28

Comparing Australia and New Zealand Broadband Policies 20 April 2015 CommsDay Summit 2015 Westin Hotel, Sydney 12225542 Dr Ross Patterson Partner, Competitors & Economic Regulation

| Date post: | 15-Jul-2015 |

| Category: |

Technology |

| Upload: | grahame-lynch |

| View: | 76 times |

| Download: | 0 times |

Comparing Australia and New Zealand Broadband

Policies

20 April 2015

CommsDay Summit 2015Westin Hotel, Sydney

12225542

Dr Ross PattersonPartner, Competitors & Economic

Regulation

Page l 2

Comparing Australia and New Zealand Broadband Policies

1. Process

2. Regulatory Framework

3. Progress Against Plan

4. Penetration and Uptake

5. Services and Prices

6. Conclusions

Page l 3

New Zealand

Process

2007 2008 2009 2010

Telecom Op Sep Undertakings – 80% of lines

capable of delivering 10 Mbps by 2011 with enforceable roll out obligations (FTTN)

PPP tender $4.7 billion (FTTN model) Expert Panel

concluded no bid was viable – recommended

FTTP model

PPP tender terminated. Announcement of $41.3

billion publicly owned network (93% FTTP,7%

(wireless and satellite) by 2020)

NBNCo established

Australia

Page l 4

ProcessOECD Fixed Broadband Penetration Rankings

15

16

17

18

19

20

21

22

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

New Zealand

Australia

Source: OECD Broadband Portal

OECD median

th

th

nd

st

th

th

th

th

(out of 34)

