17

VIII Britcham International Seminar Mauro Andrade – [email protected] Petroleum Services, November 2008 Potential Impacts for the Brazilian Economy: Case study .

VIII Britcham International Seminar

Mauro Andrade – [email protected]

Petroleum Services, November 2008

Potential Impacts for the Brazilian Economy:

Case study .

2 ©2008 Deloitte. All rights reserved1-Dec-08

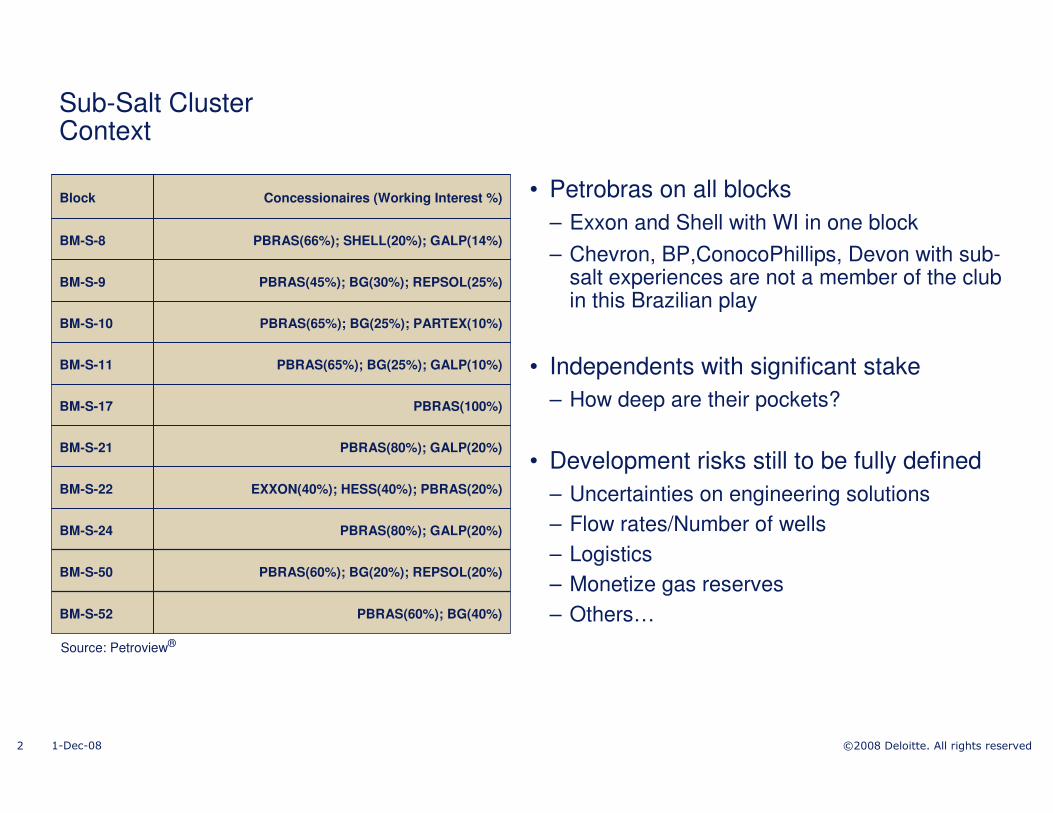

Sub-Salt ClusterContext

PBRAS(60%); BG(20%); REPSOL(20%)BM-S-50

PBRAS(80%); GALP(20%)BM-S-21

PBRAS(100%)BM-S-17

PBRAS(65%); BG(25%); GALP(10%)BM-S-11

PBRAS(45%); BG(30%); REPSOL(25%)BM-S-9

PBRAS(66%); SHELL(20%); GALP(14%)BM-S-8

PBRAS(65%); BG(25%); PARTEX(10%)BM-S-10

PBRAS(60%); BG(40%)BM-S-52

PBRAS(80%); GALP(20%)BM-S-24

EXXON(40%); HESS(40%); PBRAS(20%)BM-S-22

Concessionaires (Working Interest %)Block • Petrobras on all blocks

– Exxon and Shell with WI in one block

– Chevron, BP,ConocoPhillips, Devon with sub-salt experiences are not a member of the club in this Brazilian play

• Independents with significant stake

– How deep are their pockets?

