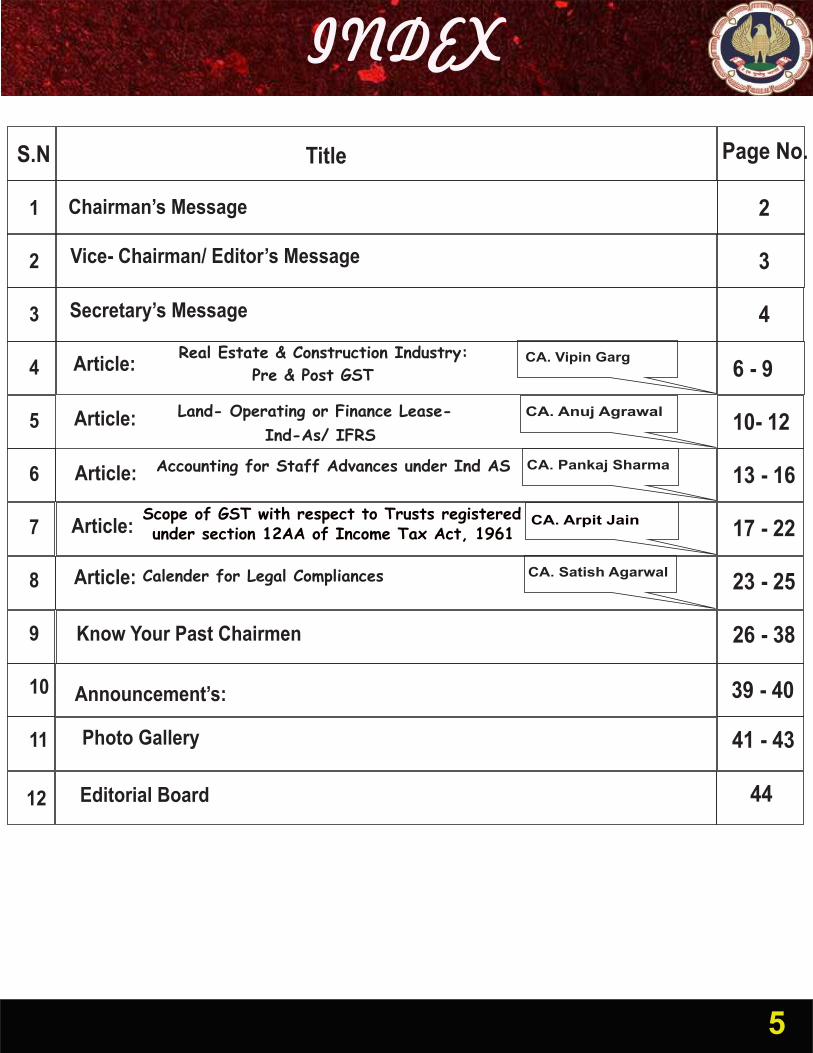

Central India Regional Council of The Institute of Chartered Accountants of India Central India Regional Council of The Institute of Chartered Accountants of India Central India Regional Council of The Institute of Chartered Accountants of India Central India Regional Council of The Institute of Chartered Accountants of India CIRC Newsletter Volume 2: 2017-2018

We chartered accountants have been the conscience keepers of our national economy for decades, but the current grim global financial-economic scenario requires us to be all the more vigilant on this front for a secure future of our country. I wish to emphasise on the crucial need of not only keeping intact the glory of the profession's past achievements, but also amplifying these in future by meticulous and objective planning and efficient execution. Rather than adapting to the changes, all of us need to lead the changes for the better.

The legislature of India has cast an important responsibility on the able shoulders of chartered accountants to lubricate the wheels of economic growth by ensuring that the financial information reaching the intended users is reliable. We have to live up to the expectations of our society and the trust bestowed in us by the founding fathers of our nation.

The only thing that is never-changing is the change itself. And every change offers a new beginning. This is the eternal phenomenon that encompasses everything - our profession and the ICAI included. Being the backbone of financial discipline in India and conscience keeper of national economy fo r decades , ou r profession has today come to be known as one of the most vibrant

forces of socio-economic growth. .As I carry the baton of Vice- Chairmanship, I promise not to let you down, particularly when it comes to upholding the interests of the profession and the nation.

After new economic reforms there are exciting yet challenging times for Indian chartered accountants. World economy is in turmoil and is casting its shadow on India, thereby putting the role of CAs in sharp focus. The resilient Indian economy will surely withstand any trouble. The high status for the CAs and growing expectations from them also mean h ighe r respons ib i l i t i es and pressures on them. With the calls for private sector and governments to b e m o r e a c c o u n t a b l e a n d transparent getting louder, modern accountant's role is bound to come under frequent scrutiny. Remember, the future belongs to us. These are times to lead by example.

A journey of a thousand miles begins with a single step. So, join me in taking that first step together and rededicate ourselves to promote professional excel lence and opportunities to conquer these challenging times.

Respected Professional Colleagues,

CA. Churchill JainVice Chairman CIRC & Editor CIRC Newsletter

Secretary CIRCCA. Mukesh Bansal

Mobile: 9350774515

E.Mail: camukeshbansal@@gmail.com

4

From Secretary’s Desk

Respected members,

I feel pleasure to interact with you through this newsletter. Last few months were busy for all of us as we all were very busy on companies and Tax audits and further the introduction of GST has burdened us with so many returns and compliances specially in the month of October which is also the month of festivals like Deepawali, Durga pooja and many others. Despite all these we all are always devoted to our profession with full dedication and determination and that is why we are able to discharge our responsibility in the best possible manner.

In the month of August we had our regional conference at Kanpur where speakers from different parts of the country deliberated on various topics of professional in terest and th is conference was attended by members of many branches of CIRC. The chief guest of the conference, Hon’ble Dr. Dinesh Sharma ji Deputy Chief Minister of Uttar Pradesh addressed the gathering and also recognized the importance of CAs in maintenance of financial Discipline and to curb the corruption. He also invited our CIRC to submit suggestions in the process of preparation budget of Uttar Pradesh and also assured to consider our various suggestions regarding our profession.

As I always say that our Branches are our backbone and all the branches are very active and work very hard for holding of various activities for our members and students. Recently we had the opportunity to visit various branches of CIRC and we sincerely appreciate the devotion and dedication of managing committee members for effective working of the branches. I also thank Udaipur branch for successfully

hosting CIRC Cricket Tournament 2017, one of the biggest event of CIRC. In this tournament 16 teams from different branches participated and this is for the first time that sixteen teams took participation. I Congratulate Udaipur Branch for winning the tournament and organising this event in such a wonderful manner.

