Expatriates Incoming Seminar on Taxation of Expatriates ICAI, Bangalore Chapter, 18 May 2007 Agenda Residential Status Alternative Income Streams – Tax Implications Avoidance of double taxation - Tax Credits Tax Equalization Vishnu Bagri

Transcript

Expatriates IncomingSeminar on Taxation of ExpatriatesICAI, Bangalore Chapter, 18 May 2007

Agenda

Residential Status

Alternative Income Streams – Tax Implications

Avoidance of double taxation - Tax Credits

Tax Equalization

Vishnu Bagri

Introduction…

Expatriates are usually only temporarily placed in the host country and most of the time plan on returning to their home country

General cross-border taxation principle Treaty determines the taxing rights of the countries

Most India treaties –

Host country taxes income sourced in their land

Home country taxes worldwide income and gives credit for taxes paid in Host country

Where is the “home”? …..Who is the “host” ? …

……..Sometimes the “host” becomes the “home”

India Tax Incidence

India tax incidence dependent upon Residential status

Resident – [Ordinary (ROR) or Not Ordinary (RNOR)]

Non-resident

Scope of Taxable Income

ROR liable to tax on worldwide Income

Treaty provides for taxation rights for different income streams

Host country can also tax subject to treaty limitations

Avoidance of double taxation

RESIDENTIAL STATUS

Residency under Domestic Law

Resident Individual is present for atleast 182 days in India during the

previous year; or

Present atleast 60 days (182 days in certain cases involving persons of India origin) during the previous year and 365 days in the four years immediately preceding the previous year

ROR - A person who is not a RNOR

RNOR Has been non-resident for 9 out of the 10 years preceding the

previous year; or

During the seven years preceding the previous year been in India for 729 days or less

While computing the number of days of stay in India, whether the day of arrival into,

and/or, the day of departure from India, should be considered? (223) ITR 462 (AAR)

Residency under Treaty

Any person who under the laws of the State is liable to tax therein by the reason of his domicile, residence, place of management or any other criteria of similar nature Liable to tax vs. subject to tax vs. actual payment of tax

Indian software company is exempt from income tax, so will it be entitled to treaty relief’s?

Individuals domiciled in UAE

Language could be different amongst treaties e.g. Singapore

Residency under Treaty

Does not include any person who is liable to tax in that State in respect only of income from sources in that State or capital situated therein (OECD model, US treaty; absent in Singapore, UK) Do RNOR qualify as residents under the treaty?

Residency under Treaty

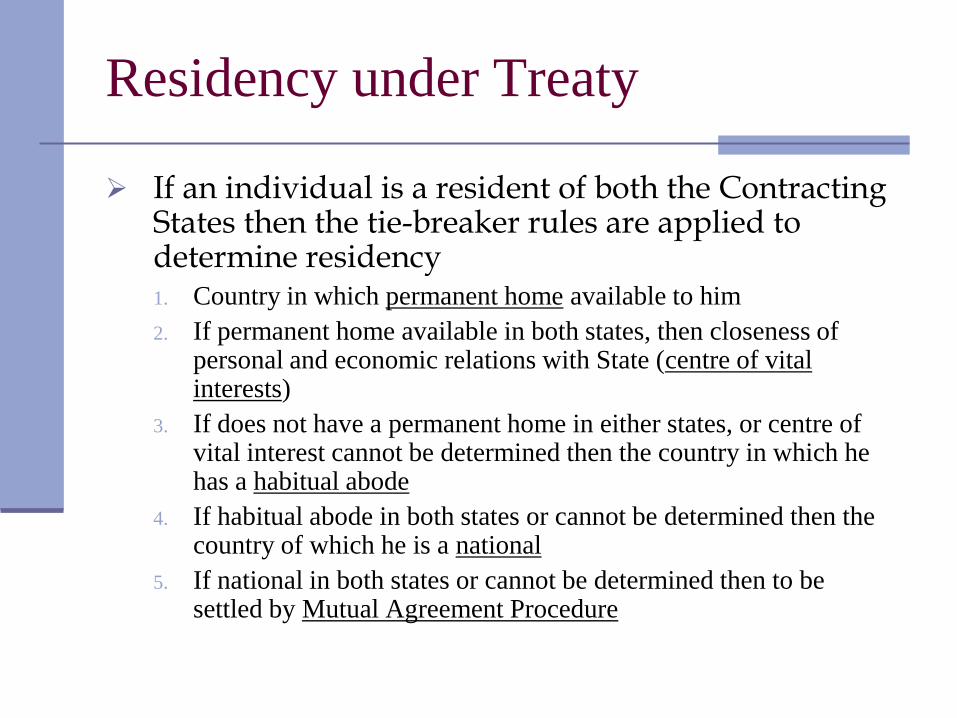

If an individual is a resident of both the Contracting States then the tie-breaker rules are applied to determine residency1. Country in which permanent home available to him

