40

CHALLENGES AND OPPORTUNITIES IN THE TANKER MARKETS MARK WILLIAMS, MANAGING PARTNER, AFFINITY RESEARCH 20/10/2017

CHALLENGES AND OPPORTUNITIES IN THE TANKER MARKETS

MARK WILL IAMS,

MANAGING PARTNER, AFF IN ITY RESEARCH

2 0 / 1 0 / 2 0 1 7

SYNOPSIS

WHAT HAPPENED TO 2017?

MACRO ECONOMIC and GEOPOLITICAL ISSUES

OIL AND TANKER DEMAND TRENDS

TANKER SUPPLY

FREIGHT MARKET OUTLOOK

TECH TRENDS AND TANKER SHIPPING

CONCLUSIONS…AND UNANSWERABLE QUESTIONS

LPG COMMENTS

LNG COMMENTS

20/10/2017

Challenges and Opportunities in the Tanker Markets

2

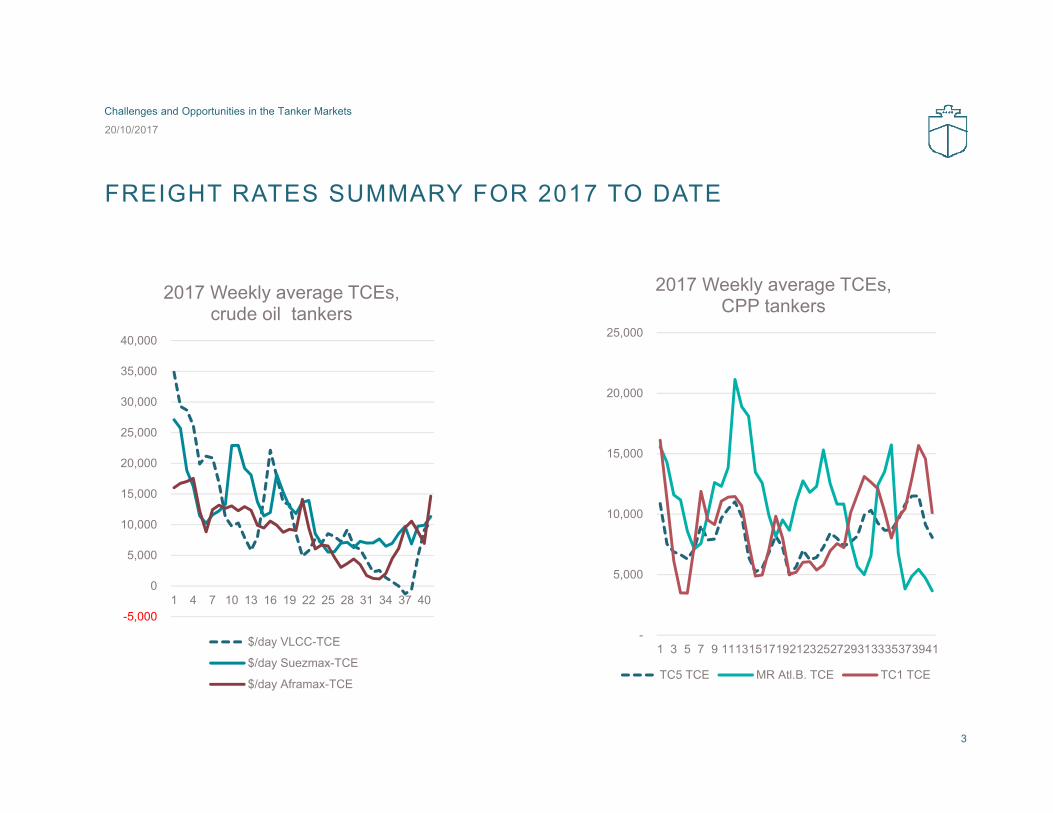

FREIGHT RATES SUMMARY FOR 2017 TO DATE

20/10/2017

Challenges and Opportunities in the Tanker Markets

3

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1 4 7 10 13 16 19 22 25 28 31 34 37 40