In the recent time one of the most important emerging professional opportunities for our members is in the area of Insolvency and bankruptcy code. This area is expected to grow very fast and till now very few insolvency professionals are available. I request members to pass Limited Insolvency examination and to become Insolvency Professional. We at CIRC are also planning to organize workshops on Insolvency and bankruptcy code so that it may be helpful to the members to pass the examination.

We at CIRC always try to serve the profession to the best of our abilities and also need your guidance and active participation by giving your suggestions regarding the working of CIRC and any new and innovative idea that come to your mind for overall benefit of members and profession.

A dream doesn't become reality through magic; it takes sweat, determination and hard work.

Real Estate & Construction Industry: Pre & Post GST

The never ending litigation of taxation relating to works contracts, particularly in construction industry and more particularly & challenging in real estate industry, gets a fresh turn in GST regime. Let us travel through the recently retired regime of works contract in pre GST, to newly born GST regime, presently grappling with transitional issues. The subject is a little lengthy, hope you stay the length of present Article.

Works Contract under Pre-GST: Service Tax LawThe Service Tax Law was reincarnated on 1st July 2012 when the concept of Negative List came into being. In this Negative list Regime, a new sec 66E was introduced to specify certain services as “declared services” wherein two clauses (b) and (h) of Sec 66E dealt with cases of a Works Contract.

Clause (b) to sec 66E: Const ruc t ion o f a complex, building, civil structure including a complex or building indented for sale to a buyer except where the entire consideration is received after the completion certificate.

Clause (h) to sec 66E: Service portion in the execution of a Works Contract.

It is interesting to note that though the services

declared in clause (b) relating to construction of complex as above very much falls within the meaning of Works Contract in clause (h), but still the legislature in its wisdom specifically also declared the construction of complex service separately in clause (b). It seems as if it has been done as an abundant caution to ensure that House Buyer Agreements (HBA)/ Builders Buyer Agreements (BBA) entered into by Real Estate developers with the prospective buyers of apartments, if in litigation are upheld as out of the meaning of Works Contracts under clause (h), still the Government can levy service tax under clause (b). However, the litigation went in favor of Government when the Supreme Court in the year 2013 upheld that such House Buyer Agreements by real estate developers does fall within the scope of Works Contracts, in the matter of L&T c a s e , s e e f u l l j u d g e m e n t a t http://judis.nic.in/supremecourt/imgs1.aspx?filename=40833Valuation of Service portion in a Works Contract.

It is to be noted that it is only the service portion of works contract/construction of complex, which can be the subject matter of service tax levy. A Works Contract is a composition of 'Goods' as well as 'Services' which are so intermingled with each other that it forms a Single Indivisible

6

Composite Contract. Furthermore, in the case of House Buyers Agreement (HBA) executed by real estate developers, (which is also a Works Contract as upheld by Apex Court in L&T case supra), it is a composition of three things, undivided share in Land, Goods and Services, three of which are so intermingled that it forms a Single Indivisible Composite Contract. Thus the challenge is as to how to extract the value of service portion out of the Composite Value of such a Works Contract.

In Pre-GST Service Tax law there were two notifications to deal with this valuation aspect of services from a Works Contract.

Notification No. 24/2012 dt 06.06.2012 amended rule 2A, dealt with works contracts covered in clause (h) of sec 66E i.e. other than real estate House Buyer Agreements (HBA).

(see fu l l Not i f icat ion No 24/2012 at http://www.cbec.gov.in/htdocs-servicetax/st-notifications/st-notifications-2012/st24-2012

Notification No. 26/2012 dt 20.06.2012 amended by Notification 08/2016 dealt with abatement in case of House buyers agreements (HBA) covered in clause (b) of sec 66E in case of Real Estate.

( s e e f u l l N o t i f i c a t i o n N o . 8 / 2 0 1 6 a t http://www.cbec.gov.in/resources//htdocs-servicetax/st-notifications/st-notifications-2016/st08-2016.pdf

Broadly speaking in case of construction contract (original works) the valuation of service portion used to be taken at 40% and in case of real estate House Buyer Agreements (HBA) the value of service portion used to be taken at 30%.

Works Contract under Pre-GST: State VAT LawsBy and large all State Laws dealing with VAT defined Works Contract with quite a large scope

including all the agreements of building construction, manufacture, processing, fabrications, erections, installations, fitting out, improvement , modi f icat ion, repai r, or commissioning of any Movable or Immovable property. All the State VAT Laws levied VAT on the value of Goods transferred in the course of executing the works contracts. All state VAT laws prescribed valuation rules to arrive at the value of Goods involved in the execution of works contracts and also notified an alternate way of composition scheme whereby in lieu of VAT, specific percentage of aggregate value of turnover was levied as composition levy. Most of the contractors as well as real estate developers used to opt for composition levy instead of going by valuation as per valuation rules. That is how the VAT liability used to be discharged till 30th June 2017.

Works Contract under GST Regime

Under GST regime the very difference of 'Goods' and 'Services' has been dispensed with. The concept of sale, manufacture and provision of service has gone and only a single concept of supply (whether of Goods or Services) has been brought in.

GST Law has come up with a new concept of “Composite Supply” which broadly means a supply consisting of two or more taxable supplies of goods or services or both or any combination thereof which are naturally bundled and supplied in conjunction with each other, one of which is principal supply.

Going by this definition of “Composite Supply” u/s 2(30) of the CGST Act, one can appreciate that all works contracts very much fall within the meaning of Composite Supply.

Further the concept of Works Contract has been redefined under the GST Law u/s 2(119) of CGST Act whereby the works contracts pertaining to

7

movable property have been excluded from the definition of Works Contract and therefore only works contracts relating to immovable property fall within its statutory definition u/s 2(119). Thus in GST regime the hitherto concept of Works Contract gets bifurcated into

(a) Works Contract (Immovable Property) covered u/s 2(119) of CGST Act

(b) Works Contract (Movable Property) excluded from statutory definition of Works Contract and classified a Composite Supply u/s 2(30) of CGST Act.

Taxation of works contracts (Immovable Property) u/s 2(119)

Like under Pre GST Service Tax law, the GST Regime has come up with Schedule II (Para 5 & 6) to declare certain supplies to be treated as supply of services. The clauses (b) and (h) of erstwhile sec 66E have been reintroduced as clause (b) of Para 5 & clause (a) of Para 6 to schedule II of CGST Act.

