41

Sr. Risk Management Consultant Sageworks Vice President Sageworks

| Date post: | 23-Jan-2018 |

| Category: |

Economy & Finance |

| Upload: | libby-bierman |

| View: | 419 times |

| Download: | 2 times |

Sr. Risk Management Consultant

Sageworks

Vice President

Sageworks

• Ask questions throughout the session using the GoToWebinar control panel

• The slides and the recording will be sent out to attendees after today’s session

2

• Financial information company that provides credit and risk management software solutions to thousands of financial institutions

• Trusted by more financial institutions for the ALLL than any other solution

• Awards

» Named to Inc. 500 list of fastest growing privately held companies in the U.S.

» Named to Deloitte’s Technology Fast 500

» NC Tech Awards: Excellence in Customer Service

3

Sr. Risk Management Consultant Sageworks

4

ED BAYERAARON LENHART

Vice PresidentSageworks

5

• Background on current expected credit losses (CECL), timeline and current status

• How to measure expected credit losses (ECLs)

• Overview of methodologies, including challenges, benefits and examples

» Migration Analysis

» Probability of default / loss given default (PD / LGD)

» Vintage Analysis

• How to choose the right method

• Q&A

6

• FASB released proposal December 2012

• Current expected credit losses (CECL)

• What’s changed from Incurred Loss Model?

» Forward-looking requirements

» “Probable loss” threshold removed

• “No triggers, no thresholds” (“Fed Perspectives,” 2015)

» Need for accessible, loan-level data

» Longer loss horizon

» Makes ALLL more credit union-wide calculation

• Purpose: Quicker recognition of losses. Changes in ALLL reserve balances will reflect changes in credit quality and flow through earnings (“Fed Perspectives,” 2015)

7

8

December 20, 2012FASB Proposes CECL Model

May 31, 2013Comment period ends

July 24, 2014IASB’s IFRS 9 Financial Instruments

February 2015Basel ECL guidance released

Q1 2016Expected release of FASB’s CECL model

9

Q1 2016Expected release of FASB’s CECL model

December 15, 2019Effective for smaller entities (non-SEC filers) and all other entities

December 15, 2018Effective for public businesses that meet definition of SEC filer

December 2020Private business organizations implement CECL for interim financial statements

• Effective dates set during November 11th FASB board meeting (“Tentative Board Decisions,” 2015)

• Staff members said that the wide variation in the size of public financial institutions warranted distinguishing between small and large institutions when it comes to the effective dates, and board members agreed. (“FASB sets CECL effective dates,” 2015)

• The FASB is confident that the new standard will be voted on and released in Q1 of 2016, according to their spokeswoman

• In October, the Federal Reserve hosted the first webinar in a series of webinars on the CECL model

• On November 11th, FASB members agreed to amend the proposed standard so that TDRs would be measured under the CECL model with no cost-basis adjustments

• Discussions on other outstanding issues are expected to continue at the board’s Nov. 23 meeting

