107

Audited Annual Report as of December 31, 2015 CGS FMS Société d’Investissement à Capital Variable R.C.S. Luxembourg B 157.442 Administrative Agent:

Audited Annual Reportas of December 31, 2015

CGS FMS

Société d’Investissement à Capital Variable

R.C.S. LuxembourgB 157.442

Administrative Agent:

CGS FMS

l CGS FMS Global Evolution Emerging Frontier

Paying and information agent for Germany:

Marcard, Stein & Co AG

Ballindamm 36

20095 Hamburg

has been appointed as paying and information agent in the Federal Republic of Germany (the ’’German Paying and Information Agent’’).

The conversion prices correspond to the redemption and subscription prices or the Net Asset Value per share. Requests for redemption and conversion may be submitted to the German Paying and Information Agent. All payments (redemption

proceeds, any distributions and other payments) may be paid by the German Paying- and Information Agent to the Shareholders. Any notices to shareholders shall be published in the Bundesanzeiger.

The statement of changes in the composition of the investment portfolio is also available free of charge upon request at the office of the German Paying and Information Agent.

For the following sub-fund no notification for distribution in the Federal Republic of Germany was submitted and Shares in this sub-fund may NOT be offered to investors within the scope of the German Investment Code. As a

consequence, the following Sub-Funds are NOT available to investors in Germany:

Additional Information for Investors in the Federal Republic of Germany

The Articles of Incorporation, the Prospectus and Key Investor Information Document, semi-annual and annual reports, the subscription and redemption prices are available free of charge from the Management Company and the German Paying

and Information Agent during usual business hours. In addition, this information is available electronically at the Management Company’s website on http://www.universal-investment.lu.

The current Net Asset Value per share, subscription and redemption prices of all share classes are available free of charge at the German Paying and Information Agent. Additionally these prices (Net Asset Value per Share, Subscription, and

Redemption) of all share classes are published and visible at www.universal-investement.lu.

An investor is allowed to convert shares from one Share Class into another Share Class (please refer to the prospectus for more information); the conversion price(s) correspond to the redemption and subscription prices or the Net Asset Value

per share. Requests for redemption and conversion may be submitted to the German Paying and Information Agent.

1

CGS FMS

�

�

�

�

�

Paying and Information Agent for the shares of the SICAV authorized for public distribution in Austria:

ERSTE BANK der oesterreichischen Sparkassen AG

Am Belvedere 1

1010 Wien, Austria.

-

-

-

-

-

Additional Information for Investors in Austria

The following documents and information may be obtained in hard copy and free of charge at the registered office of the Management Company (Universal-Investment-Luxembourg S.A.) and at the Austrian Paying and Information Agent andcan be inspected at the offices of the Austrian Paying agent during normal business hours:

The following Sub-Funds are available to investors in Austria:

Applications for the redemption, subscriptions and conversion of shares may be sent to the Austrian Paying Agent. All payments to investors, including redemption proceeds, potential distributions and other payments, may, upon request, bepaid through the Austrian Paying and Information Agent.

The prospectus and the articles of incorporation;

Key Investor Information Documents (KIIDs);

The annual report and semi-annual report;

Redemption or Subscription prices;

Any investor notices.