2. If permanent home available in both states, then closeness of personal and economic relations with State (centre of vital interests)

3. If does not have a permanent home in either states, or centre of vital interest cannot be determined then the country in which he has a habitual abode

4. If habitual abode in both states or cannot be determined then the country of which he is a national

5. If national in both states or cannot be determined then to be settled by Mutual Agreement Procedure

Residency under Treaty

OECD commentary suggests …

Tie-breaker rules application to be based on the facts existing during the period when the residence of the taxpayer affects tax liability, which may be less than an entire taxable period

For example, in one calendar year an individual is a tax resident of UK for the period 1 April 06 to 30 June 06, then moves to India. For 06-07, the individual qualifies as a resident in India. Applying the rules to the period 1 April 06 to 30 June 06, the individual was a resident of UK. Therefore, both UK and India should treat the individual as a UK resident for that period, and as an Indian resident from 1 July to 31 March

Acceptance of split-residency under Indian tax laws to be tested

Case Study

“X” has been deputed by its US employer to work for its Indian subsidiary. He qualifies as a ROR for 2006-07 (he came to India in 2002-03) and thereby liable to tax on worldwide income

X is also a US citizen and thereby liable to tax on worldwide income

Other details X plans to stay in India till 2011. His wife has accompanied him

to India. His 2 sons and his parents continue to reside in the US X stays in India in a company leased accomodation. The

agreement is till his period of service in India X renders services to Indian company and draws his salary

income from the Indian company X owns a house in the US which is not rented out X has other substantial investments in the US in the form of

stock and investment trusts

Case Study

As per treaty X is a resident in India and US, so tie-breaker rules will apply

Where is his permanent home? Principles

Permanence of the home is essential; it can be owned or rented

the individual has arranged to have the dwelling available to him at all times continuously, and not occasionally for the purpose of a stay - OECD

To be understood in an objective sense as an opposite of “ for a limited period” – AAR in Dr. Rajnikant Bhat’s case (222 ITR 562)

Appears that the homes in US and India both could qualify as permanent home

Case Study

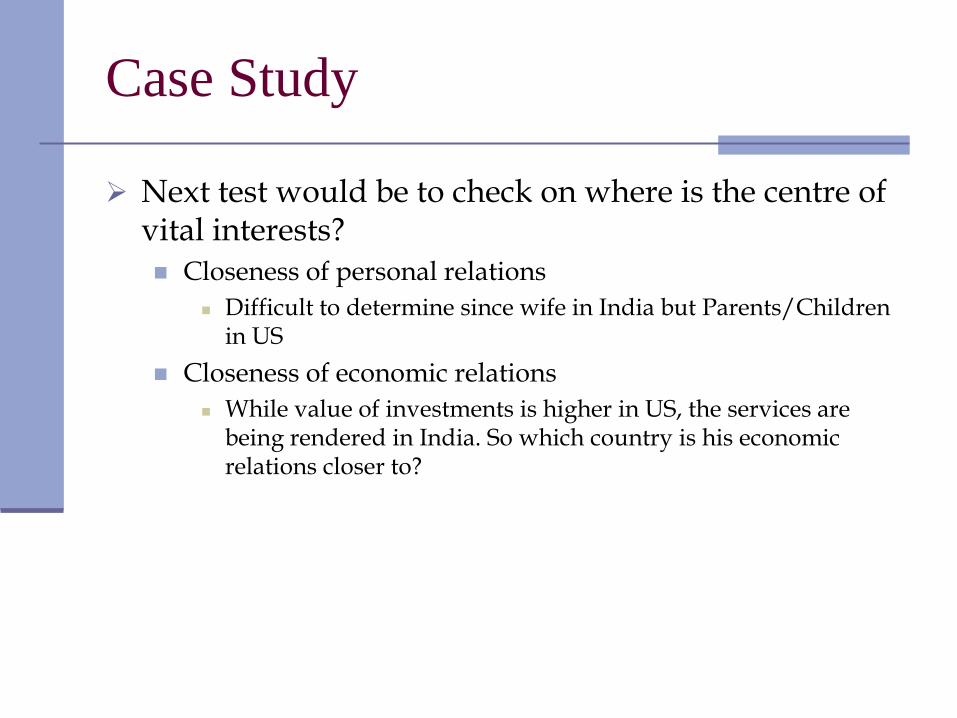

Next test would be to check on where is the centre of vital interests? Closeness of personal relations

Difficult to determine since wife in India but Parents/Children in US

Closeness of economic relations

While value of investments is higher in US, the services are being rendered in India. So which country is his economic relations closer to?