Page l 5

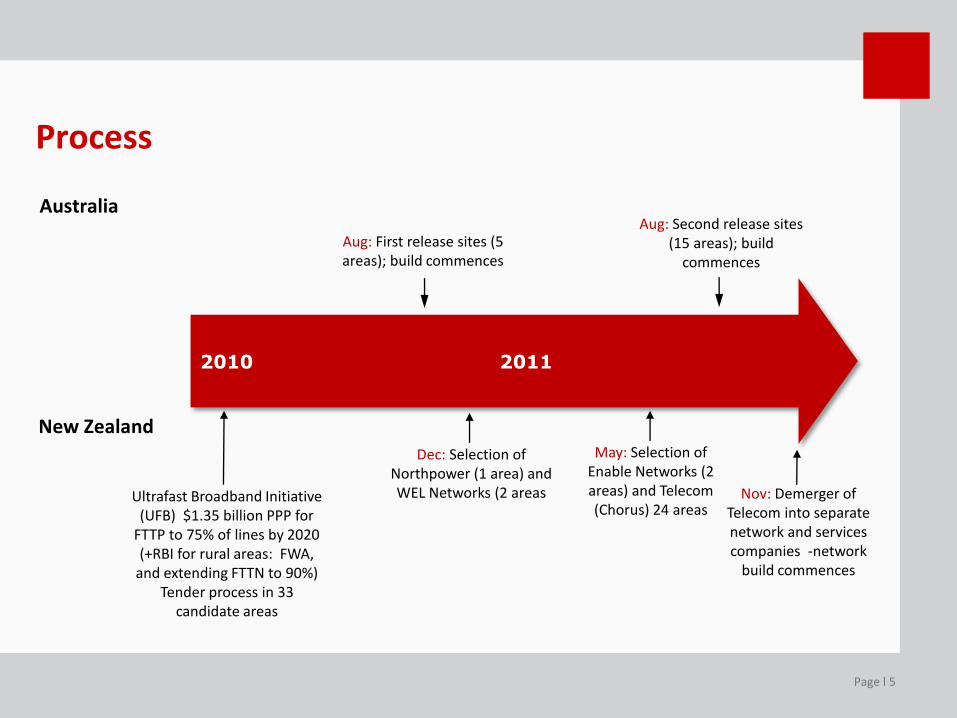

New Zealand

Process

2010 2011

Ultrafast Broadband Initiative (UFB) $1.35 billion PPP for

FTTP to 75% of lines by 2020 (+RBI for rural areas: FWA,

and extending FTTN to 90%) Tender process in 33

candidate areas

Aug: First release sites (5 areas); build commences

Aug: Second release sites (15 areas); build

commences

Australia

Dec: Selection of Northpower (1 area) and WEL Networks (2 areas

May: Selection of Enable Networks (2 areas) and Telecom (Chorus) 24 areas

Nov: Demerger of Telecom into separate network and services companies -network

build commences

Page l 6

Australia

Process

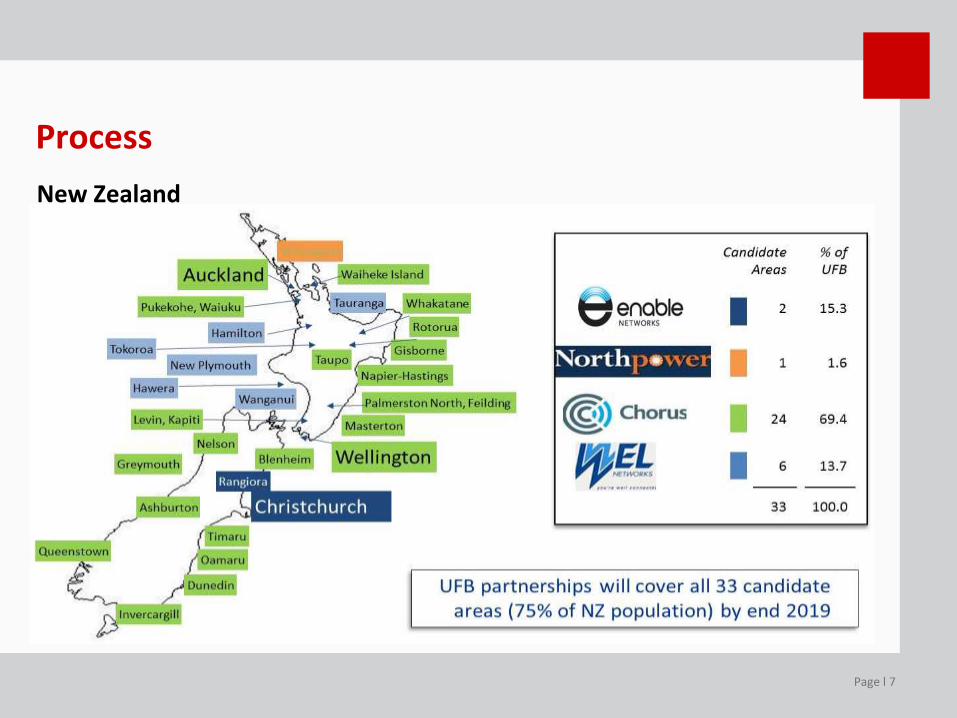

Page l 7

New Zealand

Process

Page l 8

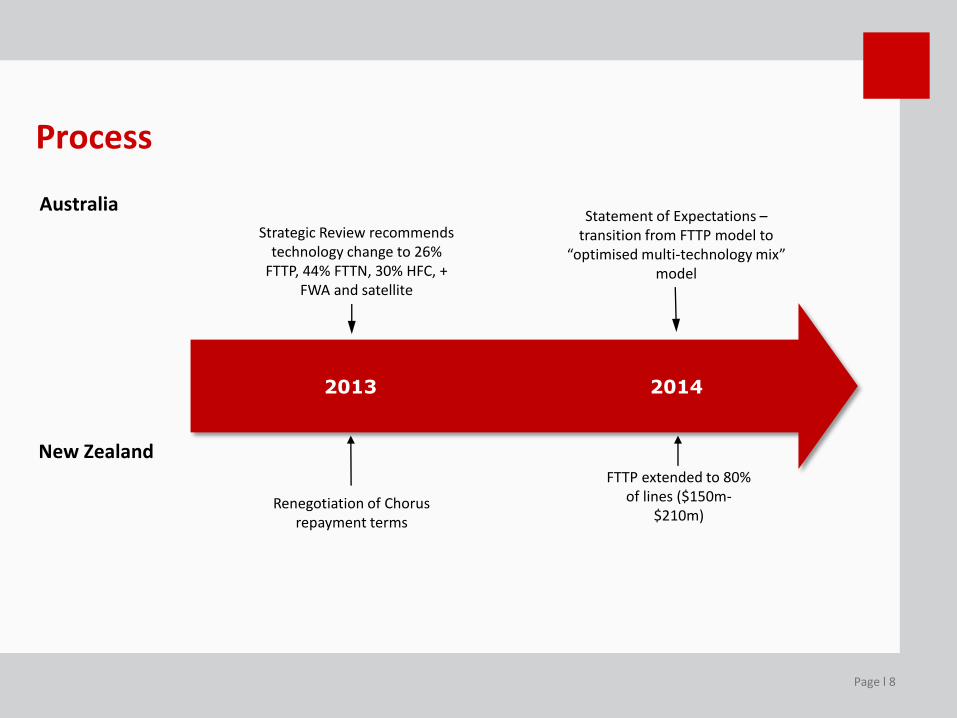

New Zealand

Process

2013 2014

Renegotiation of Chorus repayment terms

Australia

FTTP extended to 80% of lines ($150m-

$210m)

