November 2014 TaxMatters@EY CCPC status and unanimous shareholder agreements Gael Melville, Vancouver The Canada Revenue Agency (CRA) recently reversed its longstanding position regarding the application of a unanimous shareholders’ agreement (USA) when determining Canadian- controlled private corporation (CCPC) status. Corporations qualifying as CCPCs enjoy a number of tax preferences that may include: • Reduced rate of income tax on up to $500,000 per annum of active business income • Enhanced rate of 35% (vs. 15%) scientific research investment tax credits • Refundable (vs. applied to income tax otherwise payable) investment tax credits Background In very general terms, a corporation that is controlled by nonresidents or by public or listed corporations cannot be a CCPC. For purposes of calculating whether such shareholders hold sufficient shares to control a corporation, the CCPC definition for income tax purposes sets out a hypothetical person test. The shareholdings of all nonresidents, public corporations and listed corporations are aggregated and treated as though they were in the hands of a single shareholder. If that hypothetical shareholder would control the corporation, the corporation fails the test and cannot be a CCPC. Building a better working world means understanding your tax situation and how the ever-changing global tax landscape affects you. TaxMatters@EY is a monthly Canadian bulletin that summarizes recent tax news, case developments, publications and more. For more information, please contact your EY advisor. In this issue What boards should know about the OECD BEPS initiative 5 That time of year again: GST/HST and taxable benefits 3 Active trading in an RRSP is not evidence of a trading business 7 Publications and articles 10

Transcript

November 2014

TaxMatters@EY

CCPC status and unanimous shareholder agreements Gael Melville, Vancouver

The Canada Revenue Agency (CRA) recently reversed its longstanding position regarding the application of a unanimous shareholders’ agreement (USA) when determining Canadian-controlled private corporation (CCPC) status.

Corporations qualifying as CCPCs enjoy a number of tax preferences that may include:

• Reduced rate of income tax on up to $500,000 per annum of active business income

• Refundable (vs. applied to income tax otherwise payable) investment tax credits

BackgroundIn very general terms, a corporation that is controlled by nonresidents or by public or listed corporations cannot be a CCPC. For purposes of calculating whether such shareholders hold sufficientsharestocontrolacorporation,theCCPCdefinitionforincometaxpurposessetsout a hypothetical person test. The shareholdings of all nonresidents, public corporations and listed corporations are aggregated and treated as though they were in the hands of a single shareholder. If that hypothetical shareholder would control the corporation, the corporation fails the test and cannot be a CCPC.

Building a better working world means understanding your tax situation and how the ever-changing global tax landscape affects you. TaxMatters@EY is a monthly Canadian bulletin that summarizes recent tax news, case developments, publications and more. For more information, please contact your EY advisor.

In this issue

What boards should know about the OECD BEPS initiative

5

That time of year again: GST/HST and taxablebenefits

3

Active trading in an RRSP is not evidence of a trading business

7

Publications and articles 10

2 TaxMatters@EY November 2014

The type of control referred to in the hypothetical person testisdejureorlegalcontrol(thiswasconfirmedinthe Tax Court of Canada judgment in Bagtech1). De jure control rests with the owner of shares that carry the voting rights to elect the majority of the directors of a corporation (the test set out in the leading cases of Buckerfield’s and Duha Printers2). In Duha Printers the Supreme Court of Canada recognized that although the starting point for an analysis of who holds de jure control of a corporation is an examination of the corporation’s share register, the terms of the corporation’s constating documents and of any USA must also be considered.

Following Duha Printers and prior to the Bagtech case, the CRA took the position that for purposes of the CCPC definition,ifthehypotheticalpersonownedamajorityof voting shares in the corporation then the terms of any USA were essentially irrelevant. The USA could not prevent the hypothetical person from being deemed to have control of the corporation. The basis for this view was that the hypothetical person, being nothing more thanalegalfiction,wasneitherapartytotheUSAnordeemed to be a party to it.

Bagtech caseIn Bagtech no single nonresident shareholder held a majority of the taxpayer’s shares, but cumulatively, nonresidents held more than 50% of its outstanding voting shares in the relevant taxation years. However, a USA entered into by the taxpayer and its shareholders pursuant to the Canada Business Corporations Act gave Canadian residents the right to elect four members of the seven-person board of directors.

