438 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION Chapter 9 introduced regression modeling of the relationship between two quantitative variables. Multivariate relationships require more complex models, containing several explanatory variables. Some of these may be predictors of theoretical interest, and some may be control variables. To predict Y = college GPA, for example, it is sensible to use several predictors in the same model. Possibilities include X 1 = high school GPA, X 2 = math college entrance exam score, X 3 = verbal college entrance exam score, and X 4 = rating by high school guidance counselor. This chapter presents models for the relationship between a response variable Y and a collection of explanatory variables. A multivariable model provides better predictions of Y than does a model with a single explanatory variable. Such a model also can analyze relationships between variables while controlling for other variables. This is important because Chapter 10 showed that after controlling for a variable, an association can appear quite different from when the variable is ignored. Thus, this model provides information not available with simple models that analyze only two variables at a time. Sections 11.1 and 11.2 extend the regression model to a multiple regression model that can have multiple explanatory variables. Section 11.3 defines correlation and r-squared measures that describe association between Y and a set of explanatory variables. Section 11.4 presents inference procedures for multiple regression. Section 11.5 shows how to allow statistical interaction in the model, and Section 11.6 presents a test of whether a complex model provides a better fit than a simpler model. The final two sections introduce measures that summarize the association between the response variable and an explanatory variable while controlling other variables. 11.1 The Multiple Regression Model Chapter 9 modeled the relationship between the explanatory variable X and the mean of the response variable Y by the straight-line (linear) equation E(Y )= α + βx. We refer to this model containing a single predictor as a bivariate model, because it contains only two variables. The Multiple Regression Function Suppose there are two explanatory variables, denoted by X 1 and X 2 . As in earlier chapters, we use lower-case letters to denote observations or particular values of the variables. The bivariate regression function generalizes to the multiple regression function E(Y )= α + β 1 x 1 + β 2 x 2 . In this equation, α, β 1 , and β 2 are parameters discussed below. For particular values of x 1 and x 2 , the equation specifies the population mean of Y for all subjects with those values of x 1 and x 2 . When there are additional explanatory variables, each has a βx term, for example E(Y )= α + β 1 x 1 + β 2 x 2 + β 3 x 3 + β 4 x 4 with four predictors. The multiple regression function is more difficult to portray graphically than the bivariate regression function. With two explanatory variables, the x 1 and x 2 axes are

Transcript

438 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

Chapter 9 introduced regression modeling of the relationship between two quantitative

variables. Multivariate relationships require more complex models, containing several

explanatory variables. Some of these may be predictors of theoretical interest, and

some may be control variables.

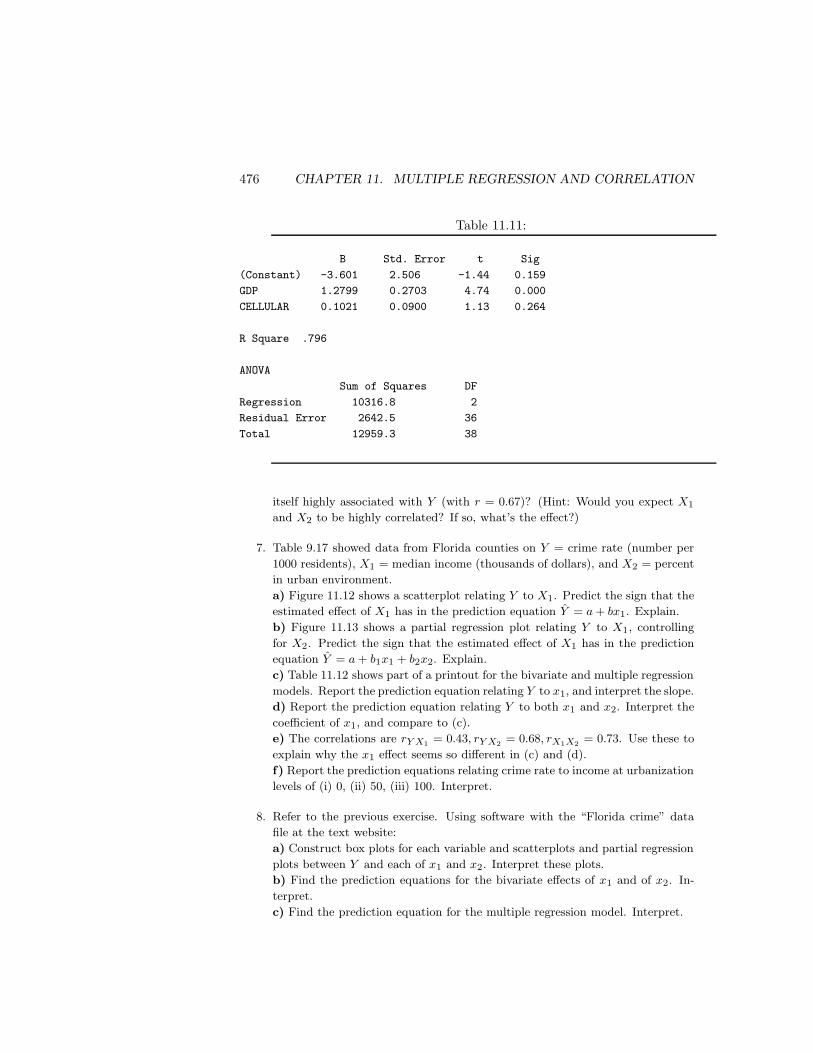

To predict Y = college GPA, for example, it is sensible to use several predictors

in the same model. Possibilities include X1 = high school GPA, X2 = math college

entrance exam score, X3 = verbal college entrance exam score, and X4 = rating by

high school guidance counselor. This chapter presents models for the relationship

between a response variable Y and a collection of explanatory variables.

A multivariable model provides better predictions of Y than does a model with

a single explanatory variable. Such a model also can analyze relationships between

variables while controlling for other variables. This is important because Chapter 10

showed that after controlling for a variable, an association can appear quite different

from when the variable is ignored. Thus, this model provides information not available

with simple models that analyze only two variables at a time.

Sections 11.1 and 11.2 extend the regression model to a multiple regression

model that can have multiple explanatory variables. Section 11.3 defines correlation

and r-squared measures that describe association between Y and a set of explanatory

variables. Section 11.4 presents inference procedures for multiple regression. Section

11.5 shows how to allow statistical interaction in the model, and Section 11.6 presents

a test of whether a complex model provides a better fit than a simpler model. The

final two sections introduce measures that summarize the association between the

response variable and an explanatory variable while controlling other variables.

11.1 The Multiple Regression Model

Chapter 9 modeled the relationship between the explanatory variable X and the mean

of the response variable Y by the straight-line (linear) equation E(Y ) = α + βx. We

refer to this model containing a single predictor as a bivariate model, because it

contains only two variables.

The Multiple Regression Function

Suppose there are two explanatory variables, denoted by X1 and X2. As in earlier

chapters, we use lower-case letters to denote observations or particular values of the

variables. The bivariate regression function generalizes to the multiple regression

function

E(Y ) = α + β1x1 + β2x2.

In this equation, α, β1, and β2 are parameters discussed below. For particular values

of x1 and x2, the equation specifies the population mean of Y for all subjects with

those values of x1 and x2. When there are additional explanatory variables, each has

a βx term, for example E(Y ) = α + β1x1 + β2x2 + β3x3 + β4x4 with four predictors.

The multiple regression function is more difficult to portray graphically than the

bivariate regression function. With two explanatory variables, the x1 and x2 axes are

11.1. THE MULTIPLE REGRESSION MODEL 439

Figure 11.1: Graphical Depiction of a Multiple Regression Function with TwoExplanatory Variables

((Fig. 11.1 in 3e))

perpendicular but lie in a horizontal plane and the Y axis is vertical and perpendicular

to both the x1 and x2 axes. The equation E(Y ) = α + β1x1 + β2x2 traces a plane (a

flat surface) cutting through three-dimensional space, as Figure 11.1 portrays.

The simplest interpretation treats all but one explanatory variable as control vari-

ables and fixes them at particular levels. This leaves an equation relating the mean

of Y to the remaining explanatory variable.

Example 11.1 Do Higher Levels of Education Cause Higher Crime Rates?

Exercise 39 in Chapter 9 contains recent data on several variables for the 67

counties in the state of Florida. For each county, let Y = crime rate (annual number

of crimes per 1000 population), X1 = education (percentage of adult residents having

at least a high school education), and X2 = urbanization (percentage living in an

urban environment).

The bivariate relationship between crime rate and education is approximated by

E(Y ) = −51.3 + 1.5x1. Surprisingly, the association is moderately positive, the cor-

relation being r = 0.47. As the percentage of county residents having at least a high

school education increases, so does the crime rate.

A closer look at the data reveals strong positive associations between crime rate

and urbanization (r = 0.68) and between education and urbanization (r = 0.79).

This suggests that the association between crime rate and education may be spurious.

Perhaps urbanization is a common causal factor. See Figure 11.2. As urbanization

increases, both crime rate and education increase, resulting in a positive correlation

between crime rate and education.

The relation between crime rate and both predictors considered together is ap-

proximated by the multiple regression function

E(Y ) = 58.9 − 0.6x1 + 0.7x2.

For instance, the expected crime rate for a county at the mean levels of education

Figure 11.2: The Positive Association Between Crime Rate and Education MayBe Spurious, Explained by the Effects of Urbanization on Each

((Fig. 11.2 in 3e))

440 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

(x1 = 70) and urbanization (x2 = 50) is E(Y ) = 58.9− 0.6(70) + 0.7(50) = 52 annual

crimes per 1000 population.

Let’s study the effect of x1, controlling for x2. We first set x2 at its mean level of

50. Then, the relationship between crime rate and education is

Figure 11.3 plots this line. Controlling for x2 by fixing it at 50, the relationship be-

tween crime rate and education is negative, rather than positive. The slope decreased

and changed sign from 1.5 in the bivariate relationship to −0.6. At this fixed level of

urbanization, a negative relationship exists between education and crime rate. We use

the term partial regression equation to distinguish the equation E(Y ) = 93.9 − 0.6x1

from the regression equation E(Y ) = −51.3 + 1.5x1 for the bivariate relationship

between Y and x1. The partial regression equation refers to part of the potential

observations, in this case counties having x2 = 50.

