Professur für BWL, insb. Internationale Wirtschaft Cases II International Financial Management Folie 1 Case: Cemex S.A. & P.T. Semen Gresik - Multinational Capital Budgeting - -International Acquisitions and Valuation- - Political risk -

Transcript

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 1

Case: Cemex S.A. & P.T. Semen Gresik

- Multinational Capital Budgeting -

-International Acquisitions and Valuation-

- Political risk -

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 2

1. Overview 2. Multinational Capital Budgeting3. International Acquisitions & Valuation4. Lessons Learned From The Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 3

1. Overview2. Multinational Capital Budgeting3. International Acquisitions & Valuation4. Lessons Learned From The Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 4

Objectives

• Understand… basic principles of multinational capital budgeting… how to use valuation techniques for international acquisitions… significance of political risk

• Learn … how to evaluate investment opportunities abroad... how to adjust for risk... how to align an international expansion strategy with

privatization needs of emerging Asian economies

Cementos Mexicanos (CEMEX) from Mexico considers international expansion in Asia

Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 5

Cemex S.A.

• Largest cement manufacturer in the Americas, 3rd largest in the world

• Based in Monterey, Mexico w/ operations in 22 countries• High operating margins, crisis experienceCorporate Strategy• Leverage the core business • Maintain high growth• Concentrate on developing markets

Asian expansion in order to turn Cemex into a global player

• Market Entry 1997 Philippines (30% stake in Rizal Cement)

• New target: Indonesian market

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 6

Global and Indonesian Cement Markets I• Cement: commodity with high transportation cost

=> regionally segmented markets• Most important market in Indonesia is Java:

Jakarta- dominated by Indocement, West Java- dominated by Semen Cibinong, East Java dominated by Semen Gresik

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 7

Global and Indonesian Cement Markets II

• Asian crisis turmoil slashed relative prices across Asia• Indonesian government deregulated cement market by

abolishing the local guideline price systemprice war? Squeeze of Indonesian gross margins

– turned exporting into a beneficial business strategy within Asia (ex. Taiwan)Even US markets could be “conquered”

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 8

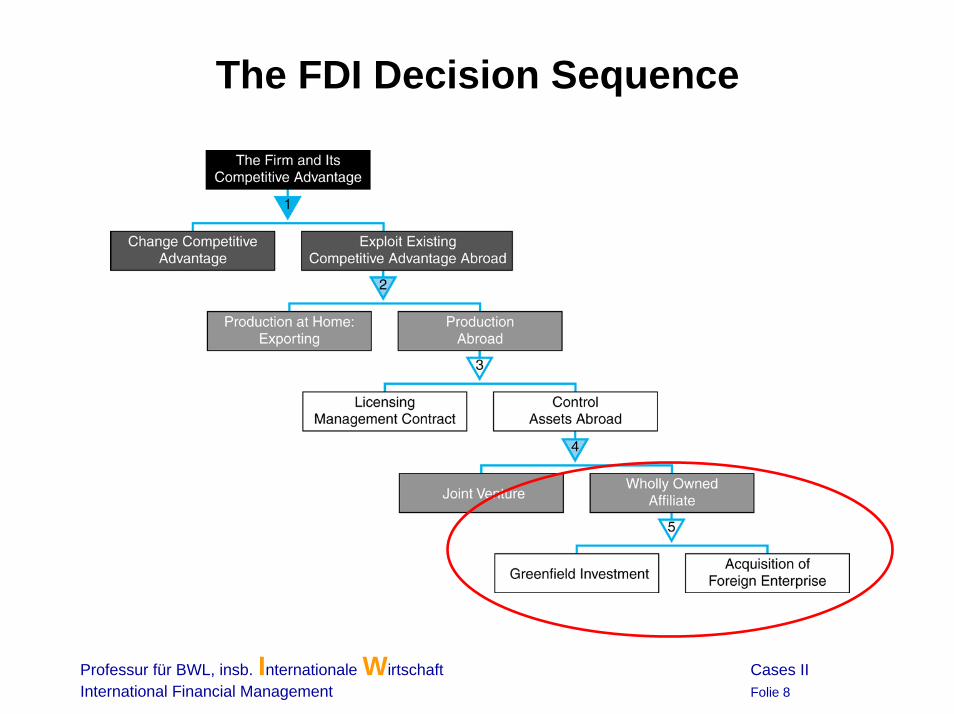

The FDI Decision Sequence

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 9

Market Entry ViewMarket Entry Modes• Enter by greenfield investment or by acquisition?• Decide on a case-to-case basis• Decision techniques:

– greenfield investment: CAPITAL BUDGETING– acquisition of foreign enterprise: VALUATION METHODS

multiplesdiscounted cash flow (DCF) method

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 10

1. Overview2. Multinational Capital Budgeting3. International Acquisitions & Valuation4. Lessons Learned From The Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 11