Clause (b) of sec 66E pertaining to construction of complex services has became clause (b) of Para 5 of Schedule II

Clause (h) of sec 66E pertaining to works contract service has become clause (a) of Para 6 of schedule II

The appreciable improvement is that in case of real state, apart from completion certificate, the first occupation of the Complex has also been given the sanctity of completion of the project irrespective that completion certificate of the project is awaited, thus after actual occupation of the complex, there will be no liability of GST only because the completion certificate is awaited from competent authority where delay is a routine.

Hence the application of brute force to composite

works contracts to extract the value of goods and services for the levy of VAT and Service Tax, is no longer required, as under GST regime the works contracts is essentially service by deeming provision of declared services incorporated under schedule II of GST regime.

Rate of Tax: The GST rate as per notified tariff via notification 11/2017-Central Tax (Rate) dated 28.06.2017 under CGST Act is 9% as per Serial No. 3. Equally 9% is the rate under SGST, thus a combined GST rate is 18%. However in case of Real Estate House Buyers Agreements (HBA) which involve value of Land also, there is a provision of abatement of 1/3rd value as per Para 2 of the aforesaid notification, thus the effective rate in case of Real Estate is 12%.

Input Tax Credit: Full ITC u/s 16 (CGST Act) will be available on al l inward supply of Goods/Services including Goods/Services under reverse charge, used as inputs for supply of works contracts service as per ITC rules. Provided in case of Real estate any excess ITC over output GST liability, will not be eligible for any refund.

At times there is a doubt raised whether clause (c) and clause (d) of sec 17(5) which restrict the ITC in relation to an immovable property, would pose any problem in availment of ITC in construction & real estate industry as both industries deal in construction of immovable property only. The author's view is abundantly clear that the aforesaid doubt is absolutely unfounded and clause (c)/(d) of sec 17(5) has no application and there is no restriction at all in availing ITC because of these clauses of sec 17(5).

Transition from Pre GST to GST regime

The transition provisions are provided under chapter XX of CGST Act. Broadly the ITC pertaining to stock as on 30 June 2017 is allowed to be carried forward under GST regime. There is no composition scheme under GST regime and

8

the construction industry has to maintain all books of accounts and inward supply record, to claim ITC from output liability on execution of works contract classified as supply of service.

In case of Government contractors they need to close their sales invoices which practically consist of completion of measurement books (MB) in government (Contractee) records. The MB completed and recorded till 30 June 2017 will remain under Pre GST regime while the MB prepared from 1st July 2017 onwards will attract full rate of 18% GST under new regime. For Government contractors with low inventory of WIP as on 30th June 2017, it will lower their tax burdens as their ITC on stock as on 30th June 2017 is likely to be low impacting their cash flow in new regime. Further the construction contractors and particularly government contractors need to revisit their construction contracts to ascertain the burden of additional tax liability under GST and to renegotiate with contractee as per revised costing under GST regime.

Taxation of Works Contracts (Movable Property) u/s 2(30)

All works contracts relating to movable property are no longer a works contract under statutory scheme of GST but rather all such works contracts relating to movable property are simply a case of composite supply u/s 2(30) of CGST Act. Therefore the rate of GST will be decided on

the basis of “Principle Supply” under such works contracts (movable property). If the principle supply is that of services then the applicable GST rate on respective service will apply, and if the principle supply is that of Goods, then the applicable GST rate of such principle supply of goods will apply. Thus in GST regime, the theory of dominance test is back under the nomenclature of principle supply.

Full ITC u/s 16 (CGST Act) will be available on all inward supply of Goods/Services including Goods/Services under reverse charge, used as inputs for supply of works contracts service as per ITC rules.

Conclusion

Now under GST regime there is no mandatory extraction from composite value of Contract, to arrive at the value of Goods and Services separately but rather it is an issue of classification of works contracts (movable property) on the basis of principle supply. Thus now under GST the entire works contract (movable property), either it is a supply of goods or supply of service as decided as per dominant test called as principle supply test.

So far as the works contract (immovable property) is concerned, it is essentially a supply of service by virtue of schedule II.

In the current Indian accounting system, all lands are being shown as fixed assets in the financial statements of any Company and are being depreciated based on their lives accordingly.

After the introduction of Ind-As for Indian Companies, there is a need to evaluate such lands related payments and their structures whether it falls under Operating leases or Finance lease and account them accordingly. Building/ Structures made on these lands will then be depreciated separately based on their own useful lives.

Para 58 of Ind-As 16 “Property, plant & equipment” states that “Land and buildings are separable assets and are accounted for separately, even when they are acquired together……

Para 4 of Ind-As 17- “Leases” states that “A lease is an agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time.

A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an asset. Title may or may not eventually be transferred.

An operating lease is a lease other than a finance lease.

Now, there could be a situation where land has been purchased and a legal title has been passed to the entity or it is in a process to getting it transferred in the name of the entity then such lands will be shown as Land under fixed assets and will not generally be depreciated considering that there is an unlimited useful live for any land.

If the land which has not been legally transferred/ in a process to transfer (considering all possible legal terms) in the name of the entity then it could either be Operating or Finance lease assuming that the entity has got right to use such lands based on the other classification criteria which defines operating or finance leases. The broad accounting can be summarized as below –

1- Assuming an entity has obtained a lease land for around 30-35 years for some business purposes and there is some upfront premium

10

which entity has paid at the inception of such arrangements to the land owner and it requires some monthly rental payments to be made over the period of the lease term. Now, there is a current practice to show this upfront premium paid as fixed assets component and hence it is being depreciated from the fixed assets schedule, however after the applicability of Ind-As these premium paid will be treated as prepaid rent on operating leases and will be required to re-class such amounts from fixed assets schedule to current/ non-current assets to show as prepaid rent and amortize it over the period of such operating leases through Profit and Loss account. The normal monthly payments of such land will continue to charge into profit and loss as it is being done in the current practice,

2- Now, suppose there is a land which has been given around 70-80 years by paying some upfront premium at the inception with some monthly rentals. Assuming that after considering all criteria to satisfy it being a finance lease, the Management of the entity classifies the same as finance lease (assuming that it covers major economic life of the land), then because of the introduction of Ind-As which require to separate land & building, then the entity needs to calculate PV of all minimum lease payments and finance lease accounting will then be followed separately. Here one can argue that if the lease period for which such lands has been given for use is for longer period let's say 90 or more years then the fair value computation for finance lease will have no material difference comparing to its carrying value, these can be documented by making a policy for evaluating finance lease computation (for example the management can make a policy that all lands upto 30 to 60 years will be evaluated for operating leases and upto 60 to 90 years will be for finance leases purposes, rest all will not be considered because of immaterial effect),

