62

Century Banking Corporation Ltd Denominated in Mauritian Rupees Directors' Report and Financial Statements Year ended December 31, 2011

Century Banking Corporation Ltd

Denominated in Mauritian Rupees

Directors' Report and Financial Statements

Year ended December 31, 2011

1

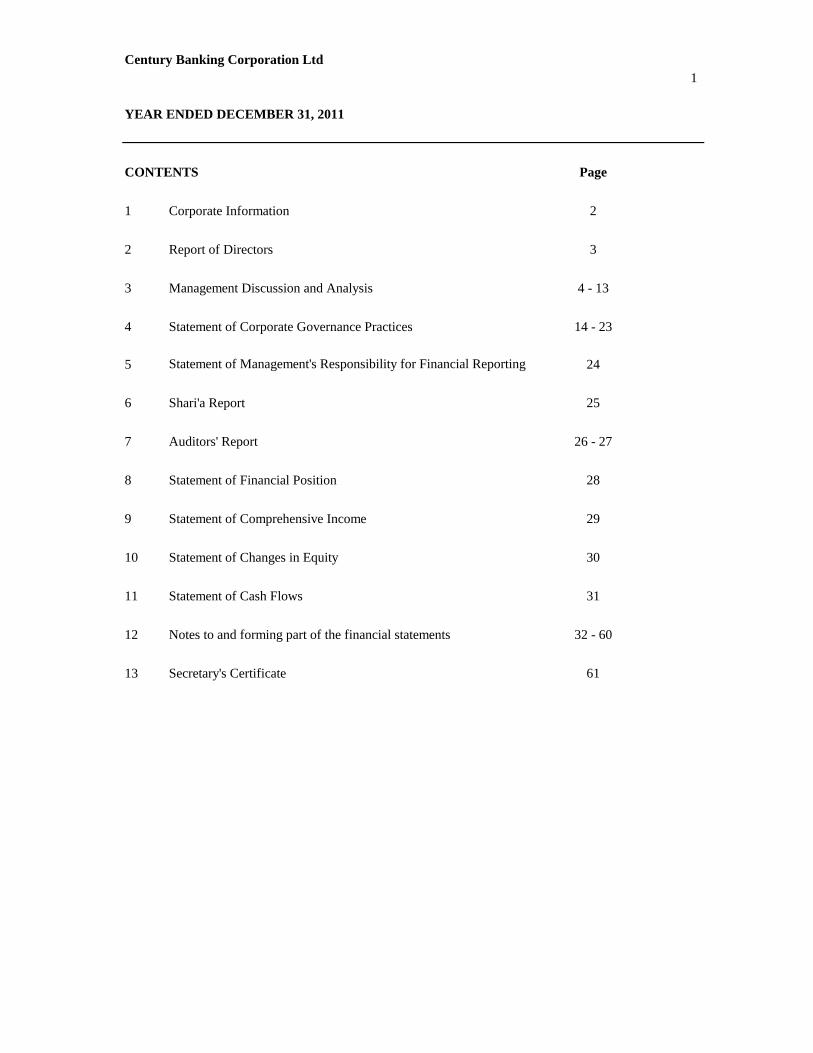

CONTENTS Page

1 Corporate Information 2

2 Report of Directors 3

3 Management Discussion and Analysis 4 - 13

4 Statement of Corporate Governance Practices 14 - 23

5 24

6 Shari'a Report 25

7 Auditors' Report 26 - 27

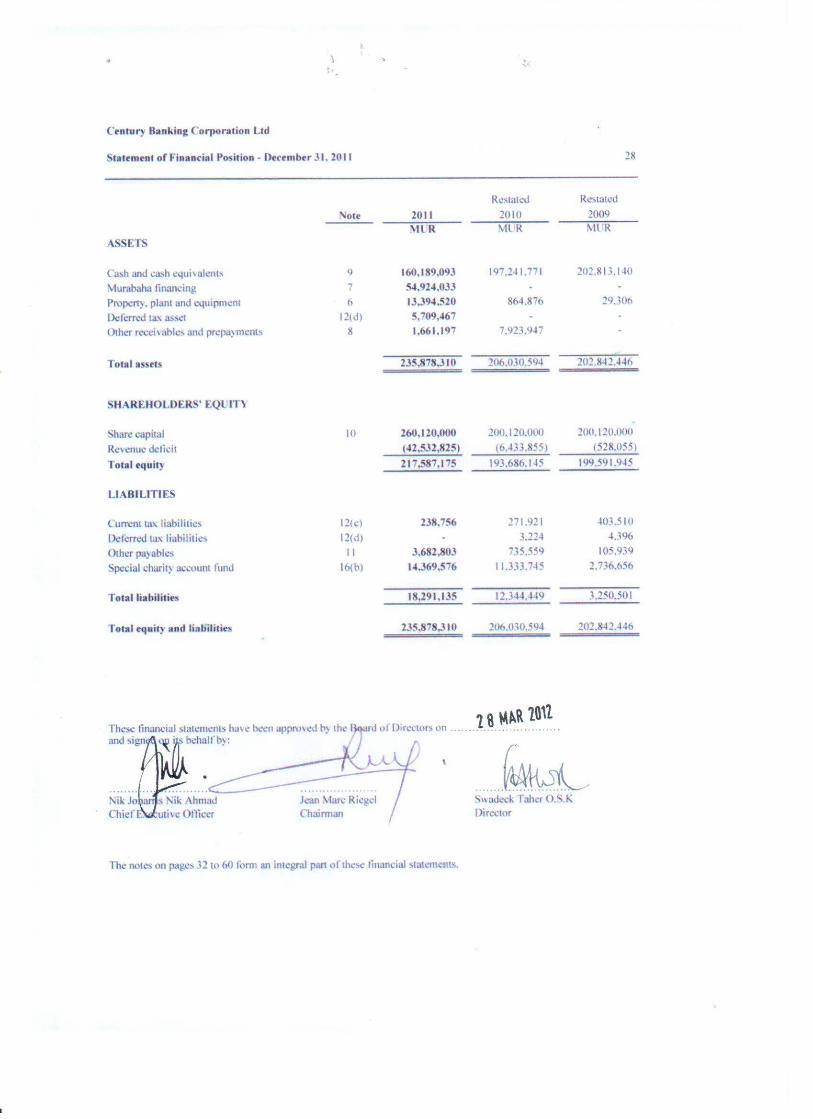

8 Statement of Financial Position 28

9 Statement of Comprehensive Income 29

10 Statement of Changes in Equity 30

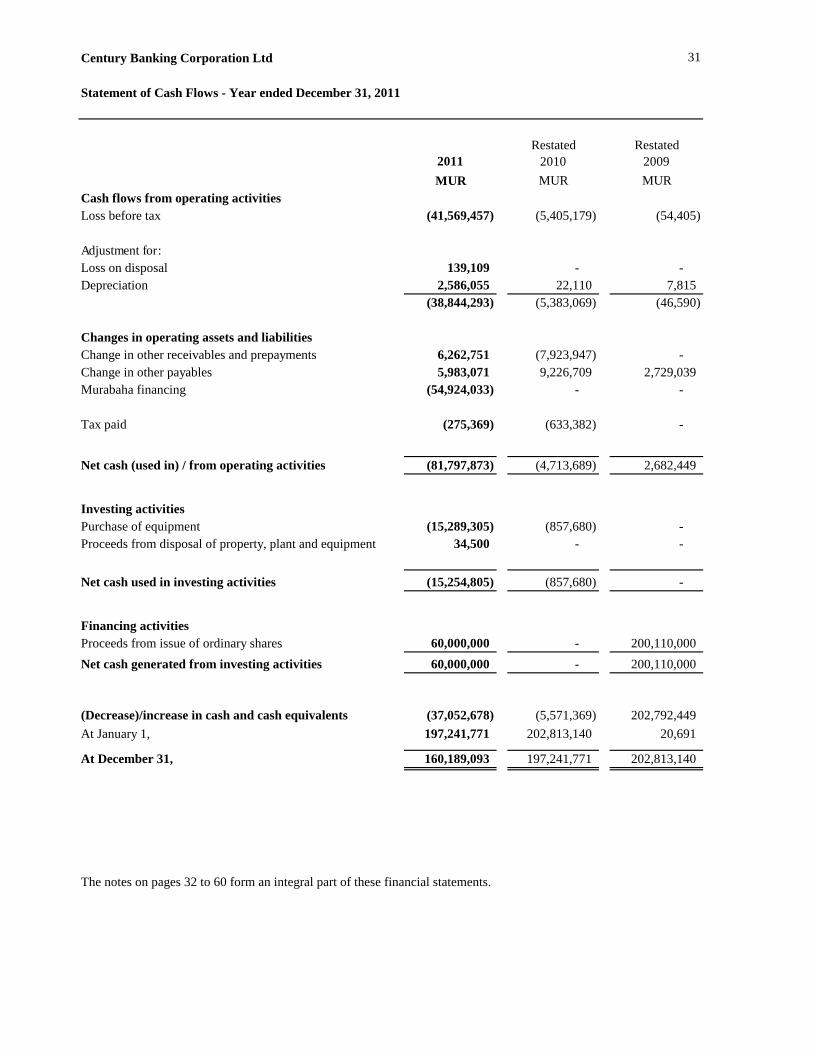

11 Statement of Cash Flows 31

12 Notes to and forming part of the financial statements 32 - 60

13 Secretary's Certificate 61

Century Banking Corporation Ltd

YEAR ENDED DECEMBER 31, 2011

Statement of Management's Responsibility for Financial Reporting

Year ended December 31, 2011 2

Corporate Information

Chief Executive Officer: Nik Joharris Nik Ahmad

Directors: Jean Marc A. RiegelMohamed G.M.H. ZeineldinIsa M.I. HabibE.M. Swadeck Taher O.S.KSaleem R. Beebeejaun

Secretary: BA Corporate Services Ltd25 Pope Hennessy StreetPort-Louis

Business Address: Century Banking Corporation LtdSuite 405, 4th Floor,Barkly Wharf,Caudan Waterfront, Port-Louis,Mauritius

Registered Office: 25, Pope Hennessy Street,Port Louis

Legal Advisor : Imteaz BundhooSuite 405, 4th Floor,Barkly Wharf,Caudan Waterfront, Port-Louis,Mauritius

Bankers: Bramer Banking Corporation Ltd26 Pope Hennessy StreetPort-Louis

Auditors: KPMGKPMG Centre31 CyberCityEbène

Shari'a Advisor Bait Al-Mashura Finance ConsultationsFirst Finance Company Building,C-Ring Road (Facing Labor Department),P.O Box 23471,Doha, Qatar

Century Banking Corporation Ltd

4

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis The management of Century Banking Corporation Ltd (the “Bank”) is pleased to present its Management Discussion and Analysis, in accordance with the Bank of Mauritius Guideline on Public Disclosure of Information. The Bank started its operation on 31 March 2011. For the financial year 2011, the main focus of the management was to put together the required resources, chart the direction of the Bank together with the Board of Directors (“Board”) and firm up the Bank’s operation. This report covers the first nine-months of the Bank’s operations, from 31 March 2011 up to 31 December 2011. The strategy of the Bank for the first few years of its operation is to develop sustainable income, establish retail banking business and focus on asset management and investment banking services to generate fee-based income. 1. Financial Review

For the period under review, the Bank has recorded a pre-tax loss of MUR 41.6 million. This is expected as the Bank is at its early development stage. The Bank generated fees and profits of MUR 1.2 million from Shari’a compliant financing transactions extended to two (2) corporate bodies in Mauritius during the fourth quarter of 2011, totalling to MUR 56.0 million, on the back of its total operating expenses of MUR 42.8 million.

Being the first Islamic bank in Mauritius, it is comprehensible that the Bank would take time to launch any Islamic banking concepts/products in the market. Nevertheless, in addition to the above mentioned corporate financing transactions closed in 2011, the Bank managed to introduce a Shari’a compliant short term liquidity instrument in Mauritius in January 2012, which paved the way for the Bank to generate returns on its cash balances in Mauritian Rupee.

