15

CBI Product Factsheet: Aprons in Europe

CBI | Market Intelligence Product Factsheet Cloves in Germany | 1

CBI Product Factsheet:

Aprons in Europe

CBI | Market Intelligence Product Factsheet Aprons in Europe | 2

Introduction

The home-cooking trend and the recovery of imports from developing countries offer interesting opportunities for

suppliers. Exporters of aprons are expected to find the most opportunities in the middle-high segments, where they will

not have to compete with China, India and other large suppliers who tend to dominate the lower segments.

Product Theme HS code PRODCOM code

Aprons Masterchef & Sharing

and Showing

Refer to Trend

mapping for more

information on this

theme.

6211.42.10

Women’s or girls’ aprons,

overalls, smock-overalls

and other industrial and

occupational clothing

(whether or not also

suitable for domestic

use) - in cotton

1412.2120

Women's or girls'

ensembles, in cotton or

man-made fibres, for

industrial or

occupational wear

Please note that HS and prodcom codes concern not only aprons but industrial and

occupational wear in general.

In terms of fabric, only cotton is included in the HS code.

As data for men´s aprons is unavailable, only women´s aprons are included in this survey.

For the aforementioned reasons, the data analysed below should only be used as a guide.

Aprons are protective clothing used during food preparation to protect clothing from being

stained and for hygienic reasons. It is a garment covering the front of the body and is used

both in restaurants and at home. Aprons can be made of several materials, but the ones used for cooking are mostly made of

cotton or other textile material. Waterproof household aprons can also be made of oilcloth

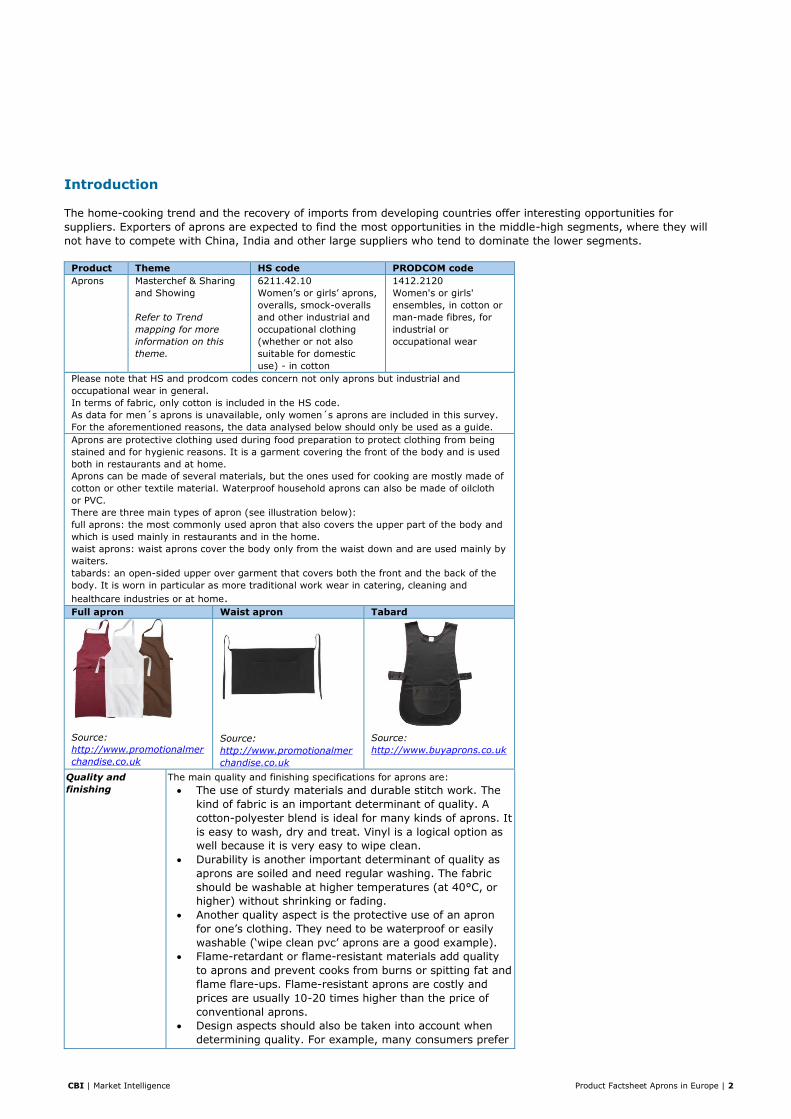

or PVC. There are three main types of apron (see illustration below):

full aprons: the most commonly used apron that also covers the upper part of the body and

which is used mainly in restaurants and in the home.

waist aprons: waist aprons cover the body only from the waist down and are used mainly by

waiters.

tabards: an open-sided upper over garment that covers both the front and the back of the

body. It is worn in particular as more traditional work wear in catering, cleaning and

healthcare industries or at home.