Figure 11.3: Partial Relationships Between E(Y ) and x1 for the Multiple Re-gression Equation E(Y ) = 58.9− 0.6x1 + 0.7x2. These partial regression equa-tions fix x2 to equal 50 or 40.

((Fig. 11.3 in 3e))

Next we fix x2 at a different level, say x2 = 40 instead of 50. Then, you can check

that E(Y ) = 86.9 − 0.6x1. Thus, decreasing x2 by 10 units shifts the partial line

relating Y to x1 downward by 10β2 = 7.0 units (see Figure 11.3). The slope of −0.6

for the partial relationship remains the same, so the line is parallel to the original one.

Setting x2 at a variety of values yields a collection of parallel lines, each having slope

β1 = −0.6.

Similarly, setting x1 at a variety of values yields a collection of parallel lines,

each having slope 0.7, relating the mean of Y to x2. In other words, controlling for

education, the slope of the partial relationship between crime rate and urbanization

is β2 = 0.7.

In summary, education has an overall positive effect on crime rate, but it has

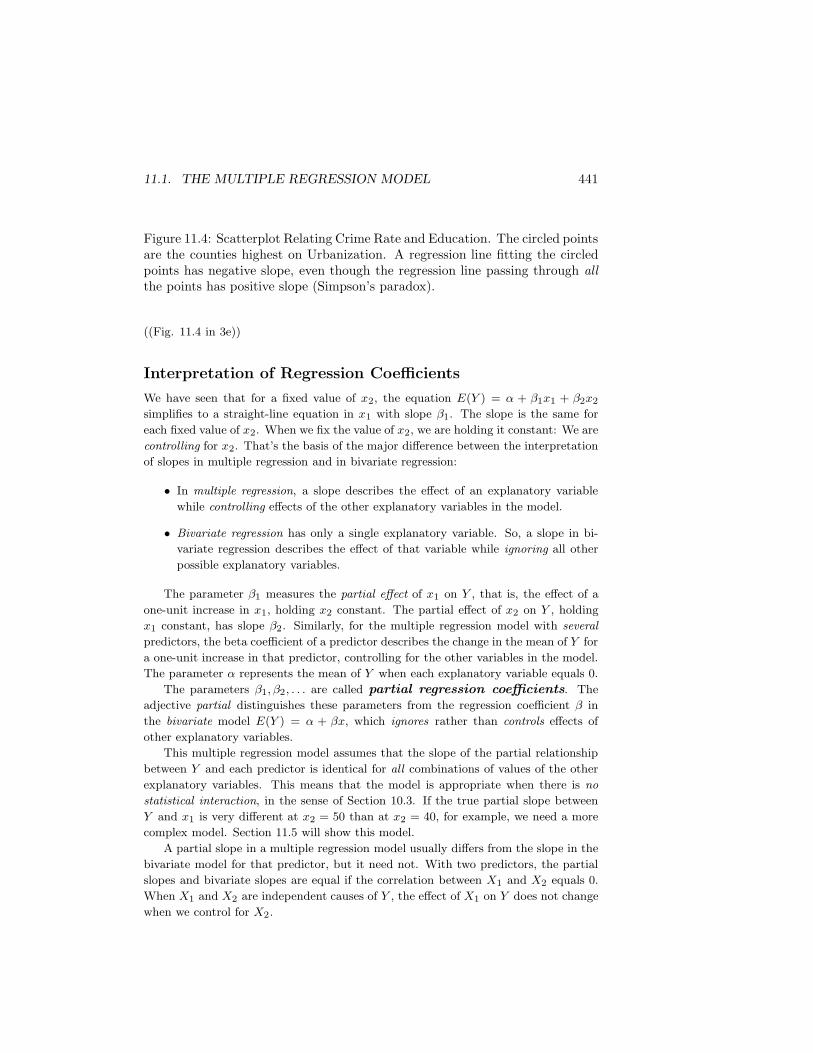

a negative effect when controlling for urbanization. The partial association has the

opposite direction from the bivariate association. This is called Simpson’s para-

dox. Figure 11.4 illustrates how this happens. It shows the scatterplot relating crime

rate to education, portraying the overall positive association between these variables.

The diagram circles the 19 counties that are highest in urbanization. That subset of

points for which urbanization is nearly constant has a negative trend between crime

rate and education. The high positive association between education and urbanization

is reflected by the fact that most of the highlighted observations that are highest on

urbanization also have high values on education.

2

11.1. THE MULTIPLE REGRESSION MODEL 441

Figure 11.4: Scatterplot Relating Crime Rate and Education. The circled pointsare the counties highest on Urbanization. A regression line fitting the circledpoints has negative slope, even though the regression line passing through all

the points has positive slope (Simpson’s paradox).

((Fig. 11.4 in 3e))

Interpretation of Regression Coefficients

We have seen that for a fixed value of x2, the equation E(Y ) = α + β1x1 + β2x2

simplifies to a straight-line equation in x1 with slope β1. The slope is the same for

each fixed value of x2. When we fix the value of x2, we are holding it constant: We are

controlling for x2. That’s the basis of the major difference between the interpretation

of slopes in multiple regression and in bivariate regression:

• In multiple regression, a slope describes the effect of an explanatory variable

while controlling effects of the other explanatory variables in the model.

• Bivariate regression has only a single explanatory variable. So, a slope in bi-

variate regression describes the effect of that variable while ignoring all other

possible explanatory variables.

The parameter β1 measures the partial effect of x1 on Y , that is, the effect of a

one-unit increase in x1, holding x2 constant. The partial effect of x2 on Y , holding

x1 constant, has slope β2. Similarly, for the multiple regression model with several

predictors, the beta coefficient of a predictor describes the change in the mean of Y for

a one-unit increase in that predictor, controlling for the other variables in the model.

The parameter α represents the mean of Y when each explanatory variable equals 0.

The parameters β1, β2, . . . are called partial regression coefficients. The

adjective partial distinguishes these parameters from the regression coefficient β in

the bivariate model E(Y ) = α + βx, which ignores rather than controls effects of

other explanatory variables.

This multiple regression model assumes that the slope of the partial relationship

between Y and each predictor is identical for all combinations of values of the other

explanatory variables. This means that the model is appropriate when there is no

statistical interaction, in the sense of Section 10.3. If the true partial slope between

Y and x1 is very different at x2 = 50 than at x2 = 40, for example, we need a more

complex model. Section 11.5 will show this model.

A partial slope in a multiple regression model usually differs from the slope in the

bivariate model for that predictor, but it need not. With two predictors, the partial

slopes and bivariate slopes are equal if the correlation between X1 and X2 equals 0.

When X1 and X2 are independent causes of Y , the effect of X1 on Y does not change

when we control for X2.

442 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

Prediction Equation and Residuals

Corresponding to the multiple regression equation, software finds a prediction equation

by estimating the model parameters using sample data. For simplicity of notation, so

far we’ve used just two predictors. In general, let k denote the number of predictors.

Notation for Prediction Equation

The prediction equation that estimates the multiple regression equation E(Y ) =

α + β1x1 + β2x2 + · · · + βkxk is denoted by y = a + b1x1 + b2x2 + · · · + bkxk.

For multiple regression, it is almost imperative to use computer software to find the

prediction equation. The calculation formulas are complex and are not shown in this

text.

We get the predicted value of Y for a subject by substituting the x-values for that

subject into the prediction equation. Like the bivariate model, the multiple regression

model has residuals that measure prediction errors. For a subject with predicted

response y and observed response y, the residual is y − y. The next section shows an

example.

The sum of squared errors (SSE),

SSE =∑

(y − y)2

summarizes the closeness of fit of the prediction equation to the response data. Most

software calls SSE the residual sum of squares. The formula for SSE is the same

as in Chapter 9. The only difference is that the predicted value y results from using

several explanatory variables instead of just a single predictor.

The parameter estimates in the prediction equation satisfy the least squares

criterion: The prediction equation has the smallest SSE value of all possible equations

of form Y = a + b1x1 + · · · + bkxk.

11.2 Example with Multiple Regression Com-

puter Output

We illustrate the methods of this chapter with the data introduced in the following

example:

Example 11.2 Multiple Regression for Mental Health Study

A study in Alachua County, Florida, investigated the relationship between certain

mental health indices and several explanatory variables. Primary interest focused on

an index of mental impairment, which incorporates various dimensions of psychiatric

symptoms, including aspects of anxiety and depression. This measure, which is the

response variable Y , ranged from 17 to 41 in the sample. Higher scores indicate

greater psychiatric impairment.

The two explanatory variables used here are X1 = life events score and X2 =

socioeconomic status (SES). The life events score is a composite measure of both

the number and severity of major life events the subject experienced within the past

three years. These events range from severe personal disruptions such as a death in the

family, a jail sentence, or an extramarital affair, to less severe events such as getting

a new job, the birth of a child, moving within the same city, or having a child marry.

This measure1 ranged from 3 to 97 in the sample. A high score represents a greater

number and/or greater severity of these life events. The SES score is a composite

index based on occupation, income, and education. Measured on a standard scale, it

ranged from 0 to 100. The higher the score, the higher the status.