Case Study

Since cannot determine centre of vital interests the next test of “his habitual abode” would need to be applied Principle

The comparison must cover a sufficient length of time for it to be possible to determine whether the residence in each of the two States is habitual and to determine also the intervals at which the stays take place

Given the employment relationship with India, it appears that India would qualify as the habitual abode

THUS, WILL QUALIFY AS A RESIDENT OF INDIA

ALTERNATIVE STREAMS OF INCOME

TAX IMPLICATIONS - TREATY

Scope of Taxable Income

Whether non- resident in India?

Whether ordinary residentin India?

Liable to tax on India sourced income plus overseas income derived from business controlled from India

Liable to tax on India sourced income

Liable to tax on worldwide India

Yes

Yes

No

No

Alternative Streams of Income

Income Stream

Tax Position

(Assume Non-resident in India as per treaty)

Treaty Reference

(OECD Model)

Salary India will have a right to tax if employment exercised in India, subject to short stay exemptions

Article 15: Income from Employment (also referred to as Dependent Personal Services)

Dividend India will have a right to tax if income sourced in India. However within the limitations provided by the treaty.

Article 10: Dividends

Interest Article 11: Interest

Capital Gains

India will typically have a right to tax if asset situated in India (exceptions Mauritius, Cyprus, Singapore treaty)

Article 13: Capital gains

Salary Income

Domestic Law Income from salary earned in India is deemed to accrue or

arise in India

If services rendered in India, the remuneration would be earned in India

Treaty Position Salaries, wages and other similar remuneration derived by a

resident of a Contracting State in respect of an employment shall be taxable only in that State unless the employment is exercised in the other Contracting State.

If the employment is so exercised, such remuneration as is derived therefrom may be taxed in that other State.

Short Stay Exemption (Treaty)

Non resident expatriates can consider claiming the short stay exemption benefit He/she is present in India for a period or periods not

exceeding in the aggregate 183 days in any twelve month period (some treaties refer to the tax or fiscal year e.g. US)commencing or ending in the fiscal year concerned; and

the remuneration is paid by, or on behalf of, an employer who is not a resident of India; and

the remuneration is not borne by (some treaties adopt the words deducted/deductible) a PE which the employer has in the other State

Short Stay Exemption (Treaty)

While planning, Caution to be exercised on the short stay exemption for

expatriates vis-à-vis potential PE exposure for foreign employer in India

Resident expatriates could consider use of short stay exemption under domestic law (applies to individuals who are not citizens of India)

Case Study

X is employed with an Indian company and qualifies as RNOR under the domestic law

Under tie-breaker rule in treaty X qualifies as a non-resident of India. He chooses this position for determining his tax incidence on employment and dividend income streams

X earns long term capital gains from the transfer of listed

securities

Can X take benefit of the preferential rate of 10% (under Sec 112) applicable for residents?

Case Study

Does Treaty residence override domestic residency?

Role of Section 90(2): in relation to the assessee to whom such agreement applies the provisions of this Act shall apply to the extent they are more beneficial to that assessee

Residency under treaty (Article 4) states the residency is for the purposes of the convention