Full apron Waist apron Tabard

Source:

http://www.promotionalmer

chandise.co.uk

Source:

http://www.promotionalmer

chandise.co.uk

Source:

http://www.buyaprons.co.uk

Quality and

finishing

The main quality and finishing specifications for aprons are:

The use of sturdy materials and durable stitch work. The

kind of fabric is an important determinant of quality. A

cotton-polyester blend is ideal for many kinds of aprons. It

is easy to wash, dry and treat. Vinyl is a logical option as

well because it is very easy to wipe clean.

Durability is another important determinant of quality as

aprons are soiled and need regular washing. The fabric

should be washable at higher temperatures (at 40°C, or

higher) without shrinking or fading.

Another quality aspect is the protective use of an apron

for one’s clothing. They need to be waterproof or easily

washable (‘wipe clean pvc’ aprons are a good example).

Flame-retardant or flame-resistant materials add quality

to aprons and prevent cooks from burns or spitting fat and

flame flare-ups. Flame-resistant aprons are costly and

prices are usually 10-20 times higher than the price of

conventional aprons.

Design aspects should also be taken into account when

determining quality. For example, many consumers prefer

CBI | Market Intelligence Product Factsheet Aprons in Europe | 3

aprons with handy pockets or pouches and the ‘look’ of an

apron is becoming more and more important. As the

hospitality business depends a lot on image, ‘style’ is

something that should not be overlooked. Appealing

designs can be accomplished through an apron’s cut and

the material’s pattern. Aprons should thus be stylish and

practical in design at the same time.

Size Most aprons are one-sized as most of them can be adjusted to fit.

Common standard sizes (however they vary widely) for aprons in Europe

are:

Full apron: 61x84 cm, 58x73 cm, 60x70 cm, 73x80 cm

Waist apron: 30x60 cm, 35x60 cm, 60x100 cm

Tabard:

S M L XL

Unisex sizes 80x88 cm 92x100 cm 104x112 cm 116x124 cm

Labelling Labels for transport normally

include information on the

producer, consignee,

composition of the product

and the size of the product,

number of pieces, bale/box

identification and total

number of bales/boxes, and

net and gross weight.

Most important information on the product or packing

labels for aprons is composition, size, origin and care

labelling. Most European companies use the international

care labelling code GINETEX, which is a voluntary

labelling service to consumers. The use of their

symbols is dependent on a contract with

GINETEX.

For more information and illustrations of product

labelling, please refer to Labelling of home

textiles under Legal requirements. For more

information on GINETEX, please visit their

website: http://ginetex.net

(Examples of

GINETEX

symbols)

Packaging All products should be

packed in agreement with

the importer, and this

usually consists of plastic

wrapping to protect the

fabric from water, solar

radiation and staining. Proper packaging minimises the

risk of damage through fluctuations in humidity.

Packaging dimensions and weight should make it easy to

handle. Ideally, it should be possible to place packaging

together on pallets meaning that they should be stackable

and if possible of a convenient size.

Packaging symbols are nationally and internationally

standardised and added to communicate aspects of

transportation and product safety. The symbols above

stand for: ‘keep away from sunlight’ and ‘keep the

package away from rain or damp conditions’.

Aprons for domestic use are usually displayed and sold

hanging. Therefore, if used, consumer packaging must be

simple in design, but utilitarian: it needs to protect against

water and staining.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 4

Illustration

Sources:

Pauls Discount

(http://www.paulsdi

scount.co.uk)

Buy Aprons

(http://www.buyapr

ons.co.uk)

House of Fraser

(http://www.houseo

ffraser.co.uk)

Not on the

Highstreet

(http://www.notont

hehighstreet.com)

Basic aprons

Fashionable aprons

What is the demand for aprons in Europe?