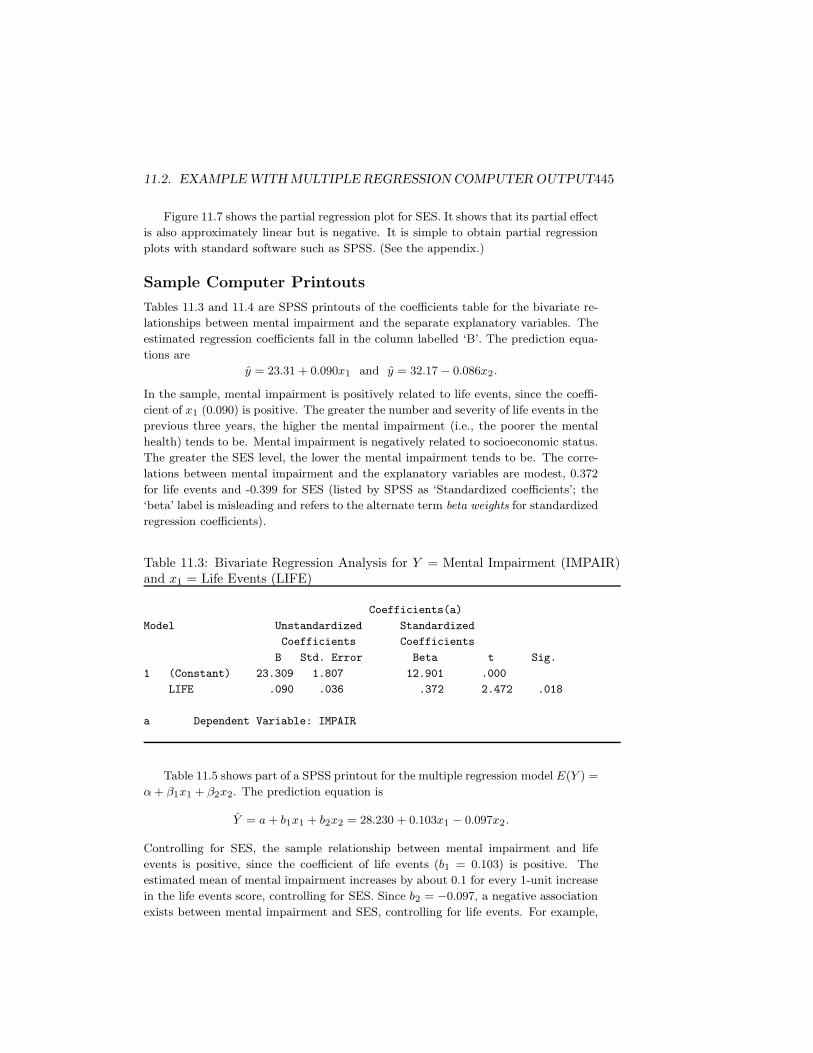

Table 11.1 shows data on the three variables for a random sample of 40 adults in

the county. [These data are based on a larger survey. The authors thank Dr. Charles

Holzer for permission to use the study as the basis of this example.] Table 11.2

summarizes the sample means and standard deviations of the three variables.

Table 11.1: Scores on Y = Mental Impairment, X1 =Life Events, and X2 = Socioeconomic Status

The correlation r and its square describe strength of linear association for bivariate

relationships. This section presents analogous measures for the multiple regression

model. They describe the strength of association between Y and the set of explanatory

variables acting together as predictors in the model.

The Multiple Correlation

The explanatory variables collectively are strongly associated with Y if the observed y-

values correlate highly with the y-values from the prediction equation. The correlation

between the observed and predicted values summarizes this association.

Multiple Correlation

The multiple correlation for a regression model is the correlation between the ob-

served y-values and the predicted y-values.

For each subject, the prediction equation provides a predicted value y. So, each

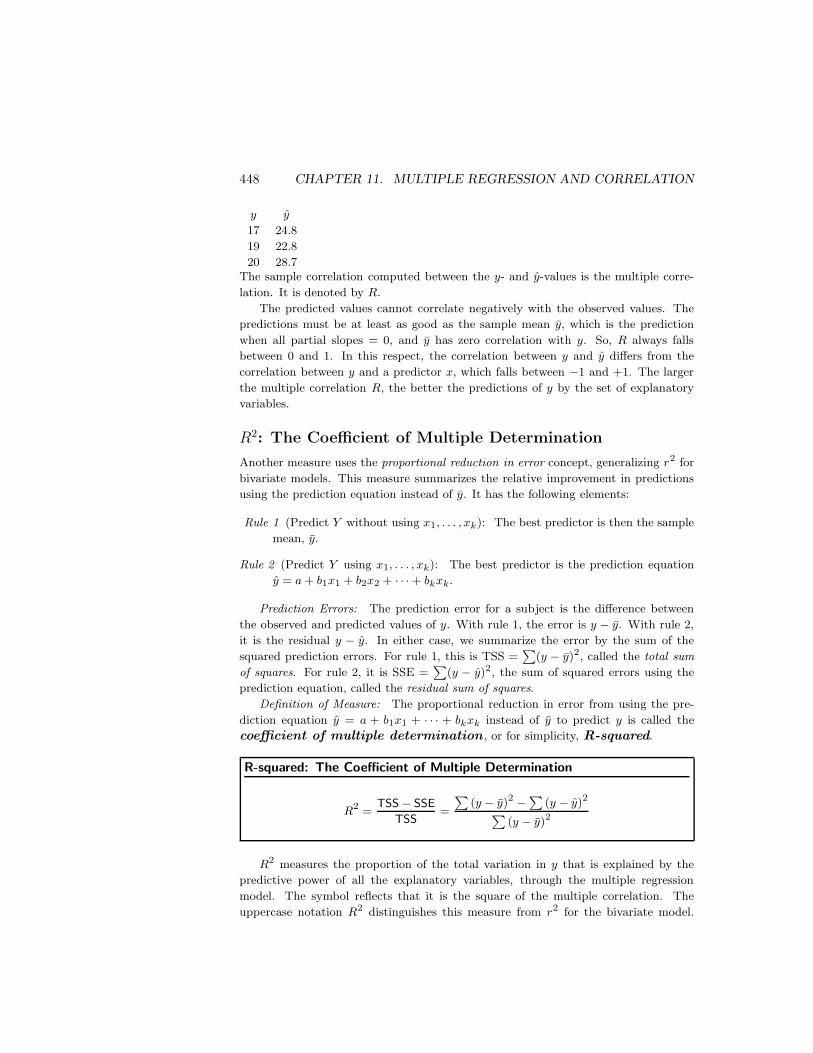

subject has a y-value and a y-value. For example, above we saw that the first subject

in the sample had y = 17 and y = 24.8. For the first three subjects in Table 11.1, the

observed and predicted y-values are:

448 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

y y

17 24.8

19 22.8

20 28.7The sample correlation computed between the y- and y-values is the multiple corre-

lation. It is denoted by R.

The predicted values cannot correlate negatively with the observed values. The

predictions must be at least as good as the sample mean y, which is the prediction

when all partial slopes = 0, and y has zero correlation with y. So, R always falls

between 0 and 1. In this respect, the correlation between y and y differs from the

correlation between y and a predictor x, which falls between −1 and +1. The larger

the multiple correlation R, the better the predictions of y by the set of explanatory

variables.

R2: The Coefficient of Multiple Determination

Another measure uses the proportional reduction in error concept, generalizing r2 for

bivariate models. This measure summarizes the relative improvement in predictions

using the prediction equation instead of y. It has the following elements:

Rule 1 (Predict Y without using x1, . . . , xk): The best predictor is then the sample

mean, y.

Rule 2 (Predict Y using x1, . . . , xk): The best predictor is the prediction equation

y = a + b1x1 + b2x2 + · · · + bkxk.

Prediction Errors: The prediction error for a subject is the difference between

the observed and predicted values of y. With rule 1, the error is y − y. With rule 2,

it is the residual y − y. In either case, we summarize the error by the sum of the

squared prediction errors. For rule 1, this is TSS =∑

(y − y)2, called the total sum

of squares. For rule 2, it is SSE =∑

(y − y)2, the sum of squared errors using the

prediction equation, called the residual sum of squares.

Definition of Measure: The proportional reduction in error from using the pre-

diction equation y = a + b1x1 + · · · + bkxk instead of y to predict y is called the

coefficient of multiple determination , or for simplicity, R-squared.

R-squared: The Coefficient of Multiple Determination

R2 =TSS − SSE

TSS=

∑

(y − y)2 −∑

(y − y)2

∑

(y − y)2

R2 measures the proportion of the total variation in y that is explained by the

predictive power of all the explanatory variables, through the multiple regression

model. The symbol reflects that it is the square of the multiple correlation. The

uppercase notation R2 distinguishes this measure from r2 for the bivariate model.

11.3. MULTIPLE CORRELATION AND R2 449

Their formulas are identical, and r2 is the special case of R2 applied to a regression

model with one explanatory variable. For the multiple regression model to be useful

for prediction, it should provide improved predictions relative not only to y but also

to the separate bivariate models for y and each explanatory variable.

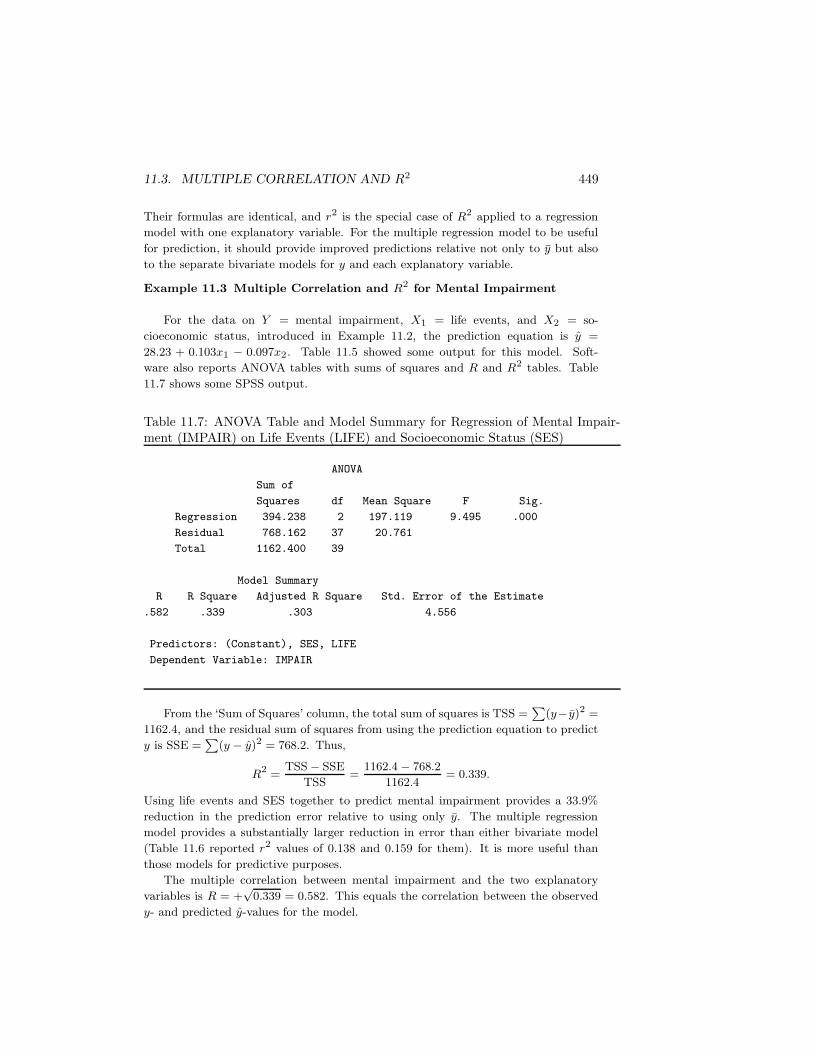

Example 11.3 Multiple Correlation and R2 for Mental Impairment

For the data on Y = mental impairment, X1 = life events, and X2 = so-

cioeconomic status, introduced in Example 11.2, the prediction equation is y =

28.23 + 0.103x1 − 0.097x2. Table 11.5 showed some output for this model. Soft-

ware also reports ANOVA tables with sums of squares and R and R2 tables. Table

11.7 shows some SPSS output.

