57

Cassava: Adding value for Africa Annual review (April 1 st 2010-March 31 st 2011) Uganda Report

Cassava: Adding value for Africa

Annual review

(April 1st 2010-March 31st 2011)

Uganda Report

Summary of country strategy

• Delivering HQCF/grits to 3 sector markets.

Biscuit manufacturers.

Agri-food/composite flour.

Small town bakeries.

• Sundried production of grits & HQCF by community processing groups.

• Linking groups to markets through association.

Revised milestones, UgandaObj. no.

Key milestone Target at end period

Target at period end

Target at period end

Cumulative target

March 31st

’11Apr 1st ‘11 -Mar 31st ‘12

Apr 1st ’12-Mar 31st ‘13

Mar 31st

2013

1a Farmers benefit from sundried HQCF/cassava grits prod.

432 1,584 2,592(576 new)

2,592

1b Processors benefit from sundried HQCF/cassava grits prod.

400 1,465 2,398(533 new)

2,398

2 Increase in prod of consistent quality HQCF

216 t 792 t 1,296 t(288 t new)

1,296 t

3 Regular & increased qty of HQCF purchased by end-user industries

216 t 792 t 1,296 t(288 t)

1,296 t

Highlights of community levels

• There are 9 C:AVA initiated and 2 partner points of HQCF processing.

• Some communities (clusters) trained under FAO, NAADS, Farm radio).

• Have set up voluntary management through committees (Executive, construction, production, quality assurance & marketing).

• Most of the activities are community shared labour.

Highlights of community levels:

• Some members are purely providing labour (harvesting, peeling, sieving).

• Each has sundrying area with an ultimate space for 400 sq. metres per site.

• Each has a cassava grater (800-1000 kg/hr) and press.

• Each has store (private or hired).

• Each has a lot number for traceability.

• Market under auspices of mother association.

Highlights of intermediaries

• 3 of them (PATA, P’KWII, SOSPPA).

• Each has a batch number for traceability.

• Previously engaged in bulk selling of gari, honey, sunflower, sweetpotato vines, sweetpotato composite flour.

• Been battling to get certification to penetrate high-end markets/supermarkets for gari, tapioca, honey, sun flower oil, SP composite flour.

• Have legal existence at local (SOSPPA) or national level (PATA,P’KWII).

Highlights of Intermediaries.• Currently streamlining food manufacturing

requirements & have applied for HQCF UNBS certification.

• UNBS may temporarily upset exceeding Uganda standards but is the surest way for sustainability.

• Introducing cleaning schedules, maintenance schedules, Instruction tips and records as evidenceand core values of food industry standards.

• Negotiate quantities, price, transport of products, assure quality, bulk HQCF, deduct commissions for maintaining equipments.

Highlights of markets• Categorisation:

local communities (markets, schools, shops, roadside stalls, for chen chens, doughtnuts, buns, etc).

Small towns bakeries (rural markets buns, doughnuts, bread, chen chens, cakes).

Large end-users (high end-users)

• Differentiating critical factors:

Consistence, quality & quantity.

Consumer preferences & sensitivity.

Income targets

Beneficiary category

Annual benefit(US $)

Annual benefit(Ushs)