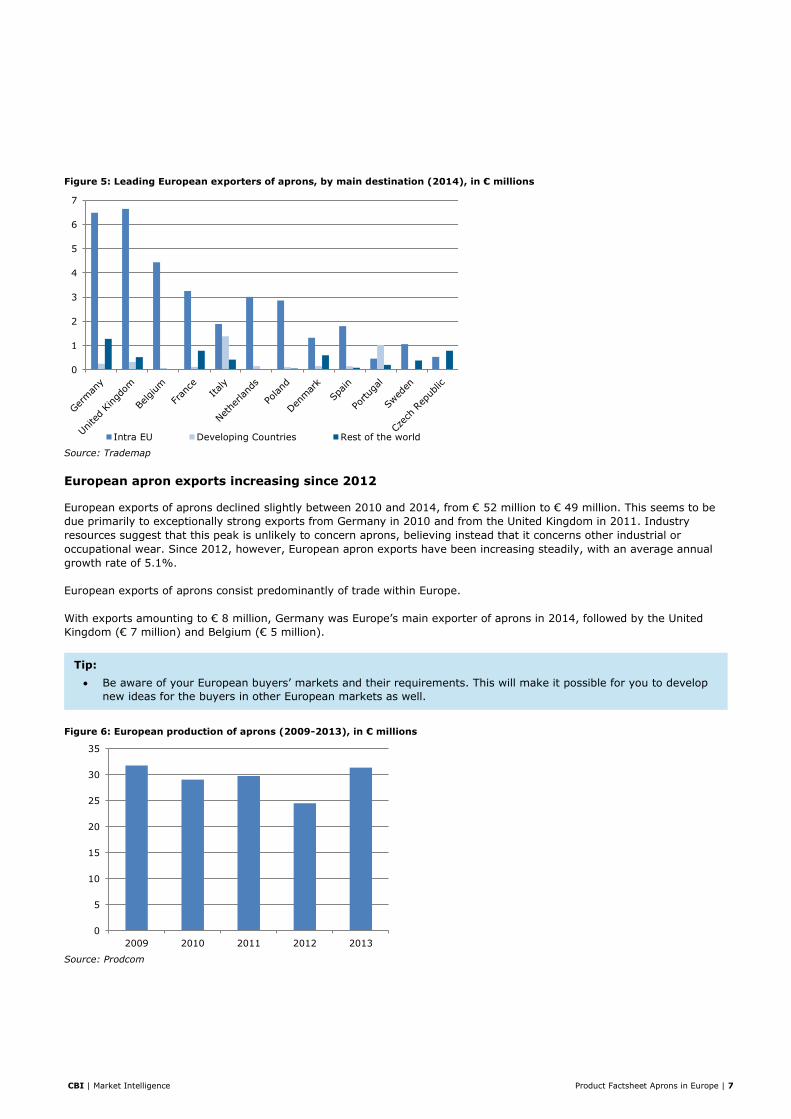

Following a period of fluctuation, European imports of aprons are increasing. Germany and the United Kingdom are

especially interesting focus markets for suppliers from developing countries. Most opportunities are located in the middle

and high-end markets, as the low-end market is dominated by inexpensive mass production from China and India.

Figure 1: European imports of aprons, by main origin, in € millions

Source: Trademap

0

10

20

30

40

50

60

2010 2011 2012 2013 2014

Intra EU Developing Countries Rest of the world

CBI | Market Intelligence Product Factsheet Aprons in Europe | 5

Figure 2: Leading European importers of aprons, by main origin (2014), in € millions

Source: Trademap

Figure 3: Absolute growth in imports from developing countries (2010-2014), in € millions (countries in order of import volume)

Source: Trademap

European imports of aprons are recovering

Between 2010 and 2014, European imports of aprons fluctuated, resulting in a slight decline from € 83 million to € 81

million, with an average annual growth rate of -0.8%. It is interesting to note that European imports of aprons increased in

2014, with an annual growth rate of 3.0%.

Given that developing countries are Europe’s leading source of aprons, European imports of aprons from developing

countries exhibited a similar pattern of fluctuation, decreasing slightly from € 54 million in 2010 to € 52 million in 2014,

with an average annual growth rate of -0.9%. In 2014, European apron imports from developing countries showed

recovery, with a promising growth of 4.8%. This recovery is expected to continue and, with it, the recovery of European

apron imports in general.

0

2

4

6

8

10

12

14

Intra EU Developing Countries Rest of the world

-3,0

-2,5

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

Tips:

Germany, France and the United Kingdom are by far the largest importers of aprons in Europe. With their strong

presence of suppliers from developing countries, Germany and the United Kingdom are especially interesting

focus markets.

Benchmark your products against the competition from China and India. Factors to consider include the market

segments served; perceived price and quality; and countries served. One source that can be used for finding

exporters by country is ITC Trademap.

The low-end market is dominated by products from China and India and it will be almost impossible to compete

with this type of cheap mass-production. Therefore, opportunities are mostly to be found in the middle and high-

end markets, implying that you will need to pay particular attention to design and high-quality.

