16

CCAB Training Providers Event 17 November 2008 Reviews Required by QAC Heather Briers Director Chartered Accountants Regulatory Board Chartered Accountants Regulatory Board

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | jeffrey-west |

| View: | 213 times |

| Download: | 0 times |

CCAB Training Providers Event 17 November 2008

Reviews Required by QAC

Heather BriersDirector

Chartered Accountants Regulatory Board

Chartered Accountants Regulatory Board

Mission and Values

Our Purpose

To regulate members of the Institute of Chartered Accountants in Ireland, independently, openly and in the public interest

Our Mission

To deliver a regulatory system of the highest quality thereby enhancing the confidence of all stakeholders

Committee Organisation Chart

Compliance

Quality Assurance Committee

InsolvencyLicensing

Committee

ComplaintsCommittee

DisciplinaryTribunal

Review Committee

Appeal Committee

Co-OrdinatingPolicy

Professional StandardsCommittee

Ethics Committee

Planning, Budget and

PerformanceCommittee

UK Joint Recognised Professional

Bodies

Joint Insolvency Committee

JointAudit

Committee

Joint Professional Indemnity Insurance

Committee

CCAB Ethics Group

Joint Chartered Accountants Committees

JointInvestment Business

Committee

Chartered Accountants Regulatory Board

Chartered Accountants Compensation Scheme

Board

Governance, Risk and Audit

Committee

Quality Assurance

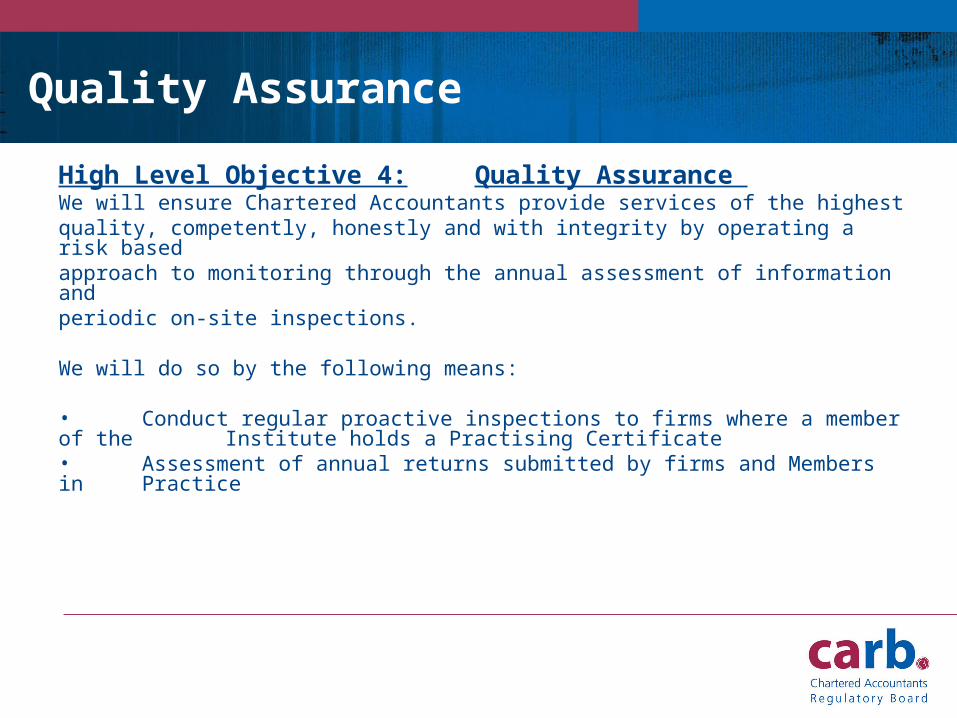

High Level Objective 4: Quality Assurance We will ensure Chartered Accountants provide services of the highestquality, competently, honestly and with integrity by operating a risk based approach to monitoring through the annual assessment of information andperiodic on-site inspections.

We will do so by the following means:

• Conduct regular proactive inspections to firms where a member of the Institute holds a Practising Certificate