Table 11.7: ANOVA Table and Model Summary for Regression of Mental Impair-ment (IMPAIR) on Life Events (LIFE) and Socioeconomic Status (SES)

ANOVA

Sum of

Squares df Mean Square F Sig.

Regression 394.238 2 197.119 9.495 .000

Residual 768.162 37 20.761

Total 1162.400 39

Model Summary

R R Square Adjusted R Square Std. Error of the Estimate

.582 .339 .303 4.556

Predictors: (Constant), SES, LIFE

Dependent Variable: IMPAIR

From the ‘Sum of Squares’ column, the total sum of squares is TSS =∑

(y− y)2 =

1162.4, and the residual sum of squares from using the prediction equation to predict

y is SSE =∑

(y − y)2 = 768.2. Thus,

R2 =TSS − SSE

TSS=

1162.4 − 768.2

1162.4= 0.339.

Using life events and SES together to predict mental impairment provides a 33.9%

reduction in the prediction error relative to using only y. The multiple regression

model provides a substantially larger reduction in error than either bivariate model

(Table 11.6 reported r2 values of 0.138 and 0.159 for them). It is more useful than

those models for predictive purposes.

The multiple correlation between mental impairment and the two explanatory

variables is R = +√

0.339 = 0.582. This equals the correlation between the observed

y- and predicted y-values for the model.

450 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

SPSS reports R and R2 in a separate ‘Model Summary’ table, as Table 11.7 shows.

Most software also reports an adjusted version of R2 that is a less biased estimate

of the population value. Exercise 63 defines this measure, and Table 11.7 reports its

value of 0.303.

2

Properties of R and R2

The properties of R2 are similar to those of r2 for bivariate models.

• R2 falls between 0 and 1.

• The larger the value of R2, the better the set of explanatory variables (x1, . . . , xk)

collectively predict y.

• R2 = 1 only when all the residuals are 0, that is, when all y = y, so that

SSE = 0. In that case, the prediction equation passes through all the data

points.

• R2 = 0 when the predictions do not vary as any of the x-values vary. In that

case, b1 = b2 = · · · = bk = 0, and y is identical to y, since the explanatory

variables do not add any predictive power. When this happens, the correlation

between y and each explanatory variable equals 0.

• R2 cannot decrease when we add an explanatory variable to the model. It is

impossible to explain less variation in y by adding explanatory variables to a

regression model.

• R2 for the multiple regression model is at least as large as the r2-values for the

separate bivariate models. That is, R2 for the multiple regression model is at

least as large as r2Y X1

when Y as a linear function of x1, r2Y X2

when Y as a

linear function of x2, and so forth.

Properties of the multiple correlation R follow directly from the ones for R2, since

R is the positive square root of R2. For instance, the multiple correlation for the

model E(Y ) = α + β1x1 + β2x2 + β3x3 is at least as large as the multiple correlation

for the model E(Y ) = α + β1x1 + β2x2.

The numerator of R2, TSS − SSE, summarizes the variation in Y explained by

the multiple regression model. This difference, which equals∑

(y − y)2, is called the

regression sum of squares. The ANOVA table in Table 11.7 lists the regression

sum of squares as 394.2. (Some software, such as SAS, labels this the ‘Model’ sum

of squares.) The total sum of squares TSS of the y-values about y partitions into

the variation explained by the regression model (regression sum of squares) plus the

variation not explained by the model (the residual sum of squares, SSE).

11.4. INFERENCES FOR MULTIPLE REGRESSION COEFFICIENTS 451

Multicollinearity with Many Explanatory Variables

When there are many explanatory variables but the correlations among them are

strong, once you have included a few of them in the model, R2 usually doesn’t increase

much more when you add additional ones. For example, for the “house selling price”

data set at the text website (introduced in Example 9.10), r2 is 0.71 with the house’s

tax assessment as a predictor of selling price. Then, R2 increases to 0.77 when we

add house size as a second predictor. But then it increases only to 0.79 when we

add number of bathrooms, number of bedrooms, and whether the house is new as

additional predictors.

When R2 does not increase much, this does not mean that the additional variables

are uncorrelated with Y . It means merely that they don’t add much new power for

predicting Y , given the values of the predictors already in the model. These other

variables may have small associations with Y , given the variables already in the model.

This often happens in social science research when the explanatory variables are highly

correlated, no one having much unique explanatory power. Section 14.3 discusses this

condition, called multicollinearity .

Figure 11.8, which portrays the portion of the total variability in Y explained by

each of three predictors, shows a common occurrence. The size of the set for a predictor

in this figure represents the size of its r2-value in predicting Y . The amount a set for

a predictor overlaps with the set for another predictor represents its association with

that predictor. The part of the set for a predictor that does not overlap with other

sets represents the part of the variability in Y explained uniquely by that predictor.

In Figure 11.8, all three predictors have moderate associations with Y , and together

they explain considerable variation. Once x1 and x2 are in the model, however, x3

explains little additional variation in Y , because of its strong correlations with x1 and

x2. Because of this overlap, R2 increases only slightly when x3 is added to a model

already containing x1 and x2.

For predictive purposes, we gain little by adding explanatory variables to a model

that are strongly correlated with ones already in the model, since R2 will not increase

much. Ideally, we should use explanatory variables having weak correlations with

each other but strong correlations with Y . In practice, this is not always possible,

especially if we want to include certain variables in the model for theoretical reasons.

In practice, the sample size you need to do a multiple regression well gets larger

when you want to use more explanatory variables. Technical difficulties caused by

multicollinearity are less severe for larger sample sizes. Ideally, the sample size should

be at least about 10 times the number of explanatory variables (for example, at least

about 40 for 4 explanatory variables).

11.4 Inferences for Multiple Regression Coeffi-

cients

The multiple regression function

E(Y ) = α + β1x1 + · · · + βkxk

452 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

describes the relationship between the explanatory variables and the mean of the

response variable. For particular values of the explanatory variables, α+β1x1 + · · ·+βkxk represents the mean of Y for the population having those values.

To make inferences about the parameters, we formulate the entire multiple regres-

sion model. This consists of this equation together with a set of assumptions:

• The population distribution of Y is normal, for each combination of values of

x1, . . . , xk.

• The standard deviation, σ, of the conditional distribution of responses on Y is

the same at each combination of values of x1, . . . , xk.

• The sample is randomly selected.

Under these assumptions, the true sampling distributions exactly equal those

quoted in this section. In practice, the assumptions are never satisfied perfectly.

Two-sided inferences are robust to the normality and common σ assumptions. More

important are the assumptions of randomization and that the regression function de-

scribes well how the mean of Y depends on the explanatory variables. We’ll see ways

to check the latter assumption in Section 14.2.

Two types of significance tests are used in multiple regression. The first is a global

test of independence. It checks whether any of the explanatory variables are statisti-

cally related to Y . The second studies the partial regression coefficients individually,

to assess which explanatory variables have significant partial effects on Y .

Testing the Collective Influence of the Explanatory Vari-

ables

Do the explanatory variables collectively have a statistically significant effect on the

response variable? We check this by testing

H0 : β1 = β2 = · · · = βk = 0.

This states that the mean of Y does not depend on the values of x1, . . . , xk. Under

the inference assumptions, this states that Y is statistically independent of all k

explanatory variables.

The alternative hypothesis is

Ha : At least one βi 6= 0.

This states that at least one explanatory variable is related to Y , controlling for the

others. The test judges whether using x1, · · · , xk together to predict y, with the

prediction equation y = a + b1x1 + · · · + bkxk, is better than using y.

These hypotheses about {βi} are equivalent to

H0 : Population multiple correlation = 0 Ha : Population multiple correlation > 0.

11.4. INFERENCES FOR MULTIPLE REGRESSION COEFFICIENTS 453

The equivalence occurs because the multiple correlation equals 0 only in those situa-

tions in which all the partial regression coefficients equal 0. Also, H0 is equivalent to

H0: population R-squared = 0.

For these hypotheses about the k predictors, the test statistic equals

F =R2/k

(1 − R2)/[n − (k + 1)].

The sampling distribution of this statistic is called the F distribution . We next

study this distribution and its properties.

The F Distribution

The symbol for the F test statistic and its distribution honors the most eminent

statistician in history, R. A. Fisher, who discovered the F distribution in 1922. Like

the chi-squared distribution, the F distribution can take only nonnegative values and

it is somewhat skewed to the right. Figure 11.9 illustrates.

The shape of the F distribution is determined by two degrees of freedom terms,

denoted by df1 and df2:

df1 = k, the number of explanatory variables in the model.

df2 = n − (k + 1) = n − number of parameters in regression equation.

The first of these, df1 = k, is the divisor of the numerator term (R2) in the F test

statistic. The second, df2 = n−(k+1), is the divisor of the denominator term (1−R2).

The number of parameters in the multiple regression model is k + 1, representing the

k beta terms and the alpha term.

