Videsh Sanchar Nigam Ltd. (VSNL) Disinvestment in Videsh Sanchar Nigam Ltd. 1.The Government has approved sale of 25% equity share holding out of a total government shareholding of 52.97% in Videsh Sanchar Nigam Ltd. (VSNL) on 5 th February 2002. The total paid-up capital of VSNL is Rs. 285 crore, the Government holding being Rs. 151crore. Rs. 71.25 crore of this equity is being sold to M/s Panatone (Tata Group) at a p rice of Rs. 1,439 crore. 2.The Government had decided to disinvest in VSNL in January 2001 and the advertisement forinviting Expression of Interest was issued in February 2001. Several interested parties had submitted their Expressions of Interest. After the process of due diligence was completed and the transaction documents frozen, financial bids were invited from the bidders on 1 st February 2002. Two bids were received. 3.SBI Capital Markets Ltd. and CSFB were appointed as the advisors at a fee of 0.19% of the transaction value. M/s Crawford Ba yley & Co. is the legal advisor an d the asset valuer is Pricewaterhouse Coopers Ltd. After considering the Advisor's report, the Evaluation Committee/IMG/CGD submitted their recommendations regarding acceptance of the higher bid to the CCD. 4.The Government has in the process of disinvestment in VSNL received approximately Rs. 3,689 crore, Rs. 1,439 crore as the bid price, Rs. 1,887 crore as dividend and Rs. 363 crore as dividend tax. Thus, the Government has sold its shares at a price of Rs. 202 per share, taken additional amount as dividend, special dividend and dividend tax. Besides, the Government has also taken measures to take out surplus, yet very valuable land (value Rs. 778 crore) from VSNL, and also restrict use/sale of land through provisions in transaction documents. 5.The market price of VSNL shares as on 1 st February 2002 was Rs. 158 per share. The Government had earned Rs. 10.4 crore per year on 25% of its equity in the last eight years. This year the Government has earned Rs. 3,689 crore from sale of VSNL and if this money is kept in the bank it would earn an interest of 368.9 crore, i.e., the Government would gain more than Rs. 350 crore every year. 6.The strategic partner had was provided a call option for the fifth year subject to the condition that the Government would be retaining at least one share and hence one vote position to enforce its affirmative vote on assets. In addition, 1.97% share was given to employees at concessional rates.

1. The Government has approved sale of 25% equity share holding out of a total government

shareholding of 52.97% in Videsh Sanchar Nigam Ltd. (VSNL) on 5th

February 2002. The total

paid-up capital of VSNL is Rs. 285 crore, the Government holding being Rs. 151crore. Rs. 71.25

crore of this equity is being sold to M/s Panatone (Tata Group) at a price of Rs. 1,439 crore.2. The Government had decided to disinvest in VSNL in January 2001 and the advertisement for

inviting Expression of Interest was issued in February 2001. Several interested parties had

submitted their Expressions of Interest. After the process of due diligence was completed and thetransaction documents frozen, financial bids were invited from the bidders on 1

stFebruary 2002.

Two bids were received.

3. SBI Capital Markets Ltd. and CSFB were appointed as the advisors at a fee of 0.19% of the

transaction value. M/s Crawford Bayley & Co. is the legal advisor and the asset valuer isPricewaterhouse Coopers Ltd. After considering the Advisor's report, the Evaluation

Committee/IMG/CGD submitted their recommendations regarding acceptance of the higher bid

to the CCD.

4. The Government has in the process of disinvestment in VSNL received approximately Rs. 3,689crore, Rs. 1,439 crore as the bid price, Rs. 1,887 crore as dividend and Rs. 363 crore as dividend

tax. Thus, the Government has sold its shares at a price of Rs. 202 per share, taken additional

amount as dividend, special dividend and dividend tax. Besides, the Government has also takenmeasures to take out surplus, yet very valuable land (value Rs. 778 crore) from VSNL, and also

restrict use/sale of land through provisions in transaction documents.

5. The market price of VSNL shares as on 1st

February 2002 was Rs. 158 per share. The

Government had earned Rs. 10.4 crore per year on 25% of its equity in the last eight years. Thisyear the Government has earned Rs. 3,689 crore from sale of VSNL and if this money is kept in

the bank it would earn an interest of 368.9 crore, i.e., the Government would gain more than Rs.

350 crore every year.6. The strategic partner had was provided a call option for the fifth year subject to the condition that

the Government would be retaining at least one share and hence one vote position to enforce its

affirmative vote on assets. In addition, 1.97% share was given to employees at concessionalrates.

16. The new management had assured that revision of pay scales would be implemented within 30

days of their becoming strategic partners and that they would finalise the modalities of payment

of arrears within 90 days. The new management has implemented the revised wages w.e.f.March 2002. The revision would mean:

Average increase of Rs. 2,789 per month for 1,140 regular employees

Average salary to go up from Rs. 9,360/- to Rs. 12,419per month (increase of about 28.74%) Additional financial burden of Rs. 31.61 lakh per month (approx. Rs. 3.79 crore per annum)

17. Since inception, PPL‟s plants had produced raw material at 40% of plant capacity which are nowworking at 110% capacity. The production of fertiliser has gone up from 20,000 metric tonnes to

70,000 metric tonnes in May-June 2002, which is 120% of rate capacity.

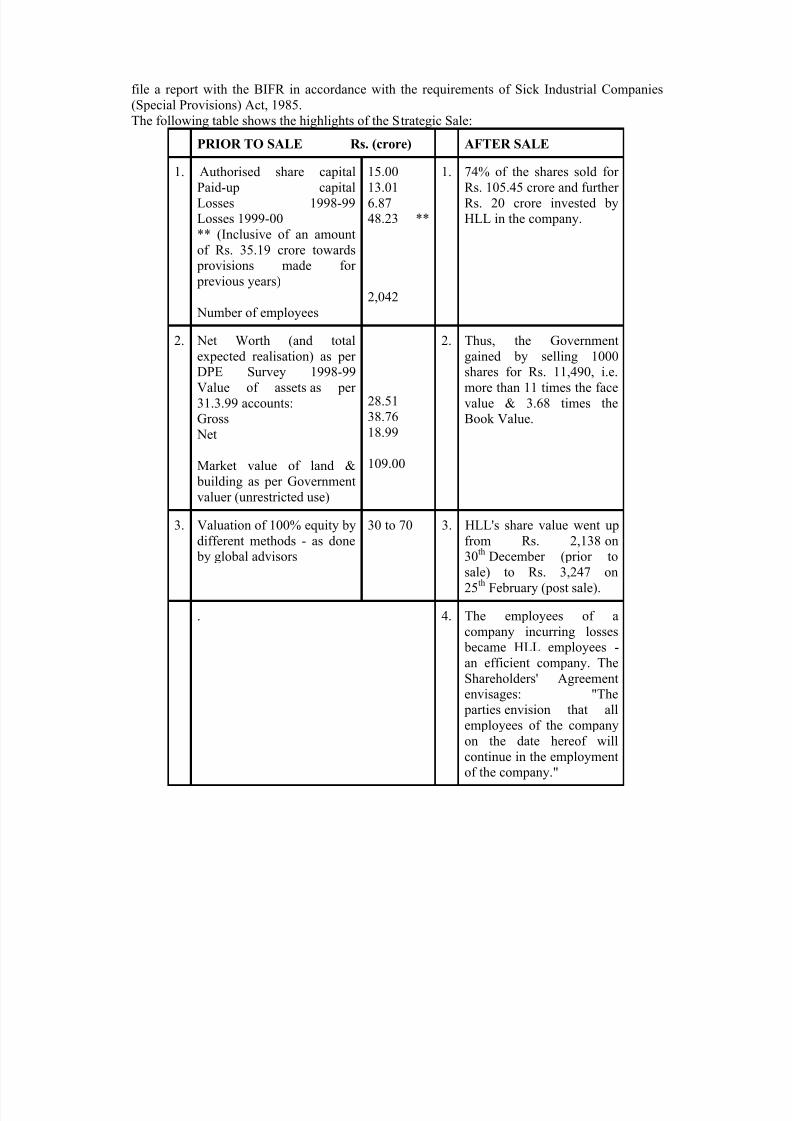

Modern Food Industries Ltd.