Case Study

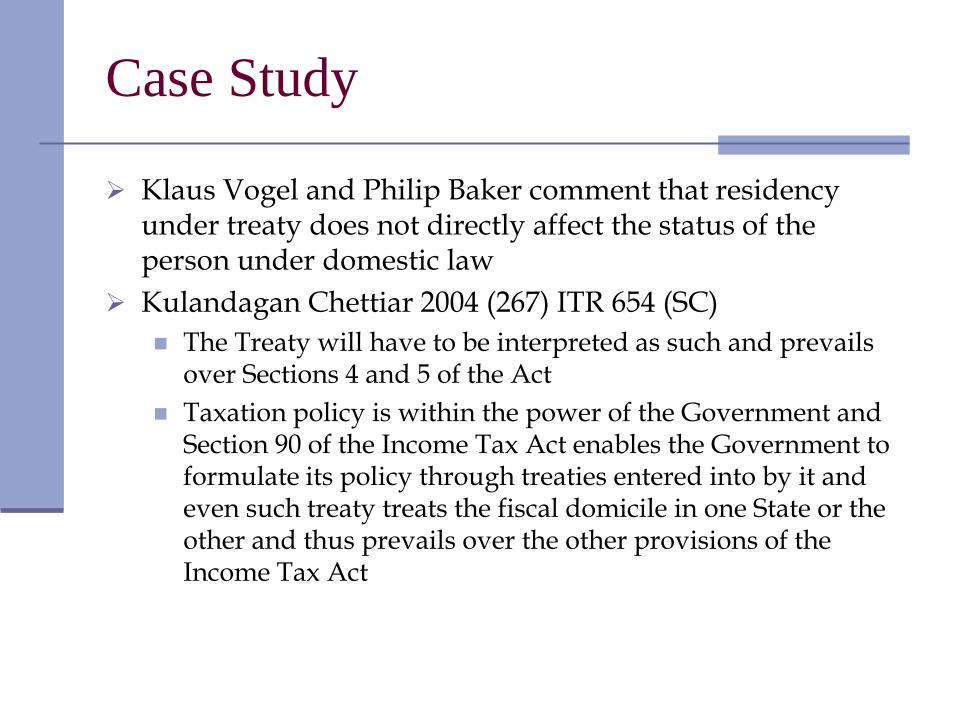

Klaus Vogel and Philip Baker comment that residency under treaty does not directly affect the status of the person under domestic law

Kulandagan Chettiar 2004 (267) ITR 654 (SC)

The Treaty will have to be interpreted as such and prevails over Sections 4 and 5 of the Act

Taxation policy is within the power of the Government and Section 90 of the Income Tax Act enables the Government to formulate its policy through treaties entered into by it and even such treaty treats the fiscal domicile in one State or the other and thus prevails over the other provisions of the Income Tax Act

AVOIDANCE OF DOUBLE TAXATION

TAX CREDITS

Avoidance of Double Taxation

Unilateral tax credits available under domestic law in case of countries with which India does not have a treaty (Section 91)

Treaty countries provide for credits by the resident country i.e. Country of which the expatriate is a resident should typically allow a credit (deduction) for taxes paid in the host country. Such deduction shall not, however, exceed that part of the income tax which is payable in the resident country on such income

Issues on FTC

Timing mismatch Computational and procedural issues for claiming tax

credits where the fiscal/tax years in the two jurisdictions are different

Situations where one tax authority perceives that taxation in the other Contracting State is not in accordance with the provisions of the DTAA

Consideration of foreign tax credits while computing withholding taxes

Definition of “tax “ Taxation of ESOPs under new law (FBT)

Can employee claim credit for FBT initially paid by employer and recovered from employee

TAX EQUALIZATION

Tax Equalization

Expatriate should be neither better nor worse off from a tax point of view by accepting an overseas assignment. He will continue to be subject to the same level of tax as if he had

remained at home

The tax impact of the assignment is therefore neutralized for the expatriate

The mechanism to ensure that the expatriate employee continues to bear the same level of tax involves the deduction of so called "hypothetical" home country tax This hypo tax is used by the employer settle the applicable host

and home country taxes. In addition the employer will pay any taxes due over and above the hypo tax

If the home and host country taxes are less than the hypo tax then the employer enjoys the benefit

Tax Equalization

Home Country (Tax Rate 20%)

Host Country (Tax Rate 30%)

Taxable Salary 100 100

Tax payable 20 30

Net pay 80 70

Employee worse off by 10 (80-70) by accepting international

assignment

Thus a tax equalization could be considered

Tax Equalization – How it works

Salary in home country 100

Less hypo tax (20%) 20

Net salary 80

Add tax in host country (30/70* 80) 34.28

Revised Salary 114.28

Tax in home country @ 20%

Credit for taxes in host country so no tax outflow in home country

22.85

Net take home (114.28 – 34.28) 80

Can it be argued that the taxable income in India (say host

country) is 94.28 (114.28-20), since hypo tax has been

![Cenvat Accounting[1]](https://static.documents.pub/doc/80x56/54193e3a7bef0a05088b4642/cenvat-accounting1.jpg)