The Federal Court of Appeal in Bagtech upheld the Tax Court of Canada’s decision that a USA that restricted the ability of nonresident shareholders to elect directors preserved a corporation’s CCPC status even though nonresident shareholders collectively held more than 50% of the corporation’s voting shares. In particular, the Court held that the hypothetical person was deemed to have the same rights and to be subject to the same obligations as the nonresident shareholders of the taxpayer corporation; this included being bound by a USA. For more information on the Bagtech case, see the September 2013 edition of TaxMatters@EY.

The Crown did not appeal the judgment of the Federal Court of Appeal to the Supreme Court of Canada and the CRA had not until recently issued any public comments on the outcome of the Bagtech case.

CALU QuestionAt the 2014 Conference for Advanced Life Underwriting (CALU), the CRA was asked whether it accepted that theCCPCdefinitionforincometaxpurposesshouldberead taking into account any restrictions in a USA on the directors’ power and on the ability of the holders of a majority of shares to elect the directors.

The CRA responded that its earlier position, as expressed at the Canadian Tax Conferences in 2009 and 2010, and in Income Tax Technical News 44, could not be reconciled with the Court’s interpretation in Bagtech. The CRA will now apply Bagtech in determining which shareholders have “effective” or “long run” control of a corporation.

ConclusionThe CRA has reversed its position on the interpretation of theCCPCdefinitionandacceptstherelevanceofthetermsof a valid USA in determining a corporation’s CCPC status.

Taxpayers must still exercise caution, however, if they want to rely on a USA to preserve CCPC status where in aggregate the shareholdings of nonresidents and public corporationswouldbesufficienttoconferdejurecontrolof a corporation. For example, the agreement must be a valid USA under the relevant corporate law — a simple shareholders’ agreement would not affect de jure control. Similarly, a valid USA is one that restricts the directors’ powers to carry on the business; whether or not it also contains terms that restrict the majority shareholder’s ability to elect members of the board of directors (and hence affects de jure control) is a separate question.

You should consult a professional to ensure the terms of any USA achieve their intended purpose. u

1 The Queen v PriceWaterhouse Coopers Inc., acting in the capacity of trustee in bankruptcy of Bioartificial Gel Technologies (Bagtech) Inc., (2012 TCC 120 (T.C.C.), aff’d by 2013 FCA 164 (F.C.A.))

2 Buckerfield’s Ltd. et al v. MNR (64 DTC 5301(Ex.Ct.); Duha Printers (Western) Ltd. v The Queen (98 DTC 6334 (S.C.C.))

That time of year again: GST/HST and taxable benefits Michael Zender, Toronto

The requirement to calculate and remit GST/HST on taxablebenefits(otherthanbenefitsthatareexemptorzero-rated) provided to individuals who are employees or shareholders is often overlooked.

Taxablebenefitsprovidedtoanemployeeorshareholderare required to be calculated by the end of February following the year they were incurred (when T4 slips are prepared). The GST/HST in respect of these taxable benefitsisrequiredtoberemittedontheGST/HSTreturnthat includes the month of February.

Taxable benefitsUnder the Income Tax Act,anybenefitreceivedorenjoyed by an employee (or someone related to the employee)byvirtueofhisorherofficeoremploymentmust be included in income, subject to some exceptions.

An employer must determine whether a payment to an employee or shareholder in respect of a property or service that the employer has provided constitutes abenefit.

Themostcommonbenefitsprovidedtoanemployeearethe personal use of an employer-provided automobile and automobile operation costs. Other examples include:

The CRA’s Interpretation Bulletin IT-470R (Consolidated), Employees’ Fringe Benefits, sets out various examples of employment-relatedbenefitsthatareconsideredtobetaxablebenefits.Thisbulletin,aswellastheCRA’sannualGuide T4130, Employers’ Guide: Taxable Benefits and Allowances, should be consulted for information on the CRA’s administrative procedures in this area.

Benefit subject to GST/HSTForGST/HSTpurposes,whereabenefitprovidedtoanemployee is subject to GST/HST, the employer is deemed to have used the property or service in the course of the employer’s commercial activity, thereby allowing the employer to claim an input tax credit to recover any related GST/HST.

Where this is the case, the employer is required to calculateandremitGST/HSTonthebenefit.Thereisnorequirement for the employer to actually collect the GST/HST from the employee, but it is to be included in the employee’s T4 slip. The intent is to put the employee in thesamepositionheorshewouldbeinhadthebenefitbeen acquired outside of the employment.