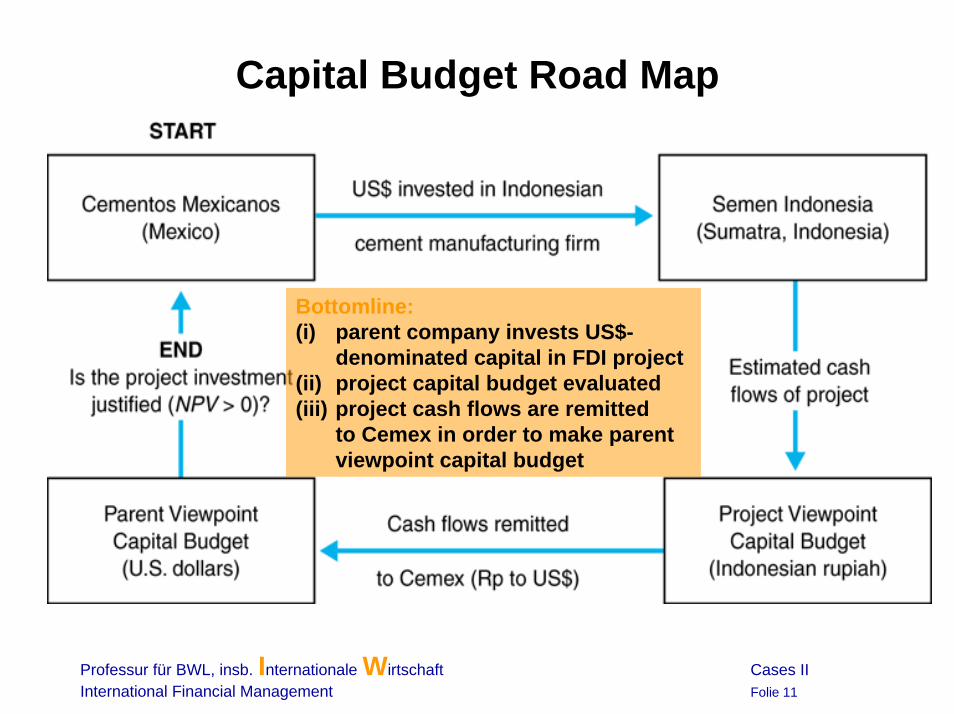

Capital Budget Road Map

Bottomline:(i) parent company invests US$-

denominated capital in FDI project (ii) project capital budget evaluated (iii) project cash flows are remitted

to Cemex in order to make parent viewpoint capital budget

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 12

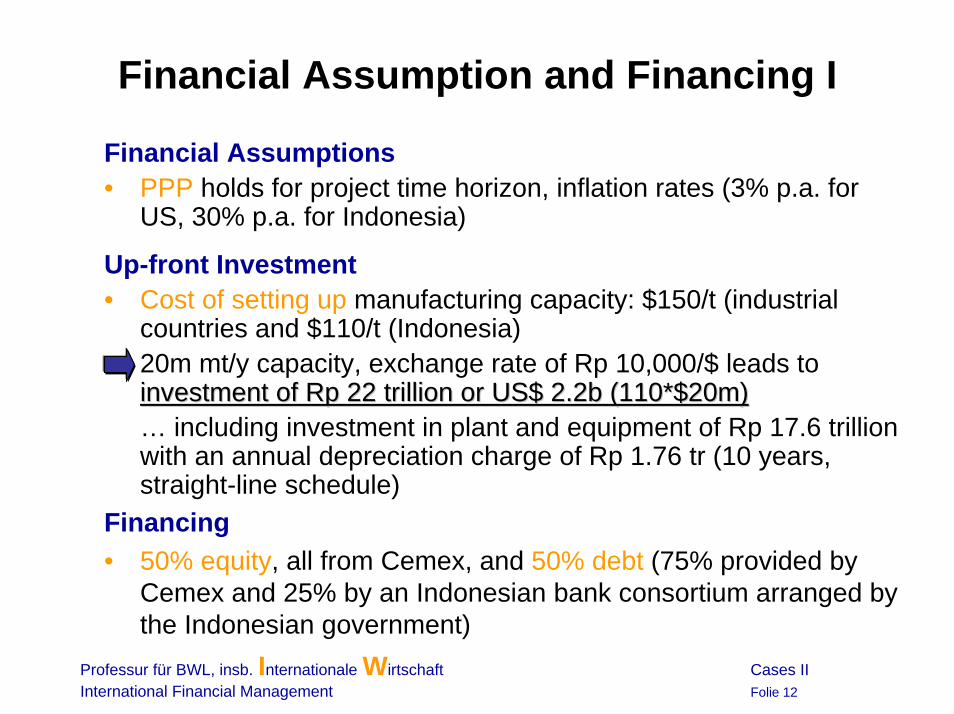

Financial Assumption and Financing I

Financial Assumptions• PPP holds for project time horizon, inflation rates (3% p.a. for

US, 30% p.a. for Indonesia)

Up-front Investment• Cost of setting up manufacturing capacity: $150/t (industrial

countries and $110/t (Indonesia)20m mt/y capacity, exchange rate of Rp 10,000/$ leads to investment of investment of RpRp 22 trillion or US$ 2.2b (110*$20m)22 trillion or US$ 2.2b (110*$20m)… including investment in plant and equipment of Rp 17.6 trillion with an annual depreciation charge of Rp 1.76 tr (10 years, straight-line schedule)

Financing• 50% equity, all from Cemex, and 50% debt (75% provided by

Cemex and 25% by an Indonesian bank consortium arranged by the Indonesian government)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 13

Financial Assumption and Financing IIFinancing (cnd)*• WACC

– Cemex US$ : 11.98%, – project WACC: 33.257%

• Indonesian loan: – 8 year maturity, fully amortizing– in Rupiah, 35% p.a. (fully deductible) interest

• Parent loan: – 5 year maturity– in US$, 10% (in PPP-rupiah terms: 38.835% calculated by

determining the internal rate of return of repaying the dollar loan in full in Rp)

• Debt Service schedule, cf.exhibit 18.3 (p.543)

* Given in the case, exh. 18.2, p.541

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 14

Pro Forma Income StatementRevenues• All sales are exports• Expected capacity utilization

Costs• Cash cost of manufacturing Rp 115,000/t for 1999 rising at the

rate of inflation (30% p.a.)• Additional production cost: Rp 20,000 also rising @30%• Loading cost of $2/t, shipping cost of $10/t rising @3%• License fees: 2% of sales• G&AE of 8% rising @1% p.a.