Farmers 102 239,700

Processors 125 293,750

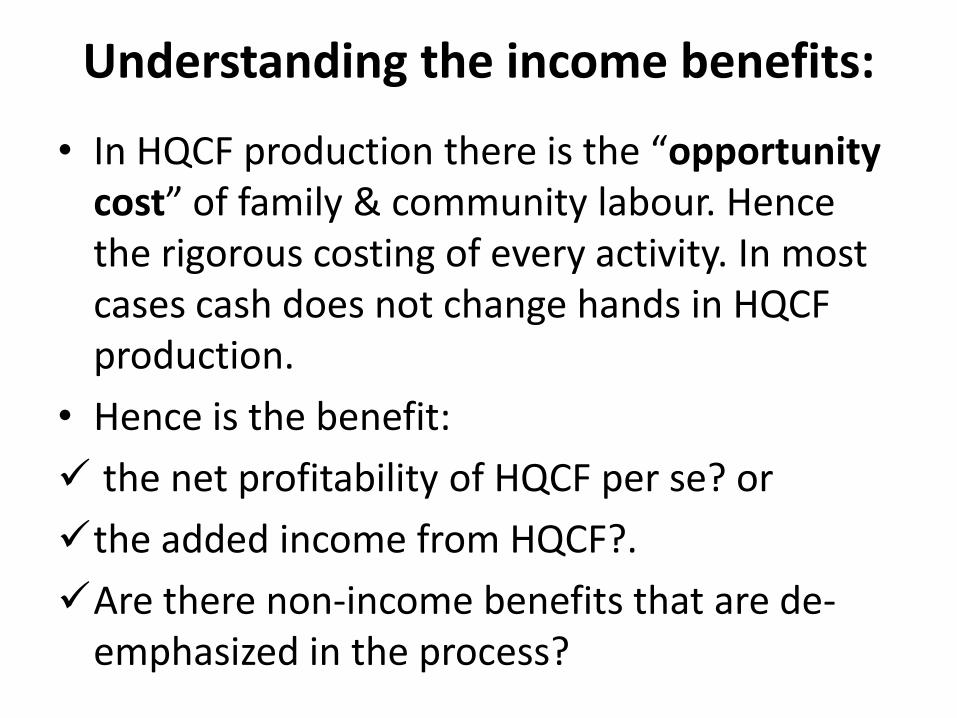

Understanding the income benefits:

• Current farm-gate price for local cassava chips in project area is 250=/ kg.

• In local cassava chips there is cost of fresh tubers, harvesting, transporting, peeling, cleaning the ferments, drying, storage, bagging.

• In HQCF the cost is 950= per kg.

• In HQCF you have cost of fresh tubers, harvesting tubers, transporting, peeling, washing, grating, de-watering, drying, milling, bagging.

Understanding the income benefits:

• In HQCF production there is the “opportunity cost” of family & community labour. Hence the rigorous costing of every activity. In most cases cash does not change hands in HQCF production.

• Hence is the benefit:

the net profitability of HQCF per se? or

the added income from HQCF?.

Are there non-income benefits that are de-emphasized in the process?

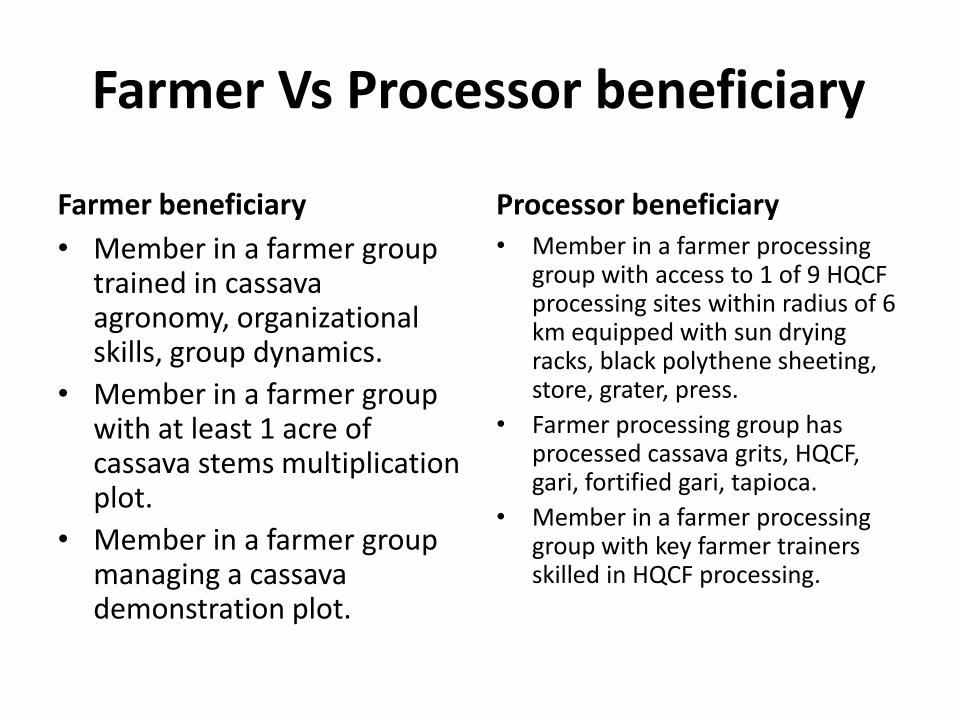

Farmer Vs Processor beneficiary

Farmer beneficiary

• Member in a farmer group trained in cassava agronomy, organizational skills, group dynamics.

• Member in a farmer group with at least 1 acre of cassava stems multiplication plot.

• Member in a farmer group managing a cassava demonstration plot.