Modern Food Industries Ltd. was incorporated as Modern Bakeries ( India ) limited in 1965. It

had 2,042 employees as on 31st

January 2000. It went through minor restructuring during 1991-

94 when its Ujjain plant was closed, the Silchar project was abandoned and the production of Rasika drink was curtailed. The company was referred to the Disinvestment Commission in

1996. In February 1997, the Commission recommended 100% sale of the company, treating it in

the non-core sector. While making this recommendation, the Disinvestment Commission cited

underutilisation of the production facilities, large work force, low productivity and limitedflexibility in decision-making, as some of its weaknesses.

In September 1997, the Government approved 50% disinvestment to a Strategic Partner through

competitive global bidding. In October 1998, ANZ Investment bank was appointed as the GlobalAdvisor for assisting in disinvestment. In January 1999, the Government decided to raise the

disinvestment level to 74%, and an advertisement, inviting Expression of Interest from the

prospective Strategic Partners, was issued in April 1999.

Pursuant to the advertisement and other marketing efforts by the Advisor, 10 parties submittedExpressions of Interest. Out of these, only 4 conducted the due diligence of the company, which

included visits to Data Room, interaction with the management of the MFIL, and site visits.

After due diligence, only 2 parties remained in the field, and on the last day for submission of the

financial bid (15th

October 1999), the only bid received was that from Hindustan Lever Limited(HLL). The Government approved the selection of HLL as the Strategic Partner in January 2000,

and the deal was closed on 31st January 2000.As per the accounting procedure prior to disinvestment (31

stJanuary 2000), MFIL did not make

any provisions for old receivables outstanding for more than 5 years. After privatisation, the new

management provided for all outstanding receivables that were over 3 years old, on the ground

that it was warranted by the strict application of the accepted accounting principles. The revisedaccounts, thus prepared, showed an accumulated loss of Rs. 3,099.97 lakh, and Net Worth of Rs.

201 lakh. Since the Net Worth of the company got eroded by more than 50% of its peak Net

Worth (Rs. 1,756.79 lakh) during the immediately preceding four financial years, MFIL had to

Post - Privatisation Scenario The decline in the sales of Modern Bread, which continued till the beginning of 2000, has

been arrested. Weekly sales in December 2000 were around 44 lakh SL, which is a 100%increase over the figure of April 2000

As on 31st

December 2000, HLL has extended secured corporate loans to MFIL to the extent

of Rs. 16.5 crore for meeting the requirement of funds for working capital and capitalexpenditure

HLL has provided a corporate guarantee to MFIL's banker, viz., Punjab National Bank, which

has helped the Company in getting the interest rate reduced considerably to the extent of 3-4%

of its earlier borrowing cost

Steps have been taken to improve the quality of bread, its packaging and marketing withtrade-promotion activities, and to train the manpower in quality control systems

November 2002 wages have increased by an average of Rs.1,800 per employee

Rs. 30 crore has been spent on VRS and Rs. 7 crore infused for safety & hygiene purposes at

various manufacturing locations

The Government was also entitled to „Put‟ its share of remaining equity of 26% at Fair Market

Value for 2 years from 31st

January 2001 to 30th

January 2003. The Government hasd

exercised this option and thereby received Rs. 44.07 crore on 28th

November 2002

Maruti Udyog Ltd. (MUL)

1. On 14th May 2002, the Government approved disinvestment in Maruti Udyog Ltd. through atwo-stage process:

A rights issue of Rs. 400 crore by MUL in the first phase with the Government renouncing itsrights shares to Suzuki. Suzuki would gain majority control and pay Rs. 1,000 crore to the

Government as control premium.

Sale of its existing shares through a public issue in the second phase; the issue to be

underwritten by Suzuki.

Highlights of the Agreement reached 2. The highlights of the agreement reached between the Negotiating Teams of the GOI and

Suzuki are summarised below:

The total value of the rights issue would be Rs. 400 crore

The rights issue price would be Rs. 3,280 per share. Thus, the rights issue would be for a totalof 12,19,512 shares of Rs. 100 each

The fair value for the purpose of working out renunciation premium would be the average of

the 3 values indicated above, i.e., Rs. 3,280 per share

GOI will renounce the whole of its rights share of 6,06,585 shares and Suzuki will subscribe

to the whole of the rights shares so renounced by GOI at the fair market value

Suzuki would, through this method and those spelt out below, enhance the value of MUL and

Suzuki will pay a control premium of Rs.1,000 crore to GOI, without GOI parting with even a

single of its shares in MUL

Suzuki and GOI have agreed to enter into a Revised Joint Venture Agreement (JVA). The

Revised JVA shall constitute the entire agreement between GOI, Suzuki and MUL with

respect to the subject matter of the Revised JVA and any prior understanding and agreements between the Parties with respect to such subject matter shall be superseded

Suitable amendments in the Memorandum and Articles of Association of MUL would be

carried out to bring them in line with the decisions recorded above and also to enable the

listing of MUL shares on the stock exchange

The Revised JVA envisages that GOI would sell its existing shares in the domestic market

with participation of Indian and Global investors as permitted by law after the completion of

the rights issue transaction

Suzuki has agreed to underwrite the first public issue of approximately 36 lakh shares held byGOI at a price of Rs. 2,300 per share. For the balance shares, GOI has a „put‟ option at a

discount of 15% and/or 10% of average market price. GOI always has a „put‟ option up to

30

th

April 2004 at the book value now (Rs. 2,000) or then, whichever is higher 3. Since the rights issue will be of a size of 12,19,512 shares, the relative shareholding of Suzuki

and GOI after completion of the rights issue would be 54.20% and 45.54% respectively.

4. The price per share that emerges now is Rs. 3,684, which should be compared to the value per share that would be arrived at if the formula agreed to between Suzuki and GOI in the

1992 agreement were to be used. Using that formula the price per share works out to Rs. 1,153

based on the provisional figures for the latest year i.e., 2001-02.

Achieved in Constraints 5. Because of the earlier agreement, GOI‟s negotiating position has all along been highly

disadvantageous because of the following constraints:

The clause in the existing agreement that SUZUKI‟s consent is required for GOI to transfer itsshare

In the earlier transactions with SUZUKI in 1982 and 1992, when Suzuki‟s shareholding was

allowed to be increased (vis-a-vis GOI), first from 26% to 40% and then from 40% to 50%,no control premium had been paid by Suzuki, though control had passed to them. As a matter

of fact, the Government received no payment at this

stage as shareholding was allowed to be increased by issuance of new shares to MUL. Exitoptions were also not built in

The pricing formula in 1992 also yielded a low price per share of Rs. 269 at which the

transaction was done

Using the same formula of 1992 now, the price per share would be Rs.1,153 as stated above.As against this, the current transaction would be at a minimum of Rs. 3,684 assuming

undertaking at Rs. 2,300

If we examine the rights issue alone, the new shares are being allotted to Suzuki at Rs.

3,280 against Rs. 269 in the last transaction(equivalent value Rs.1153). Also, against „nil‟ control premium last time, the GOI is being paid Rs. 1,000 crore as control premium

Suzuki already has 50% control in the company and GOI in a minority position at 49.74%

An atmosphere of distrust between the two sides, due to the previous arbitration case beingcontested by both sides during 1997

6. Suzuki‟s initial offer was of Rs. 170 crore as control premium, which was increased to Rs.

286 crore after considerable negotiations. Thereafter, it took the negotiating team over a month

to negotiate a sum of Rs. 1,000 crore presently offered by Suzuki.

7. Similarly, initially Suzuki was totally reluctant to incorporate any underwriting of the

public issue by GOI shares. SUZUKI has now agreed to underwrite the public issue of the36,12,169 existing shares at Rs. 2,300 per share and the balance 29,68,012 at a minimum of the present book value of about Rs. 2,000 per share. Once MUL is listed, and when GOI goes for a

public issue with full backing of Suzuki, the share prices are likely to be above the book value.

This would mean higher receipts to GOI.

Analysis of the Deal 8. The MUL disinvestment is unique in nature as compared to the other strategic sale transactions

completed so far such as VSNL, BALCO, HZL, CMC, etc. Therefore, this transaction would

have to be judged using different methods as discussed below.