10

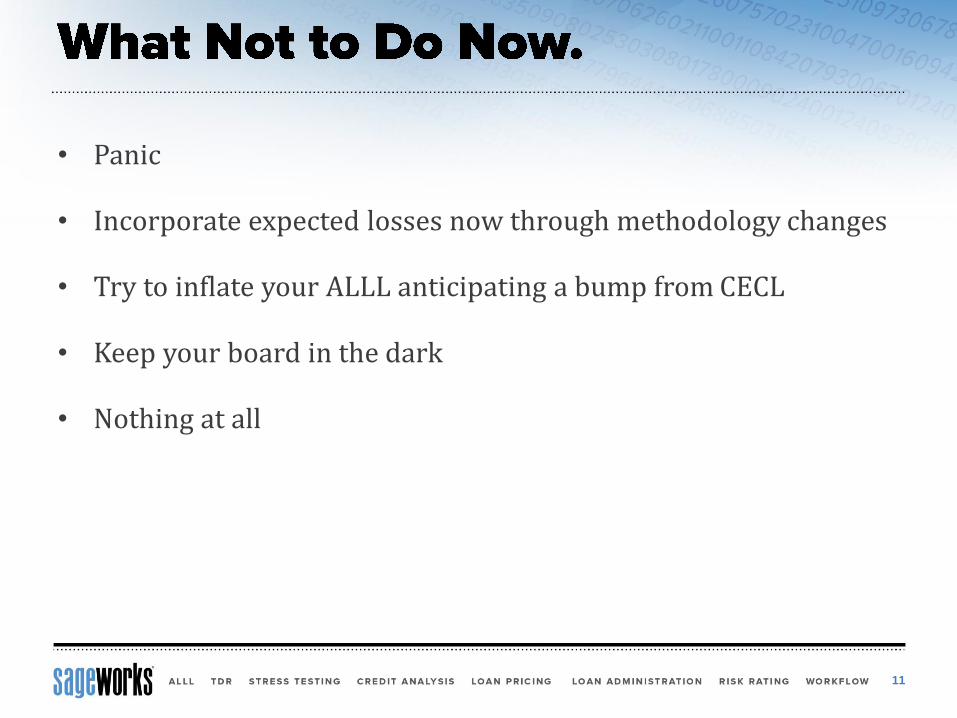

• Panic

• Incorporate expected losses now through methodology changes

• Try to inflate your ALLL anticipating a bump from CECL

• Keep your board in the dark

• Nothing at all

11

- Articles and references have wrongly stated that banks and credit unions will be required to forecast 30 years

- To try and curtail the problem of misinformation, the FASB plans to provide educational webinars on the guidance

12

Source: “FASB Warns of Misinformation About Credit Impairment Rules,” Bloomberg BNA, November 5, 2015

Misinformation is coming from “people who have a financial interest in telling you you have a problem so that they can come in and sell you a solution to fix the problem that you didn't really have.”

- FASB Vice Chairman James Kroeker

• Steve Merriett, the Fed’s chief accountant and deputy associate director of its Division of Banking Supervision and Regulation, said in a recent call the new accounting standards represent a fundamental change in accounting requirements for banks and credit unions. “This is not a tweak, and we do not believe that existing methodologies are OK without any adjustment.”

• “We think bank management will need to plan for the larger allowance levels we expect under the new standard.” (“Begin preparing now for CECL, says Federal Reserve,” 2015)

• “Small banks DO NOT need complex models: However, they may need to make changes to current systems for data collection and analysis”

» Steve Satwah, Sr. Accounting Policy Analyst, Board of Governors of the Federal Reserve System (“On The Horizon,” 2014)

• “I’m not trying to say there’s not going to be effort involved; there will be. For larger, more complex institutions or even institutions with complex credit exposure, this is going to be difficult. But for a lot of places, this may be not as hard as it seems.”

» Graham Dyer, Grant Thornton (“How to Forecast Future ECLs,” 2015)

13

1. Minimize risk in loans you’re underwriting today

2. Start cross-department conversation now, including Credit and Finance

3. Capture, archive and incorporate loan-level detail into the ALLL calculation

4. Reduce dependency on spreadsheets

5. Consider the impact of moving to a more robust calculation – migration analysis, PD/LGD

6. Review/strengthen risk rating procedures at the credit union

7. Improve data processes and increase data integrity

8. Be proactive rather than reactive

14

In a document released on November 9th, the Federal Reserve Bank of Richmond issued a

Supervision News Flash that included nine suggestions for what credit unions and other

financial institutions should be doing now to prepare for CECL. (“Supervision News Flash,”

2015)

Highlights:

• Involve all areas within your company to identify data points and any potential system

changes

• Review current ALLL and credit risk management practices

• Begin collecting data for all existing credits as well as any new loan originations that

might be used in a lifetime expected credit loss model

• Continue following existing GAAP guidance for maintaining the allowance until the new

rule is effective

• Begin evaluating capital levels to ensure they will be sufficient to support the

implementation of CECL on day one

15

“CECL implementation is, in many ways, a project management challenge that will affect most parts of your business to one degree or another.” (“Fed Quarterly Conversations,” 2015)

16

• IT Systems

•Vendor ManagementOperational

•Credit Business Lines

•Mergers & Acquisitions

•Counter-partiesCredit

•Regulatory Reporting

•Tax

•Financial ReportingLegal/ComplianceR

isk

Man

agem

ent

Note. Adapted from “Current Expected Credit Loss (CECL) Model: Answers to Your Questions,” by the Federal Reserve Bank of St Louis, 2015, Quarterly Conversations, Live from Eagle Bank and Trust Little Rock, AR. Retrieved from: https://bsr.stlouisfed.org/conversations/includes/resources/November%202015%20Quarterly%20Conversations%20(CECL)_FINAL.pdf