• Assessment of annual returns submitted by firms and Members in Practice

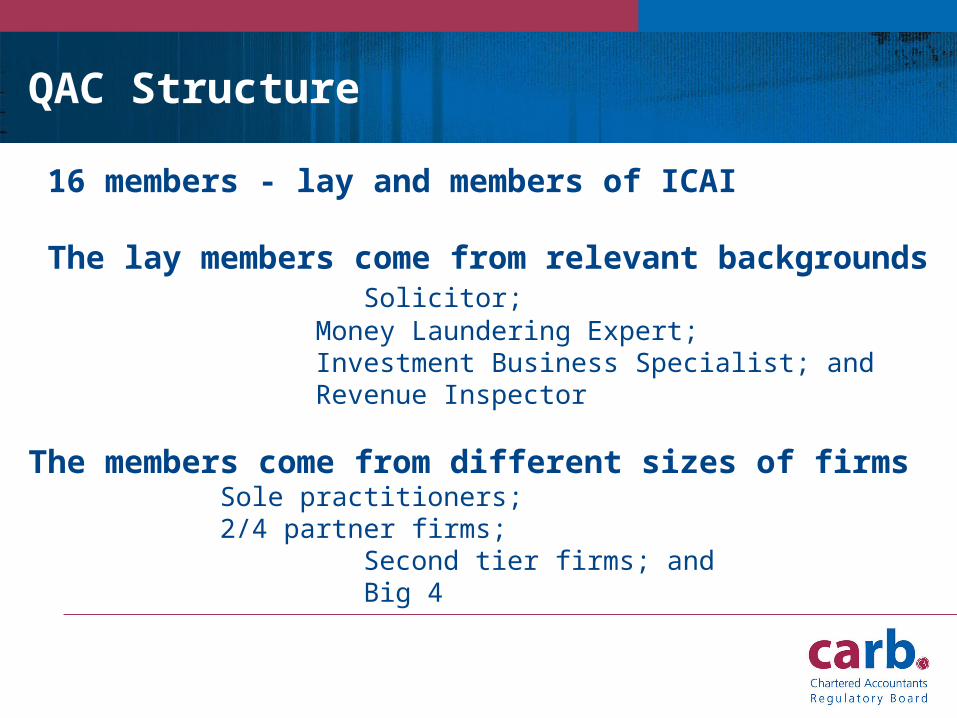

QAC Structure

16 members - lay and members of ICAI

The lay members come from relevant backgroundsSolicitor;

Money Laundering Expert;Investment Business Specialist; andRevenue Inspector

The members come from different sizes of firms Sole practitioners;2/4 partner firms;

Second tier firms; and Big 4

QAC Goals

• To improve the standards and quality

• To ensure compliance going forward

• To ensure adequate procedures

• To ensure that practitioners have the appropriate

competence

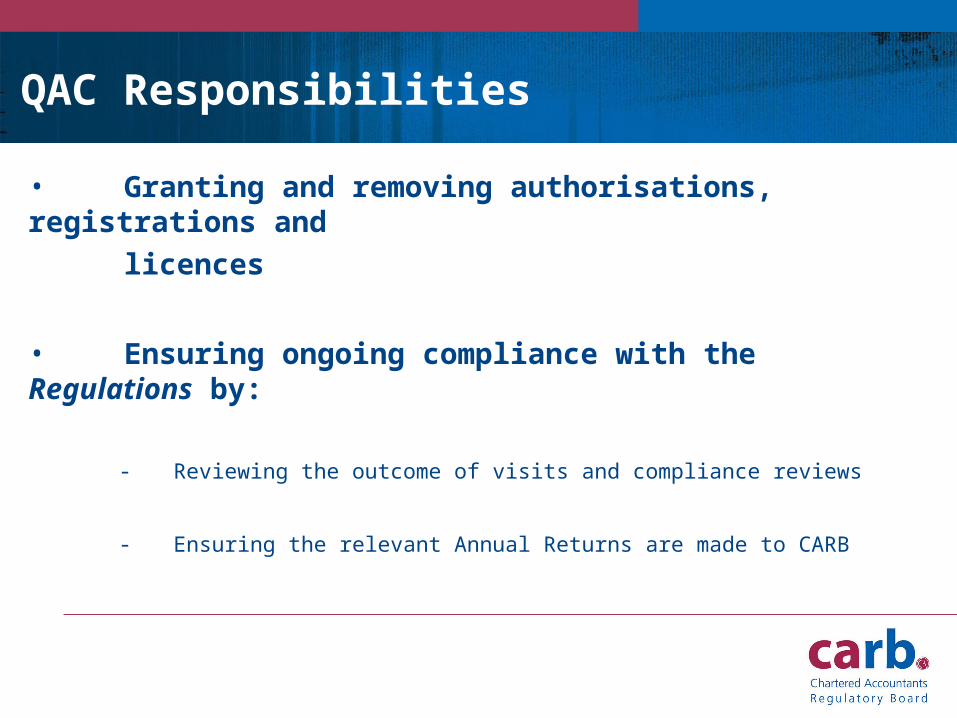

QAC Responsibilities

• Granting and removing authorisations, registrations and

licences

• Ensuring ongoing compliance with the Regulations by:

- Reviewing the outcome of visits and compliance reviews

- Ensuring the relevant Annual Returns are made to CARB

Committee Sanctions

• Remove any licence etc• Suspend any licence etc • Restrict any licence etc• Impose conditions on the firm or any individual • Require a monitoring visit• Offer a regulatory penalty• Make a referral to the Complaints Committee

Restrictions and Suspensions

Restrictions include:• Restricting the type of audit client, eg, no new regulated

client• No new investment business clients• Not providing compliance review for others.