3- At the transition, all such fixed assets within land and building will be reclassified to other parts

of balance sheet (current assets/ non-current assets),

4- All the structures/ building which are being made upon these lands will be evaluated for their expected useful lives and presented separately in the fixed assets schedule and will be depreciated accordingly,

5- Lease equalization will be required in case rentals which are being paid for using these lands , however Ind-As 17 has brought with a CARVE OUT (carve out means difference in Ind-As comparing to IFRS as issued by IASB) which requires no adjustment if such changes are normal inflation rates whereas IASB issued standard on Leases i.e. IAS-17 on “Leases” requires to make lease equalization irrespective of inflation is expected one or not. One can argue that there could always be difference in the expected inflation rate and the escalation clasues rates which has exempted from any adjustment by the Ind-As 17,

6- If there is any rent free period/ or any other incentives which has been provided to the entity, then the same will be required to be adjusted in the rent equalization,

7- There could be some instances where lease agreement of land has some restriction to use it in a specific manner and does not give lessee a right to get further renewal after the expiry of the terms mentioned in the contract, then usually it will be significant notion while deciding the classification be it operating or finance lease, There is one more interesting thing to note that as per IAS-40 “Investment Property” (Standard issued by IASB) which gives an option to classify such operating leased land into Investment property and show them at fair value through profit and loss account however by using a CARVE OUT Indian version of this standard i.e. Ind-As -40 does not give such option to use Investment property for such operating leases.

11

These are some snapshots about the changes related to lands classification in our existing accounting system and how internationally accredited standards i.e. IFRS require to do that. These will change some of the perception/ planning from management point of view as well as it changes fixed assets schedule and ratios as well.

Above ment ioned a l l in te rpre ta t ions /

explanations are based on best practices which are broadly used by large industries using IFRS frameworks and should not be construed as advice because there could be many terms/ instances where measurement/ classification could change/ differ what has mentioned above. For any further discussion, please email on [email protected]

Companies in their normal course of business extends loan to its employees under some favourable terms in the form of nil or below market interest rate. It may be noted that where the loans are extended under normal commercial terms, there is no special consideration involved and accordingly no specific accounting issues arises. Therefore, the normal accounting principles prevails to record such transactions.

However, where the loan is extended under some favourable terms then such transaction includes a special consideration which shall also be required to be recorded in the financial statement appropriately.

Existing IGAAP doesn't provide any guidance relating to the accounting treatment of such special consideration whereas under Ind AS there is an adequate guidance relating to the accounting treatment of loan extended at nil or below market interest rate.

Accounting Treatment under existing IGAAP

AS 15 Employees benefits doesn't provide any specific guidance relating to the accounting treatment for nil or below market interest rate loans to employees. Therefore, under the existing IGAAP, whenever any employee is advanced with any amount which is at nil or below market interest rate, it should be recorded in the financial statement equivalent to the amount disbursed. Interest income for the period is also calculated by reference to the contracted rate (nil or concessional rate) and recognised in the statement of profit and loss account.

Case Study

Let understand the required accounting treatment of staff advances as per the existing IGAAP with the help of a practical example:-

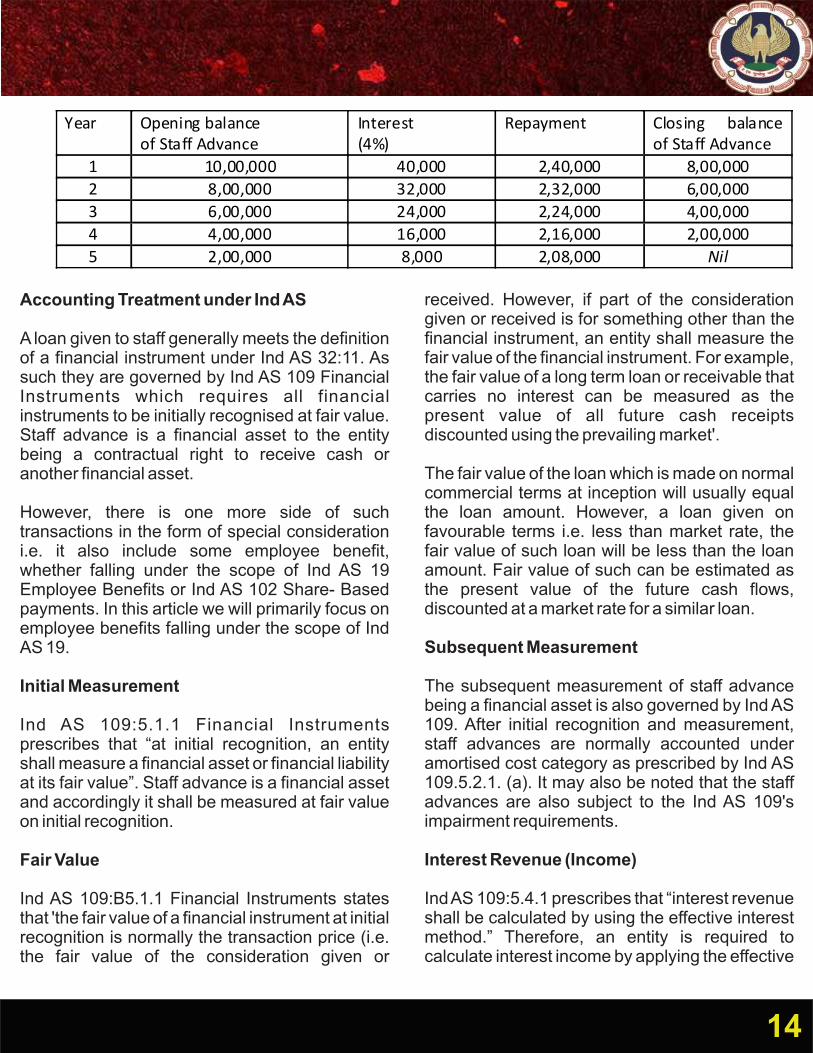

Jupiter ltd has advance a loan of Rs 10,00,000 to its employee at 4% (market rate 10%) which is repayable in 5 equal annual installments along with interest at each year end.

