looking statements to reflect future events orcircumstances.

CUMI @ 2013 2

Murugappa GroupAn Overview

CUMI @ 2013 3

MURUGAPPA GROUP MURUGAPPA GROUP INR 225 BillionConglomerate

O f th l t f il t d

Conglomerate

One of the largest family promoted, professionally managed, diversified business groups

CUMI @ 2013 4

Th Phil h h i hThe Philosophy we cherish

The fundamental principle of economic activity is that No man you transact with will lose; then you shall not.

CUMI @ 2013 5

Murugappa Group Today

~ INR 225 Billion ConglomerateOne of the largest family promoted, professionally managed, diversified g y p , p y g ,business Groups…

CUMI @ 2013 6

The Spirit of the Murugappa Group

CUMI @ 2013 7

Corporate Social Responsibility

AMM Foundation

1% of PAT from Group companies to AMM1% of PAT from Group companies to AMMFoundation

4 Schools, a polytechnic; approximately 11,000 students

4 Hospitals - over 8,00,000 patients treated last yeartreated last year

Scholarships for needy meritorious Students

Research centre for technology for therural & urban poor

CUMI @ 2013 8

Carborundum Universal

CUMI @ 2013 9

Birth Of CUMI

19541954

CARBORUNDUM UNIVERSALUK

• Incorporated as a joint venturebetween Carborundum CompanyUSA, Universal Grinding WheelCompany, UK and the Murugappa,India USA UKIndia

• Acquired a coated abrasives facilityfrom Ajax products Pvt Ltd

• B d d b i f ilit t i• Bonded abrasives facility set up inChennai India

CUMI @ 2013 10

Business PortfolioCUMI – FY 13Sales Share PBIT ShareCUMI – FY 13

Revenue :Rs. 19.4 bn EBIT :Rs. 1.8 bn Capital Employed :Rs. 15.8 bn

Abrasives Revenue : Rs 8.1 bn

Ceramics Revenue : Rs 5.0 bn

Electro-minerals Revenue : Rs 6.7 bn

EBIT : Rs 0.8 bn Capital Employed : Rs 5.4 bn

EBIT : Rs 0.8 bn Capital Employed : Rs 3.7 bn

EBIT : Rs 0.2 bn Capital Employed : Rs 5.3 bn

Industrial Ceramics Super Refractories

Heat ResistanceWear Resistance

CUMI @ 2013 11

AbrasionHeat ResistanceWear Resistance

Electro Resistivity Electro Minerals

25 F t i 7 C t i

CUMI Consolidated

25 Factories 7 CountriesOver 4750 plus Employees. 2100 plus employees outside India Consolidated Gross Sales Rs 2042 cr (FY 12‐13 )Market Cap ~ Rs 2250 cr.Products being sold in 43 countries

CUMI @ 2013 12

RUSSIA Abrasives

CUMI World Wide- By Business Verticals

CANADA

CHINA

Ceramics

Electro mineralsAbrasives

Ceramics

USA

CHINA

Abrasives

Ceramics

THAILAND

Abrasives

Abrasives

INDIA AUSTRALIAUAEEUROPES. AFRICAFoskor ZirconiaTRI

Electro Minerals Abrasives

Ceramics

Ceramics

Electro minerals

AbrasivesAbrasives

Electro minerals

Electro Minerals

Ceramics

Abrasives l Ceramics l Electro Minerals CUMI @ 2013

Electro minerals

Manufacturing Base Marketing & Distribution Base13

OUR VISION/MISSION

ISIO

NIS

ION We will be an Admired Company in

Abrasives & Technical Ceramics, drivenby Innovation to create StakeholderVIVI by Innovation, to create StakeholderWealth.

SSIO

NSS

ION Become one of the largest Abrasives

(including Super Abrasives) / TechnicalCeramics in the Company in the World by

MIS

MIS Ceramics in the Company in the World by

2020.

CUMI @ 2013 14

ABRASIVESABRASIVES

CUMI @ 2013 15

ABRASIVES – Product Range

Coated AbrasivesThin wheels

A Strong Regional Player with the

A Strong Regional Player with thePlayer with the

complete Range of products.

Player with the complete Range

of products.

Bonded

Super AbrasivesConstruction

Products

CUMI @ 2013

Power toolsMetal Working Fluids

16

• Abrasives are made of hard tough and wear resistant materials used to shape or

ABRASIVES• Abrasives are made of hard, tough and wear resistant materials used to shape or

finish a work-piece. Abrasives are used for diverse applications ranging from material removal, polishing and finishing in multiple industries like automobile, auto-ancillaries, fabrication, construction and wood-working. There are 3 types of Abrasives

– Bonded: Bonded abrasives are mostly in the form of grinding wheels and used in diverse applications like fabrication & grinding

– Coated: A coated abrasive comprises an abrasive fixed to a backing material such as paper, cloth and fibre. Sandpaper is a very common coated abrasive. They are used in polishing.

– Super Abrasives: Involve high quality grains such as diamond or cubic boron nitride.

• CUMI manufactures all the 3 types of Abrasives (Super Abrasives through the JV Wendt India)

CUMI @ 2013 17

ABRASIVES - Application

Bonded Products and other applications ….

For Rough Grinding and Cutting applications:-

General EngineeringFabricationFoundryRolling MillsProjects

and other applications ….

and other applications ….

Thin Wheels

Coated Products

CUMI @ 2013 18

ABRASIVES - Application

Wood working Metal working Construction

and other applications ….