Strategic Review recommends technology change to 26%

FTTP, 44% FTTN, 30% HFC, + FWA and satellite

Statement of Expectations –transition from FTTP model to

“optimised multi-technology mix” model

Page l 9

Australia New Zealand

Regulatory Framework – ownership and services

State owned and operated network –able to be privatised after 2020 [subject to Productivity Commission review]

PPP for the 3 LFCs (A and B shares); Chorus funding arrangement (equity and debt securities)

Wholesale layer 2 provider only –unbundling possible after 2020

Wholesale layer 2 provider only –required to supply unbundled layer 1 services from 2020 (EOI-capable)

Non-discrimination and transparency obligations

Non-discrimination and transparency obligations

No participation in retail services No participation in retail services

Page l 10

Australia New Zealand

Regulatory Framework – prices and roll out

Prices and service offerings set out in Special Access Undertaking (SAU) subject to acceptance by the ACCC following public consultation

Prices and services set by contract with CFH through tender process

Roll out obligations set by NBN Co in three year plan approved by shareholding Ministers

Roll out obligations set by contract with CFH through tender process

Page l 11

Australia New Zealand

Regulatory Framework – structural separation

Progressive structural separation of Telstra as customers migrate to fibre

Structural separation of Telecom a pre-condition to its participation in UFB

Existing copper services subject to “robust, effective and appropriate equivalence” but less than functional separation

De-merger of Telecom into separate listed network and retail companies in November 2011

Structural separation applies to copper as well as fibre services

Page l 12

Regulatory Framework

Source: Telecom NZ

Page l 13

Regulatory Framework – migration

Mandated migration (18 months from date of service availability)