Source: Eurostat

(2013)

Source: Eurostat

(2013) Source: Eurostat

(2013)

Source: Eurostat

(2013)

Source: Eurostat

(2013)

CBI | Market Intelligence Product Factsheet Aprons in Europe | 6

With imports valued at € 17 million, Germany was Europe’s leading importer of aprons in 2014, followed by France (€ 13

million) and the United Kingdom (€ 11 million). Germany is also the leader in apron imports from developing countries (€

13 million), followed by the United Kingdom (€ 10 million) and France (€ 7.0 million).

The strong performance of apron suppliers from developing countries in Germany is further evidenced by its increase of

€ 1.3 million between 2010 and 2014. Imports of aprons from developing countries also increased in the United Kingdom,

Denmark, Sweden, Spain and the Netherlands (ranging from € 0.1 million to € 0.8 million). In France, Italy and Belgium,

however, apron imports from developing countries declined (by € 2.4 million, € 1.3 million and € 1.2 million, respectively).

European apron imports are dominated by China (€ 18 million) and India (€ 14 million). Other leading suppliers from

developing countries include Pakistan (€ 4.5 million), Tunisia (€ 4.4 million), Indonesia (€ 2.7 million), Turkey

(€ 2.0 million) and Morocco (€ 1.7 million).

Several other developing countries are also performing well. Ukraine is among the leading suppliers of aprons in Germany.

France also imports from Bangladesh and Madagascar. In the United Kingdom, Cambodia is the fourth largest supplier of

aprons.

Figure 4: European exports of aprons, by main destination, in € millions

Source: Trademap

0

10

20

30

40

50

60

2010 2011 2012 2013 2014Intra EU Developing Countries Rest of the world

Tips:

Invest in long-term relationships with your buyers, giving them less incentive to switch to a competitor. In this

highly competitive market, buyer power is relatively strong.

In the longer run, Eastern European countries might form a threat as well, as transportation time and costs are

much lower than for developing countries.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 7

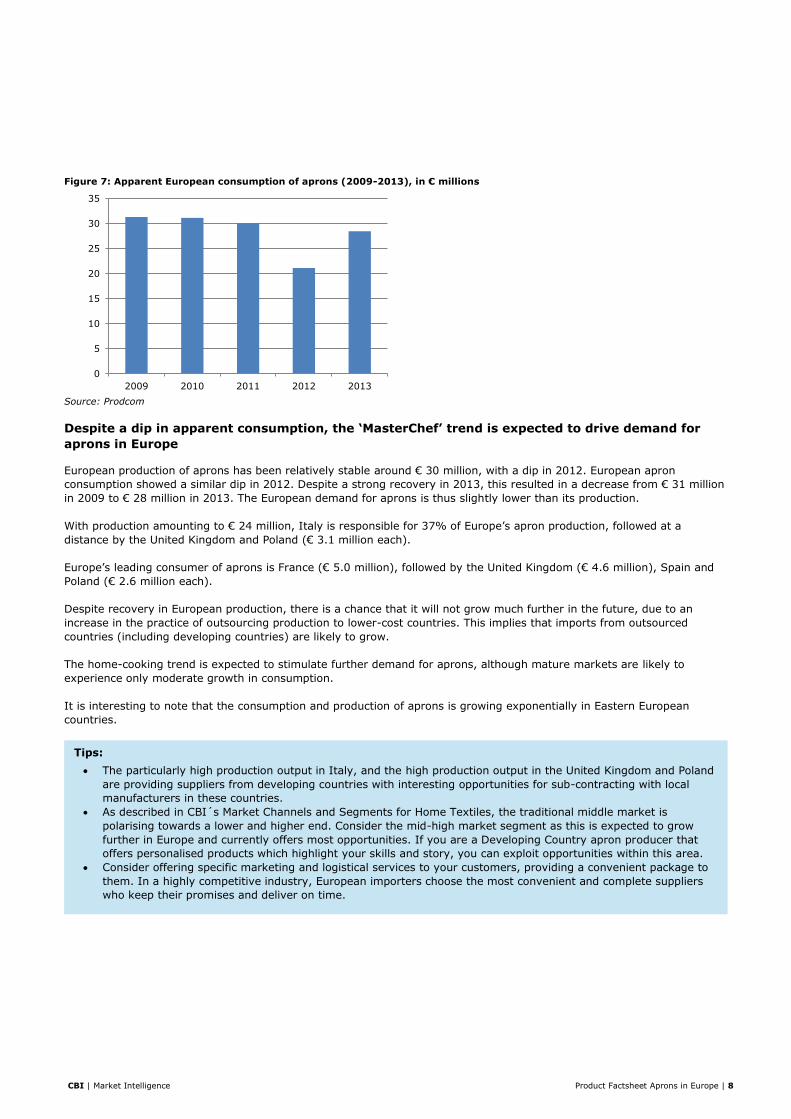

Figure 5: Leading European exporters of aprons, by main destination (2014), in € millions