• Development risks still to be fully defined

– Uncertainties on engineering solutions

– Flow rates/Number of wells

– Logistics

– Monetize gas reserves

– Others…

Source: Petroview®

3 ©2008 Deloitte. All rights reserved1-Dec-08

Source: Deloitte Petroleum Services

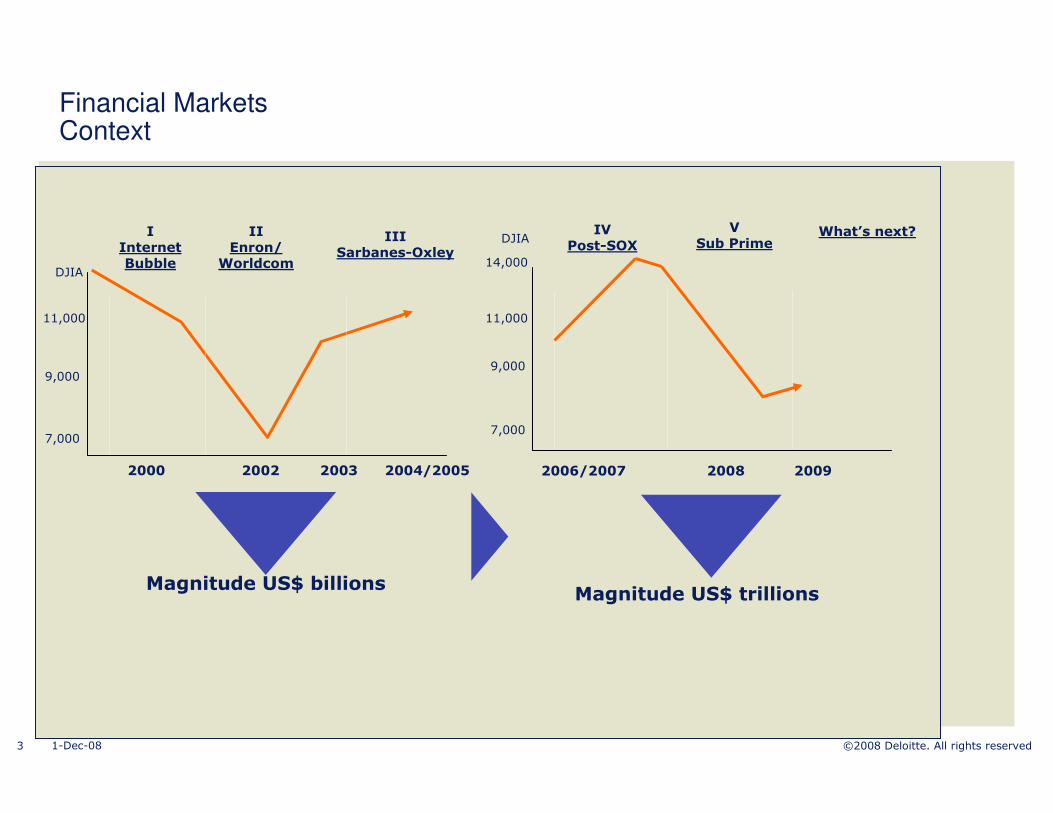

2000 2002 2003 2004/2005

7,000

11,000

9,000

DJIA

IIEnron/

Worldcom

IIISarbanes-Oxley

Magnitude US$ billions

IInternetBubble

2006/2007 2008 2009

7,000

11,000

9,000

DJIA

Magnitude US$ trillions

14,000

What’s next?VSub Prime

IVPost-SOX

Financial MarketsContext

4 ©2008 Deloitte. All rights reserved1-Dec-08

# of companies with interest in Sub-Salt Blocks in Selected Regions

Sub Salt Blocks Participants in Selected Areas

33

20

8

0

5

10

15

20

25

30

35

40

GOM West Africa Brazil

Source: Deloitte Petroleum Services

5 ©2008 Deloitte. All rights reserved1-Dec-08

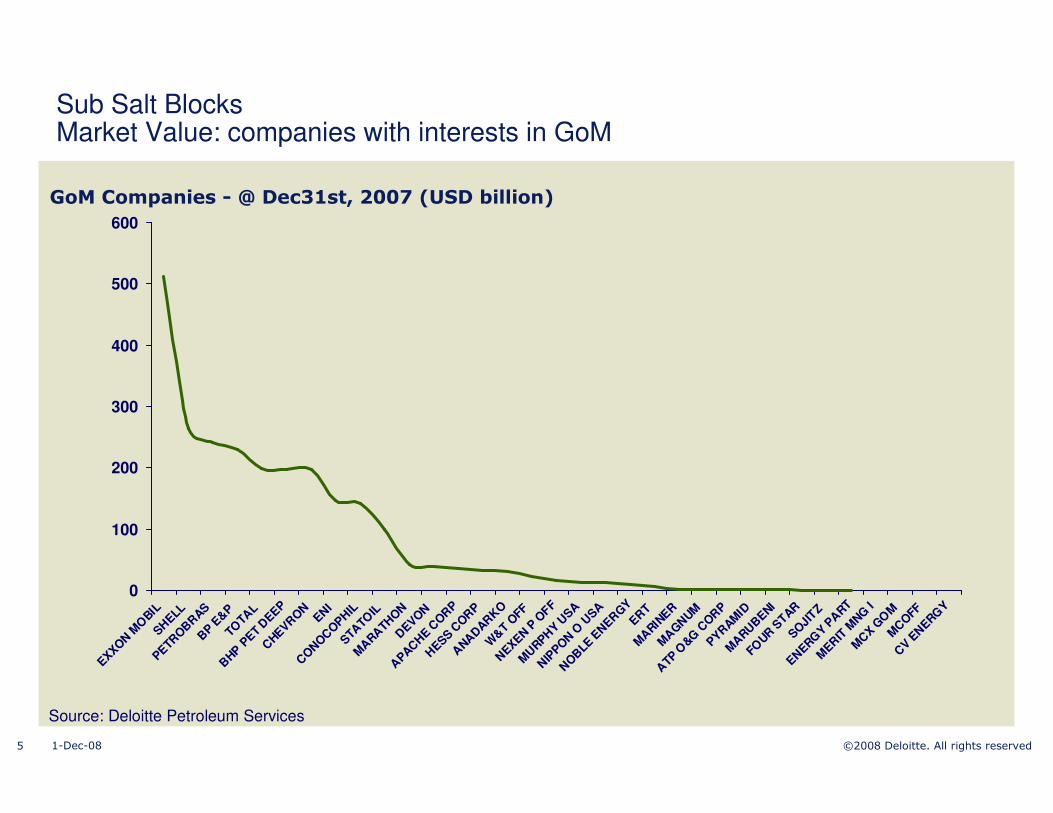

GoM Companies - @ Dec31st, 2007 (USD billion)

Sub Salt BlocksMarket Value: companies with interests in GoM

0

100

200

300

400

500

600

EXXON

MO

BIL

SHELL

PETRO

BR

AS B

P E&

P TO

TAL

BHP P

ET D

EEP

CHEVR

ON

ENI

CO

NO

CO

PHIL

STA

TOIL

MA

RATH

ON

D

EVON

APAC

HE C

OR

P

HESS C

OR

P

ANA

DAR

KO

W&

T O

FF

NEXEN P

OFF

MU

RPHY U

SA

NIP

PON

O U

SA

NO

BLE

EN

ERG

Y ER

TM