Power Tools

Rotary Tools Cutting Tool industries

Creep Feed grindingNotch and Slot grinding

Power Tools

Super Abrasives Products

gPrinting and Paper Roll grinding

Ceramic and Tile grindingWood Working Tools

Notch and Slot grindingTungsten Carbide Roll grindingCeramic and Refractory grindingGlass Industry

and other applications ….

CUMI @ 2013 19

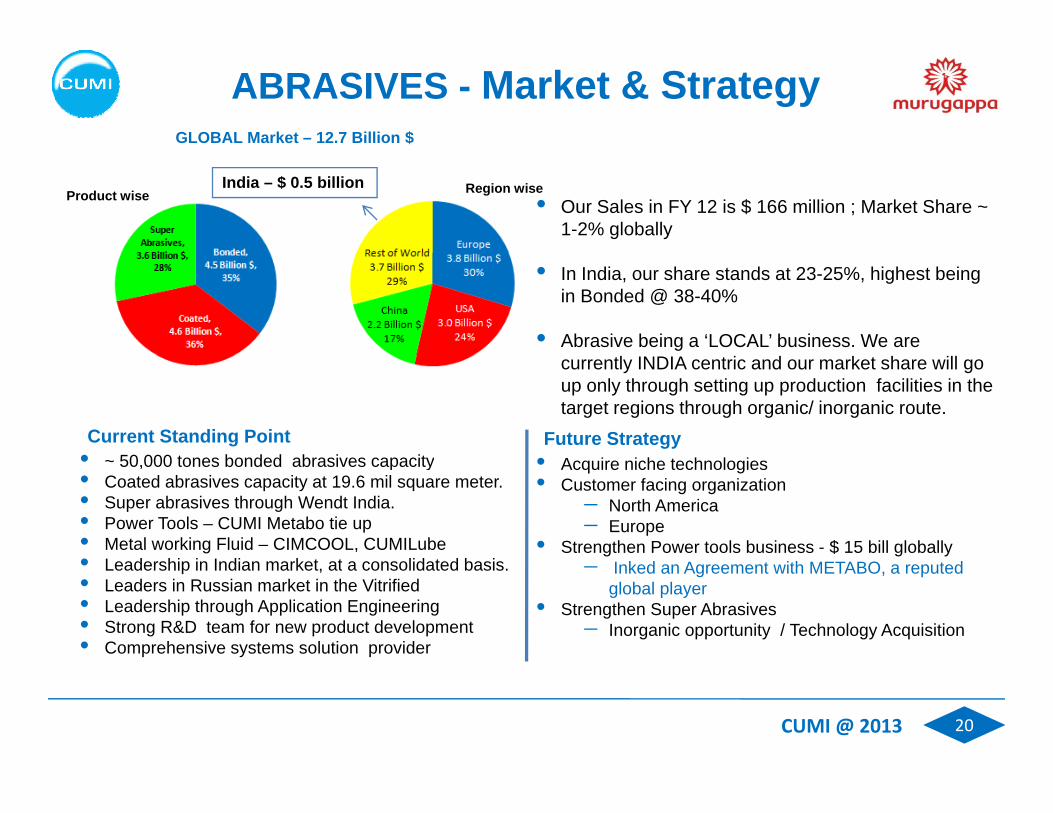

ABRASIVES - Market & StrategyGLOBAL Market – 12.7 Billion $

• Our Sales in FY 12 is $ 166 million ; Market Share ~ 1-2% globally

Product wise Region wiseIndia – $ 0.5 billion

• In India, our share stands at 23-25%, highest being in Bonded @ 38-40%

• Abrasive being a ‘LOCAL’ business. We are currently INDIA centric and our market share will go up only through setting up production facilities in the target regions through organic/ inorganic route.

• 50 000 tones bonded abrasives capacity • A i i h t h l iCurrent Standing Point Future Strategy

• ~ 50,000 tones bonded abrasives capacity• Coated abrasives capacity at 19.6 mil square meter.• Super abrasives through Wendt India.• Power Tools – CUMI Metabo tie up• Metal working Fluid – CIMCOOL, CUMILube• L d hi i I di k t t lid t d b i

• Acquire niche technologies• Customer facing organization

North America Europe

• Strengthen Power tools business - $ 15 bill globally • Leadership in Indian market, at a consolidated basis.• Leaders in Russian market in the Vitrified• Leadership through Application Engineering• Strong R&D team for new product development• Comprehensive systems solution provider

Inked an Agreement with METABO, a reputed global player

• Strengthen Super Abrasives Inorganic opportunity / Technology Acquisition

CUMI @ 2013 20

Abrasives Marketing Network

Plants Plants

Warehouses Institutions

Dealers We have ~ 500 dealersWe have ~ 1000 sub dealersSales Mix is 40% institutions, 60%

through channels to retail customers

Sub Dealerthrough channels to retail customers

Retail Customer Small Institutions

CUMI @ 2013 21

ABRASIVES – FacilitiesMarketing & Manufacturing

Sriperumbudur, Chennai CUMI Middle EastThiruvottriyur, Chennai Hosur, Tamil Nadu UttarkhandDistribution

dia

CACCL, ChinaVAW, Russia

CUMI Canada

Ind

Venlo Netherlands

Ove

rsea

s

Wendt, India Wendt, Thailand/CME Sterling Abrasives, Gujarat

CUMI USA

Sub

s / J

V’s

CUMI @ 2013 22

ABRASIVES INDUSTRY VALUE CHAIN

Input Materials Manufacturing Marketing Sales and ServiceInput Materials

Internal access to key

Manufacturing

Process

Marketing

Application

Sales and Service

Brand and access to key inputs.