Australia

Migration left to market forces

New Zealand

Page l 14

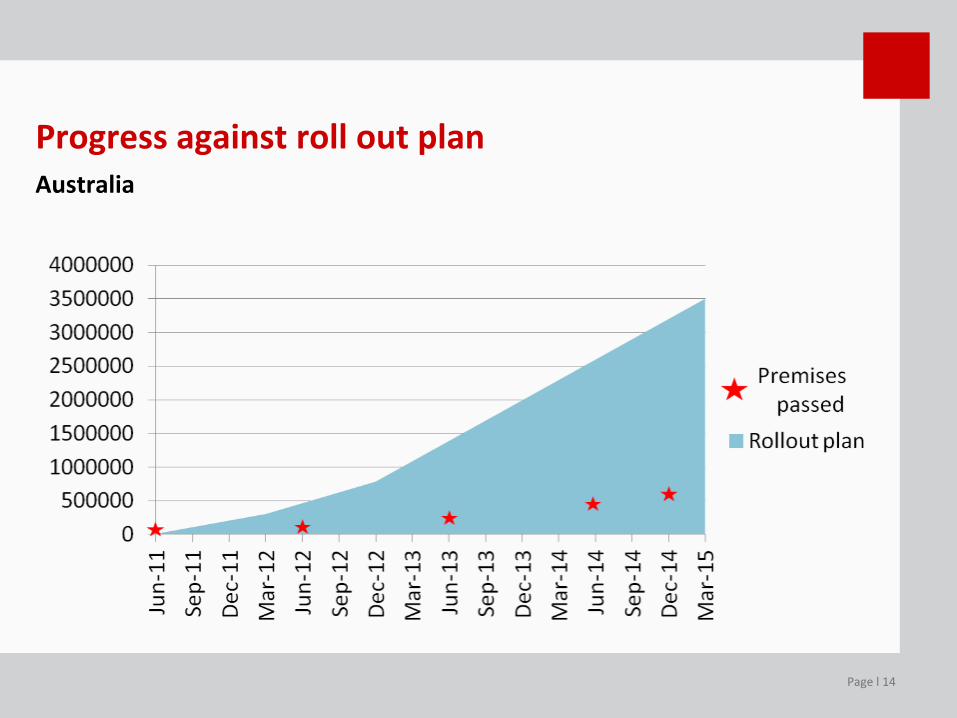

Progress against roll out planAustralia

Page l 15

New Zealand

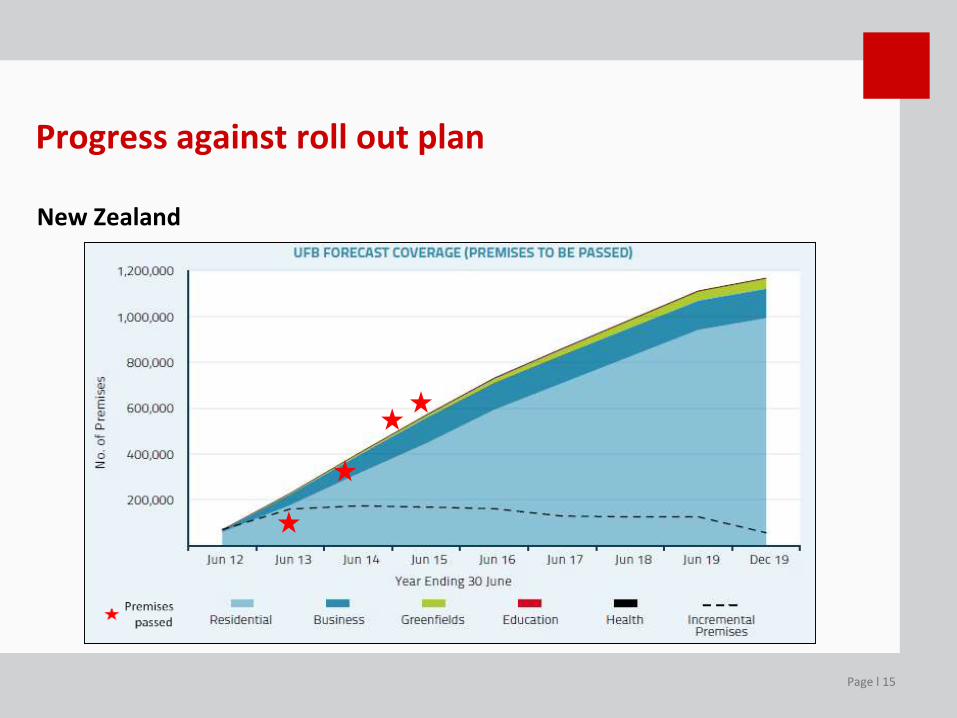

Progress against roll out plan

Page l 16

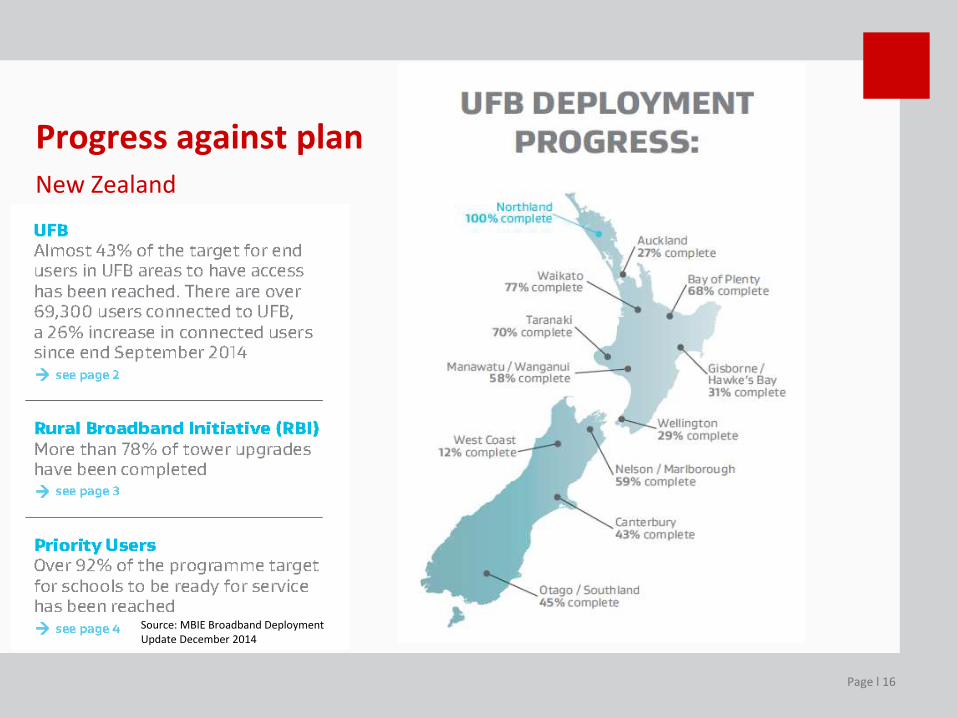

New Zealand

Source: MBIE Broadband Deployment Update December 2014

Progress against plan

Page l 17

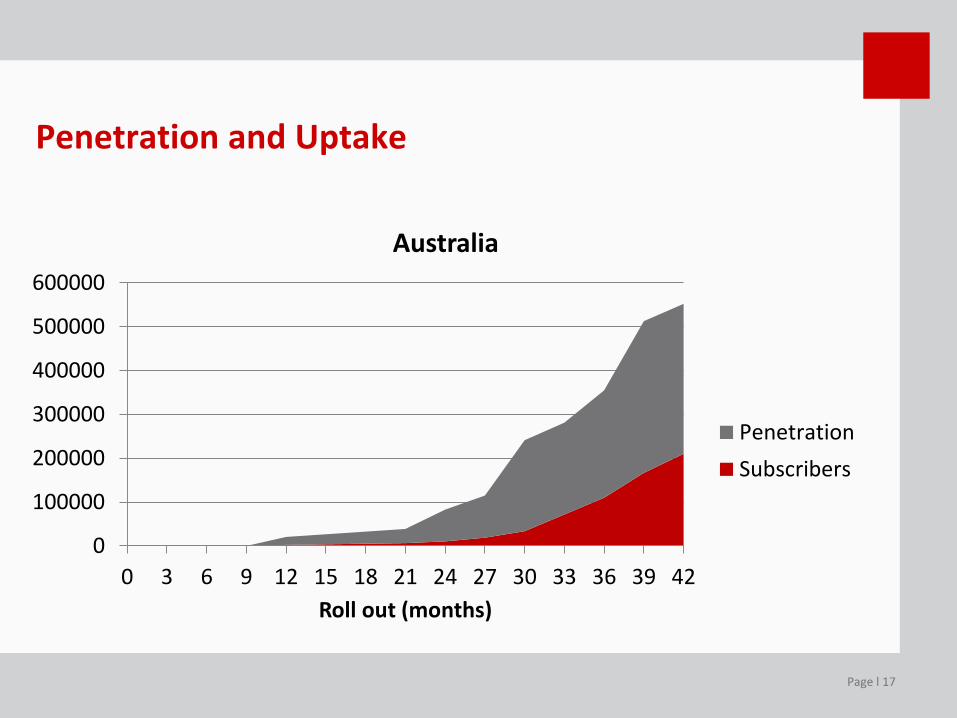

Penetration and Uptake

0

100000

200000

300000

400000

500000

600000

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42

Roll out (months)

Australia

Penetration

Subscribers

Page l 18

Penetration and Uptake

0

100000

200000

300000

400000

500000

600000

0 3 6 9 12 15 18 21 24 27 30 33 36

Roll out (months)

New Zealand

Penetration

Subscribers

Page l 19

Australia New Zealand

Services and PricesWholesale

25/10 $30.00 30/10 $37.50*

50/20 $34.00 50/20 $37.50**

100/40 $38.00 100/20100/50

200/20

$40.00**$55.00* ($45.00**)