CGS FMS - Global Evolution EM Blended Debt

CGS FMS - Global Evolution EM Debt

CGS FMS - Global Evolution EM Debt and FX

CGS FMS - Global Evolution EM Local Debt

CGS FMS - Global Evolution Frontier Markets

3

CGS FMS

Table of Contents

Independent auditor’s report 6

Organisation 7

Report of the Board of Directors 8 - 9

Report of the Asset Manager 10 - 27

CGS FMS - SICAV

Combined Statement of Net Assets 28

Combined Statement of Operations (including income equalisation) 29 - 30

Combined Statement of Changes in Net Assets 31

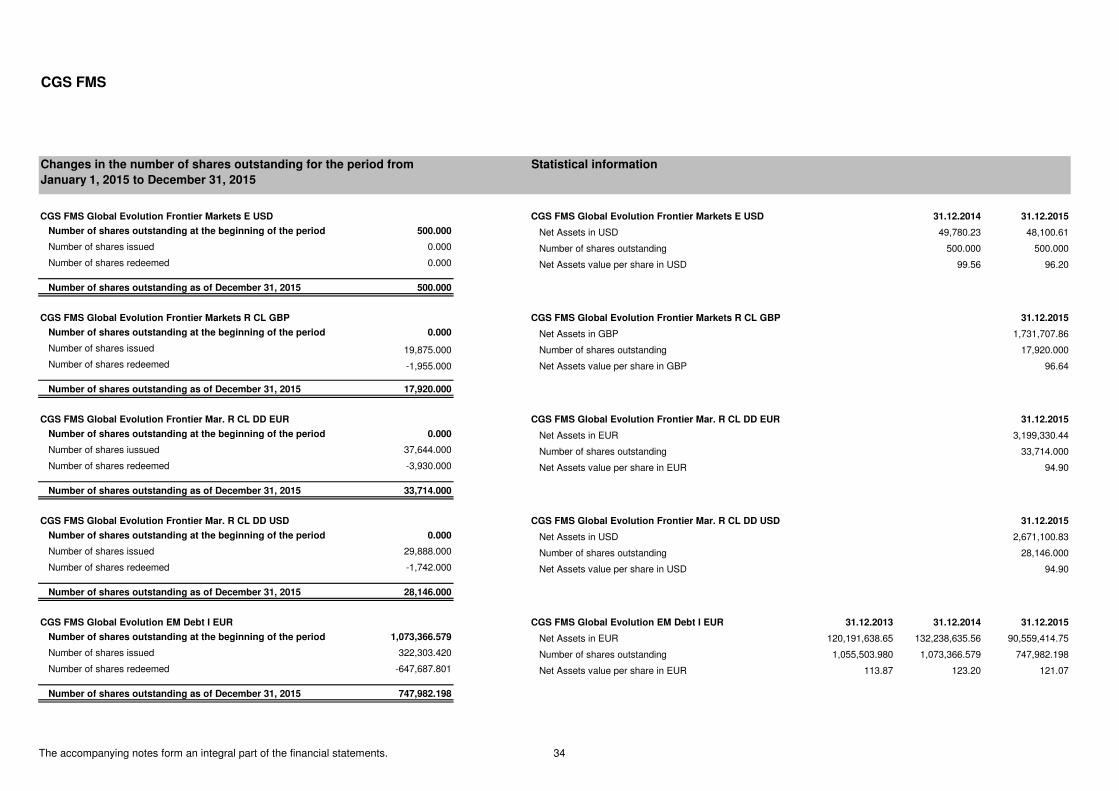

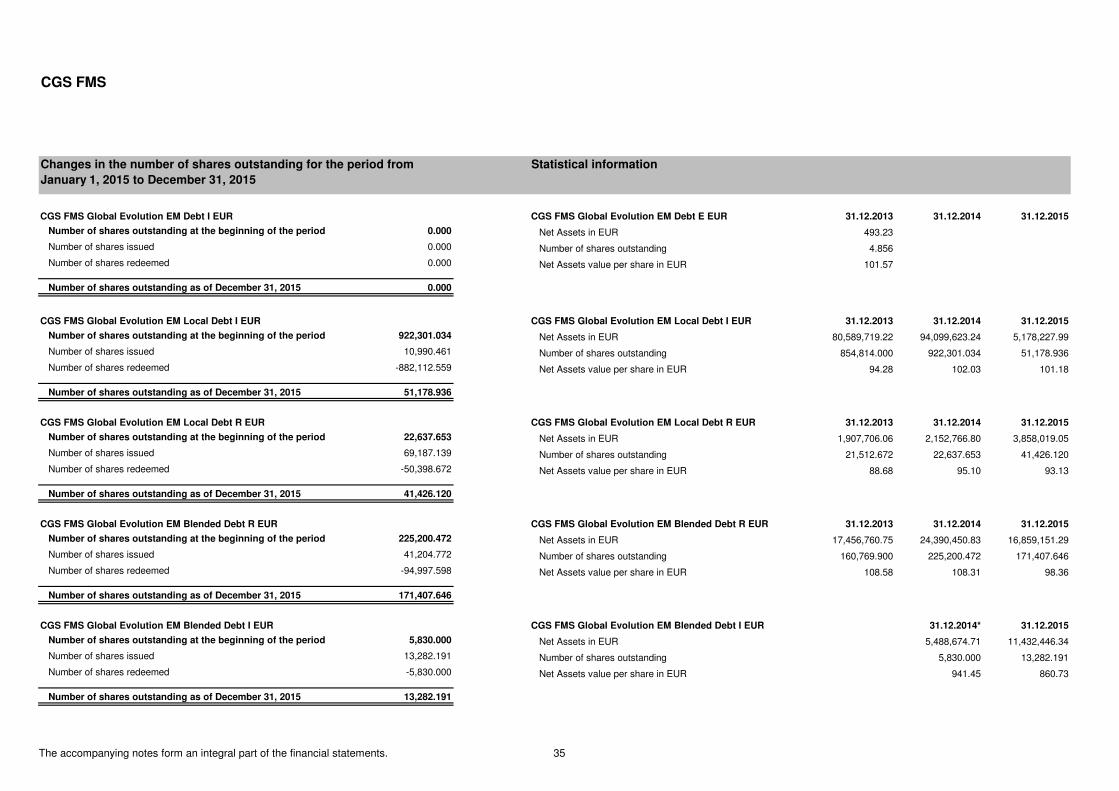

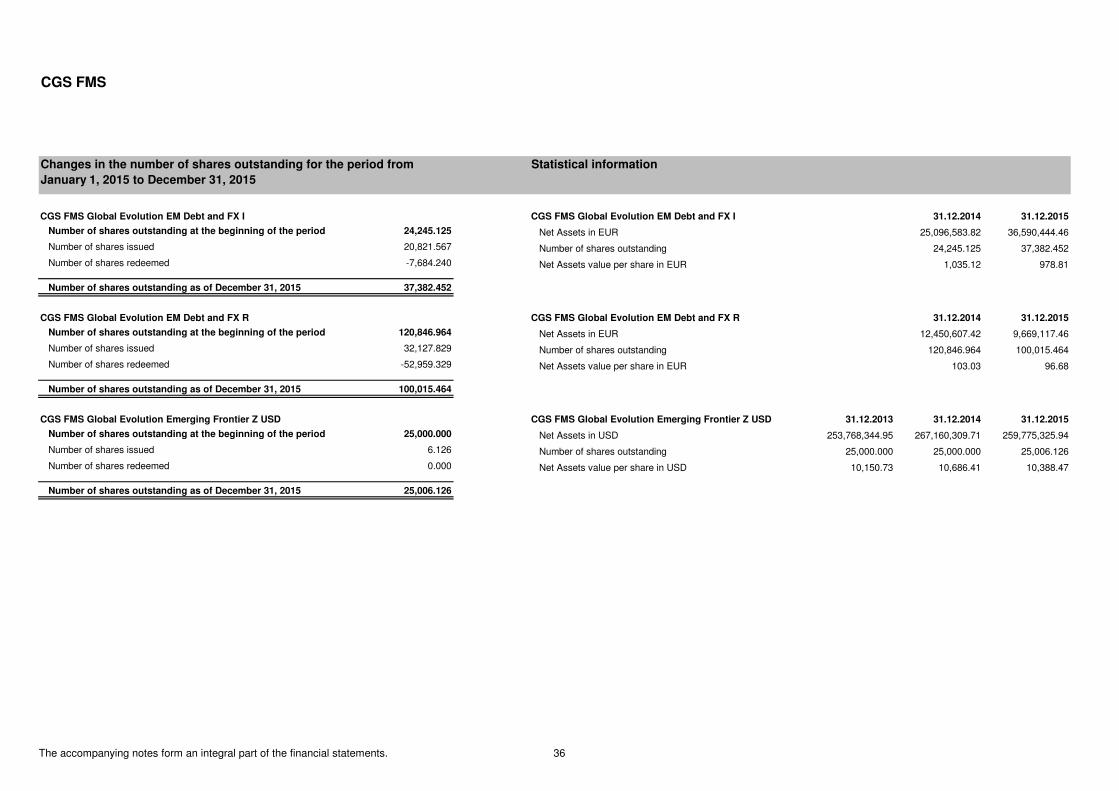

Changes in the number of shares outstanding 32 - 37

Statistical Information 32 - 37

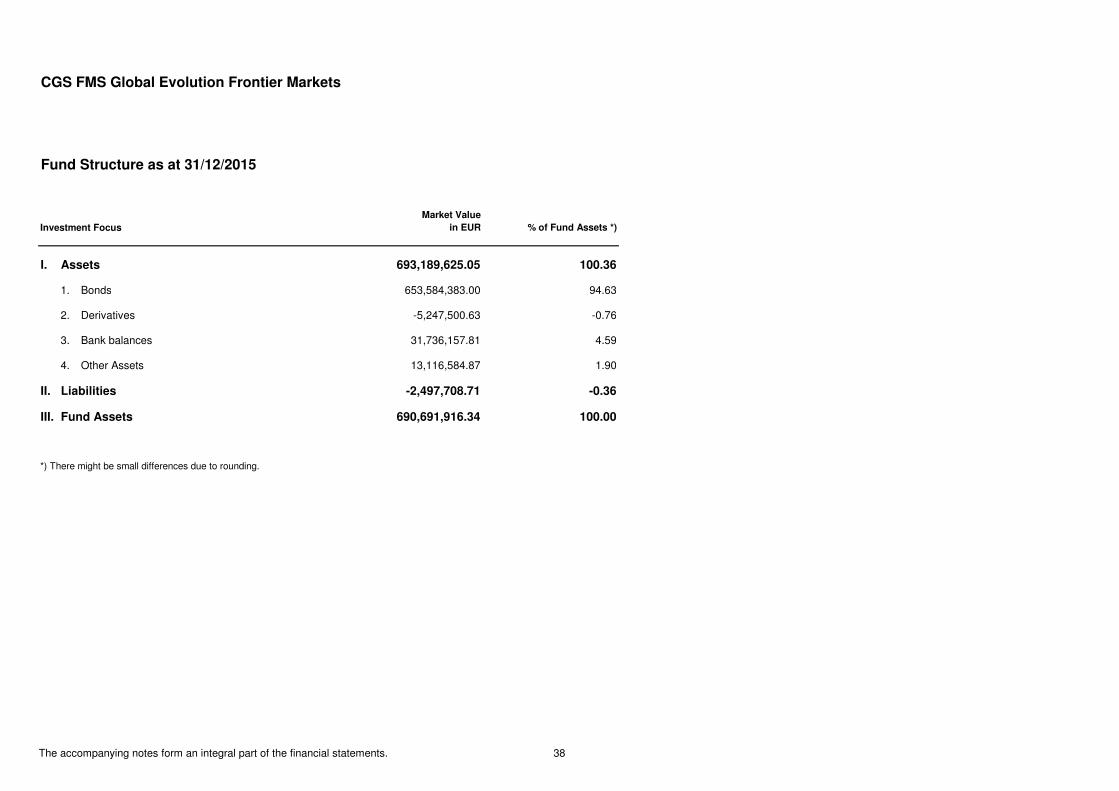

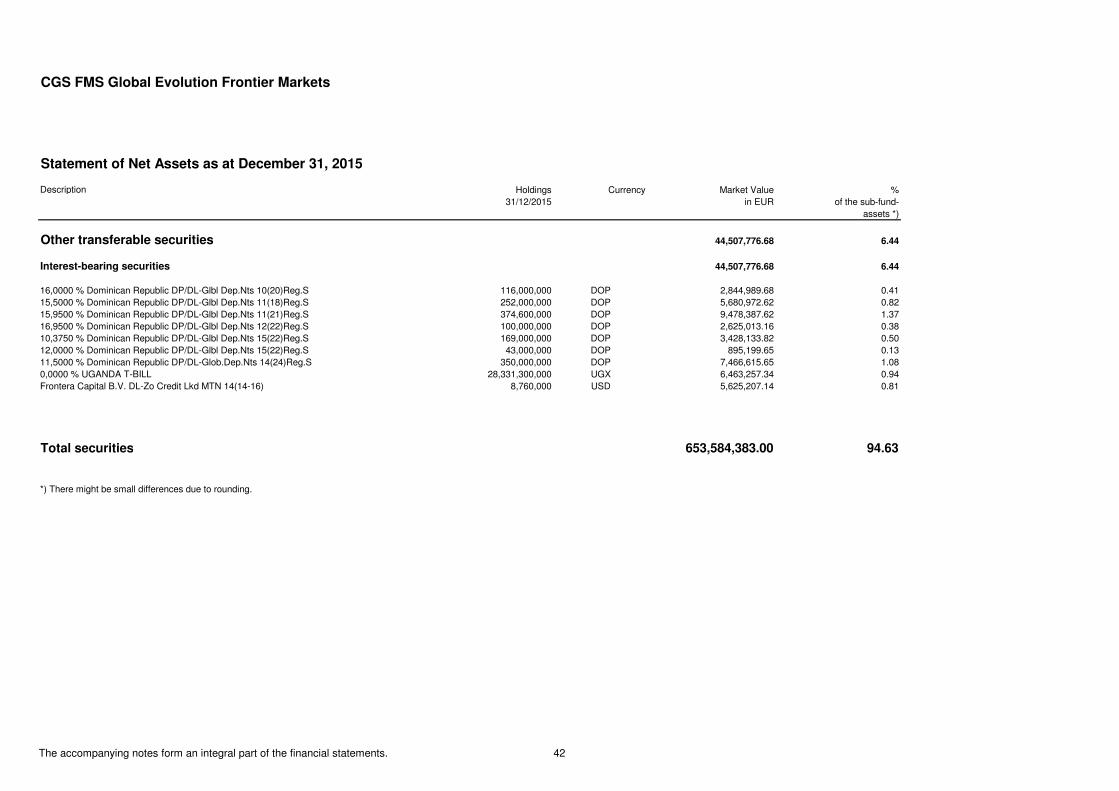

CGS FMS - Global Evolution Frontier Markets

Fund Structure 38

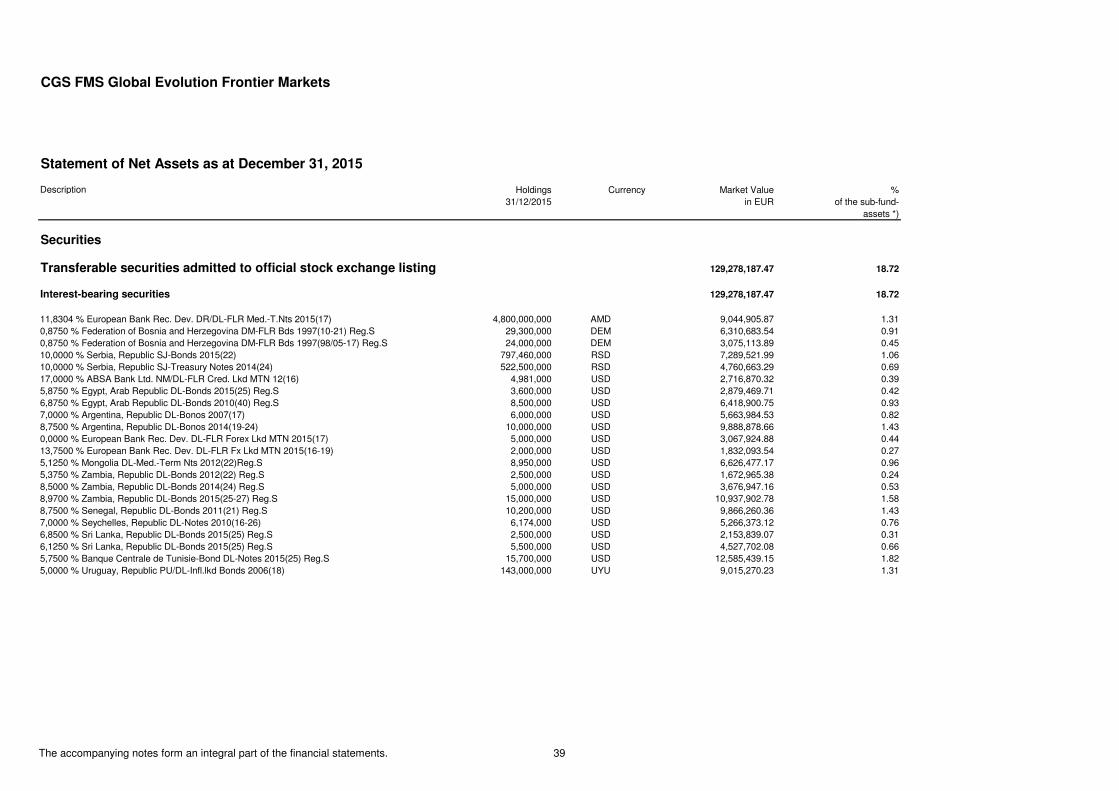

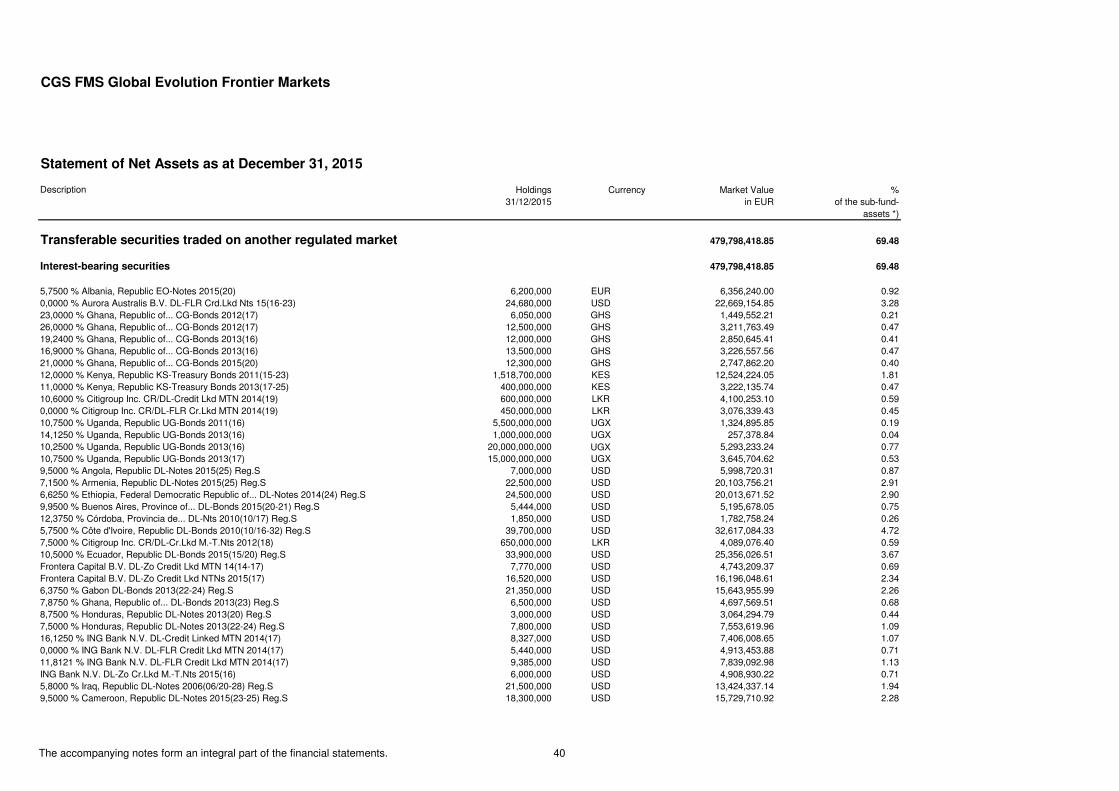

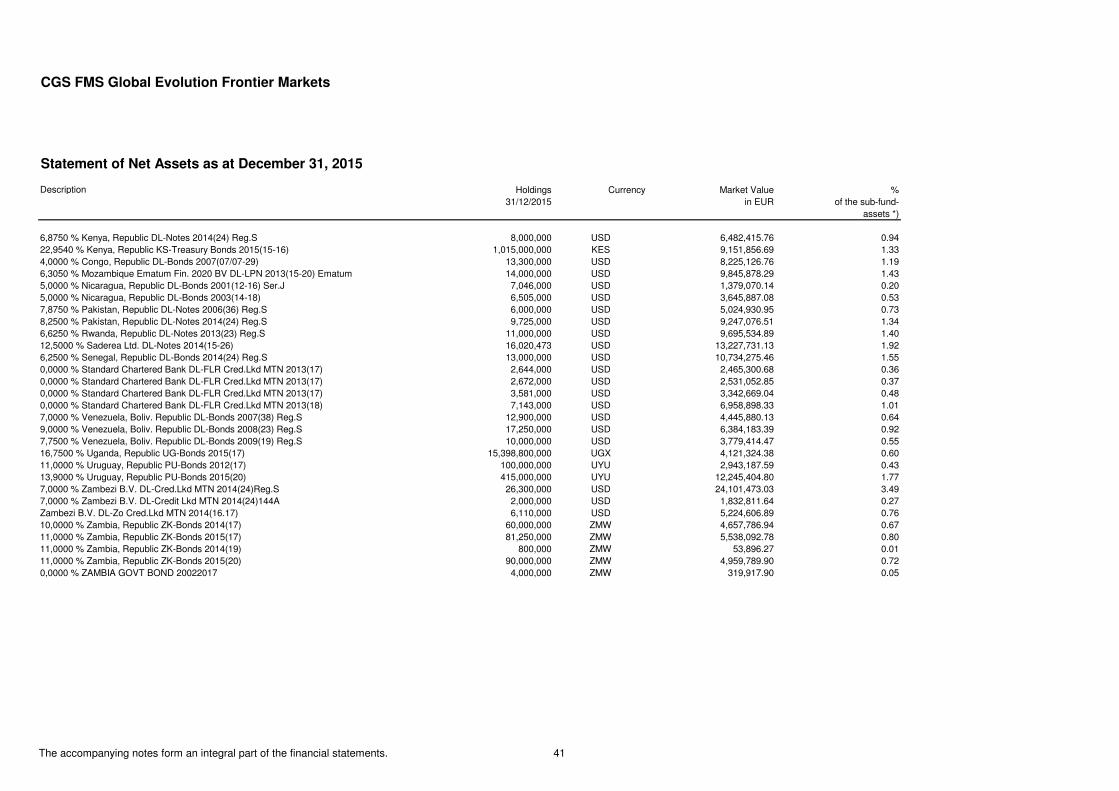

Statement of Securities 39 - 42

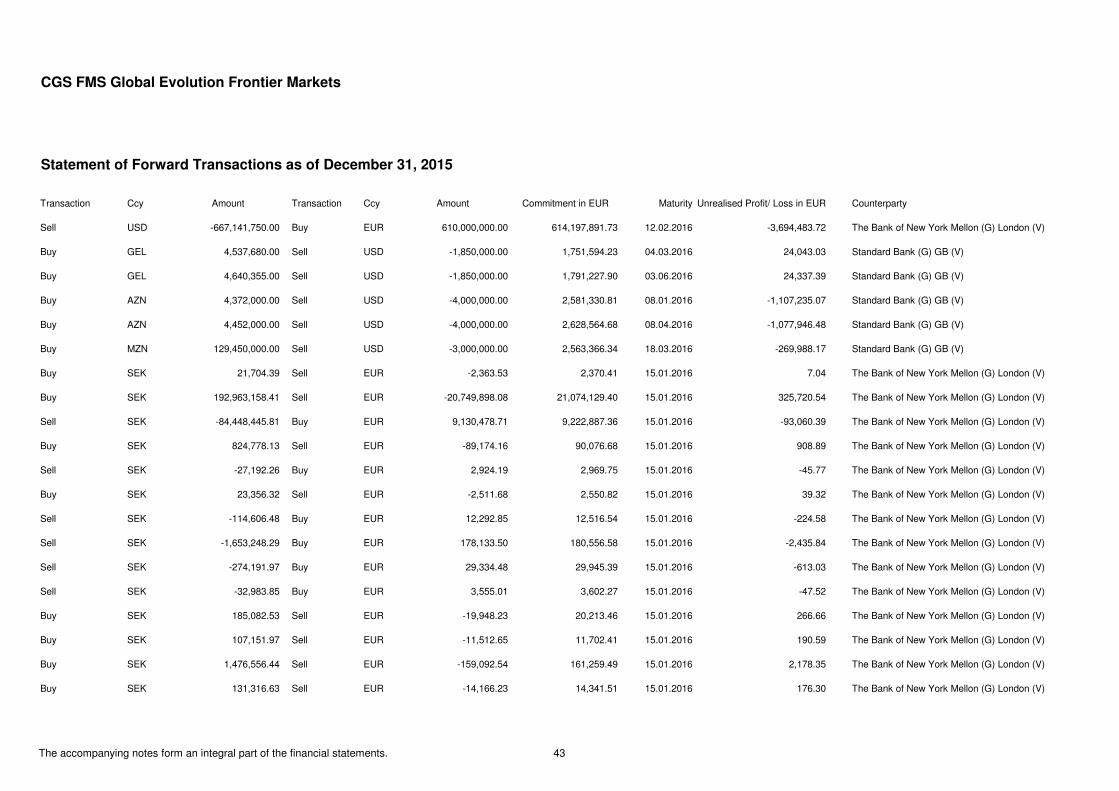

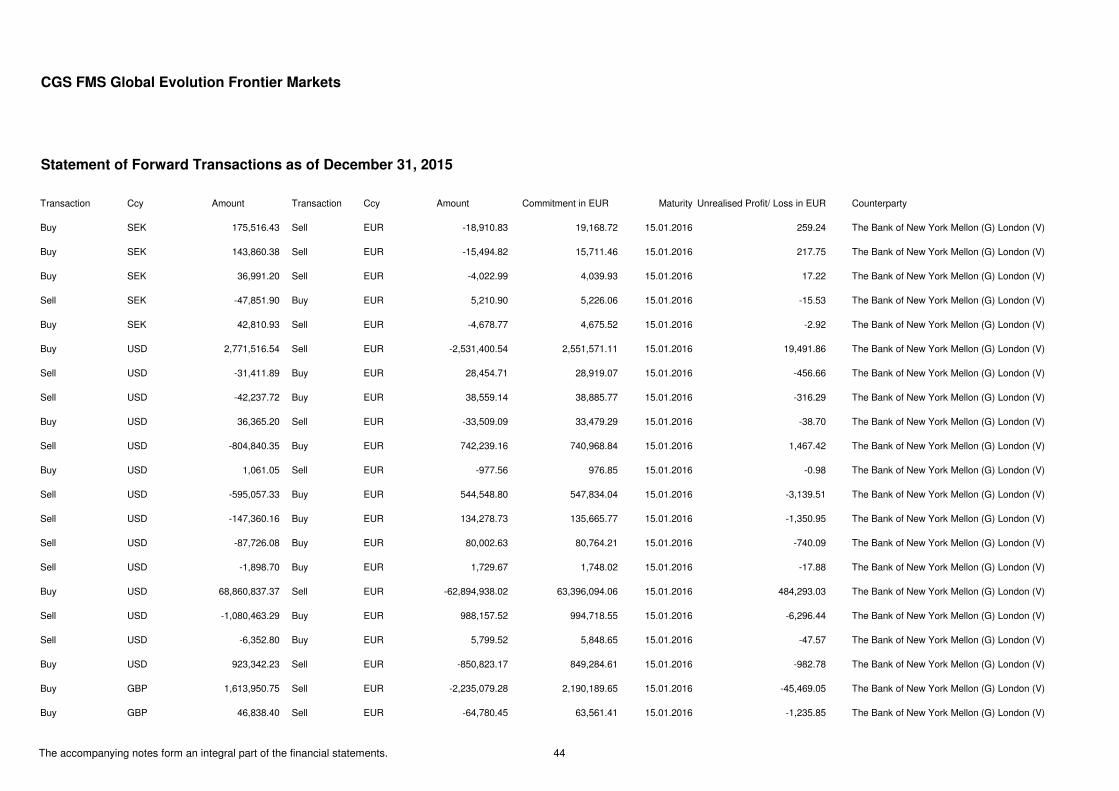

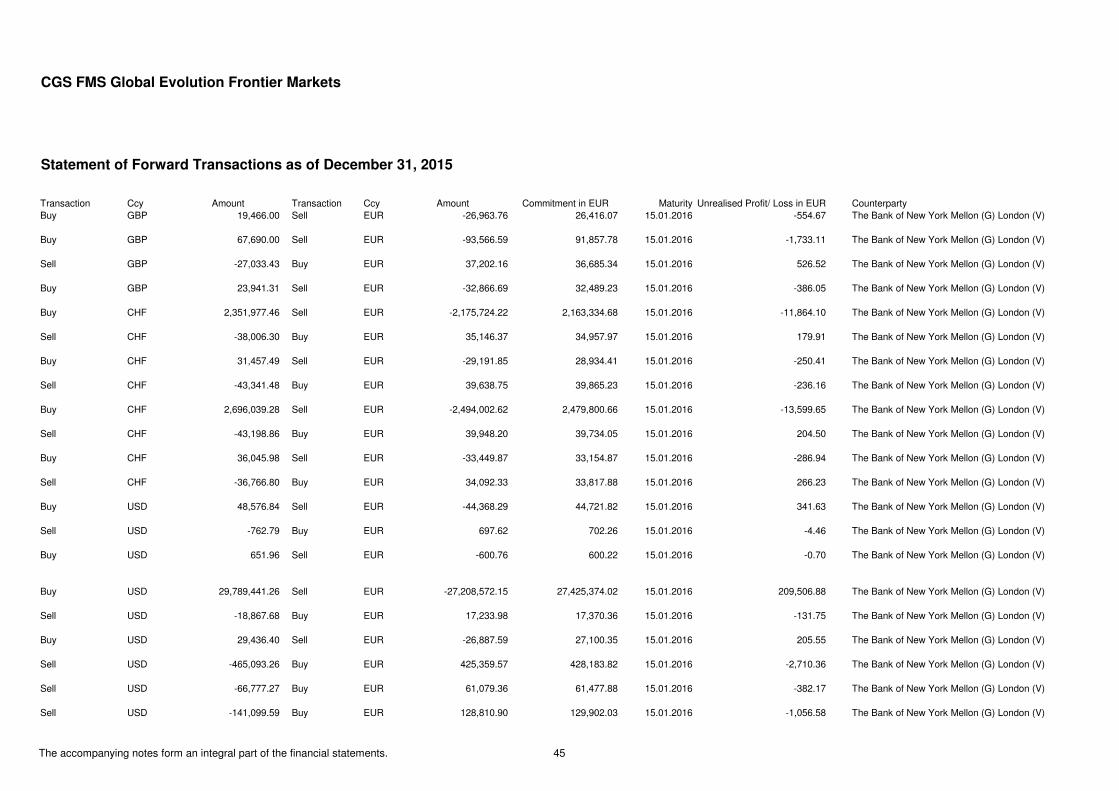

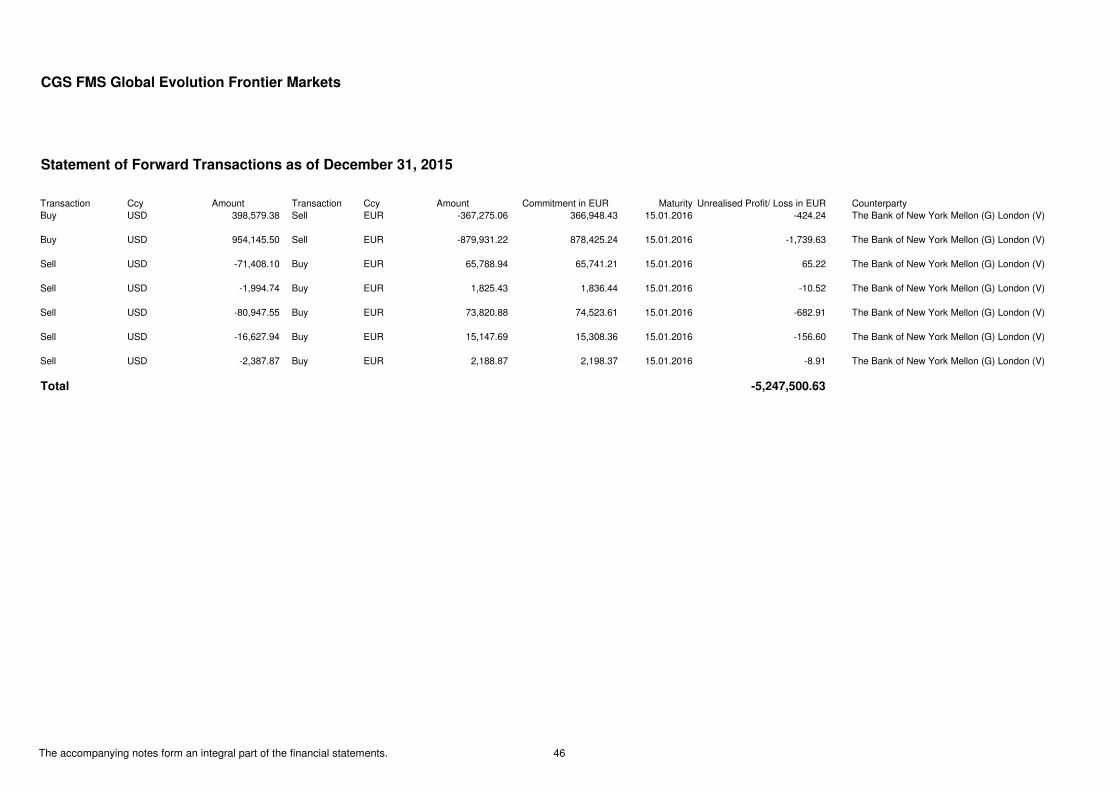

Statement of Forward Transactions 43 - 46

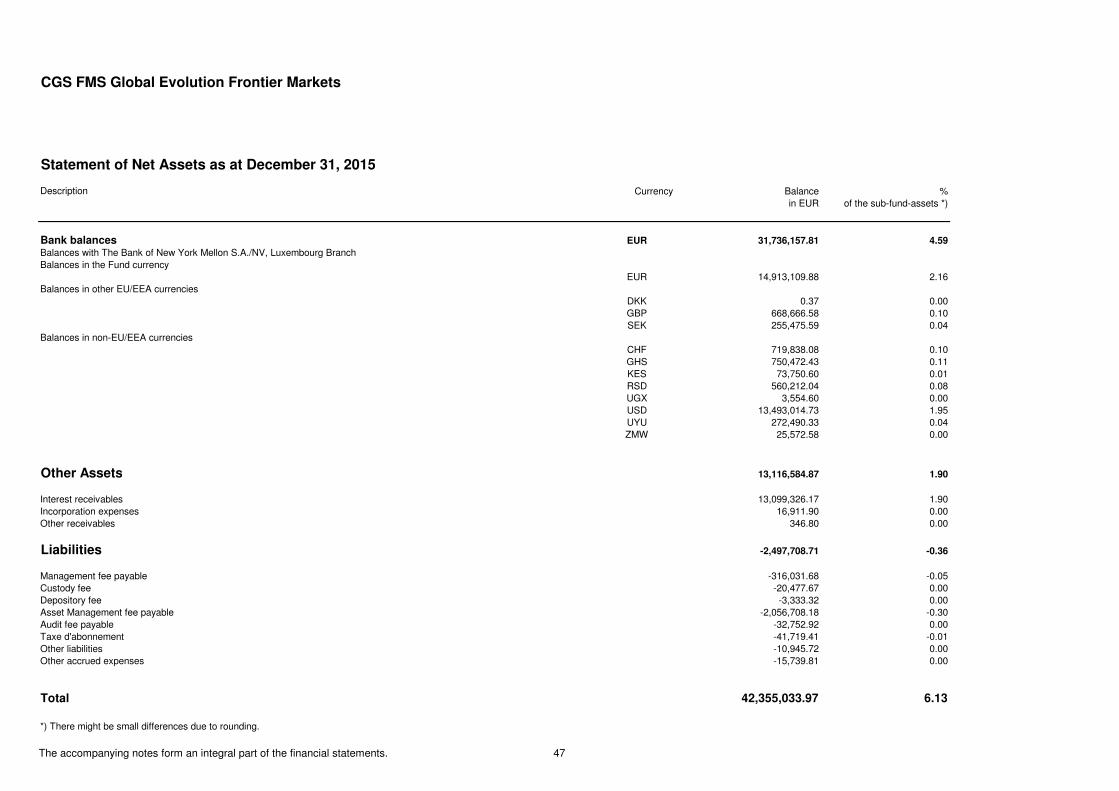

Statement of Bank balances, Other Assets and Liabilities 47

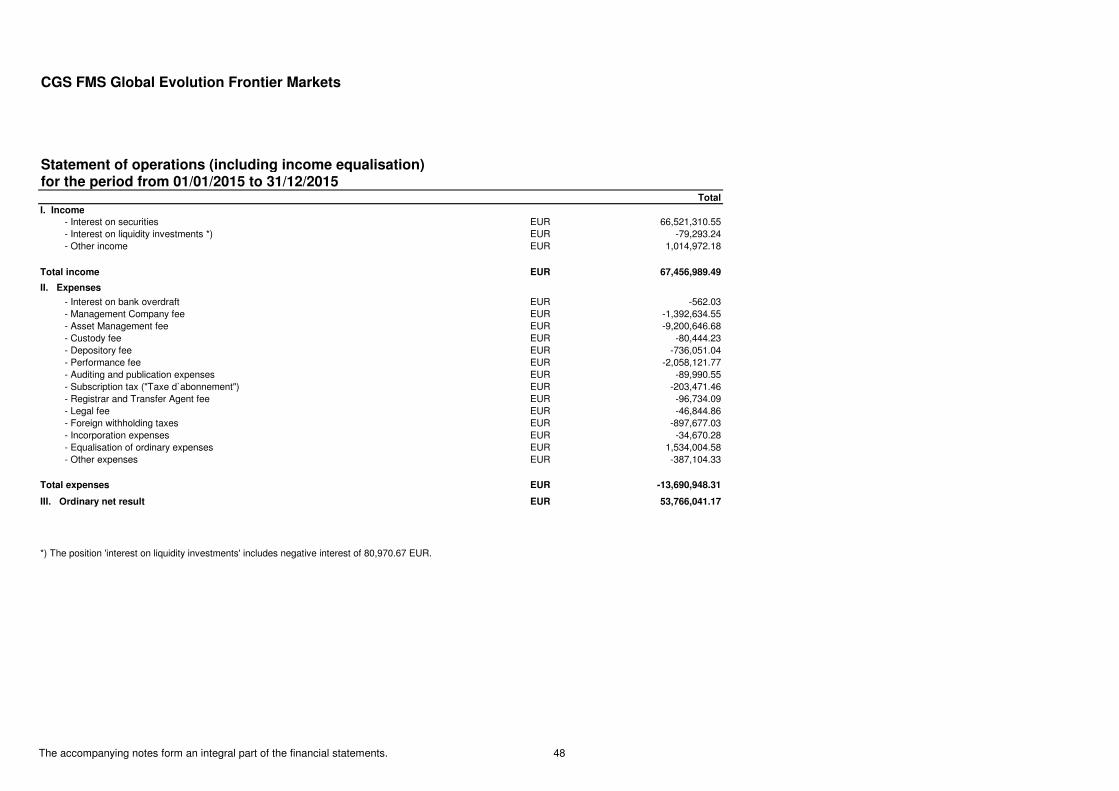

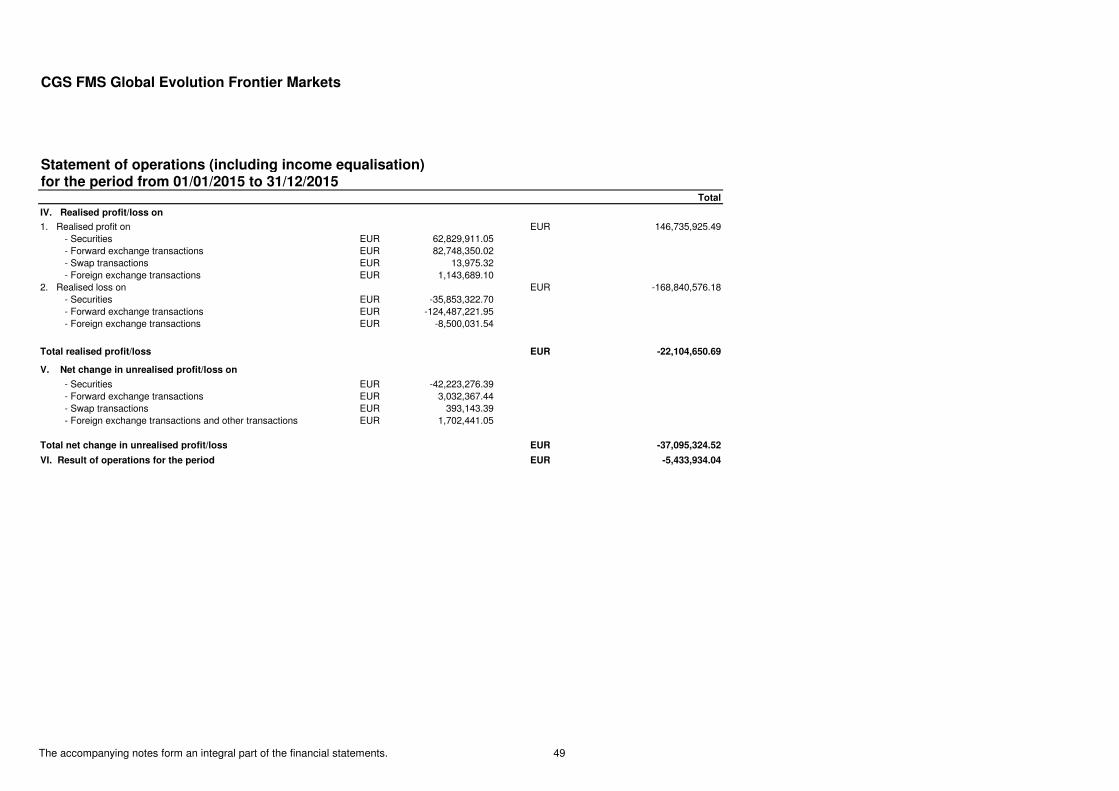

Statement of Operations (including income equalisation) 48 - 49

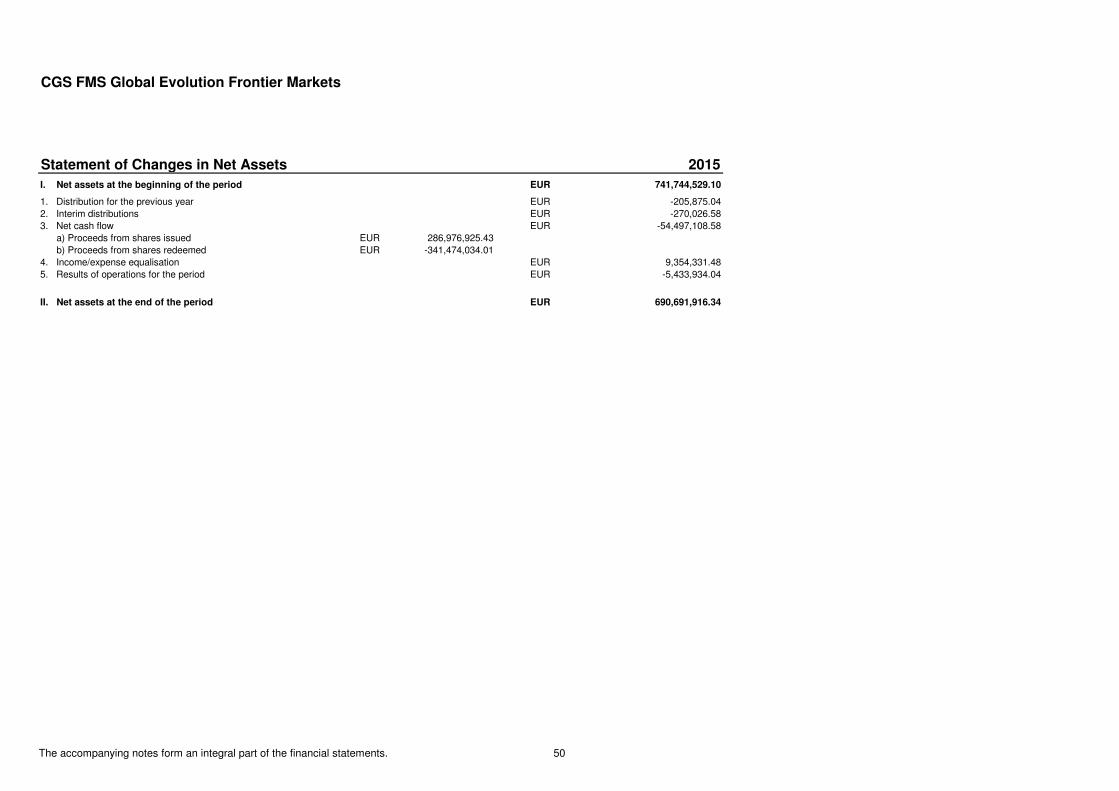

Statement of Changes in Net Assets 50

CGS FMS - Global Evolution EM Debt

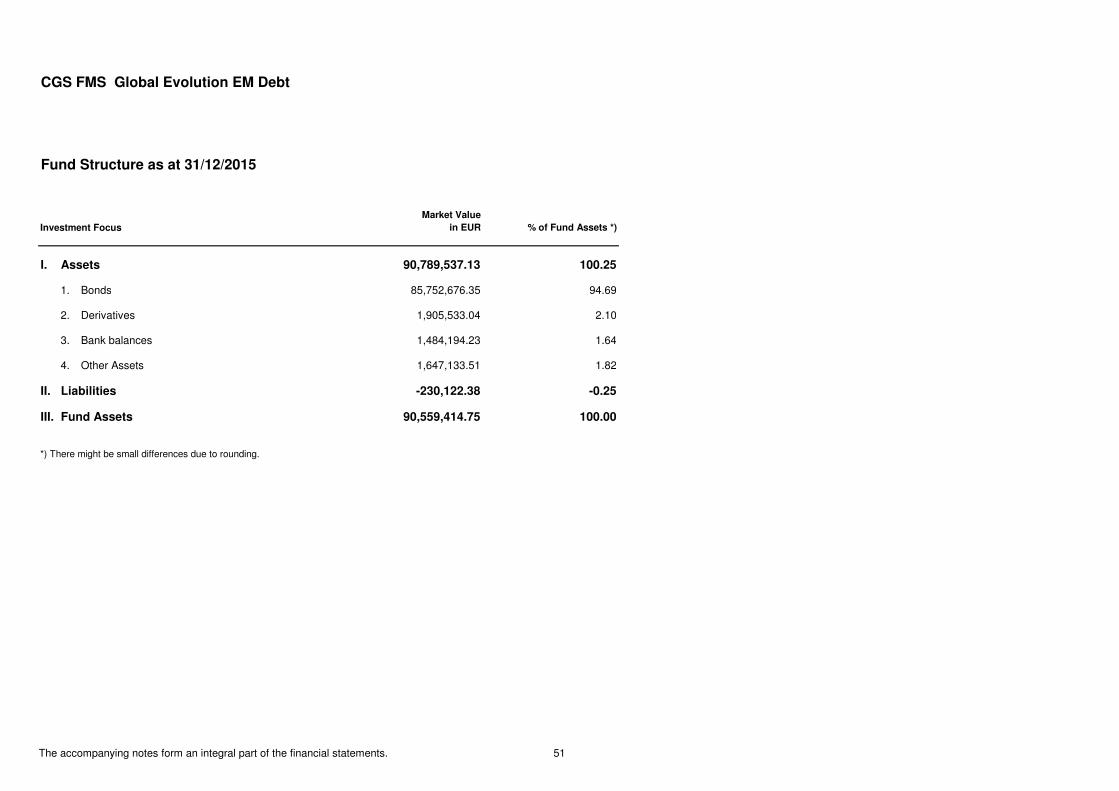

Fund Structure 51

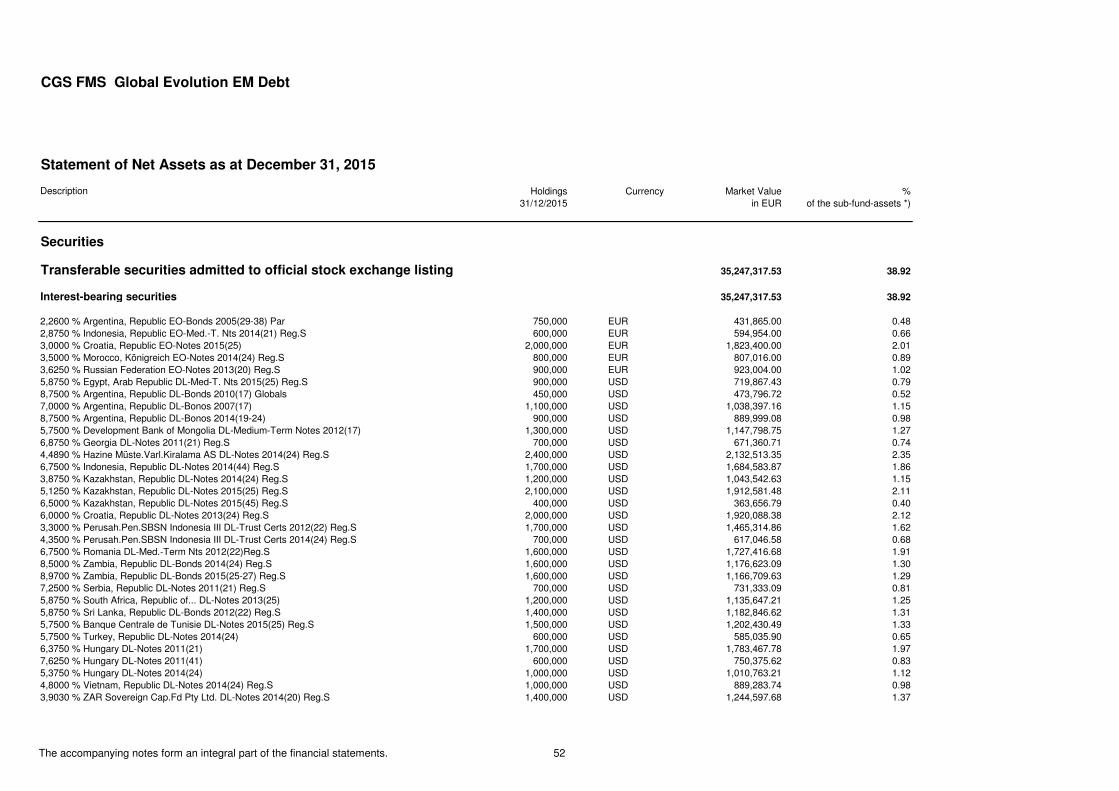

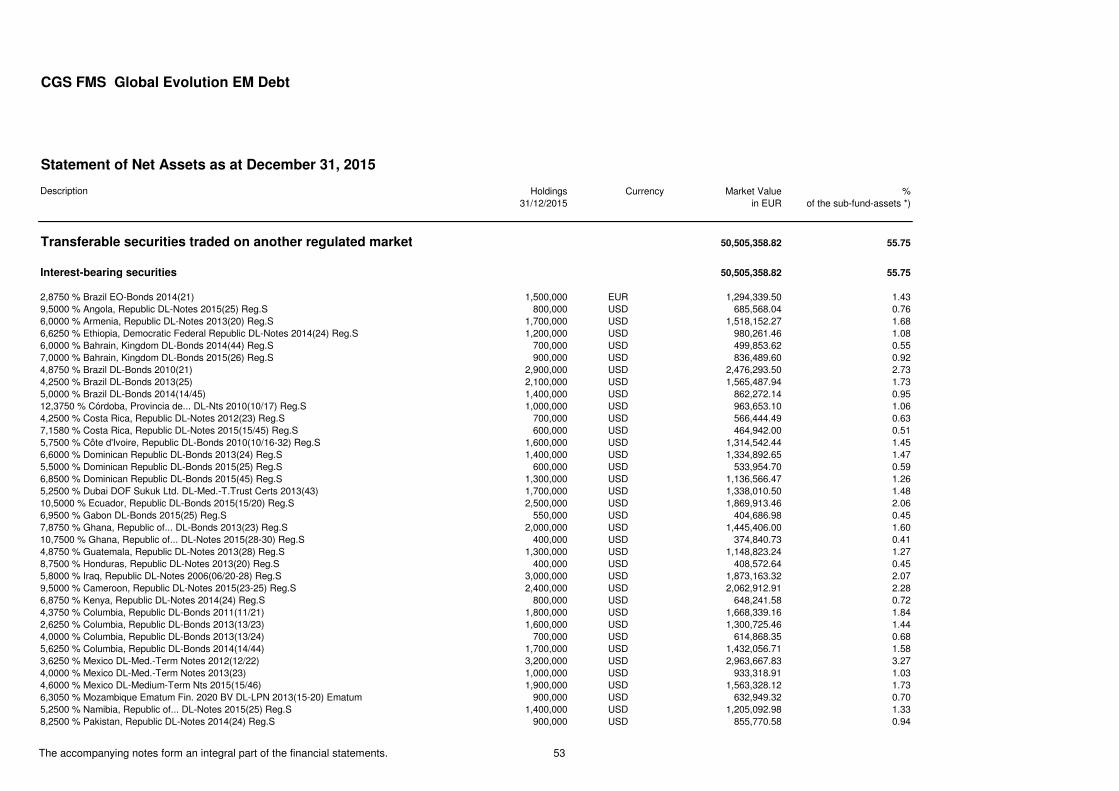

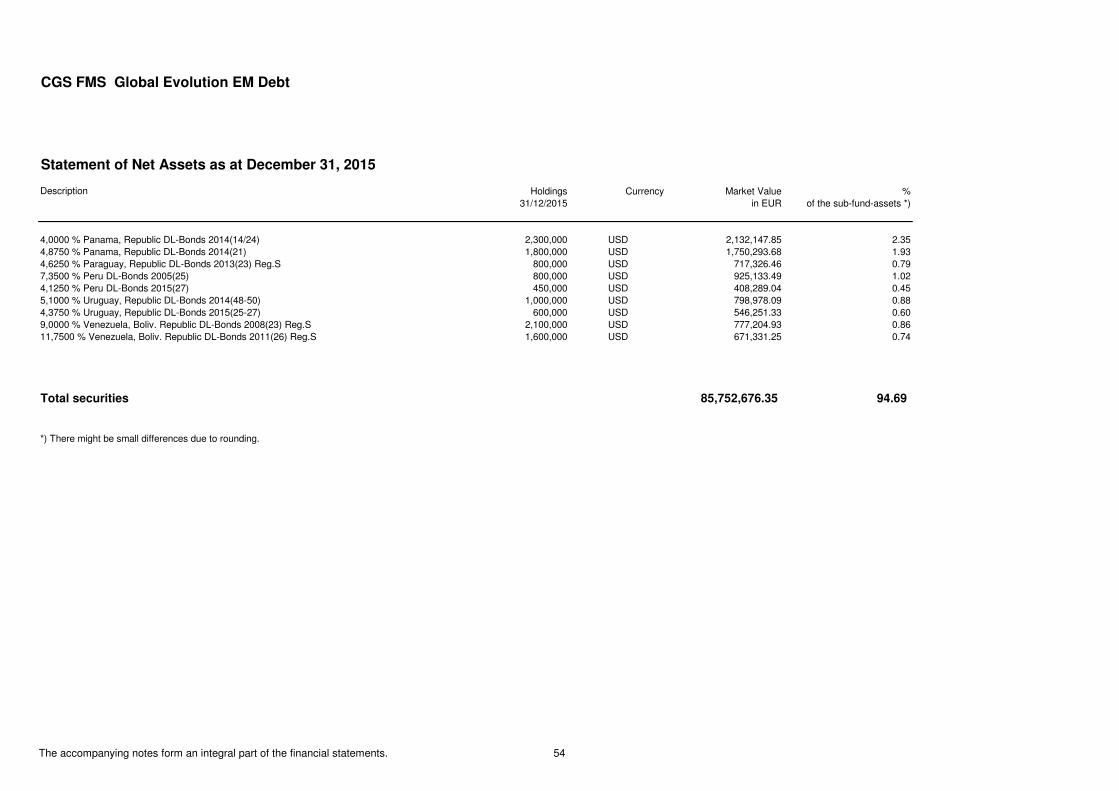

Statement of Securities 52 - 54

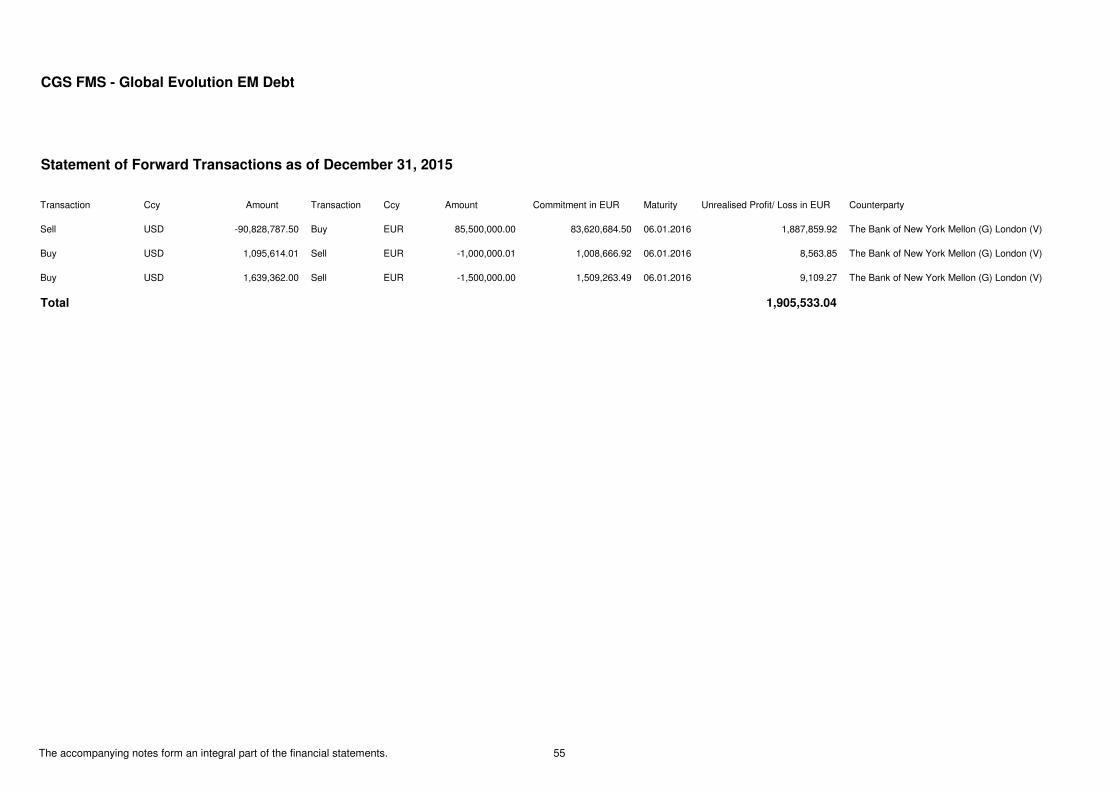

Statement of Forward Transactions 55

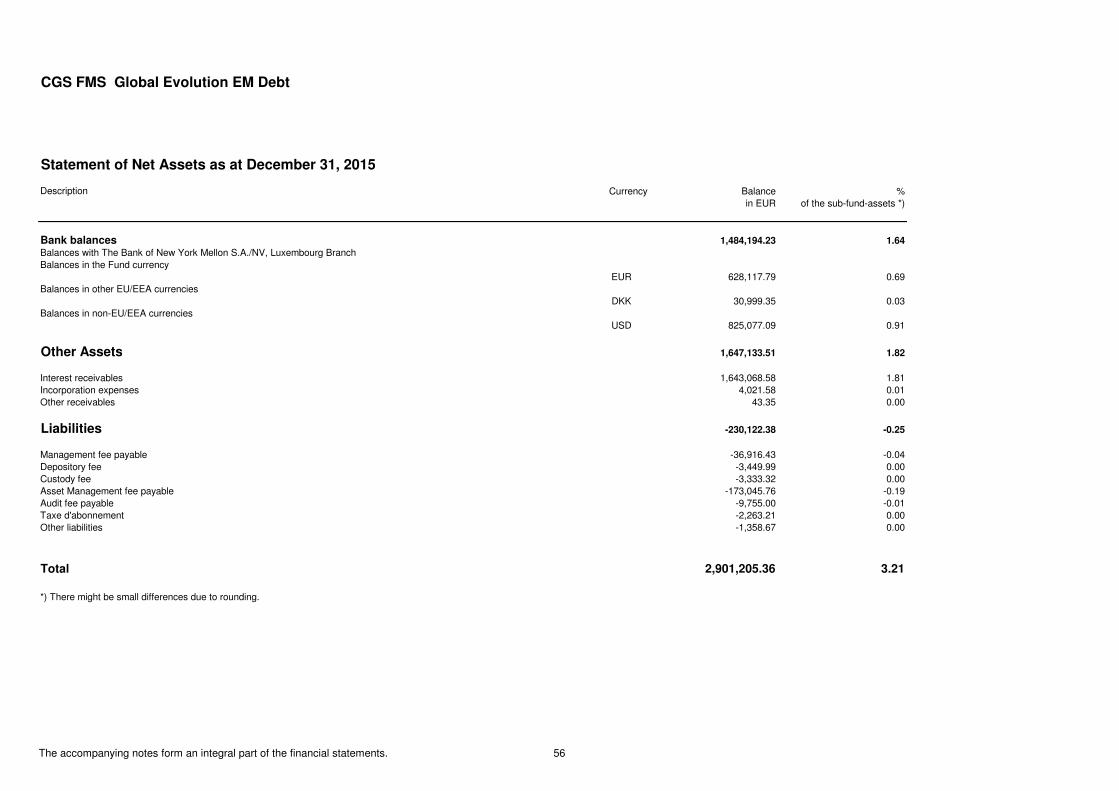

Statement of Bank balances, Other Assets and Liabilities 56

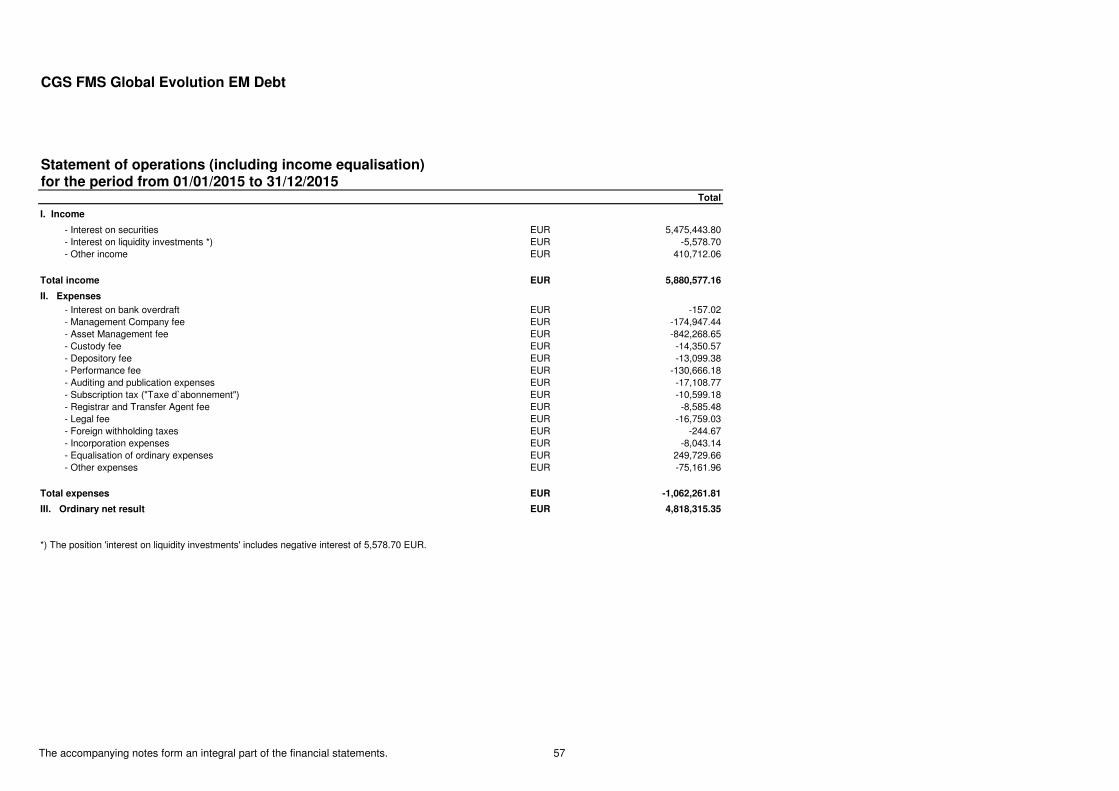

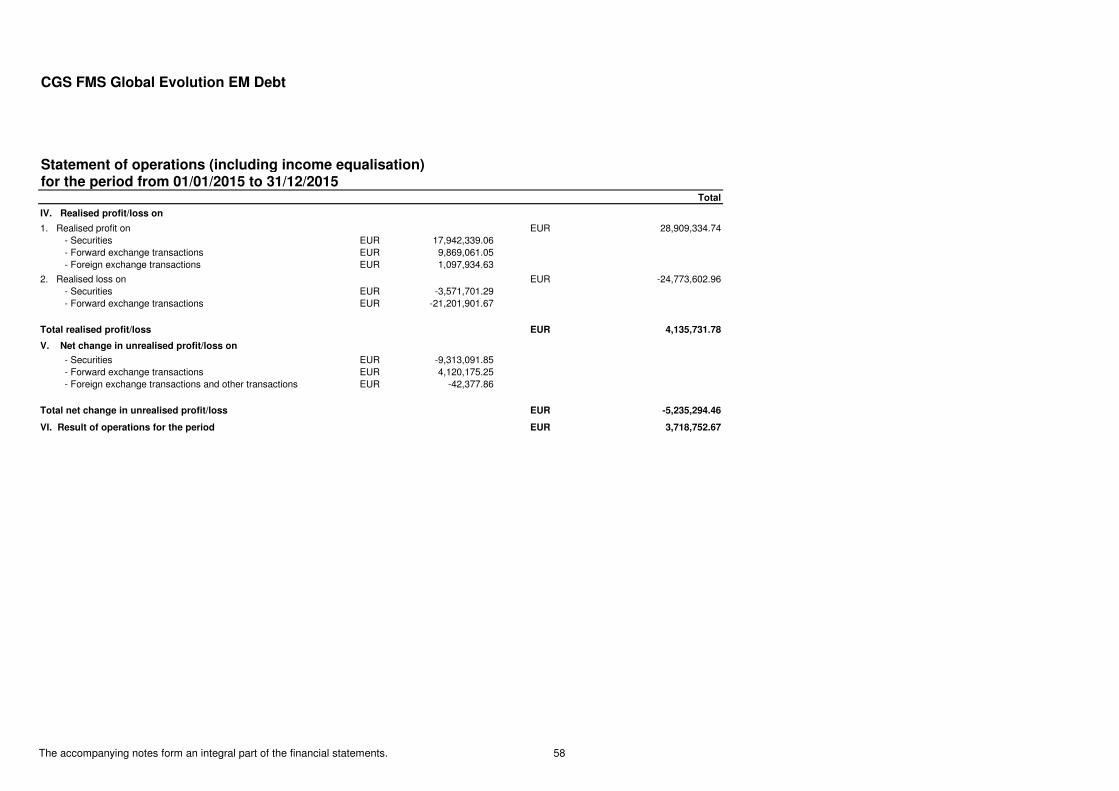

Statement of Operations (including income equalisation) 57 - 58

Statement of Changes in Net Assets 59

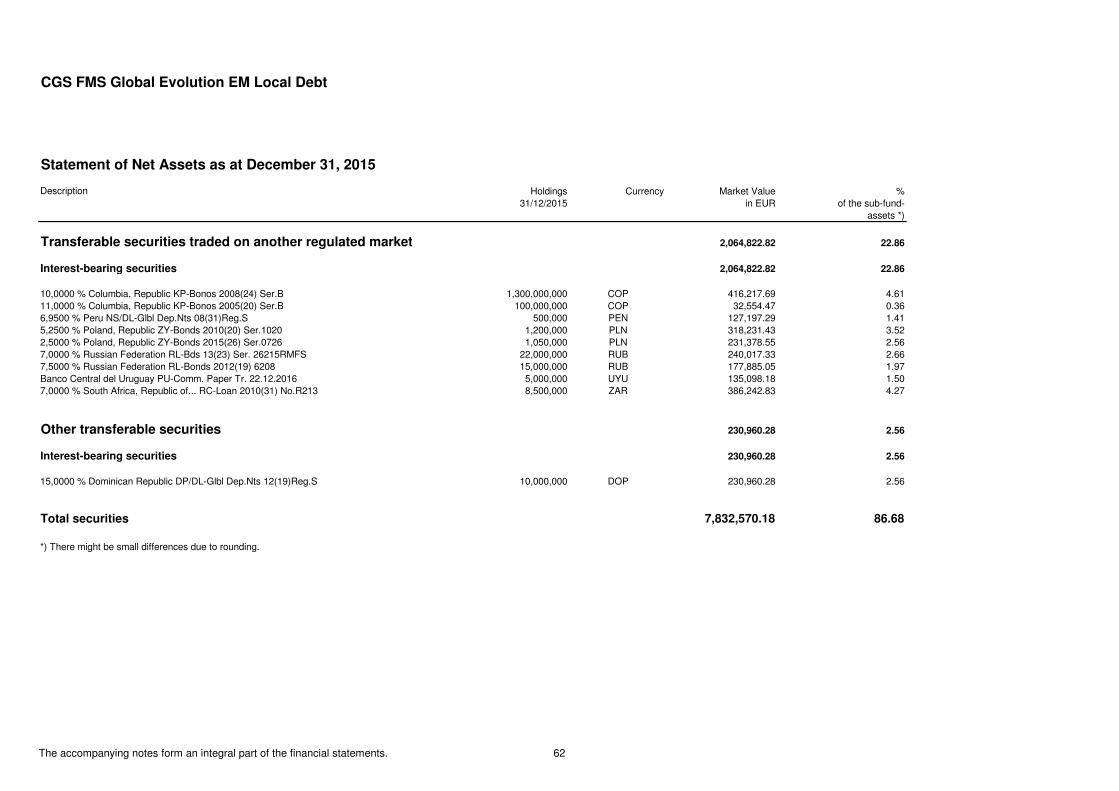

CGS FMS - Global Evolution EM Local Debt

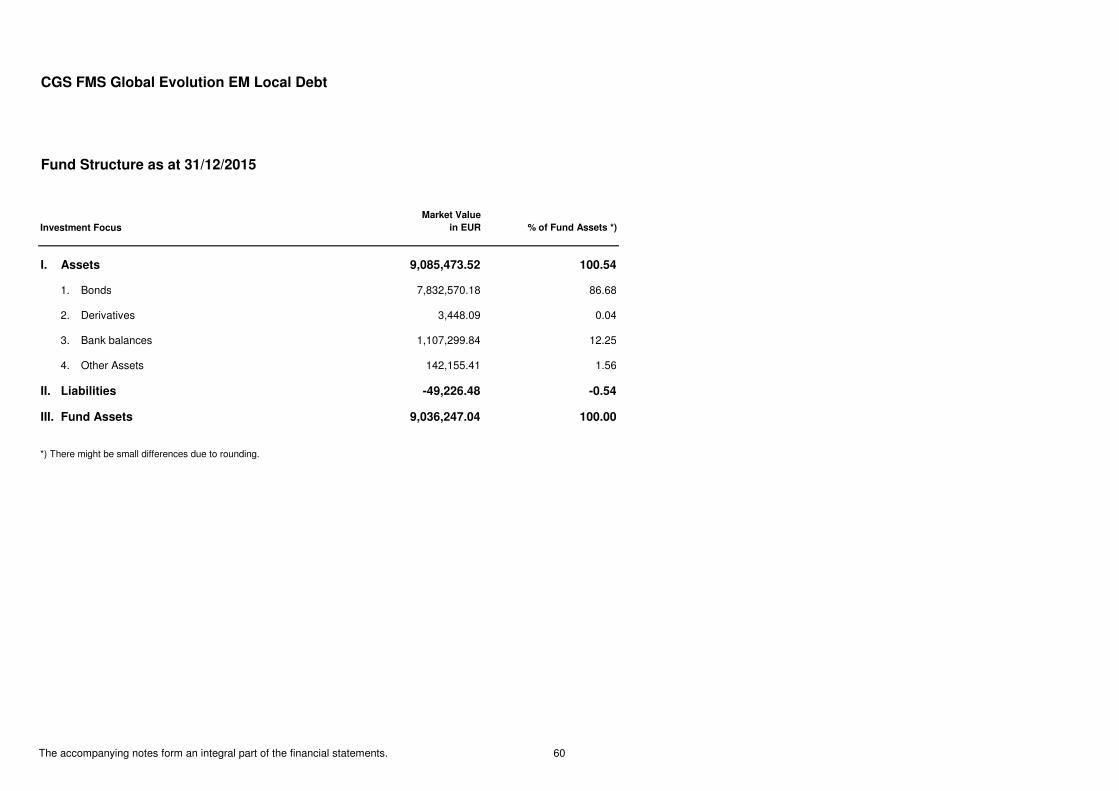

Fund Structure 60

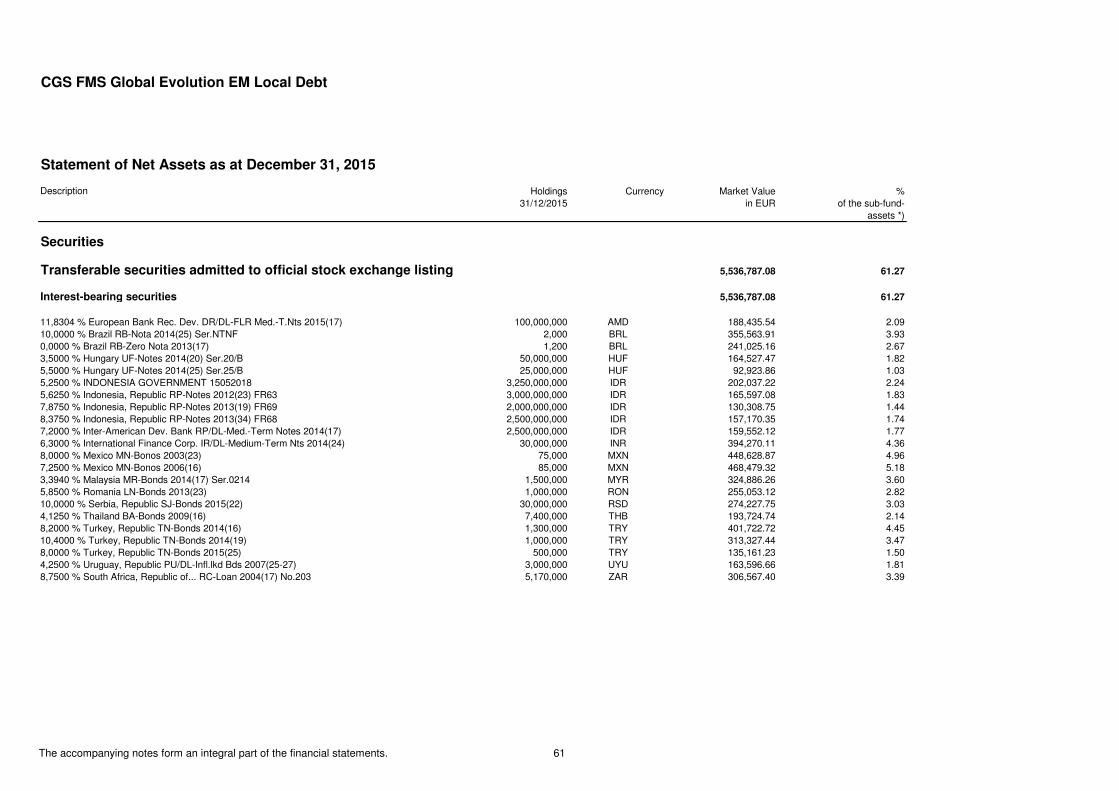

Statement of Securities 61 - 62

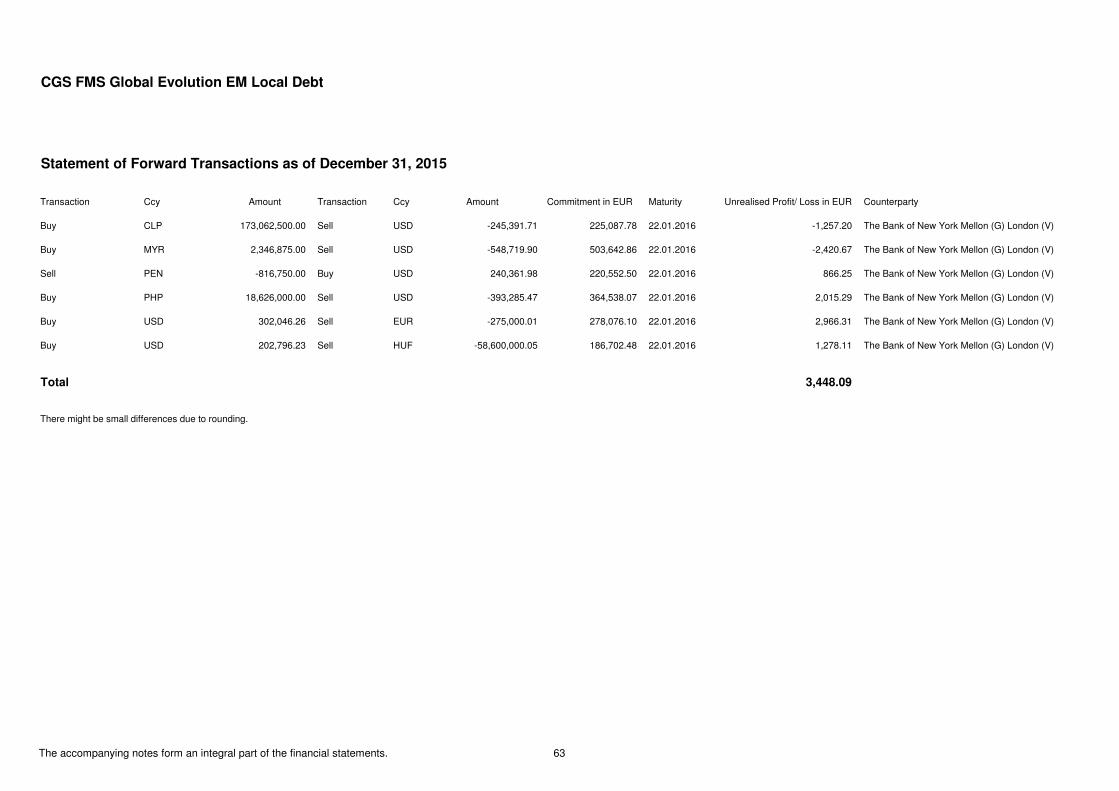

Statement of Forward Transactions 63

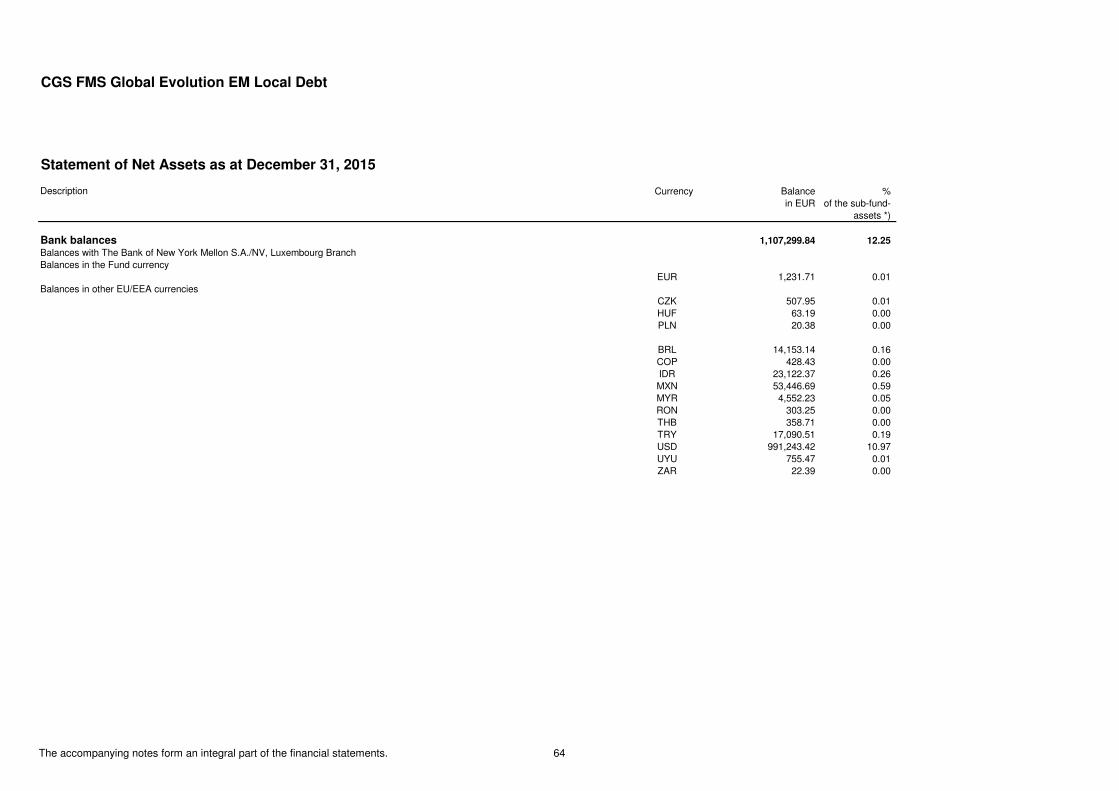

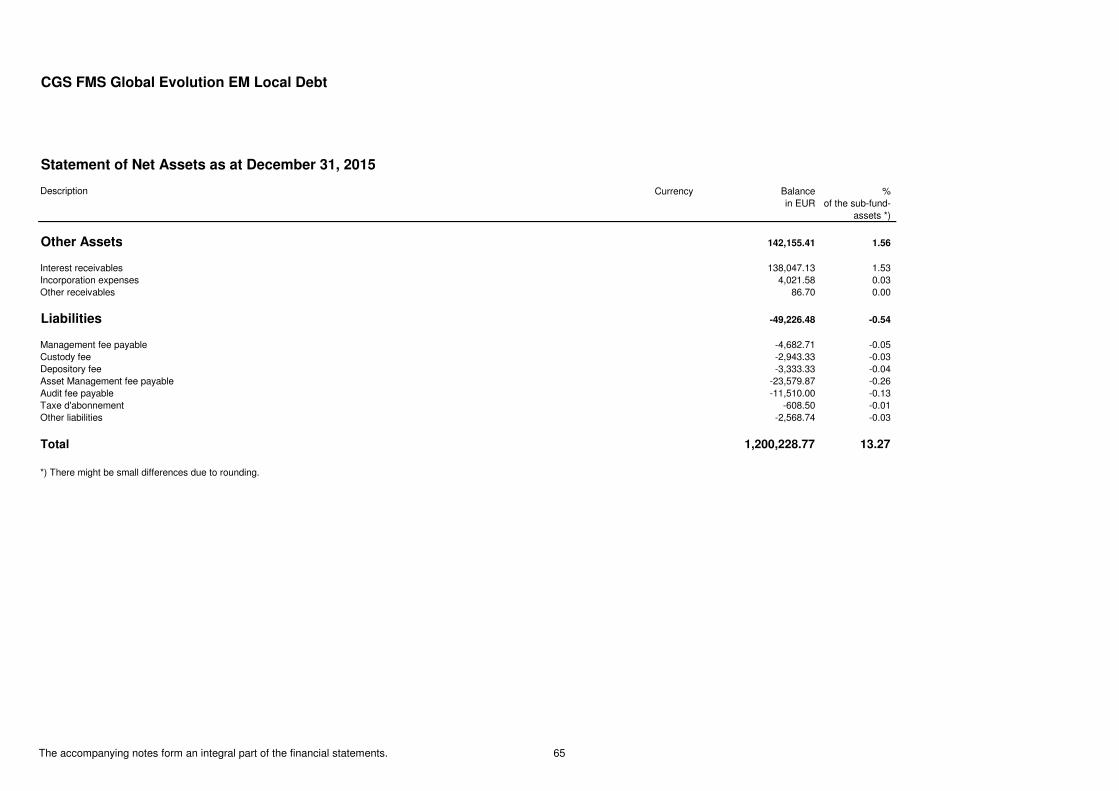

Statement of Bank balances, Other Assets and Liabilities 64 - 65

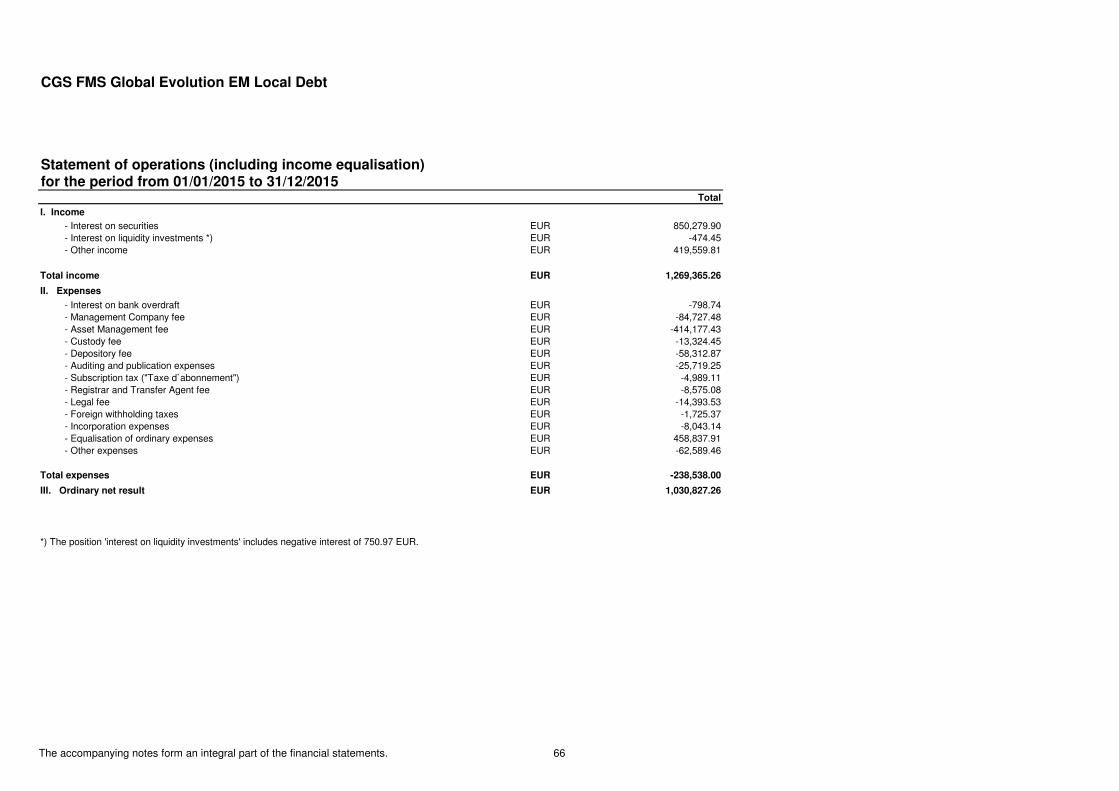

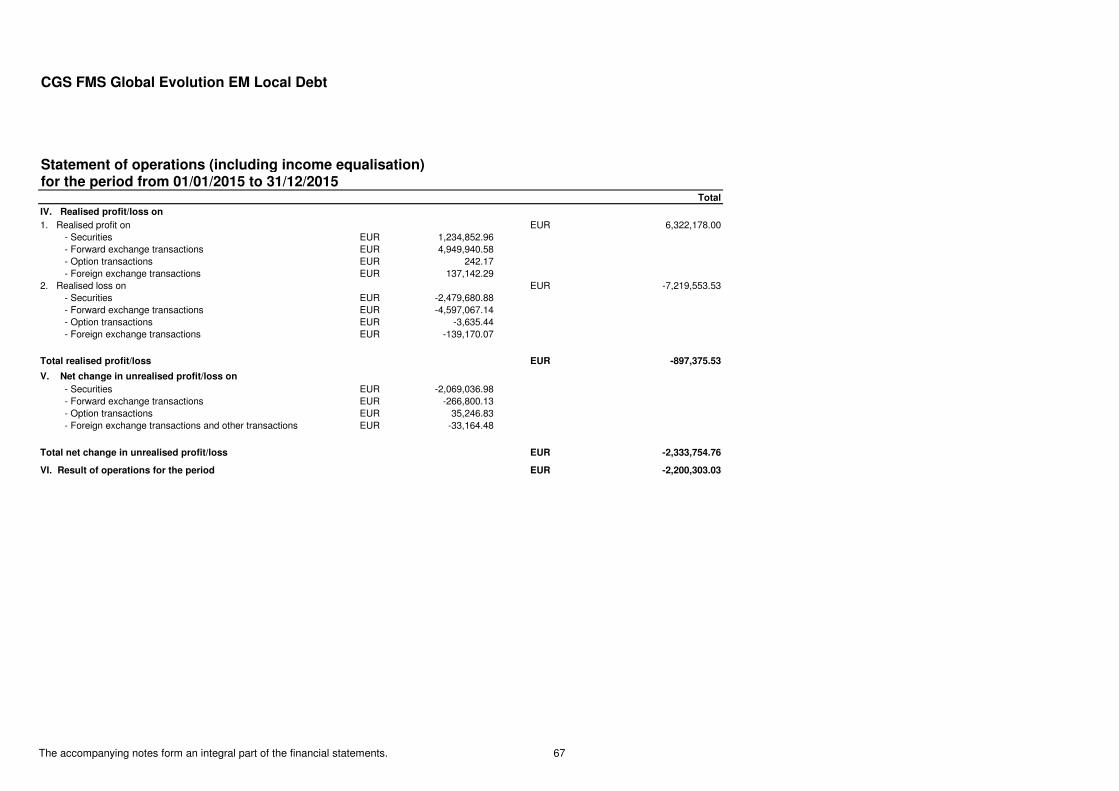