New input t i l

Capability

Low cost

ppEngineering

New Product

Distribution

Customer f i material

development

S l

Low cost locations

R

New Product Development facing

Organization

Scale Range

CUMI @ 2013 23

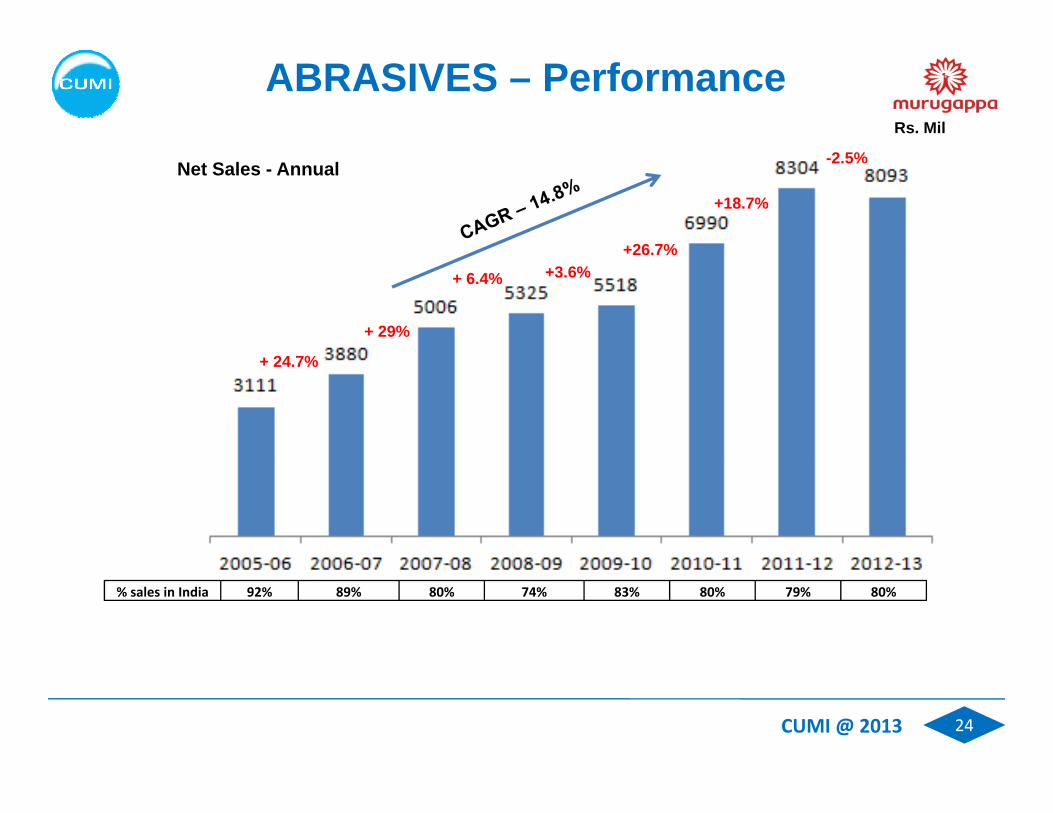

ABRASIVES – PerformanceRs. Mil

Net Sales - Annual

+26.7%

+18.7%

-2.5%

24 %

+ 29%

+ 6.4% +3.6% +26.7%

+ 24.7%

% sales in India 92% 89% 80% 74% 83% 80% 79% 80%

CUMI @ 2013 24

INDUSTRIALINDUSTRIAL CERAMICS

CUMI @ 2013 25

INDUSTRIAL CERAMICS Product Range

Wear Protection

ICMetallized Ceramics

Engineered Ceramics

CUMI @ 2013 26

INDUSTRIAL CERAMICS • A ceramic is an inorganic, non metallic solid prepared by the action of heat and subsequent

cooling CUMI is into Alumina based Industrial ceramics There are broadly three productcooling. CUMI is into Alumina based Industrial ceramics. There are broadly three product categories, which CUMI is into

– Wear Resistant products (Tiles): These are weldable and pastable alumina ceramic tiles that can be bonded onto the surface to be protected from wear. They are used in p yindustries where bulk material movement causes heavy wear of the equipment and thus these products are used to protect equipment from heavy abrasion and wear.

– Lined Equipments - these are fabricated steel lined with ceramics as per customers' requirement. They are also used in industries for Wear and corrosion resistance application

– Engineered Ceramics: These come in different types: - Ceramic Seals, Customized Ceramics, Insulators & Ignitors, Textile components and Zirconia components.

– Metz Cylinders and Devices: They are used in industries for Electrical resistivity application. The products come in three different types:-

– Metallized Ceramics for vacuum interruptersM t lli d C i f l t i l d l t i d i

CUMI @ 2013

– Metallized Ceramics for electrical and electronic devices– Metallized ceramic brazed components

27

INDUSTRIAL CERAMICS ApplicationsP G ti Power Generation

Coal Mill (Inner Cone, Multiport Outlet Valve, Mill Discharge Valve, Mill Inner Dia Lining, Orifices, Ventury Vanes)

Bends (Tranisitions & Y- Pieces) Ash Handling (Bends & Slurry Pipes)

Wear Resistant Productsg ( y p )

Cement Industry – Coal and Raw Mill

Coal washeries and Material Handling

Lined Equipment

Pulverized Fuel Bends Cement Industry

Boiler industry Textile industry Boiler industry Pump Shaft Sleeves Pump plungers Pump Cylinder Liners

Textile industry Electronics

Engineering Ceramics

Electrical transmission and distribution Electronics industry Textile machinery Defense

Medical Electronics Solid Oxide Fuel Cells

CUMI @ 2013

DefenseMetalized Products

28

INDUSTRIAL CERAMICS – Market & Our Standing

• Over 6800 tons tiles and 0.8 million cylinderscapacity in India

GLOBAL Market for Advanced CERAMICS• Out of the total $ 13 billion market, Alumina based Ceramics

material is around ~ 5 billion.