Suspension means: • The firm will not be allowed to take on any new Audit or IB

clients• Hot File Reviews will be required• The firm is under ongoing supervision and monitoring

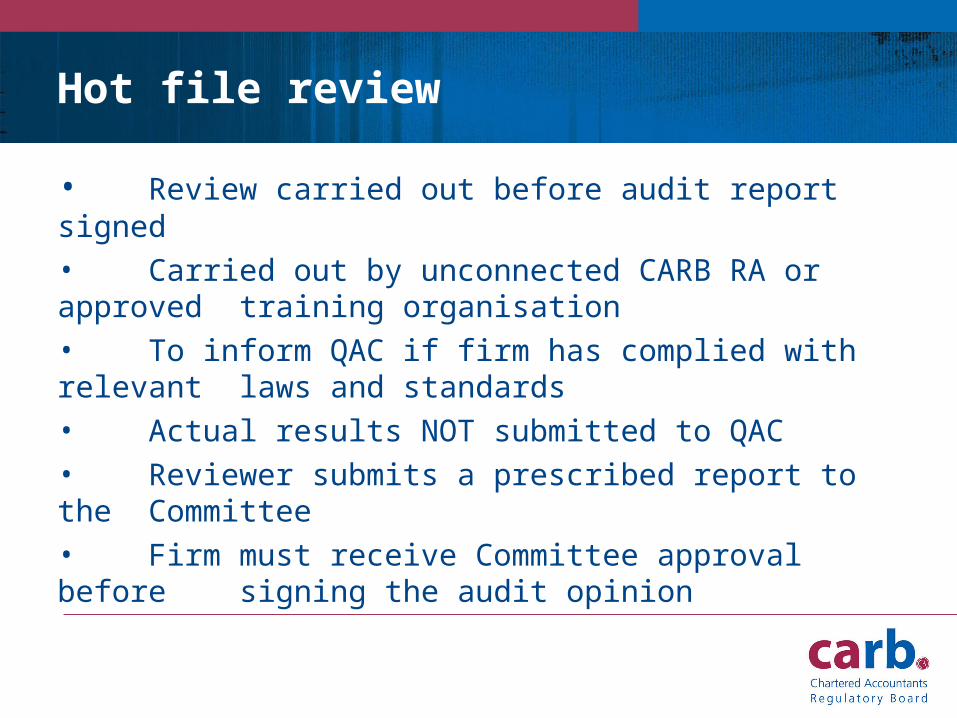

Hot file review

• Review carried out before audit report signed

• Carried out by unconnected CARB RA or approved training organisation

• To inform QAC if firm has complied with relevant laws and standards

• Actual results NOT submitted to QAC• Reviewer submits a prescribed report to the Committee • Firm must receive Committee approval before signing the audit opinion

Hot File Review Report

• Client company name• Confirmation review conducted in accordance with

firm and QAC instructions• Statement that the reviewing entity has not performed a second audit• Statement that the report for QAC use only• Details of remedial action required by the firm before