5

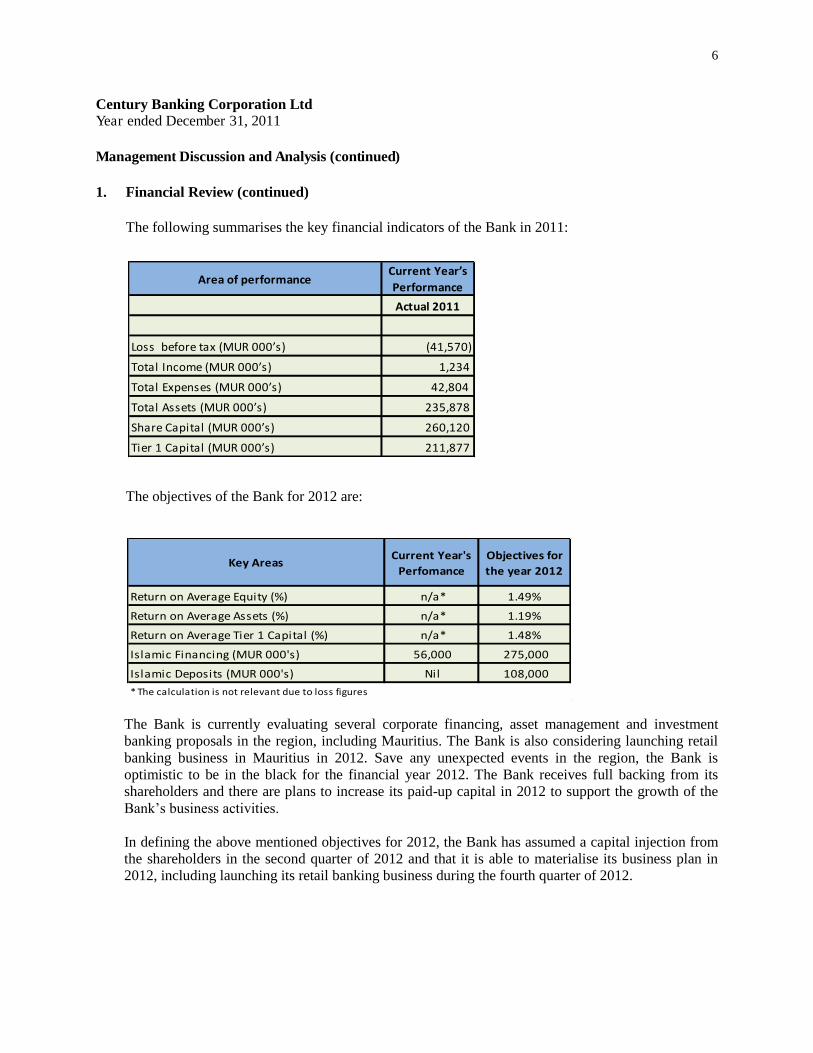

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 1. Financial Review (continued)

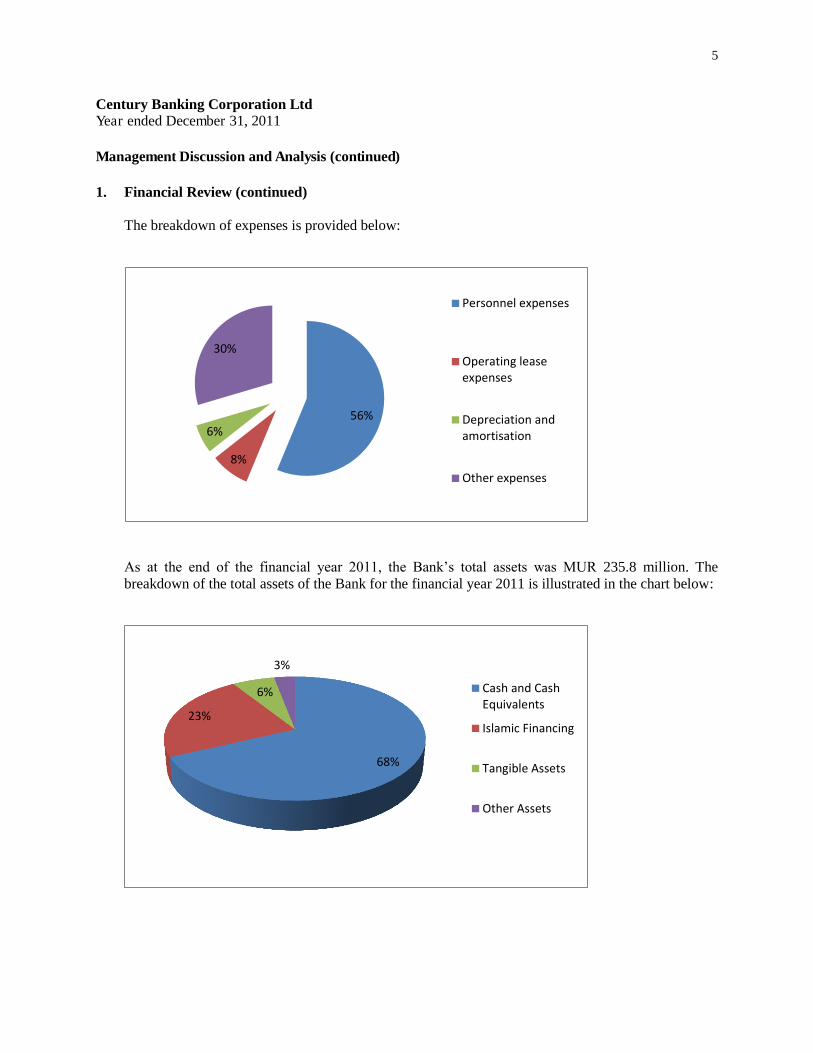

The breakdown of expenses is provided below:

As at the end of the financial year 2011, the Bank’s total assets was MUR 235.8 million. The breakdown of the total assets of the Bank for the financial year 2011 is illustrated in the chart below:

56%

8%

6%

30%

Personnel expenses

Operating lease

expenses

Depreciation and

amortisation

Other expenses

68%

23%

6%

3%

Cash and Cash

Equivalents

Islamic Financing

Tangible Assets

Other Assets

6

Key AreasCurrent Year's

Perfomance

Objectives for

the year 2012

Return on Average Equity (%) n/a* 1.49%

Return on Average Assets (%) n/a* 1.19%

Return on Average Tier 1 Capital (%) n/a* 1.48%

Islamic Financing (MUR 000's) 56,000 275,000

Islamic Deposits (MUR 000's) Nil 108,000

* The calculation is not relevant due to loss figures

Area of performanceCurrent Year’s Performance

Actual 2011

Loss Hefore tax ふMUR ヰヰヰ’sぶ (41,570)

Total IミIoマe ふMUR ヰヰヰ’sぶ 1,234

Total Expeミses ふMUR ヰヰヰ’sぶ 42,804

Total Assets ふMUR ヰヰヰ’sぶ 235,878

Share Capital ふMUR ヰヰヰ’sぶ 260,120

Tier ヱ Capital ふMUR ヰヰヰ’sぶ 211,877

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 1. Financial Review (continued)

The following summarises the key financial indicators of the Bank in 2011:

The objectives of the Bank for 2012 are:

The Bank is currently evaluating several corporate financing, asset management and investment banking proposals in the region, including Mauritius. The Bank is also considering launching retail banking business in Mauritius in 2012. Save any unexpected events in the region, the Bank is optimistic to be in the black for the financial year 2012. The Bank receives full backing from its shareholders and there are plans to increase its paid-up capital in 2012 to support the growth of the Bank’s business activities.

In defining the above mentioned objectives for 2012, the Bank has assumed a capital injection from the shareholders in the second quarter of 2012 and that it is able to materialise its business plan in 2012, including launching its retail banking business during the fourth quarter of 2012.

7

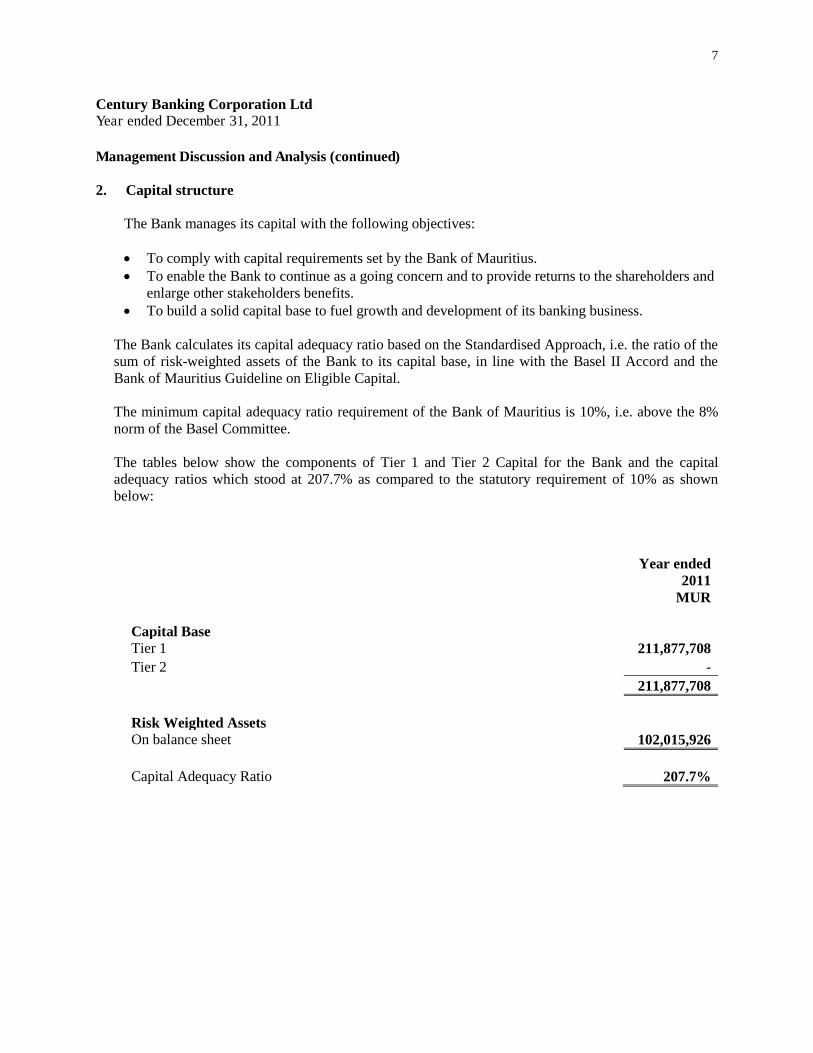

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 2. Capital structure

The Bank manages its capital with the following objectives: To comply with capital requirements set by the Bank of Mauritius. To enable the Bank to continue as a going concern and to provide returns to the shareholders and

enlarge other stakeholders benefits. To build a solid capital base to fuel growth and development of its banking business.