Alumina based C i M k Million $ Our Market

Sh

Current Standing Point

• Leadership in Indian and Australian market.Active player in North American and SouthAfrican market

• This being a GLOBAL business, 65% of the

Ceramics Market Million $ ShareEnergy and Aerospace 250 6%Wear Resistant 1000 3%Bio Ceramics 3500 ‐Defense 75 ‐

produce is exported.

• Leadership established, through

Developing manufacturing technology and

• In Energy and Aerospace category, market for Metallizedproducts would be around 80 million $. Our Share in theMetallized Ceramics market is around 18% and in the overall

Cutting Tools 175 ‐Total 5000

achieving process efficiency and scale Designing and providing end to end solution

in India and Installation/ Servicing incustomer country

Energy and Aerospace is 6%

• In Wear Resistant application, global market for our range ofWear resistant products would be around 200 million $. OurShare in the market would be 14% and in the overall WearResistance is 3% • The division uses Lean and Six Sigma to drive

efficiencyResistance is 3%

• Our strategic intent is to (a) increase market share byaddressing newer geographies (b) introduce new productofferings to increase our addressable market size which iscurrently limited to 280 million $

CUMI @ 2013

currently limited to 280 million $

29

INDUSTRIAL CERAMICS – Future Strategy

• Currently we are in the business of Alumina based Ceramics. We constantly look at extending offerings in that range and target

Products Competing Criteriag g g g

newer industries.

• Move up the Value Chain constantly by offering high value products We have been

Metz Cylinders

chai

n

Technology, Process Capability

offering high value products. We have been actively pursuing the same as depicted in the picture alongside.

Armored & Engineered ceramics

the

valu

e c

Technology, Process Capability

• Build customer facing entities as we have in Australia to provide end to end solutions in other geographies – South Africa / North America.

Wear & Corrosion resistant product

Mov

ing

up t

Cost, Installation Service Capability

• Grow in Ceramic medical businessGrinding Media M

Cost

CUMI @ 2013 30

INDUSTRIAL CERAMICS Facility

We have World Class facility based out of HOSUR, Tamil Nadu

We have one of the few six sigma ceramic operations in the World

CUMI @ 2013 31

INDUSTRIAL CERAMICS INDUSTRY VALUE CHAIN

Input Materials Design and Manufacturing Sales and Input Materials

Internal access

Engineering

Application

Manufacturing

Process

Installation

Customer facing to key inputs.

New input t i l

ppKnowledge

EPC Contractors /

Capability

S l

facing Organization

Installation / S i material

developmentContractors /

Consultant Approvals

Scale

Plant

Service capability

Scale Plant Engineering

CUMI @ 2013 32

SUPERSUPER REFRACTORIES

CUMI @ 2013 33

SUPER REFRACTORIES– Product RangeCUMI Refractory Products

Fired products

Silicon Carbide (CUMIFRAC)

Monolithics

Conventional Dense

C t bl

Precast Shapes

(CUMIFRAC)

Nitride bonded Silicon Carbide

Castables (CUMICRETE)

Insulation Castables

(CUMICRETE Li ht W i ht)

Mulite (CUMILITE)

Light Weight)

Low cement castables

(CUMIHICAST & CUMIPLASCAST)

High Alumina (CUMILOX)

Zirconia Mulliteand Zircon (

Self Flow Castables (CUMIFLOW

&CUMICAST EF)

(CUMIZITE & CUMIZON)

Insulation Firebricks (CUMILAG)

Ramming Mass (CUMIRAM)

Laying Mortars (CUMILAG)(CUMI Bond)

CUMI @ 2013 34

SUPER REFRACTORIES

R f t i t i l th t ith t d hi h t t CUMI i• Refractory is any material that can withstand high temperature. CUMI is into High Alumina, Silicon Carbide, Zirconia based refractories which are capable to withstand very high temperature:-

Fired Refractories: Is a block of refractory ceramic material used in lining furnaces, kilns & fireplaces. A refractory brick is built primarily to withstand high temperature.

Monolithics: These are refractory material in powder form. These are materials which are installed as some form of suspension that ultimately harden to form a solid mass.

• The division also manufactures and sells Anti-corrosive products: Corrosion is a degradation of materials’ properties caused by chemical reaction with their environments. Anti-corrosive products are used in plants/ products which undergo such corrosion.

CUMI @ 2013 35

SUPER REFRACTORIES - Application

Ceramic Industries Chemical Process Industries Non – FerrousCeramic IndustriesInsulatorsSanitaryware & TablewareAbrasives

Chemical Process IndustriesCarbon BlackFertilizerPetro-Chem. / Refinery

Non FerrousAluminumCopperZinc

Wall TilesRefractoriesElectro Ceramics

Cement Iron & Steel

GlassContainer

Soda lime

Power Generation Boiler

Sponge Iron (DRI)Gas-Based Coal - Based

Soda-limeBoro-silicate

DecorativeFibreglass

Foundries

g

CUMI @ 2013 36

REFRACTORY MARKET

World Refractory Demand ($30 billion) by Regions

World Refractory Demand ($30 billion) by Industry

Global Refractory market - $30 BillionGlobal demand for refractories is projected to rise 4-5 percent per year

CUMI @ 2013 37

SUPER REFRACTORIES – Market & Strategy• The Global size of Refractory business could be estimated to

th t t f $ 30 billi • Over 9 500 tons Fired capacity in India andCurrent Standing Point

the extent of ~ $ 30 billion• Refractory is a ‘LOCAL’ business. 90% of our sales are in

domestic market.India Market

P d t i Industry CUMI’s Addressable CUMI’s

Rs. Cr

• Over 9,500 tons Fired capacity in India and Russia. Around 32,000 tons monolithic capacity in India; NbSiC capacity in Russia

• Leadership in Indian market in select productsActive player in the Russian marketProduct wise y

Market Size Market Size Market Share

Basic 1200Dolomite 400High Alumina 1100 200 38%

Active player in the Russian market.