9. Comparison with other disinvestment cases: Since MUL is not a listed company, both sides had

agreed to determine the fair value of MUL shares through valuation by three independentvaluers. This average value worked out to Rs. 3,280 per share. Therefore, the value of

Government‟s existing 65,80,181 shares works out to approximately Rs. 2,158 crore based on

this fair value. What Government is receiving from Suzuki now is Rs. 1,000 crore as control

premium and considering the undertaking at Rs. 2,300 per share for the 36 lakh shares and Rs.2,000 per share for the balance approximately 29 lakh shares, it would be an additional amount

of Rs. 1,424 crore for the existing shares. If the existing shares could be sold at more than the

present book value, GOI‟s receipt would further go up. Thus, the GOI will, at a minimum, getout of the transaction of handing over the control and selling its existing shares forRs. 2,424

crore, which is Rs. 266 crore above the fair value of Rs. 2,158 crore mentioned above. If we

compare this with similar figures of earlier transactions it would be seen that the present

transaction is even better than what has been possible in them.

10. Suzuki already has 50% shares in MUL and control and management rights which were more

than equal as per earlier agreements. This was due to their being technology suppliers. In other cases of disinvestment, the strategic partner does not have any control before acquiring GOI

shares but acquires control only after the strategic sale. Thus, the control premium presently

offered by Suzuki should be viewed in this background.

11. Annual Cash Inflows to the Government: Currently, GOI receives dividend on its shareholding.

The dividend received by GOI in the past several years has been about Rs.13-20 crore per

annum. In the year 2000-01, MUL did not declare any dividend. In case this transaction iscompleted, GOI would receive Rs.1,000 crore upfront which would yield interest of Rs. 100

crore per annum at the conservative rate of 10%. Added to this would be the dividend on the

existing shares, even if Government does not sell these shares. If it sells the shares then GOI

would receive a minimum of Rs. 142 crore per annum (at the rate of 10%) on the balance receiptof Rs. 1,424 crore as indicated above. Thus, the minimum annual yield to GOI would be Rs. 242

crore against the present dividend level of Rs. 13-20 crore per annum.

12. Value enhancement by Suzuki: The Revised JVA incorporates commitment by Suzuki that:

Suzuki will endeavour to make MUL the source for some of its models globally.

Suzuki will assist MUL to access new export markets.

Suzuki will give discount on certain components as previously agreed to by it.

Suzuki will set up a task force to explore the possibilities of further reduction incosts at MUL.

Suzuki will promote MUL and its products in the global market.

Suzuki will aggressively strengthen MUL‟s manufacturing and technical capabilities so as tomake MUL‟s products internationally competitive in terms of quality and cost.

In case the withdrawal of GOI results in Suzuki undertaking the above activities, the beneficiary

would not only be Suzuki but also the Indian automobile sector. MUL today contributes nearly

Rs. 2,500 crore to the national exchequer annually. Also, higher growth and earnings of MULwould result in higher receipts to GOI through taxes from MUL. Further, all the above measures

by Suzuki would enhance the value of MUL and hence ensure the possibility of much higher

receipts than the minimum estimated above.

13. Price Multiple Ratio Analysis: One other way to look at the transaction would be to test the P/Ein this case with the P/E of earlier disinvestments. The P/E in earlier cases have been 37 (HTL),

63 (IBP), 11 (VSNL), 19 (Balco), 12 (CMC) and 26 (HZL). In case we take the conservative

scenario discussed above, GOI receives Rs. 2,424 crore for 49.74% holding which means anequity value of Rs. 4,873 crore for MUL as a whole. The profit earned by MUL in 2001-02 was

Rs. 55 crore. This gives a P/E ratio of about 89, which compares very well with P/E of the earlier

disinvestments.

14. Comparable Companies: Taking the conservative scenario discussed above, the per share value

works out to about Rs. 3,684, which is far above the present Book Value of about Rs. 2,000 per

share, resulting in price to book value ratio of 1.8. Also, it is higher than the valuation made bythe three valuers. This is relevant as most automobile sector companies are currently trading at

less than even their book values.

Background to Negotiations 15. MUL, India ‟s dominant automobile manufacturer, is a joint venture of Government of India

(GOI) and Suzuki Motor Corporation (SUZUKI). As on year ended March 31, 2001, MUL had

an equity capital of 132.30 crore and a net worth of Rs. 2,642 crore. With the advent of

competition, Maruti‟s profitability has been under pressure.

16. As per the existing joint venture agreement, both GOI and SUZUKI had joint control over the

management of MUL and took turns in appointing the Chairman and Managing Director of thecompany. In addition, the joint venture agreement restrained the GOI from selling the shares of

MUL to a third party without the consent of SUZUKI.

17. The Government had decided in February 2001 on disinvestment in MUL through the option of MUL offering shares on a rights basis to existing shareholders with a renunciation option.

Government constituted a Negotiating Team to negotiate on behalf of the Government with

SUZUKI. The Team comprised of Secretary, Ministry of Disinvestment; Secretary, Department

of Heavy Industry and Shri K.V. Kamath, Managing Director and CEO, ICICI Ltd. TheCommittee was asked to negotiate and finalise the modalities of disinvestment with SUZUKI.

Meetings with SUZUKI 18. The first round of meetings was held between the Negotiating Team of GOI and SUZUKI

between 2nd

March 2001 and 12th

March 2001 at New Delhi . At the conclusion of the

discussions, a record note of discussions was signed by both the parties on 13th

March 2001. To

summarise, both the sides had agreed that the roadmap for disinvestment of GOI shares in MUL

would comprise of two phases – rights issue in the first phase and, after the completion of therights issue, sale of existing GOI shares in the market in the second phase. It was acknowledged

that this road map would help in bringing in capital into MUL required for its expansion and

growth and at the same time lead to increase in the value of MUL and its share price discoverythrough a transparent manner, which would help determine the benchmark for further disinvestment.

19. The value of the rights issue agreed upon was Rs.400 crore, which was arrived at primarily onthe basis of the estimates of capex requirements in MUL.

20. Regarding valuation of Maruti shares, it was agreed that GOI and SUZUKI would jointly

identify and appoint three reputed valuers to determine the value of shares and the average of thethree values accepted.

21. KPMG, Ernst & Young and S.B. Billimoria were appointed as Valuers and they submitted their valuation reports in January 2002, copies of which were also made available to SUZUKI. The

fair value per share recommended by the three valuers are Rs. 3,200 by KPMG, Rs. 3,142.18 by

Ernst & Young and Rs. 3,500 by S.B. Billimoria. The average of the valuations made by three

different valuers works out to Rs.3,280.

22. After receipt of the valuation report, the second round of meetings was held between the

Negotiating Teams of the GOI and SUZUKI between 12th

February 2002 and 29th

April 2002 at New Delhi to arrive at an agreement on the price at which the rights issue would be made, the

portion of the GOI‟s rights share to be subscribed by SUZUKI, the renunciation premium and

the control premium and modalities for the sale of existing shares held by GOI, etc. Discussions

were also held to finalise the Revised Joint Venture Agreement. At the conclusion of thediscussion, a record note of discussion was signed by both the parties.

23. Kotak Mahindra Capital Company Limited (KMCC) acted as the financial advisor to GOI. Dua& Associates were legal advisors to the Government.

"In September 2005, the Government decided to disinvest 8% Equity (out of 18.28%Government of India Holding) to Indian Public Sector Banks. The Government sold 8% Equity

(2,31,12,804 shares) for a consideration of Rs. 1,567.60 crore. The weighted average per share

was Rs. 678.24.”

On 21st

December 2006, the Cabinet Committee on Economic Affairs approved thedisinvestment of residual 10.27% Government owned equity in Maruti Udyog Ltd. to the Public

Sector Financial Institutions, Indian Public Sector Banks and Indian Mutual Funds. Expressions

of Interest (EoIs) were received from 39 institutions/banks/mutual funds on 9th

March

2007,. Out of the above 39 interested parties, 36 institutions/banks/mutual funds submitted thefinancial bids on 8

thMay, 2007 On the basis of the differential auction method, 32

institutions/banks/mutual funds were allocated shares. The total realization to the Government

from the sale of 10.27% stake in Maruti Udyog Limited would be Rs. 2366.94 crore at aweighted average price of Rs. 794.49 per share.