Source: Trademap

European apron exports increasing since 2012

European exports of aprons declined slightly between 2010 and 2014, from € 52 million to € 49 million. This seems to be

due primarily to exceptionally strong exports from Germany in 2010 and from the United Kingdom in 2011. Industry

resources suggest that this peak is unlikely to concern aprons, believing instead that it concerns other industrial or

occupational wear. Since 2012, however, European apron exports have been increasing steadily, with an average annual

growth rate of 5.1%.

European exports of aprons consist predominantly of trade within Europe.

With exports amounting to € 8 million, Germany was Europe’s main exporter of aprons in 2014, followed by the United

Kingdom (€ 7 million) and Belgium (€ 5 million).

Figure 6: European production of aprons (2009-2013), in € millions

Source: Prodcom

0

1

2

3

4

5

6

7

Intra EU Developing Countries Rest of the world

0

5

10

15

20

25

30

35

2009 2010 2011 2012 2013

Tip:

Be aware of your European buyers’ markets and their requirements. This will make it possible for you to develop

new ideas for the buyers in other European markets as well.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 8

Figure 7: Apparent European consumption of aprons (2009-2013), in € millions

Source: Prodcom

Despite a dip in apparent consumption, the ‘MasterChef’ trend is expected to drive demand for

aprons in Europe

European production of aprons has been relatively stable around € 30 million, with a dip in 2012. European apron

consumption showed a similar dip in 2012. Despite a strong recovery in 2013, this resulted in a decrease from € 31 million

in 2009 to € 28 million in 2013. The European demand for aprons is thus slightly lower than its production.

With production amounting to € 24 million, Italy is responsible for 37% of Europe’s apron production, followed at a

distance by the United Kingdom and Poland (€ 3.1 million each).

Europe’s leading consumer of aprons is France (€ 5.0 million), followed by the United Kingdom (€ 4.6 million), Spain and

Poland (€ 2.6 million each).

Despite recovery in European production, there is a chance that it will not grow much further in the future, due to an

increase in the practice of outsourcing production to lower-cost countries. This implies that imports from outsourced

countries (including developing countries) are likely to grow.

The home-cooking trend is expected to stimulate further demand for aprons, although mature markets are likely to

experience only moderate growth in consumption.

It is interesting to note that the consumption and production of aprons is growing exponentially in Eastern European

countries.

0

5

10

15

20

25

30

35

2009 2010 2011 2012 2013

Tips:

The particularly high production output in Italy, and the high production output in the United Kingdom and Poland

are providing suppliers from developing countries with interesting opportunities for sub-contracting with local

manufacturers in these countries.

As described in CBI´s Market Channels and Segments for Home Textiles, the traditional middle market is

polarising towards a lower and higher end. Consider the mid-high market segment as this is expected to grow

further in Europe and currently offers most opportunities. If you are a Developing Country apron producer that

offers personalised products which highlight your skills and story, you can exploit opportunities within this area.

Consider offering specific marketing and logistical services to your customers, providing a convenient package to

them. In a highly competitive industry, European importers choose the most convenient and complete suppliers

who keep their promises and deliver on time.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 9

Figure 8: Real GDP (2014-2016), % change from previous year

Source: Eurostat (2015)

Figure 9: Real private consumption expenditures (2014-2016), % change from previous year

Source: Eurostat (2015)

Economic indicators are promising

Predictions of GDP and private consumption expenditures are important indicators for the European apron market. The

home-textiles sector, which consists predominantly of non-essential items, is closely linked to economic conditions. When

money is tight, consumers can easily postpone replacing non-essential items like aprons until they once again have

sufficient disposable income.

Between 2014 and 2016, European GDP and private consumption expenditures are expected to increase. This means that

the consumption of luxury and decorative products is also likely to rise. Increases in GDP create room for this type of

spending, especially in emerging markets. Due to saturation, growth in consumption will be moderate for mature markets.

Which trends offer opportunities on the European market for aprons?

The economic down-turn and a revived interest in nutrition, health and local food have increased home cooking.

Consumers of aprons in emerging markets generally follow the same trends as those observed in established markets,

although a smaller part of the population is interested in aprons as fashionable accessories.

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

2014 2015 2016

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

2014 2015 2016

Tip:

Monitor GDP and private consumption expenditures. When these indicators are positive, expenditures for aprons

and other home textiles are expected to increase.