Statement of Operations (including income equalisation) 66- 67

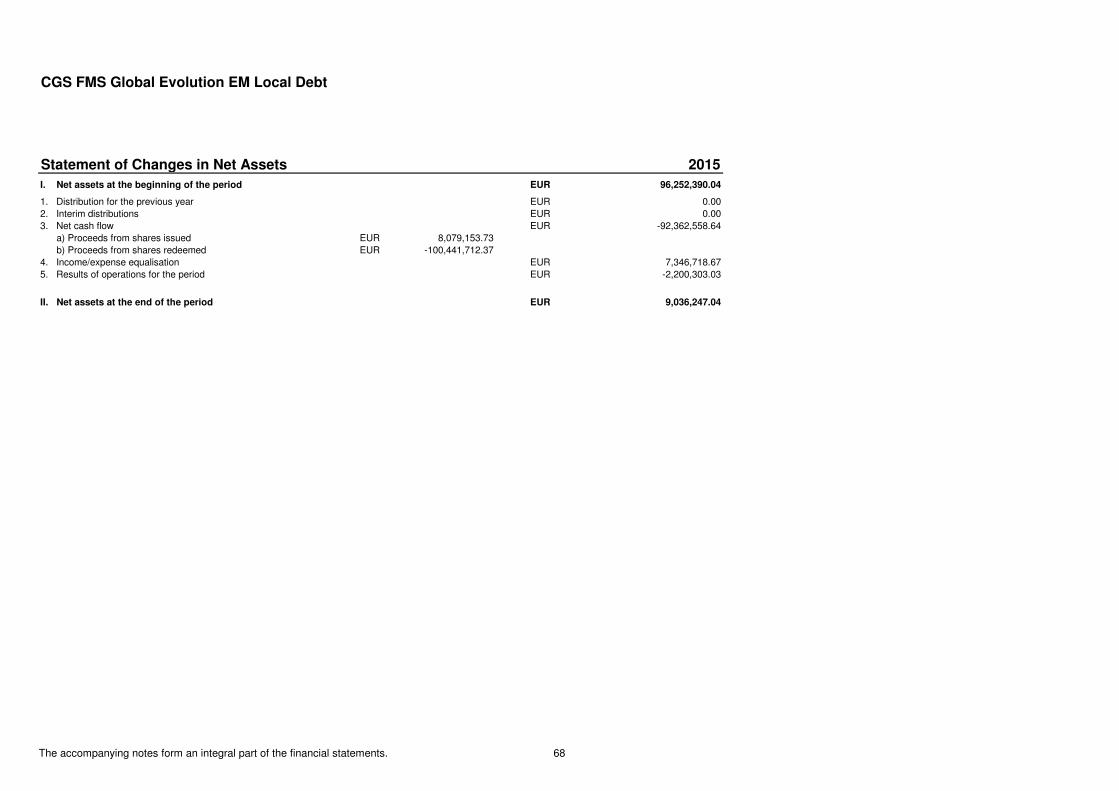

Statement of Changes in Net Assets 68

4

CGS FMS

Table of Contents

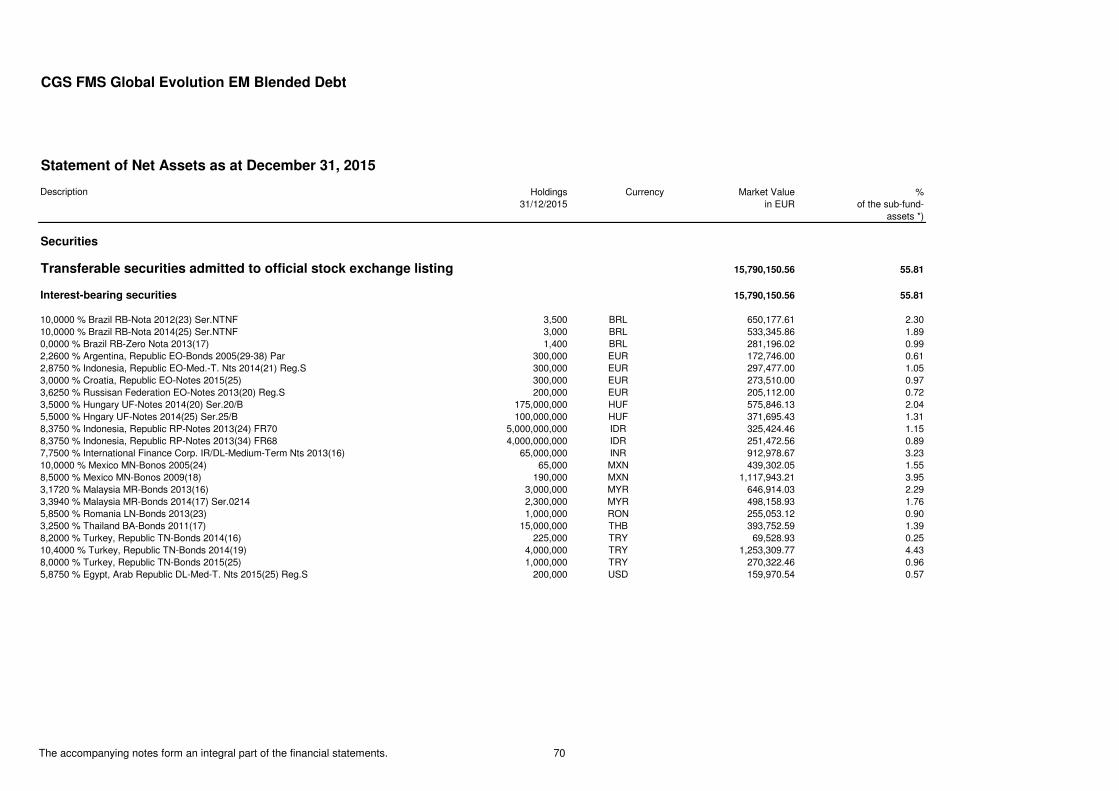

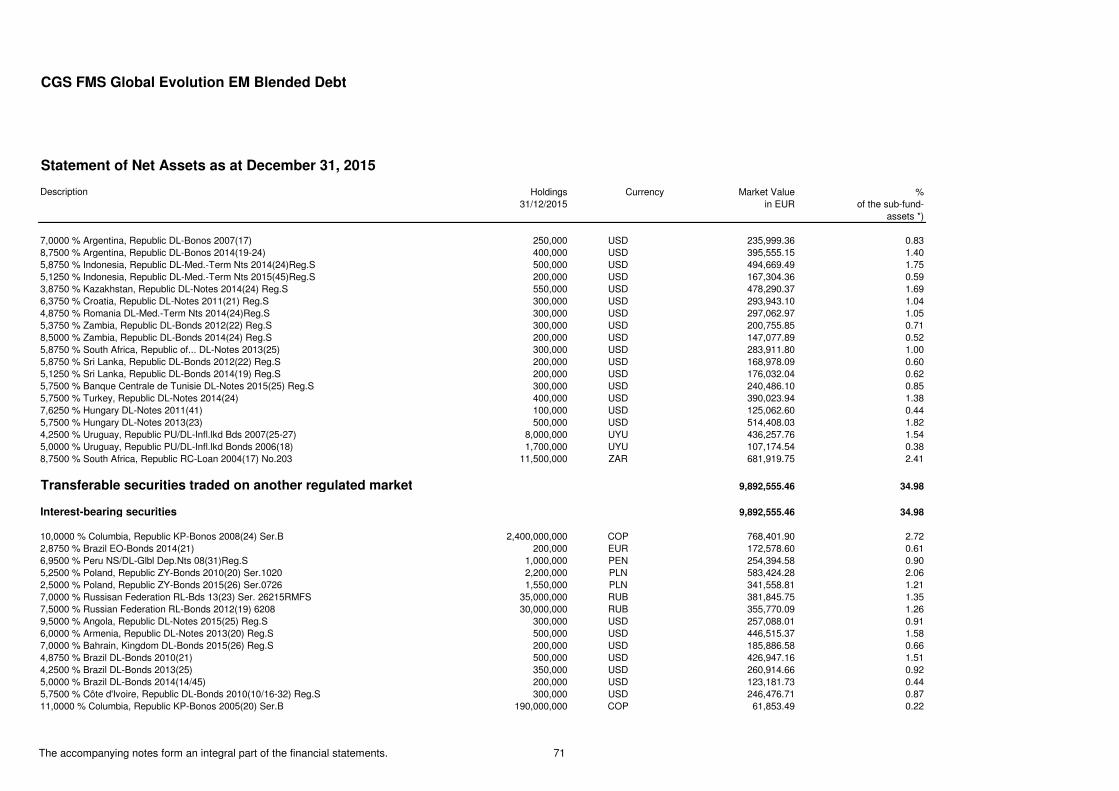

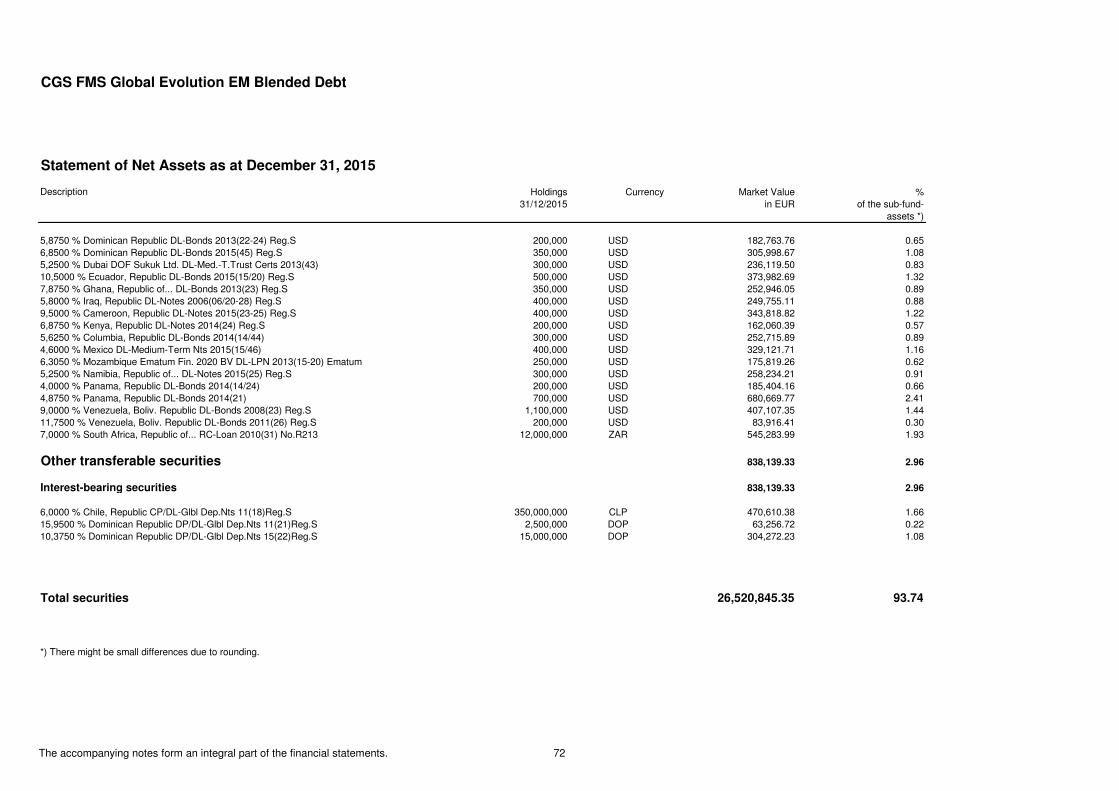

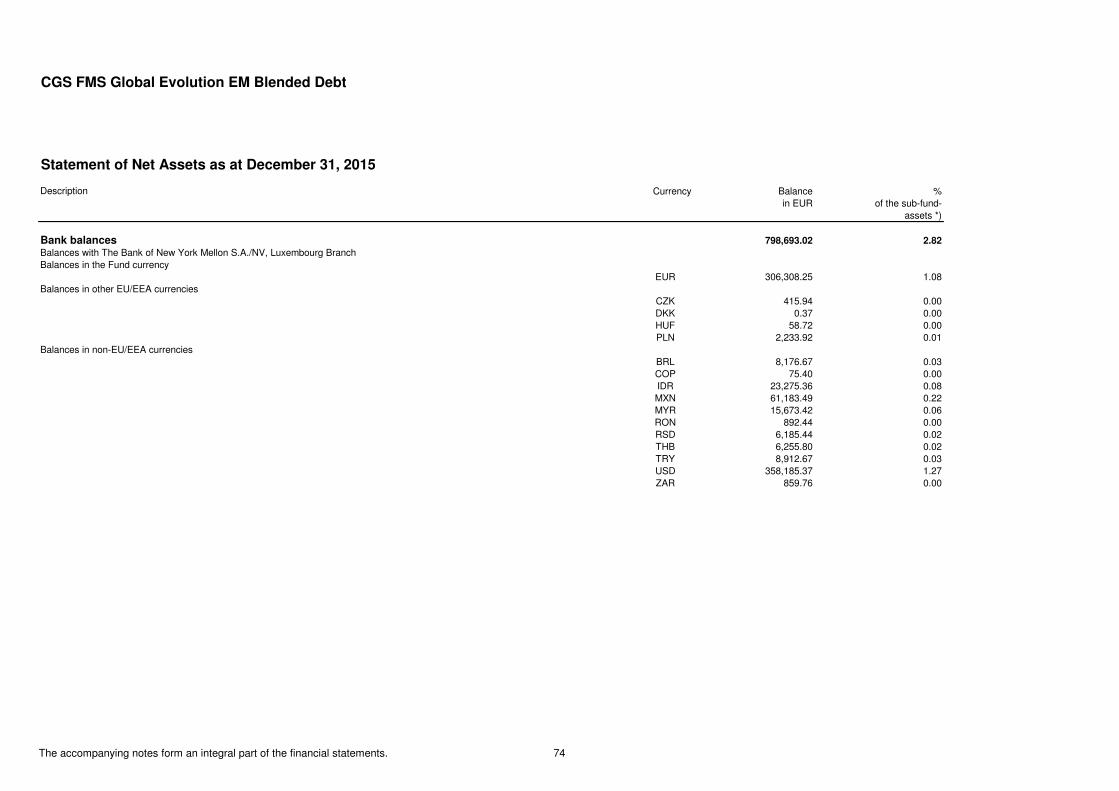

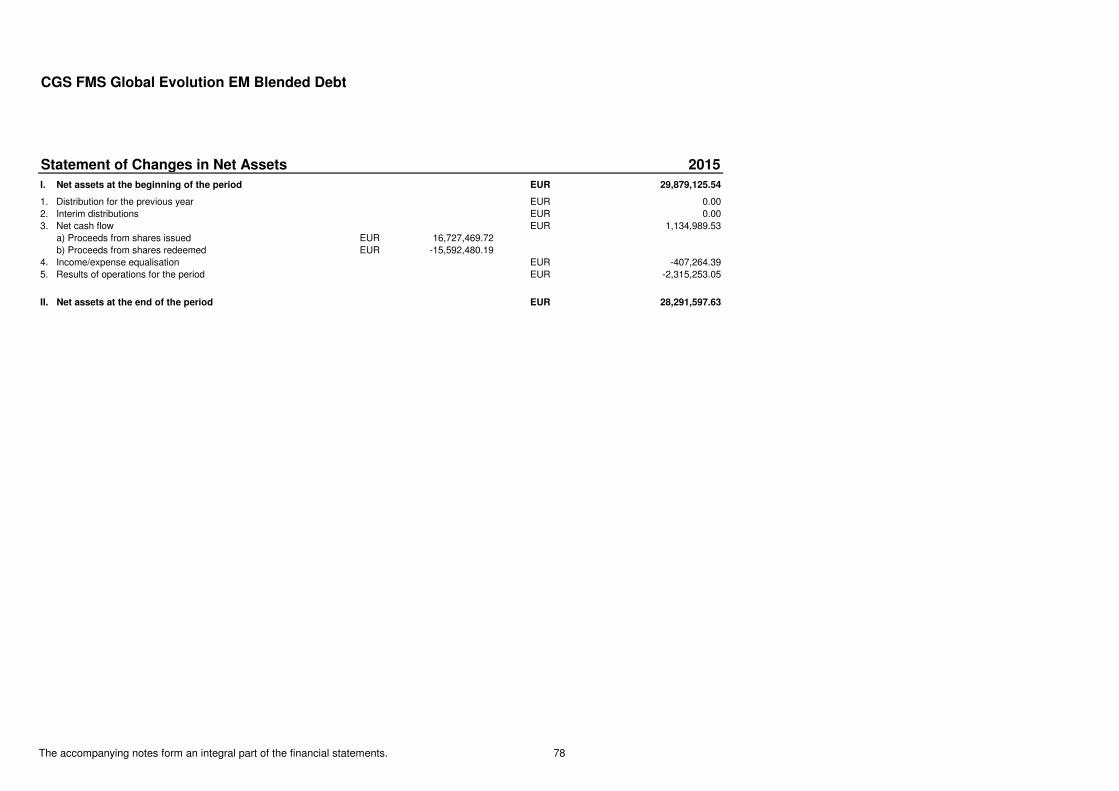

CGS FMS - Global Evolution EM Blended Debt

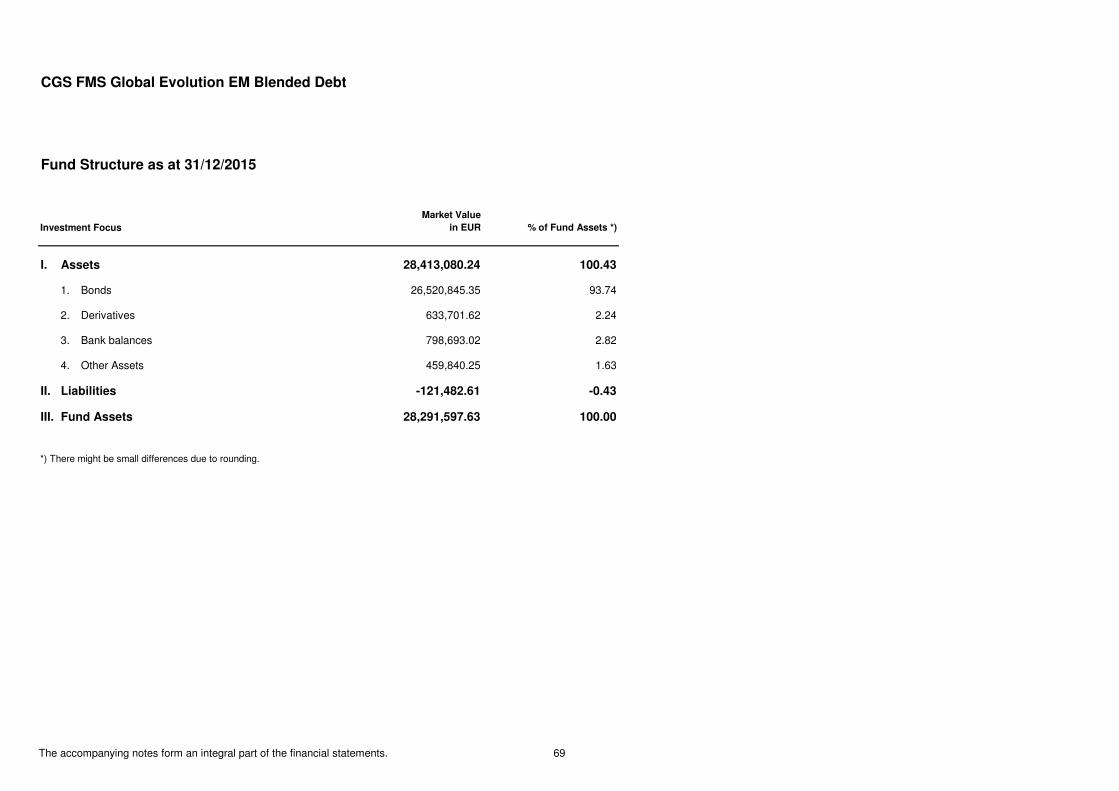

Fund Structure 69

Statement of Securities 70 - 72

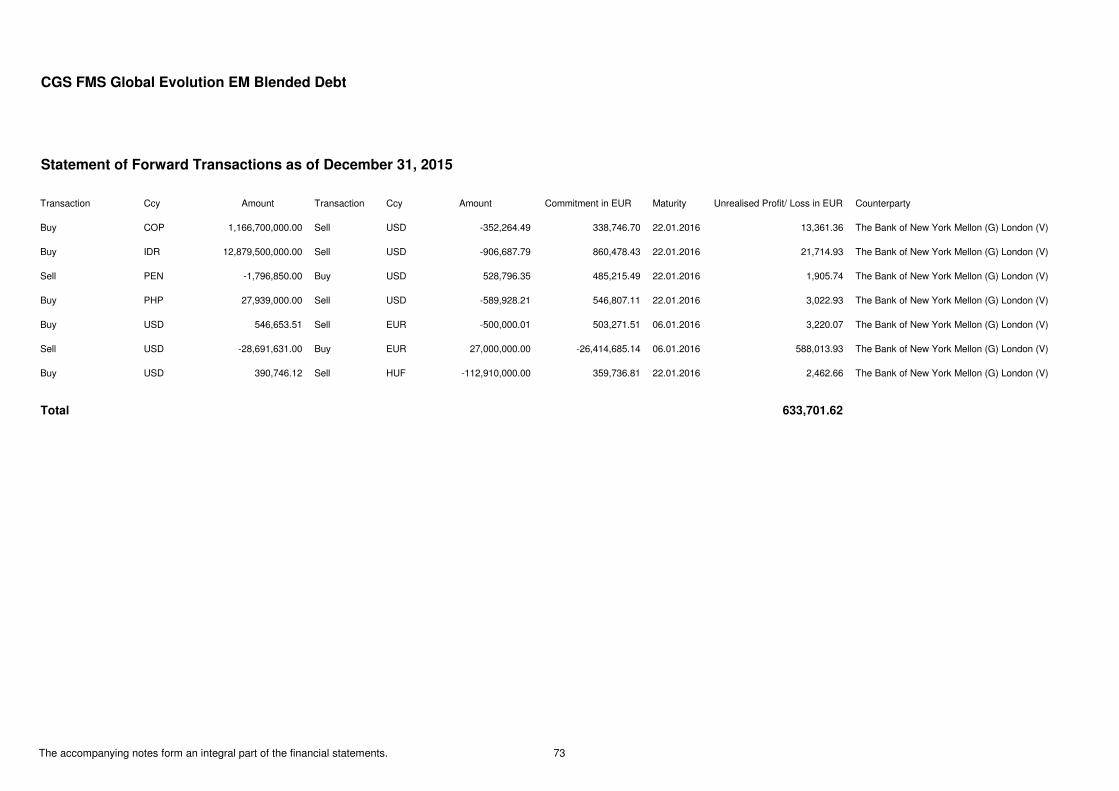

Statement of Forward Transactions 73

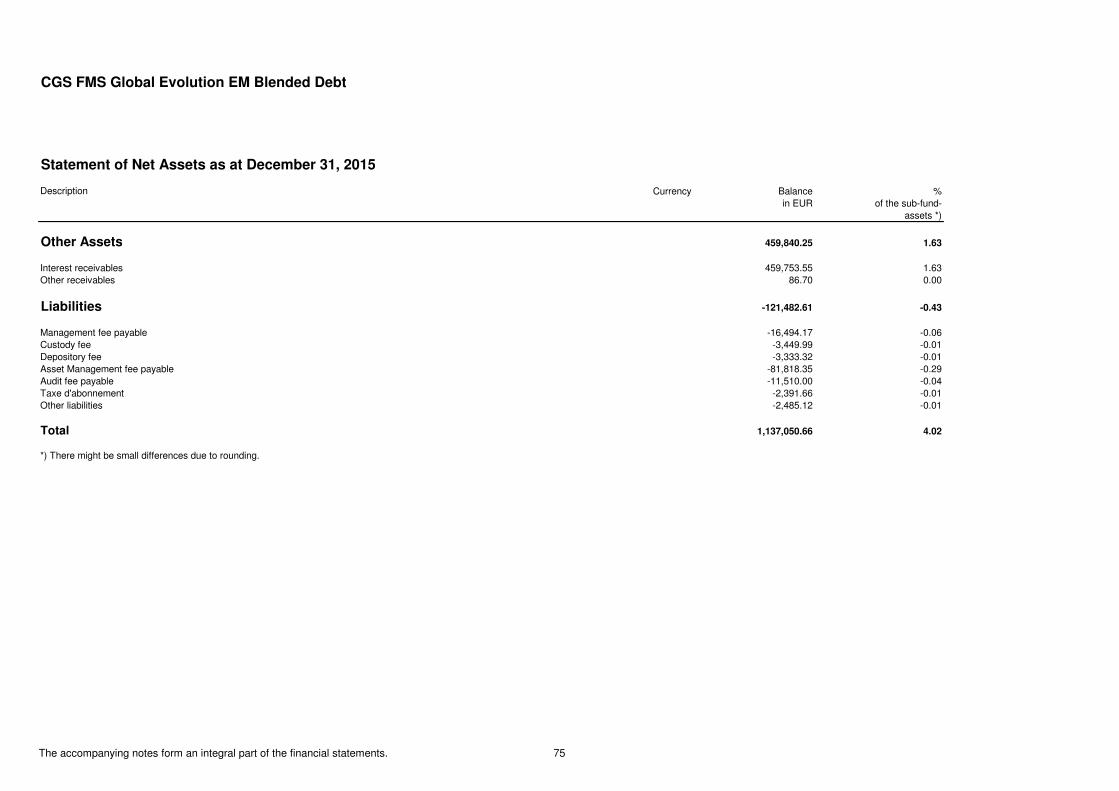

Statement of Bank balances, Other Assets and Liabilities 74 - 75

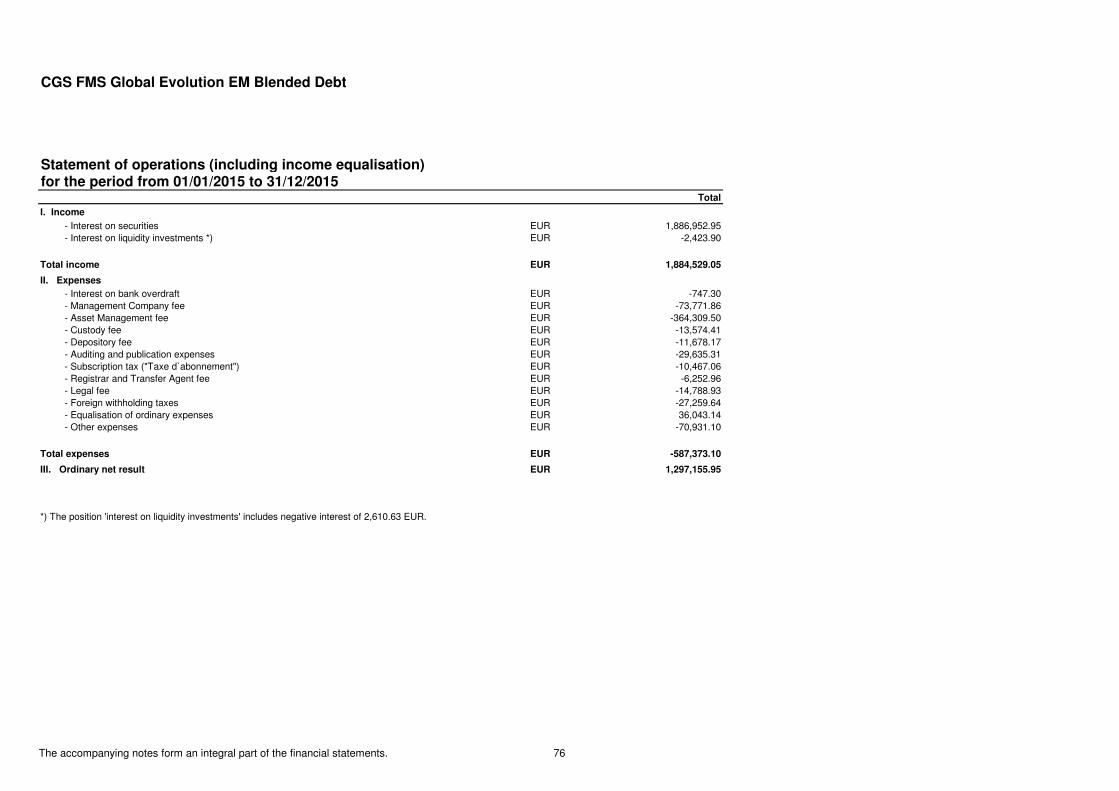

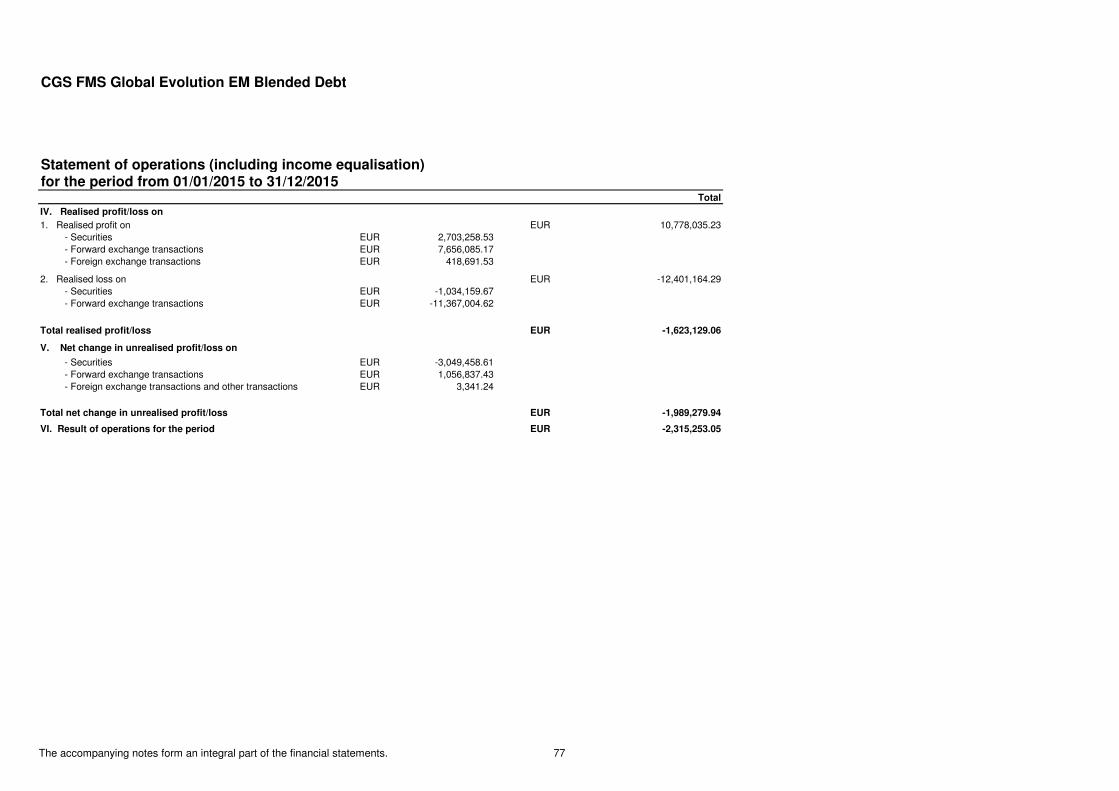

Statement of Operations (including income equalisation) 76 - 77

Statement of Changes in Net Assets 78

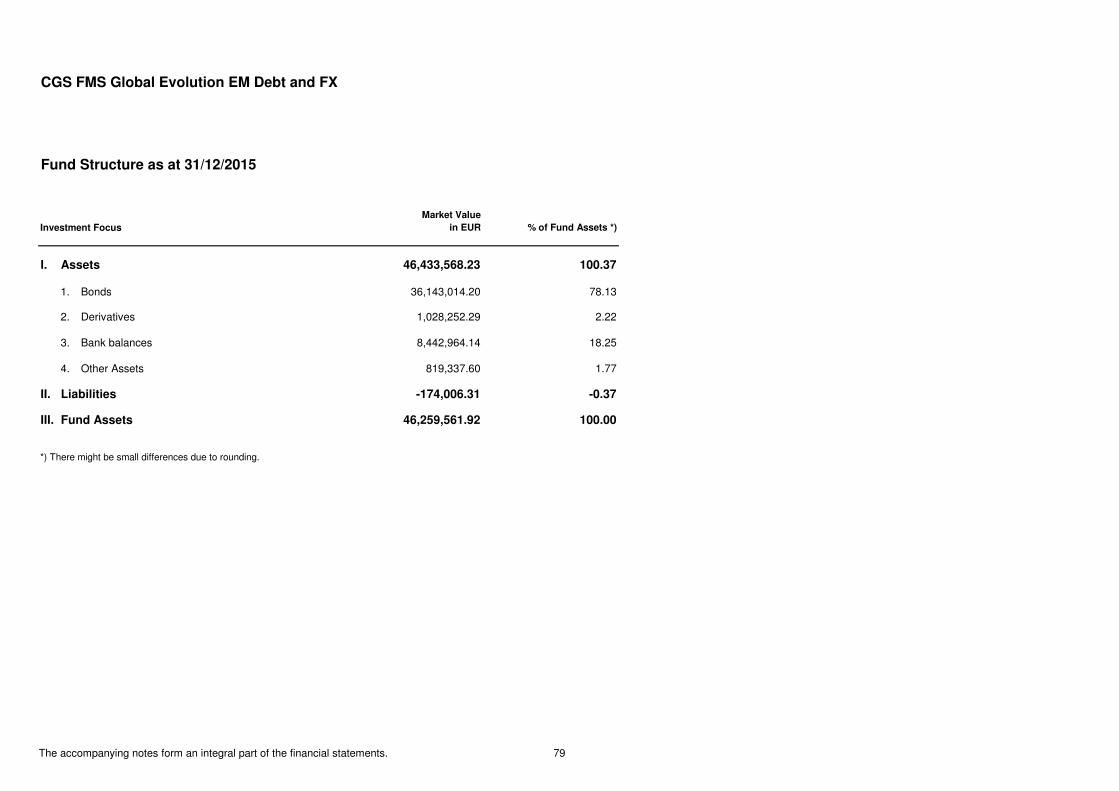

CGS FMS - Global Evolution EM Debt and FX

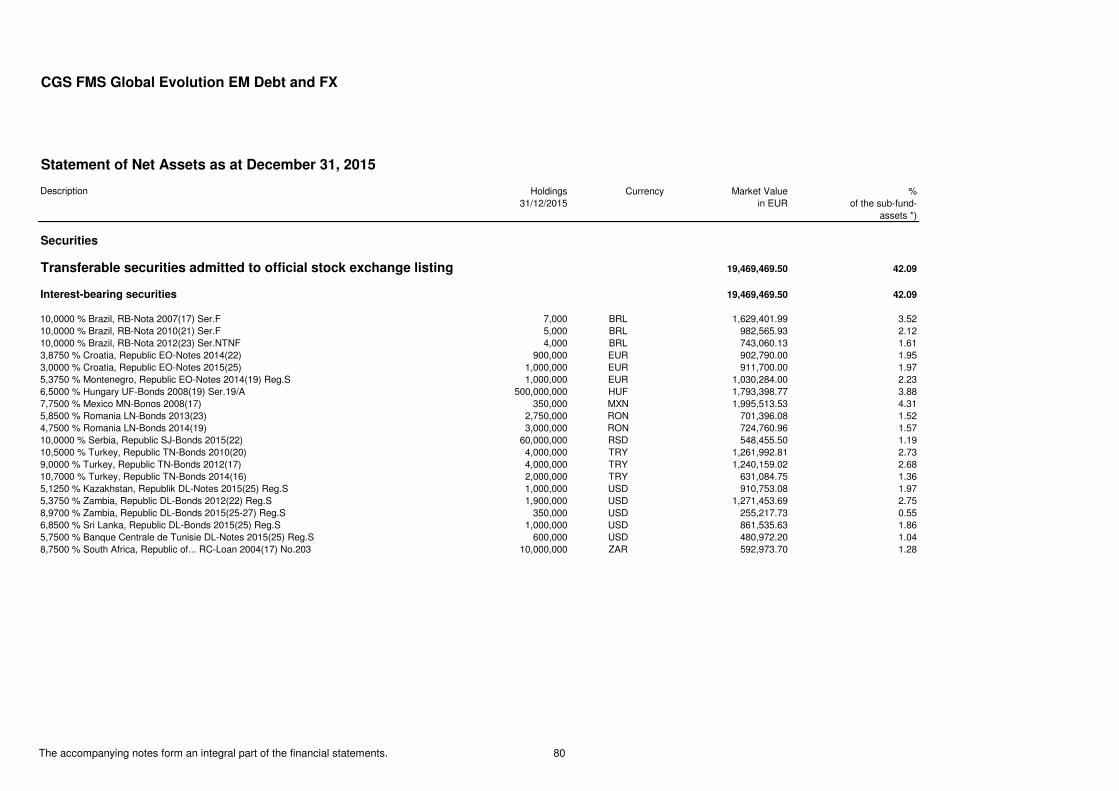

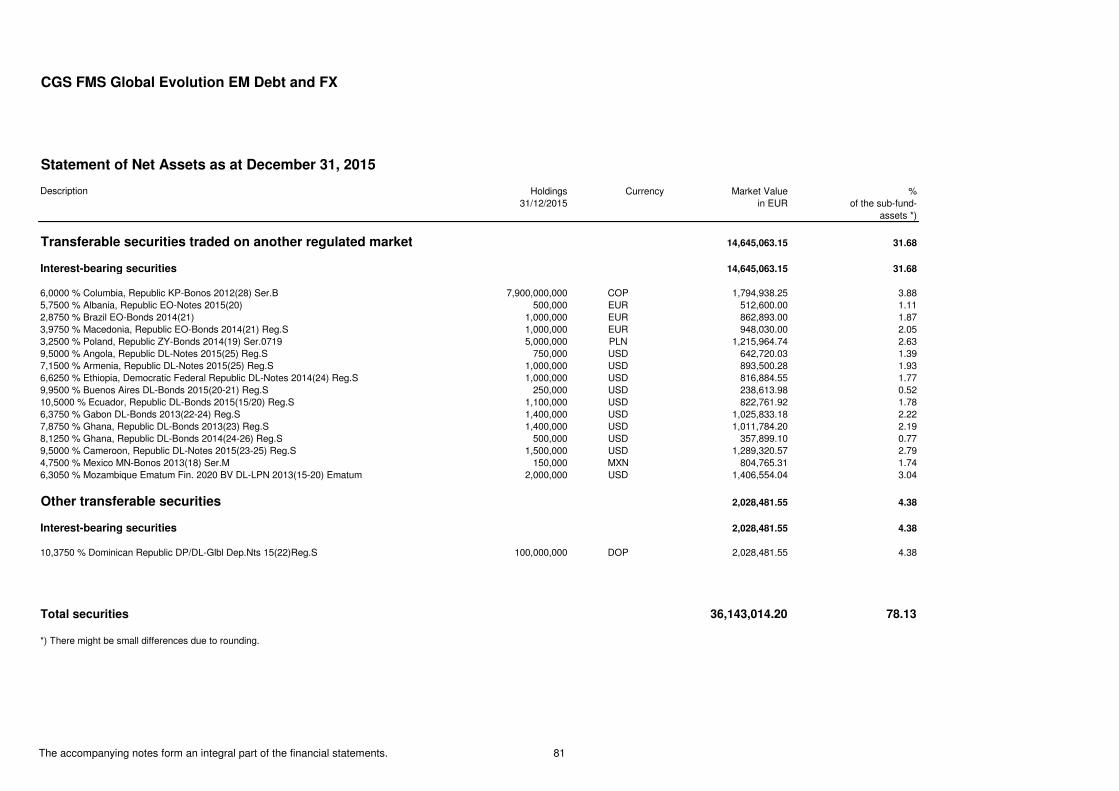

Fund Structure 79

Statement of Securities 80 - 81

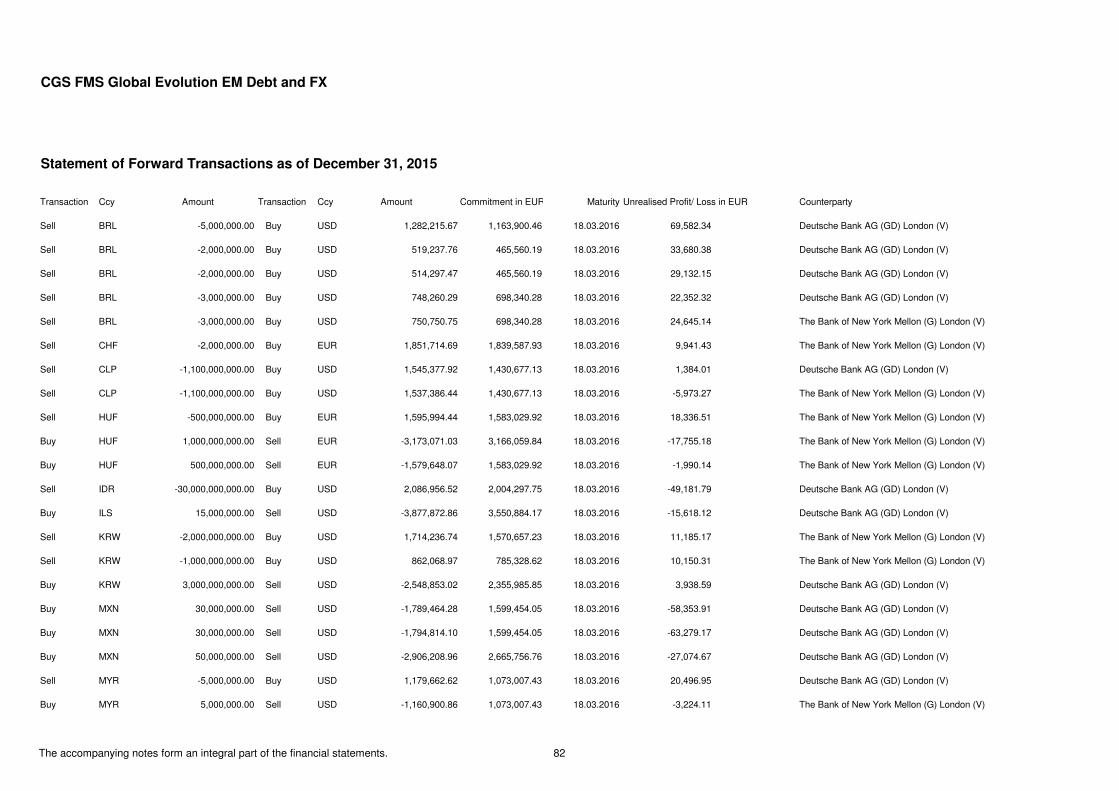

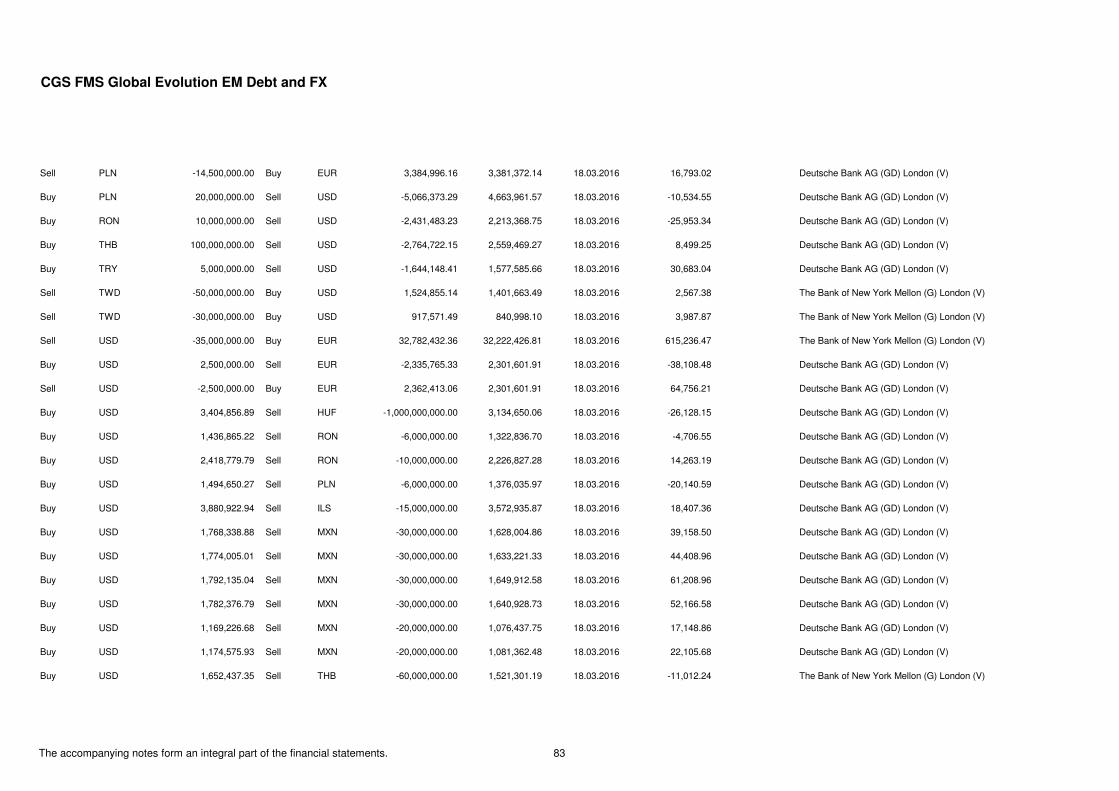

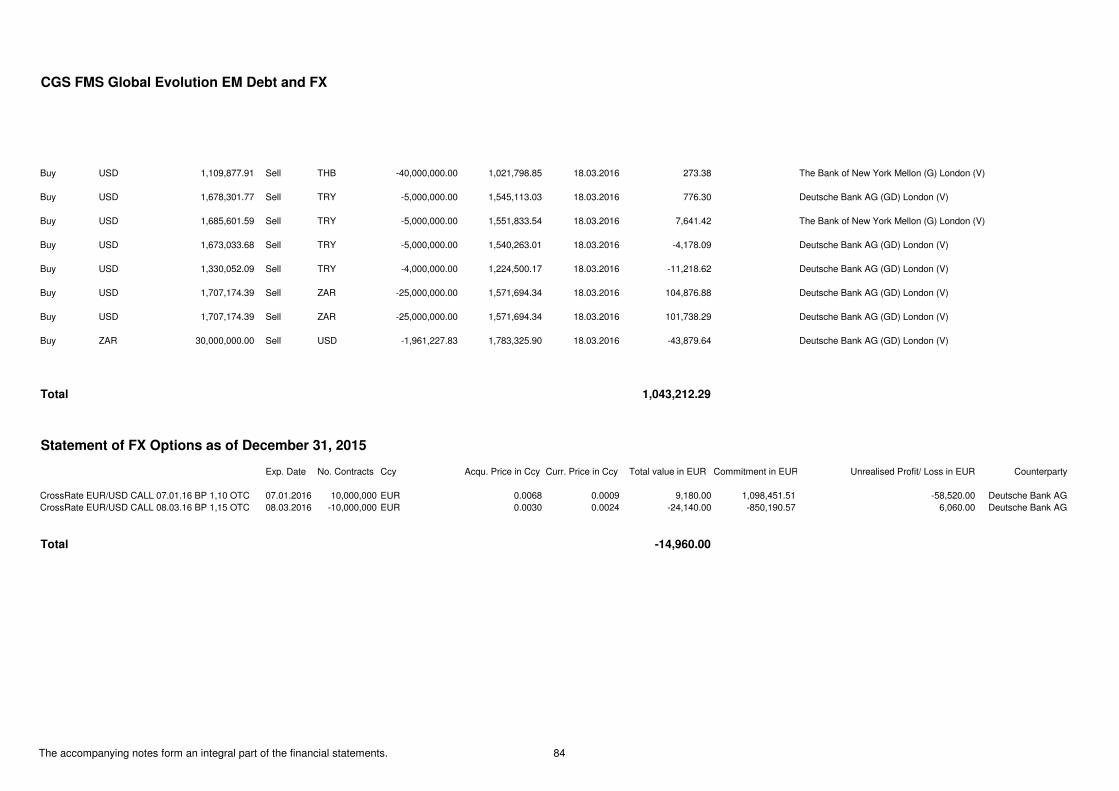

Statement of Forward Transactions 82 - 84

Statement of FX Options 84

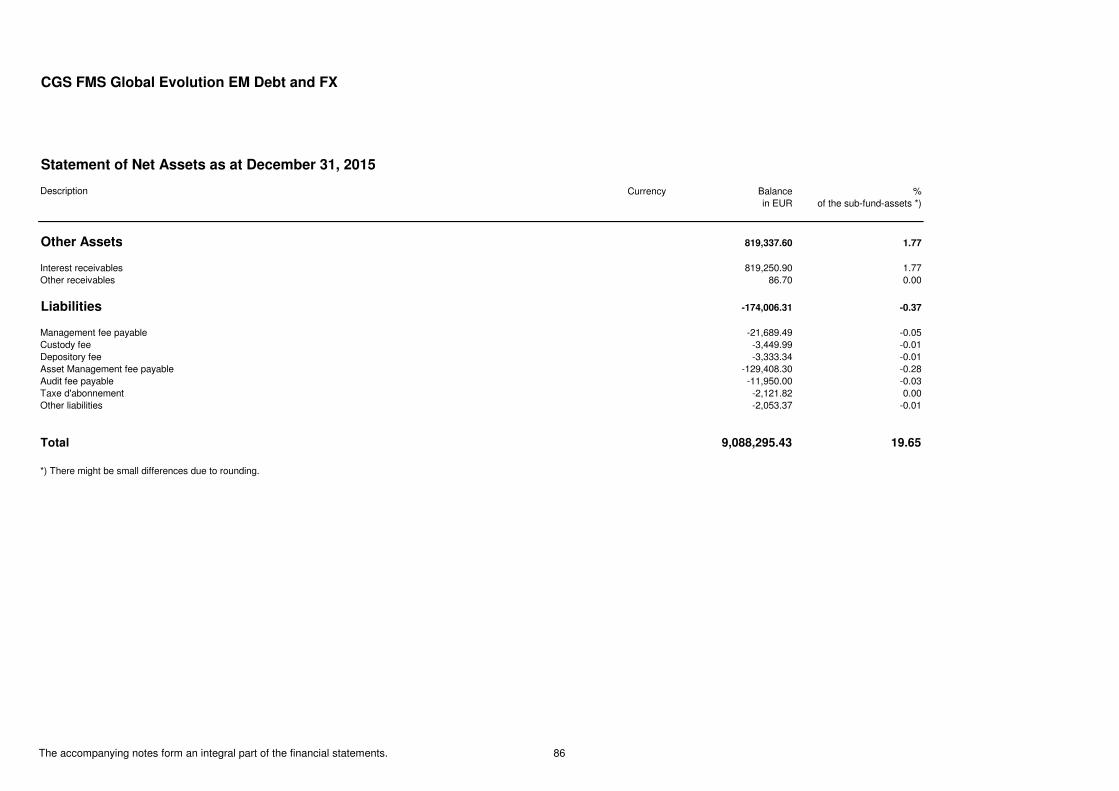

Statement of Bank balances, Other Assets and Liabilities 85 - 86

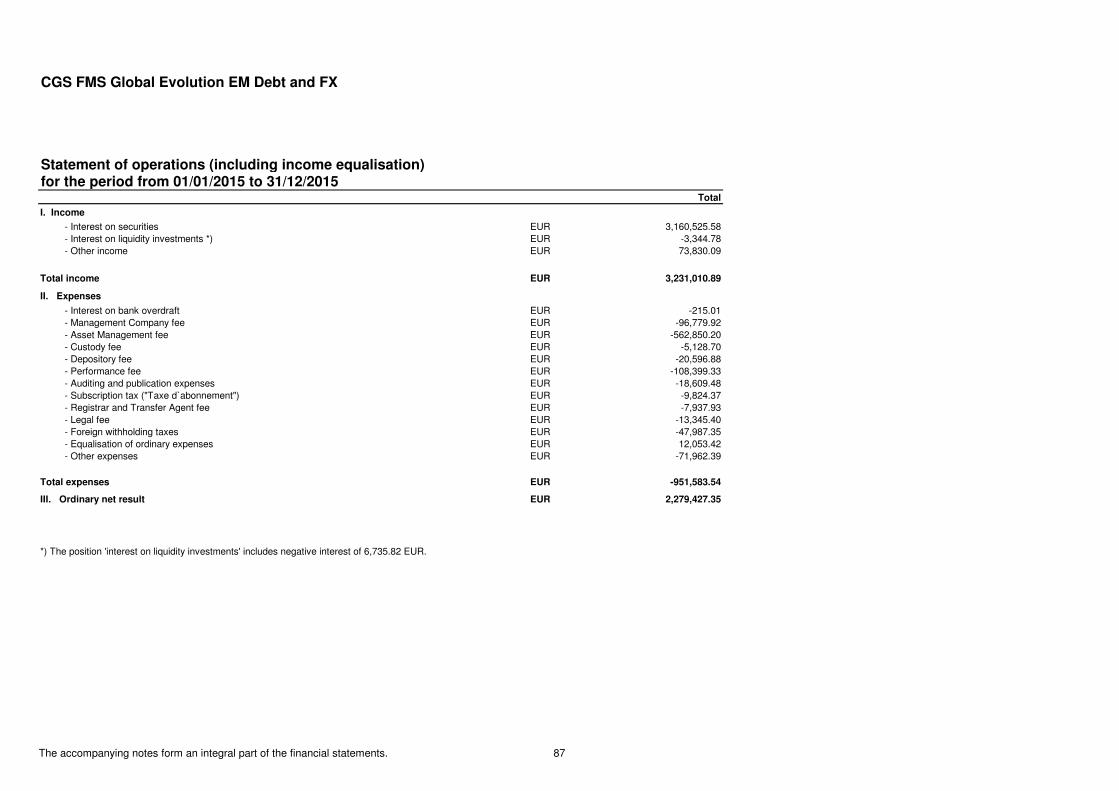

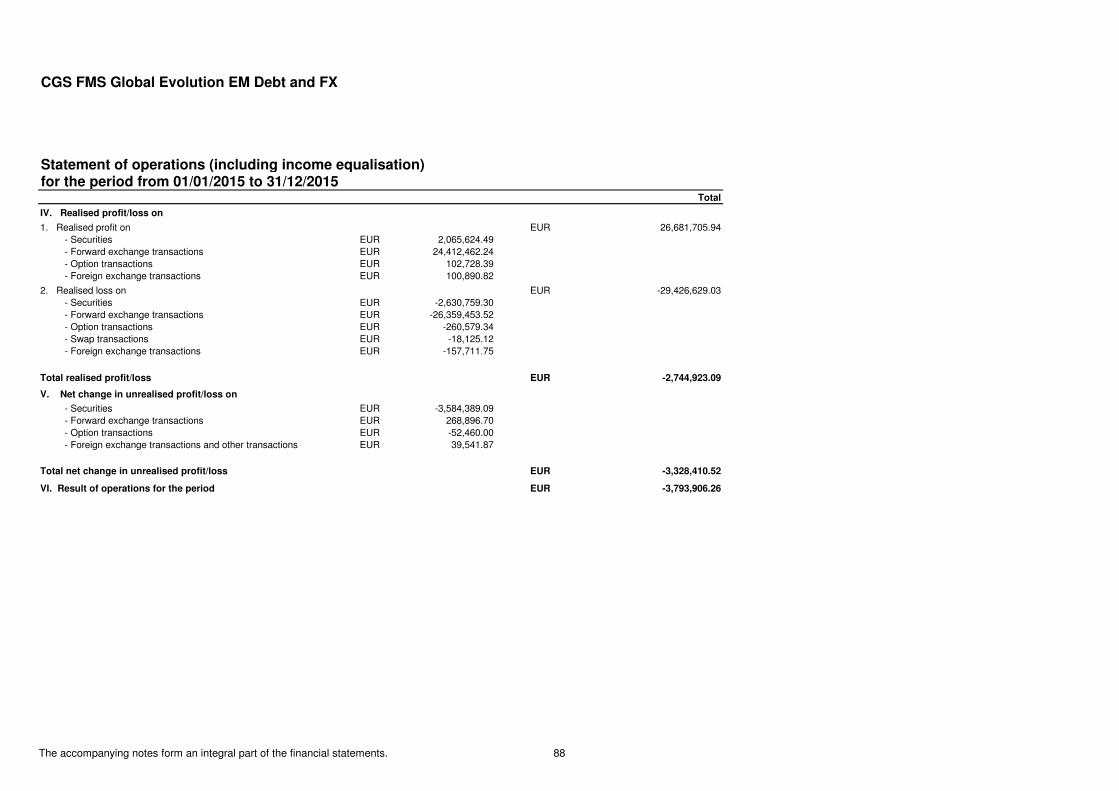

Statement of Operations (including income equalisation) 87 - 88

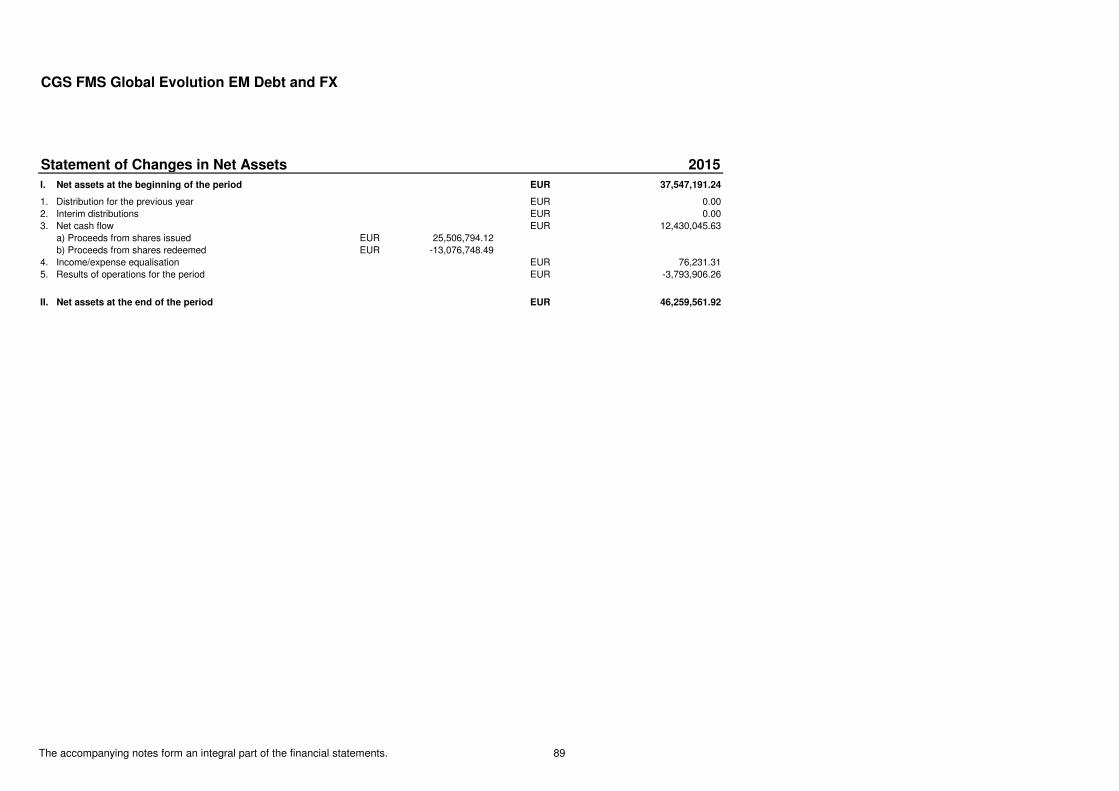

Statement of Changes in Net Assets 89

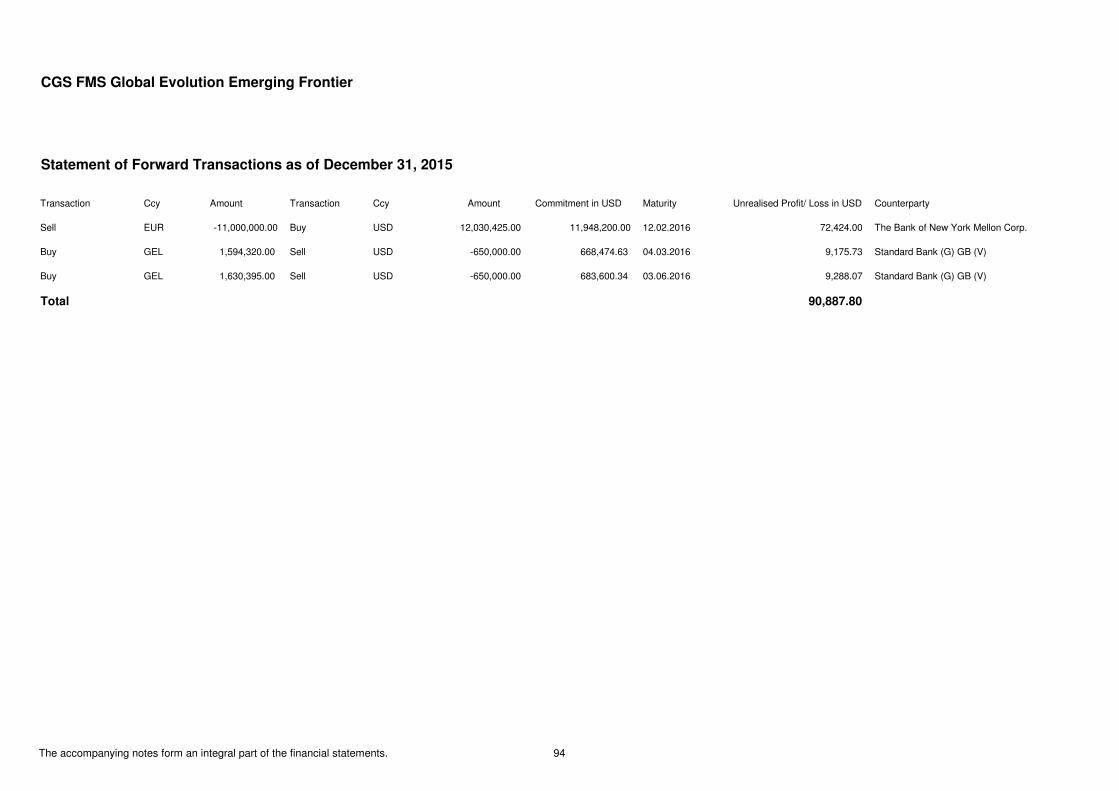

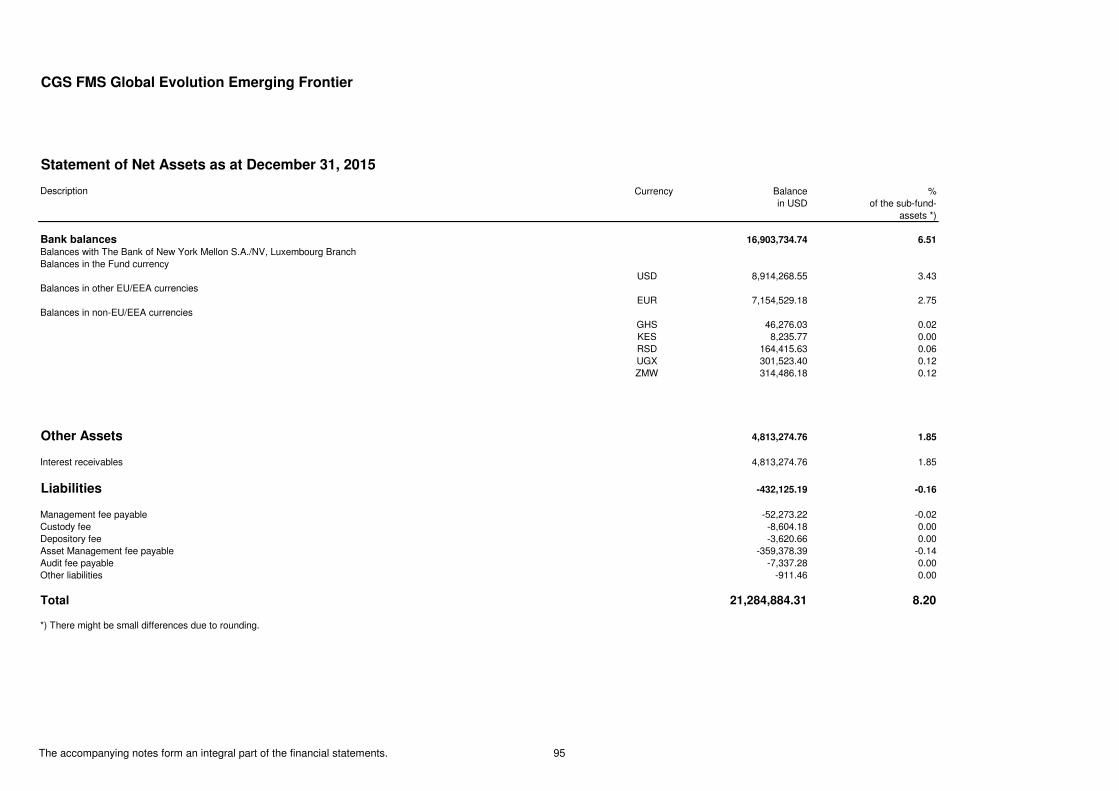

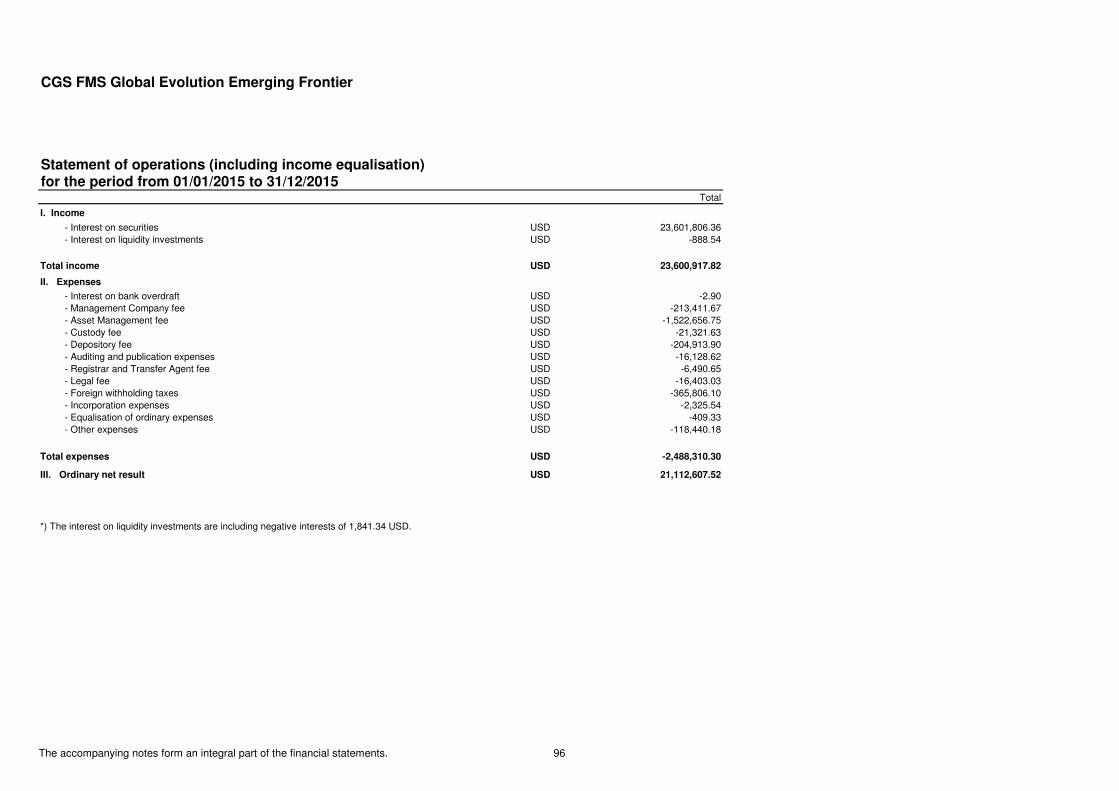

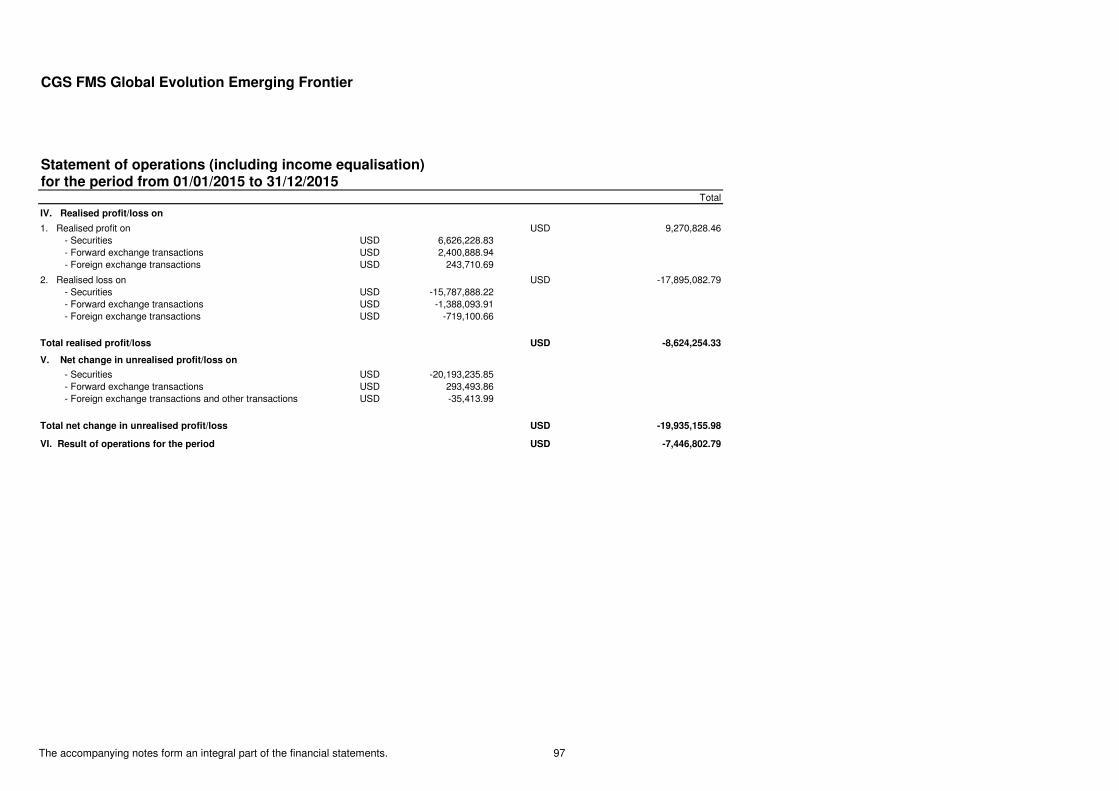

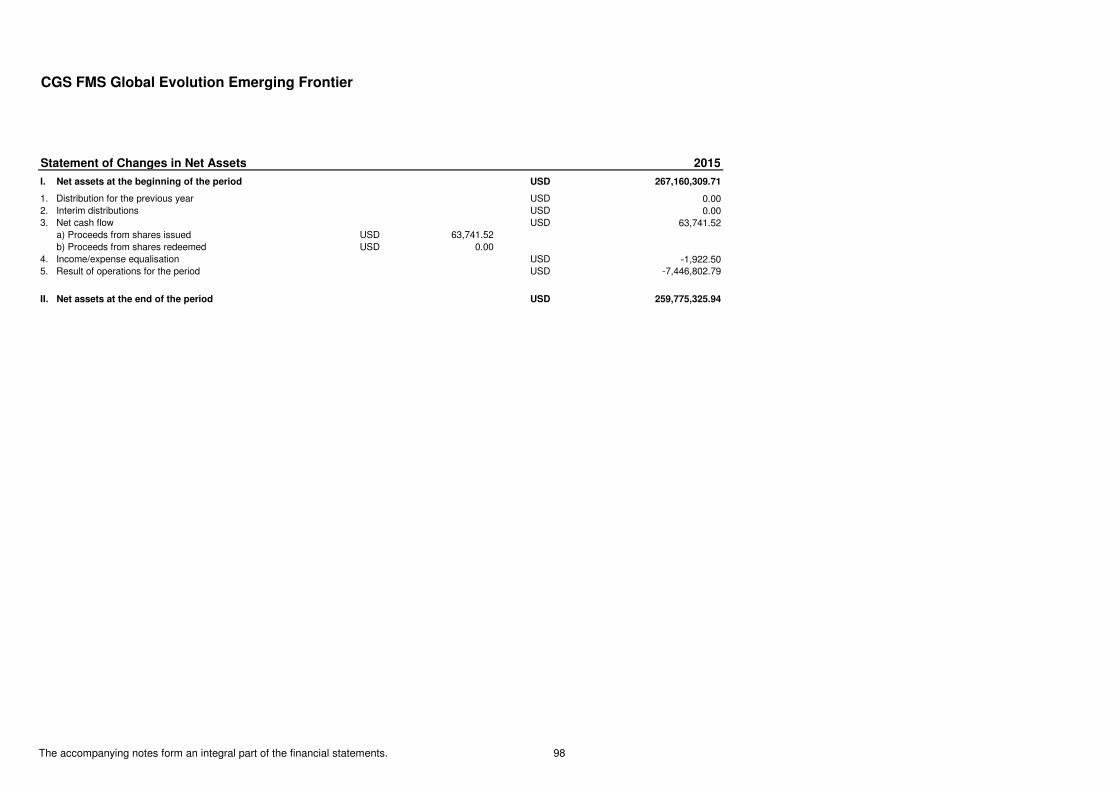

CGS FMS - Global Evolution Emerging Frontier

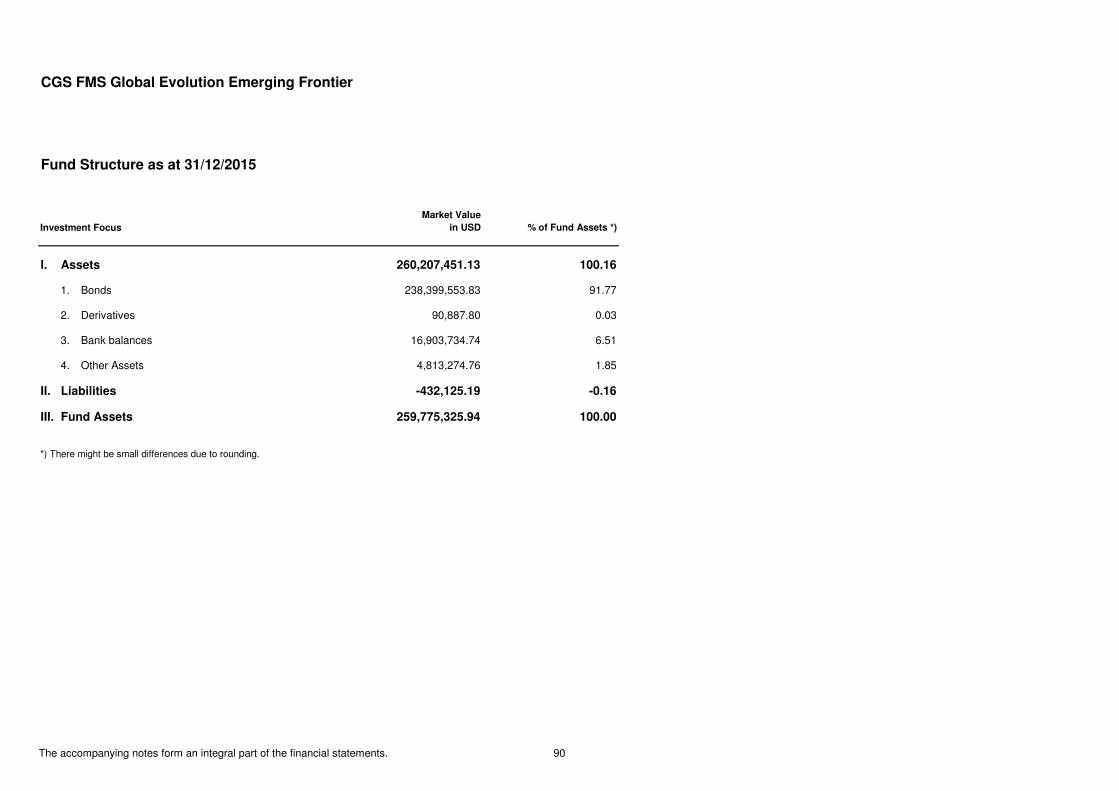

Fund Structure 90

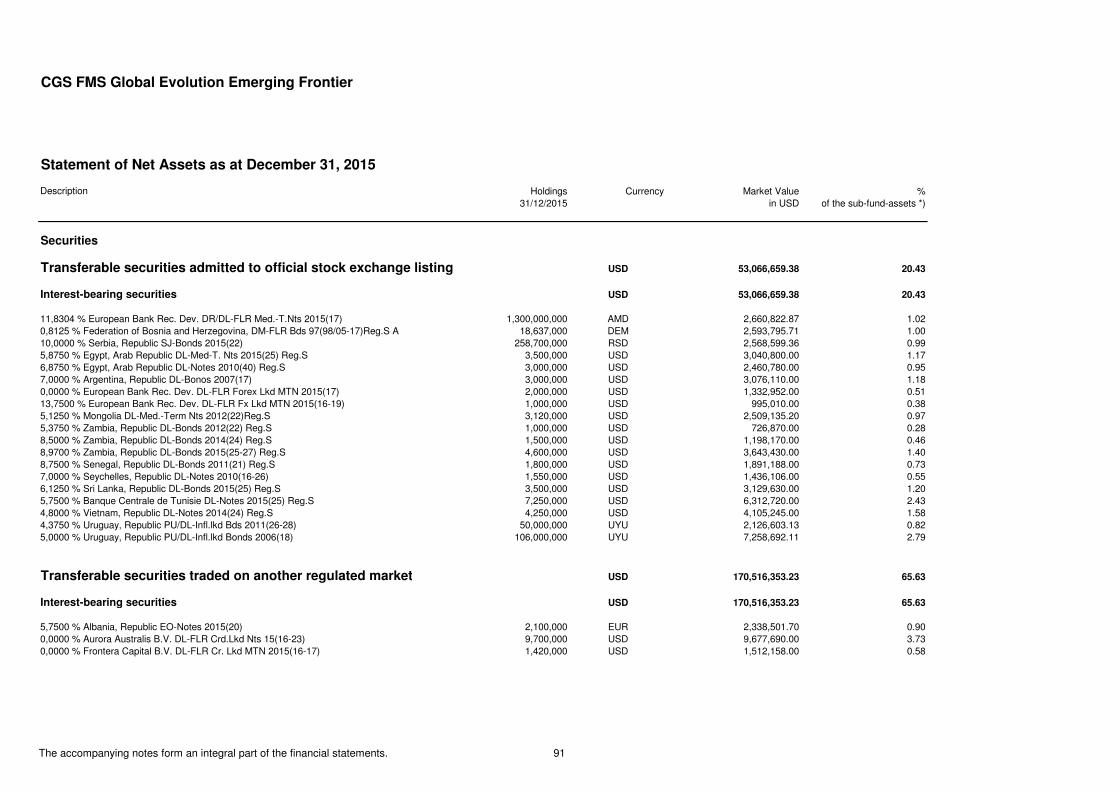

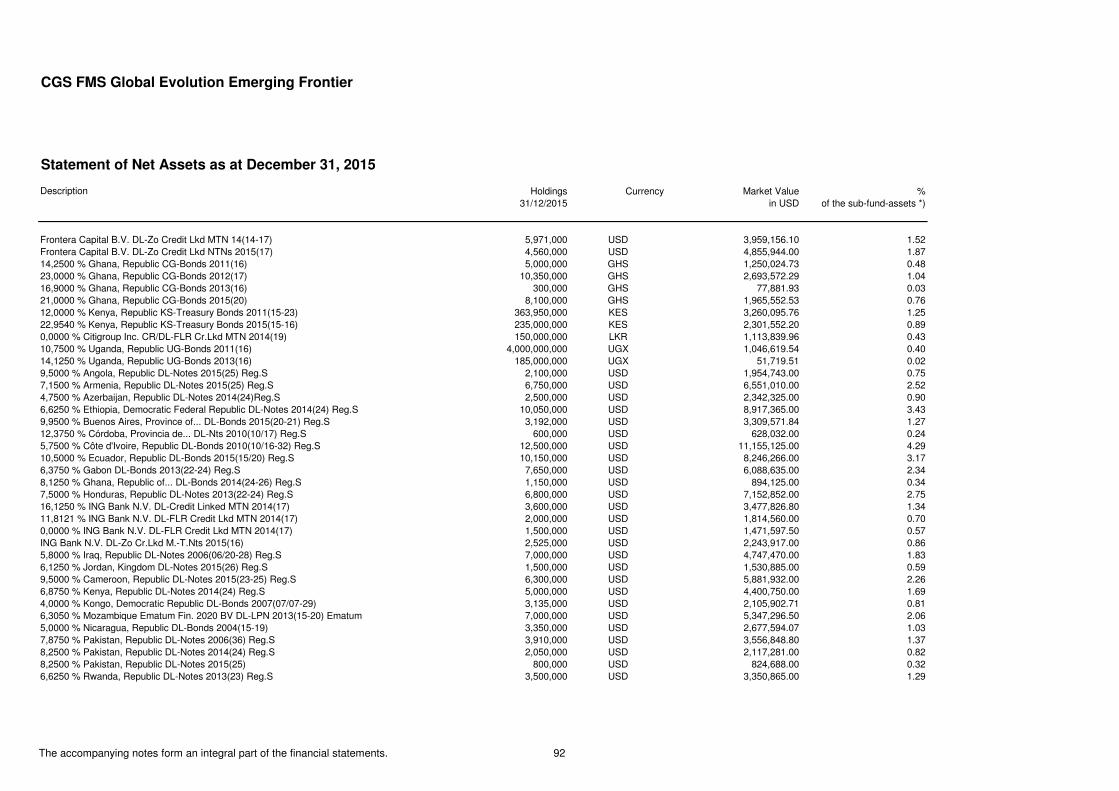

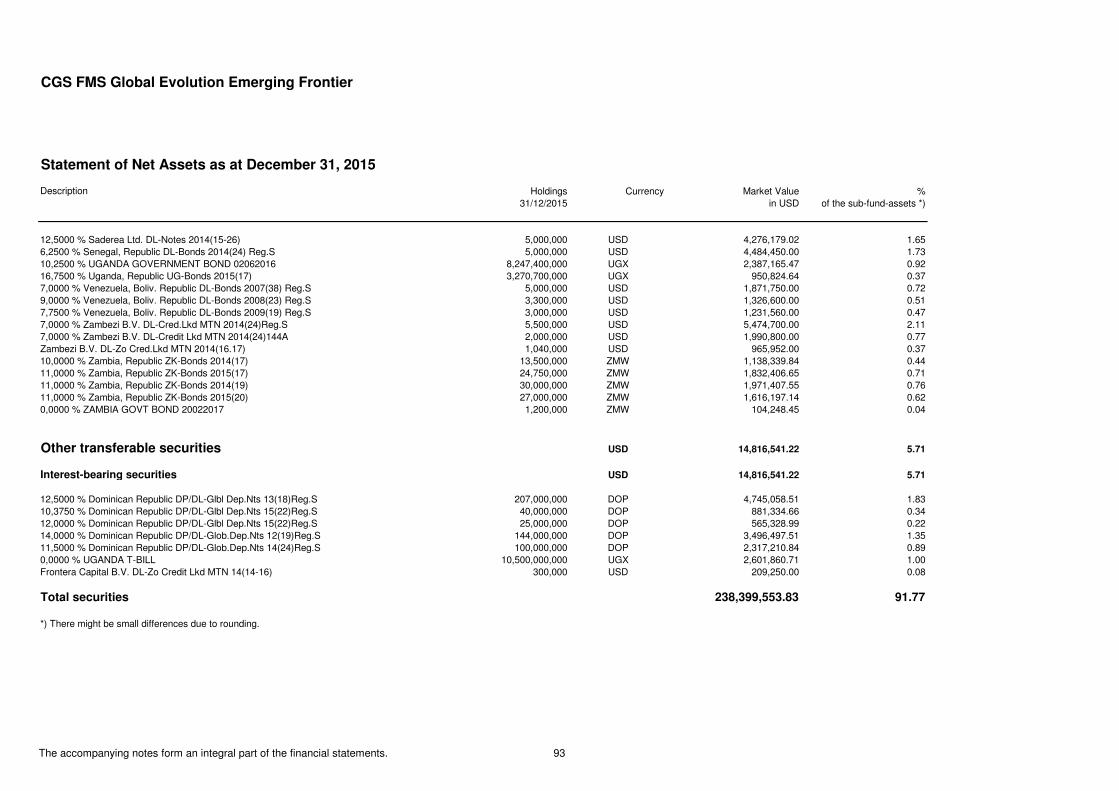

Statement of Securities 91 - 93

Statement of Forward Transactions 94

Statement of Bank balances, Other Assets and Liabilities 95

Statement of Operations (including income equalisation) 96 - 97

Statement of Changes in Net Assets 98

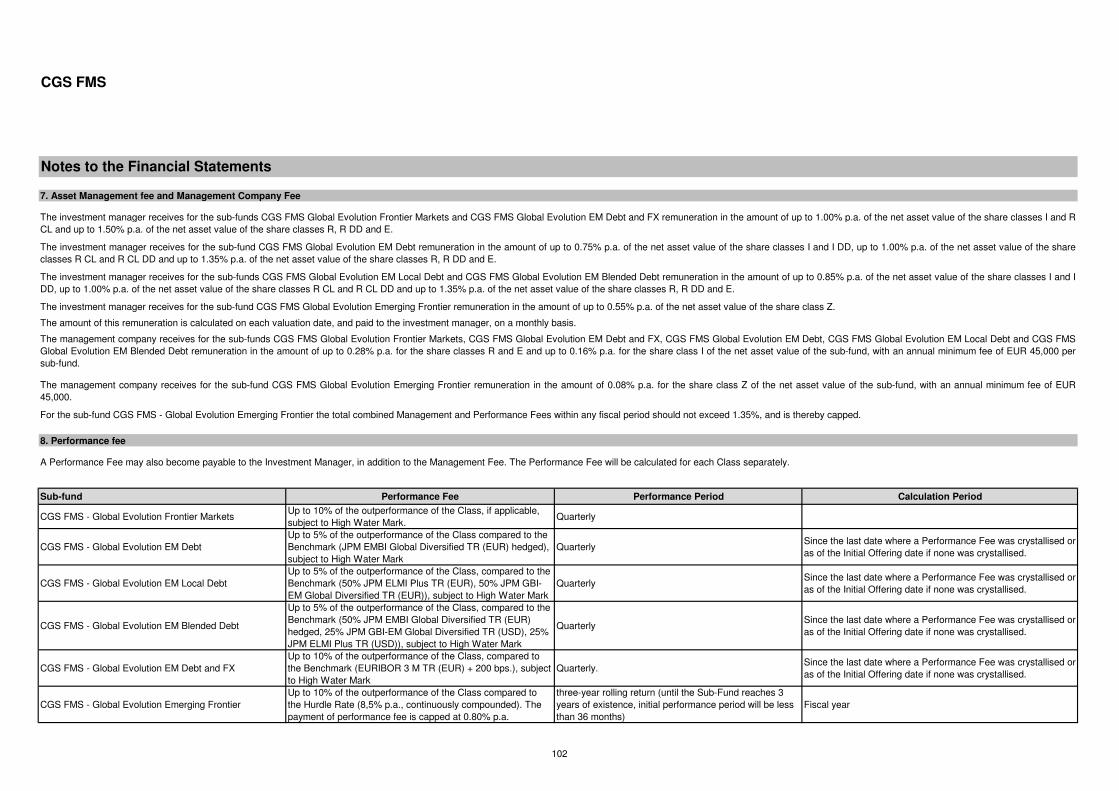

Notes to the Financial Statements 99 - 104

Supplementary information (unaudited)

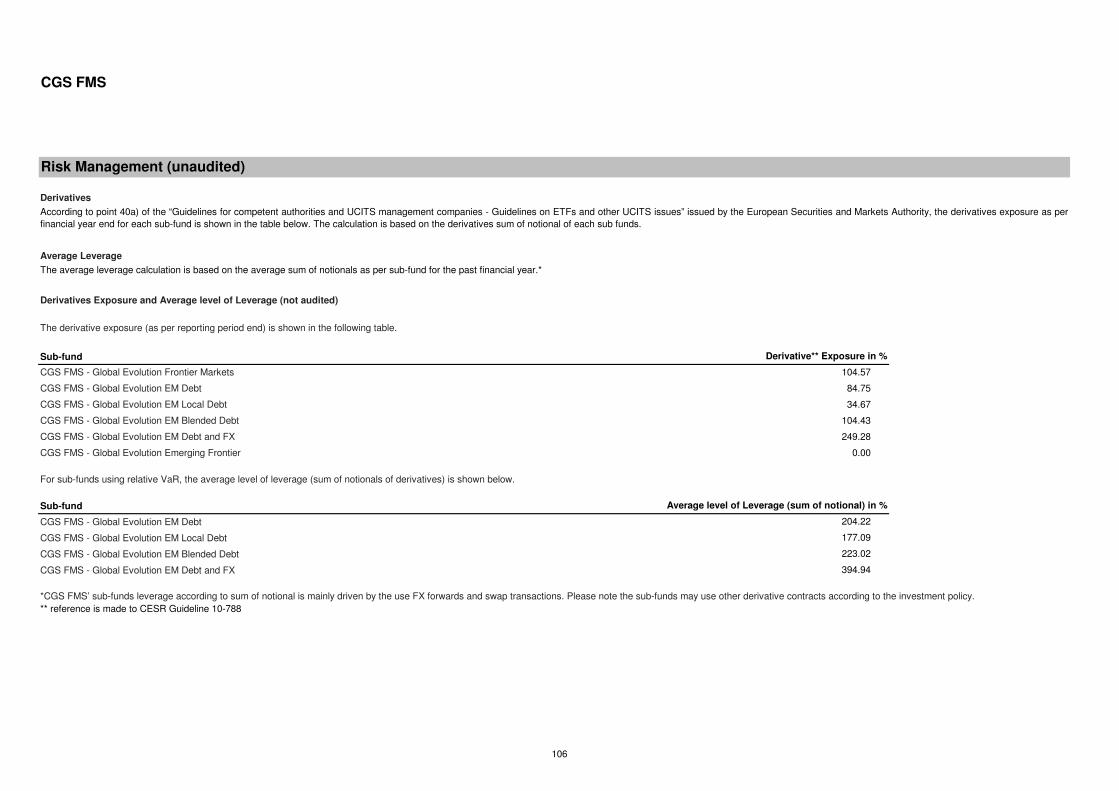

Global Exposure 105

Risk Management 106

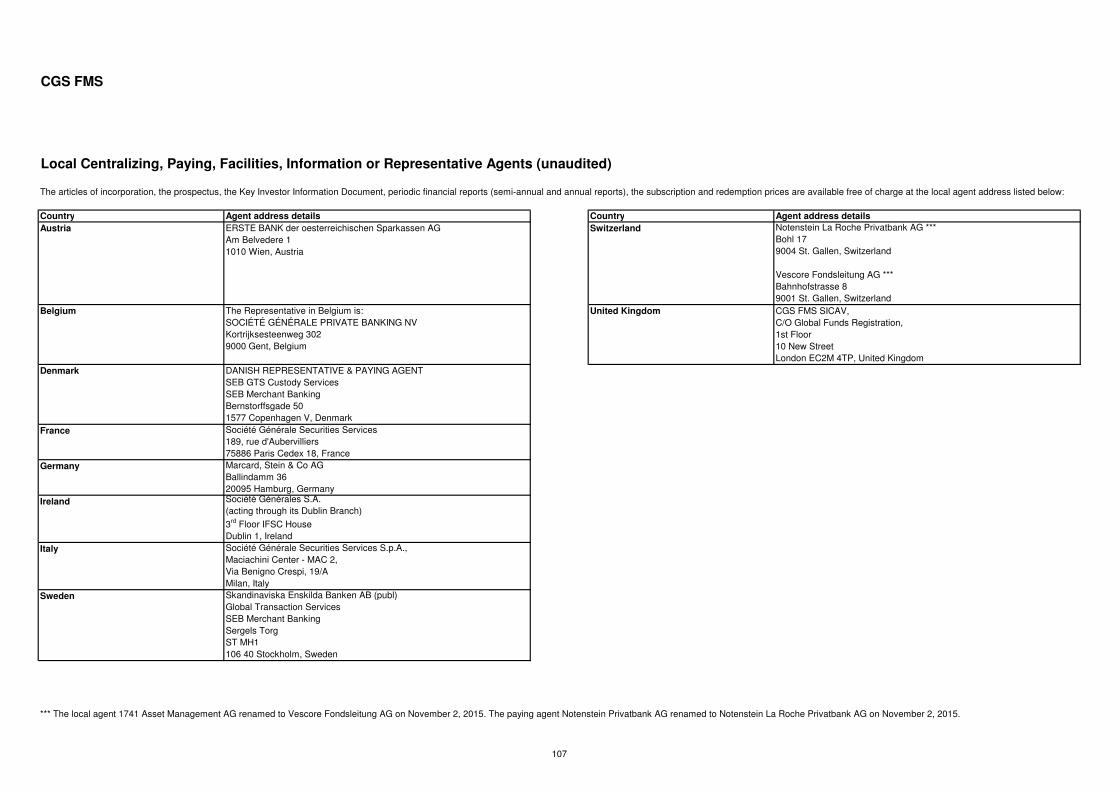

Local Centralizing, Paying, Facilities, Information or Representative Agents 107

5

CGS FMS

To the Shareholders of

CGS FMS SICAV

Vertigo Building - Polaris

2 - 4, rue Eugène Ruppert