Asageneralrule,thevalueofthebenefitforGST/HSTpurposesisthetotaloftheamountofthebenefitreportedon the employee’s T4 slip. However, in the case of a company-provided vehicle, any employee reimbursement is ignored for purposes of calculating and remitting the GST/HST. If an employer is reimbursed by the employee for any portionofthevalueoftheautomobilebenefit,theamountof the reimbursement is not included in the employee’s income, but the GST/HST must be calculated on the full valueofthebenefit,priortoanyreimbursements.

It is important to note that there is no requirement to remit GST/HSTonabenefitwheretheemployercannotclaimaninput tax credit. For example, an employer is not entitled to claim an input tax credit on the cost of a golf membership because it is considered to be exclusively for the personal use of an employee. Similarly, no tax applies to exempt or zero-rated supplies, such as low-interest loans (exempt) or benefitsenjoyedoutsideCanada(zero-rated).

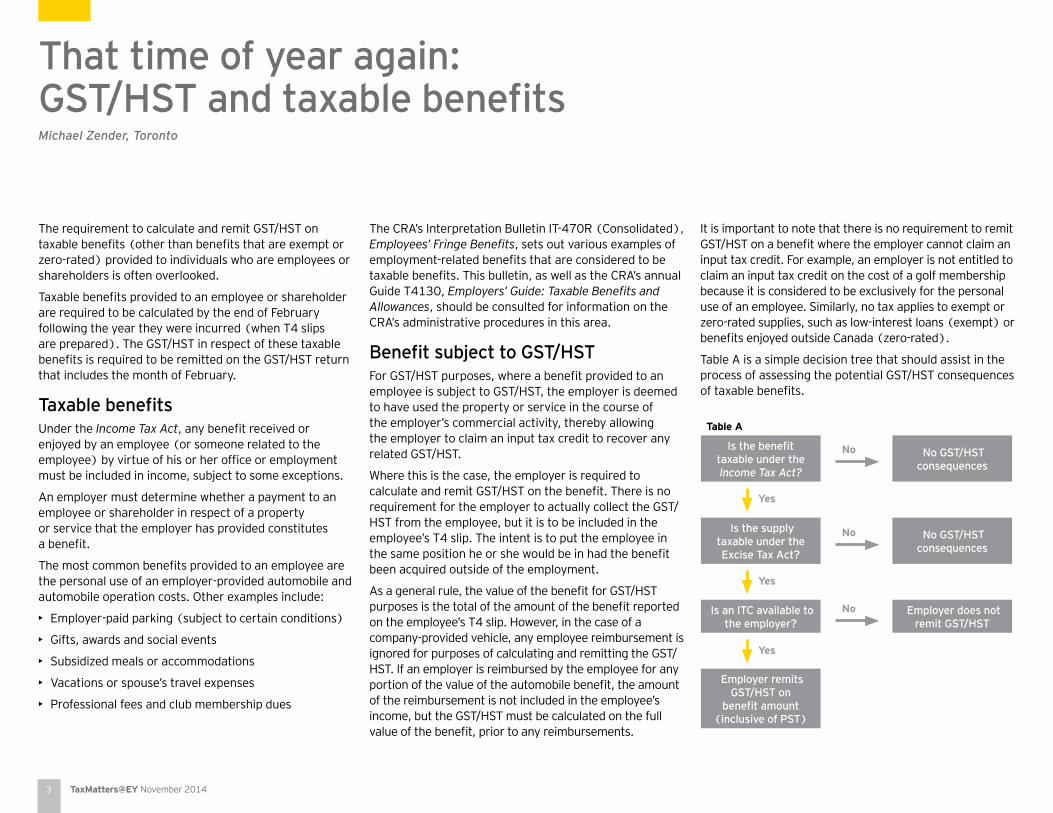

Table A is a simple decision tree that should assist in the process of assessing the potential GST/HST consequences oftaxablebenefits.

Table A

Is the benefit taxable under the Income Tax Act?

No GST/HST consequences

Is the supply taxable under the Excise Tax Act?

No GST/HST consequences

Is an ITC available to the employer?