Source: Eurostat

(2013)

Source: Eurostat

(2013) Source: Eurostat

(2013)

CBI | Market Intelligence Product Factsheet Aprons in Europe | 10

Master chefs

Consumers are now spending more time in the kitchen which has led to a trend of amateur home cooks ‘presenting

themselves as master chefs’. In line with this, people are willing to pay more for professional quality kitchenware

(durability, energy/space saver, ergonomic, ‘glam’ kitchen tools etc.). A lot of the kitchen story is linked to ‘showing’ the

space, the equipment and ‘sharing’ the meal. This is likely to boost the market for (fashionable) aprons as well. Aprons can

be as expressive as any other pieces of clothing and still maintain a practical function.

The middle market is polarising towards a lower and higher end segment

The lower market segment is betting on extremely low prices at the expense of a product’s quality. This trend requires

innovative ways to keep production costs as low as possible. Examples are smaller sized aprons and loosely woven cotton;

low-end aprons are becoming as basic as possible. In order to add value to lower priced aprons, there is a strong trend

towards the use of prints which is relatively cheap, especially when compared to higher quality weaving.

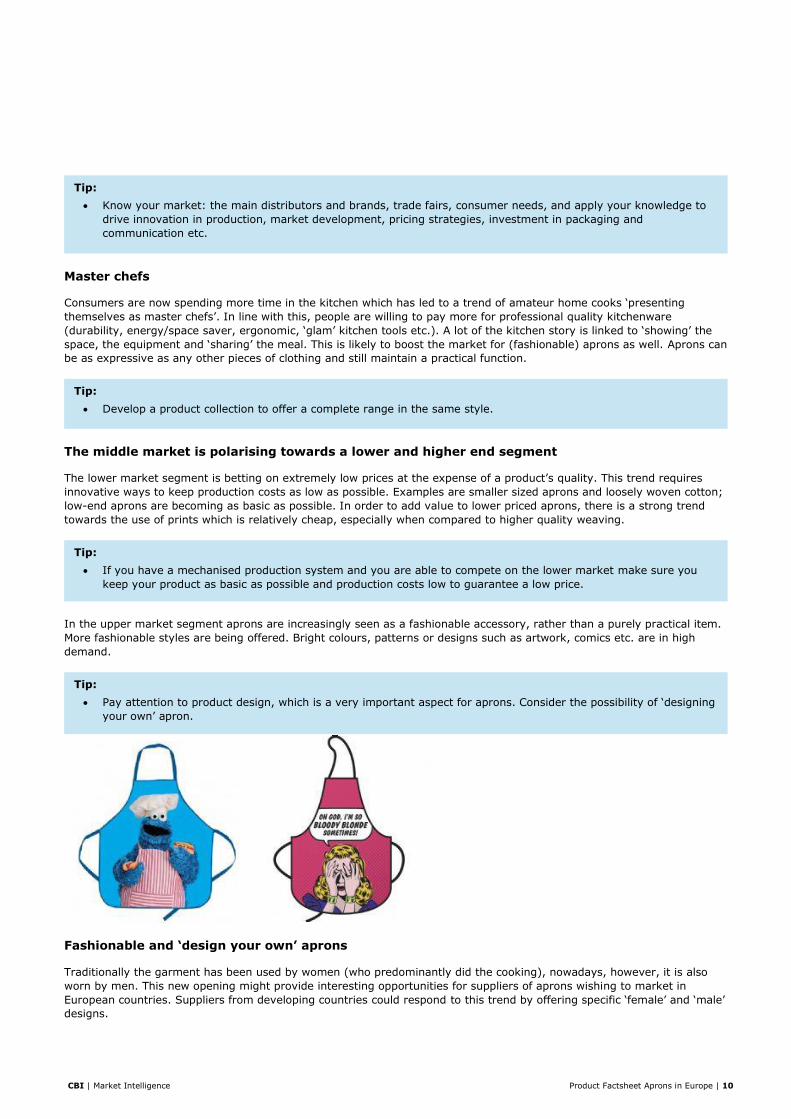

In the upper market segment aprons are increasingly seen as a fashionable accessory, rather than a purely practical item.

More fashionable styles are being offered. Bright colours, patterns or designs such as artwork, comics etc. are in high

demand.

Fashionable and ‘design your own’ aprons

Traditionally the garment has been used by women (who predominantly did the cooking), nowadays, however, it is also

worn by men. This new opening might provide interesting opportunities for suppliers of aprons wishing to market in

European countries. Suppliers from developing countries could respond to this trend by offering specific ‘female’ and ‘male’

designs.