L - 2453 Luxembourg

Ernst & Young

Société anonyme

Cabinet de révision agréé

Isabelle Nicks

Luxembourg, 23 March 2016

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing as adopted for Luxembourg by the “Commission de Surveillance du SecteurFinancier”. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

Independent auditor’s report

We have audited the accompanying financial statements of CGS FMS SICAV (the “SICAV”) and of each of its sub-funds, which comprise the statement of net assets, the statement of forward transactions, the statement of swaps and the statement of optionsrights as at 31 December 2015 and the statement of operations and the statement of changes in net assets for the year then ended, and a summary of significant accounting policies and other explanatory information.

Responsibility of the Board of Directors of the SICAV for the financial statements

The Board of Directors of the SICAV is responsible for the preparation and fair presentation of these financial statements in accordance with Luxembourg legal and regulatory requirements relating to the preparation and presentation of the financial statementsand for such internal control as the Board of Directors of the SICAV determines is necessary to enable the preparation and presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Responsibility of the “réviseur d’entreprises agréé”

Only the English version of the present Annual Report has been reviewed by the independent auditors. Consequently, the independent auditor’s report only refers to the English version of the Annual Report; other versions result from a conscientioustranslation made under the responsibility of the Board of Directors of the SICAV. In case of differences between the English version and the translation, the English version should be retained.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the judgement of the “réviseur d’entreprises agréé”, including the assessment of the risks ofmaterial misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the “réviseur d’entreprises agréé” considers internal control relevant to the entity’s preparation and fair presentation of the financial statementsin order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policiesused and the reasonableness of accounting estimates made by the Board of Directors of the SICAV, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements give a true and fair view of the financial position of CGS FMS SICAV and of each of its sub-funds as of 31 December 2015, and of the results of their operations and changes in their net assets for the year then ended inaccordance with Luxembourg legal and regulatory requirements relating to the preparation and presentation of the financial statements.