Employer does not remit GST/HST

Employer remits GST/HST on

benefit amount (inclusive of PST)

No

No

No

Yes

Yes

Yes

4 TaxMatters@EY November 2014

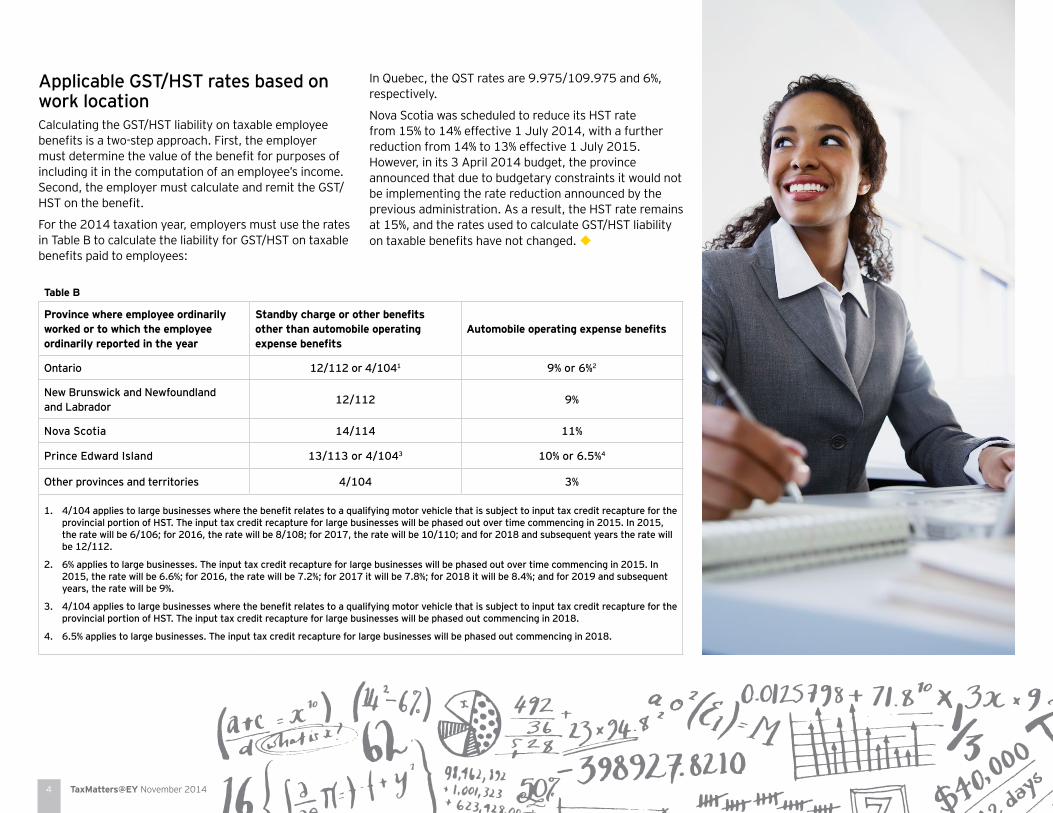

Applicable GST/HST rates based on work locationCalculating the GST/HST liability on taxable employee benefitsisatwo-stepapproach.First,theemployermustdeterminethevalueofthebenefitforpurposesofincluding it in the computation of an employee’s income. Second, the employer must calculate and remit the GST/HSTonthebenefit.

For the 2014 taxation year, employers must use the rates in Table B to calculate the liability for GST/HST on taxable benefitspaidtoemployees:

In Quebec, the QST rates are 9.975/109.975 and 6%, respectively.

Nova Scotia was scheduled to reduce its HST rate from 15% to 14% effective 1 July 2014, with a further reduction from 14% to 13% effective 1 July 2015. However, in its 3 April 2014 budget, the province announced that due to budgetary constraints it would not be implementing the rate reduction announced by the previous administration. As a result, the HST rate remains at 15%, and the rates used to calculate GST/HST liability ontaxablebenefitshavenotchanged.u

Table B

Province where employee ordinarily worked or to which the employee ordinarily reported in the year

Standby charge or other benefits other than automobile operating expense benefits

Automobile operating expense benefits

Ontario 12/112 or 4/1041 9% or 6%2

New Brunswick and Newfoundland and Labrador

12/112 9%

Nova Scotia 14/114 11%

Prince Edward Island 13/113 or 4/1043 10% or 6.5%4

Other provinces and territories 4/104 3%

1. 4/104 applies to large businesses where the benefit relates to a qualifying motor vehicle that is subject to input tax credit recapture for the provincial portion of HST. The input tax credit recapture for large businesses will be phased out over time commencing in 2015. In 2015, the rate will be 6/106; for 2016, the rate will be 8/108; for 2017, the rate will be 10/110; and for 2018 and subsequent years the rate will be 12/112.

2. 6% applies to large businesses. The input tax credit recapture for large businesses will be phased out over time commencing in 2015. In 2015, the rate will be 6.6%; for 2016, the rate will be 7.2%; for 2017 it will be 7.8%; for 2018 it will be 8.4%; and for 2019 and subsequent years, the rate will be 9%.