Processor beneficiary• Member in a farmer processing

group with access to 1 of 9 HQCF processing sites within radius of 6 km equipped with sun drying racks, black polythene sheeting, store, grater, press.

• Farmer processing group has processed cassava grits, HQCF, gari, fortified gari, tapioca.

• Member in a farmer processing group with key farmer trainers skilled in HQCF processing.

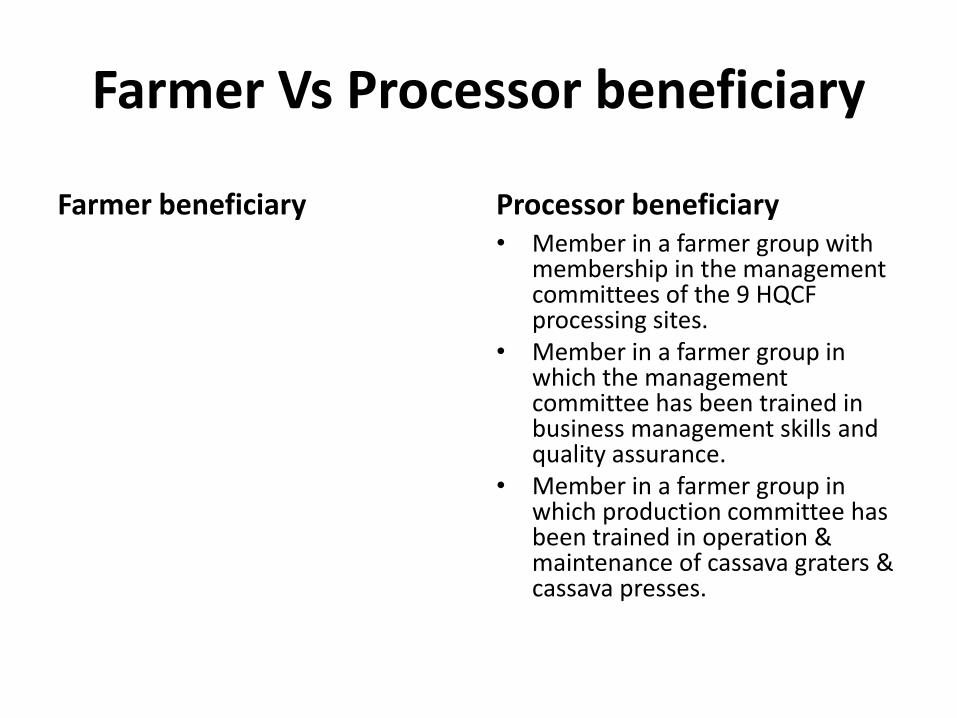

Farmer Vs Processor beneficiary

Farmer beneficiary Processor beneficiary• Member in a farmer group with

membership in the management committees of the 9 HQCF processing sites.

• Member in a farmer group in which the management committee has been trained in business management skills and quality assurance.

• Member in a farmer group in which production committee has been trained in operation & maintenance of cassava graters & cassava presses.

Farmer Vs Processor beneficiary

Processor beneficiary

• Farmer processors who sold some HQCF but whose majority sales are still local cassava grits.

• Non-members who processed HQCF at the processing sites at a fee.

• Farmer processors who also had similar benefits as the farmer beneficiaries.

