18

Cash Grants in Lieu of Tax Credits A Financing Opportunity for Renewable Energy July 22, 2009 Travis L.L. Blais Sahir C. Surmeli

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | barry-richard |

| View: | 215 times |

| Download: | 2 times |

Cash Grants in Lieu of Tax Credits A Financing Opportunity for Renewable Energy

July 22, 2009

Travis L.L. Blais

Sahir C. Surmeli

Speakers

Travis L.L. Blais, Esq. Sahir C. Surmeli, Esq.

Copyright © 2009 Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C . This presentation may be considered attorney advertising under the rules of some states. The information and materials contained

herein have been provided as a service by the law firm of Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C. ; however, the information and materials do not, and are not intended to, constitute legal advice. Neither transmission nor receipt of such

information and materials will create an attorney-client relationship between the sender and receiver. The hiring of an attorney is an important decision that should not be based solely upon advertisements or solicitations. Users are advised not to take, or refrain from taking, any action based upon the information and materials contained herein without consulting legal counsel engaged for a

particular matter. Furthermore, prior results do not guarantee a similar outcome.

New Development

• The American Recovery and Reinvestment Act of 2009 created a cash grant program for qualified renewable energy facilities

• Eligible applicants may receive cash grants of up to 30 percent of the tax basis of eligible property

• No statutory cap on amount of grants• On July 9, 2009, Treasury issued guidance on

electing these cash grants in lieu of tax credits• The Treasury guidance, a sample application, and

related materials are available at www.treasury.gov/recovery

Review of Renewable Energy Production Credit (PTC)

• 2.1 cents (’08) per kWh of electricity produced by:• Wind• Closed-loop biomass• Geothermal energy

• 1.0 cents (’08) per kWh of electricity produced by:• Open-loop biomass• Municipal solid waste (landfill gas and trash)• Qualified hydropower (including small irrigation

power)• Credit to producer of energy sold over 10-year

period

Review of Business Energy Credit (ITC)

• One-time, up-front income tax credit for “energy property” placed in service

• Generally 10% or 30% of the basis of energy property

• 5-year recapture period• 50% of credit reduces basis

Review of ITC, continued…

“Energy property” includes:• Solar property• Qualified fuel cell property• Qualified microturbine property• Qualified small wind energy property• Combined heat and power system property• Geothermal power production property• Geothermal heat pump property

American Recovery and Reinvestment Act of 2009

• Extension of PTC and ITC• Election to ITC Instead of PTC• Grants in Lieu of PTC and ITC• New Energy Manufacturing Credit• New Allocations of Tax-Exempt Bonds• Non-Tax Economic Incentives

Who is Eligible for a Grant?

• Generally, any individual or entity who is the original user of “specified energy property”

• Original user may be the first owner or lessee of the property– Both lessor and lessee must be eligible– Lessor must waive rights to grant, PTC, and ITC– Lessee must agree to include 50% of grant in gross income

ratably over 5-year recapture period

• Lessee in a sale-leaseback may be eligible– Lessee must have originally placed property in service– Property must be sold and leased back by lessee within 3

months after originally placed in service

Ineligible Recipients

• Federal, state, or local governments• Tax-exempt organizations (includes most

pension funds)• Clean renewable energy bond lenders,

cooperative electric companies, or governmental bodies

• Pass-through entities having an equity owner who is described above– Unless interest is owned through a corporate “blocker”

• Foreign persons or entities– Unless more than 50% of the foreign person or entity’s gross

income derived from the property is subject to U.S. federal income tax

What Property is Eligible for a Grant?

• “Specified energy property” is property otherwise eligible for ITC, including “PTC-type” property now able to elect ITC

• Tangible property, integral to the facility, for which depreciation is allowed

• Original use of the property must begin with applicant– But used parts can account for 20% of total cost

• Property must be physically located within the U.S. for more than 50% of the year

Project and Application Deadlines

• Construction must begin by end of 2010• If construction began before 2009:

– Property must be placed in service by end of 2010– Application must be submitted after placed-in-service date, but

before October 1, 2011

• If construction began in 2009 or 2010:– Property must be placed in service by the end of

• 2012 for wind facility eligible for PTC• 2013 for other property eligible for PTC• 2016 for property eligible for ITC

– Application must be submitted after construction begins, but before October 1, 2011

Project Deadlines, continued…

• “Construction begins” when “physical work of a significant nature” begins, either directly or under written contract– Preliminary activities do not constitute physical work (e.g.,

planning, designing, securing financing)– Safe harbor: construction begins upon incurring or spending

5% of the total cost of the property (excluding preliminary activities)

• Property is “placed in service” when it is ready and available for its intended use, i.e., substantially complete and ready to produce energy