Other matter

Supplementary information included in the annual report has been reviewed in the context of our mandate but has not been subject to specific audit procedures carried out in accordance with the standards described above. Consequently, we express noopinion on such information. However, we have no observation to make concerning such information in the context of the financial statements taken as a whole.

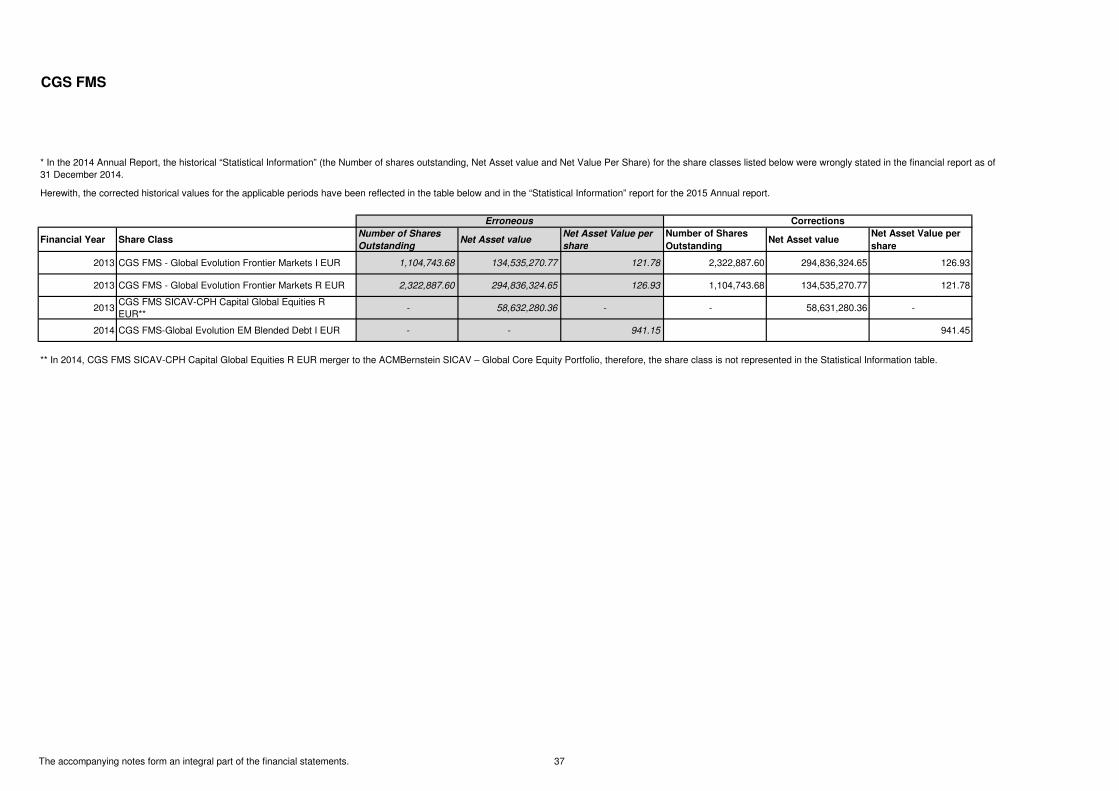

The financial statements of CGS FMS SICAV for the year ended 31 December 2014 were audited by another auditor who expressed an unmodified opinion on 15 April 2015.

6

CGS FMS

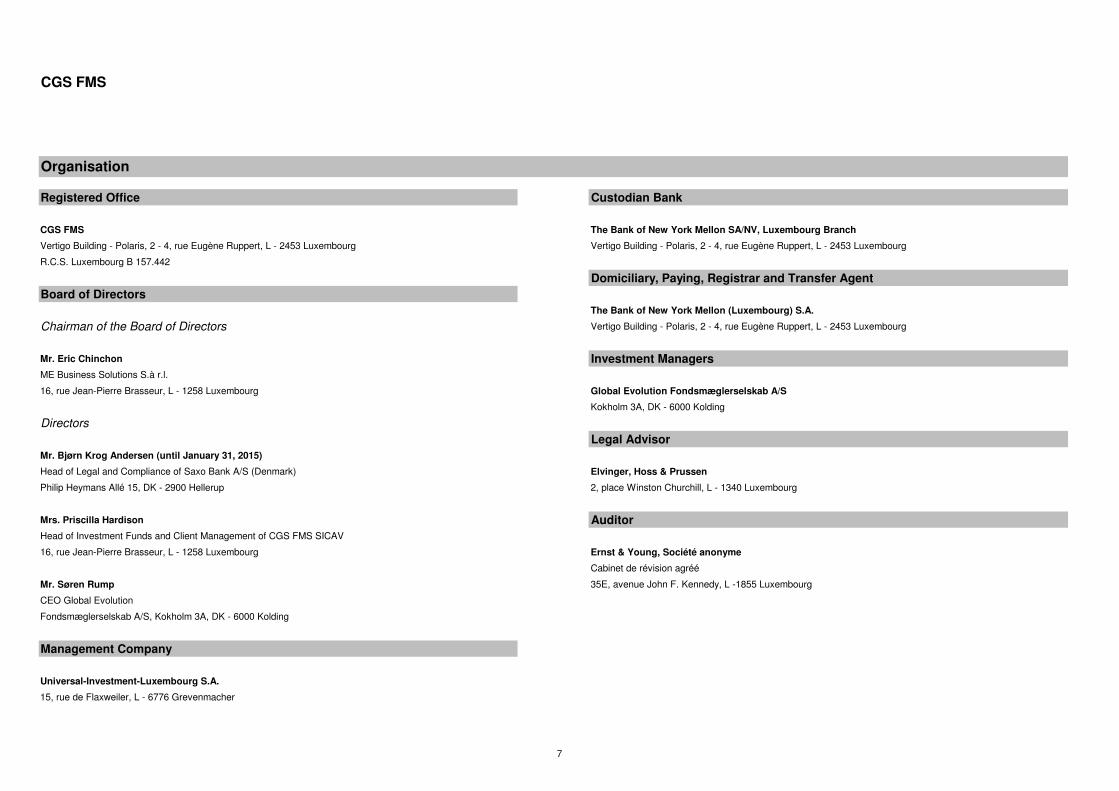

Registered Office Custodian Bank

CGS FMS The Bank of New York Mellon SA/NV, Luxembourg Branch

Vertigo Building - Polaris, 2 - 4, rue Eugène Ruppert, L - 2453 Luxembourg Vertigo Building - Polaris, 2 - 4, rue Eugène Ruppert, L - 2453 Luxembourg

R.C.S. Luxembourg B 157.442

Domiciliary, Paying, Registrar and Transfer Agent

Board of Directors

The Bank of New York Mellon (Luxembourg) S.A.

Chairman of the Board of Directors Vertigo Building - Polaris, 2 - 4, rue Eugène Ruppert, L - 2453 Luxembourg

Mr. Eric Chinchon Investment Managers

ME Business Solutions S.à r.l.

16, rue Jean-Pierre Brasseur, L - 1258 Luxembourg Global Evolution Fondsmæglerselskab A/S

Kokholm 3A, DK - 6000 Kolding

Directors

Legal Advisor

Mr. Bjørn Krog Andersen (until January 31, 2015)

Head of Legal and Compliance of Saxo Bank A/S (Denmark) Elvinger, Hoss & Prussen

Philip Heymans Allé 15, DK - 2900 Hellerup 2, place Winston Churchill, L - 1340 Luxembourg

Mrs. Priscilla Hardison Auditor

Head of Investment Funds and Client Management of CGS FMS SICAV

16, rue Jean-Pierre Brasseur, L - 1258 Luxembourg Ernst & Young, Société anonyme

Cabinet de révision agréé

Mr. Søren Rump 35E, avenue John F. Kennedy, L -1855 Luxembourg

CEO Global Evolution

Fondsmæglerselskab A/S, Kokholm 3A, DK - 6000 Kolding

Management Company

Universal-Investment-Luxembourg S.A.

15, rue de Flaxweiler, L - 6776 Grevenmacher

Organisation

7

CGS FMS

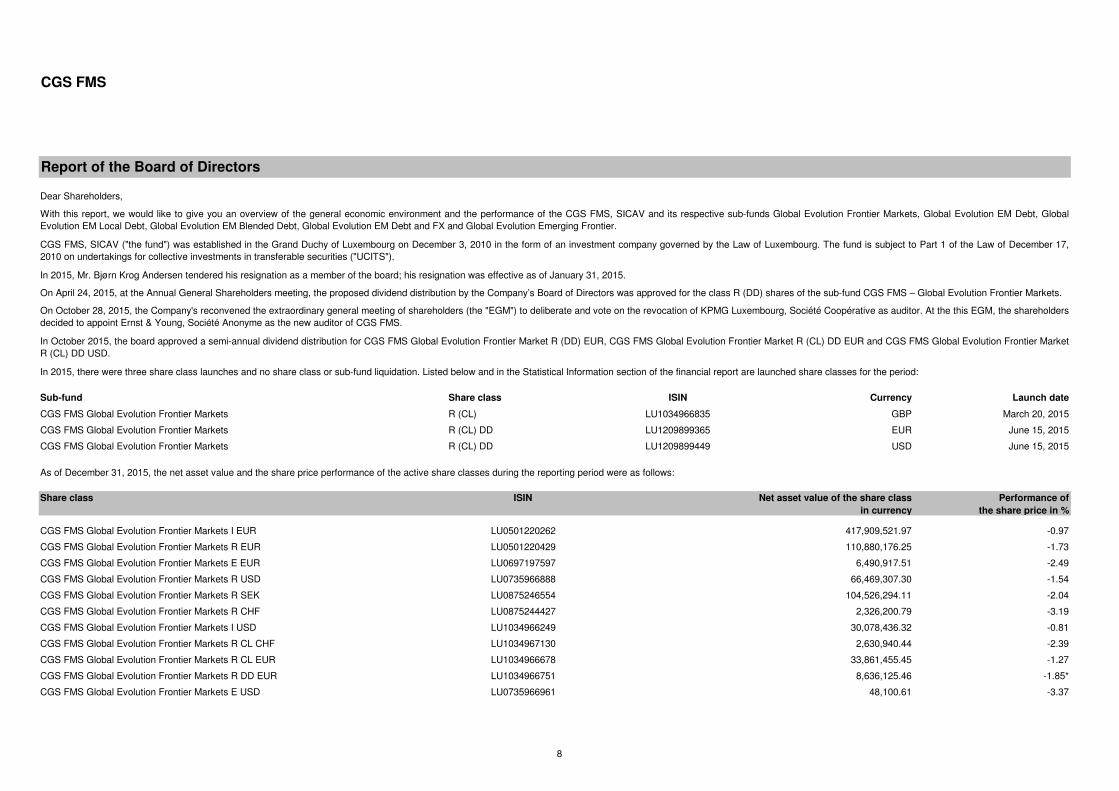

Sub-fund Share class ISIN Currency Launch date

CGS FMS Global Evolution Frontier Markets R (CL) LU1034966835 GBP March 20, 2015

CGS FMS Global Evolution Frontier Markets R (CL) DD LU1209899365 EUR June 15, 2015

CGS FMS Global Evolution Frontier Markets R (CL) DD LU1209899449 USD June 15, 2015

Share class ISIN Performance of

the share price in %

CGS FMS Global Evolution Frontier Markets I EUR LU0501220262 417,909,521.97 -0.97

CGS FMS Global Evolution Frontier Markets R EUR LU0501220429 110,880,176.25 -1.73

CGS FMS Global Evolution Frontier Markets E EUR LU0697197597 6,490,917.51 -2.49