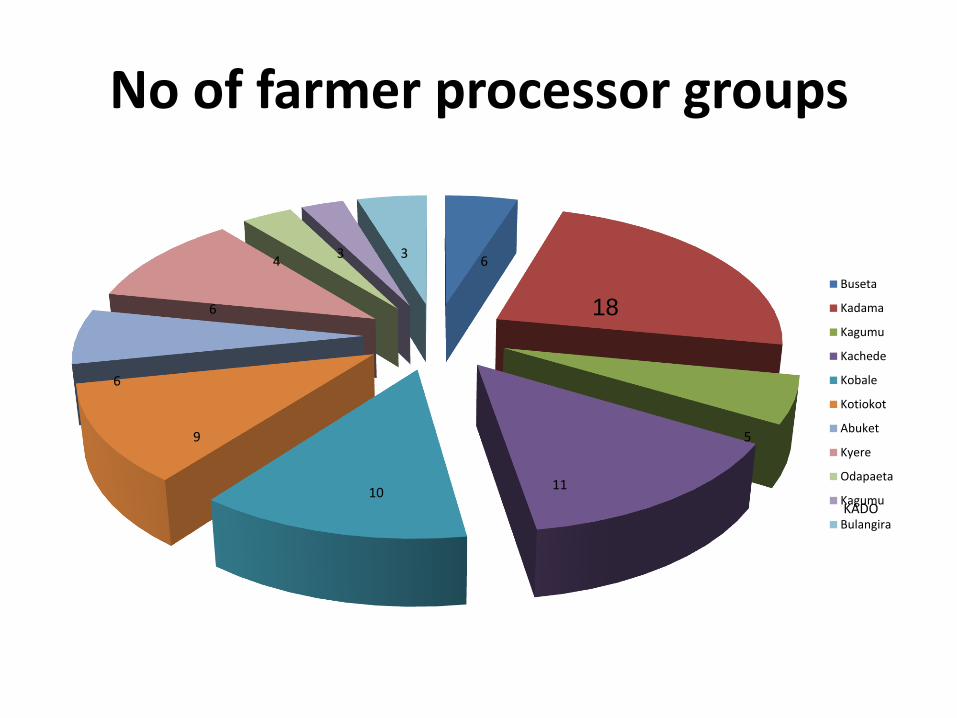

9 processing sites in UgandaAssociation Processing

siteNo. of farmer processing groups

No. of farmer processors

HQCFBatch no.

Pallisa Agri-business training association(PATA)

Buseta 6 95 01/01

Kadama 18 458 01/02

Kagumu 5 109 01/03

Popular Knowledge for (Wo)men Initiative (P’KWII)

Kachede 11 275 02/04

Kobale 10 250 02/05

Kotiokot 9 225 02/06

Sweetpotato Producers & Processors Association(SOSPPA)

Abuket 6 128 03/07

Kyere 6 216 03/08

Odapaeta 4 66 03/09

Kagumu Development Organisation (KADO)

Kagumu 3 56

Uganda Women Girl Child Concern

Bulangira 3 91

Total 81 1,969

No of farmer processor groups

Buseta

Kadama

Kagumu

Kachede

Kobale

Kotiokot

Abuket

Kyere

Odapaeta

Kagumu

Bulangira

11

9

10

5

6

6

43 3

6

KADO

18

No of farmer processors

Buseta

Kadama

Kagumu

Kachede

Kobale

Kotiokot

Abuket

Kyere

Odapaeta

Kagumu

Bulangira

458

108

275

250

225

128

216

6656

9195

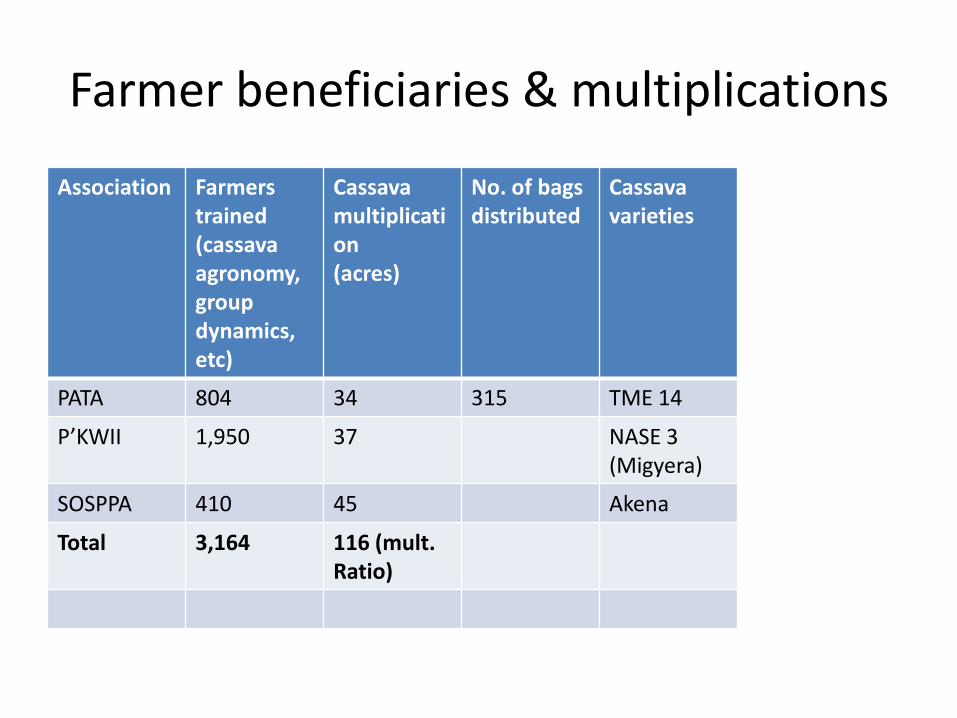

Farmer beneficiaries & multiplications

Association Farmerstrained (cassava agronomy, group dynamics, etc)