The Bank calculates its capital adequacy ratio based on the Standardised Approach, i.e. the ratio of the sum of risk-weighted assets of the Bank to its capital base, in line with the Basel II Accord and the Bank of Mauritius Guideline on Eligible Capital. The minimum capital adequacy ratio requirement of the Bank of Mauritius is 10%, i.e. above the 8% norm of the Basel Committee. The tables below show the components of Tier 1 and Tier 2 Capital for the Bank and the capital adequacy ratios which stood at 207.7% as compared to the statutory requirement of 10% as shown below:

Year ended

2011

MUR

Capital Base Tier 1

211,877,708 Tier 2

-

211,877,708

Risk Weighted Assets On balance sheet

102,015,926

Capital Adequacy Ratio

207.7%

8

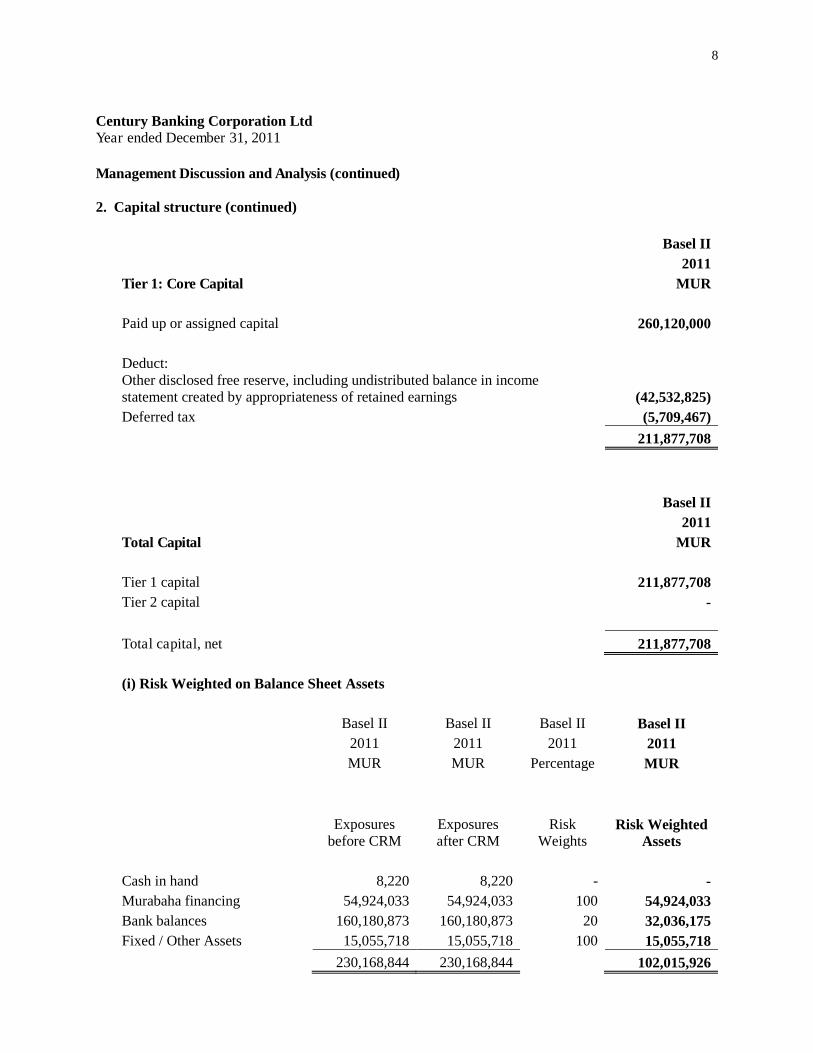

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 2. Capital structure (continued)

Basel II

2011

Tier 1: Core Capital

MUR

Paid up or assigned capital

260,120,000

Deduct: Other disclosed free reserve, including undistributed balance in income

statement created by appropriateness of retained earnings

(42,532,825) Deferred tax

(5,709,467)

211,877,708

Basel II

2011

Total Capital

MUR

Tier 1 capital

211,877,708 Tier 2 capital

-

Total capital, net

211,877,708

(i) Risk Weighted on Balance Sheet Assets

Basel II Basel II Basel II Basel II

2011 2011 2011 2011

MUR MUR Percentage MUR

Exposures before CRM

Exposures after CRM

Risk Weights

Risk Weighted Assets

Cash in hand

8,220 8,220 - - Murabaha financing

54,924,033 54,924,033 100 54,924,033

Bank balances

160,180,873 160,180,873 20 32,036,175 Fixed / Other Assets

15,055,718 15,055,718 100 15,055,718

230,168,844 230,168,844

102,015,926

9

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued)

3. Risk Management Policies and Controls

Despite at the early stage of its establishment, the Bank has built a risk management framework to define the principal risks assumed in conducting its business activities. The management team is responsible to develop the Bank’s risk management framework under the purview of the Conduct Review and Risk Management Committee. The effectiveness of this framework is enhanced by participation of the Board in approving all risk management policies. Credit risk is created through financing and, participation in asset management and investment banking products, where the Bank is exposed to repayment risks. There are two (2) levels of approving authorities for any of the above mentioned activities, namely the Investment and Product Development Committee and Board. Each approving authority has been delegated a specific approving limit depending on the amount of financing or participation as a percentage to the Bank’s Core Capital. The terms of reference of the Investment and Product Development Committee were reviewed by the Conduct Review and Risk Management Committee and approved by the Board, and they are subject to revision in line with the growth of the Bank and changes in the market conditions.

Any risk undertaken by the Bank is monitored through periodic reporting by the management to the Conduct Review and Risk Management Committee, which thereafter reports to the Board. Additionally, Internal Audit would independently monitor the effectiveness of risk management policies and has direct reporting to the Audit Committee. Outstanding financing as at 31 December 2011 was as follows: Automobile: MUR 39.5 million Education: MUR 15.4 million The Bank is in compliance with all the guidelines issued by the Bank of Mauritius relating to risk exposures. Market risk The Bank is subject to movement in Bank of Mauritius’ Key Repo Rate if it uses the Key Repo Rate as the benchmark to raise funding or provide financing to its clients. However, for the financial year 2011, the Bank was operating solely on its capital and financing was provided at fixed profit rates. In the future, it is possible that there is a risk of an adverse effect on the profit margins of the Bank in the event of major changes in Key Repo Rate, if the Bank uses the Key Repo Rate as its benchmark to raise funding and/or for financing purposes. As far as foreign currency risk is concerned, for the financial year 2011, there was very minor foreign currency risk for the Bank as its capital and lending activities were entirely in Mauritian Rupee. The Bank kept a small amount of its cash in foreign currency in 2011 but this was very minimal, i.e less than 1% of the Bank’s Core Capital. In the future, the Bank may be affected by movements in foreign exchange rates if it starts raising funds or providing financing in foreign currencies.

10

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 3. Risk Management Policies and Controls (continued)

Liquidity risk The Asset and Liability Committee provides management with an oversight of liquidity risk and meets on a monthly basis to review the Bank’s liquidity profile. It measures and forecasts cash inflows and outflows, manages the Bank’s diversification of funding sources (when necessary) and ensures the Bank maintains sufficient liquidity to support its payment obligations.

Operational risk The Bank operates within a defined and approved organisation structure, and has established policies and procedures and reporting structure for its operations. The Bank’s operation does not currently require heavy staffing and systems infrastructure to support its activities. The asset and liabilities management, authority matrix and human resources policies currently control the minimal operational risk inherent in the Bank. Related Party Transactions The Bank provides regular services to its related parties in the ordinary course of business. These services are on terms similar to those offered to non-related parties. The Investment and Product Development Committee is responsible in assessing transactions with related parties that may materially affect the Bank and ensuring compliance with the Banking Act and Guidelines from the Bank of Mauritius on related party transactions. The Bank has granted financing facility to a related party for an amount of MUR 40.0 million, representing 18% of the Bank’s Core Capital. No related party exposure is non-performing. Internal audit The internal audit function has been outsourced to an external service provider in March 2012 and it reports directly to the Audit Committee. Internal Auditor performs an independent appraisal of the Bank’s compliance with internal control systems, accounting practices, information systems, providing assurance regarding the Bank’s corporate governance, control systems, and risk management processes. A summarised implementation status of all issues of the internal audit report will be communicated to the management and Audit Committee on a quarterly basis. Compliance The Bank is committed to the highest standards of business integrity, transparency and professionalism in its activities. The purpose of compliance function is to ensure that all business transactions and activities comply with appropriate laws, regulations, policies, guidelines and ethical standards.

11

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 3. Risk Management Policies and Controls (continued)

The compliance function operates as per good corporate governance practices. This unit is fully operational and attends regularly all the Compliance Committees organised for the banking industry.

12

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 4. Forward-looking statements

The Bank’s public communications may include oral or written forward-looking statements. Statements of this type are included in this document, and may be included in other filings or in other communications. Forward-looking statements may include comments with respect to the Bank’s objectives, strategies to achieve those objectives, expected financial results (including those in the area of risk management) and the outlook for the Bank’s businesses. By their very nature, forward-looking statements involve numerous assumptions, inherent risks and uncertainties, both general and specific, and there is a risk that predictions and other forward-looking statements will not prove to be accurate. Readers of these forward-looking statements are requested not to unduly rely on them as a number of important factors, many of which are beyond the Bank’s control, could cause actual results to differ materially from the estimates and intentions expressed in such forward-looking statements. These factors include, but are not limited to, the following: Economic and financial conditions in Mauritius and globally; Fluctuations in currency values; Effect of changes in monetary policy; Legislative and regulatory developments in Mauritius and elsewhere, including changes in tax

laws; Accuracy and completeness of information the Bank receives on customers and counterparties; The Bank’s ability to expand existing distribution channels and to develop and realize revenues from new distribution channels; Changes in accounting policies and methods the Bank uses to report its financial condition and the results of its operations, including uncertainties associated with critical accounting assumptions and estimates; The effect of applying future accounting changes; The Bank’s ability to attract and retain key executives; Unexpected changes in consumer spending and saving habits; Technological developments; Fraud by internal or external parties, including the use of new technologies in unprecedented ways to defraud the Bank or its customers; Competition, both from new entrants and established competitors; Judicial and regulatory proceedings; Acts of God;

13

Century Banking Corporation Ltd Year ended December 31, 2011 Management Discussion and Analysis (continued) 4. Forward-looking statements (continued) The possible impact of international conflicts and other developments, including terrorist acts and

war on terrorism; The effects of disease or illness on local, national or international economies; Disruptions to public infrastructure, including transportation, communication, power and water; and The Bank’s anticipation of and success in managing the risks implied by the foregoing.

A substantial amount of the Bank’s business involves financing or otherwise committing resources to specific companies, industries or countries. Unforeseen events affecting such borrowers, industries or countries could have a material adverse effect on the Bank’s financial results, businesses, financial condition or liquidity. These and other factors may cause the Bank’s actual performance to differ materially from that contemplated by forward-looking statements. The preceding list of important factors is not exhaustive. When relying on forward-looking statements to make decisions with respect to the Bank, investors and others should carefully consider the preceding factors, other uncertainties and potential events. The Bank does not undertake to update any forward looking statements, whether written or oral, that may be made from time to time by itself or on its behalf.

14

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices 1. Shareholding Structure

The shareholding structure of the Century Banking Corporation Ltd (the “Bank”) as at 31 December 2011 was as follows:- Domasol Limited 60% British American Investment Co. (Mtius) Ltd 40% The parent company is Domasol Limited, a company incorporated in Malta.

2. The Board of Directors

Company law requires the Board to prepare financial statements for each financial year which indicates fairly the financial position, financial performance, changes in equity and cash flows of the Bank. In preparing those financial statements, the Board is required to: select suitable accounting policies and apply them consistently; make judgements and estimates that are reasonable and prudent; state whether International Financial Reporting Standards have been followed, subject to any

material departures disclosed and explained in the financial statements; and prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Bank will continue in business.

The Board confirms that the above requirements in preparing the financial statements have been complied with. The directors of the Bank are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financial position of the Bank and to enable them to ensure that the financial statements comply with the Banking Act 2004 and the Companies Act 2001 applicable to banks. They are also responsible for safeguarding the assets of the Bank and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities. The Board of Directors delegates the day to day running of the Bank to the Chief Executive Officer and relevant committees. The Bank believes that sound corporate governance standards and practices are vital for maintaining the confidence in the banking system and for maximizing long term value creation for the shareholders. The Board of Directors of the Bank values the importance of such sound corporate governance standards and practices and is fully committed of the Bank’s initiatives and has given full support to ensure the maintenance of highest standards of corporate governance in all aspects of the Bank’s business.

15

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 2. The Board of Directors (continued)

The Bank’s Corporate Governance framework follows the principles and best practices as laid out in the Mauritius Code of Conduct on Corporate Governance (Revised 2009), the Guidelines on Corporate Governance issued by Bank of Mauritius and, also subscribes to industry and international best practices. As at 31 December 2011, the Board comprised five (5) non-executive members of whom three (3) are independent.

Jean Marc A. Riegel - Chairman Mr. Riegel was appointed as an independent director in July 2011 and is the Chairman of the Board since November 2011. He holds an MBA from the Hautes Etudes Commerciales (HEC) Montreal Business School and a Diploma from the French Business School (Grandes Ecoles ESC Sophia Antipolis). He has more than twenty-four years of experience in the field of international banking and audit, having worked in France, Canada, Bahrain and Qatar including twelve years in Islamic banking. He is currently working as the Chief Investment Officer for one of the largest group in Qatar. Mohamed G.M.H. Zeineldin Mr. Zeineldin is an independent director of the Bank and was appointed in December 2009. He holds a professional qualification in engineering from the Cairo University. He is also the Chief Executive Officer of A’Ayan Holding Group based in Cairo. Isa M.I. Habib Mr. Habib was appointed as independent director on the Board of the Bank in March 2011. He has extensive experience in banking, treasury and asset management having worked in Kuwait and Qatar. He also holds several directorships in Bahrain, Kuwait and Qatar and currently works as a financial advisor. Saleem R. Beebeejaun Mr. Beebeejaun was appointed as the non-executive director on the Board of the Bank in May 2008. He is a fellow of the Chartered Institute of Insurance. He was President of the Insurers` Association from 2003 to 2005. He also acts as the Honorary Consul of Malaysia in Mauritius. E.M. Swadeck Taher O.S.K. Mr. Taher O.S.K. was appointed as the non-executive director on the Board of the Bank in November 2009. He is a fellow of both the Institute of Chartered Accountants of England and Wales and Association of Chartered Certified Accountants of UK. He is currently the President and Chief Executive Officer of Bramer Corporation. He was recipient of the prestigious ACCA Achievement Award in 2007.

