16

Ch. 11 Credit and Debit

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | burton-nunez |

| View: | 12 times |

| Download: | 0 times |

Ch. 11Ch. 11

Credit and DebitCredit and Debit

If a friend asks you to borrow money what are some of the questions you are going to

ask?

If a friend asks you to borrow money what are some of the questions you are going to

ask?

Terms to KnowTerms to Know

• Credit - buy now, pay later• Creditor - party lending the money• Debtor - Party buying the

goods/services (borrrowing the money)• Interest - fee creditors charge for

lending money

• Credit - buy now, pay later• Creditor - party lending the money• Debtor - Party buying the

goods/services (borrrowing the money)• Interest - fee creditors charge for

lending money

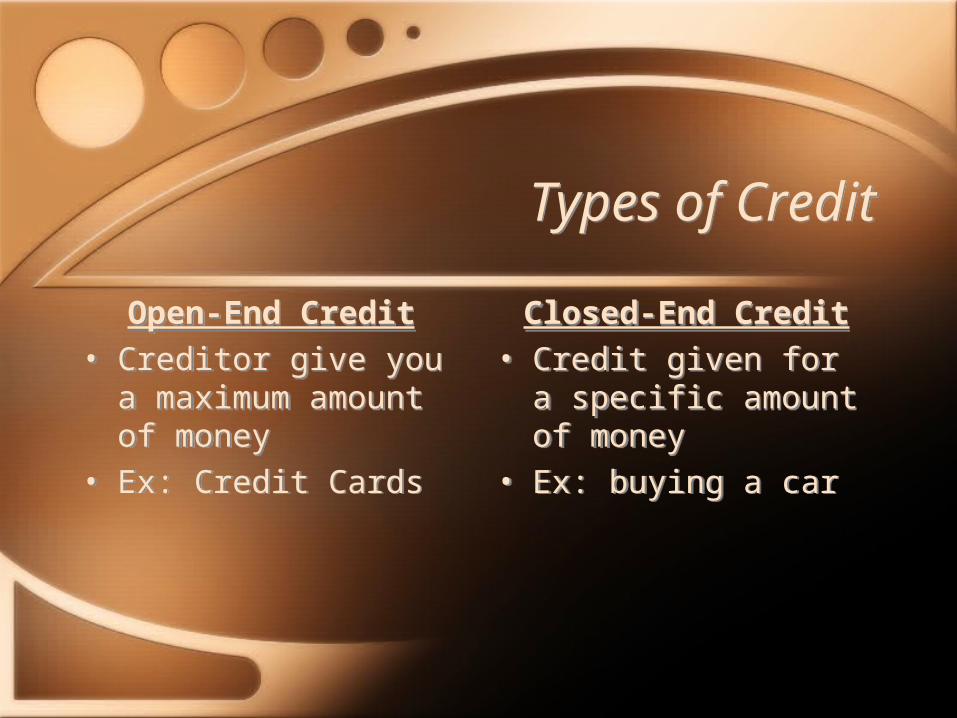

Types of CreditTypes of Credit

Open-End Credit• Creditor give you a

maximum amount of money

• Ex: Credit Cards

Open-End Credit• Creditor give you a

maximum amount of money

• Ex: Credit Cards

Closed-End Credit• Credit given for a

specific amount of money

• Ex: buying a car

Closed-End Credit• Credit given for a

specific amount of money

• Ex: buying a car

CreditCredit

• How do you obtain credit? • What do they look at?• What is the difference between credit

cards and debit cards?• How does repayment work?• What if you don’t repay?

• How do you obtain credit? • What do they look at?• What is the difference between credit

cards and debit cards?• How does repayment work?• What if you don’t repay?

Secured TransactionsSecured Transactions

• Secured Loan - Loan backed up with collateral that the credit can take if not paid.

• Collateral - property offered as a security interest

• Security Interest - creditor’s right to use collateral to recover debt

• Secured Party - Person holding security interest

• Default - not repaying the loan

• Secured Loan - Loan backed up with collateral that the credit can take if not paid.

• Collateral - property offered as a security interest

• Security Interest - creditor’s right to use collateral to recover debt

• Secured Party - Person holding security interest

• Default - not repaying the loan

Unsecured LoanUnsecured Loan

• Doesn’t require collateral• Interest is usually higher than a secured

loan

• Doesn’t require collateral• Interest is usually higher than a secured

loan

Buying a Car - Financing

Buying a Car - Financing

• Regulation Z of the Truth in Lending Act specifies lenders must disclose 2 things:

•APR - true interest rate of the loan•Finance Charge - cost of loan in $

and cents

• Regulation Z of the Truth in Lending Act specifies lenders must disclose 2 things:

•APR - true interest rate of the loan•Finance Charge - cost of loan in $

and cents

Things to know before you finance:

Things to know before you finance:

キキ Exact price of vehicle

キキ Amount you are financing

キキ Finance charge

キキ APR

キキ Number and amount of payments

キキ Total sales price

キキ Exact price of vehicle

キキ Amount you are financing

キキ Finance charge

キキ APR

キキ Number and amount of payments

キキ Total sales price

Defective VehiclesDefective Vehicles

• Seller can be held liable if:•Breach of express warranty, they made a promise to

do something and they didn’t do it.