Cassava multiplication(acres)

No. of bags distributed

Cassava varieties

PATA 804 34 315 TME 14

P’KWII 1,950 37 NASE 3 (Migyera)

SOSPPA 410 45 Akena

Total 3,164 116 (mult. Ratio)

Farmer and processor beneficiaries(Apr 2010-March 2011)

Association Farmer beneficiaries

Processor beneficiaries

Total

PATA 142 662 804

P’KWII 1,200 750 1,950

SOSPPA - 410 410

KADO - 56 56

Bulangira - 91 91

Total 1,342 1,969 3,311

Target 432 400 832

Achievement for period (%)

310.65 492.25 397.96

Achievement for period end of march 2013 (%)

51.78 82.11 66.35

Number of farmer & processor beneficiaries

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1 2

Total

Target

Processors

Farmers

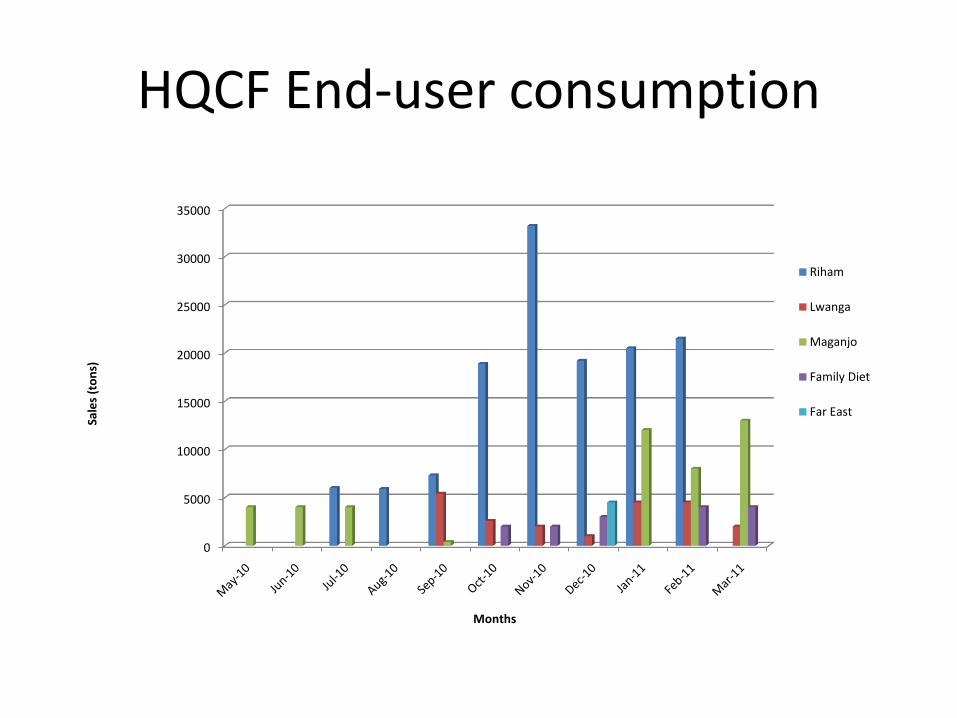

HQCF sales (end-user) achievements (kg)

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Total

Riham 6000 5900 7300 18900 33200 19200 20500 21500 132500Lwanga 5400 2600 2000 1000 4500 4500 2000 22000

Maganjo 4000 4000 4000 400 12000 8000 13000 45400

Family Diet 2000 2000 3000 4000 4000 15000

Far East 4500 4500

Total 4000 4000 10000 59001310

0 23500 37200 27700 37000 38000 19000 219400

HQCF sales achievements

0

5

10

15

20

25

30

35

40

45

Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10 Nov-10 Dec-10 Jan-11 Feb-11 Mar-11

Pro

du

ctio

n a

nd

Sal

es

(to

ns)

Months

Production and Sales

Production (tons)

Sales (tons)

HQCF End-user consumption

0

5000

10000

15000

20000

25000

30000

35000

Sale

s (t

on

s)

Months

Riham

Lwanga

Maganjo

Family Diet

Far East

End-user/sales of grits/HQCF (219.4t)