Tip:

Know your market: the main distributors and brands, trade fairs, consumer needs, and apply your knowledge to

drive innovation in production, market development, pricing strategies, investment in packaging and

communication etc.

Tip:

Develop a product collection to offer a complete range in the same style.

Tip:

If you have a mechanised production system and you are able to compete on the lower market make sure you

keep your product as basic as possible and production costs low to guarantee a low price.

Tip:

Pay attention to product design, which is a very important aspect for aprons. Consider the possibility of ‘designing

your own’ apron.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 11

A general trend in ‘design your own’ products has also reached the market for aprons. The development of websites that

offer custom made aprons is increasing and such aprons are often sold as gifts (http://www.customapron.co.uk/).

Aprons as gift items

As the practical use of an apron in the higher segment is making way for appearance and decorative aspects, an

opportunity can be found within the gift market. Entering the gift market with your apron could increase your chances on

the European market.

Environmental and social responsibility

Even though it is still niche, there is a trend towards the use of more sustainable materials and a sustainable production

process. This trend is growing strongly in the apron market. Social and environmental responsibility is an increasingly

important aspect when addressing the mid-high to high-end market segment. You can address this trend by using and

promoting natural materials or recycled fibres, or by obtaining certification.

The protective role of aprons

Protection is playing an increasingly important role. New designs are being offered to meet the highest hygienic

requirements. ‘Easy to wipe clean’ or waterproof household aprons are the most popular offers.

Please refer to CBI Trend mapping for Home Decoration & Textiles for more information on general trends in home textiles,

and the ‘masterchef’ theme in specific.

With which requirements should aprons comply in order to be allowed on the European

market?

Musts

Product safety

Products placed on the European market should be safe when used as intended. The European Union has regulated

product safety in the General Product Safety Directive (GPSD), which applies to all consumer products marketed in Europe.

Tip:

As men are increasingly making use of aprons, make sure that you can deliver aprons in different styles to cater

to customers of both genders.

Tip:

If you consider entering the gift market with aprons make sure you can offer your product in a gift package. It

also requires more marketing efforts. Co-creation with producers, retailers and marketers can increase your

opportunities on this market.

Tips:

Promote the use of alternative natural materials, like linen or cotton and address the ‘sustainability’ or your

unique selling point of your product so that buyers are aware of this. The main way to differentiate in the apron

market is by making unique combinations of materials.

You can also use organic cotton or other certifications to further enhance your product. Please refer to non-

legislative requirements for the relevant certifications in the apron market.

Tip:

In order to satisfy the demand for waterproof aprons, offer aprons of different materials such as oilcloth or PVC.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 12

European legislation prohibits the presence of certain flame retardants in textile products that come into contact with

skin, including aprons. If your products do not comply with this legislation, they will be withdrawn from the European

market.

Textile Labelling

The European Union has harmonised legislation regarding the names, composition and labelling of textile products

Chemical substances

The use of several chemicals in textiles is restricted

Azo dyes are often used in the dyeing process for several textile products. The use of certain azo dyes is illegal in Europe,

as these dyes can be carcinogenic.

Additional requirements

Social and environmental responsibility on the rise

Consumers are increasingly aware of social and environmental circumstances during production. As a consequence,

requirements regarding sustainability and certification are becoming more important to buyers.

Implementing a management system (e.g. ISO 14000 for environmental aspects or SA 8000 for social conditions), or

using sustainably produced (e.g. organic or Oeko-Tex certified) materials may give you competitive advantage.

Codes of conduct

European buyers may expect you to comply with their supplier codes of conduct, which are often based on the ILO labour

standards. This could be the importer’s own code of conduct or a code of conduct as a part of an initiative in which the

importer is participating (e.g. ETI or BSCI).

Tip:

Consider implementing a management system or code of conduct in order to show to your buyer that you have

taken appropriate safety measures.

Tip:

Stay up-to-date on developments by the sector regarding alternative substances to the prohibited flame

retardants TRIS, TEPA and PBB. You can do so for instance through the European Flame Retardants Association

(EFRA).

Tip:

Make sure that your products comply with labelling requirements; you need to indicate the fibre content using

prescribed fibre names.

Tips:

Make sure that your aprons do not contain any of the azo dyes that are prohibited in Europe.

Consider natural dyes for your products, which are a sustainable alternative to azo dyes.

Tips:

Think about sustainable production methods and consider certification because it adds value to your products.

This is useful when targeting the higher market segments.