Amortisation table:

13

Accounting Treatment under Ind AS

A loan given to staff generally meets the definition of a financial instrument under Ind AS 32:11. As such they are governed by Ind AS 109 Financial Instruments which requires all financial instruments to be initially recognised at fair value. Staff advance is a financial asset to the entity being a contractual right to receive cash or another financial asset.

However, there is one more side of such transactions in the form of special consideration i.e. it also include some employee benefit, whether falling under the scope of Ind AS 19 Employee Benefits or Ind AS 102 Share- Based payments. In this article we will primarily focus on employee benefits falling under the scope of Ind AS 19.

Initial Measurement

Ind AS 109:5.1.1 Financial Instruments prescribes that “at initial recognition, an entity shall measure a financial asset or financial liability at its fair value”. Staff advance is a financial asset and accordingly it shall be measured at fair value on initial recognition.

Fair Value

Ind AS 109:B5.1.1 Financial Instruments states that 'the fair value of a financial instrument at initial recognition is normally the transaction price (i.e. the fair value of the consideration given or

received. However, if part of the consideration given or received is for something other than the financial instrument, an entity shall measure the fair value of the financial instrument. For example, the fair value of a long term loan or receivable that carries no interest can be measured as the present value of all future cash receipts discounted using the prevailing market'.

The fair value of the loan which is made on normal commercial terms at inception will usually equal the loan amount. However, a loan given on favourable terms i.e. less than market rate, the fair value of such loan will be less than the loan amount. Fair value of such can be estimated as the present value of the future cash flows, discounted at a market rate for a similar loan.

Subsequent Measurement

The subsequent measurement of staff advance being a financial asset is also governed by Ind AS 109. After initial recognition and measurement, staff advances are normally accounted under amortised cost category as prescribed by Ind AS 109.5.2.1. (a). It may also be noted that the staff advances are also subject to the Ind AS 109's impairment requirements.

Interest Revenue (Income)

Ind AS 109:5.4.1 prescribes that “interest revenue shall be calculated by using the effective interest method.” Therefore, an entity is required to calculate interest income by applying the effective

Year Opening balance of Staff Advance

Interest (4%)

Repayment Closing balance of Staff Advance

1 10,00,000 40,000 2,40,000 8,00,000

2 8,00,000 32,000 2,32,000 6,00,000

3 6,00,000 24,000 2,24,000 4,00,000

4 4,00,000 16,000 2,16,000 2,00,000

5 2,00,000 8,000 2,08,000 Nil

14

interest method to the amortised cost rather than using the contracted rate on the principal outstanding.

Difference between Loan amount and Fair Value

Ind AS 19:8 Employee Benefits defines “Employee benefits are all forms of consideration given by an entity in exchange for service rendered by employees”. Granting of advance at nil or below market rate interest to employees on the basis of services rendered by them is an implied benefit toward the employees. Accordingly, this implied benefit should be recognised as an employee benefit expense.

However, Ind AS 19 Employee Benefits does not provide any direct guidance relating to the accounting treatment for this kind of benefit. In the absence of any direct guidance, the general principles of Ind AS 19 shall be applied to determine:

(i). whether this benefit should be immediately written off or amortised over some longer period; and (ii). what should be the basis of allocation, if an entity decides to amortise it. Immediate expense recognition or amortisation of

employee benefitWhere the staff advance is extended under favourable terms without any service obligation on part of employee, then such benefit relates to past services, and accordingly it should be recognised in profit or loss immediately.

On other hand, the amount of benefit should be amortised over the period in which the services are rendered by the employee, where the staff advance extended under favourable term is linked with any service obligation.

The basis of amorisation of such benefit over a period of service may be:

(i). straight-line amortisation of the initial difference over the applicable service period; or

(ii). difference between interest income computed with reference to effective interest method and interest payable in each period by the employee.

Case Study

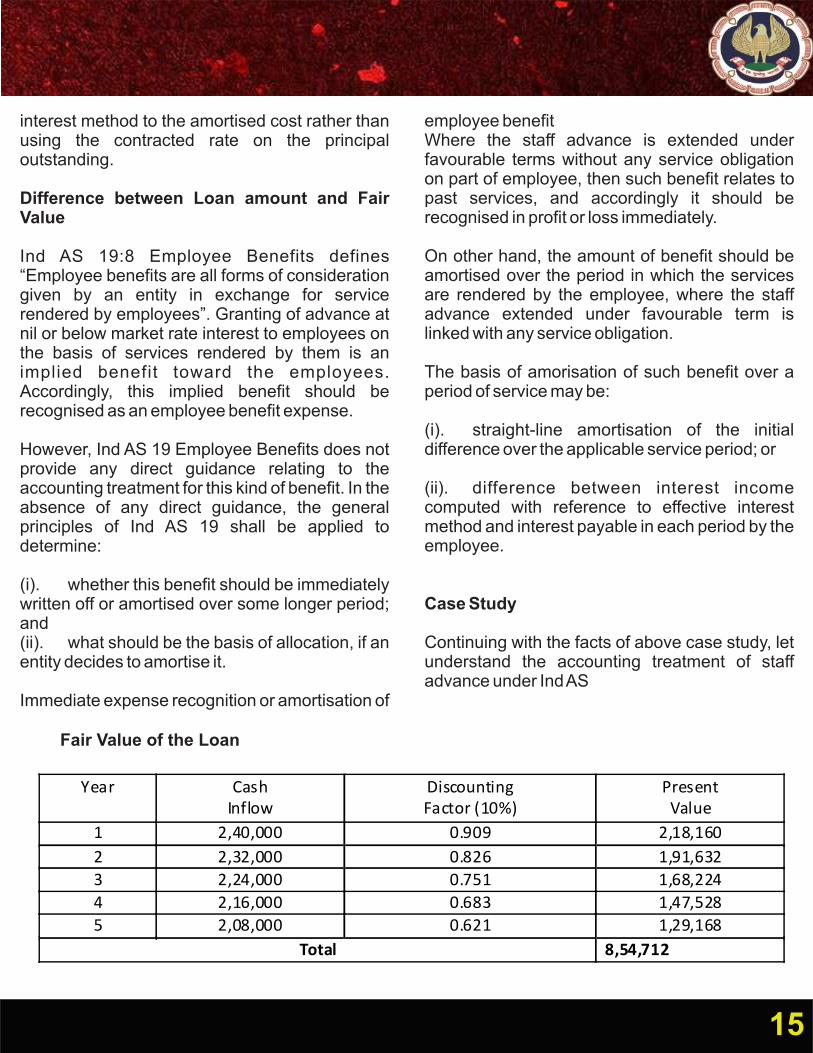

Continuing with the facts of above case study, let understand the accounting treatment of staff advance under Ind AS