• Pro forma income statement to determine profitability• Break even expected in 3rd year of operation

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 15

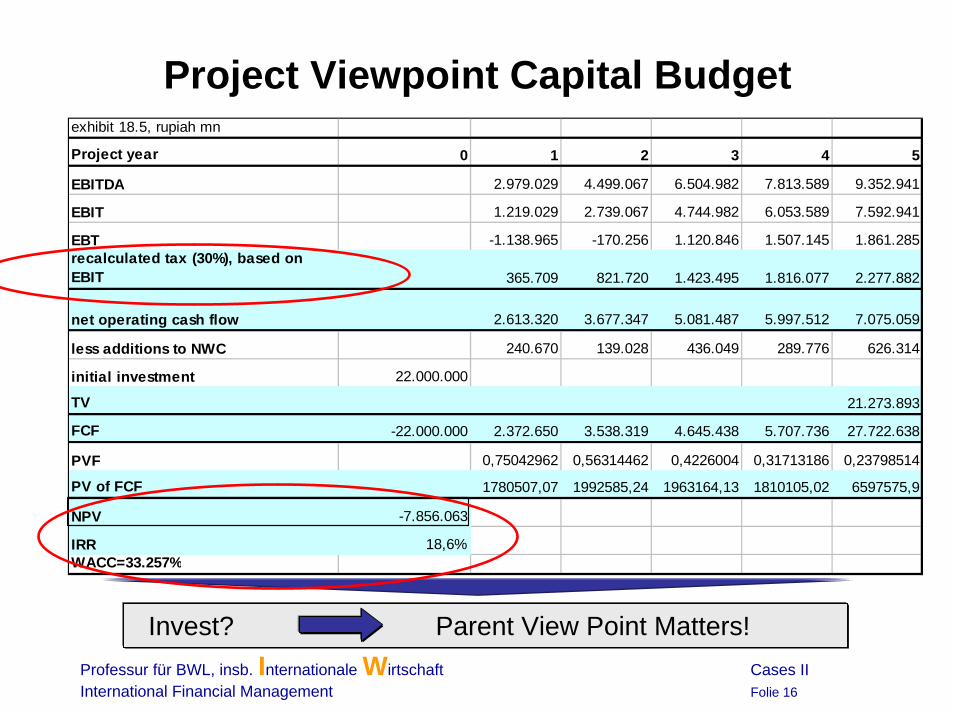

Project Viewpoint Capital BudgetNet Present Value and Internal Rate of Return• FCF = EBITDA – taxes + chg net working capital • Chg net working capital: Days sales outstanding (DSO)

– Receivables: 50-55 days, inventories: 65-70 days– Payables and trade credit: 114 days

• Initial capital investment: Rp 22m

• Terminal value– continuing value after year 5, i.e. perpetual net operating

cash flow (NOCF) generated in the fifth year

Net DSO: 15

trillionRpRpRpgk

gNOCFTVWACC

7.19000,000,686,19 033257.

)01( 059,547,6 )1(5 ==−

+=

−+

=

• WACC = 33.257%

Exh. 18.5

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 16

Project Viewpoint Capital Budgetexhibit 18.5, rupiah mn

PV of FCF 1780507,07 1992585,24 1963164,13 1810105,02 6597575,9

NPV -7.856.063

IRR 18,6%WACC=33.257%

Invest? Parent View Point Matters!

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 17

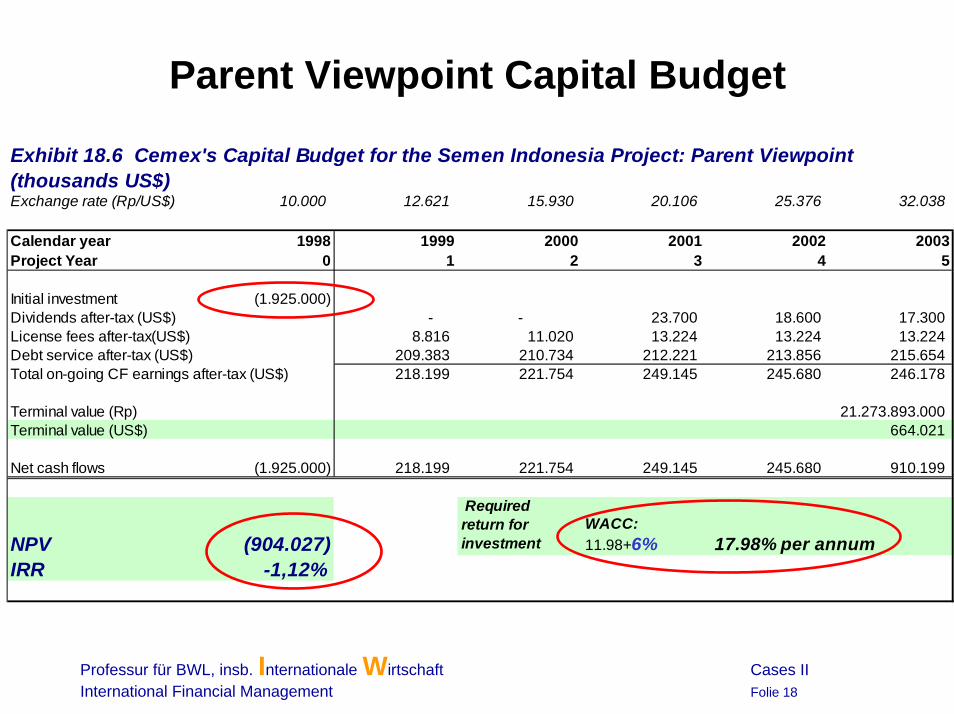

Parent Viewpoint Capital BudgetRepatriating Cash FlowsWhat counts are US$ cash in- and outflows, within project time horizon, after-tax, discounted at its appropriate WACC

Parent viewpoint capital budget build in two steps:

(1) individual cash flows are isolated, - adjusted for any withholding taxes, - and converted to US$ (not taxed again in MEX)

(2) Combine US$ after-tax cash-flows with the initial investment to determine NPV in the eyes of Cemex

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 18

Parent Viewpoint Capital Budget

Exhibit 18.6 Cemex's Capital Budget for the Semen Indonesia Project: Parent Viewpoint (thousands US$)Exchange rate (Rp/US$) 10.000 12.621 15.930 20.106 25.376 32.038

Calendar year 1998 1999 2000 2001 2002 2003Project Year 0 1 2 3 4 5

compensation for book vs market value, claim structure of debt repayments, nationality of creditors, ...)