Be aware that implementing management systems can be expensive. Make a proper cost calculation before you

start the certification process.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 13

Codes of conduct

European buyers may expect you to comply with their supplier codes of conduct, which are often based on the ILO labour

standards. This could be the importer’s own code of conduct or a code of conduct as a part of an initiative in which the

importer is participating (e.g. ETI or BSCI).

The Ethical Trading Initiative (ETI) is an alliance of companies, trade unions and voluntary organisations that partner up to

improve the working conditions of poor and vulnerable workers who make or grow consumer goods across the globe.

The Business Social Compliance Initiative (BSCI) has been developed by European retailers to improve social conditions in

sourcing countries. Suppliers of BSCI participants are expected to comply with the BSCI Code of conduct. To prove

compliance, your production process can be audited at the request of the importer. Once a company is audited, it will be

included in a database which can be used by all BSCI participants.

Consumer Labels

There are several labels for textile products which may give your items a competitive advantage. For example:

The Global Organic Textile Standard (GOTS) is a textile-processing standard for organic fibres. Textile products that

contain a minimum of 70% organic fibres can obtain GOTS certification.

Tip:

European buyers are increasingly taking responsibility for improving the working conditions of the people who

make the products they sell. Companies with a commitment to ethical trade can adopt a code of labour practice

that they expect all of their suppliers to work towards. Such codes address issues like wages, hours of work,

health and safety and the right to join free trade unions.

Tip:

As more and more European importers participate in BSCI, you can expect that complying with the BSCI code of

conduct will be seen as a basic requirement. Because it can harm your position on the market if you are far from

complying with this initiative, you are advised to anticipate by performing a self-assessment, which is available on

the BSCI website.

Tip:

Check the possibility of sourcing organic raw material for your aprons as it attracts buyers who search for

environmentally friendly or ethical products.

CBI | Market Intelligence Product Factsheet Aprons in Europe | 14

The Oeko-Tex Standard consists of three certifications for textiles. These address the effects of textile production

processes on humans and the environment, as well as the effects of the textiles themselves (including the chemicals) on

the health and well-being of consumers

Care Labelling

There is no Europe-wide legislation on the use of symbols for washing instructions and other care aspect of textile clothing

articles. This is odd as consumers consider care information to be the second most important aspect of information on a

product’s label (after size). You are therefore advised to follow ISO standards on this matter.

What competition do I face on the European market for aprons?

Please refer to CBI Competition for Home Decoration & Home Textiles and CBI Top 10 Tips for Doing Business with

European Buyers, because competitiveness for aprons does not differ significantly from this general overview.

What do the trade channels and interesting market segments for aprons look like in

Europe?

Please refer to CBI Market Channels and Segments for Home Textiles, because apron channels and segments do not differ

significantly from this general overview. The following additional aspect should be taken into account:

Please note that small and medium sized enterprises from developing countries will struggle to directly reach the B-

to-B market. They are more likely to find opportunities through buying agents and importers/wholesalers.

E-commerce is growing in importance. Consider targeting online retailers, in order to reach a broader range of

customers. This means, however, supplying small batches/being prepared to pre-stock and offer more just-in-time

supply concepts. As e-commerce is expected to grow explosively in the coming years, this could be a strategy for

exporters that can scale up in a short time span.

Useful Sources

The following trade associations and fairs are useful sources for finding trading partners in Europe.

British Home Enhancement Trade Association - http://www.bheta.co.uk

Natural & Organic Products Europe - http://www.naturalproducts.co.uk

Pure (London, United Kingdom) – http://www.purelondon.com

Heimtextil (Frankfurt, Germany) - http://www.heimtextil.de

Ambiente (Frankfurt, Germany) - http://ambiente.messefrankfurt.com

Prêt à Porter Paris (Paris, France) – http://www.whosnext.com

Maison & Objet (Paris, France) - http://www.maison-objet.com

Pitti Immagine (Florence, Italy) – http://www.pittimmagine.com

Tip:

Consider the Oeko-Tex Standard for your product. This standard is mainly used for textile products that come into

direct contact with skin, like aprons (53% of the certificates were in this product class in 2011, making it the

largest category).

Tip:

Many European retailers use care symbols instead of words. You are advised to follow ISO 3758: 2012 on care

labelling.

Source: Eurostat,

2013

CBI Market Intelligence

P.O. Box 93144

2509 AC The Hague

The Netherlands

www.cbi.eu/market-information

This survey was compiled for CBI by Globally Cool: Creative solutions for sustainable business,

in collaboration with CBI sector expert Remco Kemper

Disclaimer CBI market information tools: http://www.cbi.eu/disclaimer

September 2015