Example: they are going to fix the alignment before you buy it and they don’t

•Breach of warranty of merchantability, seller was a dealer and the car was not fit to be driven.

• Seller can be held liable if:•Breach of express warranty, they made a promise to

do something and they didn’t do it.

Example: they are going to fix the alignment before you buy it and they don’t

•Breach of warranty of merchantability, seller was a dealer and the car was not fit to be driven.

Defective VehicleDefective Vehicle

• Seller can be held liable if:

•Fraud or breach of express warranty, seller made statements about the car that weren’t true

Example: seller said the car had new brakes when the brakes aren’t new

•Breach of the state consumer protection law, only if vehicle is for personal use.

• Seller can be held liable if:

•Fraud or breach of express warranty, seller made statements about the car that weren’t true

Example: seller said the car had new brakes when the brakes aren’t new

•Breach of the state consumer protection law, only if vehicle is for personal use.

Lemon LawLemon Law

• To be considered defective in many states it must be:• Substantially defective• At the dealer 3 time for repairs• No older than 1 year• Not exceed 15,000 miles

• To be considered defective in many states it must be:• Substantially defective• At the dealer 3 time for repairs• No older than 1 year• Not exceed 15,000 miles

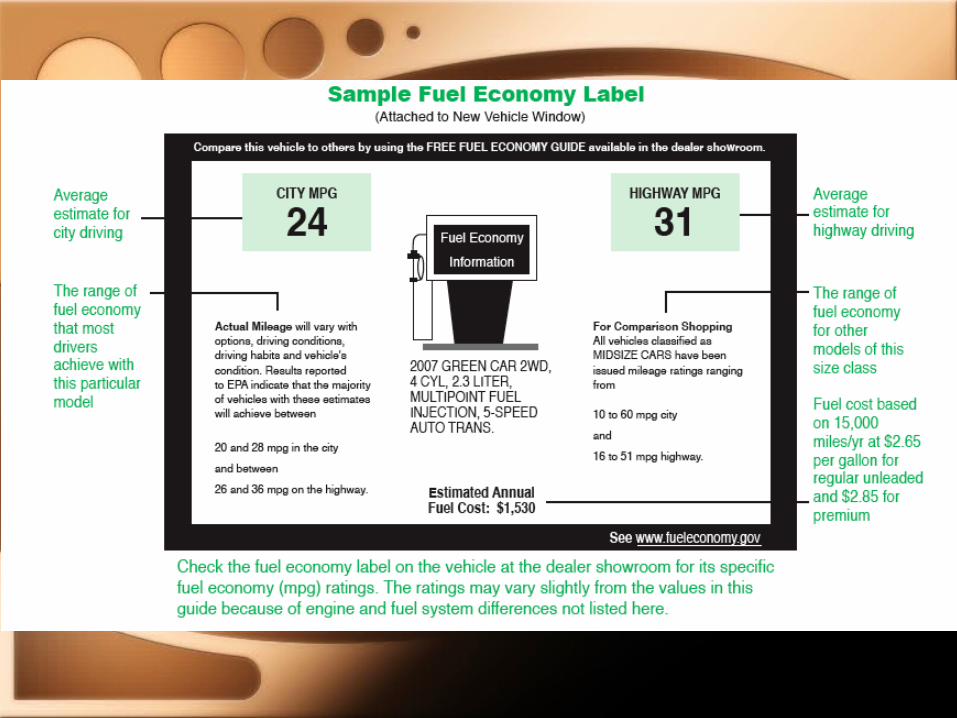

Motor Vehicle and Cost Savings Act

Motor Vehicle and Cost Savings Act

• Bumper Standards• Average Fuel economy standards

• Produce cars that use less fuel• Annual fuel cost listed• Range of fuel economy listed

• Odometer Protection• Can’t turn back/disconnect odometer

• Bumper Standards• Average Fuel economy standards

• Produce cars that use less fuel• Annual fuel cost listed• Range of fuel economy listed