ARIN

ER

MA

GN

UM

ATP

O&G

CO

RP

PYRAM

IDM

ARU

BENI

FOUR

STAR

SO

JITZ

ENERG

Y PA

RT

MER

IT M

NG I

MC

X GO

M

MC

OFF

CV E

NERG

Y

Source: Deloitte Petroleum Services

6 ©2008 Deloitte. All rights reserved1-Dec-08

West Africa Companies - @ Dec31st, 2007 (USD billion)

Sub Salt BlocksMarket Value: companies with interests in West Africa

0

100

200

300

400

500

600

700

800

CH

INA

NA

T P

ET C

OR

P

EXX

ON

MO

BIL

CO

RP

SIN

OP

EC

CO

RP

PETR

ON

AS

BP

TO

TA

LC

HEV

RO

N

EN

I

AL T

HA

NI E

MIR

ATE

S

STA

TO

ILH

YD

RO

ASA

GA

Z D

E F

RA

NC

E

MA

RA

TH

ON

OIL

CO

RP

DO

MIN

ION

PETR

OLE

UM

GA

LP E

NE

RG

IATU

LLO

W O

IL P

LC

SU

DA

PET

SO

NA

NG

OL

PETR

OD

AR

RO

C O

IL

DA

NA

PE

TRO

LE

UM

Source: Deloitte Petroleum Services

7 ©2008 Deloitte. All rights reserved1-Dec-08

Companies in Brazil - @ Dec31st, 2007 (USD billion)

Sub Salt BlocksMarket Value: companies with interests in Brazil

0

100

200

300

400

500

600

700

800

EXXO

N MO

BIL

SH

ELL

PETRO

BR

AS

BG

GR

OUP

REP

SO

L-YP

F

HES

S C

OR

P

GA

LP

PAR

TEX

Source: Deloitte Petroleum Services

8 ©2008 Deloitte. All rights reserved1-Dec-08

So Far, So Good...So What?Funding the Oil Bonanza

• Finance investment needs can be an issue…

– Pace of developments (phased, modular, ??)