Year Cash Inflow

Discounting Factor (10%)

Present Value

1 2,40,000 0.909 2,18,160

2 2,32,000 0.826 1,91,632

3 2,24,000 0.751 1,68,224

4 2,16,000 0.683 1,47,528

5 2,08,000 0.621 1,29,168

Total 8,54,712

Fair Value of the Loan

15

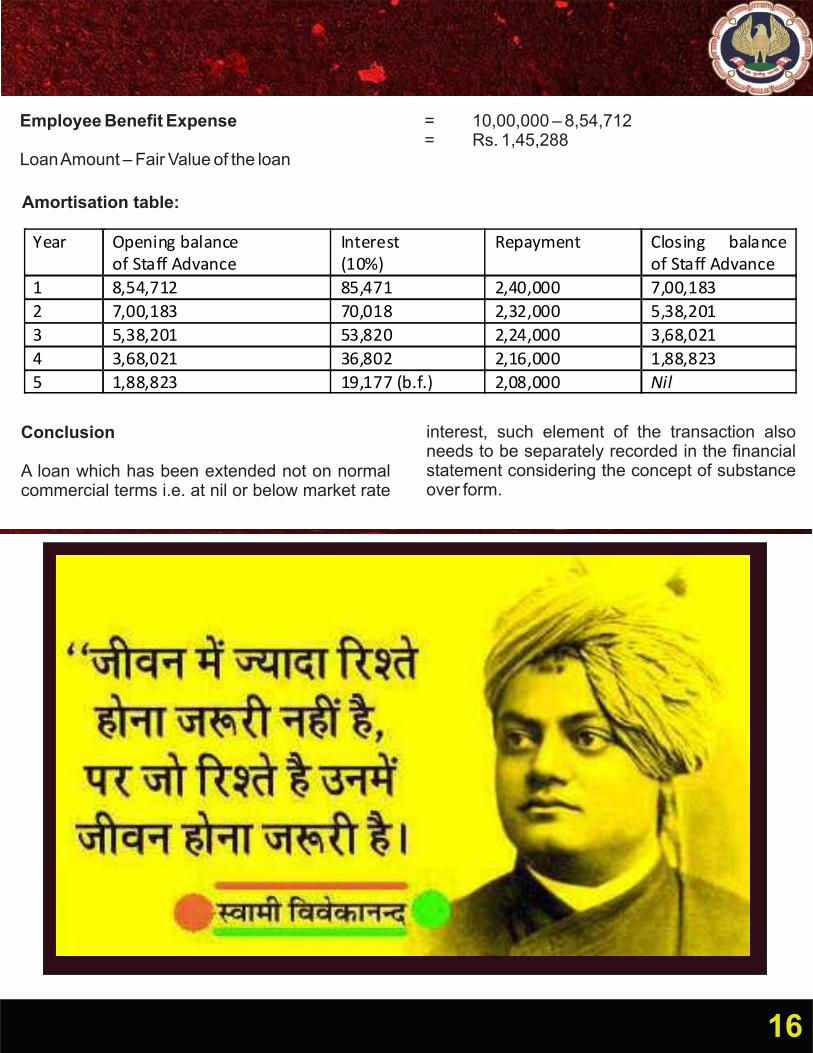

Employee Benefit Expense

Loan Amount – Fair Value of the loan

Conclusion

A loan which has been extended not on normal commercial terms i.e. at nil or below market rate

= 10,00,000 – 8,54,712= Rs. 1,45,288

interest, such element of the transaction also needs to be separately recorded in the financial statement considering the concept of substance over form.

1. GST has finally rolled out in the nation from 1st July, 2017. It is considered to be a biggest tax reform in India, post independence.

2. After the GST Act have been passed by the state of Jammu and Kashmir with effect from 06th July, 2017, the dream of “One Nation, One Tax”, of honorable Prime Minister – Shri Narendra Modi, came true. He always regarded GST as “Good and Simple Tax”. In this article I have attempted to cover the scope of GST on the religious and charitable trusts registered under section 12AA ofIncome Tax Act, 1961 (hereinafter referred as Charitable Trusts), and consequently analyzing how much good and simple the provisions are.

3. There are a lot many services provided by the Charitable Trusts. The provisions relating to taxation on activities carried out by the charitable trusts has been borrowed from erstwhile service tax provisions. All the services provided by such entities are not exempt from GST. Hence there are many services which will come within the ambit of GST.

4. Some exemptions has been provided by way of notification number 12/2017 Central Tax

(Rate), dated 28.06.2017. In further paragraphs I will try to cover various areas of revenue along with their GST implications on charitable trustskeeping in mind various exemptions provided by the aforementioned notification.

5. Revenue from charitable activities - since the trusts are charitable trusts, they would obviously be involved in charitable activities. There are some specific exemptions (discussed under para 6-8) available to charitable trusts and some general exemptions (discussed under para 9-15) which are available to every person. Firstly talking about the specific exemptions.

6. S no.1 of said notification exempts charitable services and reads as under:

“(1) Services by an entity registered under section 12AA of the Income-tax Act, 1961 (43 of 1961) by way of charitable activities."

The term charitable activities has been defined in clause (r) of the said notification. Therefore it should be interpreted in a restricted manner:

“(r) charitable activities means activities relating to-

17

(i) public health by way of ,-

(A) care or counseling of (I) terminally ill persons or persons with severe physical or mental disability; (II) persons afflicted with HIV or AIDS; (III) persons addicted to a dependence-forming substance such as narcotics drugs or alcohol; or(B) public awareness of preventive health, family planning or prevention of HIV infection;

(ii) advancement of religion , spirituality or yoga;

(iii) advancement of educational programmes or skill development relating to,-(A) abandoned, orphaned or homeless children;(B) physically or mentally abused and traumatized persons;(C) prisoners; or

(D) persons over the age of 65 years residing in a rural area;

(iv) preservation of environment including watershed, forests and wildlife;”

All the above activities will be treated as charitable activities and are unconditionally exempted from GST. Hence other services provided by charitable trusts which do not fall within the definition of charitable activities, would become taxable, unless exempted otherwise.