16

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 2. The Board of Directors (continued)

The following directors held office during the year:

Directors Appointment date Resignation date Hesham A.S.M. Shokry December 17, 2009 October 23, 2011

Mohammed H.M.H. Al -Hamadi December 17, 2009 August 3, 2011

Izzat N. Nuseibeh March 30, 2011 November 21, 2011

The Board has not yet appointed any executive director and will consider such appointment in line with the Code of Corporate Governance.

3. Secretary

B A Corporate Services Ltd acts as secretary to the Board. 4. Directors’ Ethics

The Directors act with utmost good faith towards the Bank in any transaction and, act honestly and responsibly in the exercise of their powers in discharging their duties.

5. Statement of Remuneration Policy

Executive remuneration packages are prudently designed to attract, motivate and retain executive management and senior management of high calibre to maintain the Bank’s position in the market. It is also designed to reward them for enhancing the Bank’s performance. The review of their performance and the determination of their annual remuneration packages are considered and approved by the Corporate Governance, Nominations and Remuneration Committee.

6. Directors’ Emoluments

Remuneration and benefits of directors and key management personnel paid during the financial year are as follows:-

2011 2010 2009 MUR MUR MUR Emoluments: Key management personnel 17,435,084 269,000 -

========= ======== ========

Note: Directors were not granted any fixed remuneration or benefits. The Bank only covered the travelling and lodging expenses incurred by the directors for meetings arranged by the Bank.

17

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 7. Fixed-term contract

The Chief Executive Officer and the heads of department have service contracts of three (3) years with the Bank.

8. Duties and Responsibilities of the Board

The Board is the ultimate decision-making body of the Bank, except with respect to matters reserved for the shareholders. It acts as an advisor to the management and defines and enforces standards of accountability, all with a view to enabling the management to execute its responsibilities effectively. The Board’s principal responsibilities include: To provide clear objectives and policies within which senior executives of the Bank are to operate. To ensure that there are adequate controls and systems in place to facilitate the implementation of

the Bank’s policies. To monitor management’s effectiveness in implementing the approved strategies, plans and budget. To understand the principal risks of all aspects of the business in which the Bank is engaged in and ensure that systems are in place to effectively monitor and manage these risks with a view to the long-term viability and success of the Bank. To monitor and assess development which may affect the Bank’s strategic plans. To review the adequacy and the integrity of the Bank’s internal control systems and management information systems, including systems for compliance with applicable laws, regulations, rules, directives and guidelines. To monitor market and liquidity risks, the quality of the Bank’s exposure and changes in the Bank’s resources. To avoid conflicts of interest and ensure disclosure of possible conflicts of interest. To uphold and observe banking and relevant laws, rulings and regulations.

9. Board Committees

In discharging its duties, the Board delegates specific responsibilities to various Board Committees. These Committees operate within clearly defined terms of reference. The structure under which the Bank operates ensures effectiveness in the oversight function. Reports of the respective Committees’ meetings are presented to the Board for information and where required, for further deliberation and approval.

18

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 9. Board Committees (continued)

The Committees reporting to the Board are as follows: Audit Committee; Corporate Governance, Nominations and Remuneration Committee; and Conduct Review and Risk Management Committee. Members of Committees of the Board are exclusively Board Members. Following reconstitution of the Board, membership of the Committees is reviewed, as and when necessary. 9.1 Audit Committee

The Audit Committee comprises three (3) independent Directors, namely Mr. Isa Habib (Chairman), Mr. Jean Marc Riegel and Mr. Mohamed Zeineldin. The terms of reference of the Audit Committee are to: review the audited and unaudited periodical financial statements of the Bank before they are

approved by the Board; review, evaluate and approve policies to implement and maintain appropriate accounting, internal controls and financial disclosures;

provide oversight of the Bank’s internal and external auditors, and review and approve the audit scope and frequency; and review any transaction or conduct reported by the internal auditor, external auditor and/or officers of the Bank that could adversely affect the sound financial condition of the Bank and ensure management take adequate corrective actions in a timely manner.N

9.2 Corporate Governance, Nominations and Remuneration Committee

The Corporate Governance, Nominations and Remuneration Committee comprises three (3) non-executive Directors, namely Mr. Swadeck Taher O.S.K. (Chairman), Mr. Isa Habib and Mr. Saleem Beebeejaun.

19

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued)

9.2 Corporate Governance, Nominations and Remuneration Committee (continued)

The terms of reference of the Corporate Governance, Nominations and Remunerations Committee are to: assess and review the Bank’s general policy on corporate governance and ensure the corporate

governance report in the Bank’s annual report is in compliance with provisions of the Code of Corporate Governance in respect of required statements and disclosures; provide oversight of remuneration and compensation of directors and, all employees, and ensure that compensation is consistent with the Bank’s culture, objectives and strategy including the use of incentives, compensation plans and/or equity based remuneration plans; and

assess and review selection of prospective directors and, evaluate performance of the current directors and the effectiveness of the Board and its sub-committees.

9.3 Conduct Review and Risk Management Committee

The Conduct Review and Risk Management Committee comprises Mr. Jean Marc Riegel (Chairman), Mr. Isa Habib, Mr. Mohamed Zeineldin, Mr. Swadeck Taher O.S.K. and the Chief Executive Officer. The terms of reference of the Conduct Review and Risk Management Committee are to: review and assess the principal risks, including but not limited to credit, market, liquidity,

operational, legal and reputational risks of the Bank, and the actions taken to mitigate the risks; review and assess decisions made by the Investment and Product Development Committee and Asset and Liability Committee to ensure they are consistent with the risk appetite of the Bank and per the internal and regulatory guidelines; and

review and approve each credit exposure to related parties and ensure that market terms and conditions are applied to all related party transactions.

20

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued)

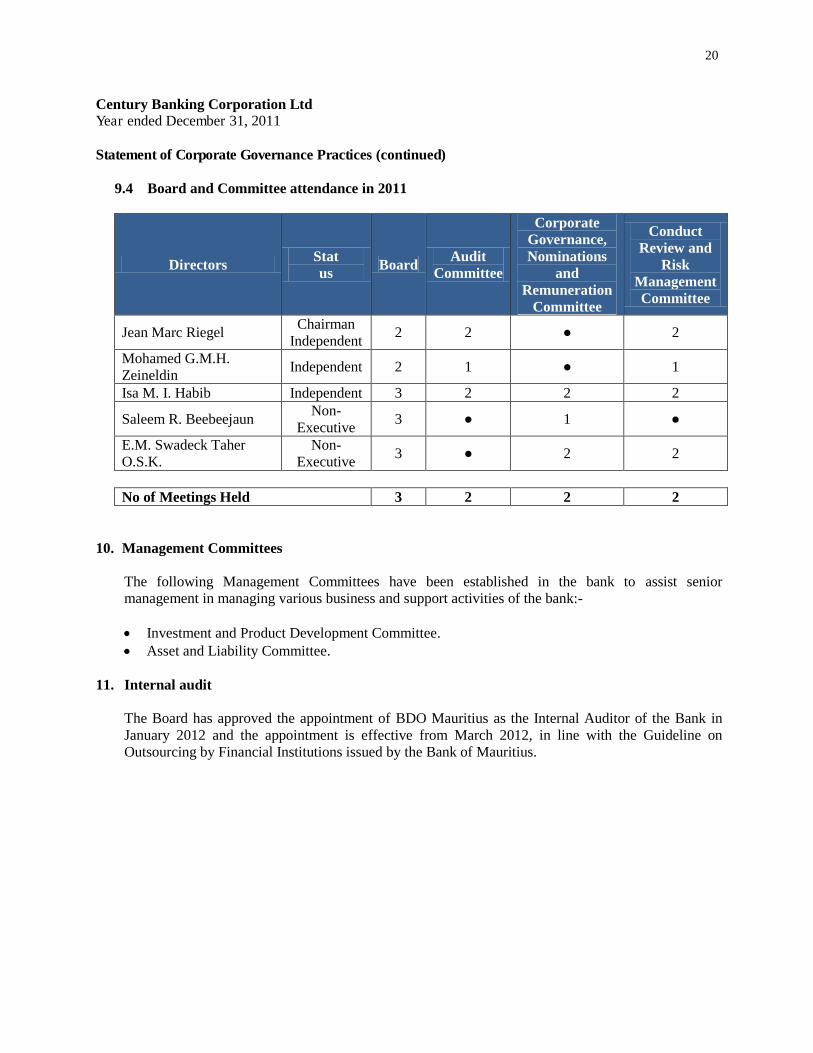

9.4 Board and Committee attendance in 2011

Directors Stat us Board Audit

Committee

Corporate Governance, Nominations

and Remuneration

Committee

Conduct Review and

Risk Management Committee

Jean Marc Riegel Chairman

Independent 2 2 ● 2

Mohamed G.M.H. Zeineldin

Independent 2 1 ● 1

Isa M. I. Habib Independent 3 2 2 2

Saleem R. Beebeejaun Non-

Executive 3 ● 1 ●

E.M. Swadeck Taher O.S.K.

Non-Executive

3 ● 2 2

No of Meetings Held 3 2 2 2

10. Management Committees

The following Management Committees have been established in the bank to assist senior management in managing various business and support activities of the bank:- Investment and Product Development Committee. Asset and Liability Committee.

11. Internal audit

The Board has approved the appointment of BDO Mauritius as the Internal Auditor of the Bank in January 2012 and the appointment is effective from March 2012, in line with the Guideline on Outsourcing by Financial Institutions issued by the Bank of Mauritius.

21

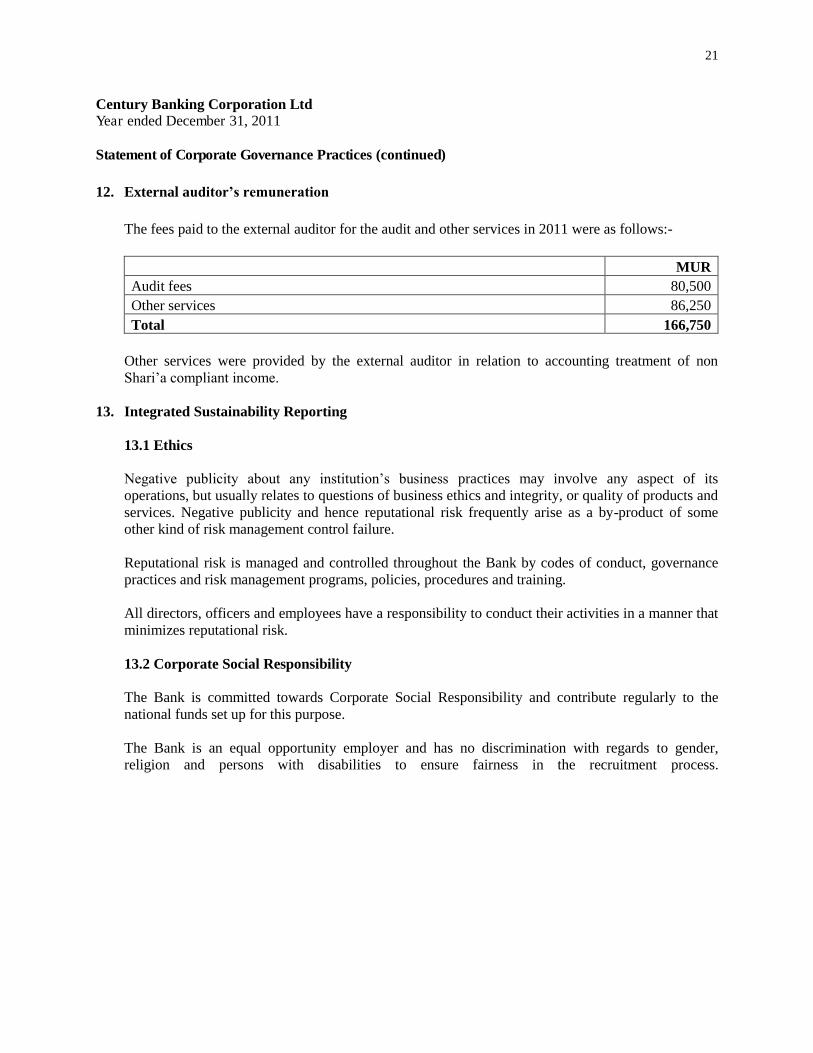

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 12. External auditor’s remuneration

The fees paid to the external auditor for the audit and other services in 2011 were as follows:-

MUR Audit fees 80,500 Other services 86,250 Total 166,750

Other services were provided by the external auditor in relation to accounting treatment of non Shari’a compliant income.