– Tax consequences? “Nice clear expropriation” often better than “bleeding to death” in terms of accounting / write-offs (tax shield)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 21

F/X Risk and other Sensitivity FactorsF/X Risk• Depreciation assumption: PPP

Impact on revenues and operating exposureImported inputs more expensive off-set by export boost?!Natural hedge? Cash in- and outflows in $!

• Appreciation assumption: Positive impact on local sales but foreign competition might increase

Other Sensitivity Variables• Change in …

… assumed TV, capacity utilization rate, size of license fee, size of initial project cost, amount of WC financed locally, tax rates in Indonesia and Mexico, …

most of variables within control of CEMEX, project could be improved

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 22

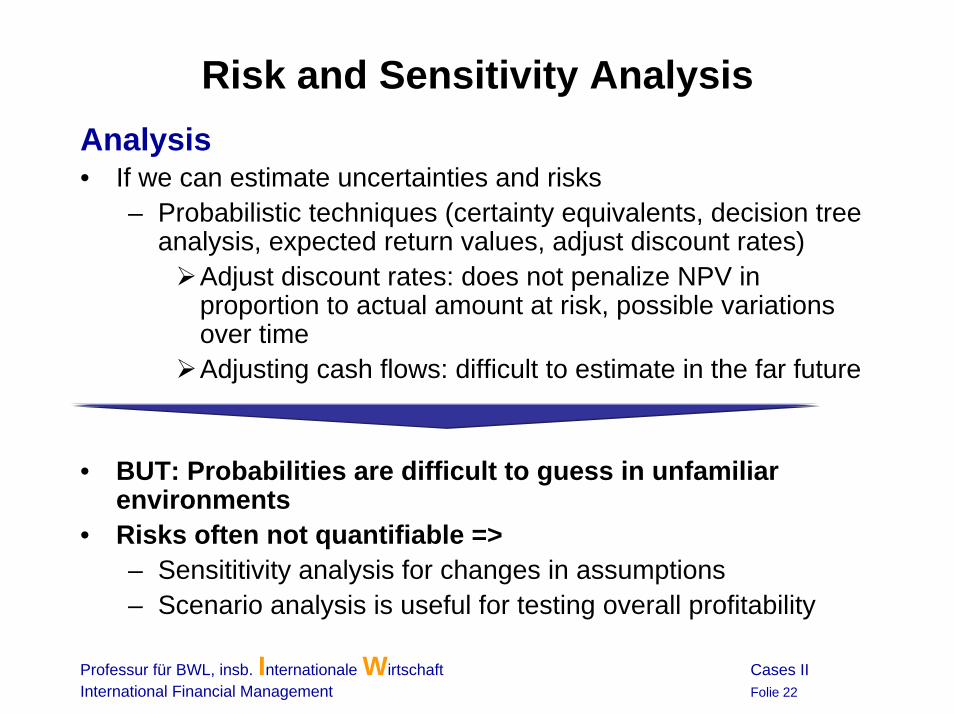

Risk and Sensitivity AnalysisAnalysis • If we can estimate uncertainties and risks

Adjust discount rates: does not penalize NPV in proportion to actual amount at risk, possible variations over timeAdjusting cash flows: difficult to estimate in the far future

• BUT: Probabilities are difficult to guess in unfamiliar environments

• Risks often not quantifiable => – Sensititivity analysis for changes in assumptions– Scenario analysis is useful for testing overall profitability

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 23

1. Overview 2. Multinational Capital Budgeting3. International Acquisitions & Valuation4. Lessons Learned From The Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 24

The FDI Decision Sequence

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 25

Global and Asian Merger and Acquisition Activity, 1990–1998

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 26

Indonesian Enterprises Slated for Privatization and Their Financial Partners

• Industries linked to infrastructure and natural resources industries• Semen Gresik one of the first privatization objects in Indonesia due to