17

18

“Begin identifying and collecting actual loss data required for the implementation of the CECL model”

– Fed Perspectives Webinar, October 30, 2015

19

Depending on chosen methodology, these are data points to consider:

** Average lifetime includes prepayments and other items

20

21

22

23

Unadjusted historical

lifetime loss experience

Adjustments for past events and

current conditions

Adjustments for reasonable and

supportable forecasts

Estimate of expected credit

losses

As outlined by the Federal Reserve in their October webinar on CECL.

Source: “Loss Data, Data Analysis, and the Current Expected Credit Loss (CECL) Model”, Fed Perspectives Webinar, 10/30/15

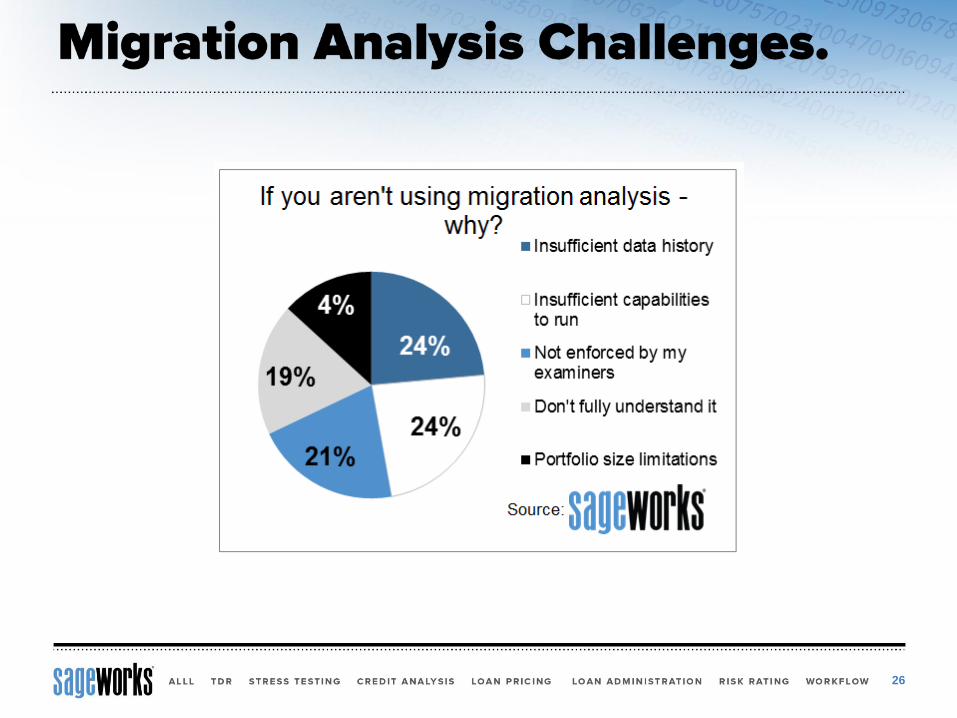

• Choice of methods include:• Loss-rate methods• PD/LGD• Migration analysis• Vintage analysis

• Any reasonable approach may be used – guidance is not prescriptive

• Data required for CECL model also required for migration analysis

• Often considered a more “robust” form of analysis

» Should result in more accurate allowance than historical loss

» More insight into sub-segmented pools (credit quality/deterioration)

» Less prone to examiner criticism if performed correctly

» More effectively justify decrease in provisions, if merited

• Adjusts ALLL provision to reflect the conditions of the current portfolio

• Can drive pro forma projections

24

• Statistically viable method to accurately derive a loss rate

• Highlights changes in portfolio composition and quality

• Reserve may be more accurate because it factors in the risk profile and underwriting standards in place during the loss horizon

• Attractive to regulators – involves a statistical, granular analysis of the portfolio

• Currently considered the most robust and comprehensive loss calculation under today’s guidance

25

26

27

• Methodology gaining popularity after mentions in Basel II, Basel III and FASB CECL guidance