13. Integrated Sustainability Reporting

13.1 Ethics

Negative publicity about any institution’s business practices may involve any aspect of its operations, but usually relates to questions of business ethics and integrity, or quality of products and services. Negative publicity and hence reputational risk frequently arise as a by-product of some other kind of risk management control failure. Reputational risk is managed and controlled throughout the Bank by codes of conduct, governance practices and risk management programs, policies, procedures and training. All directors, officers and employees have a responsibility to conduct their activities in a manner that minimizes reputational risk. 13.2 Corporate Social Responsibility

The Bank is committed towards Corporate Social Responsibility and contribute regularly to the national funds set up for this purpose. The Bank is an equal opportunity employer and has no discrimination with regards to gender, religion and persons with disabilities to ensure fairness in the recruitment process.

22

Century Banking Corporation Ltd Year ended December 31, 2011 Statement of Corporate Governance Practices (continued) 13. Integrated Sustainability Reporting (continued)

13.3 Health and Safety

The Board of Directors is committed to strict health and safety measures in order to provide a safe place of work for its employees as well as for its customers and visitors. The offices have been renovated to meet the expectations. The Health and Safety practices comply with existing legislative and regulatory frameworks including relevant provisions of the labour laws and the Occupational Safety and Health Act.

13.4 Environment

The Bank is also committed to good environmental practices. It has started several practices to reduce electricity and paper consumption. Its tariff structure and pricing policy is adapted to favour clients with a green initiative. Environmental concerns also play a prominent role in shaping the designs of the Bank’s offices so that they minimize energy consumptions. In addition, considerable recycling and resource management programs are in place within the Bank.

14. Dividend Policy

The Bank is at the start-up phase of its operation and the dividend policy is not yet defined. The objective of the Bank for the first three (3) years of its establishment is to have the right foothold in the market and strengthen its capital base.

15. Related Party Transactions

Please refer to Note 15 of the Financial Statements for details in respect of related party transactions

16. Material Clauses of the Constitution

There are no clauses of the constitution of the Bank deemed material enough for special disclosure. 17. Important Dates in 2012

May 2012 Release of results for quarter ending 31 March 2012 June 2012 Annual Meeting of Shareholders August 2012 Release of results for quarter ending 30 June 2012 November 2012 Release of results for quarter ending 30 September 2012

29

Restated RestatedNote 2011 2010 2009

MUR MUR MUR

Operating income 1,234,254 - -

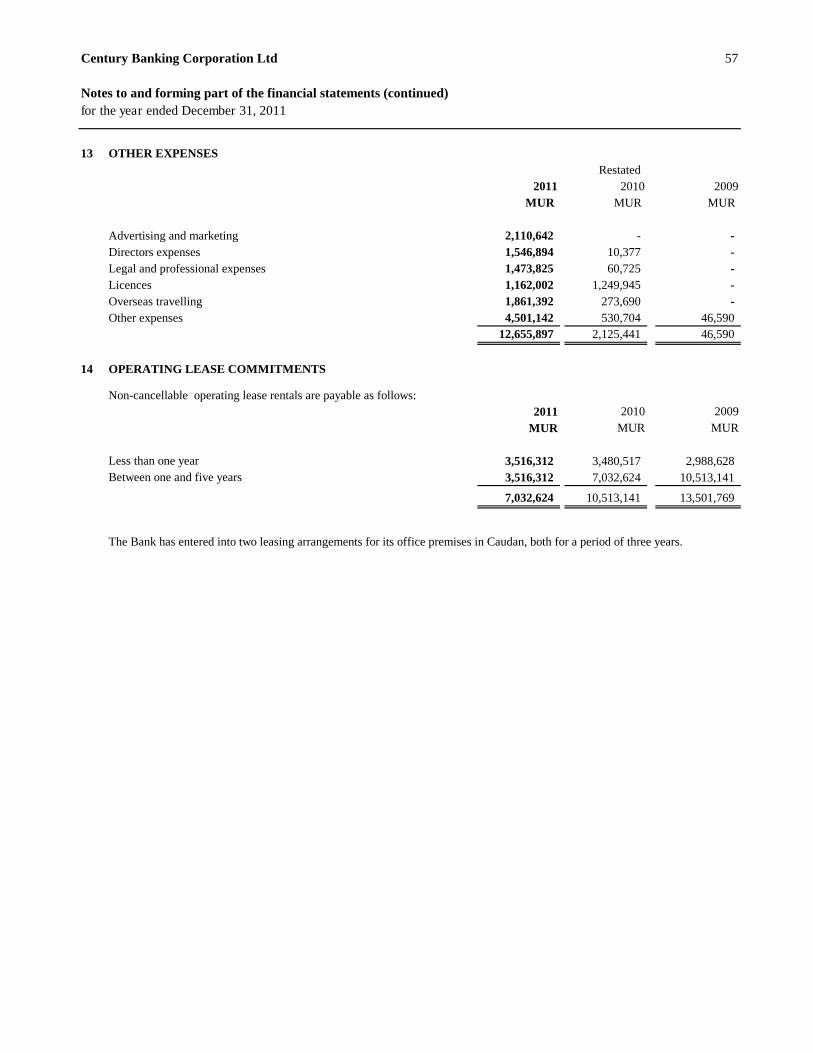

Personnel expenses 24,081,242 269,000 - Operating lease expense 3,480,517 2,988,628 - Depreciation and amortisation 2,586,055 22,110 7,815 Other expenses 13 12,655,897 2,125,441 46,590

42,803,711 5,405,179 54,405

Loss before taxation (41,569,457) (5,405,179) (54,405)

Taxation 12(a) 5,470,487 (500,621) (407,906)

Net loss for the year (36,098,970) (5,905,800) (462,311)

Other comprehensive income - - -

Total comprehensive loss for the year (36,098,970) (5,905,800) (462,311)

Century Banking Corporation Ltd

Statement of Comprehensive Income - Year ended December 31, 2011

The notes on pages 32 to 60 form an integral part of these financial statements.

30

Share Revenue capital deficit TotalMUR MUR MUR

Balance at January 1, 2009 10,000 (65,744) (55,744)

Transactions with owners recognised directly in equity:Issue of ordinary shares 200,110,000 - 200,110,000

Total comprehensive loss for the year:Loss for the year as restated - (462,311) (462,311)

Balance at December 31, 2009 200,120,000 (528,055) 199,591,945

Balance at January 1, 2010 200,120,000 (528,055) 199,591,945

Total comprehensive loss for the year:

Loss for the year as restated - (5,905,800) (5,905,800)

Balance at December 31, 2010 200,120,000 (6,433,855) 193,686,145

Balance at January 1, 2011 200,120,000 (6,433,855) 193,686,145

Transactions with owners recognised directly in equity:

Issue of ordinary shares 60,000,000 - 60,000,000

Total comprehensive loss for the year:

Loss for the year - (36,098,970) (36,098,970)

Balance at December 31, 2011 260,120,000 (42,532,825) 217,587,175

Note:

Century Banking Corporation Ltd

Statement of Changes in Equity - Year ended December 31, 2011

Statutory Reserve and General Banking Reserve are not applicable since the Bank incurred operational losses during the year and does not have retained earnings.

The notes on pages 32 to 60 form an integral part of these financial statements.

31

Restated Restated2011 2010 2009

MUR MUR MURCash flows from operating activitiesLoss before tax (41,569,457) (5,405,179) (54,405)

Adjustment for:Loss on disposal 139,109 - - Depreciation 2,586,055 22,110 7,815

(38,844,293) (5,383,069) (46,590)

Changes in operating assets and liabilitiesChange in other receivables and prepayments 6,262,751 (7,923,947) - Change in other payables 5,983,071 9,226,709 2,729,039 Murabaha financing (54,924,033) - -

Tax paid (275,369) (633,382) -

Net cash (used in) / from operating activities (81,797,873) (4,713,689) 2,682,449

Investing activitiesPurchase of equipment (15,289,305) (857,680) - Proceeds from disposal of property, plant and equipment 34,500 - -

Net cash used in investing activities (15,254,805) (857,680) -

Financing activitiesProceeds from issue of ordinary shares 60,000,000 - 200,110,000

Net cash generated from investing activities 60,000,000 - 200,110,000

(Decrease)/increase in cash and cash equivalents (37,052,678) (5,571,369) 202,792,449

At January 1, 197,241,771 202,813,140 20,691

At December 31, 160,189,093 197,241,771 202,813,140

The notes on pages 32 to 60 form an integral part of these financial statements.

Statement of Cash Flows - Year ended December 31, 2011

Century Banking Corporation Ltd

32

Century Banking Corporation Ltd Notes to and forming part of the financial statements for year ended December 31, 2011

1 Reporting entity

Century Banking Corporation Ltd (formerly known as Deen Banking Corporation Ltd) (the “Bank”) is registered in the Republic of Mauritius as a private limited Bank. The principal activity of the Bank is that of Islamic Banking in accordance with the Shari’a principles and thus, does not deal in interest bearing instruments. The term ‘interest’, if used, is not applicable to the Bank. Its registered office is situated at 25, Pope Hennessy Street, Port Louis and the Bank operates from Suite 405, 4th floor, Barkly Wharf, Caudan Waterfront.

2 Basis of preparation

(a) Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and instructions, guidelines and guidance notes issued by the Bank of Mauritius. The Bank also takes into consideration Financial Accounting Standards issued by Accounting and Auditing Organisation for Islamic Financial Institutions (“AAOIFI”) and applies Shari’a rules and principles as determined by the Shari’a Advisor.

The financial statements were authorised for issue by the Board of Directors on __28 March 2012____.

(b) Basis of measurement

The financial statements have been prepared on a historical cost basis.

(c) Functional and presentation currency

The financial statements are presented in Mauritian rupee (MUR) which is the Bank’s functional and presentation currency.

(d) Use of estimates and judgements

The preparation of the financial statements in conformity with IFRSs requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimates are revised and in any future periods affected.

Significant areas where management has used estimate, assumptions or exercised judgements are as follows:

(i) Provision for impairment of assets

The bank exercises judgment in the estimation of provision for impairment of financial assets. The methodology for the estimation of the provision is set outline in note 3 (d).

33

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies

The principal accounting policies set out below have been applied consistently to all periods presented in these financial statements.

(a) Foreign currency

Transactions in foreign currencies are translated to the Mauritian rupee at exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the reporting date are retranslated to the functional currency at the exchange rate at that date. The foreign currency gain or loss on monetary items is the difference between amortised cost in the functional currency at the beginning of the year, payments during the year, and the amortised cost in foreign currency translated at the exchange rate at the end of the year.

(b) Financial instruments

(i) Non-derivative financial assets

A financial instrument is recognised if the Bank becomes a party to the contractual provisions of the instrument. The Bank initially recognises receivables and deposits on the date that they are originated. All other financial assets (including assets designated at fair value through profit or loss) are recognised initially on the trade date, which is the date that the Bank becomes a party to the contractual provisions of the instrument. The Bank derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred.

Financial assets and liabilities are offset and the net amount presented in the statement of financial position when, and only when, the Bank has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously.

The Bank classifies non-derivative financial assets into other receivables.