2017 Weekly average TCEs, crude oil tankers

$/day VLCC-TCE

$/day Suezmax-TCE

$/day Aframax-TCE

-

5,000

10,000

15,000

20,000

25,000

1 3 5 7 9 11131517192123252729313335373941

2017 Weekly average TCEs, CPP tankers

TC5 TCE MR Atl.B. TCE TC1 TCE

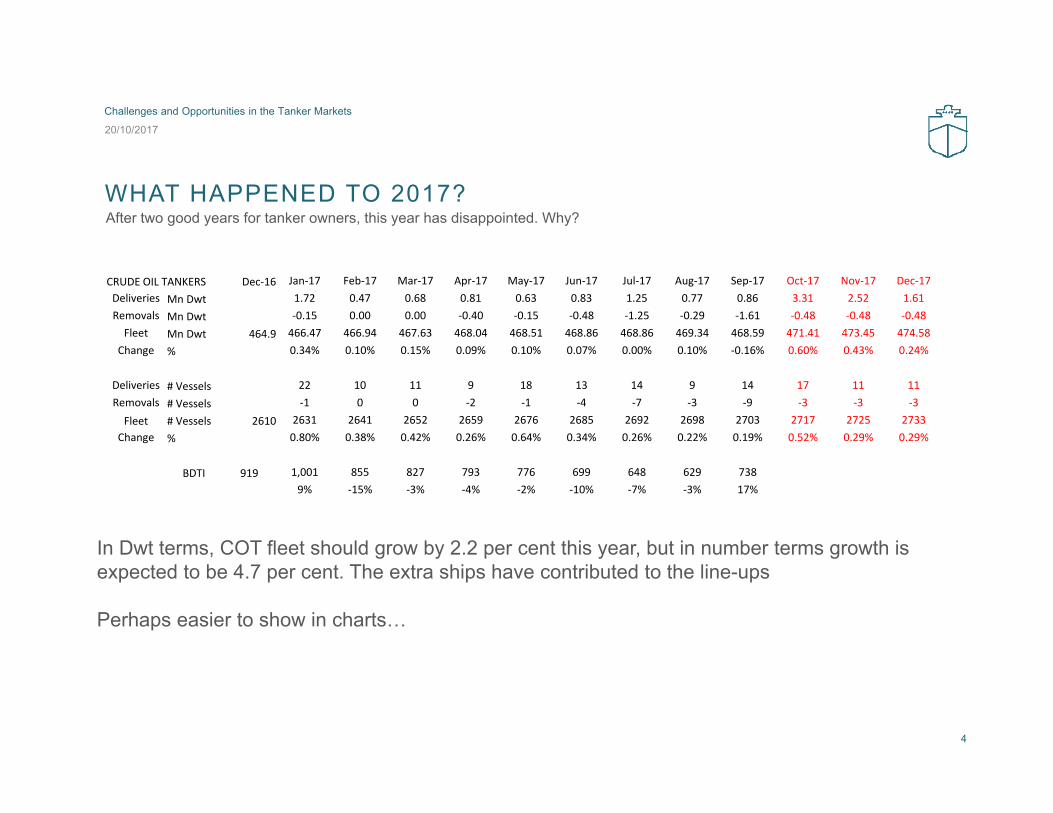

WHAT HAPPENED TO 2017?

CRUDE OIL TANKERS Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17 Oct‐17 Nov‐17 Dec‐17Deliveries Mn Dwt 1.72 0.47 0.68 0.81 0.63 0.83 1.25 0.77 0.86 3.31 2.52 1.61Removals Mn Dwt ‐0.15 0.00 0.00 ‐0.40 ‐0.15 ‐0.48 ‐1.25 ‐0.29 ‐1.61 ‐0.48 ‐0.48 ‐0.48Fleet Mn Dwt 464.9 466.47 466.94 467.63 468.04 468.51 468.86 468.86 469.34 468.59 471.41 473.45 474.58

Change % 0.34% 0.10% 0.15% 0.09% 0.10% 0.07% 0.00% 0.10% ‐0.16% 0.60% 0.43% 0.24%