3. 4/104 applies to large businesses where the benefit relates to a qualifying motor vehicle that is subject to input tax credit recapture for the provincial portion of HST. The input tax credit recapture for large businesses will be phased out commencing in 2018.

4. 6.5% applies to large businesses. The input tax credit recapture for large businesses will be phased out commencing in 2018.

5 TaxMatters@EY November 2014

What boards should know about the OECD BEPS initiative Extract from Board Matters Quarterly September 2014

“Base erosion and profit shifting (BEPS) relates to a loss of substantial corporate tax revenue because of planning aimed at eroding the taxable base and/or shifting profits to locations where they are subject to a more favourable tax treatment.”

OECD report, Addressing Base Erosion and Profit Shifting, released February 2013

The tax landscape is clearly changing. As governments search for additional revenue streams, the focus on transparency is increasing and tax policies are beingmodified.

Boards and audit committees need to be well informed about tax policy developments and trends worldwide — in the markets they currently serve and those they may be considering.

A key project to monitor is an effort by the heads of state of the G20 countries. This initiative is driven largely by concern about the potential for multinational corporations (MNCs) to shift income to low- or no-tax jurisdictions.

The Organisation for Economic Cooperation and Development’s (OECD) BEPS project is meant to better coordinate how countries address tax strategies perceived as eroding countries’ tax bases. The project is intended to spur governments to change their tax laws and treaties in order to reduce opportunities to shift profitstolower-taxedjurisdictions.

Based on a 15-point action plan issued in July 2013, the BEPS initiative focuses on several areas, including:

The OECD plans to issue a series of reports, analyses and recommendations between September 2014 and the end of 2015.

Why are the OECD’s recommendations important?While not a governmental organization, the OECD is influentialinsettingglobaltaxpolicy.Moreover,theBEPSproject involves all of the G20 countries, including China and India, which are not OECD members.

Effects of the ongoing BEPS effort are already evident as individual countries have started implementing anti-BEPS policies through both legislation and enforcementactivity,withoutwaitingfortheOECD’sfinalrecommendations.

For example, new tax laws in Canada have included severalBEPS-relatedchangesthatreflectthegovernment’s ongoing commitment “to address international aggressive tax avoidance by multinational enterprises.” These legislative changes include: thin-capitalization and upstream loan restrictions on the deductionoffinancingcosts,syntheticdispositionprovisions and character conversion transactions.

Individual country responses to the OECD recommendations will vary, as will the timing of any legislative actions.

For this reason, companies and their boards need to carefully track BEPS-related developments, both at the OECD level and within the countries where the company has current or future operations, investment or activity.

EY 33rd annual international tax conference BEPS survey

Bob Neale, Toronto

Attendees at the 9 October 2014 event held in New York City were surveyed on various aspects of the Organisation for Economic Cooperation and Development’s (OECD’s) base erosion and profitshifting(BEPS)project.Amongthesurvey’sinterestingfindings:

• 79% of respondents said that BEPS will generate significantinternationaltaxchangesinthe coming years. Most companies consider themselves unprepared.

• 30% see tax authorities raising BEPS-related issues in audits, and 65% judge the posture and tactics of foreign tax authorities as more aggressive than in the past.

• 53% report they have not yet begun analyzing what country-by-country reporting will mean for their company.

• 67% said they are more likely to consider an advance pricing arrangement (APA) to help manage risk and obtain certainty, a 12% increase from 2013.

• 60% ranked transfer pricing as the number-one BEPS focus area being raised as an audit issue.

6 TaxMatters@EY November 2014

By doing so, they can understand the trends and anticipate changes.

What is the expected outcome?Ultimately, the OECD’s recommendations are expected to play a role in reshaping country tax laws. The likely long-term result for MNCs will be more aggressive tax enforcement, heightened tax scrutiny, greater transparency requirements, increased compliance costs and, potentially, more taxes paid.

On 16 September, the OECD released a series of deliverables, including:

• Atemplateforcountry-by-countryreporting

• Guidelinesontransferpricingforintangibles

• Recommendationsonhybridmismatcharrangements(i.e., certain instruments or entities that are treated differently under the tax laws of two countries)

To learn more about the reports, read our BEPS Tax Alerts.

In most of these areas, the OECD will work on implementation and other details into 2015. The OECD will also begin work on the action items with 2015 target dates, including treatment of interest expense, allocation of risk and capital, and controlled foreign corporation rules.