• Leadership in Fiber Refractories in Indian market through MMTCL JV

• Niche product offerings in Glass and Carbon High Alumina 1100 200 38%

Silica 200Flow Control 500Monolithics 1100 400 12%

p gBlack industry in India and Aluminium industry in Russia.

• Ability to manufacture complex shapes

Future StrategyTOTAL 4500

• We operate only in Fired High Alumina and Monolithicsbusiness, that too for not entire temperature range, but only forspecific high end range . Hence our addressable market size is~ Rs 600 cr

• Green field project for capacity expansion• Inorganic opportunity – with success

100% stake in RHI Isithebe, South Africagiving us 1500 tons Fired capacity and 6000tons Mono

Future Strategy

~ Rs. 600 cr

• We have entered with Technology agreement with SheffieldRefractories, UK and Anderman Ceramics, UK . We have alsoacquired 100% stake in TRI, South Africa. With these we wouldbe entering Flow Control market and also increasing our

tons Mono Techno-commercial agreement with Sheffield

Refractories, UK and with AndermanCeramics, UK to manufacture, supply andinstall a range of high end refractory solutionsfor the Steel industry, Glass industryIn 2011 we had formed JV with Israel based

CUMI @ 2013

be entering Flow Control market and also increasing ouraddressable market size in High Alumina and Monolithics.

In 2011, we had formed JV with Israel basedcompany, for a new Refractory material.

38

SUPER REFRACTORIES

Ability to manufacture complex shapes and meet all surge requirements

CUMI @ 2013 39

REFRACTORY INDUSTRY VALUE CHAIN

Input Materials

Design and Engineering Manufacturing Sales and

Installation

Low cost input / access

Application Knowledge

Process Capability

Customer facing

Organization

Energy / Power

OE Approvals Scale

Installation / Service

capability

Plant Engineering

Low cost

CUMI @ 2013 40

CERAMICS (Industrial Ceramics and Refractories)-Performance

Net Sales - Annual Rs. Mil

+9 3%

+ 21%

+ 31%

+9.3%

+ 26.8%

+ 17.4% + 11.1%

+ 21%

+20.4%

% l i I di 54% 54% 64% 64% 62% 67% 60% 53%

CUMI @ 2013

% sales in India 54% 54% 64% 64% 62% 67% 60% 53%

41

ELECTRO MINERALSELECTRO MINERALS

CUMI @ 2013 42

ELECTROMINERALS – Product Range

Brown Fused Alumina White Fused Alumina Silicon carbide Zirconia Specialty minerals

Bonded Abrasives

Refractory Silicon wafer slicing

Diesel Particulate Filter

Coated Abrasives

Metallurgical Investment casting

Floor Laminates

Surface Engineering Refractories Energy & Environment

CUMI @ 2013

Surface Engineering Refractories Energy & Environment

43

ELECTROMINERALS - Application

Refractory Bonded Abrasives Coated Abrasives Dermabrasion

Semi Conductor Lapping Laminates Pressure Blasting

CUMI @ 2013

Photovoltaic Plasma Spray Particulate Filters Metalurgical

44

ELECTROMINERALS – Facility

11

2

1 Bauxite mines & calcination 3

2 Sili bid 5400 t

4

3 Fine powders, 11,400 tpa

2 Silicon carbide, 5400 tpa

4 Fused alumina ~22000 tpa

5 12 MW Hydel power, Maniyar

5

CUMI @ 2013

5 yde po e , a ya

45

ELECTROMINERALS – Overseas Facility

VAW -Russia

VAW Russia – Silicon Carbide, 70000 tpa

Foskor Zirconia Fused Foskor Zirconia Foskor Zirconia – Fused Zirconia, 10000 tpa

TRI – 22k tpa fusion facility

Thukela Refractory

CUMI @ 2013 46

ELECTRO MINERALS –Global Capacity & Our Standing

• Fused Zirconia Global capacity of Fused Zirconia ~ 75k tons per

annum

• Established leadership in Russian and Indian market

Global Capacity and Our Share Current Standing Point

annum. With 10k tons per annum, we are the third largest in

the world after Saint Gobain and Imerys. Around 40% capacity is in China

• Sili C bid

• Locational advantage in Russia by way of low power and pet coke cost providing significant cost competitiveness in SiCbusiness• Silicon Carbide

Global capacity is ~ 2 million tonnes. Price and Cost movements, macro factors, keeps these facilities either running or closed.