Deliveries # Vessels 22 10 11 9 18 13 14 9 14 17 11 11Removals # Vessels ‐1 0 0 ‐2 ‐1 ‐4 ‐7 ‐3 ‐9 ‐3 ‐3 ‐3Fleet # Vessels 2610 2631 2641 2652 2659 2676 2685 2692 2698 2703 2717 2725 2733

Change % 0.80% 0.38% 0.42% 0.26% 0.64% 0.34% 0.26% 0.22% 0.19% 0.52% 0.29% 0.29%

BDTI 919 1,001 855 827 793 776 699 648 629 7389% ‐15% ‐3% ‐4% ‐2% ‐10% ‐7% ‐3% 17%

After two good years for tanker owners, this year has disappointed. Why?

20/10/2017

Challenges and Opportunities in the Tanker Markets

4

In Dwt terms, COT fleet should grow by 2.2 per cent this year, but in number terms growth is expected to be 4.7 per cent. The extra ships have contributed to the line-ups

Perhaps easier to show in charts…

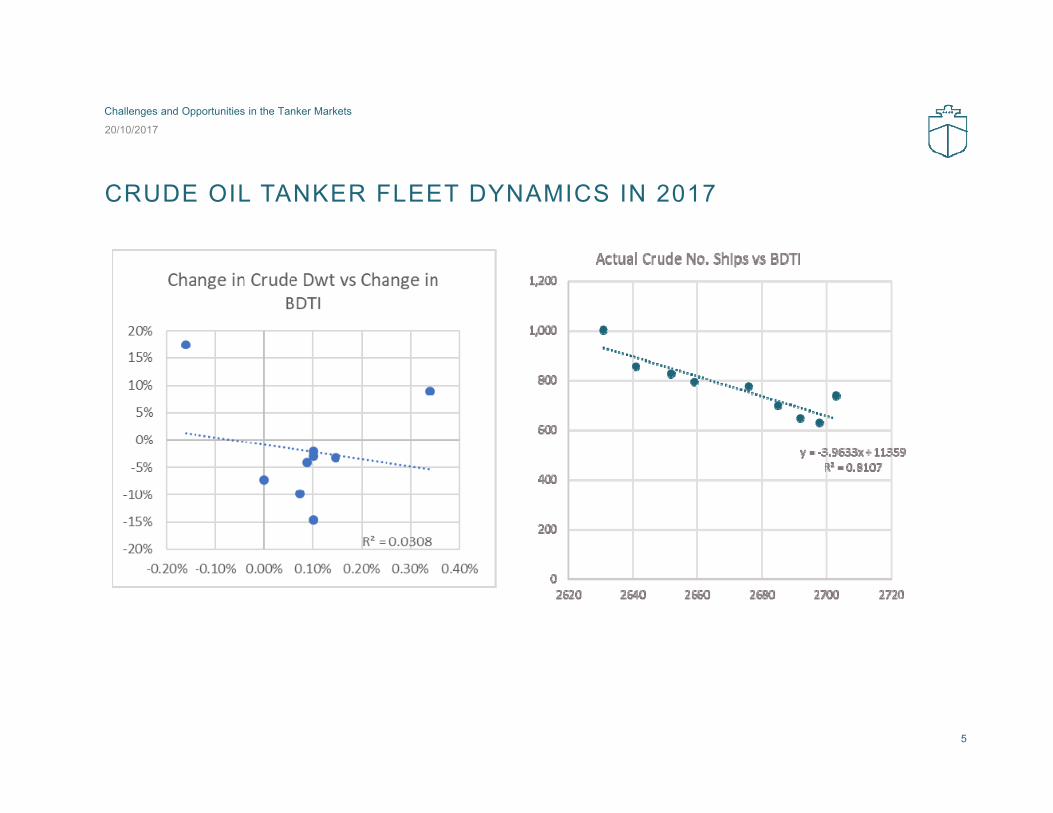

CRUDE OIL TANKER FLEET DYNAMICS IN 2017

20/10/2017

Challenges and Opportunities in the Tanker Markets

5

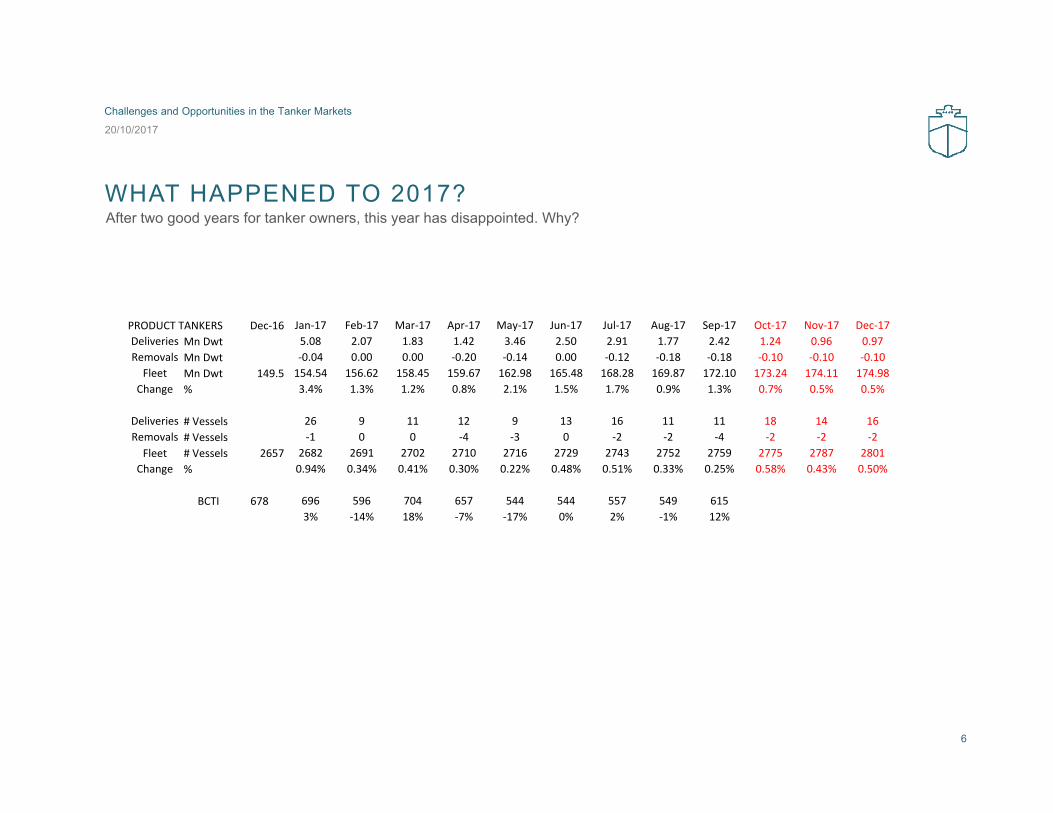

WHAT HAPPENED TO 2017?After two good years for tanker owners, this year has disappointed. Why?

20/10/2017

Challenges and Opportunities in the Tanker Markets

6

PRODUCT TANKERS Dec‐16 Jan‐17 Feb‐17 Mar‐17 Apr‐17 May‐17 Jun‐17 Jul‐17 Aug‐17 Sep‐17 Oct‐17 Nov‐17 Dec‐17Deliveries Mn Dwt 5.08 2.07 1.83 1.42 3.46 2.50 2.91 1.77 2.42 1.24 0.96 0.97Removals Mn Dwt ‐0.04 0.00 0.00 ‐0.20 ‐0.14 0.00 ‐0.12 ‐0.18 ‐0.18 ‐0.10 ‐0.10 ‐0.10Fleet Mn Dwt 149.5 154.54 156.62 158.45 159.67 162.98 165.48 168.28 169.87 172.10 173.24 174.11 174.98