CGS FMS Global Evolution Frontier Markets R USD LU0735966888 66,469,307.30 -1.54

CGS FMS Global Evolution Frontier Markets R SEK LU0875246554 104,526,294.11 -2.04

CGS FMS Global Evolution Frontier Markets R CHF LU0875244427 2,326,200.79 -3.19

CGS FMS Global Evolution Frontier Markets I USD LU1034966249 30,078,436.32 -0.81

CGS FMS Global Evolution Frontier Markets R CL CHF LU1034967130 2,630,940.44 -2.39

CGS FMS Global Evolution Frontier Markets R CL EUR LU1034966678 33,861,455.45 -1.27

CGS FMS Global Evolution Frontier Markets R DD EUR LU1034966751 8,636,125.46 -1.85*

CGS FMS Global Evolution Frontier Markets E USD LU0735966961 48,100.61 -3.37

Net asset value of the share class

in currency

As of December 31, 2015, the net asset value and the share price performance of the active share classes during the reporting period were as follows:

Report of the Board of Directors

Dear Shareholders,

In 2015, there were three share class launches and no share class or sub-fund liquidation. Listed below and in the Statistical Information section of the financial report are launched share classes for the period:

With this report, we would like to give you an overview of the general economic environment and the performance of the CGS FMS, SICAV and its respective sub-funds Global Evolution Frontier Markets, Global Evolution EM Debt, GlobalEvolution EM Local Debt, Global Evolution EM Blended Debt, Global Evolution EM Debt and FX and Global Evolution Emerging Frontier.

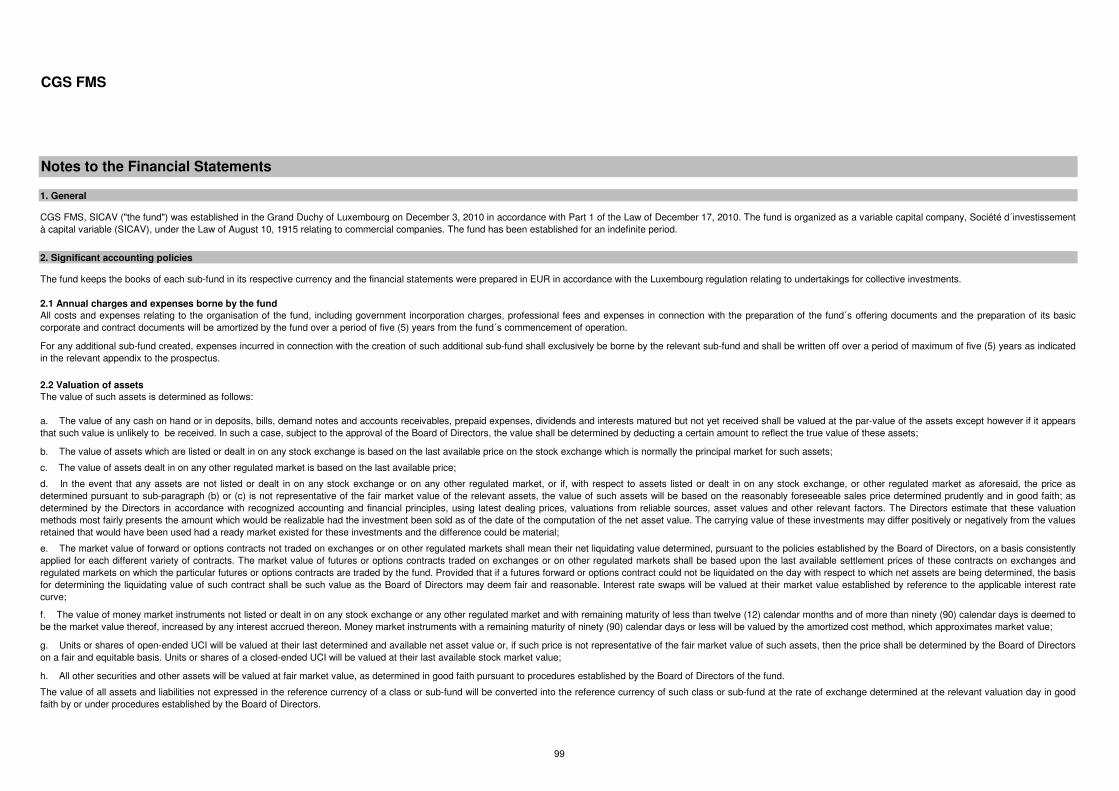

CGS FMS, SICAV ("the fund") was established in the Grand Duchy of Luxembourg on December 3, 2010 in the form of an investment company governed by the Law of Luxembourg. The fund is subject to Part 1 of the Law of December 17,2010 on undertakings for collective investments in transferable securities ("UCITS").

In 2015, Mr. Bjørn Krog Andersen tendered his resignation as a member of the board; his resignation was effective as of January 31, 2015.

On April 24, 2015, at the Annual General Shareholders meeting, the proposed dividend distribution by the Company’s Board of Directors was approved for the class R (DD) shares of the sub-fund CGS FMS – Global Evolution Frontier Markets.

On October 28, 2015, the Company's reconvened the extraordinary general meeting of shareholders (the "EGM") to deliberate and vote on the revocation of KPMG Luxembourg, Société Coopérative as auditor. At the this EGM, the shareholdersdecided to appoint Ernst & Young, Société Anonyme as the new auditor of CGS FMS.

In October 2015, the board approved a semi-annual dividend distribution for CGS FMS Global Evolution Frontier Market R (DD) EUR, CGS FMS Global Evolution Frontier Market R (CL) DD EUR and CGS FMS Global Evolution Frontier MarketR (CL) DD USD.