Riham

Lwanga

Maganjo

Family Diet

Far East

4.5

132.5

22.0

45.4

15.0

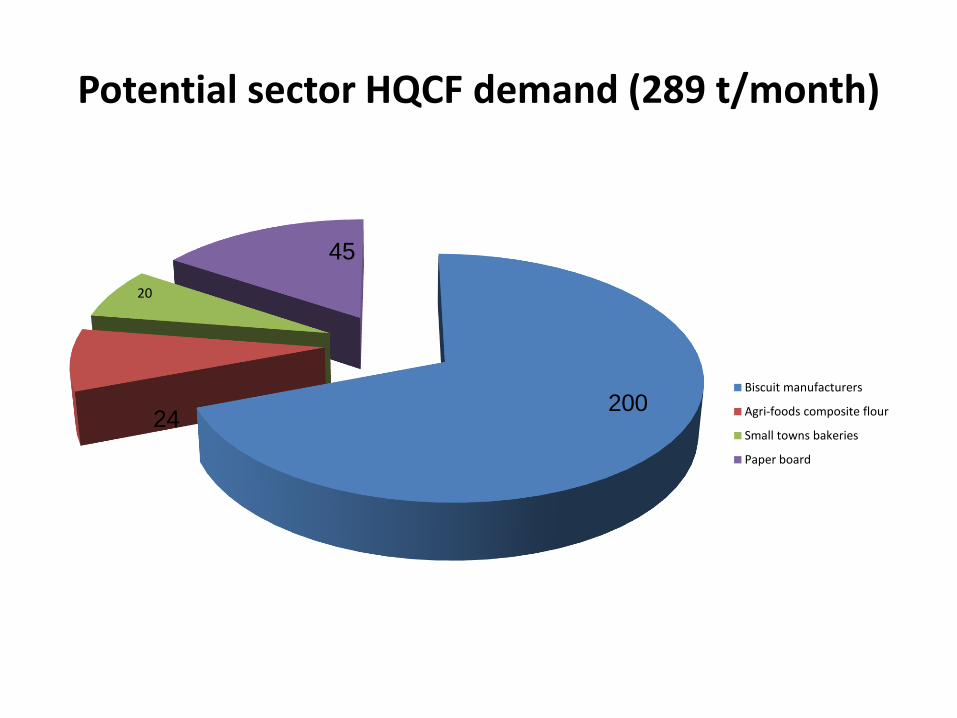

HQCF/Grits markets in Uganda

Sector Current demand(t/month)

Potential demand(t/month)

Biscuit manufacturers 100 200

Agri-foods composite flour 9 24

Small towns bakeries 10 20/ 33.8

Paper board - 45

Total per month 119 289

Total per annum 1,428 3,468

Current sector HQCF demands (119 t/month)

Biscuit manufacturers

Agri-foods composite flour

Small towns bakeries

100

9

10

Potential sector HQCF demand (289 t/month)

Biscuit manufacturers

Agri-foods composite flour

Small towns bakeries

Paper board

20

20024

45

Potential Mbale town bakeries HQCF demand

Bakery Location Potential HQCFDemand (t/month)