The Lagan Jute Machinery Company Limited (LJMC) was the first case of successful

privatisation of a Central Public Sector Undertaking, carried out by the Government. LJMC is aCalcutta-based company, and manufactures jute machinery (mainly spinning and drawing

frames). It employed around 400 employees prior to privatisation. It started making losses from

1996-97 onwards and the turnover was on a decline. LJMC's net worth as on March 1998 wasaround Rs. 5 crore and its annual turnover was also around Rs. 5 crore at that time.

LJMC had the potential to increase its turnover and be profitable. It was the main supplier of the

type of machines that it manufactured. The company was known for the quality of its products.There was scope for expanding into the spares market and exports. Some (but not substantial)

investment was required to modernize and renovate the plant and machinery. The manpower age

profile was high but there was not much surplus manpower.

In the initial stages of disinvestment, LJMC was approved for privatisation in the year 1997,

through sale of 74% stake to a strategic partner. The disinvestment process was handled by

LJMC's holding company, Bharat Bhari Udyog Nigam Ltd. (BBUNL), under the administrativecontrol and directions of the Department of Heavy Industries (DHI), Ministry of Industry,

Government of India (Government of India).

The Disinvestment Process

Objectivity and transparency were the key requirements in the whole disinvestment process. As

it was the first case of disinvestment for the Indian Government, the disinvestment processevolved as the transaction progressed.

After the issue of the advertisement for inviting bids from the potential partners, it took around

10 months to complete the disinvestment process.The advisors carried out a review of the company and gave advice on the extent, mode and

methodology of disinvestment. The issues requiring action by the management/approval of the

GOI were identified and steps taken to ensure that the process moved smoothly and shareholder

value was maximized.The Cabinet gave its approval and the necessary agreement was entered into with the strategic

partner in December 1999. After full payment against the shares and execution of share transfer

agreement, the management of the company was handed over to the strategic partner in July

2000.

Post-Privatisation Status of LJMC The strategic partner has retained the same senior management team and there has been no

retrenchment of workers. An industry expert has been appointed as the Managing Director of

LJMC. The operating and financial performance of the company has improved after the

change of management.

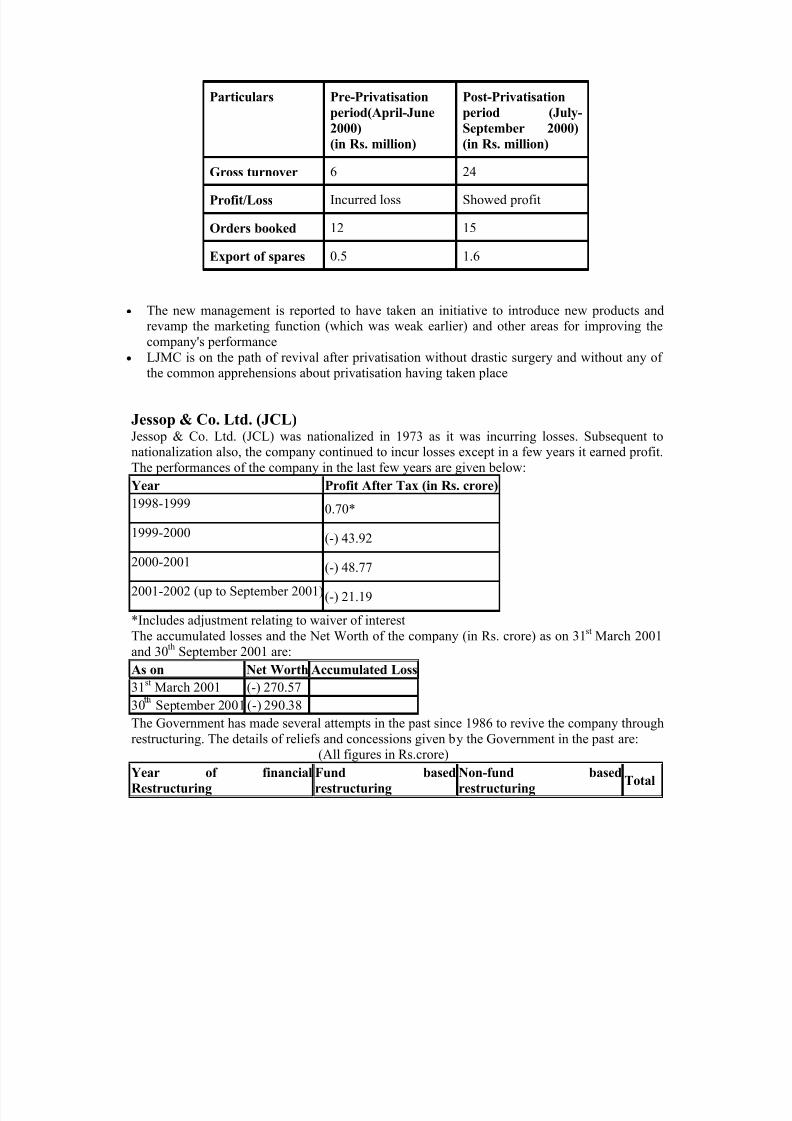

The post-privatisation performance of LJMC(July-September 2000), as compared to pre-

privatisation period (April-June 2000), as reported by the management, is given below:

The new management is reported to have taken an initiative to introduce new products andrevamp the marketing function (which was weak earlier) and other areas for improving the

company's performance LJMC is on the path of revival after privatisation without drastic surgery and without any of

the common apprehensions about privatisation having taken place

Jessop & Co. Ltd. (JCL)Jessop & Co. Ltd. (JCL) was nationalized in 1973 as it was incurring losses. Subsequent tonationalization also, the company continued to incur losses except in a few years it earned profit.

The performances of the company in the last few years are given below:

Year Profit After Tax (in Rs. crore)

1998-1999 0.70*

1999-2000 (-) 43.92

2000-2001 (-) 48.77

2001-2002 (up to September 2001) (-) 21.19

*Includes adjustment relating to waiver of interest

The accumulated losses and the Net Worth of the company (in Rs. crore) as on 31st

March 2001

and 30th

September 2001 are:

As on Net Worth Accumulated Loss

31

st

March 2001 (-) 270.5730 September 2001 (-) 290.38

The Government has made several attempts in the past since 1986 to revive the company through

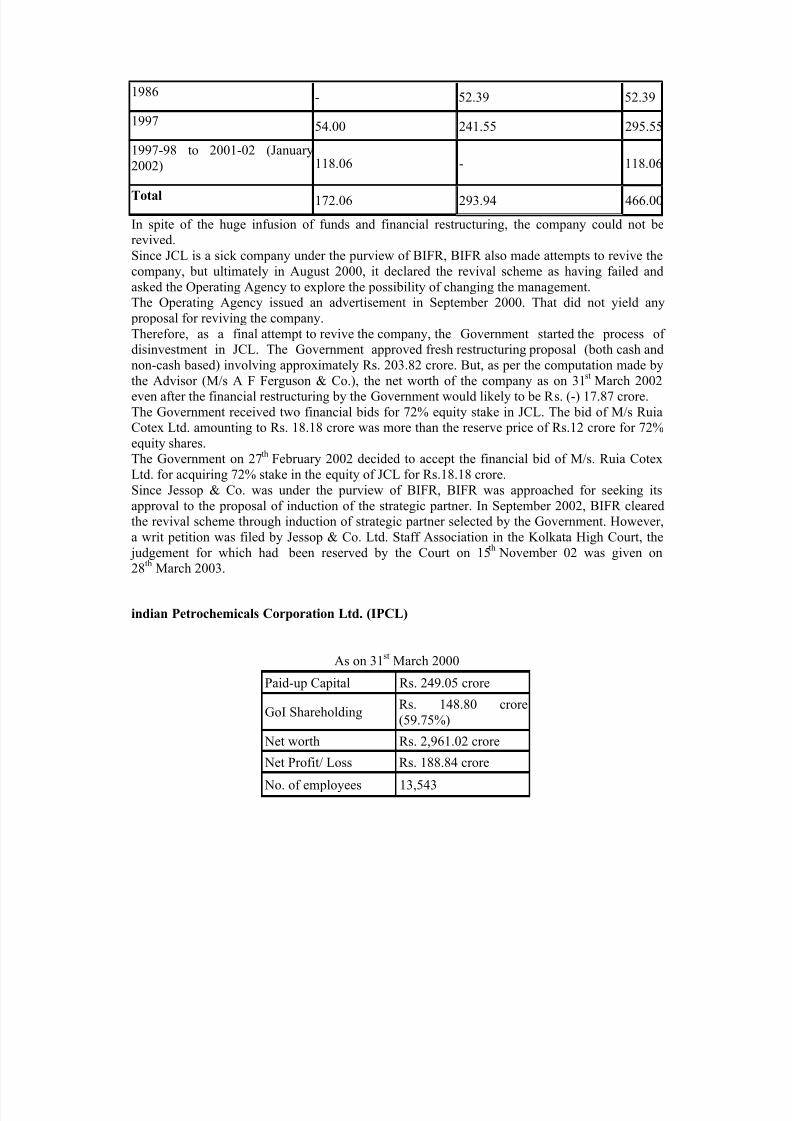

restructuring. The details of reliefs and concessions given by the Government in the past are:(All figures in Rs.crore)

In spite of the huge infusion of funds and financial restructuring, the company could not berevived.