• Currently used by larger credit unions, primarily

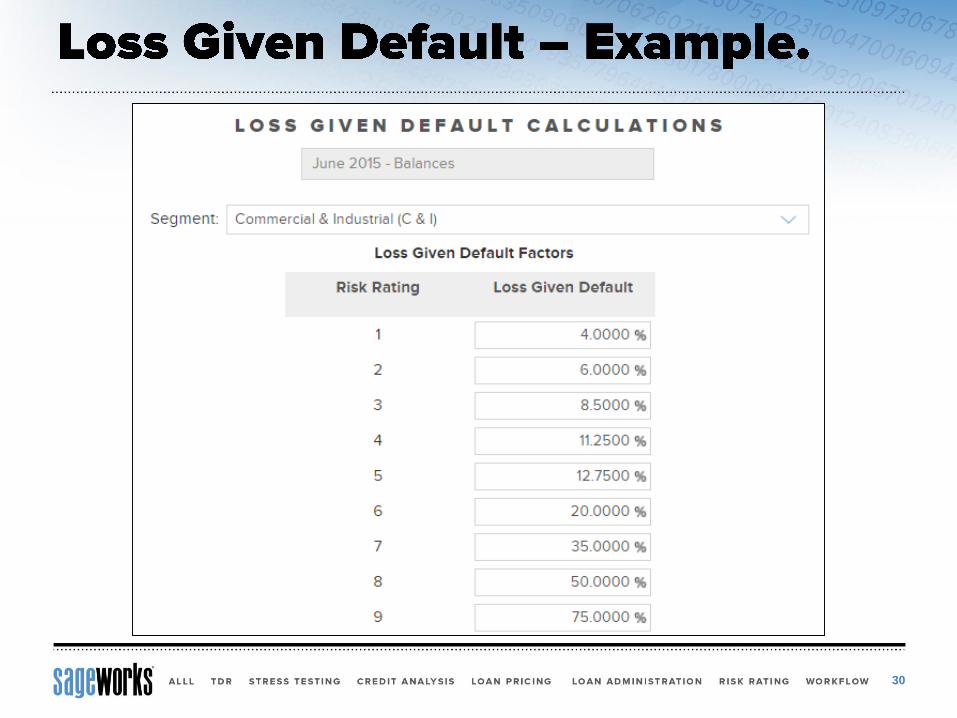

• PD (probability of default): the average percentage of borrowers that default over a certain time period

• LGD (loss given default): the percentage of exposure to a credit union if the borrower defaults

• EAD (exposure at default): an estimate of the outstanding amount, or exposure to the credit union, in the event a borrower defaults

28

• Definition of “default” must be determined – 90 days past due?

• Also, time period over which PD is measured

29

30

31

• Challenges

» Calculating PD and LGDs using internal resources – more complex

» Gathering and interpreting loss data

» Validating the model and proving forecasting accuracy

• Benefits

» Enables estimation of the reserve on a loan-by-loan basis

» Drive improvements in underwriting standards, data collection

» Leverage for Basel III or CCAR/DFAST (larger institutions)

32

• Track homogeneous loans by origination period

» Year, quarter, etc.

• Measure losses accumulated on each vintage

• Apply the expected cumulative loss to the remaining vintages outstanding

• At measurement date, adjust expected loss rate for current conditions and reasonable & supportable forecasts

33

Adapted from: “Credit Risk Management’s Role in Measuring ECLs” by Graham Dyer of Grant Thornton at 2015 Risk Management Summit

Can use economic indicators to forecast

• Challenges» Does not capture the impact of Q Factors inherently» May require more sophisticated techniques to identify

correlations» Difficult for new or growing product offerings

• Must capture life of loan in history for analysis to be meaningful

• Benefits» Establishes strong historical basis for expectation of lifetime

losses» Able to address portfolios that have inconsistent seasoning

(growing or shrinking portfolios)

34

Source: “Credit Risk Management’s Role in Measuring ECLs” by Graham Dyer of Grant Thornton at 2015 Risk Management Summit

• Carefully analyze your portfolio’s performance and loss history

» For each line of business

» Engage credit and risk management partners

• Review your credit union’s resources and data collection processes

• Account for changes in credit policies, portfolio volume and management

• Develop quantifiable research and documentation to support decision

• Consider different loss methods or periods across segments if portfolio analysis warrants the change