the reviewer could issue the report

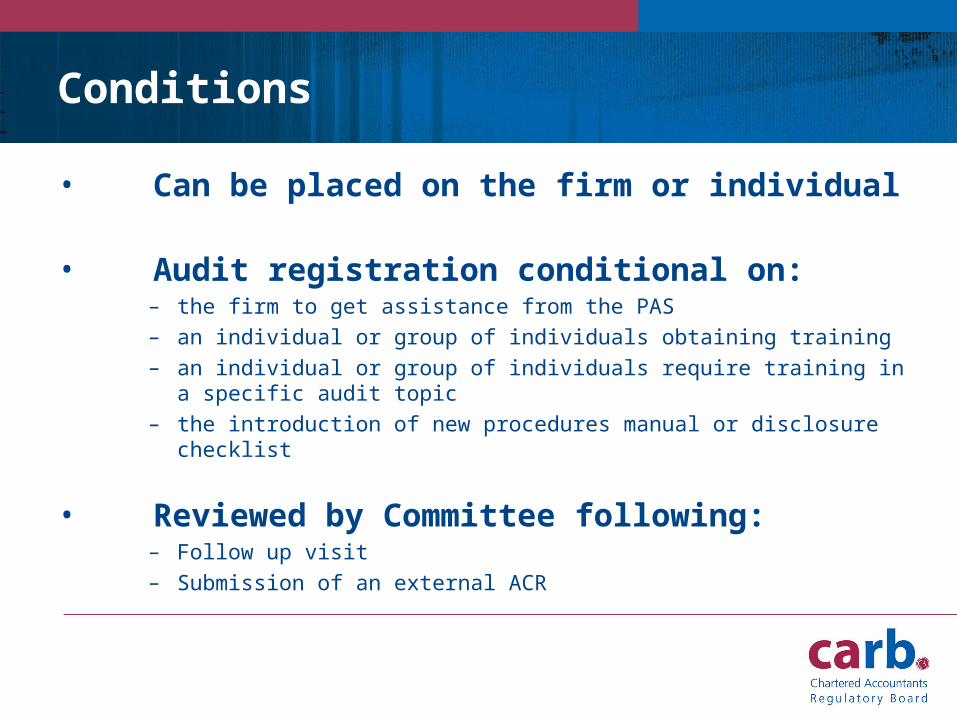

Conditions

• Can be placed on the firm or individual

• Audit registration conditional on:– the firm to get assistance from the PAS– an individual or group of individuals obtaining training– an individual or group of individuals require training in a specific audit topic– the introduction of new procedures manual or disclosure checklist

• Reviewed by Committee following:– Follow up visit– Submission of an external ACR

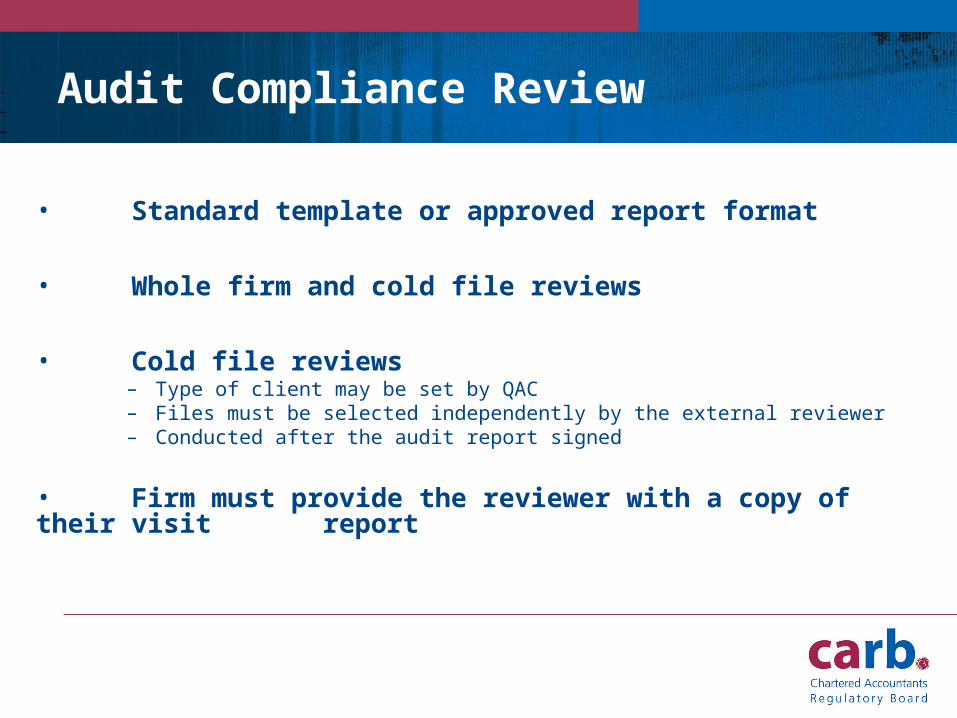

Audit Compliance Review

• Standard template or approved report format

• Whole firm and cold file reviews

• Cold file reviews – Type of client may be set by QAC– Files must be selected independently by the external reviewer– Conducted after the audit report signed

• Firm must provide the reviewer with a copy of their visit report

Audit Compliance Review

• Report must confirm (or otherwise) compliance with:– ISA’s– Statutory disclosure requirements provisions– The ICAI Audit Regulations and Guidance

• Report must include an:– overall conclusion on the quality of performance– assessment of the remedial action taken since the QA visit

• Firm must provide an action plan of remedial action to address breaches

Issues

• Incorrect (or insufficient number) files reviewed

• Files pre selected by the firm

• Breaches V Matters for Improvement unclear

• Report deficiencies including:– Lack of overall assessment– No reference to improvements from QR visit

• Changes in previously approved report format

• Report not signed off by the external reviewer

• Action plan not completed by the firm

Thank you

Heather BriersDirector

Chartered Accountants Regulatory Board

Chartered Accountants Regulatory Board