E.g. If a trust organizes a yoga camp and collect entry fees or charges, it would be treated as a commercial activity (as it is different from the advancement of religion, spirituality or yoga). Consequently it will get out from charitable activities exemption and hence liable to GST.

7. S no 13 provides exemptions relating to religious ceremony and renting of religious precincts. It reads as under:

“(13) Services by a person by way of-

(a) conduct of any religious ceremony;

(b) renting of precincts of a religious place meant for general public, owned or managed by an entity registered as a charitable or religious trust under section 12AA of the Income-tax Act, 1961 (hereinafter referred to as the Income-tax Act) or a trust or an institution registered under sub clause (v) of clause (23C) of section 10 of the Income-tax Act or a body or an authority covered under clause (23BBA) of section 10 of the said Income-tax Act:

Provided that nothing contained in entry (b) of this exemption shall apply to,-

(i) renting of rooms where charges are one thousand rupees or more per day;

(ii) renting of premises, community halls, kalyanmandapam or open area, and the like where charges are ten thousand rupees or more per day;

(iii) renting of shops or other spaces for business or commerce where charges are ten thousand rupees or more per month.”

It should be kept in mind that the services of conduct of religious ceremonies are exempt and not the services which are incidental to such ceremonies. For example - A trust organizes Durgotsav or other religious functions. Also these trusts rent out the space to advertisement agencies, which they usefor installation of a d v e r t i s e m e n t h o a r d i n g s . S e a r c h advertisement cannot be treated as services with respect to religious ceremonies and hence are chargeable to GST.

The proviso to sl no 13 has been inserted for the

18

first time under GST law. Erstwhile service tax provisions provided unconditional exemption to renting of religious precincts by way of sl no 5 of notification number 25/2012 - ST dated 20.06.2012 (Mega exemption notification). If the amount charged exceeds any threshold, then GST will come into play.

The law has given limited exemption to renting of only religious precincts meant for general public by entity registered under section 12AA of Income Tax Act, 1961. As per clause (zc) of said notification the term "general public" means"the body of people at large sufficiently defined by some common quality of public or impersonal nature".

As per clause (zy) religious place means "a place which is primarily meant for conduct of prayers or worship pertaining to a religion, meditation, or spirituality."

Precincts have not been defined in the notification and the dictionary meaning of precincts from the Oxford dictionary is "the area within the walls or perceived boundaries of a particular building or place or an enclosed or clearly defined area of ground around a Cathedral Church or college."

Therefore if the renting of area does not fall under the category of religious precincts the exemption cannot be resorted.

8. Sl no 80 of the said notification reads as under:

“(80) Services by way of training or coaching in recreational activities relating to-(a) arts or culture, or (b) sports by charitable entities registered under section 12AA of the Income-tax Act."

Therefor the services of training or coaching in recreational activities relating to art, culture or sports by the charitable trusts are exempt from GST.

9. Secondly some general exemptions are also there, which can be availed by any person including charitable trusts. We can say that such exemptions are activity based rather than person based. The general exemptions provided by Notification No. 12/2017 – Central Tax (Rate), dated 28.6.2017 are as follows:

10. Sl no. 12 provides as under:

“(12) Services by way of renting of residential dwelling for use as residence."

There are many Charitable Trusts which rent out their residential dwelling for residential purpose. They can avail the benefit of sl no 12 and such renting gets out of the purview of GST.

11. Sl no 46 provides as under:

“(46) Services by a veterinary clinic in relation to health care of animals or birds."

Some charitable trusts are involved in serving as a veterinary clinic in relation to health care of animals and birds, exemption by way of serial number 46 can be availed.

12. Sl no 50 reads as under:

“(50) Services of public libraries by way of lending of books, publications or any other knowledge-enhancing content or material."

If the trusts serve as a public library and lend books, publications etc then exemption can be availed.Here the word 'public' is important. The

19

exemption makes it clear that it is not available to private library and hence if the library is open only for the registered members (that is not open to all), the exemption cannot be resorted.

13. Sl no 54 reads as under:

“(54) Services relating to cultivation of plants and rearing of all life forms of animals, except the rearing of horses, for food, fibre, fuel, raw material or other similar products or agricultural produce by way of—

(a) agricultural operations directly related to production of any agricultural produce including cultivation, harvesting, threshing, plant protection or testing;

(b) supply of farm labour;

(c) processes carried out at an agricultural farm including tending, pruning, cutting, harvesting, drying, cleaning, trimming, sun drying, fumigating, curing, sorting, grading, cooling or bulk packaging and such like operations which do not alter the essential characteristics of agricultural produce but make it only marketable for the primary market;

(d) renting or leasing of agro machinery or vacant land with or without a structure incidental to its use;

(e) loading, unloading, packing, storage or warehousing of agricultural produce;

(f) agricultural extension services;

(g) services by any Agricultural Produce Marketing Committee or Board or services provided by a commission agent for sale or purchase of agricultural produce."

A lot many trusts are involved in agriculture, renting of agricultural land and other agriculture extension services. Let us take an example to get a better understanding of this exemption. E.g. A trust is involved in providing farm labour, renting of agro machinery, storage or warehousing of agricultural produce and other agricultural extension services to its member as well as outside farmers. By way of sl no 54 all the agriculture related services provided by the charitable trusts are exempt from GST.

14. Sl no 66 provide education related exemptions and reads as under:

"(66) Services provided -

(a) by an educational institution to its students, faculty and staff;

(b) to an educational institution, by way of,-

(i) transportation of students, faculty and staff;

(ii) catering, including any mid-day meals scheme sponsored by the Central Government, State Government or Union territory;

(iii) security or cleaning or housekeeping services performed in such educational institution;

(iv) services relating to admission to, or conduct of examination by, such institution, upto higher secondary:

Provided that nothing contained in entry (b) shall apply to an educational institution other than an institution providing services by way of pre-school education and education up to higher secondary school or equivalent.

20

The term educational institution has been defined under clause (y) of the said notification which reads as under:“(y) educational institution means an institution providing services by way of – (i) pre-school education and education up to higher secondary school or equivalent;

(ii) education as a part of a curriculum for obtaining a qualification recognised by any law for the time being in force;

(iii) education as a part of an approved vocational education course.”