8

CGS FMS

Report of the Board of Directors

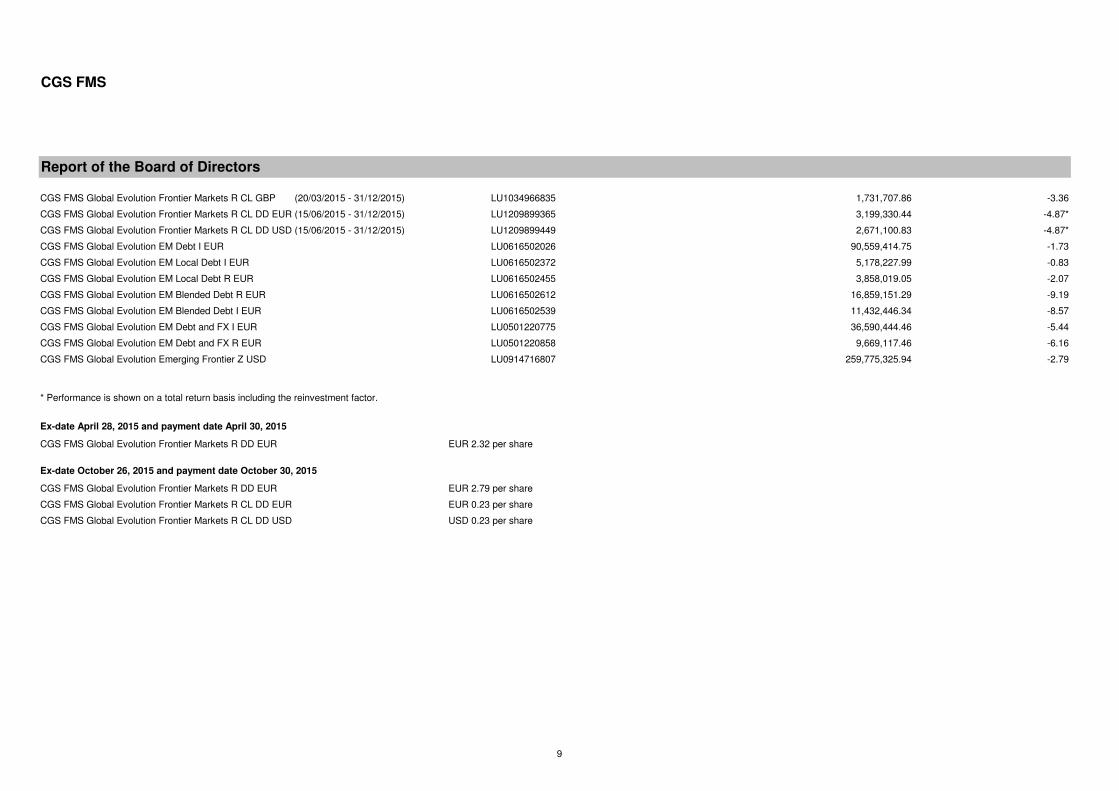

CGS FMS Global Evolution Frontier Markets R CL GBP (20/03/2015 - 31/12/2015) LU1034966835 1,731,707.86 -3.36

CGS FMS Global Evolution Frontier Markets R CL DD EUR (15/06/2015 - 31/12/2015) LU1209899365 3,199,330.44 -4.87*

CGS FMS Global Evolution Frontier Markets R CL DD USD (15/06/2015 - 31/12/2015) LU1209899449 2,671,100.83 -4.87*

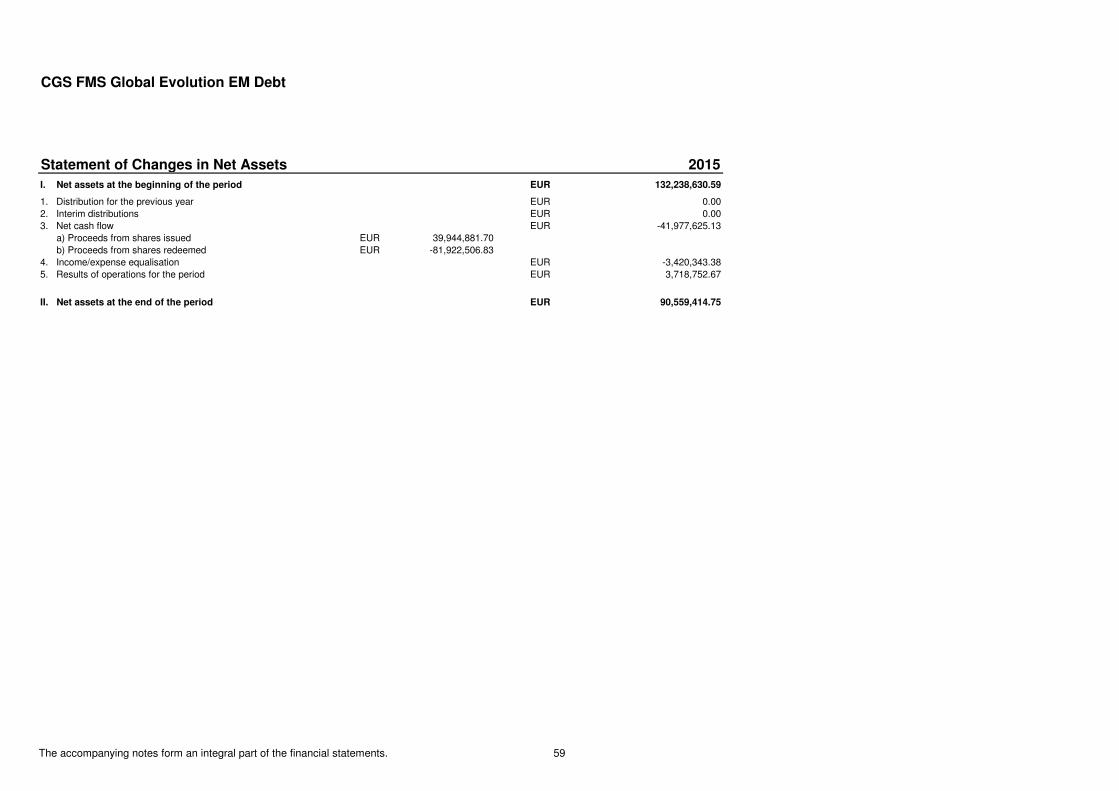

CGS FMS Global Evolution EM Debt I EUR LU0616502026 90,559,414.75 -1.73

CGS FMS Global Evolution EM Local Debt I EUR LU0616502372 5,178,227.99 -0.83

CGS FMS Global Evolution EM Local Debt R EUR LU0616502455 3,858,019.05 -2.07

CGS FMS Global Evolution EM Blended Debt R EUR LU0616502612 16,859,151.29 -9.19

CGS FMS Global Evolution EM Blended Debt I EUR LU0616502539 11,432,446.34 -8.57

CGS FMS Global Evolution EM Debt and FX I EUR LU0501220775 36,590,444.46 -5.44

CGS FMS Global Evolution EM Debt and FX R EUR LU0501220858 9,669,117.46 -6.16

CGS FMS Global Evolution Emerging Frontier Z USD LU0914716807 259,775,325.94 -2.79

* Performance is shown on a total return basis including the reinvestment factor.

Ex-date April 28, 2015 and payment date April 30, 2015

CGS FMS Global Evolution Frontier Markets R DD EUR EUR 2.32 per share

Ex-date October 26, 2015 and payment date October 30, 2015

CGS FMS Global Evolution Frontier Markets R DD EUR EUR 2.79 per share

CGS FMS Global Evolution Frontier Markets R CL DD EUR EUR 0.23 per share

CGS FMS Global Evolution Frontier Markets R CL DD USD USD 0.23 per share

9

CGS FMS

Global Evolution Frontier Markets

Report of the Asset Manager

Investment Objective

The objective of the frontier markets strategy is to create attractive returns by utilizing a non-benchmark focused and diversified strategy within sovereign frontier emerging markets globally. The fund invests in hard currency and local currencyinstruments as well as foreign exchange. To achieve the investment objective Global Evolution will use a range of financial instruments (local currency debt instruments, hard currency debt instruments and foreign exchange) and derivativefinancial instruments (interest rate futures, interest rate swaps, total return swaps, credit default swaps, FX forwards, FX options and non-deliverable forwards).

Last year’s market environment

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

A new oil order governed by Saudi Arabia

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

Pegged currency regimes faced strong headwinds

As hard commodities continued lower, commodity backed currencies came increasingly under pressure. A number of exporters gave up their currency peg (Kazakhstan, Azerbaijan), but a few die hard pegged regimes (Saudi Arabia, Nigeria)stayed put.

(Geo)political risk came to the fore

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years,European based institutional investors were left with little choice but to move up in duration or move down in credit quality. With no doubt this helped explain the contradiction between ongoing redemptions in EM debt dedicated retail funds anda solid institutional pipeline for hard currency EM mandates. Turning to the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger on rate hikes on December 16, 2015.

The trade weighted dollar index gained almost 9%

10yr US treasury yields finished the year little changed; up from 2.17% to 2.27%. However, in FX markets the dollar strengthened from EUR/USD 1.2098 to an intra-year low of EUR/USD 1.0496 but the currency pair recovered to finish the yearin 1.0862. The Federal Reserve’s broad trade weighted dollar index gained 9.7% in 2015.

10

CGS FMS

Report of the Asset Manager

Source: Global Evolution

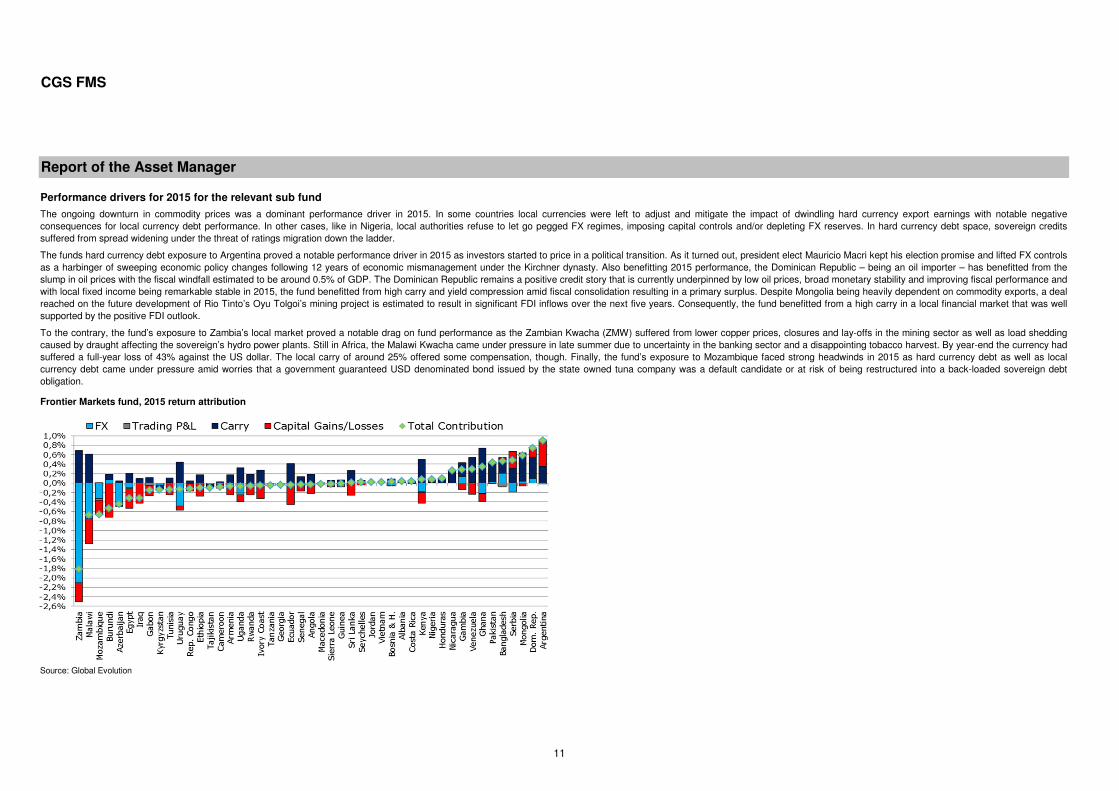

Performance drivers for 2015 for the relevant sub fund

The ongoing downturn in commodity prices was a dominant performance driver in 2015. In some countries local currencies were left to adjust and mitigate the impact of dwindling hard currency export earnings with notable negativeconsequences for local currency debt performance. In other cases, like in Nigeria, local authorities refuse to let go pegged FX regimes, imposing capital controls and/or depleting FX reserves. In hard currency debt space, sovereign creditssuffered from spread widening under the threat of ratings migration down the ladder.

The funds hard currency debt exposure to Argentina proved a notable performance driver in 2015 as investors started to price in a political transition. As it turned out, president elect Mauricio Macri kept his election promise and lifted FX controlsas a harbinger of sweeping economic policy changes following 12 years of economic mismanagement under the Kirchner dynasty. Also benefitting 2015 performance, the Dominican Republic – being an oil importer – has benefitted from theslump in oil prices with the fiscal windfall estimated to be around 0.5% of GDP. The Dominican Republic remains a positive credit story that is currently underpinned by low oil prices, broad monetary stability and improving fiscal performance andwith local fixed income being remarkable stable in 2015, the fund benefitted from high carry and yield compression amid fiscal consolidation resulting in a primary surplus. Despite Mongolia being heavily dependent on commodity exports, a dealreached on the future development of Rio Tinto’s Oyu Tolgoi’s mining project is estimated to result in significant FDI inflows over the next five years. Consequently, the fund benefitted from a high carry in a local financial market that was wellsupported by the positive FDI outlook.

To the contrary, the fund’s exposure to Zambia’s local market proved a notable drag on fund performance as the Zambian Kwacha (ZMW) suffered from lower copper prices, closures and lay-offs in the mining sector as well as load sheddingcaused by draught affecting the sovereign’s hydro power plants. Still in Africa, the Malawi Kwacha came under pressure in late summer due to uncertainty in the banking sector and a disappointing tobacco harvest. By year-end the currency hadsuffered a full-year loss of 43% against the US dollar. The local carry of around 25% offered some compensation, though. Finally, the fund’s exposure to Mozambique faced strong headwinds in 2015 as hard currency debt as well as localcurrency debt came under pressure amid worries that a government guaranteed USD denominated bond issued by the state owned tuna company was a default candidate or at risk of being restructured into a back-loaded sovereign debtobligation.

Frontier Markets fund, 2015 return attribution

11

CGS FMS

Report of the Asset Manager

Source: Global Evolution

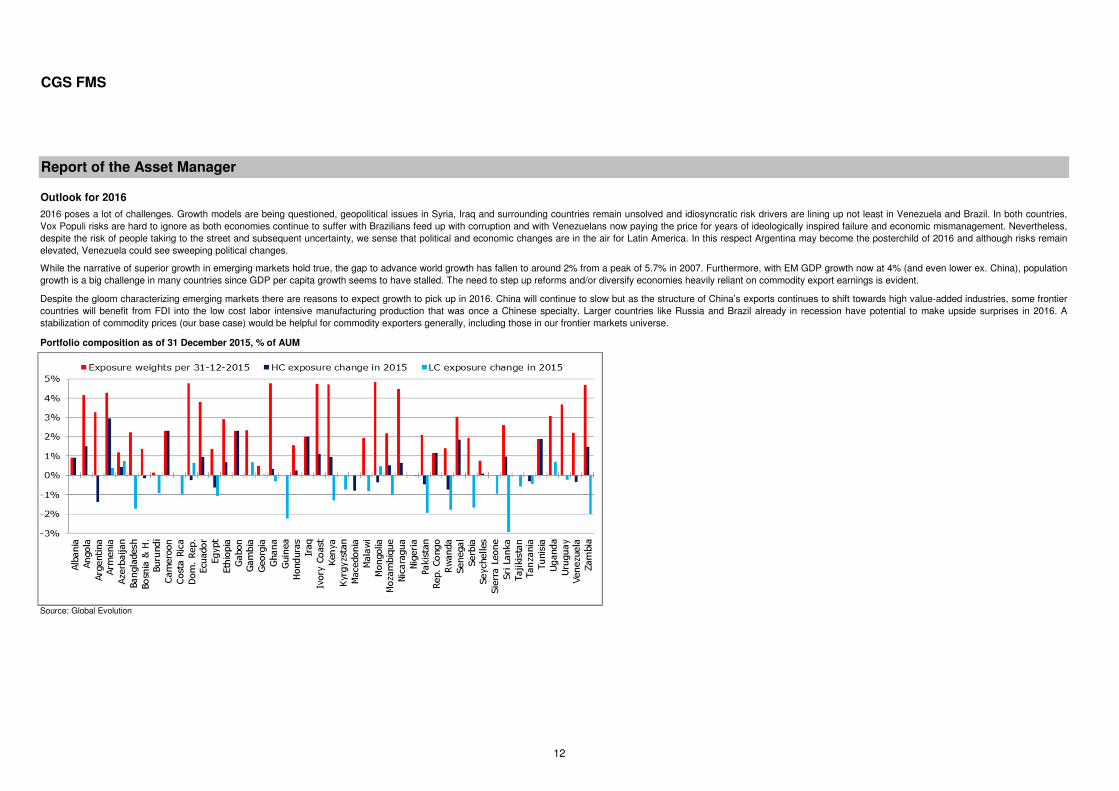

Outlook for 2016

2016 poses a lot of challenges. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela and Brazil. In both countries,Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians feed up with corruption and with Venezuelans now paying the price for years of ideologically inspired failure and economic mismanagement. Nevertheless,despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of 2016 and although risks remainelevated, Venezuela could see sweeping political changes.

While the narrative of superior growth in emerging markets hold true, the gap to advance world growth has fallen to around 2% from a peak of 5.7% in 2007. Furthermore, with EM GDP growth now at 4% (and even lower ex. China), populationgrowth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. China will continue to slow but as the structure of China’s exports continues to shift towards high value-added industries, some frontiercountries will benefit from FDI into the low cost labor intensive manufacturing production that was once a Chinese specialty. Larger countries like Russia and Brazil already in recession have potential to make upside surprises in 2016. Astabilization of commodity prices (our base case) would be helpful for commodity exporters generally, including those in our frontier markets universe.

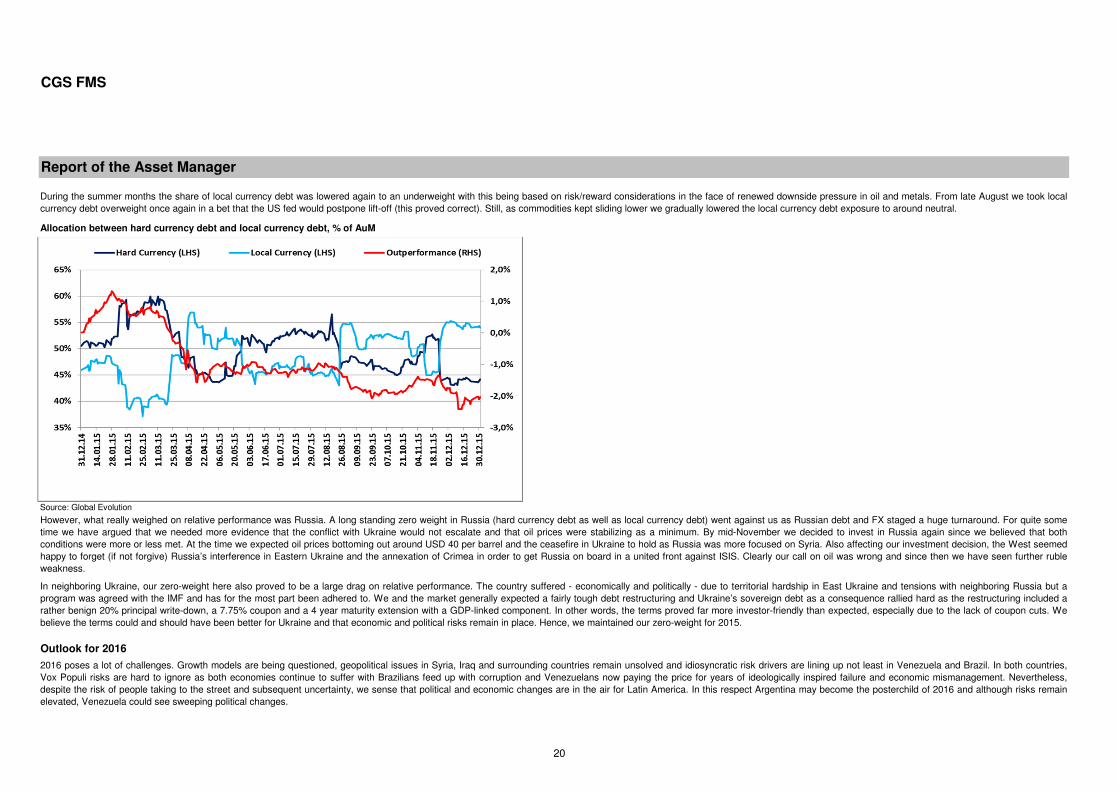

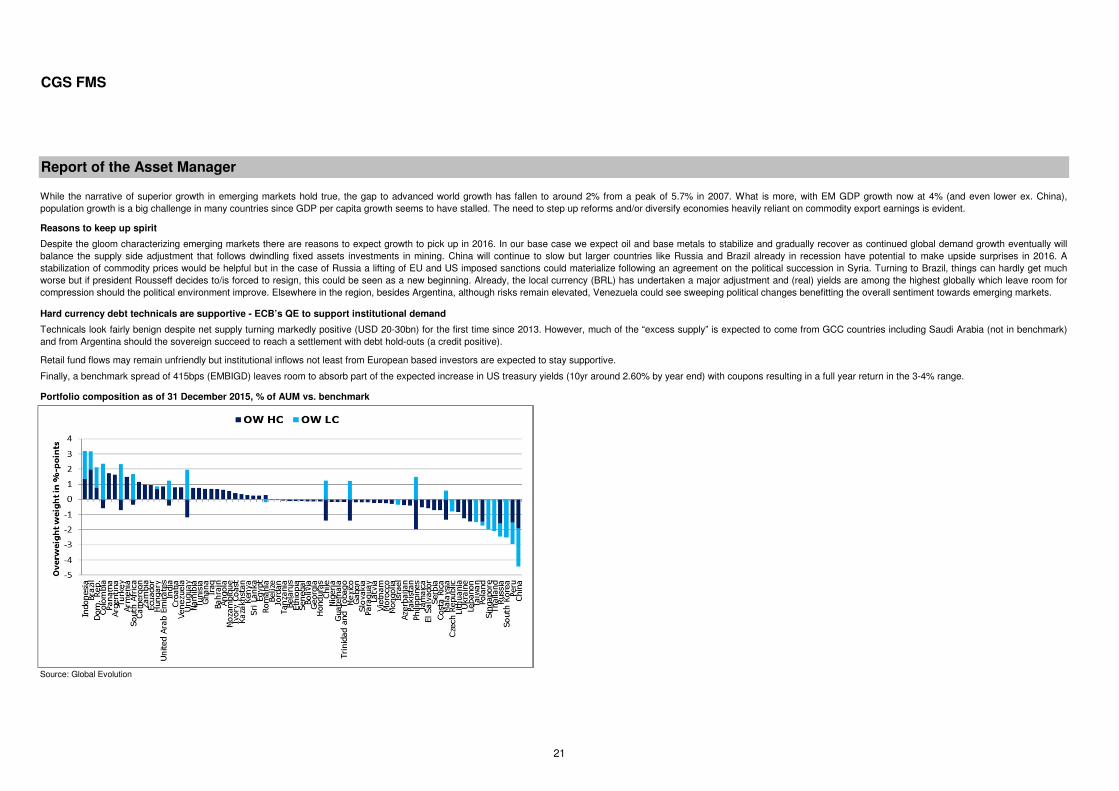

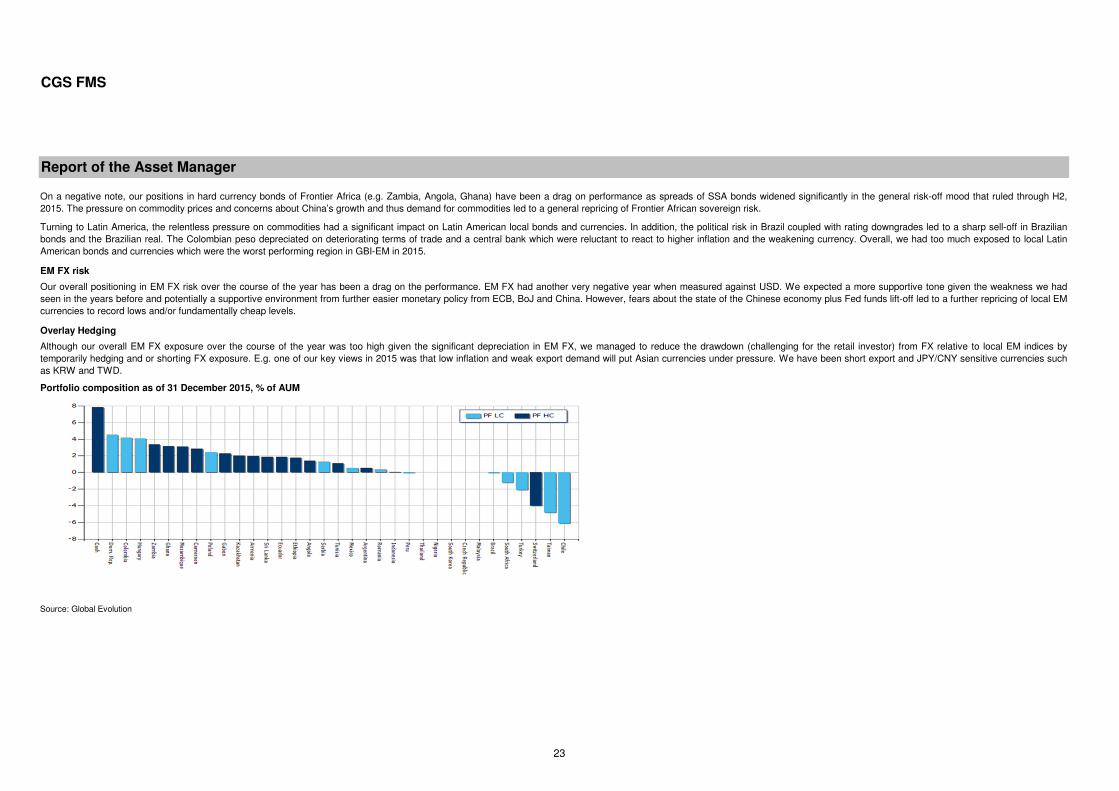

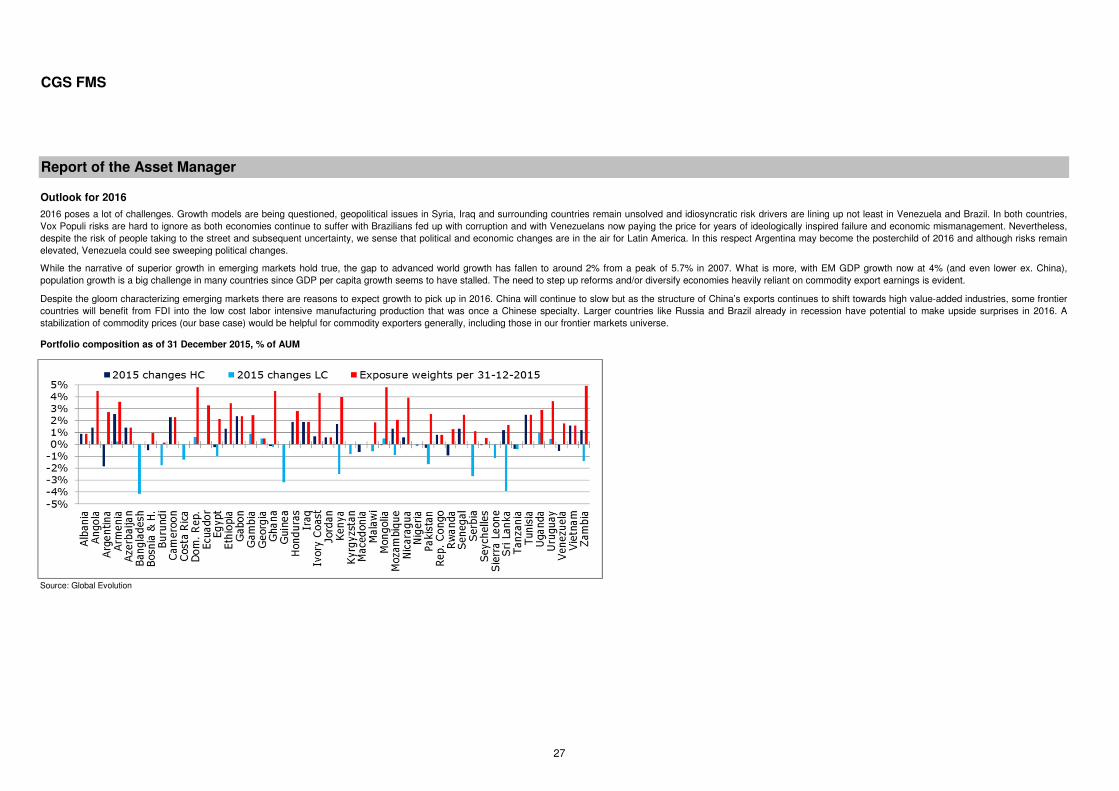

Portfolio composition as of 31 December 2015, % of AUM

12

CGS FMS

Report of the Asset Manager

Global Evolution EM Debt

The objective of the sub-fund is to create attractive returns by utilizing a non-benchmark focused and diversified strategy within emerging markets by focusing primarily on sovereign hard currency debt, but also on strategies that includesovereign local currency denominated debt and currency instruments.

Performance drivers for 2015 for the relevant sub fund

Last year’s market environment

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

Investment Objective

The funds exposure to Argentina proved a notable performance driver in 2015 as investors started to price in a political transition. As it turned out, president elect Mauricio Macri kept his election promise and lifted FX controls as a harbinger ofsweeping economic policy changes following 12 years of economic mismanagement under the Kirchner dynasty.

To the contrary, a long standing zero weight in Russia was a major drag on relative performance in 2015 as Russian assets saw a huge turnaround. For quite some time we have argued that we needed more evidence that the conflict withUkraine would not escalate and that oil prices were stabilizing as a minimum. By mid-November we decided to invest in Russia again (in EUR-denominated debt) since we believed that both conditions were more or less met. At the time weexpected oil prices to bottom out around USD 40 per barrel and the ceasefire in Ukraine to hold as Russia was more focused on Syria. Also affecting our investment decision, the West seemed happy to forget (if not forgive) Russia’sinterference in Eastern Ukraine and the annexation of Crimea in order to get Russia on board in a united front against ISIS. By year-end 2015 we were still underweighted Russia because we believed the positive expectations were now wellreflected in the pricing of Russian bonds which are back at pre-crisis levels.

A new oil order governed by Saudi Arabia

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

(Geo)political risks came to the fore

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years,European based institutional investors were left with little choice but to move up in duration or move down in credit quality. With no doubt this helped explain the contradiction between ongoing redemptions in EM debt dedicated retail funds anda solid institutional pipeline for hard currency EM mandates. Turning to the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger on rate hikes on December 16, 2015. 10yr US treasuryyields finished the year little changed; up from 2.17% to 2.27%.

13

CGS FMS

Report of the Asset Manager

Technicals are supportive - ECB’s QE to support institutional demand

Technicals look fairly benign despite net supply turning markedly positive (USD 20-30bn) for the first time since 2013. However, much of the “excess supply” is expected to come from GCC countries including Saudi Arabia (not in benchmark)and from Argentina should the sovereign succeed to reach a settlement with debt hold-outs (a credit positive).

Retail fund flows may remain unfriendly but institutional inflows not least from European based investors are expected to stay supportive.

Finally, a benchmark spread of 415bps (EMBIGD) leaves room to absorb part of the expected increase in US treasury yields (we expect 10yr yields around 2.60% by year end) with coupons resulting in a full year return in the 3-4% range.

In our base case we expect oil and base metals to stabilize and gradually recover in 2016 as continued global demand growth eventually will balance the supply side adjustment that follows dwindling fixed assets investments in mining.

In neighboring Ukraine, our zero-weight here also proved to be a large drag on relative performance. The country suffered - economically and politically - due to territorial hardship in East Ukraine and tensions with neighboring Russia but aprogram was agreed with the IMF and has for the most part been adhered to. We and the market generally expected a fairly tough debt restructuring and Ukraine’s sovereign debt as a consequence rallied hard as the restructuring included arather benign 20% principal write-down, a 7.75% coupon and a 4 year maturity extension with a GDP-linked component. In other words, the terms proved far more investor-friendly than expected, especially due to the lack of coupon cuts. Webelieve the terms could and should have been better for Ukraine and that economic and political risks remain in place. Hence, we maintained our zero-weight for 2015.

Outlook for 2016

2016 poses a lot of challenges. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela and Brazil. In both countries,Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians feed up with corruption and Venezuelans now paying the price for years of ideologically inspired failure and economic mismanagement. Nevertheless,despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of 2016 and although risks remainelevated, Venezuela could see sweeping political changes.

While the narrative of superior growth in emerging markets hold true, the gap to advanced world growth has fallen to around 2% from a peak of 5.7% in 2007. What is more, with EM GDP growth now at 4% (and even lower ex. China),population growth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Oil and base metals to gradually recover

Reasons to keep up spirit

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. China will continue to slow but larger countries like Russia and Brazil already in recession have potential to make upside surprises in2016. A stabilization of commodity prices (our base case) would be helpful for both countries but in the case of Russia a lifting of EU and US imposed sanctions could materialize following an agreement on the political succession in Syria.Turning to Brazil, things can hardly get much worse but if president Rousseff decides to or is forced to resign, this could be seen as a new beginning.

14

CGS FMS

Report of the Asset Manager

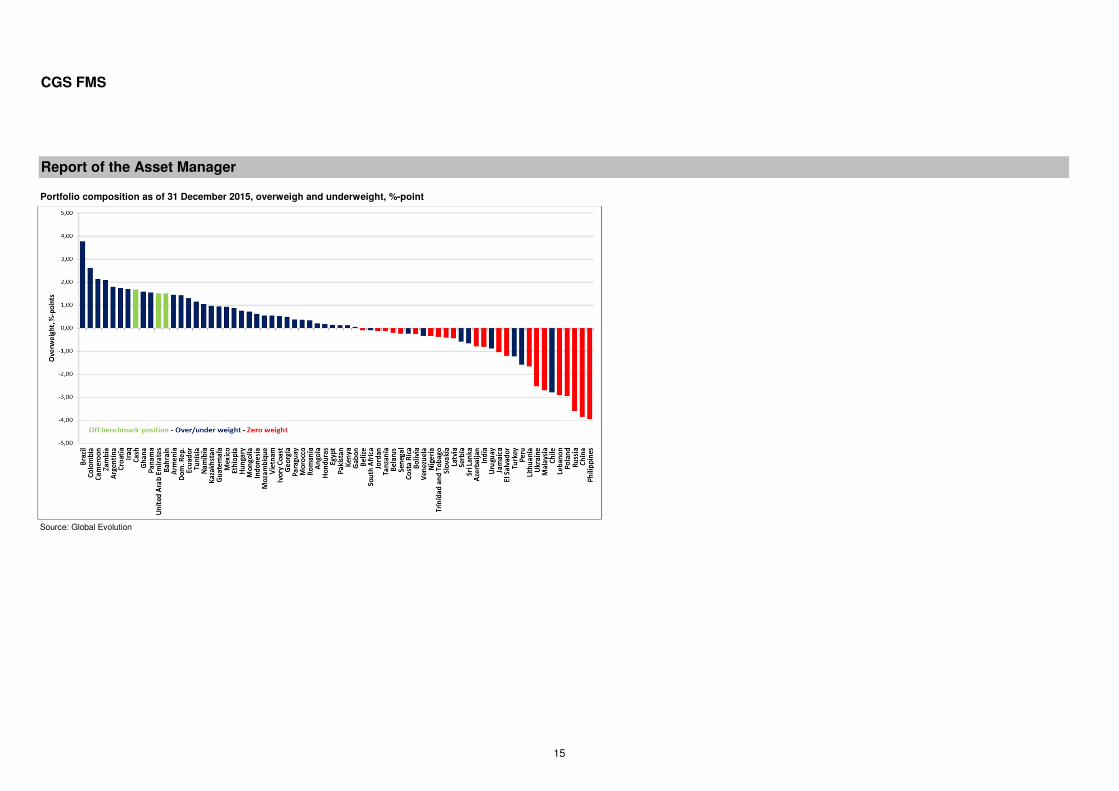

Portfolio composition as of 31 December 2015, overweigh and underweight, %-point

Source: Global Evolution

15

CGS FMS

Report of the Asset Manager

Global Evolution EM Local Debt

Performance drivers for 2015 for the relevant sub fund

Colombia was a strong contributor to outperformance; the currency risk was managed well on the back of our calls on oil prices. Colombia is an oil exporter and the fund's performance benefitted from an underweight from June to August whenoil prices collapsed 35%. Later we covered the underweight to hold a small overweight by year-end.