35

• Begin / accelerate data gathering process

• Consider the impact of moving to a more robust loss

methodology

• Begin strategic planning for:

» Collaboration on ALLL between credit and finance

» Begin strategic planning for possible capital adjustment

• Start developing a high-level implementation plan for CECL

36

37

38

AARON LENHART

Sr. Risk Management [email protected]

ED BAYER

Vice [email protected]

RISK MANAGEMENT SOLUTIONS

Save significant time – up to 80% –on each ALLL calculation

Quickly access, store loan-level data for reporting and to prepare for requirements anticipated with the FASB’s CECL model

Acronym or Abbreviation

Term

ALLL Allowance for loan and lease losses

CCAR Comprehensive Capital Analysis and Review

CECL Current Expected Credit Loss

C&I Commercial & Industrial

ECL Expected credit loss

DFAST Dodd-Frank Act stress testing

FASB Financial Accounting Standards Board

Fed Federal Reserve

GAAP Generally Accepted Accounting Principles

PD/LGD

- PD

- LGD

- EAD

Probability of default / loss given default

- Probability of default

- Loss given default

- Exposure at default

Q Factor Qualitative factor

TDR Troubled debt restructuring

39

• ALLL.com. (2015). Begin preparing now for CECL, says Federal Reserve. Retrieved from: http://www.alll.com/resource-center/begin-preparing-now-for-cecl-says-federal-reserve/

• ALLL.com. (2015). FASB sets CECL effective dates. Retrieved from: http://www.alll.com/resource-center/fasb-sets-cecl-effective-dates-2019-for-large-banks-2020-for-others/

• Biery, Mary Ellen. (2015). How to forecast future expected credit losses. Sageworks Blog. Retrieved from: http://www.sageworks.com/blog/post/2015/10/02/how-to-forecast-future-expected-credit-losses.aspx

• Dyer, Graham. (2015). Credit Risk Management’s Role in Measuring ECLs. 2015 Risk Management Summit.

• Federal Reserve Bank of Richmond. (2015). CECL – What You Can Do Now. Supervision News Flash. Retrieved from:https://www.richmondfed.org/-/media/richmondfedorg/banking/supervision_and_regulation/newsletter/2015/pdf/snl_20151009.pdf

• Financial Accounting Standards Board. (2015). Tentative Board Decisions. Retrieved from: http://www.fasb.org/cs/ContentServer?c=FASBContent_C&pagename=FASB/FASBContent_C/ActionAlertPage&cid=1176167530242

• Lugo, Denise. (2015) FASB Warns of Misinformation About Credit Impairment Rules. Bloomberg BNA.

• Merriett, S., Wakim, J., Satwah, S., (2015). An overview of the current Expected Credit Loss Model (CECL) and Supervisory Expectations. Fed Perspectives. Retrieved from:https://bsr.stlouisfed.org/perspectives/final_fedperspectives_cecl_october%202015.pdf

• Satwah, Shuchi. (2014). On the Horizon – The Current Expected Credit Losses (CECL) Model. Accounting & Auditing Forum 2014. Retrieved from: https://www.kansascityfed.org/publicat/events/banking/2014accountingandauditingforum/2014-AAF-CECL.pdf

• Stackhouse, J., Sherrer, L., Ciluffo, S., (2015). Current Expected Credit Loss (CECL) Model: Answers to Your Questions. Fed Quarterly Conversations. Retrieved from:https://bsr.stlouisfed.org/conversations/includes/resources/November%202015%20Quarterly%20Conversations%20(CECL)_FINAL.pdf

40

• ALLL.com – Everything ALLL, including news articles, whitepapers, and

peer discussions

• ALLL Forum for Bankers – LinkedIn group for credit union & bank execs

• CECL Post-release webinar - panel-style webinar with thought leaders

from top accounting firms

• CECL Prep Guide – A handy illustrated guide that covers the basics

• FASB’s CECL Prep Kit - complimentary toolkit, to help you better prepare

• Sageworksanalyst.com – Learn about Sageworks’ risk management suite

• Talk to an ALLL specialist

41