Since JCL is a sick company under the purview of BIFR, BIFR also made attempts to revive the

company, but ultimately in August 2000, it declared the revival scheme as having failed and

asked the Operating Agency to explore the possibility of changing the management.The Operating Agency issued an advertisement in September 2000. That did not yield any

proposal for reviving the company.

Therefore, as a final attempt to revive the company, the Government started the process of

disinvestment in JCL. The Government approved fresh restructuring proposal (both cash andnon-cash based) involving approximately Rs. 203.82 crore. But, as per the computation made by

the Advisor (M/s A F Ferguson & Co.), the net worth of the company as on 31st

March 2002even after the financial restructuring by the Government would likely to be Rs. (-) 17.87 crore.

The Government received two financial bids for 72% equity stake in JCL. The bid of M/s RuiaCotex Ltd. amounting to Rs. 18.18 crore was more than the reserve price of Rs.12 crore for 72%

equity shares.The Government on 27

thFebruary 2002 decided to accept the financial bid of M/s. Ruia Cotex

Ltd. for acquiring 72% stake in the equity of JCL for Rs.18.18 crore.

Since Jessop & Co. was under the purview of BIFR, BIFR was approached for seeking its

approval to the proposal of induction of the strategic partner. In September 2002, BIFR cleared

the revival scheme through induction of strategic partner selected by the Government. However,a writ petition was filed by Jessop & Co. Ltd. Staff Association in the Kolkata High Court, the

judgement for which had been reserved by the Court on 15th

Major activity Production of chemicals and petrochemicals with focus on polymers

Works located at Nagathone (Maharashtra), Gandhar and Vadodara (Gujarat)

Recommendations of Disinvestment Commission (March 1998)

To offer 25% equity to a strategic buyer along with transfer of management control through a global

competitive bidding, care being taken to ensure that the strategic sale does not lead to market dominance by

any single player

Government decision

To offer 25% equity to a strategic buyer along with transfer of management control

Present status of implementation of Government decision

Warburg Dillon Read (WDR) has been appointed as Advisor. Disinvestment transaction of selling 26%Government equity in favour of strategic partner, i.e. Reliance Group has been approved for an amount of Rs. 1,490 crore

Disinvestment in IPCL 1. Government of India (GOI) on 17

thMay 2002 approved induction of Reliance Petroinvestments

Ltd. (Reliance Group) as strategic partner in IPCL, a leading petrochemical PSU, through sale of

26% equity shares at a consideration of Rs. 1,491 crore.

Reserve Pr ice 2. The Advisor (UBS Warburg) had in their report computed the valuation of shares in IPCL by

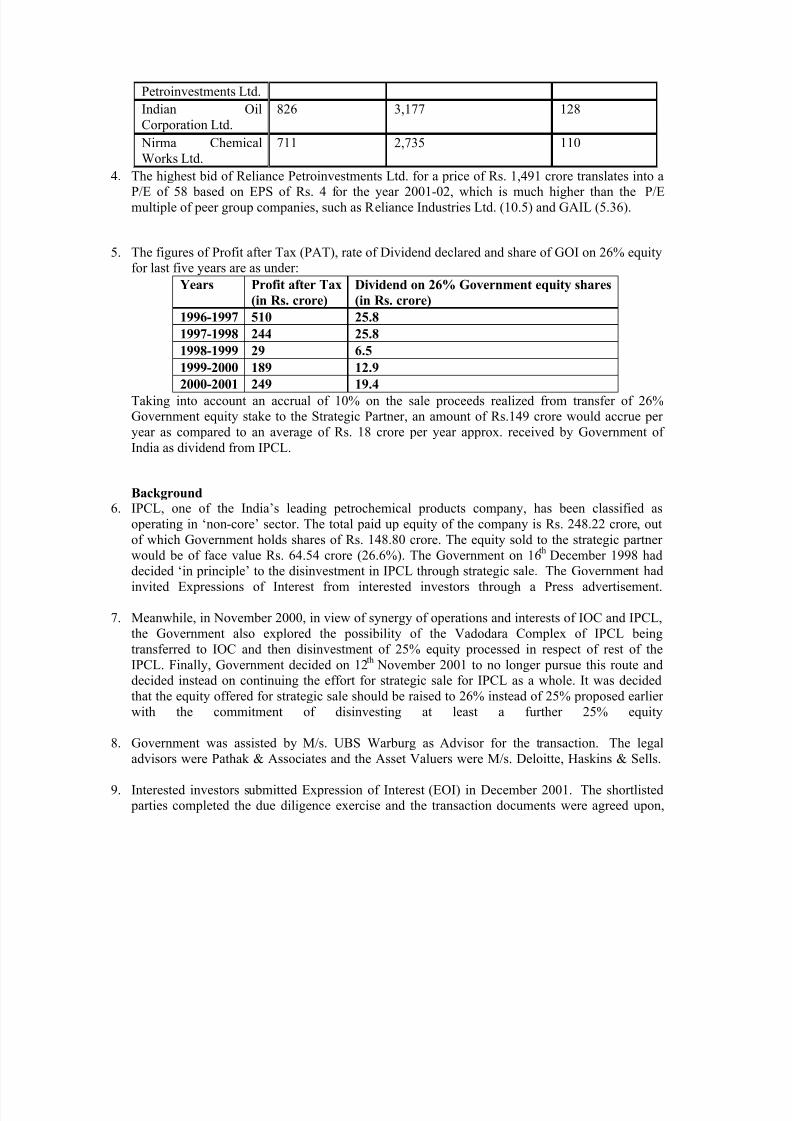

4. The highest bid of Reliance Petroinvestments Ltd. for a price of Rs. 1,491 crore translates into aP/E of 58 based on EPS of Rs. 4 for the year 2001-02, which is much higher than the P/E

multiple of peer group companies, such as Reliance Industries Ltd. (10.5) and GAIL (5.36).

5. The figures of Profit after Tax (PAT), rate of Dividend declared and share of GOI on 26% equityfor last five years are as under:

Years Profit after Tax

(in Rs. crore) Dividend on 26% Government equity shares

(in Rs. crore)

1996-1997 510 25.8

1997-1998 244 25.8

1998-1999 29 6.5

1999-2000 189 12.9

2000-2001 249 19.4

Taking into account an accrual of 10% on the sale proceeds realized from transfer of 26%Government equity stake to the Strategic Partner, an amount of Rs.149 crore would accrue per

year as compared to an average of Rs. 18 crore per year approx. received by Government of

India as dividend from IPCL.

Background 6. IPCL, one of the India‟s leading petrochemical products company, has been classified as

operating in „non-core‟ sector. The total paid up equity of the company is Rs. 248.22 crore , outof which Government holds shares of Rs. 148.80 crore. The equity sold to the strategic partner

would be of face value Rs. 64.54 crore (26.6%). The Government on 16th

December 1998 haddecided „in principle‟ to the disinvestment in IPCL through strategic sale. The Government had

invited Expressions of Interest from interested investors through a Press advertisement.

7. Meanwhile, in November 2000, in view of synergy of operations and interests of IOC and IPCL,

the Government also explored the possibility of the Vadodara Complex of IPCL being

transferred to IOC and then disinvestment of 25% equity processed in respect of rest of the

IPCL. Finally, Government decided on 12th

November 2001 to no longer pursue this route anddecided instead on continuing the effort for strategic sale for IPCL as a whole. It was decided

that the equity offered for strategic sale should be raised to 26% instead of 25% proposed earlier with the commitment of disinvesting at least a further 25% equity

8. Government was assisted by M/s. UBS Warburg as Advisor for the transaction. The legal

advisors were Pathak & Associates and the Asset Valuers were M/s. Deloitte, Haskins & Sells.