How should boards prepare?AsignificantnumberofOECDrecommendationsarenow in place, and countries are now assessing how to develop their local implementation. The timing is right for companies to review their business models and structures

against each recommendation to identify possible pressure points.

Current reporting and compliance processes should be reviewed in light of the likelihood of expanded requirements in the future. Careful assessment includes preparing for the possibility of country-by-country reportingoffinancialandoperatingprofilesforeachcountry in which an MNC operates. Proactively managing global tax controversy is also important.

Other steps companies can take to respond to BEPS-related developments include:

• Consideradvancepricingagreements(APAs)and other early engagement with tax authorities to gain greater certainty

• Considerproactivelycommunicatinginformationregarding your company’s total tax and economic contribution with key stakeholders, including regulators and shareholders

• ConsiderengagingwiththeOECDandcountrypolicymakers on these international tax issues

Given the many moving pieces of the BEPS initiative, relevant information that emerges from discussions with policymakers should be shared frequently with a company’s management, board and other relevant stakeholders. u

Questions for the board and audit committee to consider:

• Has management conducted a strategic review of the implications of potential cross-border tax changes for the company’s business models and structures?

• Has management shared this evaluation with the board?

• Has the board evaluated how the company can position itself for the evolving global tax landscape?

• Is the company ready for heightened scrutiny and tax audit risk, which can place increased pressure on cash tax and effective tax rate positions?

• Is the company prepared for the potentially substantial increase in global reporting requirements and the commensurate increase in compliance costs?

Active trading in an RRSP is not evidence of a trading business Prochuk v The Queen, 2014 TCC 17 (T.C.C.) Dalia Hamdy, Toronto and Allison Blackler, Vancouver

In this decision, the Tax Court of Canada considered whether a person actively trading investments inside his registered retirement savings plan (RRSP) can be considered to be carrying on a trading business outside of his RRSP. The Court concluded that trading inside an RRSP cannot itself be a business, nor can it provide evidence of a trading business carried on outside of an RRSP.

FactsThetaxpayerworkedinthefinancialindustryforapproximately 13 years, until he decided to leave the business and take care of his own investments. From that time onwards, he made his livelihood from gains made within his RRSP and in fact increased the balance in his RRSP by a factor of eight. The taxpayer reported his RRSP withdrawals as income, but did not report any amounts as income from business or property.

In 2005, using funds withdrawn from his RRSP, he invested $250,000 in an offshore foreign exchange currency fund, which promised a return of 17.52% a year. Under the subscription terms, the taxpayer’s investment would be locked in for more than two years and would yield guaranteed payments twice a year. While he did receive some initial return on his investment, the fund turned out to be fraudulent and he lost $186,250 of his original investment.

The taxpayer claimed a business loss in respect of this amount on his 2007 income tax return on the basis that he was either in the business of trading or that his investment in the fraudulent fund was an “adventure or concern in the nature of trade.” The Minister of National

Revenue reassessed the taxpayer on the basis that the loss was a capital loss. The taxpayer appealed to the Tax Court of Canada, but his appeal was dismissed.

The Tax Court of Canada decisionIn determining whether the taxpayer’s investment in the fund was on account of income or capital, the Court reasoned that although property that yields income is, generally speaking, a capital asset, such property can also be inventory of a business, depending on the circumstances. Accordingly, the Court evaluated the taxpayer’s particular circumstances to determine whether he was in the business of trading and if not whether his investment in the fund could constitute an “adventure or concern in the nature of trade.”

The taxpayer was not a trader

In determining whether the taxpayer was in the business of trading investments, the Court considered the business activityfactorsidentifiedinThe Queen v Vancouver Art Metal Works Ltd. ([1993] 2 FC 179 (F.C.A.)):

The Court determined that the taxpayer had only made one investment outside his RRSP since 2000, namely his investment in the fund. The taxpayer held the investment

in the fund for an extended period, as it was locked in for a period of 28 months and could not be sold before that date. The taxpayer intended to hold the investment for thelongtermtoearnincomefromitandtomakeaprofit.In the Court’s view, the taxpayer was merely a passive participant with respect to the investment in the fund and did little or nothing to receive a return on his investment.