• Petrobras has USD 13 billion per year until 2012 to put the existing projects on stream

• Per our estimates a hyphotetical field in ultra-deep water with 5 bi boe of reserves wouldrequire US$ 50 billion capex

• Joint financial effort from all players

– Oil companies

– Suppliers

– Service Providers

9 ©2008 Deloitte. All rights reserved1-Dec-08

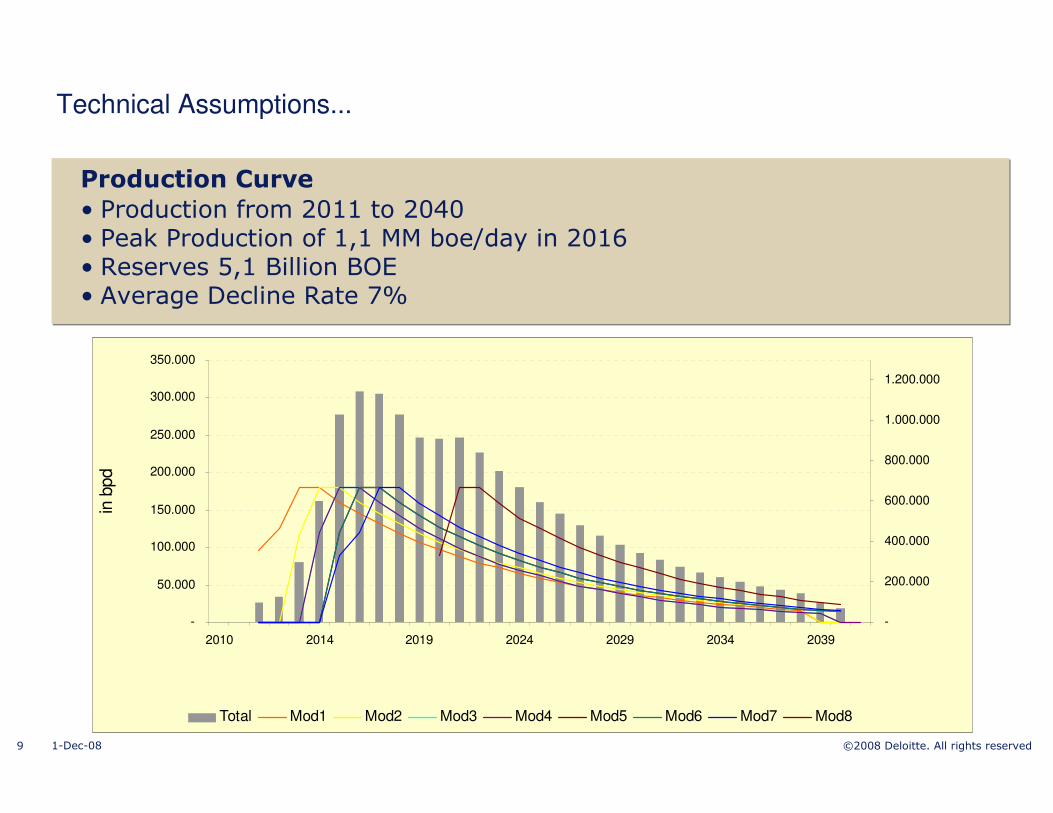

Production Curve

• Production from 2011 to 2040• Peak Production of 1,1 MM boe/day in 2016• Reserves 5,1 Billion BOE• Average Decline Rate 7%

Technical Assumptions...