The mean of the F distribution is approximately equal to 1.2 The larger the R2

value, the larger the ratio R2/(1 − R2), and the larger the F test statistic becomes.

Thus, larger values of the F test statistic provide stronger evidence against H0. Under

the presumption that H0 is true, the P -value is the probability the F test statistic

is larger than the observed F value. This is the right-tail probability under the F

distribution beyond the observed F -value, as Figure 11.9 shows.

Table D at the end of the text lists the F scores having P -values of 0.05, 0.01,

and 0.001, for various combinations of df1 and df2. This table allows us to determine

whether P > 0.05, 0.01 < P < 0.05, 0.001 < P < 0.01, or P < 0.001. Software for

regression reports the actual P -value.

Example 11.4 F Test for Mental Health Impairment Data

In Example 11.2, we used multiple regression for n = 40 observations on Y =

mental impairment, with k = 2 explanatory variables, life events and SES. The null

hypothesis that mental impairment is statistically independent of life events and SES

is H0: β1 = β2 = 0.

2It equals df2/(df2 − 2), which is usually close to 1 unless n is quite small.

454 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

In Example 11.3 we found that this model has R2 = 0.339. The F test statistic

value is

F =R2/k

(1 − R2)/[n − (k + 1)]=

0.339/2

0.661/[40 − (2 + 1)]= 9.5.

The two degrees of freedom terms for the F distribution are df1 = k = 2 and df2 =

n − (k + 1) = 40 − 3 = 37, the two divisors in this statistic.

From Table D, when df1 = 2 and df2 = 37, the F -value with right-tail probability

of 0.001 falls between 8.77 and 8.25. Since the observed F test statistic of 9.5 falls

above these two, it is farther out in the tail and has smaller tail probability than 0.001.

Thus, the P -value is P < 0.001. Part of the SPSS printout in Table 11.7 showed the

ANOVA table

Sum of Squares df Mean Square F Sig.

Regression 394.238 2 197.119 9.495 .000

Residual 768.162 37 20.761

in which we see the F statistic. The P -value, which rounded to three decimal places

is P = 0.000, appears under the heading ‘Sig’ in the ANOVA table.

This extremely small P -value provides strong evidence against H0. It suggests

that at least one of the explanatory variables is related to mental impairment. Equiv-

alently, we can conclude that the population multiple correlation and R-squared are

positive. So, we obtain significantly better predictions of y using the multiple regres-

sion equation than by using y.

2

Normally, unless the sample size is small and the associations are weak, this F

test has a small P -value. If we choose variables wisely for a study, at least one of

them should have some explanatory power.

Inferences for Individual Regression Coefficients

Suppose the P -value is small for the F test that all the regression coefficients equal 0.

This does not imply that every explanatory variable has an effect on Y (controlling

for the other explanatory variables in the model), but merely that at least one of them

has an effect. More narrowly focused analyses judge which partial effects are nonzero

and estimate the sizes of those effects. These inferences make the same assumptions as

the F test, the most important being randomization and that the regression function

describes well how the mean of Y depends on the explanatory variables.

Consider an arbitrary explanatory variable xi, with coefficient βi in the multiple

regression model. The test for its partial effect on Y has H0: βi = 0. If βi = 0,

the mean of Y is identical for all values of xi, controlling for the other explanatory

variables in the model. The alternative can be two-sided, Ha: βi 6= 0, or one-sided,

Ha: βi > 0 or Ha: βi < 0, to predict the direction of the partial effect.

The test statistic for H0: βi = 0, using sample estimate bi of βi, is

t =bi

se,

11.4. INFERENCES FOR MULTIPLE REGRESSION COEFFICIENTS 455

where se is the standard error of bi. As usual, the t test statistic takes the best

estimate (bi) of the parameter (βi), subtracts the H0 value of the parameter (0), and

divides by the standard error. The formula for se is complex, but software provides

its value. If H0 is true and the model assumptions hold, the t statistic has the t

distribution with df = n − (k + 1). The df value is the same as df2 in the F test.

It is more informative to estimate the size of a partial effect than to test whether it

is zero. Recall that βi represents the change in the mean of Y for a one-unit increase

in xi, controlling for the other variables. A confidence interval for βi is

bi ± t(se).

The t score comes from the t table, with df = n − (k + 1)2. For example, a 95%

confidence interval for the partial effect of x1 is b1 ± t.025(se).

Example 11.5 Inferences for Separate Predictors of Mental Impairment

For the multiple regression model for Y = mental impairment, X1 = life events,

and X2 = SES,

E(Y ) = α + β1x1 + β2x2

let’s consider the effect of life events. The hypothesis that mental impairment is

statistically independent of life events, controlling for SES, is H0: β1 = 0. If H0 is

true, the multiple regression equation reduces to E(Y ) = α + β2x2. If H0 is false,

then β1 6= 0 and the full model provides a better fit than the bivariate model.

Table 11.5 contained the results,

B Std. Error t Sig.

(Constant) 28.230 2.174 12.984 .000

LIFE .103 .032 3.177 .003

SES -.097 .029 -3.351 .002

This tells us that the point estimate of β1 is b1 = 0.103 and has standard error

se = 0.032. The test statistic equals

t =b1se

=0.103

0.032= 3.2.

This appears under the heading ‘t’ in the table in the row for the variable LIFE. The

statistic has df = n−(k+1) = 40−3 = 37. The P -value appears under ‘Sig’ in the row

for LIFE. It is 0.003, the probability that the t statistic exceeds 3.2 in absolute value.

There is strong evidence that mental impairment is related to life events, controlling

for SES.

A 95% confidence interval for β1 uses t0.025 = 2.026, the t-value for df = 37 having

a probability of 0.05/2 = 0.025 in each tail. This interval equals

b1 ± t0.025(se) = 0.103 ± 2.026(0.032), which is (0.04, 0.17).

Controlling for SES, we are 95% confident that the change in mean mental impairment

per one-unit increase in life events falls between 0.04 and 0.17. The interval does not

456 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

contain 0. This is in agreement with rejecting H0: β1 = 0 in favor of Ha: β1 6= 0 at

the α = 0.05 level.

Since this interval contains only positive numbers, the relationship between men-

tal impairment and life events is positive, controlling for SES. It may be simpler to

interpret the interval (0.04, 0.17) by noting that an increase of 100 units in life events

corresponds to anywhere from a 100(0.04) = 4 to a 100(0.17) = 17 unit increase in

mean mental impairment. The interval is relatively wide, because of the small sample

size.

2

How is the t test for a partial regression coefficient different from the t test of

H0: β = 0 for the bivariate model, E(Y ) = α + βx, studied in Section 9.5? That t

test evaluates whether Y and X are associated, ignoring other variables, because it

applies to the bivariate model. By contrast, the test just presented evaluates whether

variables are associated, controlling for other variables.

A note of caution: Suppose there is multicollinearity, that is, a lot of overlap

among the explanatory variables in the sense that any one is well predicted by the

others. Then, possibly none of the individual partial effects has a small P -value, even

if R2 is large and a large F statistic occurs in the global test for the βs. Any particular

variable may explain uniquely little of the variation in Y , even though together the

variables explain a lot of the variation.

Variability and Mean Squares in the ANOVA Table∗

The precision of the least squares estimates relates to the size of the conditional

standard deviation σ that measures variability of y at fixed values of the predictors.

The smaller the variability of y-values about the regression equation, the smaller the

standard errors become. The estimate of σ is

s =

√

∑

(y − y)2

n − (k + 1)=

√

SSE

df.

The degrees of freedom value is also df for t inferences for regression coefficients, and

it is df2 for the F test about the collective effect of the predictors. (When a model has

only k = 1 predictor, df simplifies to n − 2, the term in the s formula of Section 9.3.)

Part of the SPSS printout in Table 11.7 showed the ANOVA table

Sum of Squares df Mean Square F Sig.

Regression 394.238 2 197.119 9.495 .000

Residual 768.162 37 20.761

containing the sums of squares for the multiple regression model with the mental

impairment data. We see that SSE = 768.2. Since n = 40 for k = 2 predictors, we

have df = n − (k + 1) = 40 − 3 = 37 and

s =

√

SSE

df=

√

768.2

37=

√20.76 = 4.56.

11.4. INFERENCES FOR MULTIPLE REGRESSION COEFFICIENTS 457

If the conditional distributions are approximately bell-shaped, nearly all mental im-

pairment scores fall within about 14 units (3 standard deviations) of the mean specified

by the regression function.

SPSS reports the conditional standard deviation under the heading ‘Std. Error of

the Estimate’ in the Model Summary table that also has the R and R2values (See

Table 11.7). This is a poor choice of label by SPSS, because s refers to the variability

in Y -values, not the variability of a sampling distribution of an estimator.

The square of s, which estimates the conditional variance, is called the mean

square error , often abbreviated by MSE. Software shows it in the ANOVA table in

the ‘Mean Square’ column, in the row labeled ‘Residual’ (or ‘Error’ in some software).

For example, MSE = 20.76 in the above table. Some software (such as SAS) better

labels the conditional standard deviation estimate s as ‘Root MSE,’ because it is the

square root of the mean square error.

The F Statistic Is a Ratio of Mean Squares∗

An alternative formula for the F test statistic for testing H0 : β1 = · · · = βk = 0 uses

the two mean squares in the ANOVA table. Specifically,

F =Regression mean square

Residual mean square (MSE)=

197.1

20.8= 9.5.

This gives the same value as the F test statistic formula based on R2.

The regression mean square equals the regression sum of squares divided by its

degrees of freedom. The df equals k, the number of explanatory variables in the

model, which is df1 for the F test. On the printout shown above, the regression mean

square equalsRegression SS

df1=

394.2

2= 197.1.

Relationship Between F and t Statistics∗

We’ve seen that the F distribution is used to test that all partial regression coefficients

equal 0. Some regression software also lists F test statistics instead of t test statistics

for the tests about the individual regression coefficients. The two statistics are related

and have the same P -values. The square of the t statistic for testing that a partial

regression coefficient equals 0 is an F test statistic having the F distribution with

df1 = 1 and df2 = n − (k + 1).