9. Interested investors submitted Expression of Interest (EOI) in December 2001. The shortlisted parties completed the due diligence exercise and the transaction documents were agreed upon,

after a number of rounds of discussions with bidders. Thereafter, based on these documents,

financial bids were received from the bidders on 29th

April 2002.

Bharat Aluminium Company Ltd. (BALCO)

BALCO is a fully integrated Aluminium-producing company, having its own captive mines, analumina refinery, an Aluminium smelter, a captive power plant, and down-stream fabrication

facilities. It was set up in 1965 and has its corporate office in New Delhi . Its main plant and

facilities are situated in Korba, Chhatisgarh. It also has a fabrication unit in Bidhanbagh ( WestBengal ). The refining capacity of BALCO is 2 lakh tonnes per year and its smelting capacity is

1 lakh tonnes per year. Its employee strength was 6,436 on 2nd

March 2001.

The Government of India had 100% stake in BALCO prior to disinvestment. In 1997, theDisinvestment Commission classified BALCO as non-core for the purpose of disinvestment and

recommended immediate disinvestment of 40% of the Government stake to a strategic partner,

and a further reduction of the Government stake to 26% within 2 years of the strategic salethrough a domestic public offering. It further recommended disinvestment of the entire

remaining stake at an appropriate time thereafter. The Cabinet accepted the recommendations of

the Disinvestment Commission for disinvestment of 40% stake through a strategic sale and

further disinvestment through the capital market.

Later, in 1998, the Disinvestment Commission revised its recommendation and advised the

Government to consider 51% disinvestment in favour of a strategic buyer along with transfer of

management, which was accepted by the Cabinet. The Government thereupon appointed M/sJardine Fleming as advisor to assist in the sale of its 51% stake in BALCO to a strategic buyer.

Simultaneously, it was brought to the attention of the Government that BALCO had a bloatedequity of Rs. 489 crore and large unutilised free reserves of the level of Rs. 424 crore. It was

suggested by the Ministry of Mines that BALCO's equity be reduced by 50% prior to

disinvestment, by using its substantial cash surplus. This proposal was accepted. As a result, theGovernment received Rs. 244 crore from the capital restructuring of BALCO, and another Rs. 31

crore as tax on this amount, prior to disinvestment.

The strategic sale process for BALCO started in late 1997, after the first decision of the

Government, and finally came to end on 2nd

March 2001. The 51% stake was sold to Sterlite

Industries, the highest bidder, and fetched the Government Rs. 551.50 crore. The price received

was higher than the values indicated by the various methods of valuation used. The Government

thus recovered Rs 827.50 crore from this privatisation against approximately Rs. 10 crore asdividend it used to get against the 51% shares during the peak Aluminium cycle.

Post sale, a number of doubts had been raised by various quarters on the disinvestment of BALCO, especially with regard to transparency, valuation and protection of employees‟

interests. However, the entire sale process, including the appointment of advisor and the approval

of the price bid, was carried out in an extremely transparent manner, in keeping with the higheststandards of global practices. Of special mention are the clauses in the Shareholders‟ Agreement

with the strategic buyer, which offer adequate protection to employees of all levels with regard to

their job safety and severance packages.

Post-Privatisation Status of BALCO 1. The new management introduced VRS from 31

stJuly 2001 to 16

thAugust 2001. 981 applications

(from 151 executives and 830 workers) were received. 694 old VRS applications were also pending. A total of 956 applications were accepted mostly where units were lying closed.

2. In spite of incurring losses to the tune of Rs. 200 crore due to the strike by the employees in

2001, an ex gratia payment of Rs. 5000 was made to all the employees.

3. Long-term wage agreement for a period of 5 years was entered on 7th

October 2001 (wage

revision was due since 1stApril 1999 and the earlier revision was for 10 years) as follows:

a. Workmen get a guaranteed benefit at the rate of 20% of the basic pay

b. Increase in allowances:

Night shift allowance: Rs.10 - Rs.20/shift

Canteen allowance: Rs. 400/month (instead of subsidised canteen facilities)

Education allowance: Rs. 50 - Rs. 75/month

Hostel allowance: Rs.150 - Rs.200 per month

Scholarship amount to meritorious children doubled

Leave Travel Assistance of around Rs. 6000 as cash every year

5. The new management proposed an investment of Rs. 6,000 crore which would increase

production 4 times.

Landmark Judgement in BALCO Disinvestment

In protest of the BALCO disinvestment, the workers went on a 67-day strike. Three writ

petitions-two in Delhi High Court and one in Chhatisgarh High Court- were filed against

disinvestment in BALCO in February 2001. The Supreme Court in its unanimous judgement

delivered on 10th

December 2001 validated disinvestment of BALCO by the Government of India. The landmark judgement also defined, amongst others, the parameters of judicial review in

the Government‟s economic policy matters. The Hon‟ble Supreme Court, while validating

BALCO-disinvestment, and dismissing the petitions, remarked, “Thus, apart from the fact thatthe policy of disinvestment cannot be questioned as such, the facts herein show that fair, just and

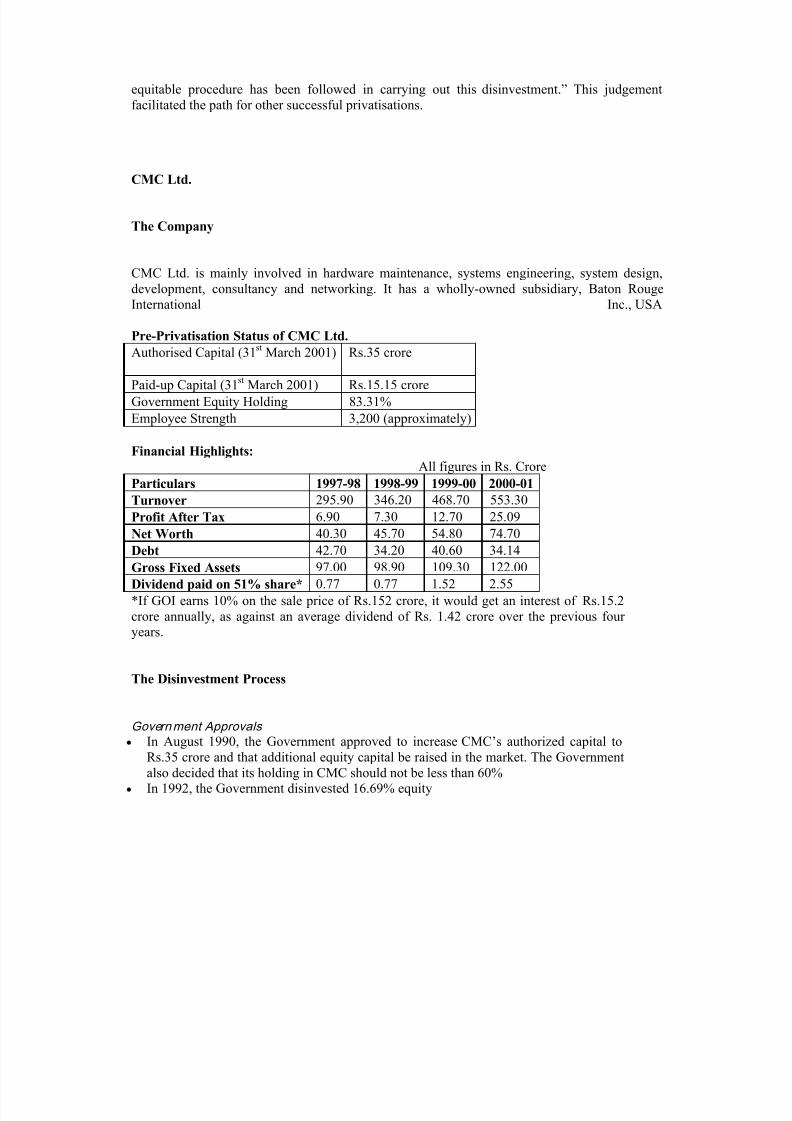

In April 1999, CMC was referred to the Disinvestment Commission, but it was

withdrawn as Government decided raising of additional equity via private placement

or by directly going for public issue

CMC could not raise the funds till November 2000 by way of either private placement

of shares or through public issue

On 1

st

February 2001, the Government decided to bring down its equity to 26% by wayof induction of a strategic partner and also by way of other means