Murabaha financing

Murabaha financing are agreements whereby the Bank sells to a customer a commodity or an asset, which the Bank has purchased and acquired based on a promise received from the customer to buy. The selling price comprises the cost plus an agreed profit margin. Amount receivable from Murabaha financing are stated at cost of goods sold plus income recognized by the Bank to the date of financial position less repayments received. Cash and cash equivalents

Cash and cash equivalents comprise cash balances and call deposits. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of change in value. Bank overdrafts that are repayable on demand form an integral part of the Bank’s cash management are included as a component of cash and cash equivalents for the purpose of the statement of cash flows.

34

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(b) Financial instruments (continued)

(i) Non-derivative financial assets (continued)

Trade and other receivables

Trade and other receivables are stated at cost less impairment.

(ii) Non-derivative financial liabilities

All financial liabilities (including liabilities designated at fair value through profit or loss) are recognised initially on the trade date, which is the date that the Bank becomes a party to the contractual provisions of the instrument. The Bank derecognises a financial liability when its contractual obligations are discharged, cancelled or expired. Financial assets and liabilities are offset and the net amount presented in the statement of financial position when, and only when, the Bank has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously. The Bank classifies non-derivative financial liabilities into the other financial liabilities category. Such financial liabilities are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition, these financial liabilities are measured at amortised cost. Other financial liabilities comprise of trade and other payables.

Trade and other payables

Trade and other payables are stated at cost.

(iii) Share capital

Ordinary shares

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares are recognised as a deduction from equity, net of any tax effects.

(c) Plant and equipment

(i) Recognition and measurement

Items of plant and equipment are measured at cost less accumulated depreciation and impairment.

Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labour, any other costs directly attributable to bringing the asset to a working condition for its intended use, and the costs of dismantling and removing the items and restoring the site on which they are located.

35

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(c) Plant and equipment (continued)

(i) Recognition and measurement (continued)

Purchased software that is integral to the functionality of the related equipment is capitalised as part of that equipment. When parts of an item of plant or equipment have different useful lives, they are accounted for as separate items (major components) of plant and equipment. The gain or loss on disposal of an item of plant and equipment is determined by comparing the proceeds from disposal with the carrying amount of the plant and equipment, and is recognised net within other income/other expenses in profit or loss. When revalued assets are sold, any related amount included in the revaluation reserve is transferred to retained earnings.

(ii) Subsequent costs

The cost of replacing part of an item of plant or equipment is recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Bank and its cost can be measured reliably. The carrying amount of the replaced component is derecognised. The costs of the day-to-day servicing of plant and equipment are recognised in statement of comprehensive income as incurred.

(iii) Depreciation

Depreciation is based on the cost of an asset less its residual value. Significant components of individual assets are assessed and if a component has a useful life that is different from the remainder of that asset, that component is depreciated separately.

Depreciation is recognised in profit or loss on a straight-line basis over the estimated useful lives of each component of an item of plant and equipment. Leased assets are depreciated over the shorter of the lease term and their useful lives unless it is reasonably certain that the Bank will obtain ownership by the end of the lease term. Land is not depreciated.

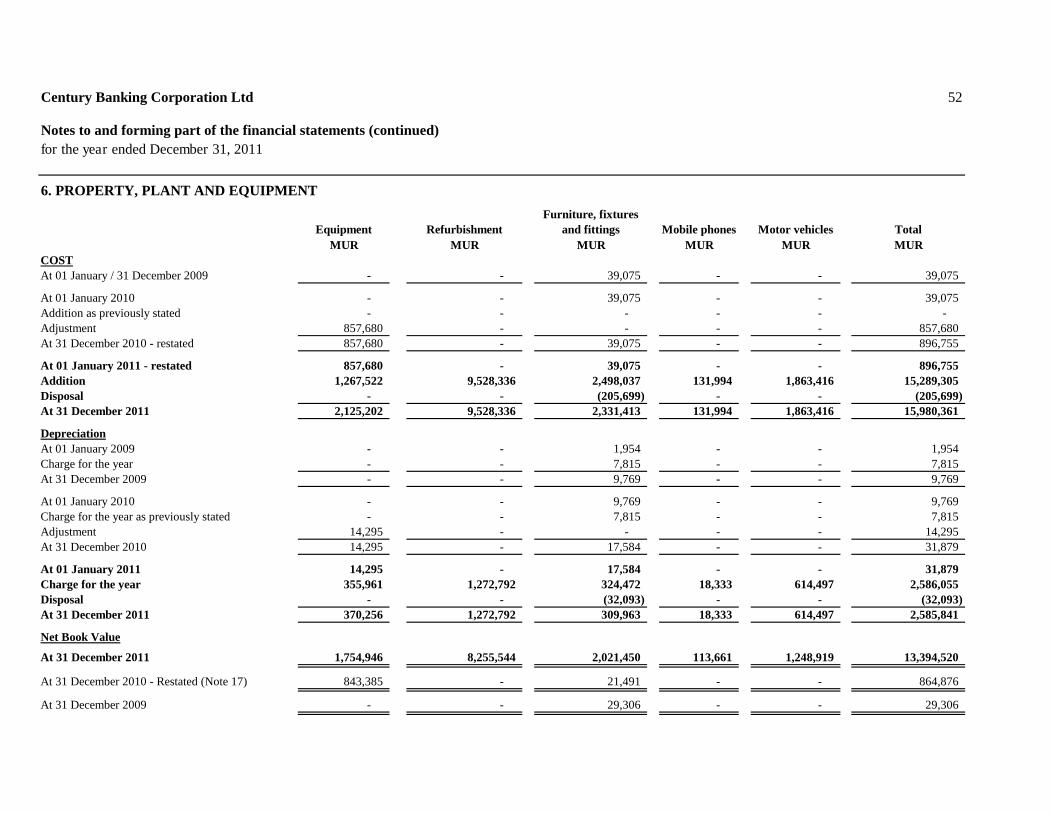

The estimated useful lives for the current and comparative years are as follows:

Rate used Refurbishment 20% Furniture and fixtures 20% Equipment 20% Motor Vehicles 33.3% Mobile Phones 33.3%

Depreciation methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

36

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(d) Impairment

(i) Non-derivative financial assets

A financial asset not carried at fair value through profit or loss is assessed at each reporting date to determine whether there is objective evidence that it is impaired. A financial asset is impaired if objective evidence indicates that a loss event has occurred after the initial recognition of the asset, and that the loss event had a negative effect on the estimated future cash flows of that asset that can be estimated reliably. Objective evidence that financial assets (including equity securities) are impaired can include default or delinquency by a debtor, restructuring of an amount due to the Bank on terms that the Bank would not consider otherwise, indications that a debtor or issuer will enter bankruptcy, adverse changes in the payment status of borrowers or issuers in the Bank, economic conditions that correlate with defaults or the disappearance of an active market for a security. In addition, for an investment in an equity security, a significant or prolonged decline in its fair value below its cost is objective evidence of impairment.

Murabaha financing The Bank considers evidence of impairment for Murabaha financing and receivables at both a specific asset and collective level. All individually significant receivables are assessed for specific impairment. All individually significant Murabaha financing found not to be specifically impaired are then collectively assessed for any impairment that has been incurred but not yet identified. Murabaha financing and receivables that are not individually significant are collectively assessed for impairment by grouping together Murabaha financing with similar risk characteristics. In assessing collective impairment the Bank uses historical trends of the probability of default, the timing of recoveries and the amount of loss incurred, adjusted for management’s judgement as to whether current economic and credit conditions are such that the actual losses are likely to be greater or less than suggested by historical trends. An impairment in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted. Losses are recognised in profit or loss and reflected in an allowance account against Murabaha financing. When a subsequent event (e.g. repayment by a debtor) causes the amount of impairment to decrease, the decrease in impairment is reversed through profit or loss.

(ii) Non-financial assets

The carrying amounts of the Bank’s non-financial assets, other deferred tax assets are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. Impairment is recognised if the carrying amount of an asset or its related cash-generating unit (CGU) exceeds its estimated recoverable amount.

37

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(d) Impairment (continued)

(ii) Non-financial assets (continued)

The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset or CGU. For the purpose of impairment testing, assets that cannot be tested individually are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or CGU. Subject to an operating segment ceiling test, for the purposes of goodwill impairment testing, CGUs to which goodwill has been allocated are aggregated so that the level at which impairment testing is performed reflects the lowest level at which goodwill is monitored for internal reporting purposes. The Bank’s corporate assets do not generate separate cash inflows and are utilised by more than one CGU. Corporate assets are allocated to CGUs on a reasonable and consistent basis and tested for impairment as part of the testing of the CGU to which the corporate asset is allocated. Impairment is recognised in profit or loss. Impairment recognised in respect of CGUs are allocated first to reduce the carrying amount of any goodwill allocated to the CGU (group of CGUs), and then to reduce the carrying amounts of the other assets in the CGU (group of CGUs) on a pro rata basis. Impairment in respect of goodwill is not reversed. In respect of other assets, impairment recognised in prior periods is assessed at each reporting date for any indications that the loss has decreased or no longer exists. Impairment is reversed if there has been a change in the estimates used to determine the recoverable amount. Impairment is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment had been recognised.

(e) Provisions

A provision is recognised if, as a result of a past event, the Bank has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the liability. The unwinding of the discount is recognised as finance cost.

(f) Revenue

Revenue earned by the Bank is recognised on the following bases:

(i) Murabaha financing

Income from Murabaha financing is accrued on a time apportionment basis over the period from the date of the actual disbursement of funds to the scheduled repayment date of installments.

38

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(f) Revenue (continued) (ii) Earnings prohibited by Shari’a

Any income earned by the Bank from sources, which is considered by management as forbidden by Shari'a, is not included in the Bank’s Statement of Comprehensive Income but is transferred immediately to the Special Charity Account Fund upon receipt by the Bank.

The accounting policies in respect of earnings prohibited by Shari’a have been applied retrospectively to prior years and relevant adjustments effected in accordance with IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors.

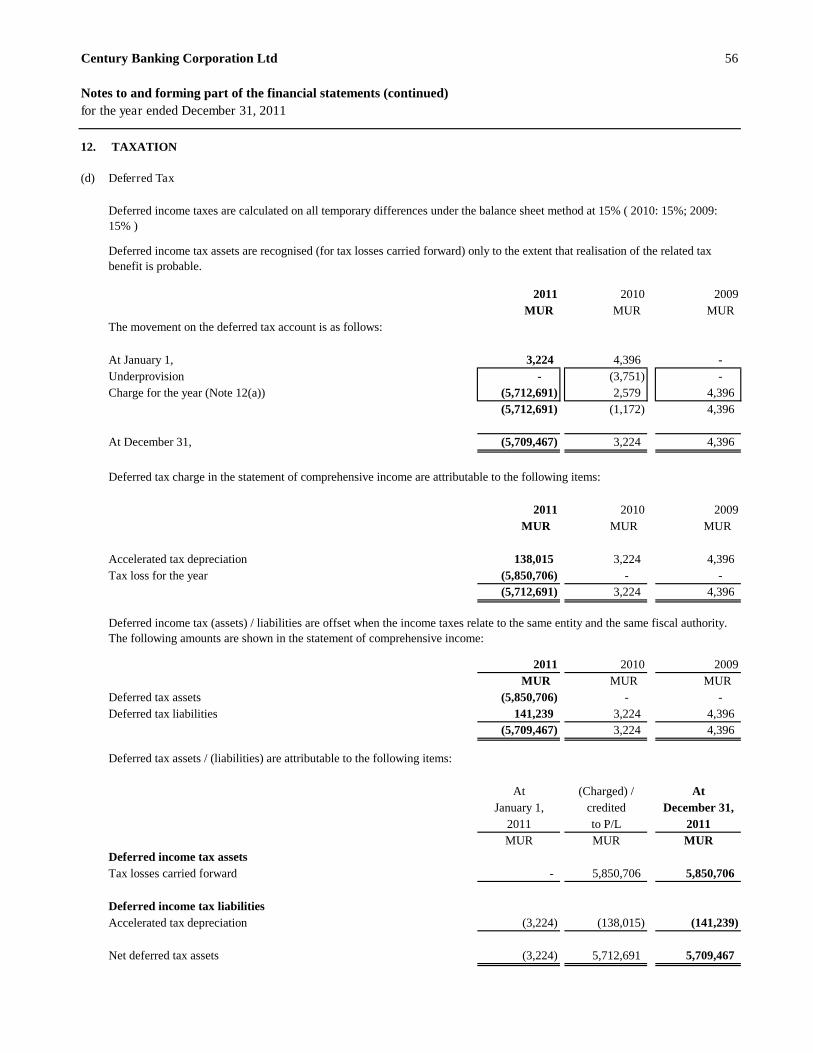

(g) Taxation

Income tax expense comprises current and deferred tax. Current tax and deferred tax is recognised in profit or loss except to the extent that it relates to a business combination, or items recognised directly in equity or in other comprehensive income. Current tax is the expected tax payable or receivable on the taxable income or loss for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable in respect of previous year. Current tax payable also includes any tax liability arising from the declaration of dividends. Deferred tax is recognised in respect of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. Deferred tax is not recognised for:

temporary differences on the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss;

temporary differences related to investments in subsidiaries and jointly controlled entities to the extent that it is probable that they will not reverse in the foreseeable future; and

taxable temporary differences arising on the initial recognition of goodwill.