With 70k tons per annum in VAW we are the second

business

• In Speciality products, CUMI has achieved leadership in this business by way of improving process capability andlargest after Saint Gobain

Around 50% of the capacity is in China, with no single identifiable big player

• Fused Aluminas

improving process capability and Micronisation

Global capacity is ~ 1.7 million tonnes CUMI share is 1% Around 50% of the capacity is in China

CUMI @ 2013 47

ELECTRO MINERALS – Future Strategy

Innovation Value PyramidInnovation Value Pyramid

CUMI @ 2013 48

ELECTRO MINERALS – Future Strategy

I ti V l P id

C11Nano

synthesisLevel 4 – Nano Powders

Innovation Value Pyramid

• Alternative application in SiC apart from Ph t lt i

C10Ultrafine powder

processing

C9Chemical processing

Level 3 – Sol gel Ceramics Sub micron powder

Powders Photovoltaic

• Synthetic Brown Alumina in the market

• Build scale and size at lowest cost locationM i t ‘Bi F ’

C8Heat

treatment

C6Powder

processing

processing

C7Sintering

Level 2 – Controlled Crystallization and Micronization

Moving to ‘Big Furnace’ FZL – doubling of capacity by Sep 2012 Acquisition of RHI giving 30k tonnes of fused

capacity

• Organic expansion of Sintered Alumina

C3Fusion

C4Grain

processing

C5Surface coating

C1Mining

C2Calcination Level 1 ‐

Fusion

• Organic expansion of Sintered Alumina

• Continued focus on establishing technology base/ process capability through internal development – produce specialty version of ZirconiaZirconia

• Gradually increase share of level 3 in the EMD consolidated basket (refer Fig alongside)

CUMI @ 2013 49

ELECTRO MINERALS INDUSTRY VALUE CHAIN

Input Materials Technology Manufacturing Product Input Materials

Access to minerals, pet

Technology

Process

Manufacturing

Capacity /

Development

Customer , pcoke, cell

grade Alumina

L t P

Capability

Development t Alt t

p y /Scale

Low cost

Partnership

R&DLow cost Power

i

to use Alternate Inputs

Low cost Location R&D

Location

CUMI @ 2013 50

ELECTRO MINERALS - Performance

N t S l A l Rs MilNet Sales - Annual Rs. Mil

+22% -8%

9 %

+13%

+25%

+21.7% +15.9%

+97%

CUMI @ 2013 51

CUMI Growth Paradigm

n ked

ally

driv

en

y ne

twor

k

-Inte

rna

Ext

erna

lly

New Materials-E

CUMI @ 2013 52

Competency based on having a very wide Technology canvas

Products and TechnologiesApplications

• Abrasives/Grains – Material cutting and removal

Key Properties

• Hardness

Products

• Grinding Wheels

• C t d P d t

Products and Technologies

and removal

• Refractories

• Insulators

• Engineered Ceramic components

• Material removal

• Thermal resistance

• Wear resistance

• Coated Products

• Fused Grains

• High purity Ceramics

• R f t i g p(Seals)

• Nuclear imaging

• Wear resistance equipments

• High density and purity

• Corrosion resistanceProcesses

• Fusion

• Refractories

• Dimensional stability

• Electrical resistivity

• Compaction

• Sintering

• Finishing

• Surface Coating

• Electro Plating

• Powder preparation

CUMI @ 2013

• Size reduction

53

Technology Platforms

40 Technology Platforms

CUMI @ 2013 54

FINANCIALS

CUMI @ 2013 55

Revenue Growth

19685 19424

909311930 12823

1600719685 19424

+7.5% +25%

+23% -1.3%

62109093

. In

Milli

on

+46%

+31%

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

Rs

CUMI @ 2013 56

International Revenue share (%)

5160

ge 31

45 44 44 48 51

405060

Per

cent

ag

13102030

010

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

CUMI @ 2013 57

Income Statement Rs Million

Income StatementIncome Statement Rs. Million

2006‐07 2007‐08 2008‐09 2009‐10 2010‐11 2011‐12 2012‐13Net Sales 6210 9093 11930 12823 16007 19685 19424

Growth % 46% 32% 7.5% 25% 33% -1%EBITDA 1390 1553 1988 2435 3130 4016 2502

R Milli

EBITDA % 22.4% 17.1% 16.7% 19.0% 19.6% 20.4% 12.9%Depreciation 195 300 351 413 504 569 711PBIT 1195 1253 1637 2022 2626 3447 1791

PBIT % 19.2% 13.8% 13.7% 15.8% 16.4% 17.5% 9.2%Excep Items 0 676 288 0 235 24 0 Rs. MillionExcep. Items 0 676 288 0 235 24 0

PBT 1119 1740 1601 1714 2580 3227 1519PBT % 18.0% 19.1% 13.4% 13.4% 16.1% 16.4% 7.8%

PAT 751 1189 1037 1017 1708 2193 898PAT % 12.1% 13.1% 8.7% 7.9% 10.7% 11.1% 4.6%

Net SalesNet Sales

CUMI @ 2013 58

Segmental Performance

Net Sales (Rs. Mil) 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Abrasives 3880 5006 5325 5518 6990 8304 8093

Ceramics 1734 2199 2582 2871 3476 4565 4991

Electro minerals 830 2153 4245 4789 5979 7272 6688

Inter segment 351 382 370 596 704 773 737Inter segment -351 -382 -370 -596 -704 -773 -737