-

50.000

100.000

150.000

200.000

250.000

300.000

350.000

2010 2014 2019 2024 2029 2034 2039

in b

pd

-

200.000

400.000

600.000

800.000

1.000.000

1.200.000

Total Mod1 Mod2 Mod3 Mod4 Mod5 Mod6 Mod7 Mod8

10 ©2008 Deloitte. All rights reserved1-Dec-08

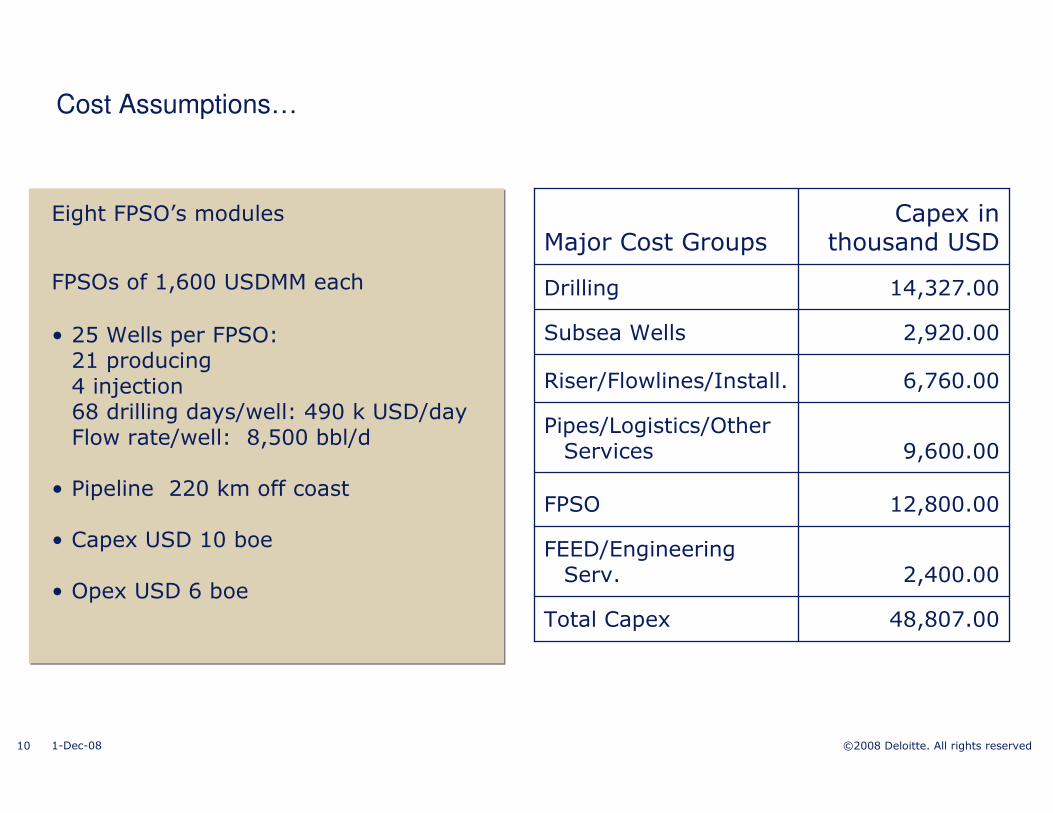

Cost Assumptions…

Eight FPSO’s modules

FPSOs of 1,600 USDMM each

• 25 Wells per FPSO:21 producing 4 injection68 drilling days/well: 490 k USD/dayFlow rate/well: 8,500 bbl/d

• Pipeline 220 km off coast

• Capex USD 10 boe

• Opex USD 6 boe2,400.00

FEED/Engineering Serv.

Capex in thousand USDMajor Cost Groups

48,807.00Total Capex

12,800.00FPSO

9,600.00Pipes/Logistics/Other Services

6,760.00Riser/Flowlines/Install.