Deferred tax is measured at the tax rates that are expected to be applied to temporary differences when they reverse, based on the laws that have been enacted or substantively enacted by the reporting date. Deferred tax assets and liabilities are offset if there is a legally enforceable right to offset current tax liabilities and assets, and they relate to income taxes levied by the same tax authority on the same taxable entity, or on different tax entities, but they intend to settle current tax liabilities and assets on a net basis or their tax assets and liabilities will be realised simultaneously. A deferred tax asset is recognised for unused tax losses, tax credits and deductible temporary differences, to the extent that it is probable that future taxable profits will be available against which they can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

39

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(g) Taxation (continued)

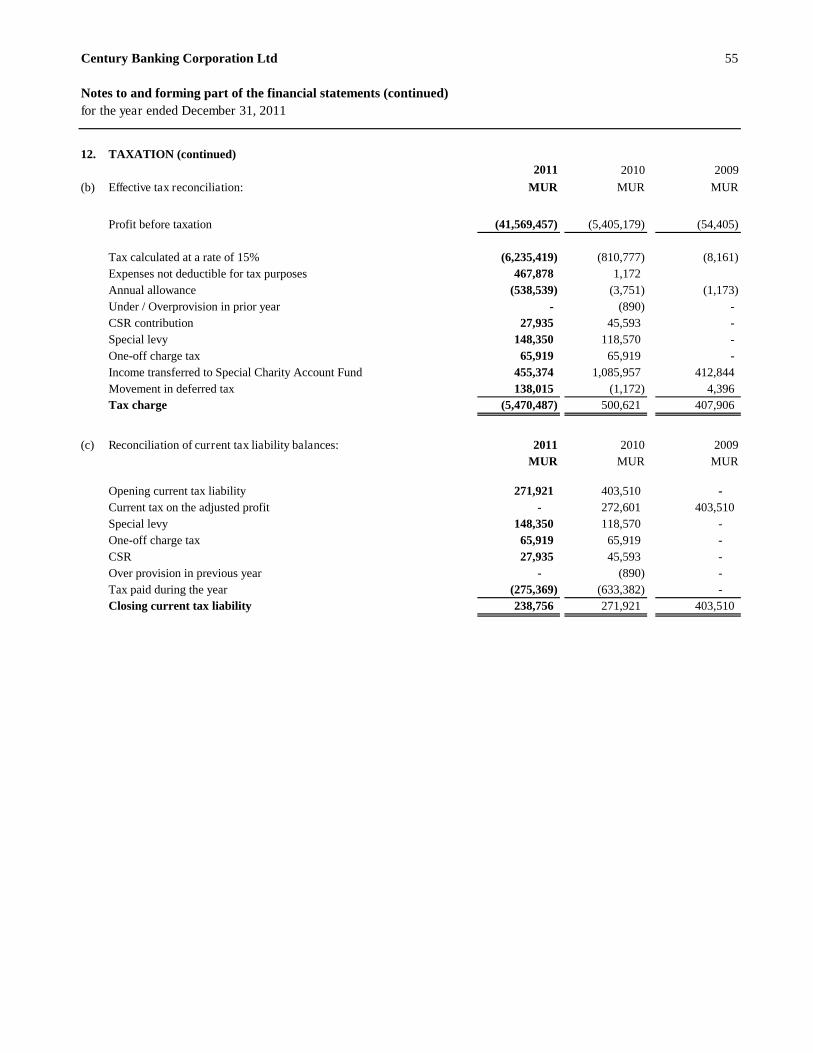

The Bank is liable to pay a special levy of MUR 148,350 (2010: MUR 118,570; 2009: nil) on total operating income derived during the year. The special levy is included in current tax liability in the financial statements.

For the year 2011, a one-off fee of 0.5% on turnover and 1.25% on book profit is levied on banks.

(h) Related parties For the purposes of these financial statements, parties are considered to be related to the Bank if they have the ability, directly or indirectly, to control the Bank or exercise significant influence over the Bank in making financial and operating decisions, or vice versa, or where the Bank is subject to common control or common significant influence. Related parties may be individuals or other entities.

(i) Comparative information

Comparative information has been restated or reclassified, as necessary, to confirm to the current year’s presentation.

(j) New standards and interpretations not adopted

At the date of authorisation of the financial statements of the Bank for the year ended 31 December 2011, the following Standards and Interpretations were in issue but not yet effective:

Standard/Interpretation Effective date

IFRS 7 amendment Disclosures – Transfers of Financial Assets

Annual periods beginning on or after 1 July 2011*

IAS 12 Amendment Deferred tax: Recovery of Underlying Assets

Annual periods beginning on or after 1 January 2012*

IAS 1 Amendment Presentation of items of other comprehensive income

Annual periods beginning on or after 1 July 2012*

IFRS 10 Consolidated Financial Statements Annual periods beginning on or after 1 January 2013*

IFRS 11 Joint Arrangements Annual periods beginning on or after 1 January 2013*

IFRS 12 Disclosure of Interest in Other Entities

Annual periods beginning on or after 1 January 2013*

IFRS 13 Fair value measurement Annual periods beginning on or after 1 January 2013*

40

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(j) New standards and interpretations not adopted (continued)

Standard/Interpretation Effective date

IAS 19 Amendment Employee Benefits Annual periods beginning on or after 1 January 2013*

IFRS 7 Amendment Disclosures: Offsetting Financial Assets and Financial Liabilities

Annual periods beginning on or after 1 January 2013*

IAS 32 Amendment Offsetting Financial Assets and Financial Liabilities

Annual periods beginning on or after 1 January 2014*

IFRS 9 Financial Instruments Annual periods beginning on or after 1 January 2015*

*All Standards and Interpretations will be adopted at their effective date (except for those Standards and Interpretations that are not applicable to the entity).

The directors have not yet estimated the impact of the remaining Standards and Interpretations:

Amendment to IFRS 7: Disclosures – Transfers of Financial Assets

Amendment to IFRS 7 will be effective for the Bank’s financial year end 31 December 2012. The amendments introduce new disclosure requirements about transfers of financial assets including disclosures for:

Financial assets that are not derecognised in their entirety; and Financial assets that are derecognised in their entirety but for which the entity retains continuing involvement

Amendment to IAS 12: Deferred tax – recovery of underlying assets

Amendment to IAS 12 will be effective for the Bank’s financial year end 31 December 2012. The amendments introduce an exception to the general measurement requirements of IAS 12 Income Taxes in respect of investment properties measured at fair value. The measurement of deferred tax assets and liabilities, in this limited circumstance, is based on a rebuttable presumption that the carrying amount of the investment property will be recovered through sale. The presumption can be rebutted only if the investment property is depreciable and held within a business model whose objective is to consume substantially all of the asset’s economic benefits over the life of the asset.

41

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(j) New standards and interpretations not adopted (continued)

Amendment to IAS 1 Presentation of Financial Statements: Presentation of Items of Other Comprehensive Income

Amendment to IFRS 7 will be effective for the Bank’s financial year end 31 December 2013.

The amendments:

require that an entity present separately the items of other comprehensive income that would be reclassified to profit or loss in the future if certain conditions are met from those that would never be reclassified to profit or loss;

do not change the existing option to present profit or loss and other comprehensive income in two statements; and

change the title of the statement of comprehensive income to the statement of profit or loss and other comprehensive income. However, the entity is still allowed to use other titles.

The amendments do not address which items are presented in other comprehensive income or which items need to be reclassified. The requirements of other IFRSs continue to apply in this regard.

The amendment is not expected to have a significant impact on the financial statements.

IFRS 10 Consolidated Financial Statements

IFRS 10 introduces a new approach to determining which investees should be consolidated and provides a single model to be applied in the control analysis for all investees.

An investor controls an investee when:

it is exposed or has rights to variable returns from its involvement with that investee it has the ability to affect those returns through its power over that investee; and there is a link between power and returns Control is reassessed as facts and circumstances change.

IFRS 11: Joint Arrangements

IFRS 11 focuses on the rights and obligations of joint arrangements, rather than the legal forms (as is currently the case). It:

distinguishes joint arrangements between joint operations and joint ventures; and always requires the equity method for jointly controlled entities that are now called joint ventures; they are stripped of the free choice of using the equity method or proportionate consolidation.

42

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(j) New standards and interpretations not adopted (continued)

IFRS 12 Disclosure of Involvement with Other Entities

IFRS 12 sets out the required disclosures for entities reporting under IFRS 10 and IFRS 11. The objective of IFRS 12 is to require entities to disclose information that helps financial statement readers to evaluate the nature, risks, and financial effects associated with the entity’s involvement with subsidiaries, associates, joint arrangements, and unconsolidated structured entities. Specific disclosures include the significant judgments and assumptions made in determining control as well as detailed information regarding the entity's involvement with these investees.

The impact on the financial statements has not yet been estimated.

IFRS 13: Fair Value Measurement

IFRS 13 replaces the fair value measurement guidance contained in individual IFRSs with a single source of fair value measurement guidance. It defines fair value, establishes a framework for measuring fair value and sets out the disclosure requirements for fair value measurements. It explains how to measure fair value when it is required or permitted by other IFRSs. It does not introduce new requirements to measure assets or liabilities at fair value, nor does it eliminate the practicability exceptions to fair value measurements that currently exist in certain standards.

Amendments to IAS 19 Employee Benefits

The amended IAS 19 include the following requirements:

Actuarial gains and losses are recognized immediately in other comprehensive income; this change will remove the corridor method and eliminate the ability for entities to recognize all changes in the defined benefit obligation and in plan assets in profit or loss, which is currently allowed under IAS 19; and

Expected return on plan assets recognized in profit or loss is calculated based on the rate used to discount the defined benefit obligation.

The impact on the financial statements has not yet been estimated.

IFRS 9: Financial Instruments

IFRS 9 will be adopted by the Bank for the first time for its financial reporting period ending 31 December 2015. The standard will be applied retrospectively, subject to transitional provisions.

IFRS 9 addresses the initial measurement and classification of financial assets and will replace the relevant sections of IAS 39.

43

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(j) New standards and interpretations not adopted (continued)

IFRS 9: Financial Instruments (continued)

Under IFRS 9 there are two options in respect of classification of financial assets, namely, financial assets measured at amortised cost or at fair value. Financial assets are measured at amortised cost when the business model is to hold assets in order to collect contractual cash flows and when they give rise to cash flows that are solely payments of principal and interest on the principal outstanding. All other financial assets are measured at fair value.

Embedded derivatives are no longer separated from hybrid contracts that have a financial asset host.

The impact on the financial statements has not yet been estimated.

Additions to IFRS 9: Financial Instruments

The additions to IFRS 9 will be adopted by the Bank for the first time for its financial reporting period ending 31 December 2015. The standard will be applied retrospectively, subject to transitional provisions.

Under IFRS 9 (2010), the classification and measurement requirements of financial liabilities are the same as per IAS 39, barring the following two aspects:

fair value changes for financial liabilities (other than financial guarantees and loan commitments) designated at fair value through profit or loss, attributable to the changes in the credit risk of the liability will be presented in other comprehensive income (OCI). The remaining change is recognised in profit or loss. However, if the requirement creates or enlarges an accounting mismatch in profit or loss, then the whole fair value change is presented in profit or loss. The determination as to whether such presentation would create or enlarge an accounting mismatch is made on initial recognition and is not subsequently reassessed. under IFRS 9 (2010) derivative liabilities that are linked to and must be settled by delivery of an unquoted equity instrument whose fair value cannot be reliably measured, are measured at fair value.