Others 116 116 148 241 266 316 389

Net sales 6210 9093 11930 12823 16007 19685 19424

PBIT Margin (%) 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13

Abrasives 16.0 13.4 9.8 9.4 13.7 15.0 10.3

Ceramics 22.5 20.0 20.3 19.4 17.6 19.7 15.8

Electro minerals 18.4 12.1 17.9 21.5 18.4 19.2 3.5

Total 19.2 14.5 13.7 15.8 16.4 17.5 9.2

CUMI @ 2013 59

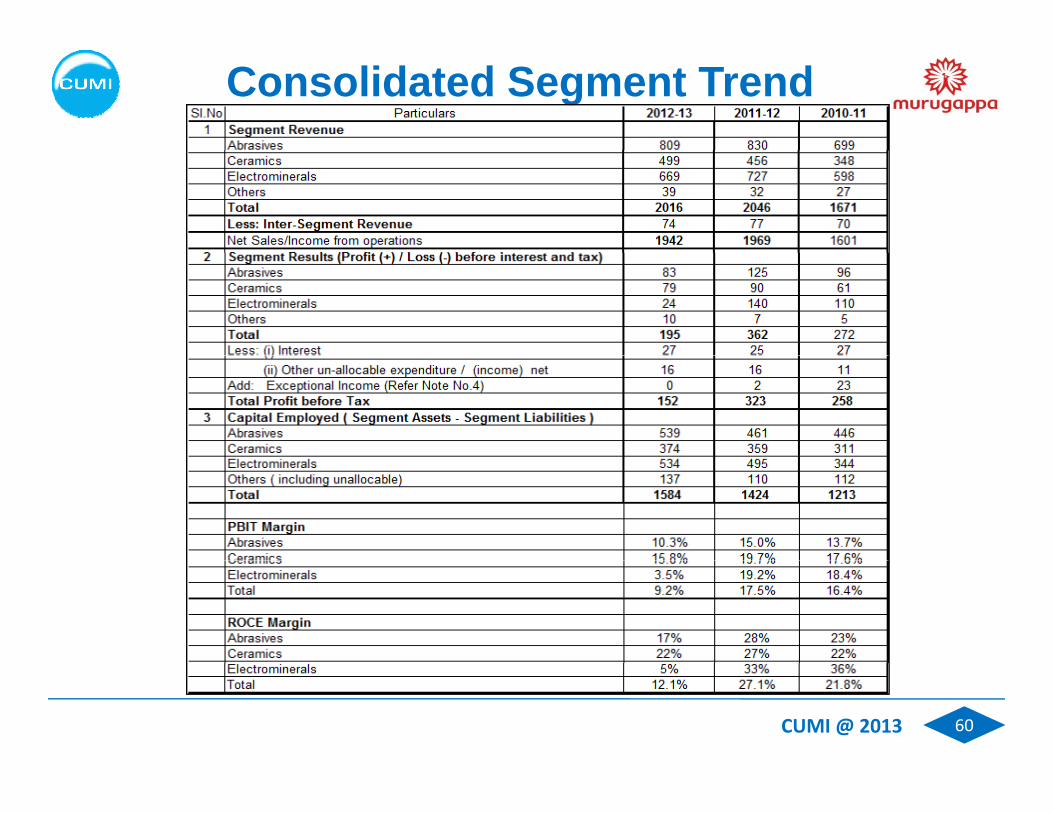

Consolidated Segment Trend

CUMI @ 2013 60

PBIT MarginSales- Rs. Mil

Segmental PerformanceAbrasives Abrasives

18 7%

-2.5%

+ 24.7% + 29% + 6.4%

+3.6% +26.7%

+18.7%

Ceramics Ceramics+ 9.3%

+20.4% + 26.8%

+ 17.4% + 11.1%

+ 21% + 31%

Electo Minerals

Electro minerals

+25%

+22% -8%

+21.7% +15.9%

+97% +13%

+25%

CUMI @ 2013 61

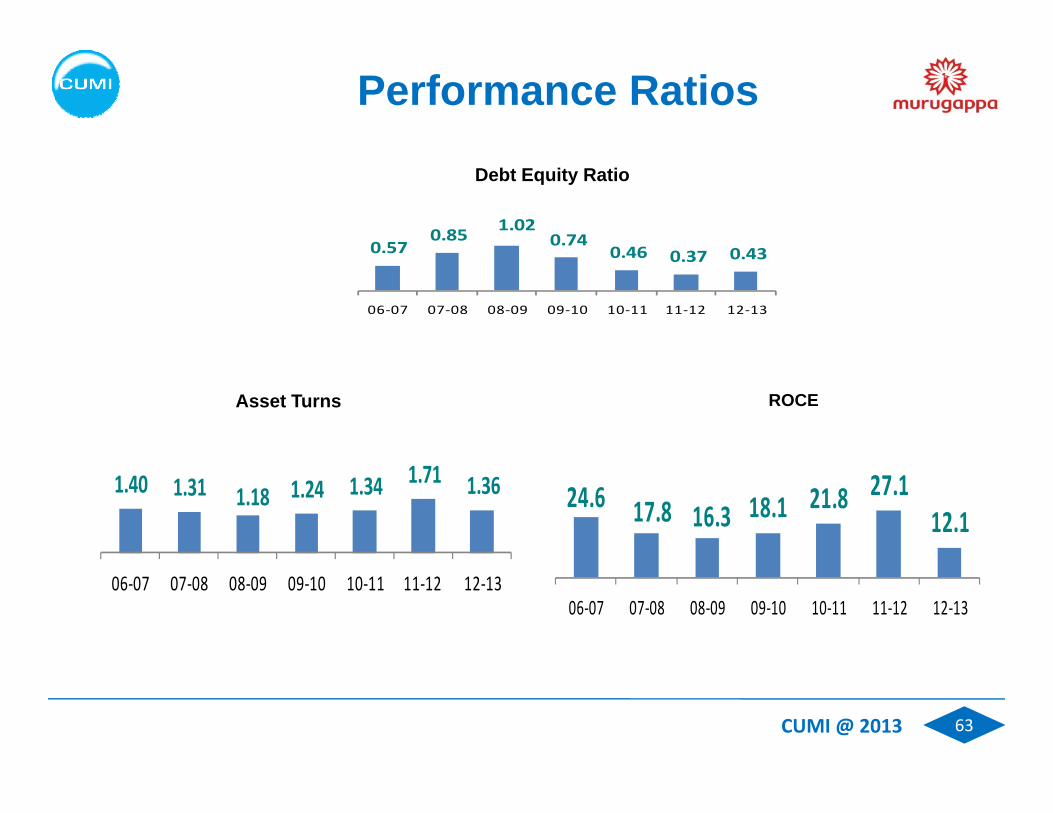

Performance Ratios

22.4 17.116.7

19.0 19.6 20.4

12.1

EBITDA %

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

19.2 16 4 17.5

PBIT %

13.8 13.715.8

16.4

9.2

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

CUMI @ 2013 62

Performance Ratios

0.570.85 1.02

0.740 46 0 37 0 43

Debt Equity Ratio

0.57 0.46 0.37 0.43

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

Asset Turns ROCE

1.40 1.31 1.18 1.24 1.34 1.71 1.36 24.6 17.8 16.3 18.1 21.8 27.112.1

06‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐1306‐07 07‐08 08‐09 09‐10 10‐11 11‐12 12‐13

CUMI @ 2013 63

Capex for 12-13 – Key Investments

AbrasivesUltra Thin Wheels Plant in UTKVAW Debottlenecking in Abrasives

~Rs.40 Crs.

Electro-minerals CUMI blue capacity expansion FZL capacity increase VAW Maintenance and Debottlenecking

~Rs.110 Crs.

Ceramics & Refractory ~Rs.45 Crs.

Expansion of NbSiC capacity Technology Acquisition in refractory

Power ~Rs. 25 Crs. SEDCO

Capex planned in 2013-14 ~ Rs. 100 crCapex executed in 2012-13 ~ Rs. 220 cr

CUMI @ 2013

p p

64

Bubble ZirconiaNew Projects – Foskor Tilt Project

Bubble Zirconia

Production Process

Applications & Markets

Refractory (80%) Refractory (80%) Specialty chemicals (5%) Fused Cast material for Glass Industry (10%) Titanium Investment Casting (5%)

Applications addressed with existing product Titanium Investment Casting (5%)

Magnesia & Calcia Double Fused products for Refractories

existing product range

g p f f Friction – Brake Linings Pigments Technical Ceramics – Calcia Stabilised, Yttria Stabilised, New applications , ,

Magnesia Stabilised, Ceria Stabilised Thermal Spray Powders Alumina Zirconia Abrasive Grains

require high purity and fine powders – Addressed with

Bubbles

Nuclear Power Generation

Applications & Markets- Bubble Zr

Glass and CeramicsPigments

Abrasives

CUMI @ 2013 68

New Projects – Alumina Zirconia Project

Only Alumina Zirconia plant in India

Fi t f Al i Zi iFirst pour of Alumina Zirconia