$55.00**

All NBNCo pricing *CFH negotiated pricing**Chorus commercial pricing

Page l 20

Australia New Zealand

Services and PricesRetail

25/5 $90 - $113 30/10 $85 - $89

100/40 $133 100/50 $109 - $119

200/20 $119 - $139

All unlimited data plans All unlimited data plans

Page l 21

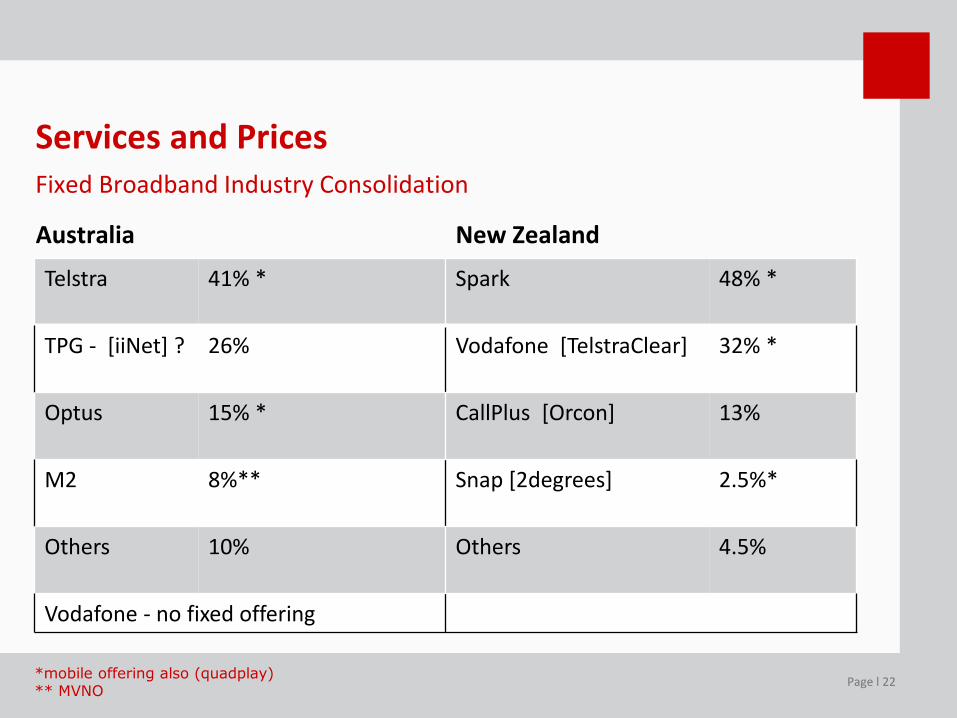

Australia New Zealand

Services and PricesNew services

Page l 22

Australia New Zealand

Services and PricesFixed Broadband Industry Consolidation

*mobile offering also (quadplay)** MVNO

Telstra 41% * Spark 48% *

TPG - [iiNet] ? 26% Vodafone [TelstraClear] 32% *

Optus 15% * CallPlus [Orcon] 13%

M2 8%** Snap [2degrees] 2.5%*

Others 10% Others 4.5%

Vodafone - no fixed offering

Page l 23

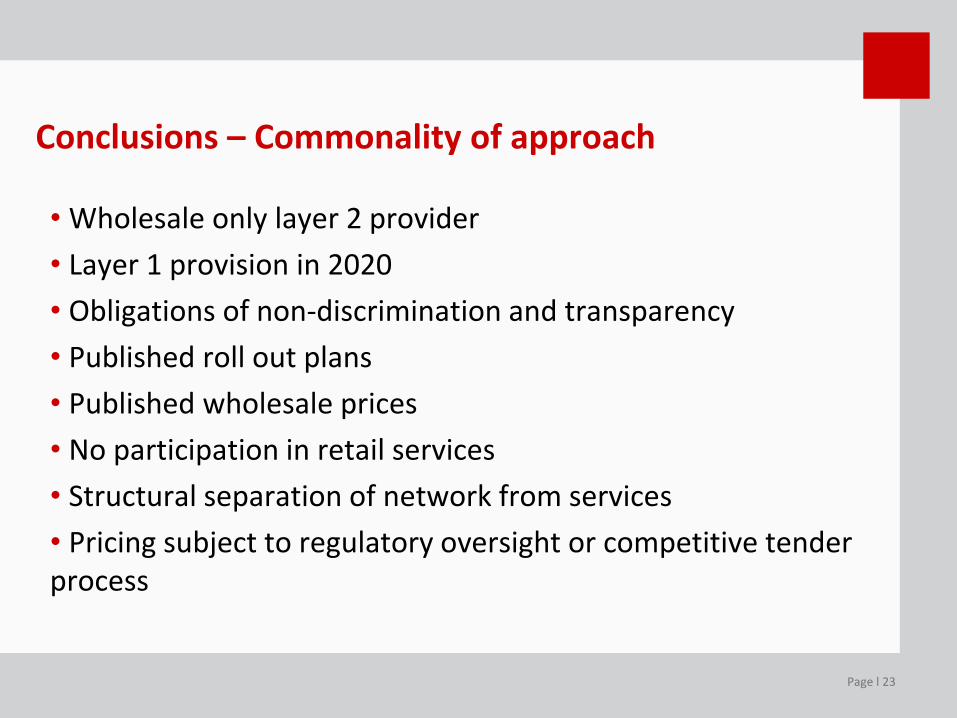

Conclusions – Commonality of approach

• Wholesale only layer 2 provider

• Layer 1 provision in 2020

• Obligations of non-discrimination and transparency

• Published roll out plans

• Published wholesale prices

• No participation in retail services

• Structural separation of network from services

• Pricing subject to regulatory oversight or competitive tender process

Page l 24

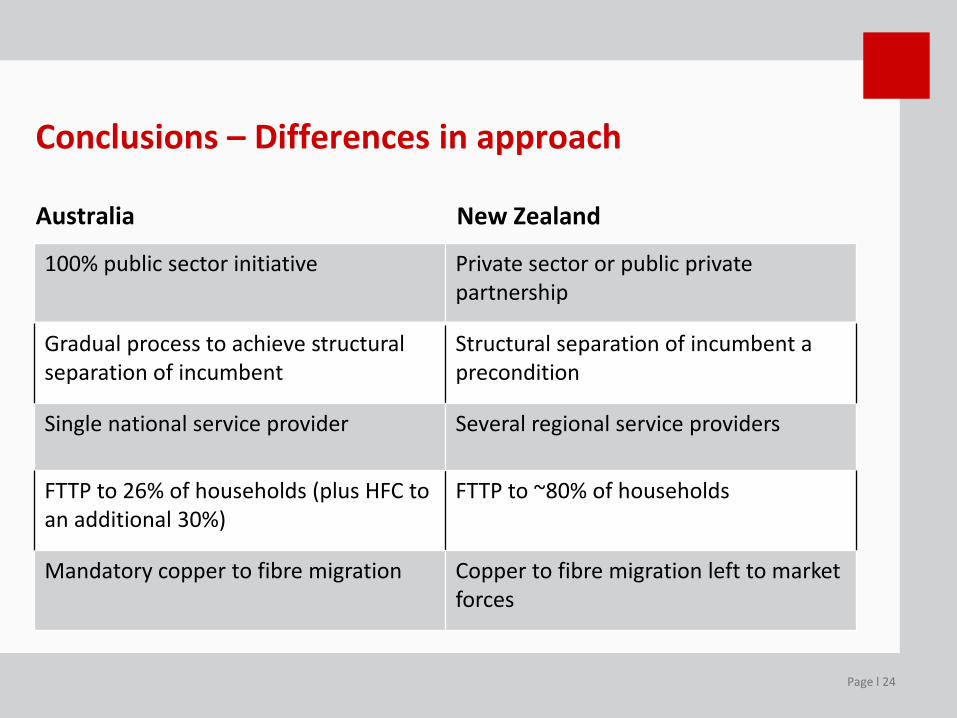

Australia New Zealand

Conclusions – Differences in approach

100% public sector initiative Private sector or public private partnership

Gradual process to achieve structural separation of incumbent

Structural separation of incumbent a precondition

Single national service provider Several regional service providers

FTTP to 26% of households (plus HFC to an additional 30%)

FTTP to ~80% of households