good management, efficiency, resiliency in declining business conditions

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 27

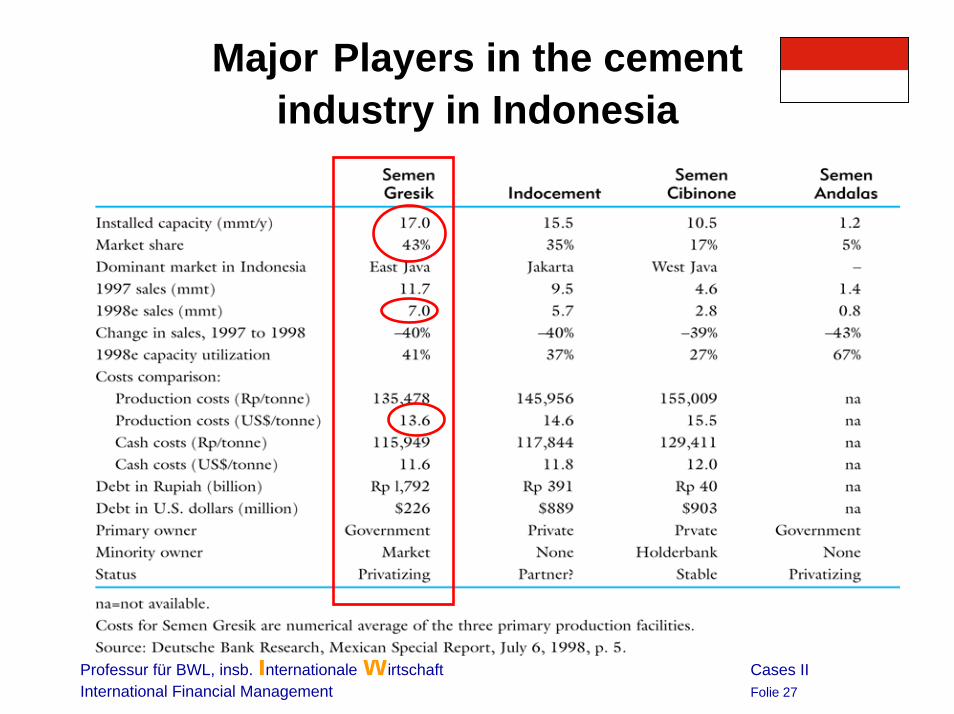

Major Players in the cement industry in Indonesia

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 28

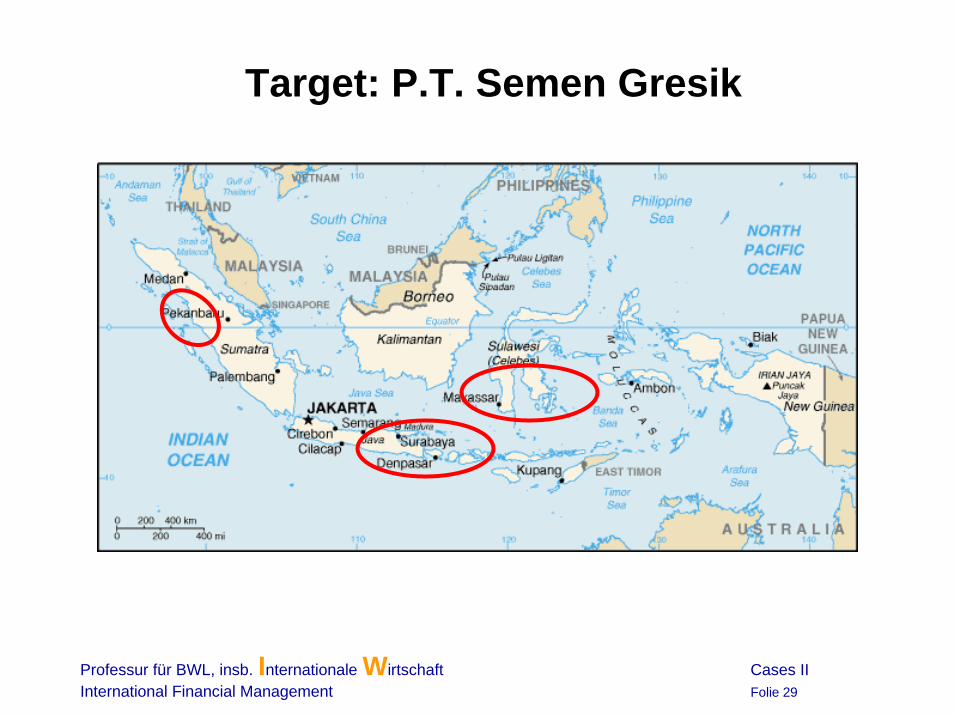

Target: P.T. Semen GresikCompany snap shot

• Public company (1957), • went public in July 1991 (free float: 35%)• Government-directed consolidation in 1995 through acquisition of

– Semen Pagang (West Sumatra) and – Semen Tonasa (South Sulawesi) – for a total of $476m

• Good shape: approx. 30% of installed capacity dates from 96/97• PTSG fought rising input costs

Now: privatization through partial sell-down (35% stake)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 29

Target: P.T. Semen Gresik

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 30

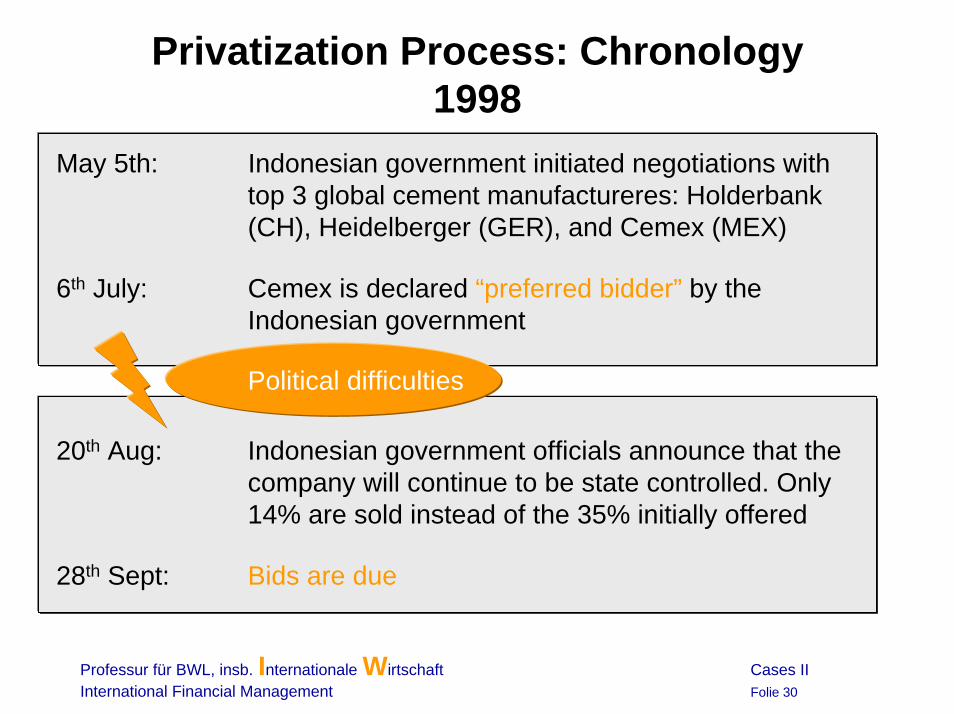

Privatization Process: Chronology1998

May 5th: Indonesian government initiated negotiations with top 3 global cement manufactureres: Holderbank (CH), Heidelberger (GER), and Cemex (MEX)