CUMI @ 2013 69

New Projects – Lite ceramics Bubble

C R I L bubble project : Only bubbleC R I L bubble project : Only bubble refractory plant in the world

CUMI @ 2013 70

Barmag commissioned to address the Refractory Market

CUMI @ 2013 71

Thukhela Refractories

W ki lif b d RHIWorking on life beyond RHI

New range of BFA,WFA at Thukhela (TRI )

CUMI @ 2013 72

Then

Volzhsky Abrasives

Then..

Cleaner, Greener Volzhsky AbrasivesNow ..

CUMI @ 2013 73

Technology Transfer Signing AgreementSigning Agreement

Technology Transfer Agreement Signing with Sheffield's

CUMI @ 2013 74

Investor Friendly Company

• 42.2% held by the Murugappa Group. 33% held by FII’s, MF, PE, Insurance Cos

• 59 years of unbroken track record of Profit and Dividendy

• Six Bonus Issues since inception – 89% of the current Equity is by way of capitalization of Reserves

• Growth in the last 5 years entirely funded by Debt Internal accruals and by• Growth in the last 5 years entirely funded by Debt, Internal accruals and by unlocking value

• Investor / Analyst Interaction

Quarterly Earnings Call and Transcripts upload

Minimum 2 investors Presentation in Mumbai and Abroad

Bi A l C i ti f t t ll i t Bi Annual Communication on company performance sent to all investors

100 plus investor visits / tele conference in a year

CUMI @ 2013 75

Market Performance RatiosDi id d P t R tiDividend Payout Ratios

CUMI @ 2013 76

Exhibition / Conference

Refractory Exhibition in Russia - Mirstekla Glasstech Asia – Bangkok

CUMI @ 2013 77

Exhibition / Conference

NMD Conference, Jamshedpur, November 2012

78CUMI @ 2013

CUMI Skill Development Center

In order to develop alternative to contract /flexi system andto contract /flexi system and ensure ready availability of Skilled Workmen, CUMI launched Skill development C t i HCenter in Hosur

CUMI @ 2013 79

Accolades

CUMI i i h S h CUMI i i h I i lCUMI team winning the Southern Region Kaizen Competitions by CII.

CUMI team winning the International Competitions of Quality Circle Forum.

CUMI has won the Safety Award of Department of Factories, Government of K l f th 2012 13

CUMI team winning the M.K.K. Nair Memorial Productivity Awards from

CUMI @ 2013

Kerala for the year 2012-13. Memorial Productivity Awards from Kerala State Productivity Council

80

Corporate Social Responsibility

Tie up with ANBALAYA SCHOOL (A school forSCHOOL (A school forphysically challenged children located at Thiruvottiyur) -C d ti F M di lConducting Free Medical Camp and Participation in World Disabled Day

CUMI @ 2013 81

Sustainability Index

Threshold of Vulnerability

We are significantly above the threshold of vulnerability on all.

High level of sustainability.

CUMI @ 2013 82

CUMI @ 2013 83