8 TaxMatters@EY November 2014

Thetaxpayerhadsuggestedthathissignificantgainsin his RRSP demonstrated that he was an active trader carrying on a trading business. However, citing Deep v The Queen (2006 TCC 315 (T.C.C.)) as authority, the Court declined to draw any conclusions from the taxpayer’s RRSP-related trading. In the Court’s view, the RRSP regime is unique and intentionally provides special tax treatment under the Income Tax Act (the Act), with restrictions on the types of investments that may be acquired,taxbenefitsthatflowfromtheirownershipandtaxconsequencesthatflowfromtheirdisposal.

The Court concluded that because of this unique tax regime, trading activity within an RRSP cannot constitute a business of the taxpayer. Further, and more important in this case, because the Act treats an individual who trades within his RRSP differently from an individual who is in the business of trading, any trading within an RRSP is not relevant to a determination of whether an individual is in the business of trading outside of an RRSP.

On this basis, the Court concluded that the taxpayer was not a trader.

The taxpayer was not engaged in an “adventure or concern in the nature of trade”

The Court then turned to the question of whether the taxpayer’s activities could be considered “an adventure or concern in the nature of trade.” The Court outlined the relevant criteria set out in Canada Safeway Ltd. v The Queen (2008 FCA 24 (F.C.A.)) for determining if a person is engaged in an “adventure or concern in the nature of trade”:

• Whetherthetaxpayerdealtwiththepropertyinthesameway as a dealer would ordinarily deal with such property

• Whetherthenatureandquantityofthepropertydictated whether it could be disposed of as capital or as a trading asset

• Whetherevidenceofthetaxpayer’sintentionwasconsistent with a trading motivation

The Court concluded that the taxpayer’s investment did not meet any of the criteria and therefore he was not engaged in an “adventure or concern in the nature of trade.” In the Court’s view, the taxpayer was a passive investor intending to hold the property on a long-term basis and to passively receive a return on his investment. He was not an active businessman intending to promptly reselltheinvestmentforaprofit.Asaresult,thetaxpayerwas not entitled to claim a non-capital loss in his 2007 taxation year, and his appeal was dismissed.

Lessons learnedThe Court’s comments that trading activity within an RRSP cannot constitute a business were incidental to the main decision, and therefore are not considered binding. However, they acknowledge that taxpayers can and do actively trade investments in their RRSPs (and arguably, in other tax-sheltered investment vehicles).

9 TaxMatters@EY November 2014

You’re invited

Private Company Webcast SeriesPros and cons of an IPO: staying private and profitable

Now more than ever, many Canadian private companies are considering alternatives to

an initial public offering.

We invite you to join us for a candid discussion examining the factors company owners

should consider when deciding between the various alternatives and what might be the

best option for your business.

Hosted by EY IPO Leader Bill Demers, Partner Gabriel Baron and Associate Partner

Jonathan Breido, this webcast will cover a range of topics, including:

• What’sinvolvedinpreparingforanIPOjourney?

• ProsandconsofanIPO

• Otheroptionsavailabletoprivatecompanyowners

• Taxconsiderationsforstayingprivate

Thursday, 20 November 2014

Noon-1 p.m. (EST)

Registration

Register online for this event by 19 November.

A webcast link will be emailed to you closer to the event date.

On 10 October 2014, the Department of Finance tabled a notice of ways and means motion (NWMM) that includes the draft legislative proposals that were released on 29 August 2014 relating to the 2014 federal budget, as well as a number of technical changes to the Income Tax Act and the Income Tax Regulations.

Finance amends TLRE rules for commercial

investment fund industry — 2014 Issue No. 54

On 20 October 2014, the Department of Finance tabled a notice of ways and means motion that includes relief from the application of the trust loss restriction event (TLRE) rules for certain trusts in the commercial investment funds industry.

BC tables LNG income tax legislation —

2014 Issue No. 55

On 21 October 2014, the BC government tabled draft proposalsforthenewliquefiednaturalgas(LNG)income tax legislation, as well as for a related natural gas corporate income tax credit. The proposals include a number of substantial changes to the LNG tax regime described in the 2014 provincial budget.

Insurance swaps and offshore banking arrangements:

Bill C-43 (2014) — 2014 Issue No. 56

On 23 October 2014, the federal government tabled Bill C-43, which includes certain tax measures announced in the 2014 federal budget and earlier with respect to insurance swaps and offshore banking arrangements.

Publications and articles

Entrepreneurs reinvented

In this update to Exceptional magazine, we learn about the importance of transformation and reinvention on the journey to entrepreneurial success.

International Estate and Inheritance Tax Guide 2014?