To illustrate, in Example 11.5, for H0: β1 = 0 and Ha: β1 6= 0, the test statistic

was t = 3.18 with df = 37. Alternatively, we could use F = t2 = 3.182 = 10.1, which

has the F distribution with df1 = 1 and df2 = 37. The P -value for this F value is

0.002, the same as Table 11.5 reports for the two-sided t test.

In general, if a statistic has the t distribution with d degrees of freedom, then

the square of that statistic has the F distribution with df1 = 1 and df2 = d. A

disadvantage of the F approach is that it lacks information about the direction of the

association. It cannot be used for one-sided alternative hypotheses.

458 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

11.5 Interaction between Predictors in their Ef-

fects

The multiple regression equation

E(Y ) = α + β1x1 + β2x2 + · · · + βkxk

assumes that the partial relationship between Y and each xi is linear and that the

slope βi of that relationship is identical for all values of the other explanatory variables.

This implies a parallelism of lines relating the two variables, at various values of the

other variables, as Figure 11.3 illustrated.

This model is sometimes too simple to be adequate. Often, there is interaction,

with the relationship between two variables changing according to the value of a third

variable. Section 10.3 introduced this concept.

Interaction

For quantitative variables, interaction exists between two explanatory variables in their

effects on Y when the effect of one variable changes as the level of the other variable

changes.

For example, suppose the relationship between x1 and the mean of Y is E(Y ) =

2 + 5x1 when x2 = 0, it is E(Y ) = 4 + 15x1 when x2 = 50, and it is E(Y ) = 6 + 25x1

when x2 = 100. The slope for the partial effect of x1 changes markedly as the fixed

value for x2 changes. There is then interaction between x1 and x2 in their effects on

Y .

Cross-product Terms

A common approach for allowing interaction introduces cross-product terms of

the explanatory variables into the multiple regression model. With two explanatory

variables, the model is

E(Y ) = α + β1x1 + β2x2 + β3x1x2.

This is a special case of the multiple regression model with three explanatory variables,

in which x3 is an artificial variable created as the cross-product x3 = x1x2 of the two

primary explanatory variables.

Let’s see why this model permits interaction. Consider how Y is related to x1,

controlling for x2. We rewrite the equation in terms of x1 as

E(Y ) = (α + β2x2) + (β1 + β3x2)x1 = α′ + β′x1

where

α′ = α + β2x2 and β′ = β1 + β3x2.

So, for fixed x2, the mean of Y changes linearly as a function of x1. The slope of the

relationship is β′ = (β1 +β3x2). This depends on the value of x2. As x2 changes, the

11.5. INTERACTION BETWEEN PREDICTORS IN THEIR EFFECTS459

slope for the effect of x1 changes. In summary, the mean of Y is a linear function of

x1, but the slope of the line depends on the value of x2.

Note that now we can interpret β1 as the effect of x1 only when x2 = 0. Unless

x2 = 0 is a particular value of interest for x2, it is not particularly useful to form

confidence intervals or perform significance tests about β2 in this model.

Similarly, the mean of Y is a linear function of x2, but the slope varies according

to the value of x1. The coefficient β2 of x2 refers to the effect of x2 only at x1 = 0.

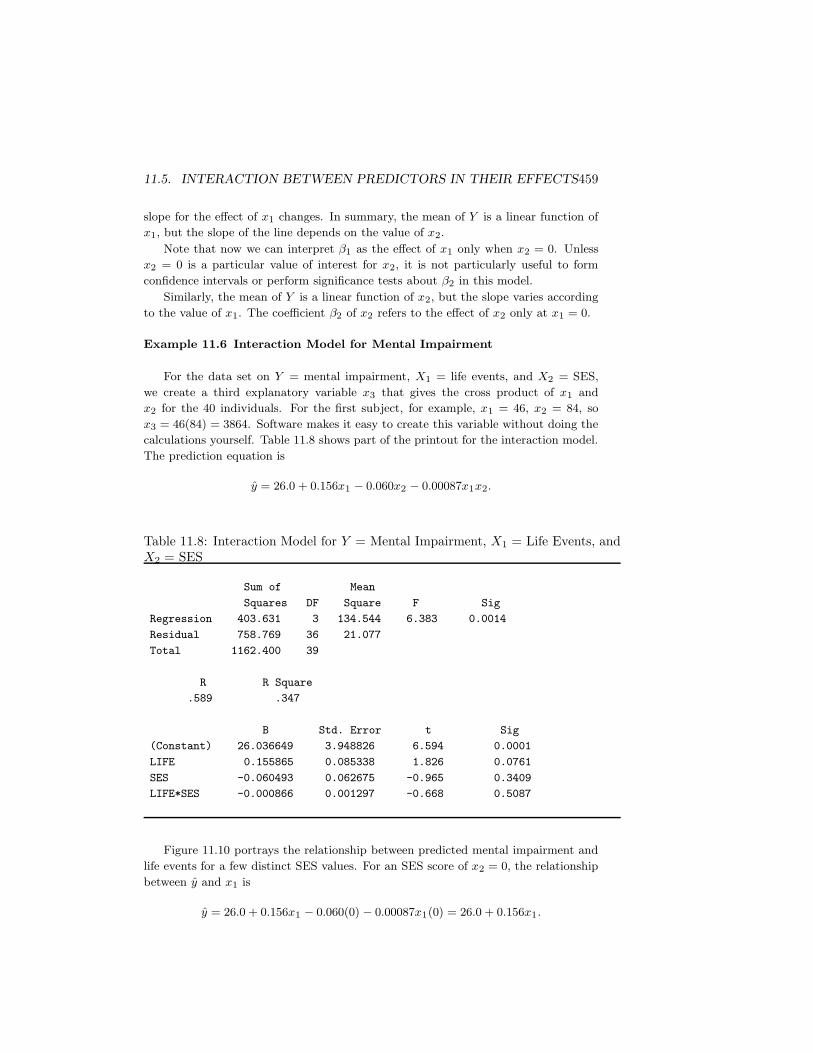

Example 11.6 Interaction Model for Mental Impairment

For the data set on Y = mental impairment, X1 = life events, and X2 = SES,

we create a third explanatory variable x3 that gives the cross product of x1 and

x2 for the 40 individuals. For the first subject, for example, x1 = 46, x2 = 84, so

x3 = 46(84) = 3864. Software makes it easy to create this variable without doing the

calculations yourself. Table 11.8 shows part of the printout for the interaction model.

The prediction equation is

y = 26.0 + 0.156x1 − 0.060x2 − 0.00087x1x2.

Table 11.8: Interaction Model for Y = Mental Impairment, X1 = Life Events, andX2 = SES

Sum of Mean

Squares DF Square F Sig

Regression 403.631 3 134.544 6.383 0.0014

Residual 758.769 36 21.077

Total 1162.400 39

R R Square

.589 .347

B Std. Error t Sig

(Constant) 26.036649 3.948826 6.594 0.0001

LIFE 0.155865 0.085338 1.826 0.0761

SES -0.060493 0.062675 -0.965 0.3409

LIFE*SES -0.000866 0.001297 -0.668 0.5087

Figure 11.10 portrays the relationship between predicted mental impairment and

life events for a few distinct SES values. For an SES score of x2 = 0, the relationship

The reduced model without the interaction terms is

E(Y ) = α + β1x1 + β2x2 + β3x3.

The test comparing the complete model to the reduced model has H0: β4 = β5 =

β6 = 0.

11.6. COMPARING REGRESSION MODELS 463

Comparing Models by Comparing SSE or R2 Values

The test statistic for comparing two regression models compares the residual sums

of squares for the two models. Denote SSE =∑

(y − y)2 for the reduced model by

SSEr and for the complete model by SSEc. Now, SSEr ≥ SSEc, because the reduced

model has fewer predictors and tends to make poorer predictions. Even if H0 were

true, we would not expect the estimates of the extra parameters and the difference

(SSEr−SSEc) to equal 0. Some reduction in error occurs from fitting the extra terms

because of sampling variability.

The test statistic uses the reduction in error, SSEr − SSEc, that results from

adding the extra variables. It has df = the number of extra terms in the complete

model. An equivalent statistic uses the R2 values, R2c for the complete model and R2

r

for the reduced model. The test statistic equals

F =(SSEr − SSEc)/df1

SSEc/df2=

(R2c − R2

r)/df1

(1 − R2c)/df2

,

where df1 is the number of extra terms in the complete model and df2 is the usual

residual df for the complete model, which is df2 = n − (k + 1). A relatively large

reduction in error (or relatively large increase in R2) yields a large F test statistic

and small P -value. As usual for F statistics, the P -value is the right-tail probability.

Example 11.7 Comparing Models for Mental Impairment

For the mental impairment data, a comparison of the complete model

E(Y ) = α + β1x1 + β2x2 + β3x1x2

to the reduced model

E(Y ) = α + β1x1 + β2x2

analyzes whether interaction exists. The complete model has just one additional term,

and the null hypothesis is H0: β3 = 0.

The sum of squared errors for the complete model is SSEc = 758.8 (Table 11.8),

while for the reduced model it is SSEr = 768.2 (Table 11.7). The difference

SSEr − SSEc = 768.2 − 758.8 = 9.4

has df1 = 1 since the complete model has one more parameter. Since the sample size

is n = 40, df2 = n − (k + 1) = 40 − (3 + 1) = 36, the df for SSE in Table 11.8. The F

test statistic equals

F =(SSEr − SSEc)/df1

SSEc/df2=

9.4/1

758.8/36= 0.45.

Equivalently, the R2 values for the two models are R2r = 0.339 and R2

c = 0.347, so

F =

(

R2c − R2

r

)

/df1(

1 − R2c

)

/df2

=(0.347 − 0.339)/1

(1 − 0.347)/36= 0.45.

464 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

From software, the P -value from the F distribution with df1 = 1 and df2 = 36 is

P = 0.51. There is little evidence that the complete model is better. The null

hypothesis seems plausible, so the reduced model is adequate.

When H0 contains a single parameter, the t test is available. In fact, from the

previous section (and Table 11.8), the t statistic equals

t =b3se

=−0.00087

0.0013= −0.67.

It also has a P -value of 0.51 for Ha: β3 6= 0. We get the same result with the t test as

with the F test for complete and reduced models. In fact, the F test statistic equals

the square of the t statistic. (Refer to the final subsection in Section 11.4.)