2,920.00Subsea Wells

14,327.00Drilling

11 ©2008 Deloitte. All rights reserved1-Dec-08

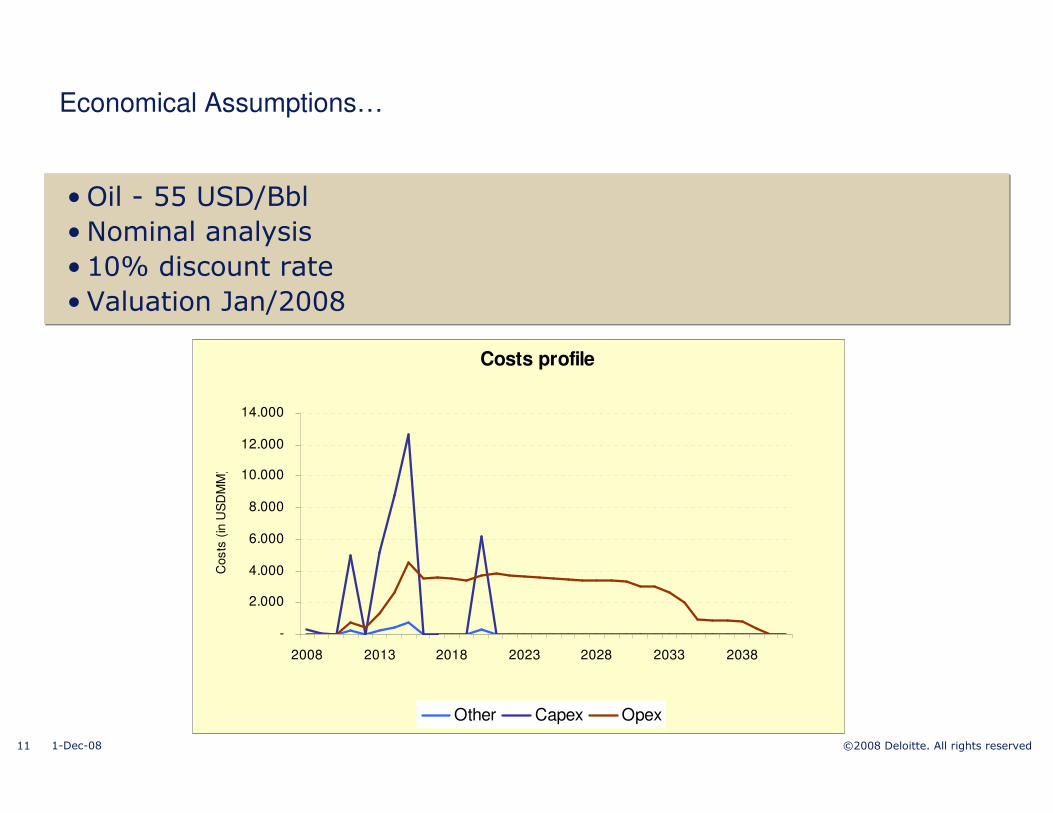

Economical Assumptions…

• Oil - 55 USD/Bbl

• Nominal analysis

• 10% discount rate

• Valuation Jan/2008

Costs profile

-

2.000

4.000

6.000

8.000

10.000

12.000

14.000

2008 2013 2018 2023 2028 2033 2038

Costs

(in

US

DM

M)

Other Capex Opex

12 ©2008 Deloitte. All rights reserved1-Dec-08

Case Study 1: Company leasing the FPSOs

Petroscope®

Economic Indicators & Cashflow Chart

Pre-Tax Post-Tax

NPV at 10% on 1 January 2008 (USDmm) 29.766,05 7.933,88

Internal Rate of Return 48,0% 18,2%PVI at 10% on 1 January 2008 2,5 1,4

Maximum Cash Exposure (USDmm) 24.142,04

Project Payback 2018,0 (7 years)

Discounted Project Payback at 10% 2019,0 (8 years)