The educational services with respect to

(A) abandoned, orphaned or homeless children;(B) physically or mentally abused and traumatized persons;

(C) prisoners; or(D) persons over the age of 65 years residing in a rural area;

are covered under the definition of charitable activities and are hence exempt by way of sl no (1). But other educational services which does not fall under charitable activities like:

(i) pre-school education and education up to higher secondary school or equivalent;

(ii) education as a part of a curriculum for obtaining a qualification recognised by any law for the time being in force;

(iii) education as a part of an approved vocational education course;

carried out by search trusts has been provided

exemption by way of this entry.

15. Sl no 74 provides exemption in relation to health care services and reads as under:

"(74) Services by way of-

(a) health care services by a clinical establishment, an authorised medical practitioner or para-medics;

(b) services provided by way of transportation of a patient in an ambulance, other than those specified in (a) above.

Many Charitable Trust are running hospital and providing health care services. Activities relating to public health of:

(I) terminally ill persons or persons with severe physical or mental disability;

(II) persons afflicted with HIV or AIDS;

(III) persons addicted to a dependence-forming substance such as narcotics drugs or alcohol; orcreating public awareness of preventive health, family planning or prevention of HIV infection; are already exempted being charitable activities.

But provision of other Healthcare services like treatment of cancer, ambulance services etc. to any person, who are not covered by the definition of charitable activities, by such charitable trusts are out of GST by way of sl no 74.

Healthcare services have been defined in clause (zg) of said notification which reads as under:

"(zg) health care services means any service by

21

way of diagnosis or treatment or care for illness, injury, deformity, abnormality or pregnancy in any recognised system of medicines in India and includes services by way of transportation of the patient to and from a clinical establishment, but does not include hair transplant or cosmetic or plastic surgery, except when undertaken to restore or to reconstruct anatomy or functions of body affected due to congenital defects, developmental abnormalities, injury or trauma;"Therefore if the cosmetic or plastic surgery is carried out simply to enhance the beauty of patient, (not required to reconstruct anatomy of functions of body affected due to congenital defects etc.), the benefit of exemption will not be available.

16. Summary: There are no specific exemptions available for supply of goods by charitable trusts. If the supply of goods is

otherwise exempt then only such trusts are not required to pay Goods and Services Tax. For example – Supply of unbranded agricultural produce have been exempted by way of specifying nil rates against their HSN codes. For example supply of “Rice [other than those put up in unit container and bearing a registered brand name]”and “Buckwheat, millet and canary seed; other cereals such as Jawar, Bajra, Ragi] [other than those put up in unit container and bearing a registered brand name]” bearing 1006 and 1008 as their chapter headings respectively, have nil rate of tax.

The goods or services provided by charitable trusts are covered by provisions of GST. If those goods or services are not specifically exempted under GST laws, the trust have to pay GST at appropriate rates.

(a) Life Member: A single payment of Rs. 2500/- shall make a person eligible to be admitted as a life member of the fund. Thereafter he shall not be liable to pay any amount on account of subscription and shall be styled as a 'Life Member'.

(b) Ordinary members: All other members shall be described as 'Ordinary Members' and shall have to pay an annual subscription of Rs. 500/-.

Apart from this any member can subscribe for 'Voluntary Contribution'.

Procedure for making payment

Membership subscription to the Chartered Accountants Benevolent Fund can be paid along with annual membership fee. Alternatively it can be paid separately by local cheque/DD to the respective Decentralised offices or Regional offices or Head office.

Members are requested to contribute to the CA Benevolent fund.

The objective for which the fund is established is to provide financial assistance for maintenance, education or any other similar purpose to necessitous persons being:-

(a) persons who are or have been members of the Institute, whether subscribers to the fund or not; or

(b) wives and children of persons who are or have been members of the Institute, whether subscribers to the fund or not.

(c) widows and children of deceased persons who have been members of the Institute whether subscribers to the fund or not.

(d) relatives or others who were dependent for support on a person who has been a member of the Institute, whether subscriber to the fund or not; and who has died without leaving a widow or child.

Procedure for becoming a member of

40

PHOTO GALLERIES

41

L-R: CA. Manoj Kr. Sharma- Guest speaker, Sanjay Sharma - CICASA Chairman, Mukesh Bansal- Secretary CIRC, CA. Atul Agrawal- Chairman Noida branch, CA. Deep Kumar Misra- Chairman CIRC, CA. Parveen Singhal- Vice Chairman Noida branch, CA. Girish Kumar

Narang- Branch committee member during 10 days certificate course on GST hosted by Noida branch and organised by Indirect Tax Committee- ICAI from 3rd to 24th June 2017

CA. CA.

On the podium - Mukesh Bansal Secretary CIRC, Tanuj Kr. Garg- Secretary Noida branch, Atul Agrawal- Chairman Noida branch, CA. Ravi Kumar Guest Speaker during 10 Days Certificate Course On Gst Hosted by Noida Branch and organised by Indirect Tax Committee-

ICAI from 3rd To 24th June 2017

CA. CA. CA.

42

L-R: CA. Prakash Chand Sharma- CICASA Chairman, CA. Vineesh Arora- Secretary Bareilly Branch, CA. Pawan Agarwal- Chairman Bareilly Branch, CA. Rajen Vidhyarthi- Past Chairman Bareilly Branch, CA. Mukesh Bansal - Secretary CIRC, CA. Manoj Fadnis- Past President ICAI, CA. Vishal Goel -

Past Chairman Bareilly Branch, CA. Pankaj G. Shah, CA. Sharad Mishra- Past Chairman Bareilly Branch, CA. Ravindra Agarwal- Past Chairman Bareilly Branch, CA. Annurugh Goel- Past Chairman Bareilly Branchduring full day seminar on ICDS & Benami Prohibition Law on 22.06.2017

by Bareilly branch jointly with CIRC.organised

On the podium- L-R: CA. Vineesh Arora- Secretary Bareilly Branch, CA. Pawan Agarwal- Chairman Bareilly Branch,

CA. Manoj Fadnis- Past President ICAI, Session Chairman & CA. Pankaj G. Shah

CA. Mukesh Bansal - Secretary CIRC addressing full day seminar on ICDS & Benami Prohibition Law on 22.06.2017 organised by Bareilly branch jointly with CIRC. Sitting

43

Disclaimer : The views and opinions expressed or implied in this e-Newsetter are those of the authors and do not necessarily reflect those of CIRC of ICAIAddress : CIRC of ICAI, ICAI BHAWAN, 16/77 B, Civil Lines, Kanpur-208001Phones : (0512) 3011151*3011153*3011182EPABX : (0512) 3989398. Fax: (0512) 3011193* E-mail : [email protected]* Website: www.circ-icai.org