6th July: Cemex is declared “preferred bidder” by the Indonesian government

Political difficulties

20th Aug: Indonesian government officials announce that the company will continue to be state controlled. Only 14% are sold instead of the 35% initially offered

28th Sept: Bids are due

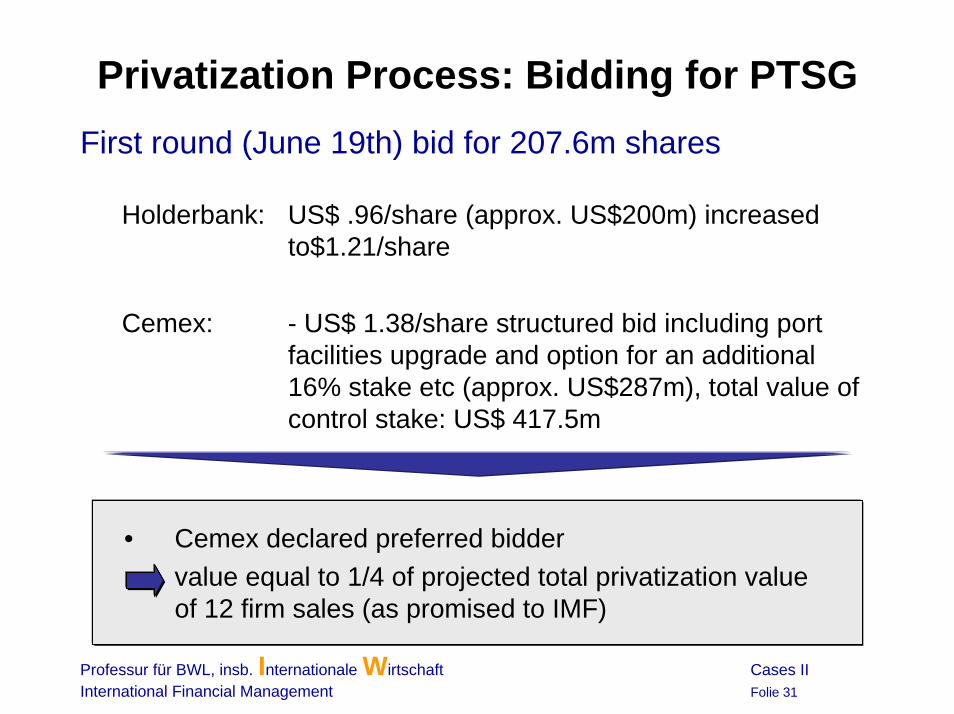

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 31

Privatization Process: Bidding for PTSG First round (June 19th) bid for 207.6m shares

Cemex: - US$ 1.38/share structured bid including port facilities upgrade and option for an additional 16% stake etc (approx. US$287m), total value of control stake: US$ 417.5m

• Cemex declared preferred biddervalue equal to 1/4 of projected total privatization value of 12 firm sales (as promised to IMF)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 32

Privatization Process: Political Difficulties

Growing political opposition• Due to falling employment levels and selling state-owned companies to

foreign investors

“Conflict of Interest”• Goldman Sachs obviously had a “conflict of interest” by advising both,

Cemex and the Indonesian government• GS withdrew as an advisor to Cemex - was replaced by Jardine Fleming

Insider Trading• Trading volumes in PTSG peaked on July 19th (bid submission day)• (finally unsuccessful) investigation into: Jardine Fleming, Bahana/GS,

and Danareksa Securities (state-controlled I-bank)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 33

Indonesia backs off – new bidding process initiated

Public opposition to Privatization• Fear of job cuts: demonstrations in West Sumatra and Jakarta

as rumors of sacking 3,000 employees circulated• Demonstrators paid by management of PTSG subsidiaries??

new bidding process

• reduction of the stake sold by the government to only 14% (goal: maintain control over PTSG)

• Restructured stage one bid is due on Sept 28

Now: new evaluation of the company

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 34

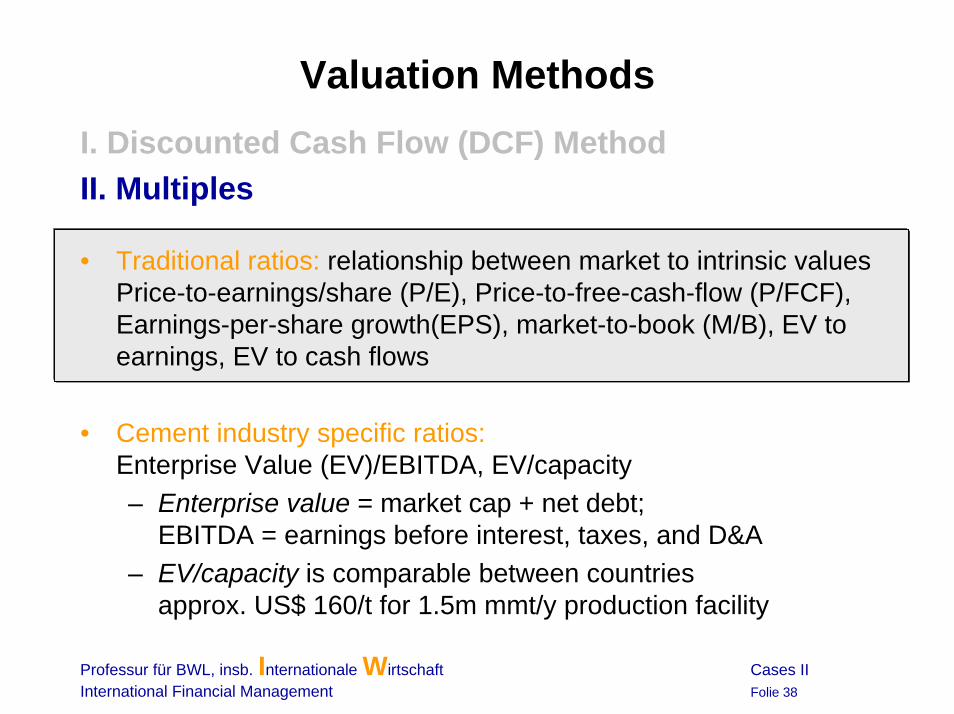

Valuation Methods

I. Discounted Cash Flow (DCF) Method• Free cash flows discounted with weighted average cost of capital

(WACC)