-10000,0

-5000,0

0,0

5000,0

10000,0

15000,0

2008 2015 2022 2029 2036

US

Dm

m

-30000

-20000

-10000

0

10000

20000

30000

40000

50000

60000

US

Dm

m

Net Cashflow Cumulative Net Cashflow

13 ©2008 Deloitte. All rights reserved1-Dec-08

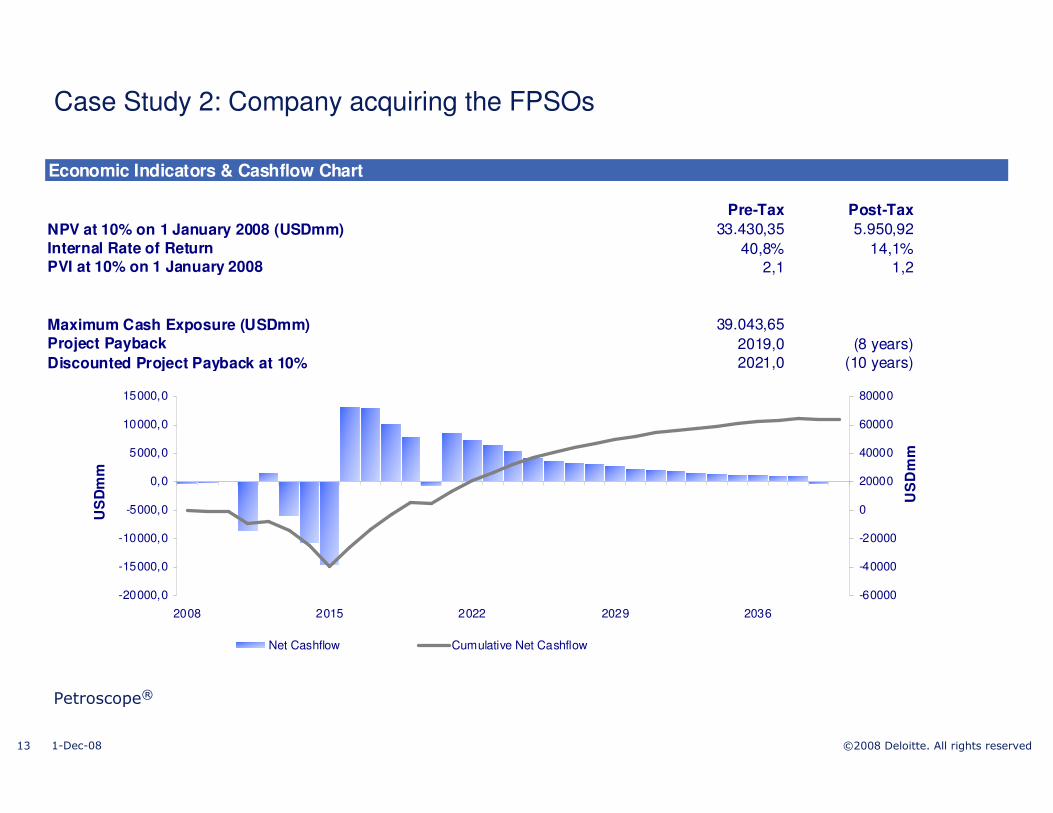

Case Study 2: Company acquiring the FPSOs

Petroscope®

Economic Indicators & Cashflow Chart

Pre-Tax Post-Tax

NPV at 10% on 1 January 2008 (USDmm) 33.430,35 5.950,92

Internal Rate of Return 40,8% 14,1%PVI at 10% on 1 January 2008 2,1 1,2

Maximum Cash Exposure (USDmm) 39.043,65

Project Payback 2019,0 (8 years)

Discounted Project Payback at 10% 2021,0 (10 years)

-20000,0

-15000,0

-10000,0

-5000,0

0,0

5000,0

10000,0

15000,0

2008 2015 2022 2029 2036

US

Dm

m

-60000

-40000

-20000

0

20000

40000

60000

80000

US

Dm

m

Net Cashflow Cumulative Net Cashflow

14 ©2008 Deloitte. All rights reserved1-Dec-08

Discounted Per barrel analysis (@ 10%)

Petroscope®

Case 1 (lease & tax optimization) Case2 (acquisition)