2

The t test method is limited to testing one parameter at a time. The F test can

test several regression parameters together to analyze whether at least one of them is

nonzero, such as in the global F test of H0 : β1 = · · · = βk = 0 or the test comparing

a complete model to a reduced model. F tests are equivalent to t tests only when H0

contains a single parameter.

11.7 Partial Correlation∗

Multiple regression models describe the effect of an explanatory variable on the re-

sponse variable while controlling for other variables of interest. Related measures

describe the strength of the association. For example, to describe the association

between mental impairment and life events, controlling for SES, we could ask, “Con-

trolling for SES, what proportion of the variation in mental impairment does life

events explain?”

These measures describe the partial association between Y and a particular pre-

dictor, whereas the multiple correlation and R2 describe the association between Y

and the entire set of predictors in the model. The partial correlation is based on the

ordinary correlations between each pair of variables. For a single control variable, it

is defined as follows:

Partial Correlation

The sample partial correlation between Y and X2, controlling for X1, is

rY X2·X1=

rY X2− rY X1

rX1X2√

(

1 − r2Y X1

) (

1 − r2X1X2

)

.

In the symbol rY X2·X1, the variable to the right of the dot represents the controlled

variable. The analogous formula for rY X1·X2(i.e., controlling X2) is

rY X1·X2=

rY X1− rY X2

rX1X2√

(

1 − r2Y X2

) (

1 − r2X1X2

)

.

11.7. PARTIAL CORRELATION∗ 465

Since one variable is controlled, the partial correlations rY X1·X2and rY X2·X1

are

called first-order partial correlations.

Example 11.8 Partial Correlation Between Education and Crime Rate

Example 11.1 discussed a data set for counties in Florida, with Y = crime rate,

X1 = education, and X2 = urbanization. The pairwise correlations are rY X1=

0.468, rY X2= 0.678, and rX1X2

= 0.791. It was surprising to observe a positive

correlation between crime rate and education. Can it be explained by their joint

dependence on urbanization? This is plausible if the association disappears when we

control for urbanization.

The partial correlation between crime rate and education, controlling for urban-

ization, equals

rY X1·X2=

rY X1− rY X2

rX1X2√

(1 − r2Y X2

)(1 − r2X1X2

)=

0.468 − 0.678(0.791)√

(1 − 0.6782) (1 − 0.7912)= −0.152.

Not surprisingly, rY X1·X2is much smaller than rY X1

. It even has a different direction,

illustrating Simpson’s paradox. The relationship between crime rate and education

may well be spurious, reflecting their joint dependence on urbanization.

2

Interpreting Partial Correlations

The partial correlation has properties similar to those for the ordinary correlation

between two variables, such as a range of −1 to +1, larger absolute values representing

stronger associations, and value free of the units. We list the properties below for

rY X1·X2, but analogous properties apply to rY X2·X1

.

• rY X1·X2falls between −1 and +1.

• The larger the absolute value of rY X1·X2, the stronger the association between

Y and X1, controlling for X2.

• The value of a partial correlation does not depend on the units of measurement

of the variables.

• rY X1·X2has the same sign as the partial slope (b1) for the effect of x1 in the

prediction equation y = a+b1x1+b2x2. This happens because the same variable

(x2) is controlled in the model as in the correlation.

• Under the assumptions for conducting inference for multiple regression (see

the beginning of Section 11.4), rY X1·X2estimates the correlation between Y

and X1 at every fixed value of X2. If we could control X2 by considering

a subpopulation of subjects all having the same value on X2, then rY X1·X2

estimates the correlation between Y and X1 for that subpopulation.

466 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

• The sample partial correlation is identical to the correlation computed for the

points in the partial regression plot (Section 11.2).

Interpreting Squared Partial Correlations

Like r2 and R2, the square of a partial correlation has a proportional reduction in

error (PRE) interpretation. It states that r2Y X2·X1

is the proportion of variation in

Y explained by X2, controlling for X1. This squared measure describes the effect of

removing from consideration the portion of the total sum of squares (TSS) in Y that

is explained by X1, and then finding the proportion of the remaining unexplained

variation in Y that is explained by X2.

Squared Partial Correlation

The square of the partial correlation rY X2·X1represents the proportion of the variation

in Y that is explained by X2, out of that left unexplained by X1. It equals

r2Y X2·X1

=R2 − r2

Y X1

1 − r2Y X1

=Partial proportion explained uniquely by X2

Proportion unexplained by X1.

Recall from Section 9.4 that r2Y X1

represents the proportion of the variation in

Y explained by X1. The remaining proportion (1 − r2Y X1

) represents the variation

left unexplained. When X2 is added to the model, it accounts for some additional

variation. The total proportion of the variation in Y accounted for by X1 and X2

jointly is R2 for the model with both X1 and X2 as explanatory variables. So, R2 −r2Y X1

is the additional proportion of the variability in Y explained by X2, after the

effects of X1 have been removed or controlled. The maximum this difference could

be is 1 − r2Y X1

, the proportion of variation yet to be explained after accounting for

the influence of X1. The additional explained variation R2 − r2Y X1

divided by this

maximum possible difference is a measure that has a maximum possible value of 1. In

fact, as the above formula suggests, this ratio equals the squared partial correlation

between Y and X2, controlling for X1.

Figure 11.11 illustrates this property of the squared partial correlation. It shows

the ratio of the partial contribution of X2 beyond that of X1, namely, R2 − r2Y X1

,

divided by the proportion (1 − r2Y X1

) left unexplained by X1. Similarly, the square

of rY X1·X2equals

r2Y X1·X2

=R2 − r2

Y X2

1 − r2Y X2

,

the proportion of variation in Y explained by X1, out of that part unexplained by X2.

Example 11.9 Partial Correlation of Life Events with Mental Impairment

We return to the mental health study, with Y = mental impairment, X1 = life

events, X2 = SES. Software reports the correlation matrix,

11.7. PARTIAL CORRELATION∗ 467

IMPAIR LIFE SES

IMPAIR 1.000 .372 -.399

LIFE .372 1.000 .123

SES -.399 .123 1.000

So, rY X1= 0.372, rY X2

= −0.399, and rX1X2= 0.123. By its definition, the partial

correlation between mental impairment and life events, controlling for SES, is

rY X1·X2=

rY X1− rY X2

rX1X2√

(

1 − r2Y X2

) (

1 − r2X1X2

)

=0.372 − (−0.399)(0.123)

√

[1 − (−0.399)2] (1 − 0.1232)= 0.463.

The partial correlation, like the correlation of 0.37 between mental impairment and

life events, is moderately positive.

Since r2Y X1·X2

= (0.463)2 = 0.21, controlling for SES, 21% of the variation in

mental impairment is explained by life events. Alternatively, since R2 = 0.339 (Table

11.7),

r2Y X1·X2

=R2 − r2

Y X2

1 − r2Y X2

=0.339 − (−0.399)2

1 − (−0.399)2= 0.21.

2

Higher-Order Partial Correlations

One reason we showed the connection between squared partial correlation values and

R-squared is that this approach also works when the number of control variables

exceeds one. For example, with three predictors, let R2Y (X1,X2,X3) denote the value

of R2. The square of the partial correlation between Y and X3, controlling for X1 and

X2, relates to how much larger this is than the R2 value for the model with only X1

and X2 as predictors, which we denote by R2Y (X1,X2). The squared partial correlation

is

r2Y X3·X1,X2

=R2

Y (X1,X2,X3) − R2Y (X1,X2)

1 − R2Y (X1,X2)

.

In this expression, R2Y (X1,X2,X3) −R2

Y (X1,X2)is the increase in the proportion of

explained variance from adding x3 to the model. The denominator 1 − R2Y (X1,X2)

is

the proportion of the variation left unexplained when x1 and x2 are the only predictors

in the model.

The partial correlation rY X3·X1,X2is called a second-order partial corre-

lation , since it controls two variables. It has the same sign as b3 in the prediction

equation y = a + b1x1 + b2x2 + b3x3, which also controls x1 and x2 in describing the

effect of x1.

Inference for Partial Correlations

Controlling for a certain set of variables, the slope of the partial effect of a predictor is 0

in the same situations in which the partial correlation between Y and that predictor is

0. An alternative formula for the t test for a partial effect uses the partial correlation.

468 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

With k predictors in the model, the equivalent t test statistic is

t =partial correlation

√

(1 − squared partial correlation)/[n − (k + 1)].

This statistic has the t distribution with df = n − (k + 1). It equals the t statistic

based on the partial slope estimate and, hence, has the same P -value.

We illustrate by testing that the population partial correlation between mental

impairment and life events, controlling for SES, is 0. From Example 11.9, rY X1·X2=

0.463. There are k = 2 explanatory variables and n = 40 observations. The test

statistic equals

t =rY X1·X2

√

(1 − r2Y X1·X2

)/[n − (k + 1)]=

0.463√

[1 − (0.463)2]/37= 3.18.

This equals the test statistic for H0: β1 = 0 in Table 11.5. Thus, the P -value is also

the same, P = 0.003.

When no variables are controlled (i.e., the number of explanatory variables is

k = 1), the t statistic formula simplifies to

t =r

√

(1 − r2)/(n − 2).

This is the statistic for testing that the population bivariate correlation equals 0

(Section 9.5). Confidence intervals for partial correlations are more complex. They

require a log transformation such as shown for the correlation in Exercise 65 in Chapter

9.

11.8 Standardized Regression Coefficients∗

As in bivariate regression (Recall Section 9.4), the sizes of regression coefficients in

multiple regression models depend on the units of measurement for the variables. To

compare the relative effects of two explanatory variables, it is appropriate to compare

their coefficients only if the variables have the same units. Otherwise, standardized

versions of the regression coefficients provide more meaningful comparisons.

Standardized Regression Coefficient

The standardized regression coefficient for an explanatory variable represents the

change in the mean of Y , in Y standard deviations, for a one standard deviation increase

in that variable, controlling for the other explanatory variables in the model. We denote

them by β∗

1 , β∗

2 , . . . .