• Odometer Protection• Can’t turn back/disconnect odometer

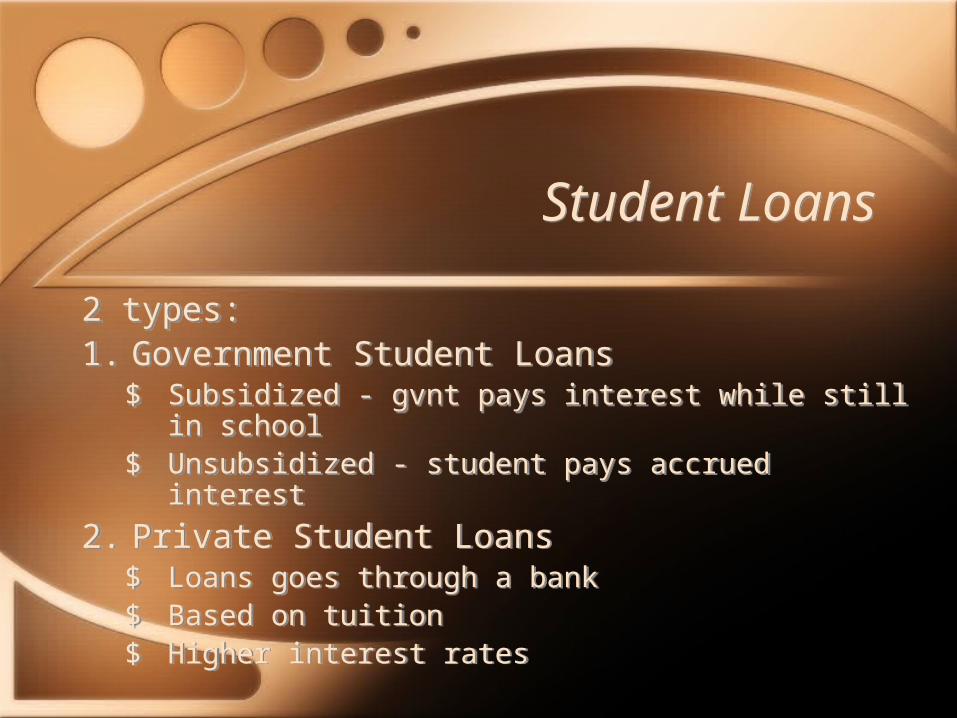

Student LoansStudent Loans

2 types:1. Government Student Loans$ Subsidized - gvnt pays interest while still in

school$ Unsubsidized - student pays accrued interest

2. Private Student Loans$ Loans goes through a bank$ Based on tuition$ Higher interest rates

2 types:1. Government Student Loans$ Subsidized - gvnt pays interest while still in

school$ Unsubsidized - student pays accrued interest

2. Private Student Loans$ Loans goes through a bank$ Based on tuition$ Higher interest rates

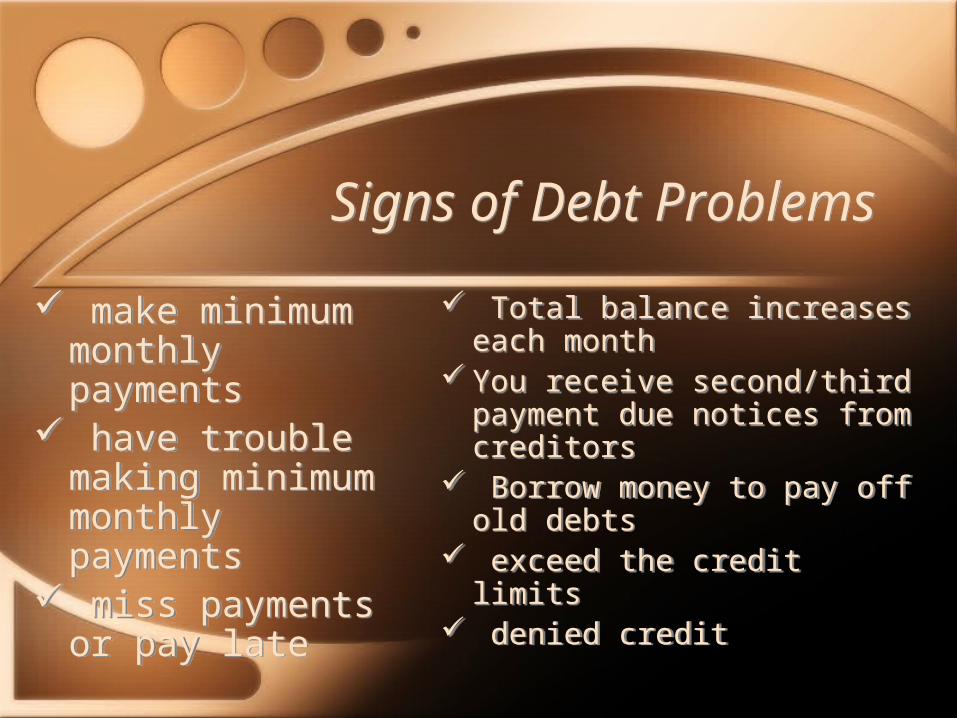

Signs of Debt Problems

Signs of Debt Problems

make minimum monthly payments

have trouble making minimum monthly payments

miss payments or pay late

make minimum monthly payments

have trouble making minimum monthly payments

miss payments or pay late

Total balance increases each month

You receive second/third payment due notices from creditors

Borrow money to pay off old debts

exceed the credit limits denied credit

Total balance increases each month

You receive second/third payment due notices from creditors

Borrow money to pay off old debts

exceed the credit limits denied credit