II. Multiples• Compare market value with some value derived of the company’s

financial statements• Compare to precedent transaction ratios or comparable firm ratios

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 35

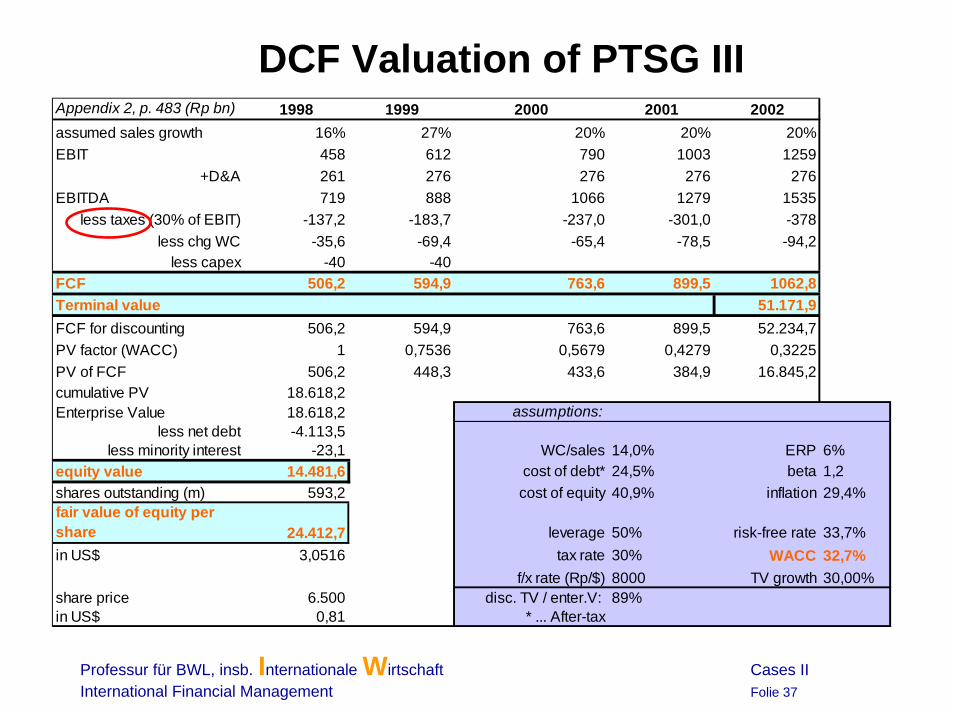

DCF Valuation of PTSG ISequential Valuation in order to obtain equity value• FCF = EBITDA – taxes + chg net working capital – capital expenditure • Including Terminal value• Discounted with WACC

• Traditional ratios: relationship between market to intrinsic valuesPrice-to-earnings/share (P/E), Price-to-free-cash-flow (P/FCF), Earnings-per-share growth(EPS), market-to-book (M/B), EV to earnings, EV to cash flows

• Cement industry specific ratios:Enterprise Value (EV)/EBITDA, EV/capacity– Enterprise value = market cap + net debt;

EBITDA = earnings before interest, taxes, and D&A– EV/capacity is comparable between countries

approx. US$ 160/t for 1.5m mmt/y production facility

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 39

Valuation of PTSG using Multiples I

i) P/E (Price/ earnings-per-share) Ratio• by far most widely used, often compared to market averages• indicates what the market is willing to pay for a unit of earnings• computation:

– current market price divided by Earnings-per-share

= 80 (as of Aug 28)Rp 10,500

Rp 78,000,000,000593,200,000 shares

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 40

Valuation of PTSG using Multiples II

ii) M/B (Market-To-Book) Ratio• Measure of market’s assessment of capital employed per share

versus what the capital costs• Computation:

– current share price divided by book value per share, here:(Rp 10,500/Rp4,123) = 2.55

• Comparable if not high (average =1, average M/B for six largest cement groups only 1.7)

• It is valued in excess of what stockholders invested in the firm

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 41

Valuation of PTSG using Multiples III

* p.475, March 1998

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 42

Synopsis of Market Entry Modes

1) Greenfield entry via “Semen Indonesia” (cf. Capital BudgetingSection): US$ -925.6m, IRR of –1.84%,

2) Acquisition of PTSG:• DCF: Fair equity value per share: Rp 24,412

$ 3.05

b) Multiples [country average in brackets]: EV/capacity = 80 [52] Price/FCF = 11.4 [9.2] M/B = 2.55 [n/a] P/E = 56, later 80 [9]

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 43

Major Issues in cross-border company valuation

Currency• What is the functional currency to value these assets? Rp? $?• If US$ is indeed the relevant currency of denomination a great

deal of share price volatility only reflected F/X volatility

Adjust for risk • Relative volatilities and correlations matter and have to be

analyzed on a case-to-case basis • Redoing DCF using adjusted WACC and forward rates (instead of

PPP-based exchange rateskWACC, adjusted < >17.98% (=11.98%+6%) ?!Risk-adjusted WACC is not a simple cost of capital plus 3% or 6% premium process!see chapter 18 appendix

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 44

Case Outcome: RealityNo one except Cemex filed a 2nd and final bid• Cemex acquired a 14% stake in PT Semen Gresik for $1.38/

share. • Cemex tendered market for add. 11.5% ($1.38/share).