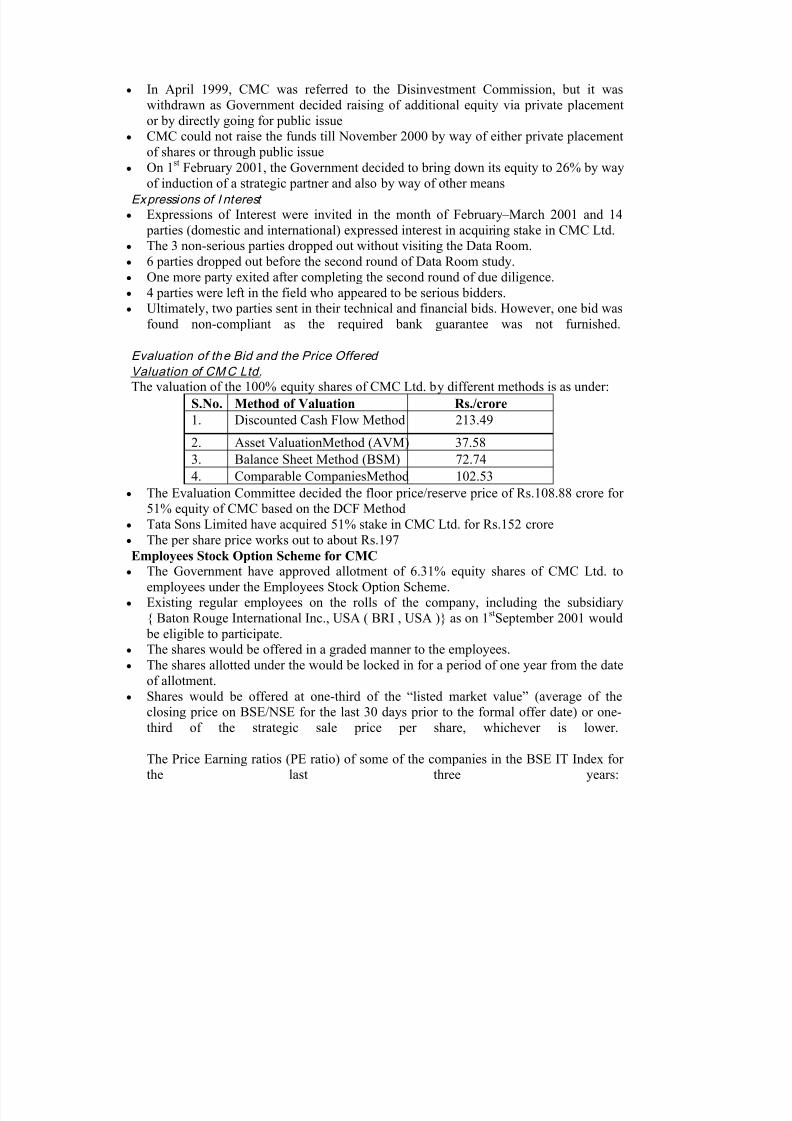

Expressions of I nterest Expressions of Interest were invited in the month of February – March 2001 and 14

parties (domestic and international) expressed interest in acquiring stake in CMC Ltd.

The 3 non-serious parties dropped out without visiting the Data Room.

6 parties dropped out before the second round of Data Room study.

One more party exited after completing the second round of due diligence.

4 parties were left in the field who appeared to be serious bidders.

Ultimately, two parties sent in their technical and financial bids. However, one bid was

found non-compliant as the required bank guarantee was not furnished.

Evaluation of the Bid and the Price Offered

Valuation of CMC Ltd. The valuation of the 100% equity shares of CMC Ltd. by different methods is as under:

S.No. Method of Valuation Rs./crore

1. Discounted Cash Flow Method 213.49

2. Asset ValuationMethod (AVM) 37.58

3. Balance Sheet Method (BSM) 72.74

4. Comparable CompaniesMethod 102.53

The Evaluation Committee decided the floor price/reserve price of Rs.108.88 crore for 51% equity of CMC based on the DCF Method

Tata Sons Limited have acquired 51% stake in CMC Ltd. for Rs.152 crore The per share price works out to about Rs.197

Employees Stock Option Scheme for CMC The Government have approved allotment of 6.31% equity shares of CMC Ltd. to

employees under the Employees Stock Option Scheme.

Existing regular employees on the rolls of the company, including the subsidiary

{ Baton Rouge International Inc., USA ( BRI , USA )} as on 1stSeptember 2001 would

be eligible to participate.

The shares would be offered in a graded manner to the employees.

The shares allotted under the would be locked in for a period of one year from the date

of allotment.

Shares would be offered at one-third of the “listed market value” (average of theclosing price on BSE/NSE for the last 30 days prior to the formal offer date) or one-

third of the strategic sale price per share, whichever is lower.

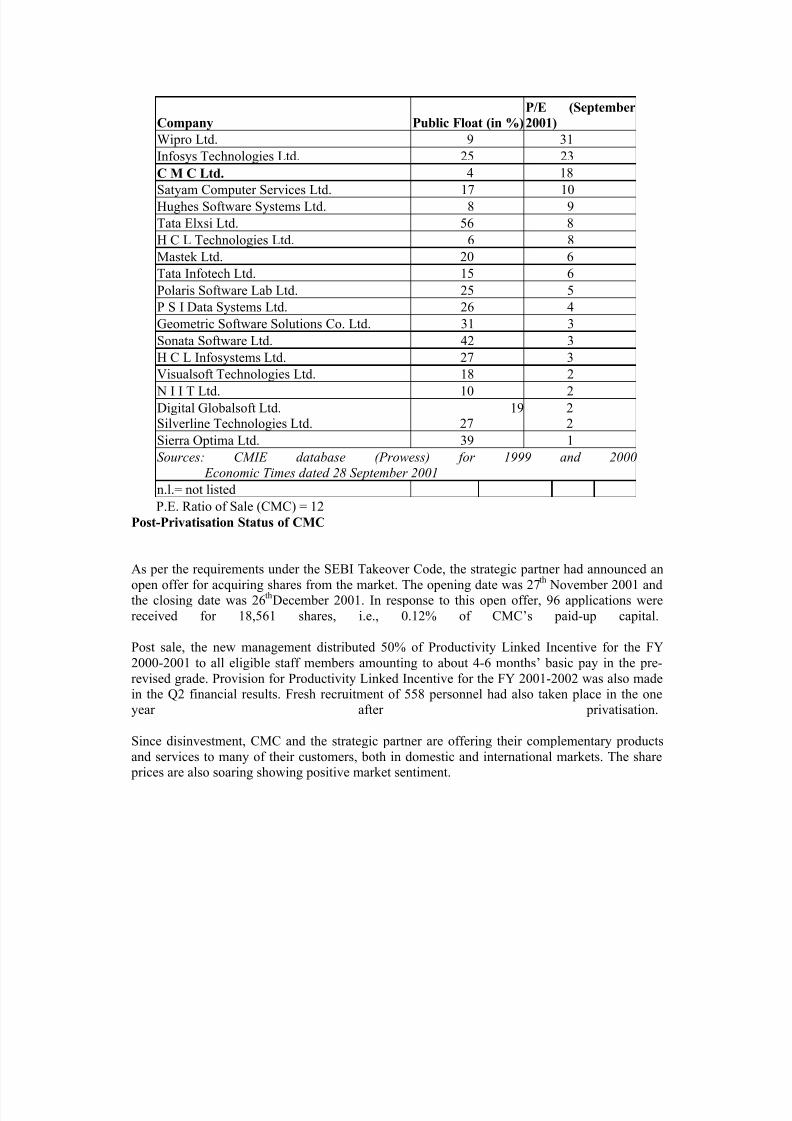

The Price Earning ratios (PE ratio) of some of the companies in the BSE IT Index for the last three years:

C M C Ltd. 4 18Satyam Computer Services Ltd. 17 10

Hughes Software Systems Ltd. 8 9

Tata Elxsi Ltd. 56 8

H C L Technologies Ltd. 6 8

Mastek Ltd. 20 6

Tata Infotech Ltd. 15 6

Polaris Software Lab Ltd. 25 5

P S I Data Systems Ltd. 26 4

Geometric Software Solutions Co. Ltd. 31 3

Sonata Software Ltd. 42 3H C L Infosystems Ltd. 27 3

Visualsoft Technologies Ltd. 18 2

N I I T Ltd. 10 2

Digital Globalsoft Ltd.Silverline Technologies Ltd.