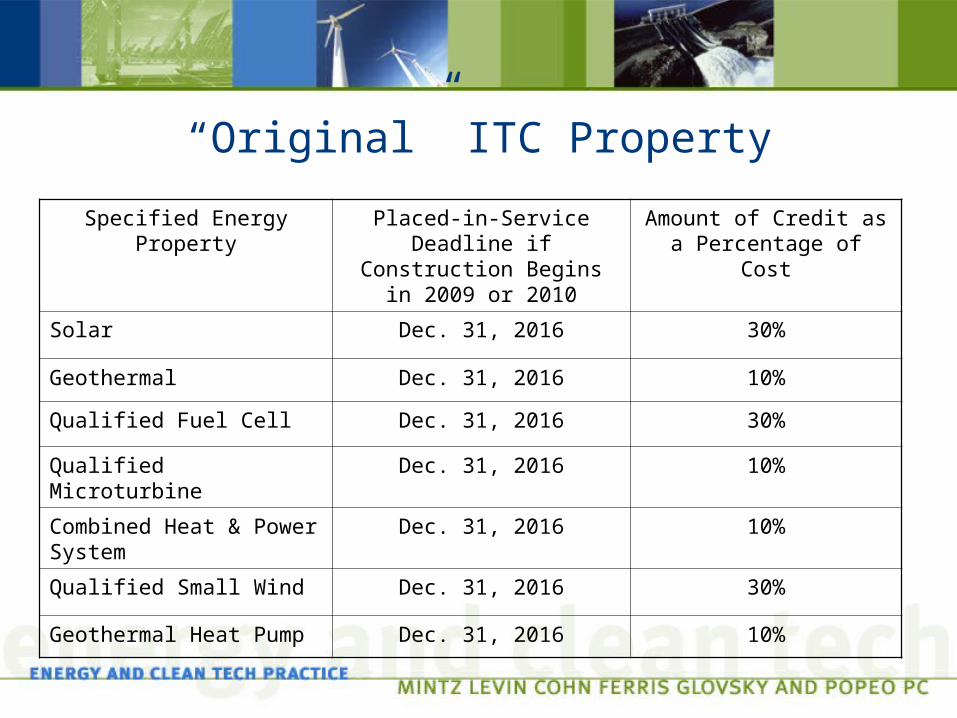

“Original” ITC Property

Specified Energy Property

Placed-in-Service Deadline if Construction Begins in 2009 or 2010

Amount of Credit as a Percentage of Cost

Solar Dec. 31, 2016 30%

Geothermal Dec. 31, 2016 10%

Qualified Fuel Cell Dec. 31, 2016 30%

Qualified Microturbine Dec. 31, 2016 10%

Combined Heat & Power System

Dec. 31, 2016 10%

Qualified Small Wind Dec. 31, 2016 30%

Geothermal Heat Pump Dec. 31, 2016 10%

“PTC-type” Property Eligible for ITC Election

Specified Energy Property

Placed-in-Service Deadline if Construction Begins in 2009 or 2010

Amount of Credit as a Percentage of Cost

Wind Facility Dec. 31, 2012 30%

Closed-Loop Biomass Dec. 31, 2013 30%

Open-Loop Biomass Dec. 31, 2013 30%

Geothermal Dec. 31, 2013 30%

Landfill Gas Dec. 31, 2013 30%

Trash Dec. 31, 2013 30%

Hydropower Dec. 31, 2013 30%

Marine & Hydrokinetic Dec. 31, 2013 30%

Application Process and Grant Funding

• Treasury accepting applications beginning on or about August 1 at www.treasury.gov/recovery

• Applications must be received before October 1, 2011• Applicants must also register with the Central

Contractor Registration at www.ccr.gov/startregistration.aspx

• Applicants must have a Dun and Bradstreet number• Treasury will notify applicants of an incomplete

application, who will have 21 days to correct• Treasury will make payments within 60 days following

the later of:(1) the date of the completed application; or(2) the date the eligible property is placed in service

Application Process, continued…

• Completed applications must include:– Signed and completed application form– Documentation supporting placed-in-service (or construction)

date (e.g., commissioning report, project engineer/equipment vendor report)

– Documentation supporting satisfaction of PTC or ITC requirements (e.g., design plans, final engineering documents, OEM spec sheets)

– Signed Terms and Conditions– Detailed breakdown of all costs to support claimed cost basis

• Independent accountant’s report required for projects costing more than $500,000

• Recipients must retain contracts and invoices to be made available upon Treasury’s request

Inclusion and Recapture Rules

• Owner: Grant is not included in recipient’s gross income

• Lessee: 50% of grant amount must be included in gross income ratably over 5-year recapture period

• Grant reduces property’s basis by 50% of the grant amount

• Grant must be repaid if property is transferred to an ineligible person or otherwise ceases to qualify within 5 years after being placed in service– Repayment is in proportion to property’s length of service– Transfer to eligible person does not trigger recapture if purchaser

agrees to be jointly liable for any recapture– Compare with recapture rule for ITC

THANK YOU!

Sahir Surmeli, Esq.Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C.

(617) [email protected]

Twitter.com/EnergyCleanTech

Travis L.L. Blais, Esq.Mintz, Levin, Cohn, Ferris, Glovsky and Popeo, P.C.

(617) [email protected]