Mandatory copper to fibre migration Copper to fibre migration left to market forces

Page l 25

Conclusions – Consequences of difference in approach

• Under public ownership roll out and cost overrun risk is borne by the taxpayer and becomes a political issue.

• Under private ownership roll out and cost overrun risk is borne by the private sector participant and is a commercial issue.

• Commercial decision makers are more likely to still be involved at the end of the project than political decision makers, and therefore have greater accountability for decisions they have made.

• Commercial operators are bound by contract and do not have the option to unilaterally change the deal if they have miscalculated.

Page l 26

Conclusions – the jury is still out

• Benefits of broadband said to deliver increase in per capita GDP – but are there measurable benefits of a 100 Mbps (fibre) consumer service compared with a 20Mbps (VDSL) service?

• Is 80% FTTP coverage measurably of greater benefit than 26% FTTP, 30% HFC and the balance FTTN?

• Does mandatory copper to fibre migration stifle inter-modal retail competition? If so, do the benefits of faster (or greater) migration outweigh the detriments of higher retail prices?

The Australian and New Zealand fibre roll outs provide a rare “natural experiment” which should over the next few years provide answers to these questions.

Page l 27

Conclusions – the good news

-50

0

50

100

150

200

250

300 Annual Growth of fibre connections among countries reporting %

Source: OECD Broadband Portal, 2015

Dr Ross Patterson PartnerCompetition & Economic Regulationt +64 9 353 9864f +64 9 353 9701m +64 21 225 [email protected]