1927

22

Sierra Optima Ltd. 39 1

Sources: CMIE database (Prowess) for 1999 and 2000

Economic Times dated 28 September 2001

n.l.= not listed

P.E. Ratio of Sale (CMC) = 12

Post-Privatisation Status of CMC

As per the requirements under the SEBI Takeover Code, the strategic partner had announced an

open offer for acquiring shares from the market. The opening date was 27th

November 2001 andthe closing date was 26

thDecember 2001. In response to this open offer, 96 applications were

received for 18,561 shares, i.e., 0.12% of CMC‟s paid-up capital.

Post sale, the new management distributed 50% of Productivity Linked Incentive for the FY

2000-2001 to all eligible staff members amounting to about 4-6 months‟ basic pay in the pre-

revised grade. Provision for Productivity Linked Incentive for the FY 2001-2002 was also made

in the Q2 financial results. Fresh recruitment of 558 personnel had also taken place in the oneyear after privatisation.

Since disinvestment, CMC and the strategic partner are offering their complementary products

and services to many of their customers, both in domestic and international markets. The share prices are also soaring showing positive market sentiment.

Government of India has decided to disinvest 26% equity in Hindustan Zinc Limited in favour of

Sterlite Opportunities and Ventures Limited (a Special Purpose Vehicle promoted by Sterlite

Industries (India) Limited and Sterlite Optical Technologies Limited), at a price of Rs. 445 crore

(amounting to Rs. 40.50/share).

This means a P/E (price/earning) ratio of about 21. The average dividend paid by the company,

calculated for 26% equity, over the last eight years till 2000, has been of the order of Rs. 3.50

crore per year. Details of P/E ratios for strategic sale of other companies are given in the

Annexure.

BNP Paribas served as the Advisor and M/s Amarchand Mangaldas & A Shroff and Company

served as the Legal Advisor to the transaction.

HZL was incorporated in January 1966 as a Public Sector Company after the takeover of the

erstwhile Metal Corporation of India Limited. Its paid-up capital is Rs. 422.53 crore, out of

which Government of India holds 75.92% while Financial Institutions, other Corporate Bodies

(including NRIs) and Indian nationals hold the balance equity. It is a profit-making and listedcompany, and its shares are traded at the Stock Exchanges of Mumbai, Delhi and Jaipur. There

has been a spurt in its share prices, especially after the successful disinvestment of VSNL, IBP,

etc. The weighted average price of shares over the last six months is about Rs.25.30 and the

average weekly high and low of closing price for last six months is over Rs.22 per share.

The decision to disinvest 26% equity through strategic sale was taken on 29.8.2000. Following

due process, price bids were invited from all the Qualified Interested Parties, to be received on

8.11.2001. Only one QIP submitted the price bid which was rejected since it was lower than the

reserve price fixed.

In pursuance of Government directions, a renewed exercise was undertaken

involving the original QIPs who had completed their due

diligence as well as the Advisors/Legal Advisors to ensure how the value depleters in the

transaction

documents and bidding conditions be modified to enhance the potential value of the company in

order to make it more attractive to the bidders. M/s URS Corporation was appointed to conduct

environmental, health and safety due diligence review of the company. Amongst the

modifications made in the transaction documents are the sequencing of call and put options and

their pricing, the provision to have the Chairman nominated by the Strategic Partner once it

acquires 51% stake, unlimited environmental indemnity for a period of three years and a clear

road map for the Government to exit from the company. Besides, sale price has been de-linked

from Public offer price under the SEBI Takeover Code. Meanwhile, on 28.2.2002 it was

announced that the customs duty will be reduced from 35% to 25%, which is likely to impact on

the profitability of the company.

Finally, price bids were invited from all the five Qualified Interested Parties (Glencore

International, Binani Industries, Indo-Gulf Corporation, Sterlite and Metdist).

Two financial bids were received from M/s Indo Gulf Corporation and M/s Sterlite Opportunities

and Ventures Limited. The reserve price fixed was Rs.32.15 per share (Rs.353.17 crore for 26%stake). Both the price bids received were above the reserve price. The higher bid, that of M/s

Sterlite Opportunities and Ventures Limited, for Rs.445 crore (translating to about Rs.40.50 per

share) was accepted. The price offered by M/s Sterlite Opportunities & Ventures Limited is

substantially higher than the offer made by Sterlite Industries in November, 2001.

The transaction was closed on 11.04.2002. An attractive ESOP scheme was offered to the

employees and full-time functional directors of the Company. 1.46% shares were sold to

employees @ Rs. 10/- per share in Dec. 2002.

As part of thr "Call Option' available to the Strategic Partner, Government parted with another 18-92% for Rs. 323.88 crore @ Rs. 40.50 per share in November, 2003.

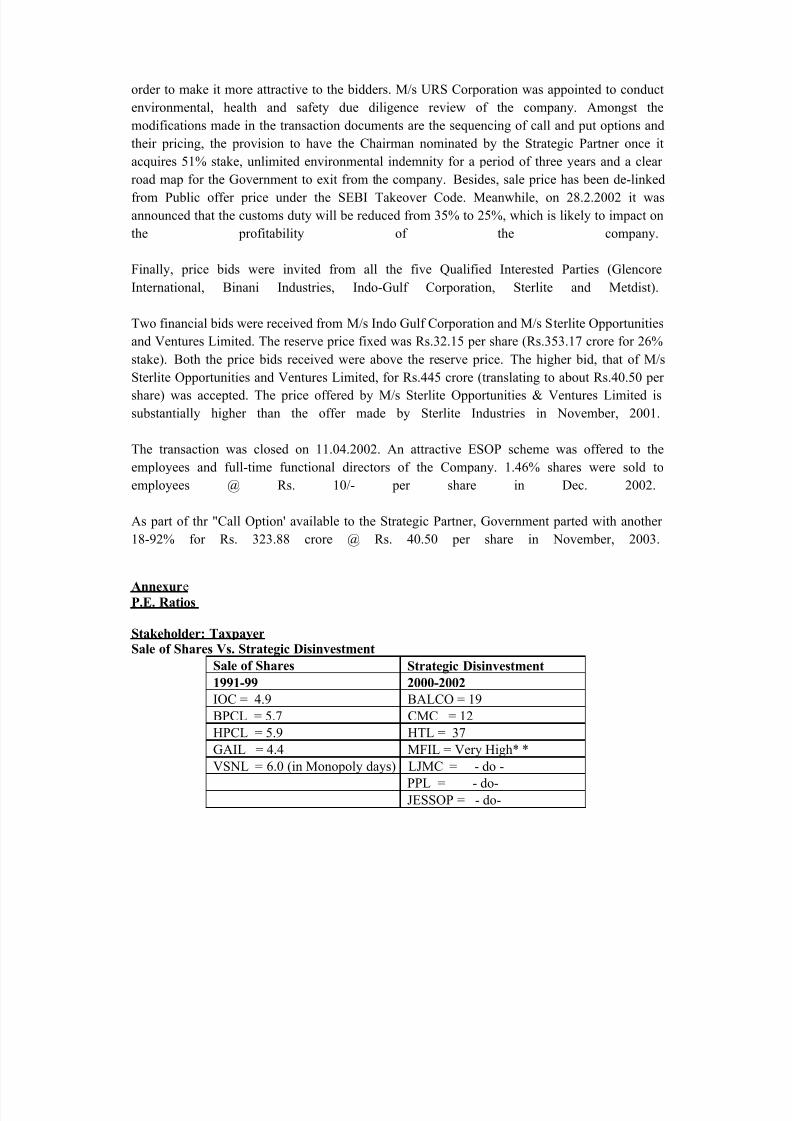

Annexure

P.E. Ratios

Stakeholder: Taxpayer Sale of Shares Vs. Strategic Disinvestment