Famous bakery Industrial area 3.5

Elgon bakers Napooli area 4.0

Sweet bread bakery Industrial area 3.0

Ntake bakery Limited Industrial area 6.5

Star bakery Industrial area 3.5

Doko-Nsambya bakery Doko-Nsambya 4.0

Mile Tano bakery Mile 5 1.5

Total 26.0

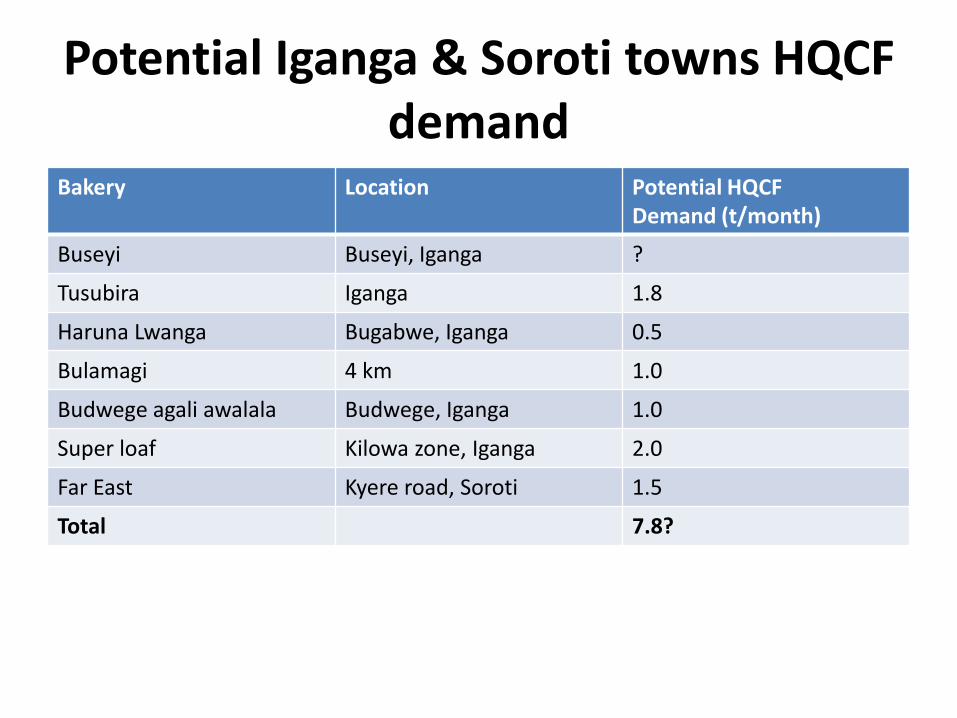

Potential Iganga & Soroti towns HQCF demand

Bakery Location Potential HQCFDemand (t/month)

Buseyi Buseyi, Iganga ?

Tusubira Iganga 1.8

Haruna Lwanga Bugabwe, Iganga 0.5

Bulamagi 4 km 1.0

Budwege agali awalala Budwege, Iganga 1.0

Super loaf Kilowa zone, Iganga 2.0

Far East Kyere road, Soroti 1.5

Total 7.8?

Success story

Key lessons learnt

• Market penetration of large end-users need marketing skills & persistence with clear benefits.

• Market penetration of small scale end-user markets.

• Integrated approach to market (HH, community level, small towns bakeries, retailing, large scale end-users).

Key lessons learnt (cont’d)

• Wheat vs HQCF prices not related at all. Prices of local cassava chips, fresh tuber roots, exchange rates, energy prices are equally critical in the promotion & pricing of HQCF.

• HQCF sun drying be integrated with production of other cassava products that need fermentation (gari).

• Need for Private sector in bulking, re-packaging & retailing.

Key lessons learnt (cont’d)

• Nearby markets with good infrastructure are a critical factor of success e.g mobile money (payments), good roads (transport of grits to family diet by Kyere/SOSPPA.

• Existence of association with past skills on selling in bulk enhances HQCF value chain development.

• Quality assurance in the food industry is evidence based & eminent.

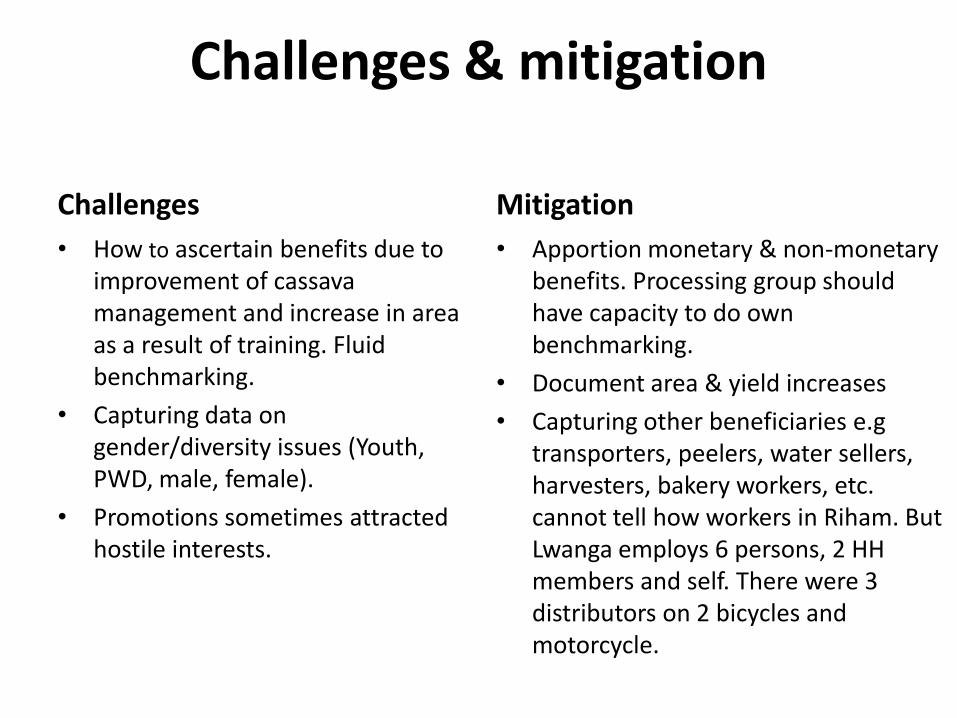

Challenges & mitigation

Challenges

• How to ascertain benefits due to improvement of cassava management and increase in area as a result of training. Fluid benchmarking.