IFRS 9 (2010) incorporates, the guidance in IAS 39 dealing with fair value measurement, derivatives embedded in host contracts that are not financial assets, and the requirements of IFRIC 9 Reassessment of Embedded Derivatives. The impact on the financial statements has not yet been estimated.

44

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

3 Significant accounting policies (continued)

(k) Lease payments

Payments made under operating leases are recognised in profit or loss on a straight-line basis over the term of the lease. Lease incentives received are recognised as an integral part of the total lease expense, over the term of the lease.

Contingent lease payments are accounted for by revising the minimum lease payments over the remaining term of the lease when the lease adjustment is confirmed.

(l) Segment information

Information on segments A and B have been provided in compliance with the guidelines issued by the Bank of Mauritius.

In compliance with the Banking Act 2004, the banking business of licensed bank is divided into two segments. Segment B relates to the banking business that gives rise to “foreign source income.” All other banking business is classified under Segment A.

The financial statements incorporate both segments.

Both Segment A and Segment B reporting currency is Mauritius Rupees (MUR).

Segment information is presented in respect of the Bank’s business and geographical segments. The primary format, business segments, is based on the Bank’s management and internal reporting structure.

Segment capital expenditure is the total cost incurred during the period to acquire equipment, and intangible assets other than goodwill.

All subsequent disclosures relate to Segment A. The Bank did not have any segment B activities during the year.

45

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

4 Shari’a Advisor

The Bank’s business activities are subject to the supervision of either a Shari’a Supervisory Board or a Shari’a Advisor. The Bank has appointed Bait Al-Mashura Finance Consultations, represented by Dr. Osama Qais Al-Dereai, as its Shari’a Advisor for a period of one year renewable. The Shari’a Advisor has the following functions:

i. to consider all that are referred to it of transactions and products introduced by the Bank for use for

the first time and rule on its conformity with the principles of the Shari’a, and to lay down the basic principles for the drafting of related contracts and other documents.

ii. to give its opinion on the Shari’a alternatives to conventional products which the Bank intends to use, and to lay down the basic principles for the drafting of related contracts and other documents, and to contribute to its development with a view of enhancing the Bank’s experience in this regard;

iii. to respond to the questions, enquiries and explanations referred to it by the Board of Executive

Directors or the management of the Bank; iv. to contribute to the Bank’s programme for enhancing the awareness of its staff members of Islamic

Banking and to deepen their understanding of the fundamentals, principles, rules and values relative to Islamic financial transactions; and

v. to submit to the Board of Executive Directors a comprehensive report showing the measure of the

Bank’s commitment to principles of Shari’a in the light of the opinions and directions given and the transactions reviewed.

46

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

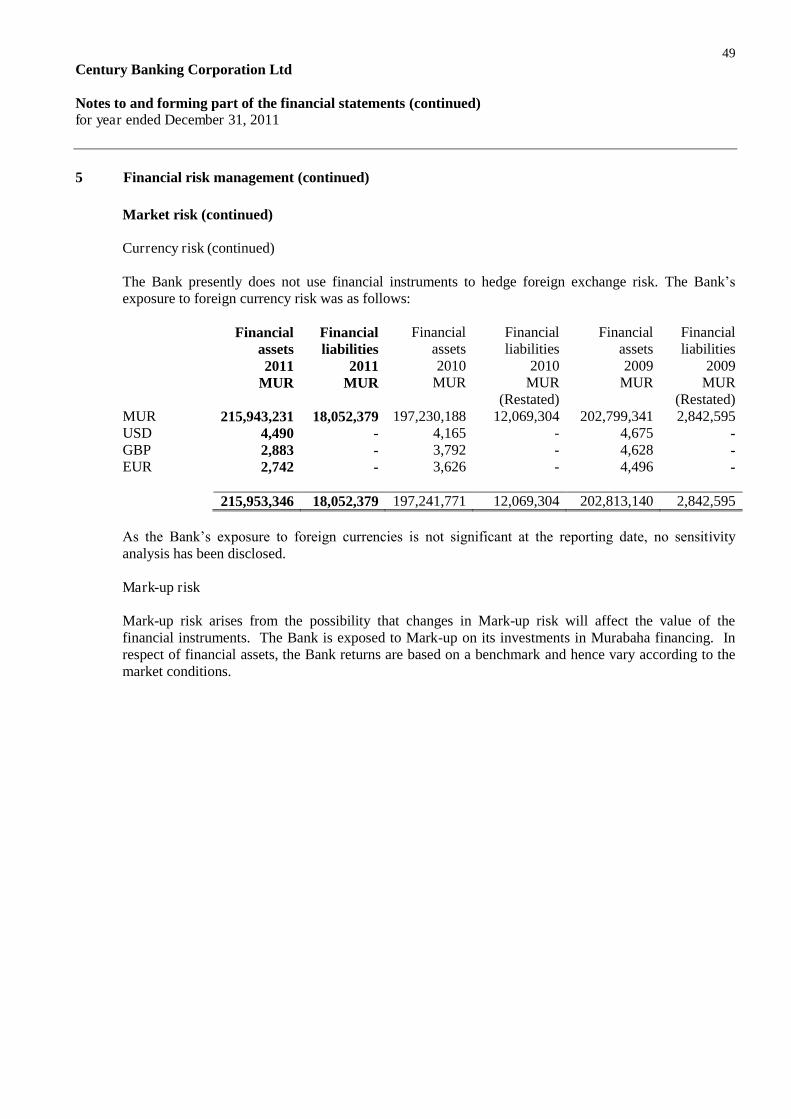

5 Financial risk management

Overview

The Bank has exposure to the following risks from its use of financial instruments: credit risk liquidity risk market risk

This note presents information about the Bank’s exposure to each of the above risks, the Bank’s objectives, policies and processes for measuring and managing risk, and the Bank’s management of capital. The Board of Directors has overall responsibility for the establishment and oversight of the Bank’s risk management framework. The Bank’s risk management policies are established to identify and analyse the risks faced by the Bank, to set appropriate risk limits and controls, and to monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Bank’s activities. The Bank, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment in which all employees understand their roles and obligations.

Credit risk

Credit risk is the risk of financial loss to the Bank if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Bank’s receivables from customers and bank balances. Murabaha contracts are secured based on a careful selection of customers and with adequate security checks. Cash and cash equivalents The bank balances are held with bank and financial institutions which are of good repute.

47

Century Banking Corporation Ltd

Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

5 Financial risk management (continued)

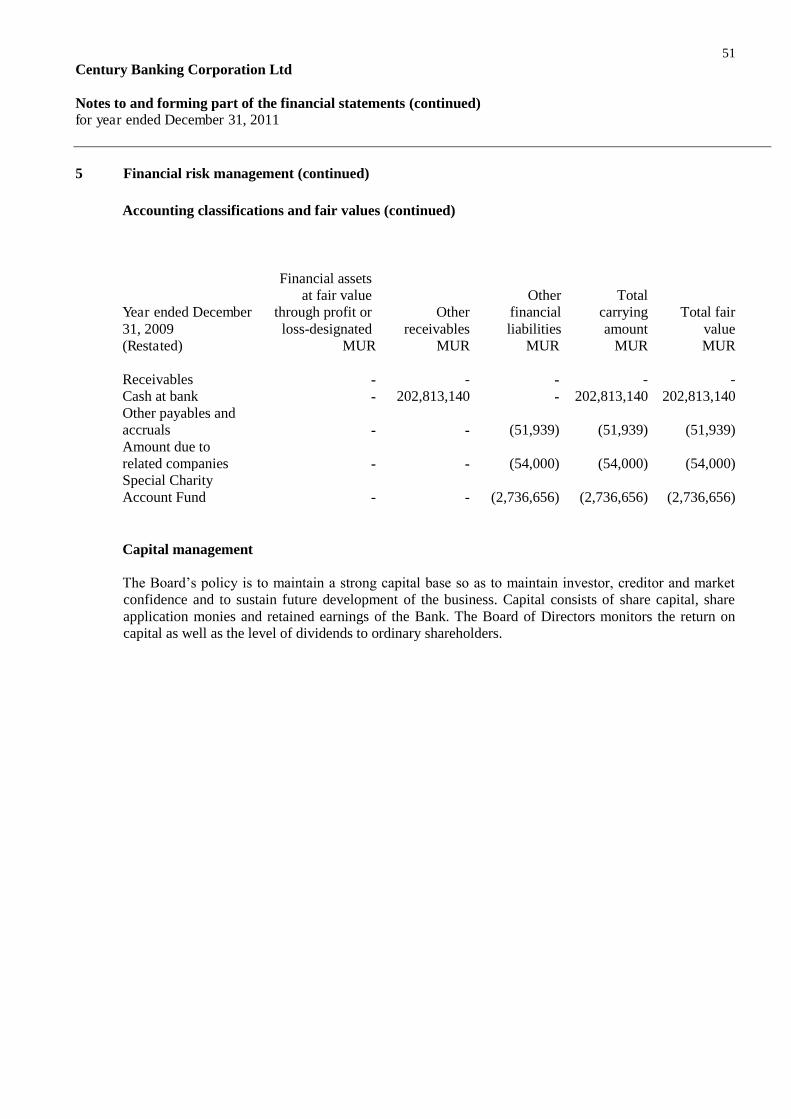

Credit risk (continued) The carrying amount of financial assets represents the maximum credit exposure. The maximum exposure to credit risk at the reporting date was:

2011 2010 2009 MUR MUR MUR

Receivables 840,220 - - Cash at bank 160,189,093 197,241,771 202,813,140 Murabaha financing 54,924,033 - -

215,953,346 197,241,771 202,813,140

The maximum exposure to credit risk for Murabaha financing and receivables at the reporting date by geographic region was:

2011 2010 2009 MUR MUR MUR

Domestic 215,953,346 197,241,771 202,813,140 215,953,346 197,241,771 202,813,140

Liquidity risk Liquidity risk is the risk that the Bank will not be able to meet its financial obligations as they fall due. The Bank’s approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Bank’s reputation.

Typically the Bank ensures that it has sufficient cash on demand to meet expected operational expenses for a period of 60 days, including the servicing of financial obligations; this excludes the potential impact of extreme circumstances that cannot reasonably be predicted, such as natural disasters.

The following are the contractual maturities of non-derivative financial liabilities and excluding the impact of netting agreements.

Year ended December 31, 2011

Carrying

amount

Contractual

cash flows

6 months or less

6-12

months

1-2

years

2-5

years

More than 5 years

2011 2011 2011 2011 2011 2011 2011 MUR MUR MUR MUR MUR MUR MUR Other payables and accruals

3,611,987

3,611,987

-

3,611,987

-

-

-

Amount due to related companies

70,816

70,816

-

70,816

-

-

-

Special Charity Account Fund

14,369,576

14,369,576

-

14,369,576

-

-

-

18,052,379 18,052,379 - 18,052,379 - - -

48

Century Banking Corporation Ltd Notes to and forming part of the financial statements (continued) for year ended December 31, 2011

5 Financial risk management (continued)

Liquidity risk (continued)

Year ended December 31, 2010

Carrying

amount

Contractual

cash flows

6 months or less

6-12

months

1-2

years

2-5

years

More than 5 years

(Restated) 2010 2010 2010 2010 2010 2010 2010 MUR MUR MUR MUR MUR MUR MUR Other payables and accruals

664,743

664,743

-

664,743

-

-

-

Amount due to related companies

70,816

70,816

-

70,816

-

-

-

Special Charity Account Fund

11,333,745

11,333,745

-

11,333,745

-

-

-

12,069,304 12,069,304 - 12,069,304 - - -

Year ended December 31, 2009

Carrying

amount

Contractual

cash flows

6 months or less

6-12

months

1-2

years

2-5

years

More than

5 years (Restated) 2009 2009 2009 2009 2009 2009 2009

MUR MUR MUR MUR MUR MUR MUR Other payables and accruals

51,939

51,939

-

51,939

-

-

-

Amount payable to related companies

54,000

54,000

-

54,000

-

-

-