This guide summarizes the estate tax planning systems and also describes wealth transfer planning considerations in 38 jurisdictions around the world, including Canada, the US, the UK, Australia, France, Germany, Italy, China and the Netherlands.

Worldwide Transfer Pricing Reference Guide 2014

This publication outlines basic transfer pricing information for more than 100 countries and territories in which EY offers Transfer Pricing services. It includes not only transfer pricing tax laws, regulations and rulings, but also OECD guidelines, priorities and pricing methods.

Websites

Business immigration alerts and updates

For the latest information on Canadian and US business immigration issues from Egan LLP, a business immigration lawfirmalliedwithEYinCanada,visitEganLLP.com.

EY’s Family Business Blog

Get the latest thinking on the most pressing issues faced by family businesses by following the EY Family Business Blog. New topics will be explored on a weekly basis. Read about succession planning, growth, wealth management, governance, entrepreneurship and more. Visitfamilybusinessblog.ey.com.

Focus on private business

Because we believe in the power of private mid-market companies, we invest in people, knowledge and services to help you address the unique challenges and opportunities you face in the private mid-market space.

Online tax calculators and rates

Frequentlyreferredtobyfinancialplanningcolumnists,thispopular feature on ey.com lets you compare the combined federal and provincial 2013 and 2014 personal tax bills in each province and territory. The site also includes an RRSP savings calculator and personal tax rates and credits for all income levels. Our corporate tax-planning tools include federal and provincial tax rates for small-business rate income, manufacturing and processing rate income, general rate income and investment income.

Tax counsel and litigation

For news and thought leadership from Couzin Taylor LLP, a tax law boutique allied with EY in Canada, visit CouzinTaylor.com.

Learn moreTo subscribe to TaxMatters@EY and other email alerts, visit ey.com/ca/EmailAlerts.

For more information on EY’s tax services, visit us at ey.com/ca/Tax.

For questions or comments about this newsletter, email [email protected].

And follow us on Twitter @EYCanada.

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights andqualityserviceswedeliverhelpbuildtrustandconfidenceinthecapitalmarketsandin economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization and may refer to one or more of the member firmsofErnst&YoungGlobalLimited,eachofwhichisaseparatelegalentity.Ernst&YoungGlobalLimited,aUKcompanylimitedbyguarantee,doesnotprovideservices to clients. For more information about our organization, please visit ey.com.

About EY Tax ServicesOur tax professionals across Canada provide you with deep technical knowledge, both global and local, combined with practical, commercial and industry experience. We offer a range of tax-saving services backed by in-depth industry knowledge. Our talented people, consistent methodologies and unwavering commitment to quality service helwp you build the strong compliance and reporting foundations and sustainable tax strategies that help your business achieve its potential. It’s how we make a difference.

For more information, please visit ey.com/ca.

About Couzin TaylorCouzinTaylorLLPisanationalfirmofCanadiantaxlawyers,alliedwithErnst&YoungLLP,specializingintaxlitigationandtaxcounselservices.

This publication contains information in summary form, current as of the date of publication, and is intended for general guidance only. It should not be regarded as comprehensive or a substitute for professional advice. Before taking any particular course of action, contact Ernst & Young or another professional advisor to discuss these matters in the context of your particular circumstances. We accept no responsibility for any loss or damage occasioned by your reliance on information contained in this publication.

ey.com/ca

CPA Canada Store

Couzin Taylor’s Guide to Canadian Income Tax Administration,

2nd Edition

David Douglas Robertson, Daniel Sandler, Brian Studniberg, Louis Tassé, Roger Taylor

Provides an accessible and comprehensive discussion of the law and administrative practice related to the administration of Canada’s federal Income Tax Act.

EY’s Complete Guide to GST/HST, 2014 (22nd) Edition

Dalton Albrecht, Jean-Hugues Chabot, Sania Ilahi, David Douglas Robertson

Canada’s leading guide on GST/HST, including GST/HST commentary and legislation, as well as a GST-QST comparison. Written by a team of EY indirect tax professionals, the guide is consolidatedto15July2014andupdatedtoreflectthelatestchanges to legislation and CRA policy.

EY’s Guide to Tax Research and Writing, 7th edition

Editors: Maureen De Lisser, Bob Neale, Yves Plante

Learn the tax research process, how laws are enacted, and howtocommunicateyourfindingstoyourclients.Writtenforaccountants, lawyers and other professionals in public practice, industry, education and government with a basic familiarity with the concepts and principles of Canadian income tax.