If |β∗

2 | > |β∗

1 |, for example, then a standard deviation increase in X2 has a greater

partial effect on Y than does a standard deviation increase in X1.

11.8. STANDARDIZED REGRESSION COEFFICIENTS∗ 469

The Standardization Mechanism

The standardized regression coefficients represent the values the regression coefficients

take when the units are such that Y and the explanatory variables all have equal

standard deviations. We standardize the partial regression coefficients by adjusting for

the differing standard deviation of Y and each Xi. Let sy denote the sample standard

deviation of Y , and let sx1, sx2

, . . . , sxkdenote the sample standard deviations of the

explanatory variables.

The estimates of the standardized regression coefficients are

b∗1 = b1

(

sx1

sy

)

, b∗2 = b2

(

sx2

sy

)

, . . . .

Example 11.10 Standardized Coefficients for Mental Impairment

The prediction equation relating mental impairment to life events and SES is

y = 28.23 + 0.103x1 − 0.097x2.

Table 11.2 reported the sample standard deviations sy = 5.5, sx1= 22.6, and sx2

=

25.3. Since the unstandardized coefficient of x1 is b1 = 0.103, the estimated standard-

ized coefficient is

b∗1 = b1

(

sx1

sy

)

= 0.103(

22.6

5.5

)

= 0.43.

Since b2 = −0.097, the standardized value equals

b∗2 = b2

(

sx2

sy

)

= −0.097(

25.3

5.5

)

= −0.45.

The estimated change in the mean of Y for a standard deviation increase in x1,

controlling for x2, has similar magnitude as the estimated change for a standard

deviation increase in x2, controlling for x1. However the partial effect of x1 is positive,

whereas the partial effect of x2 is negative.

Table 11.9, which repeats Table 11.5, shows how SPSS reports the estimated stan-

dardized regression coefficients. It uses the heading BETA, reflecting the alternative

name beta weights for these coefficients.

2

470 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

Table 11.9: SPSS Printout for Fit of Multiple Regression Model to Mental Impair-ment Data

Unstandardized Standardized

Coefficients Coefficients

B Std. Error Beta t Sig.

(Constant) 28.230 2.174 12.984 .000

LIFE .103 .032 .428 3.177 .003

SES -.097 .029 -.451 -3.351 .002

Properties of Standardized Regression Coefficients

For bivariate regression, standardizing the regression coefficient yields the correla-

tion. For the multiple regression model, the standardized partial regression coefficient

relates to the partial correlation (Exercise 67), and it usually takes similar value.

Unlike the partial correlation, however, b∗i need not fall between −1 and +1. A

value |b∗i | > 1 occasionally occurs when Xi is highly correlated with the set of other

explanatory variables in the model. In such cases, the standard errors are usually

large and the estimates are unreliable.

Since a standardized regression coefficient is a multiple of the unstandardized

coefficient, one equals 0 when the other does. The test of H0: β∗

i = 0 is equivalent to

the t test of H0: βi = 0. It is unnecessary to have separate tests for these coefficients.

In the sample, the magnitudes of the {b∗i } have the same relative sizes as the t statistics

from those tests. For example, the predictor with the greatest standardized partial

effect is the one that has the largest t statistic, in absolute value.

Standardized Form of Prediction Equation∗

Regression equations have an expression using the standardized regression coefficients.

In this equation, the variables appear in standardized form.

Notation for Standardized Variables

Let zY , zX1, . . . , zXk

denote the standardized versions of the variables Y, X1, . . . , Xk .

For instance, zY = (y − y)/sy represents the number of standard deviations that an

observation on y falls from its mean.

Each subject’s scores on y, x1, . . . , xk have corresponding z-scores for zY , zX1, . . . , zXk

.

If a subject’s score on x1 is such that zX1= (x1 − x1)/sx1

= 2.0, for instance, then

that subject falls two standard deviations above the mean x1 on that variable.

Let zY = (y − y)/sy denote the predicted z-score for the response variable. For

the standardized variables and the estimated standardized regression coefficients, the

prediction equation is

zY = b∗1zX1+ b∗2zX2

+ · · · + b∗kzXk.

11.8. STANDARDIZED REGRESSION COEFFICIENTS∗ 471

This equation predicts how far an observation on y falls from its mean, in standard

deviation units, based on how far the explanatory variables fall from their means, in

standard deviation units. The standardized coefficients are the weights attached to

the standardized explanatory variables in contributing to the predicted standardized

response variable.

Example 11.11 Standardized Prediction Equation for Mental Impairment

Example 11.10 found that the estimated standardized regression coefficients for

the life events and SES predictors of mental impairment are b∗1 = 0.43 and b∗2 = −0.45.

The prediction equation relating the standardized variables is therefore

zY = 0.43zX1− 0.45zX2

.

Consider a subject who is two standard deviations above the mean on life events

but two standard deviations below the mean on SES. This subject has a predicted

standardized mental impairment of

zY = 0.43(2) − 0.45(−2) = 1.8.

The predicted mental impairment for that subject is 1.8 standard deviations above

the mean. If the distribution of mental impairment is approximately normal, this

subject might well have mental health problems, since only about 4% of the scores in

a normal distribution fall at least 1.8 standard deviations above their mean.

2

In the prediction equation with standardized variables, no intercept term appears.

Why is this? When the standardized explanatory variables all equal 0, those variables

all fall at their means. Then, y = y, so that

zY =y − y

sy= 0.

So, this merely tells us that a subject who falls at the mean on each explanatory

variable is predicted to fall at the mean on the response variable.

Cautions in Comparing Standardized Regression Coeffi-

cients

To assess which predictor in a multiple regression model has the greatest impact on the

response variable, it is tempting to compare their standardized regression coefficients.

Make such comparisons with caution. In some cases, the observed differences in the

b∗i may simply reflect sampling error. In particular, when multicollinearity exists, the

standard errors are high and the estimated standardized coefficients may be unstable.

Keep in mind also that the effects are partial ones, depending on which other

variables are in the model. An explanatory variable that seems important in one

472 CHAPTER 11. MULTIPLE REGRESSION AND CORRELATION

system of variables may seem unimportant when other variables are controlled. For

example, it is possible that |b∗2| > |b∗1| in a model with two explanatory variables, yet

when a third explanatory variable is added to the model, |b∗2| < |b∗1|.It is unnecessary to standardize to compare the effect of the same variable for two

groups, such as in comparing the results of separate regressions for females and males,

since the units of measurement are the same in each group. In fact, it is usually unwise

to standardize in this case, because the standardized coefficients are more susceptible

than the unstandardized coefficients to differences in the standard deviations of the

predictors. For instance, Section 9.6 showed that the correlation depends strongly on

the range of x-values sampled. Two groups that have the same value for an estimated

regression coefficient have different standardized coefficients if the standard deviation

of the predictor differs for the two groups.

Finally, if an explanatory variable is highly correlated with the set of other ex-

planatory variables, it is artificial to conceive of that variable changing while the

others remain fixed in value. As an extreme example, suppose Y = height, X1 =

length of left leg, and X2 = length of right leg. The correlation between X1 and X2

is extremely close to 1. It does not make much sense to imagine how Y changes as

X1 changes while X2 is controlled.

11.9 Chapter Summary

This chapter generalized the bivariate regression model to include additional explana-

tory variables. The multiple regression equation relating a response variable Y

to a set of k explanatory variables is

E(Y ) = α + β1x1 + β2x2 + · · · + βkxk.

• The {βi} are partial regression coefficients . The value βi is the change

in the mean of Y for a one-unit change in xi, controlling for the other variables

in the model.

• The multiple correlation R describes the association between Y and the

collective set of explanatory variables. It equals the correlation between the

observed and predicted y-values. It falls between 0 and 1.

• R2 = (TSS − SSE)/TSS represents the proportional reduction in error from

predicting Y using the prediction equation y = a + b1x1 + b2x2 + · · · + bkxk

instead of y. It equals the square of the multiple correlation.

• A partial correlation , such as rY X1·X2, describes the association between

two variables, controlling for others. It falls between −1 and +1.

• The squared partial correlation between Y and xi represents the proportion of

the variation in Y that can be explained by xi, out of that part left unexplained

by a set of control variables.

Chap. 11 Problems 473

• An F statistic tests H0 : β1 = β2 = · · · = βk = 0, that the response variable

is independent of all the predictors. A small P -value suggests that at least one

predictor affects the response.

• Individual t tests and confidence intervals for {βi} analyze partial effects of each

predictor, controlling for the other variables in the model.

• Interaction between x1 and x2 in their effects on Y means that the effect of

either predictor changes as the value of the other predictor changes. We can

allow this by introducing cross-products of explanatory variables to the model,

such as the term β3(x1x2).

• To compare regression models, a complete model and a simpler reduced

model, the F test compares the SSE values or R2 values.

• Standardized regression coefficients do not depend on the units of mea-

surement. The estimated standardized coefficient b∗i describes the change in Y ,

in Y standard deviation units, for a one standard deviation increase in xi, con-

trolling for the other explanatory variables.

To illustrate, with k = 2 explanatory variables, the prediction equation is

Y = a + b1x1 + b2x2.

Fixing x2, a straight line describes the relation between Y and x1. Its slope b1is the change in y for a one-unit increase in x1, controlling for x2. The multiple

correlation R is at least as large as the correlations between Y and each predictor.

The squared partial correlation r2Y X2·X1

is the proportion of the variation of Y that

is explained by x2, out of that part of the variation left unexplained by x1. The

estimated standardized regression coefficient b∗1 = b1(sx1/sy) describes the effect of a

standard deviation change in x1, controlling for x2.

Table 11.10 summarizes the basic properties and inference methods for these mea-

sures and those introduced in Chapter 9 for bivariate regression.

The model studied in this chapter is still somewhat restrictive in the sense that

all the predictors are quantitative. The next chapter shows how to include categorical

predictors in the model.

PROBLEMS

Practicing the Basics

1. For students at Walden University, the relationship between Y = college GPA

(with range 0–4.0) and X1 = high school GPA (range 0–4.0) and X2 = college

d) Can be used to test whether the model E(Y ) = α + β1x1 + β2x2 gives a

significantly better fit than the model E(Y ) = α + β1x1 + β2x3.