• Capturing data on gender/diversity issues (Youth, PWD, male, female).

• Promotions sometimes attracted hostile interests.

Mitigation

• Apportion monetary & non-monetary benefits. Processing group should have capacity to do own benchmarking.

• Document area & yield increases

• Capturing other beneficiaries e.gtransporters, peelers, water sellers, harvesters, bakery workers, etc. cannot tell how workers in Riham. But Lwanga employs 6 persons, 2 HH members and self. There were 3 distributors on 2 bicycles and motorcycle.

Challenges & mitigation

Challenges

• Achieving appropriate particle size. Currently flour is too fine and tedious. 0.25mm sieve not in the market. This may require adjustments but there are engineers to do that. Hand sieving ensures final product is free from other particles like dead insects and pieces of vegetation before sealing of bags.

Mitigation

• Data forms designed & to be captured at community to country levels.

• Strengthen linkages & partnerships.

• East African Standard has been put at 0.18mm?

• Identifying milling as a critical control point to eliminate the need for hand sieving.

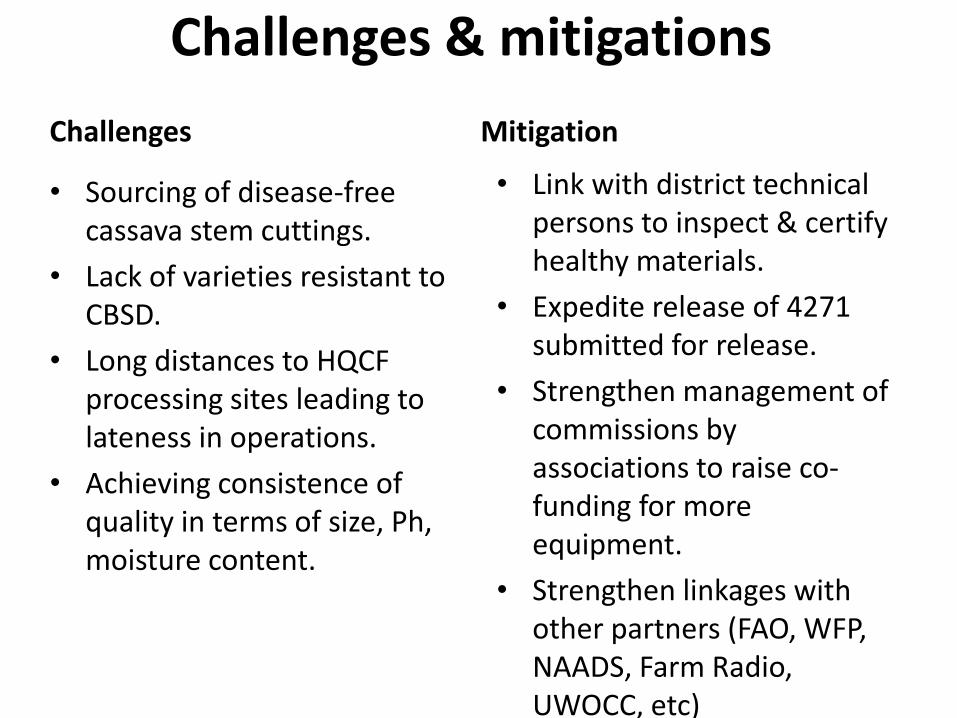

Challenges & mitigations

Challenges

• Sourcing of disease-free cassava stem cuttings.

• Lack of varieties resistant to CBSD.

• Long distances to HQCF processing sites leading to lateness in operations.

• Achieving consistence of quality in terms of size, Ph, moisture content.

Mitigation

• Link with district technical persons to inspect & certify healthy materials.

• Expedite release of 4271 submitted for release.

• Strengthen management of commissions by associations to raise co-funding for more equipment.

• Strengthen linkages with other partners (FAO, WFP, NAADS, Farm Radio, UWOCC, etc)