Also adding to positive performance, the Dominican Republic - being an oil importer - has benefitted from the slump in oil prices with the fiscal windfall estimated to be around 0.5% of GDP. The Dominican Republic remains a positive credit storythat is currently underpinned by low oil prices, broad monetary stability and improving fiscal performance and with local fixed income being remarkable stable in 2015, the fund benefitted from high carry and yield compression amid fiscalconsolidation resulting in a primary surplus.

(Geo)political risks came to the fore

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years, andEuropean based institutional investors were left with little choice but to move up in duration or move down in credit quality. In the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger onrate hikes on December 16. 10yr US treasury yields finished the year little changed; up from 2.17% to 2.27%. However, in FX markets the dollar strengthened from EUR/USD 1.2098 to an intra-year low of EUR/USD 1.0496 but the currency pairrecovered to finish the year in 1.0862. The Federal Reserve’s broad trade weighted dollar index gained 9.7% in 2015.

Investment Objective

The objective of the sub-fund is to create attractive returns by utilizing a non-benchmark focused and diversified strategy within emerging markets focusing on sovereign local currency denominated debt and currency instruments.

Last year’s market environment

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

A new oil order governed by Saudi Arabia

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

Pegged currency regimes faced strong headwinds

As hard commodities continued lower commodity backed currencies came increasingly under pressure. A number of exporters gave up their currency peg (Kazakhstan, Azerbaijan), but a few die hard pegged regimes (Saudi Arabia, Nigeria)stayed put.

16

CGS FMS

Report of the Asset Manager

Source: Global Evolution

Closer to home we held a large underweight to Eastern Europe in early 2015 because we expected noisy headlines from the Euro-area would have a negative impact on EUR/USD and CEE-performance. The call played out well; EUR/USDplummeted from around 1.20 area to around 1.05 in a matter of a few months. By mid-March we covered most of the underweight in time to lock in profits before EUR/USD in May recovered all the way back to 1.15.

Still in Europe, a long standing zero weight in Russia went against us as the Ruble and Russian local fixed income staged a huge turnaround. For quite some time we have argued that we needed more evidence that the conflict with Ukrainewould not escalate and that oil prices were stabilizing as a minimum. By mid-November we decided to invest in Russia again since we believed that both conditions were more or less met. At the time we expected oil prices bottoming out aroundUSD 40 per barrel and the ceasefire in Ukraine to hold as Russia was more focused on Syria. Also affecting our investment decision, the West seemed happy to forget (if not forgive) Russia’s interference in Eastern Ukraine and the annexationof Crimea in order to get Russia on board in a united front against ISIS. Clearly our call on oil was wrong and since then we have seen further ruble weakness. By year-end we remained underweight Russia, though.

Turning to Latin America, in Brazil the flow of negative news seemed endless in 2015 with the governing PT burdened under the biggest bribery scandal in history (state-owned Petrobras) and fundamentals continuously deteriorating. This wasnot left unnoticed by rating agencies, but despite Petrobras and the sovereign losing their respective investment grade rating and popular calls for president Rousseff to step down, president Rousseff chose to stay put. We entered 2015 into ourposition with a fairly large relatively overweight in expectation of a more pragmatic government and a congress that would get its act together. That clearly did not play out the way we had hoped and in May we cut exposure to first neutral andlater slightly underweight the benchmark. We still believe that valuations are attractive, but a move back to overweight will have to wait until we see political commitment to address the economic and fiscal deterioration.

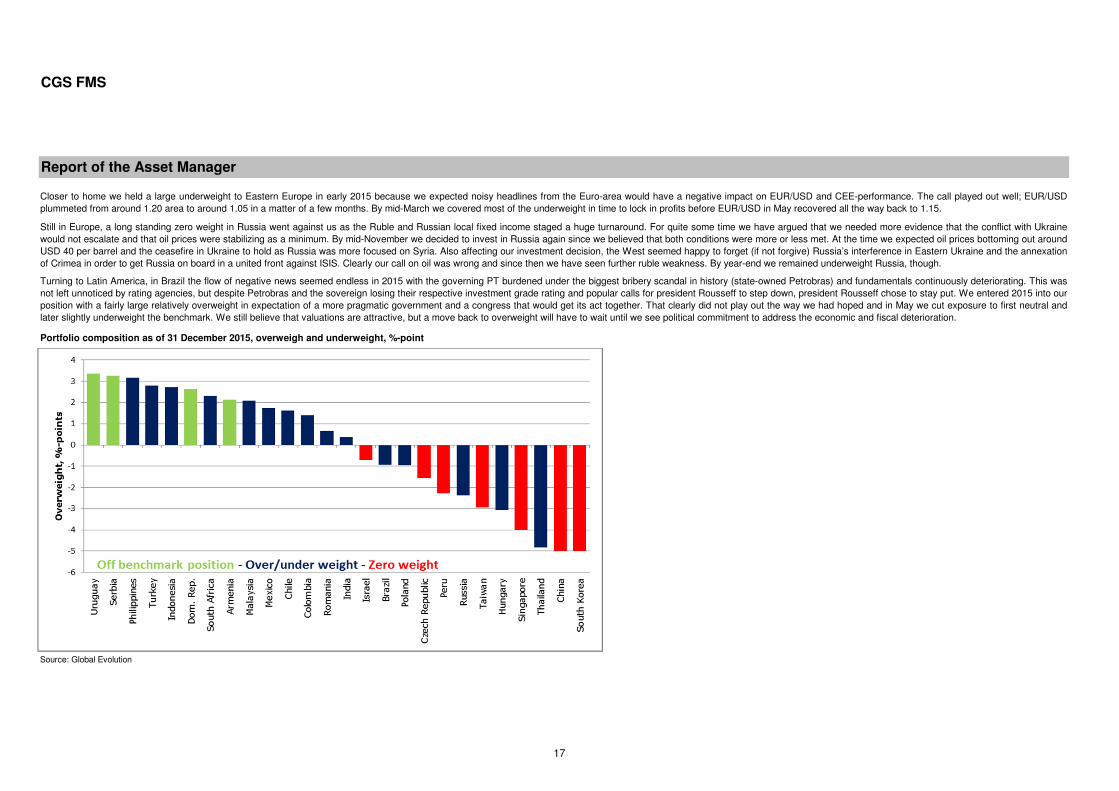

Portfolio composition as of 31 December 2015, overweigh and underweight, %-point

17

CGS FMS

Report of the Asset Manager

While the narrative of superior growth in emerging markets hold true, the gap to advanced world growth has fallen to around 2% from a peak of 5.7% in 2007. What is more, with EM GDP growth now at 4% (and even lower ex. China),population growth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. In our base case we expect oil and base metals to stabilize and gradually recover as continued global demand growth eventually willbalance the supply side adjustment that follows dwindling fixed assets investments in mining. China will continue to slow but larger countries like Russia and Brazil already in recession have potential to make upside surprises in 2016. Astabilization of commodity prices would be helpful but in the case of Russia a lifting of EU and US imposed sanctions could materialize following an agreement on the political succession in Syria. Turning to Brazil, things can hardly get muchworse but if president Rousseff decides to/is forced to resign, this could be seen as a new beginning. Already, the local currency (BRL) has undertaken a major adjustment and (real) yields are among the highest globally which leave room forcompression should the political environment improve. Elsewhere in the region, although risks remain elevated, Venezuela could see sweeping political changes benefitting the overall sentiment towards emerging markets.

We expect EUR/USD to stay in the 1.05 - 1.15 range for now with a likely test of the lower bound in Q1 and Q2 before a recovery towards 1.15 in H2. Once EUR/USD begins to recover in earnest towards the upper bound in our range thiswould most likely be the trigger for a recovery in commodity prices.

Outlook for 2016

2016 poses a lot of challenges. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela and Brazil. In both countries,Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians feed up with corruption and with Venezuelans now paying the price for years of ideologically inspired failure and economic mismanagement. Nevertheless,despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of 2016 and although risks remainelevated, Venezuela could see sweeping political changes.

18

CGS FMS

Report of the Asset Manager

Global Evolution EM Blended Debt

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

The fund objective is to create attractive returns by utilizing a non-benchmark focused and diversified strategy within emerging markets focusing on sovereign hard currency debt, local currency denominated debt and currency instruments in adynamic and very actively managed format. To achieve the investment objective Global Evolution will dynamically manage the exposure to sovereign hard currency debt, local currency instruments and frontier markets.

Last year’s market environment

A new oil order governed by Saudi Arabia

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

Pegged currency regimes faced strong headwinds

As hard commodities continued lower, commodity backed currencies came increasingly under pressure. A number of exporters gave up their currency peg (Kazakhstan, Azerbaijan), but a few die hard pegged regimes (Saudi Arabia, Nigeria)stayed put.

(Geo)political risks came to the fore

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years,European based institutional investors were left with little choice but to move up in duration or move down in credit quality. With no doubt this helped explain the contradiction between ongoing redemptions in EM debt dedicated retail funds anda solid institutional pipeline for hard currency EM mandates. Turning to the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger on rate hikes on December 16. 10yr US treasury yieldsfinished the year little changed; up from 2.17% to 2.27%. However, in FX markets the dollar strengthened from EUR/USD 1.2098 to an intra-year low of EUR/USD 1.0496 but the currency pair recovered to finish the year in 1.0862. The FederalReserve’s broad trade weighted dollar index gained 9.7% in 2015.

Performance drivers for 2015 for the relevant sub fund

Despite a benchmark agnostic dynamic investment approach and a dedicated objective to exploit the ever changing investment themes, the fund performance proved unsatisfactory. In our blended allocation strategy we held local currency debt(including CCE currencies) underweight in Q1 in a bet that negative headlines involving Greece and the wider Euro-area would translate into risk aversion and a weaker EUR. As such our call was successful since EUR/USD plummeted fromaround 1.20 to around 1.05 in a matter of months. By end Q1 we gradually raised the share of local currency debt (including CCE currencies) to an overweight – a timely move considering the following spike in EUR/USD to 1.14 and someoptimism in commodity markets.

Investment Objective

19

CGS FMS

Report of the Asset Manager

In neighboring Ukraine, our zero-weight here also proved to be a large drag on relative performance. The country suffered - economically and politically - due to territorial hardship in East Ukraine and tensions with neighboring Russia but aprogram was agreed with the IMF and has for the most part been adhered to. We and the market generally expected a fairly tough debt restructuring and Ukraine’s sovereign debt as a consequence rallied hard as the restructuring included arather benign 20% principal write-down, a 7.75% coupon and a 4 year maturity extension with a GDP-linked component. In other words, the terms proved far more investor-friendly than expected, especially due to the lack of coupon cuts. Webelieve the terms could and should have been better for Ukraine and that economic and political risks remain in place. Hence, we maintained our zero-weight for 2015.

Outlook for 2016

2016 poses a lot of challenges. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela and Brazil. In both countries,Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians feed up with corruption and Venezuelans now paying the price for years of ideologically inspired failure and economic mismanagement. Nevertheless,despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of 2016 and although risks remainelevated, Venezuela could see sweeping political changes.

Allocation between hard currency debt and local currency debt, % of AuM

Source: Global Evolution

However, what really weighed on relative performance was Russia. A long standing zero weight in Russia (hard currency debt as well as local currency debt) went against us as Russian debt and FX staged a huge turnaround. For quite sometime we have argued that we needed more evidence that the conflict with Ukraine would not escalate and that oil prices were stabilizing as a minimum. By mid-November we decided to invest in Russia again since we believed that bothconditions were more or less met. At the time we expected oil prices bottoming out around USD 40 per barrel and the ceasefire in Ukraine to hold as Russia was more focused on Syria. Also affecting our investment decision, the West seemedhappy to forget (if not forgive) Russia’s interference in Eastern Ukraine and the annexation of Crimea in order to get Russia on board in a united front against ISIS. Clearly our call on oil was wrong and since then we have seen further rubleweakness.

During the summer months the share of local currency debt was lowered again to an underweight with this being based on risk/reward considerations in the face of renewed downside pressure in oil and metals. From late August we took localcurrency debt overweight once again in a bet that the US fed would postpone lift-off (this proved correct). Still, as commodities kept sliding lower we gradually lowered the local currency debt exposure to around neutral.

20

CGS FMS

Report of the Asset Manager

While the narrative of superior growth in emerging markets hold true, the gap to advanced world growth has fallen to around 2% from a peak of 5.7% in 2007. What is more, with EM GDP growth now at 4% (and even lower ex. China),population growth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Reasons to keep up spirit

Retail fund flows may remain unfriendly but institutional inflows not least from European based investors are expected to stay supportive.

Finally, a benchmark spread of 415bps (EMBIGD) leaves room to absorb part of the expected increase in US treasury yields (10yr around 2.60% by year end) with coupons resulting in a full year return in the 3-4% range.

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. In our base case we expect oil and base metals to stabilize and gradually recover as continued global demand growth eventually willbalance the supply side adjustment that follows dwindling fixed assets investments in mining. China will continue to slow but larger countries like Russia and Brazil already in recession have potential to make upside surprises in 2016. Astabilization of commodity prices would be helpful but in the case of Russia a lifting of EU and US imposed sanctions could materialize following an agreement on the political succession in Syria. Turning to Brazil, things can hardly get muchworse but if president Rousseff decides to/is forced to resign, this could be seen as a new beginning. Already, the local currency (BRL) has undertaken a major adjustment and (real) yields are among the highest globally which leave room forcompression should the political environment improve. Elsewhere in the region, besides Argentina, although risks remain elevated, Venezuela could see sweeping political changes benefitting the overall sentiment towards emerging markets.

Source: Global Evolution

Hard currency debt technicals are supportive - ECB’s QE to support institutional demand

Portfolio composition as of 31 December 2015, % of AUM vs. benchmark

Technicals look fairly benign despite net supply turning markedly positive (USD 20-30bn) for the first time since 2013. However, much of the “excess supply” is expected to come from GCC countries including Saudi Arabia (not in benchmark)and from Argentina should the sovereign succeed to reach a settlement with debt hold-outs (a credit positive).

21

CGS FMS

Report of the Asset Manager

Global Evolution EM Debt and FX

The objective is to achieve capital appreciation through well diversified investments in emerging and frontier market debt and FX with an absolute return focus.

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

A new oil order governed by Saudi Arabia

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

Pegged currency regimes faced strong headwinds

As hard commodities continued lower commodity backed currencies came increasingly under pressure. A number of exporters gave up their currency peg (Kazakhstan, Azerbaijan), but a few die hard pegged regimes (Saudi Arabia, Nigeria)stayed put.

(Geo)political risks came to the fore

Dominican local fixed income was remarkably stable in 2015 as the sovereign benefitted from an improving credit story amidst low oil prices adding a fiscal dividend boost of around 0.5% of GDP. High carry and gradual yield compression drivenby fiscal consolidation, reforms and the achievement of a primary surplus combined with a stable currency versus the USD resulted in a positive performance contribution.

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years,European based institutional investors were left with little choice but to move up in duration or move down in credit quality. With no doubt this helped explain the contradiction between ongoing redemptions in EM debt dedicated retail funds anda solid institutional pipeline for hard currency EM mandates. Turning to the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger on rate hikes on December 16, 2015. 10yr US treasuryyields finished the year little changed; up from 2.17% to 2.27%. However, in FX markets the dollar strengthened from EUR/USD 1.2098 to an intra-year low of EUR/USD 1.0496 but the currency pair recovered to finish the year in 1.0862. TheFederal Reserve’s broad trade weighted dollar index gained 9.7% in 2015.

Performance drivers for 2015 for the relevant sub fund

Eastern Europe performed relatively well in the stormy seas of Emerging markets in 2015. The Greek crisis only had a temporary impact on the region while the ECB QE gave it a firm anchor. Local bonds of Hungary, Poland and Romania didrelatively well as central banks eased monetary policy further amidst very low inflation. Our exposure in Eastern Europe was on average the highest of all the regions and we still like the exposure into 2016 given the monetary policy outlook forboth the ECB and the central banks of the region.

Last year’s market environment

Investment Objective

22

CGS FMS

Report of the Asset Manager

Our overall positioning in EM FX risk over the course of the year has been a drag on the performance. EM FX had another very negative year when measured against USD. We expected a more supportive tone given the weakness we hadseen in the years before and potentially a supportive environment from further easier monetary policy from ECB, BoJ and China. However, fears about the state of the Chinese economy plus Fed funds lift-off led to a further repricing of local EMcurrencies to record lows and/or fundamentally cheap levels.

Overlay Hedging

Source: Global Evolution

Although our overall EM FX exposure over the course of the year was too high given the significant depreciation in EM FX, we managed to reduce the drawdown (challenging for the retail investor) from FX relative to local EM indices bytemporarily hedging and or shorting FX exposure. E.g. one of our key views in 2015 was that low inflation and weak export demand will put Asian currencies under pressure. We have been short export and JPY/CNY sensitive currencies suchas KRW and TWD.

Portfolio composition as of 31 December 2015, % of AUM

On a negative note, our positions in hard currency bonds of Frontier Africa (e.g. Zambia, Angola, Ghana) have been a drag on performance as spreads of SSA bonds widened significantly in the general risk-off mood that ruled through H2,2015. The pressure on commodity prices and concerns about China’s growth and thus demand for commodities led to a general repricing of Frontier African sovereign risk.

Turning to Latin America, the relentless pressure on commodities had a significant impact on Latin American local bonds and currencies. In addition, the political risk in Brazil coupled with rating downgrades led to a sharp sell-off in Brazilianbonds and the Brazilian real. The Colombian peso depreciated on deteriorating terms of trade and a central bank which were reluctant to react to higher inflation and the weakening currency. Overall, we had too much exposed to local LatinAmerican bonds and currencies which were the worst performing region in GBI-EM in 2015.

EM FX risk

23

CGS FMS

Report of the Asset Manager

Reasons to keep up spirit

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. In our base case we expect oil and base metals to stabilize and gradually recover as continued global demand growth eventually willbalance the supply side adjustment that follows dwindling fixed assets investments in mining. China will continue to slow but larger countries like Russia and Brazil already in recession have potential to make upside surprises in 2016. Astabilization of commodity prices would be helpful but in the case of Russia a lifting of EU and US imposed sanctions could materialize following an agreement on the political succession in Syria. Turning to Brazil, things can hardly get muchworse but if president Rousseff decides to/is forced to resign, this could be seen as a new beginning. Already, the local currency (BRL) has undertaken a major adjustment and (real) yields are among the highest globally which leave room forcompression should the political environment improve. Elsewhere in the region, besides Argentina, although risks remain elevated, Venezuela could see sweeping political changes benefitting the overall sentiment towards emerging markets.

Hard currency debt technicals are supportive - ECB’s QE to support institutional demand

Technicals look fairly benign despite net supply turning markedly positive (USD 20-30bn) for the first time since 2013. However, much of the “excess supply” is expected to come from GCC countries including Saudi Arabia (not in benchmark)and from Argentina should the sovereign succeed to reach a settlement with debt hold-outs (a credit positive).

Retail fund flows may remain unfriendly but institutional inflows not least from European based investors are expected to stay supportive.

Outlook for 2016

2016 poses a lot of challenges… but also opportunities. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela andBrazil. In both countries, Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians feed up with corruption and Venezuelans now paying the price for years of ideologically inspired failure and economicmismanagement. Nevertheless, despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of2016 and although risks remain elevated, Venezuela could see sweeping political changes.

While the narrative of superior growth in emerging markets hold true, the gap to advanced world growth has fallen to around 2% from a peak of 5.7% in 2007. What is more, with EM GDP growth now at 4% (and even lower ex. China),population growth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Finally, a benchmark spread of 415bps (EMBIGD) leaves room to absorb part of the expected increase in US treasury yields (10yr around 2.60% by year end).

24

CGS FMS

Report of the Asset Manager

Global Evolution Emerging Frontier

A new oil order governed by Saudi Arabia

Pegged currency regimes faced strong headwinds

As hard commodities continued lower commodity backed currencies came increasingly under pressure. A number of exporters gave up their currency peg (Kazakhstan, Azerbaijan), but a few die hard pegged regimes (Saudi Arabia, Nigeria)stayed put.

In H1 oil recovered some of the losses from late 2014 and early 2015. However, in H2 2015 oil and other hard commodities tanked leaving commodity exporters in pain and the December 4 OPEC meeting dealt another blow to oil prices as itbecame clear that the organization’s mission statement to “coordinate and unify the petroleum policies of its Member Countries and ensure the stabilization of oil markets” in effect had been replaced by a new oil order governed by Saudi Arabiawith the aim to defend and expand market shares at any price.

Investment Objective

The objective of the Global Evolution Emerging Frontier strategy is to create attractive returns by utilizing a non-benchmark focused and diversified strategy within sovereign frontier emerging markets globally. The fund invests in hard currencyand local currency instruments as well as foreign exchange. To achieve the investment objective Global Evolution will use a range of financial instruments (local currency debt instruments, hard currency debt instruments and foreign exchange)and derivative financial instruments (interest rate futures, interest rate swaps, total return swaps, credit default swaps, FX forwards, FX options and non-deliverable forwards).

Last year’s market environment

Broadly speaking, 2015 was certainly not a bed of roses. Starting in H1, in Europe the Greek saga made headlines as the ruling Syriza first resisted austerity and later, in a U-turn, surrendered to the Troika’s austerity demand. Meanwhile, amidongoing China growth worries, Chinese benchmark stock indices went from Good to Stellar and by mid-June the Shanghai Shenzhen 300 had made a 12 months return of around 150%. Having ignored many warning signs of a bubble in themaking, the ensuing crash caught the media’s full attention spelling doom and gloom over the Chinese economy and global commodity markets. An unexpected 1.8% devaluation of the Chinese renminbi in August and a shift to a market basedFX fixing regime added fuel to the fire.

10yr US treasury yields finished the year little changed; up from 2.17% to 2.27%. However, in FX markets the dollar strengthened from EUR/USD 1.2098 to an intra-year low of EUR/USD 1.0496 but the currency pair recovered to finish the yearin 1.0862. The Federal Reserve’s broad trade weighted dollar index gained 9.7% in 2015.

To be fair, some sovereign credits also suffered from homegrown problems. In Brazil and South Africa corruption charges, stalled reform momentums and fiscal paralysis were the prime focus areas, whereas oil exporting Venezuela was in aleague of its own in terms of economic disrepair. Brazil, once poster child for dynamic development, was eventually downgraded to junk.

Closer to home Syria turned into a geopolitical crisis involving not only neighboring countries but also the EU and NATO as Syrian refugees crossed the borders to EU in volumes and Turkey downed a Russian fighter jet on the Turkish-Syrianborder. The stand-off between Kiev and separatists in Eastern Ukraine remained largely unsolved, but as tensions gradually eased the media lost interest in the conflict. Ukraine finalized an investor friendly restructuring of its sovereign hardcurrency debt but defaulted on USD 3bn of debt owed to Russia.

Monetary policy divergence became a theme

Still in Europe, the European Central Bank (ECB) joined the QE club in March with an expansion and extension announcement in early December. This helped drive down core European yields in negative territory in tenors up till 5-6 years,European based institutional investors were left with little choice but to move up in duration or move down in credit quality. With no doubt this helped explain the contradiction between ongoing redemptions in EM debt dedicated retail funds anda solid institutional pipeline for hard currency EM mandates. Turning to the US, following a shaky hand and a failed attempt in September, the US Federal Reserve finally pulled the trigger on rate hikes on December 16, 2015.

The trade weighted dollar index gained almost 9%

(Geo)political risks came to the fore

25

CGS FMS

Report of the Asset Manager

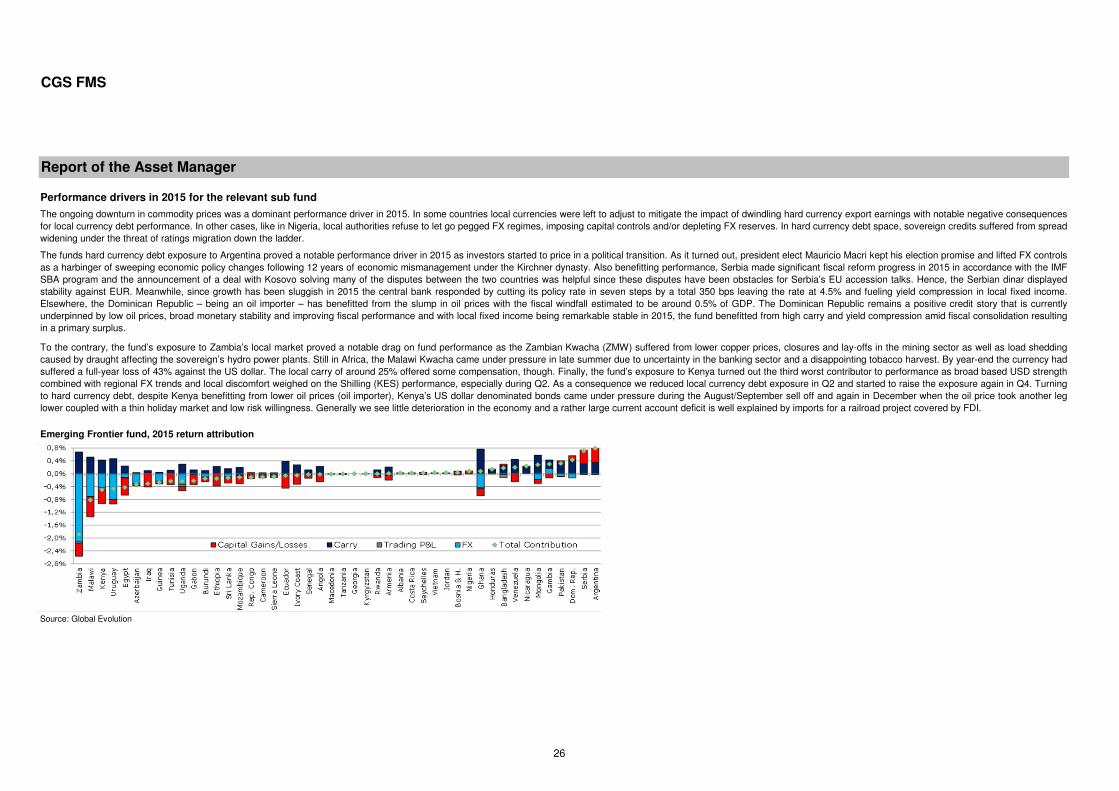

Emerging Frontier fund, 2015 return attribution

Source: Global Evolution

To the contrary, the fund’s exposure to Zambia’s local market proved a notable drag on fund performance as the Zambian Kwacha (ZMW) suffered from lower copper prices, closures and lay-offs in the mining sector as well as load sheddingcaused by draught affecting the sovereign’s hydro power plants. Still in Africa, the Malawi Kwacha came under pressure in late summer due to uncertainty in the banking sector and a disappointing tobacco harvest. By year-end the currency hadsuffered a full-year loss of 43% against the US dollar. The local carry of around 25% offered some compensation, though. Finally, the fund’s exposure to Kenya turned out the third worst contributor to performance as broad based USD strengthcombined with regional FX trends and local discomfort weighed on the Shilling (KES) performance, especially during Q2. As a consequence we reduced local currency debt exposure in Q2 and started to raise the exposure again in Q4. Turningto hard currency debt, despite Kenya benefitting from lower oil prices (oil importer), Kenya’s US dollar denominated bonds came under pressure during the August/September sell off and again in December when the oil price took another leglower coupled with a thin holiday market and low risk willingness. Generally we see little deterioration in the economy and a rather large current account deficit is well explained by imports for a railroad project covered by FDI.

Performance drivers in 2015 for the relevant sub fund

The ongoing downturn in commodity prices was a dominant performance driver in 2015. In some countries local currencies were left to adjust to mitigate the impact of dwindling hard currency export earnings with notable negative consequencesfor local currency debt performance. In other cases, like in Nigeria, local authorities refuse to let go pegged FX regimes, imposing capital controls and/or depleting FX reserves. In hard currency debt space, sovereign credits suffered from spreadwidening under the threat of ratings migration down the ladder.

The funds hard currency debt exposure to Argentina proved a notable performance driver in 2015 as investors started to price in a political transition. As it turned out, president elect Mauricio Macri kept his election promise and lifted FX controlsas a harbinger of sweeping economic policy changes following 12 years of economic mismanagement under the Kirchner dynasty. Also benefitting performance, Serbia made significant fiscal reform progress in 2015 in accordance with the IMFSBA program and the announcement of a deal with Kosovo solving many of the disputes between the two countries was helpful since these disputes have been obstacles for Serbia’s EU accession talks. Hence, the Serbian dinar displayedstability against EUR. Meanwhile, since growth has been sluggish in 2015 the central bank responded by cutting its policy rate in seven steps by a total 350 bps leaving the rate at 4.5% and fueling yield compression in local fixed income.Elsewhere, the Dominican Republic – being an oil importer – has benefitted from the slump in oil prices with the fiscal windfall estimated to be around 0.5% of GDP. The Dominican Republic remains a positive credit story that is currentlyunderpinned by low oil prices, broad monetary stability and improving fiscal performance and with local fixed income being remarkable stable in 2015, the fund benefitted from high carry and yield compression amid fiscal consolidation resultingin a primary surplus.

26

CGS FMS

Report of the Asset Manager

Source: Global Evolution

Outlook for 2016

2016 poses a lot of challenges. Growth models are being questioned, geopolitical issues in Syria, Iraq and surrounding countries remain unsolved and idiosyncratic risk drivers are lining up not least in Venezuela and Brazil. In both countries,Vox Populi risks are hard to ignore as both economies continue to suffer with Brazilians fed up with corruption and with Venezuelans now paying the price for years of ideologically inspired failure and economic mismanagement. Nevertheless,despite the risk of people taking to the street and subsequent uncertainty, we sense that political and economic changes are in the air for Latin America. In this respect Argentina may become the posterchild of 2016 and although risks remainelevated, Venezuela could see sweeping political changes.

While the narrative of superior growth in emerging markets hold true, the gap to advanced world growth has fallen to around 2% from a peak of 5.7% in 2007. What is more, with EM GDP growth now at 4% (and even lower ex. China),population growth is a big challenge in many countries since GDP per capita growth seems to have stalled. The need to step up reforms and/or diversify economies heavily reliant on commodity export earnings is evident.

Despite the gloom characterizing emerging markets there are reasons to expect growth to pick up in 2016. China will continue to slow but as the structure of China’s exports continues to shift towards high value-added industries, some frontiercountries will benefit from FDI into the low cost labor intensive manufacturing production that was once a Chinese specialty. Larger countries like Russia and Brazil already in recession have potential to make upside surprises in 2016. Astabilization of commodity prices (our base case) would be helpful for commodity exporters generally, including those in our frontier markets universe.

Portfolio composition as of 31 December 2015, % of AUM

27

CGS FMS

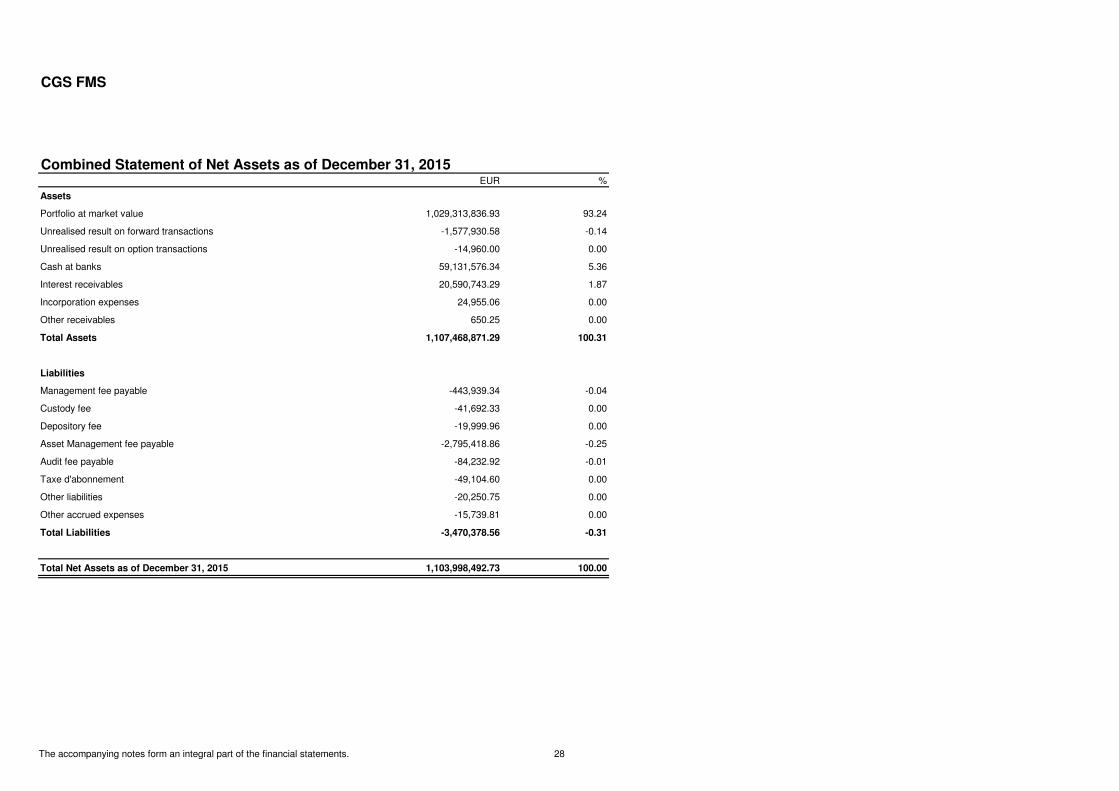

Combined Statement of Net Assets as of December 31, 2015EUR %

Assets

Portfolio at market value 1,029,313,836.93 93.24

Unrealised result on forward transactions -1,577,930.58 -0.14

Unrealised result on option transactions -14,960.00 0.00

Cash at banks 59,131,576.34 5.36

Interest receivables 20,590,743.29 1.87

Incorporation expenses 24,955.06 0.00

Other receivables 650.25 0.00

Total Assets 1,107,468,871.29 100.31

Liabilities

Management fee payable -443,939.34 -0.04

Custody fee -41,692.33 0.00

Depository fee -19,999.96 0.00

Asset Management fee payable -2,795,418.86 -0.25

Audit fee payable -84,232.92 -0.01

Taxe d'abonnement -49,104.60 0.00

Other liabilities -20,250.75 0.00

Other accrued expenses -15,739.81 0.00

Total Liabilities -3,470,378.56 -0.31

Total Net Assets as of December 31, 2015 1,103,998,492.73 100.00