Cemex: 25.5%, Government: 51%, Public: 23.5%total cost of $290 million for Cemex

Governance• mutual consent• Cemex will hold 2 seats on the Board of Directors and 2 seats

on the Board of Commissioners

Put optionGovernment holds the right to sell Cemex its 51% over 3 years –

price of $1.38/ share + 8.2% per annum Cemex would hold 71% of Semen Gresik and full control

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 45

The Case today: current developmentsPolitical level• Implementation of a regional autonomy law

– local administrations now demand control of their industries – late 2001: ownership of Semen Padang by the West

Sumatra government was proclaimed:- de-facto renationalization of the unit - legality was disputed by the central government

• Separatist tensions– Fear of separatist tensions in West Sumatra

• Foreign majority ownership in key industries– Foreign investors already control about 57% of Indonesian

cement production (if Cemex controlled Gresik: 93%)– No-no issue for certain politiciansGovernment backed down on the Cemex’ put option in 2001

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 46

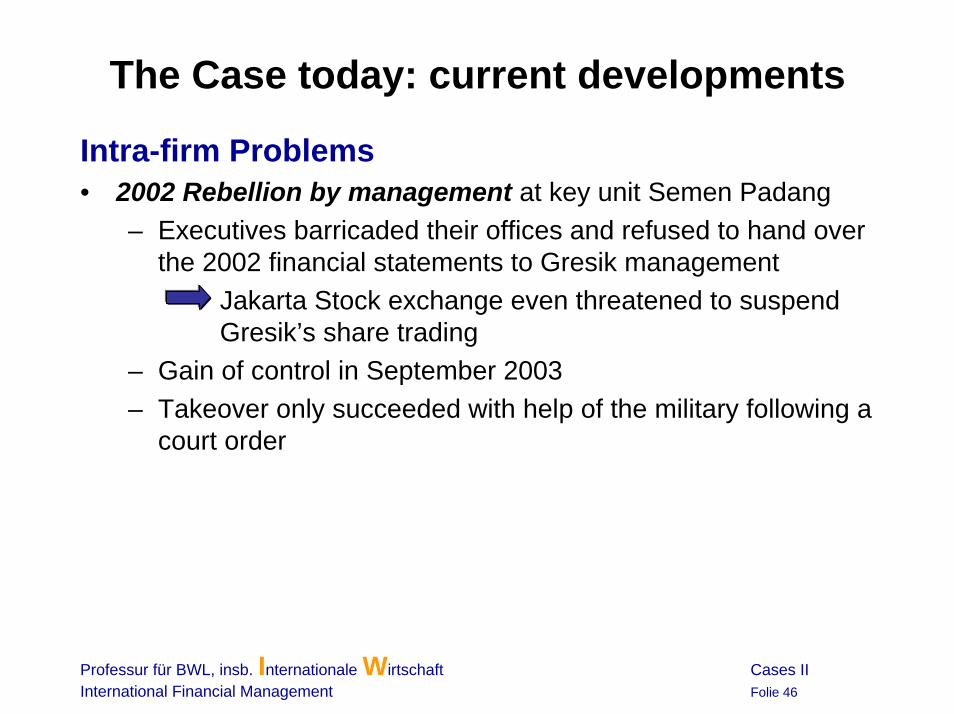

The Case today: current developments

Intra-firm Problems• 2002 Rebellion by management at key unit Semen Padang

– Executives barricaded their offices and refused to hand over the 2002 financial statements to Gresik management

Jakarta Stock exchange even threatened to suspend Gresik’s share trading

– Gain of control in September 2003– Takeover only succeeded with help of the military following a

court order

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 47

Consequences

Indonesian central government

• Government tried to find foreign investors for Cemex’s stake– BUT: investors were reluctant to commit themselves

Issue of legal ownership of Semen Panang is still not solved

Controlling majority necessary

• considered to raise money to buy-out Cemex

• Dec 2003: Cemex wanted to rescind the 1998 agreement – asked the International Center for the Settlement of Investment

Disputes (affiliate of the World Bank) to act as an arbiter– Wanted to be awarded substantial damages

• … but was still keen to increase its stake as originally planned – Cement demand on the increase in Indonesia

Cemex

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 48

May 2005

• Compromise plan: split-off of a Joint-venture in East Java to be controlled by CEMEX fails: Semen Gresik workers

opposed the deal

• 2005: according to Indonesian government CEMEX agreed to sell stake

“they agreed to use the proceeds from the stake sale to invest in Indonesia” (Aburizal Bakrie, Minister for Economic Affairs)

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 49

What happened then?

• ICSID: case is still pending 2006: Cemex wants to end the dispute

• March 2006: government will not be able to repurchase the stakes in PT Semen Gresik due to lack of funds, but “is still reviewing Cemex’s offer to acquire additional shares in Semen Gresik”

• March 2006: France’s Lafarge SA interested to buy the 25% from Cemex

• April 25, 2006: Cemex is about to sell stake to the Indonesian Rajawali Group – the deal only waits to be agreed upon by the government (team up with private equity firms, no intend to obtain majority stake)

• At the same time: Heidelberg Cement, Holcin with majority stakes in Indonesian cement manufacturers, the latter plan to build new plant in East Java, Lafarge SA new plant in Aceh

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 50

1. Overview 2. Multinational Capital Budgeting3. International Acquisitions & Valuation4. Lessons Learned From The Case

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 51

Lessons learned from the caseCapital Budgeting• NPV from parent viewpoint matters• Compare NPV from project viewpoint with similar venture

abroad• Use sensitivity analysis to analyze importance of assumptions

International M&A Strategy• Three components: (i) identification of target, (ii) execution,

(iii) post-merger integration• Use both, multiples and DCF• DCF: adjust CF or discount factor for risk

Professur für BWL, insb. Internationale Wirtschaft Cases IIInternational Financial Management Folie 52

Lessons learned from the caseAdjusting for Risk• Include possibilities of political disruptions or intervention,

restrictions, and regulations• Risks are qualitative not quantitative! Quantify prudently, use

case scenario analysis• Differentiate between project and parent perspective. Parent

perspective includes political, governance, transfer, and (residual) F/X risk (collectively referred to as country risk)