11%

32%

19%

31%

7%

PV Opex PV Capex

PV Government Take PV Taxation

PV Net Cashflow

USD/boe

PV Gross Revenue 16,23

PV Opex 1,73

PV Capex 5,32

PV Government Take 3,07

PV Taxation 5,01

PV Net Cashflow 1,09

23%

23%20%

25%

9%

PV Opex PV Capex

PV Government Take PV Taxation

PV Net Cashflow

USD/boe

PV Gross Revenue 16,23

PV Opex 3,79

PV Capex 3,73

PV Government Take 3,28

PV Taxation 3,98

PV Net Cashflow 1,45

15 ©2008 Deloitte. All rights reserved1-Dec-08

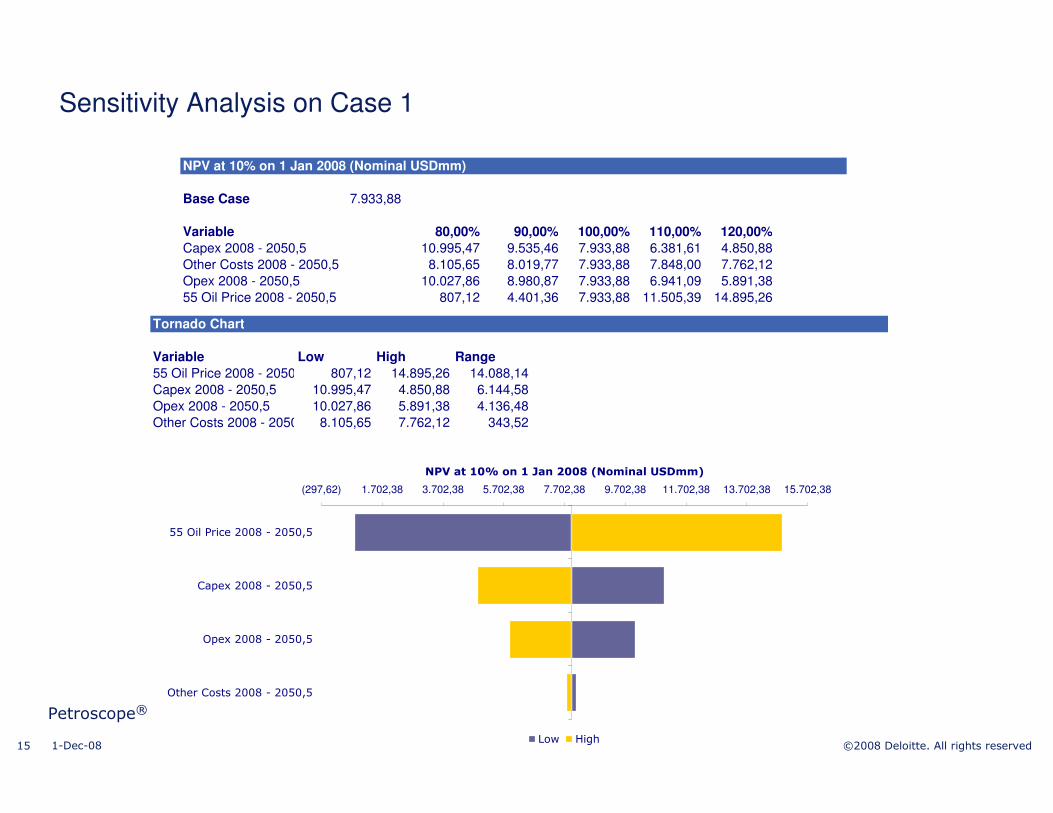

Sensitivity Analysis on Case 1

Petroscope®

NPV at 10% on 1 Jan 2008 (Nominal USDmm)

Base Case 7.933,88

Variable 80,00% 90,00% 100,00% 110,00% 120,00%

Capex 2008 - 2050,5 10.995,47 9.535,46 7.933,88 6.381,61 4.850,88

Other Costs 2008 - 2050,5 8.105,65 8.019,77 7.933,88 7.848,00 7.762,12

Opex 2008 - 2050,5 10.027,86 8.980,87 7.933,88 6.941,09 5.891,38

55 Oil Price 2008 - 2050,5 807,12 4.401,36 7.933,88 11.505,39 14.895,26

Tornado Chart

Variable Low High Range

55 Oil Price 2008 - 2050,5 807,12 14.895,26 14.088,14

Capex 2008 - 2050,5 10.995,47 4.850,88 6.144,58

Opex 2008 - 2050,5 10.027,86 5.891,38 4.136,48

Other Costs 2008 - 2050,5 8.105,65 7.762,12 343,52

(297,62) 1.702,38 3.702,38 5.702,38 7.702,38 9.702,38 11.702,38 13.702,38 15.702,38

55 Oil Price 2008 - 2050,5

Capex 2008 - 2050,5

Opex 2008 - 2050,5

Other Costs 2008 - 2050,5

NPV at 10% on 1 Jan 2008 (Nominal USDmm)

Low High

16 ©2008 Deloitte. All rights reserved1-Dec-08

Conclusions

• Under the current macroeconomic scenario finance the investments will be challenging

• Accessing cost competitive reserves is an important piece of the equation

– Would allow proper finance and the management of the risks associated with projects of such massive magnitude

• Debates over an eventual “Oil Bonanza” must ensure a fair regulatory framework

– Government wants to maximize returns from its resources, but has to ensure a fair balance

• Ensure an internationally competitive taxation system is key to attract foreign investment that will help to develop the resources

– In any given regulatory framework

17 ©2008 Deloitte. All rights reserved1-Dec-08

Deloitte provides services in audit, tax, risk management, corporate finance, consulting, outsourcing, human capital management and actuarial consulting to clients spanning multiple industries. With a global network of member firms in more than140 countries, Deloitte brings world class capabilities and deep local expertise to help clients succeed the best performance, wherever they operate.

Deloitte's 165,000 professionals are committed to becoming the standard of excellence and they are unified by a collaborative culture that fosters integrity, outstanding value to markets and clients, commitment to each other, and strength from diversity. They enjoy an environment of continuous learning, challenging experiences, and enriching career opportunities. Deloitte's professionals are dedicated to strengthening corporate responsibility, building public trust, and making a positive impact in their communities.

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms.

This presentation does not constitute tax, legal or other advice from Deloitte, which assumes no responsibility with respect to assessing or advising the

reader as to tax, legal, or other consequences arising from the reader’s particular situation.

![Advising Manual 2016-2017 - Monfort College of Businessmcb.unco.edu › pdf › advising › MCB-Advising-Manual-2016-2017.pdf · Advising Manual 2016-2017. 2 [AdvisingManual] 3 ...](https://static.documents.pub/doc/80x56/5f1169150273b0207c355cff/advising-manual-2016-2017-monfort-college-of-a-pdf-a-advising-a-mcb-advising-manual-2016-2017pdf.jpg)