Change % 3.4% 1.3% 1.2% 0.8% 2.1% 1.5% 1.7% 0.9% 1.3% 0.7% 0.5% 0.5%

Deliveries # Vessels 26 9 11 12 9 13 16 11 11 18 14 16Removals # Vessels ‐1 0 0 ‐4 ‐3 0 ‐2 ‐2 ‐4 ‐2 ‐2 ‐2Fleet # Vessels 2657 2682 2691 2702 2710 2716 2729 2743 2752 2759 2775 2787 2801

Change % 0.94% 0.34% 0.41% 0.30% 0.22% 0.48% 0.51% 0.33% 0.25% 0.58% 0.43% 0.50%

BCTI 678 696 596 704 657 544 544 557 549 6153% ‐14% 18% ‐7% ‐17% 0% 2% ‐1% 12%

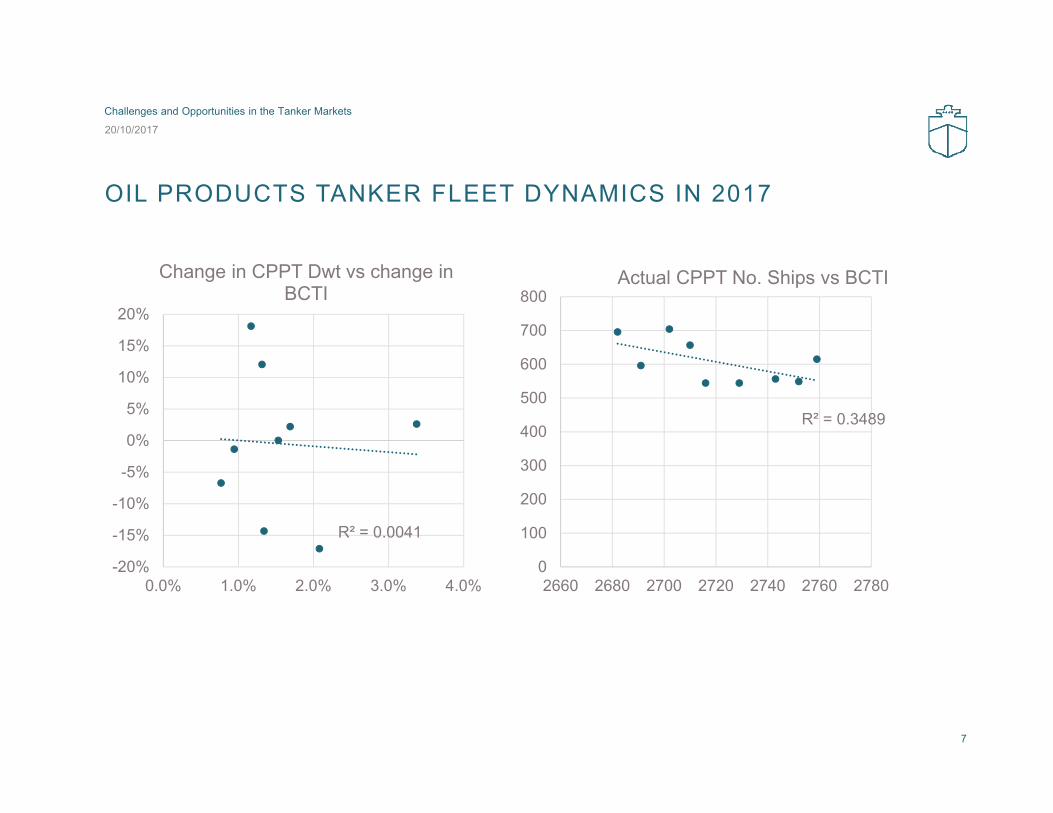

OIL PRODUCTS TANKER FLEET DYNAMICS IN 2017

20/10/2017

Challenges and Opportunities in the Tanker Markets

7

R² = 0.0041

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

0.0% 1.0% 2.0% 3.0% 4.0%

Change in CPPT Dwt vs change in BCTI

R² = 0.3489

0

100

200

300

400

500

600

700

800

2660 2680 2700 2720 2740 2760 2780

Actual CPPT No. Ships vs BCTI

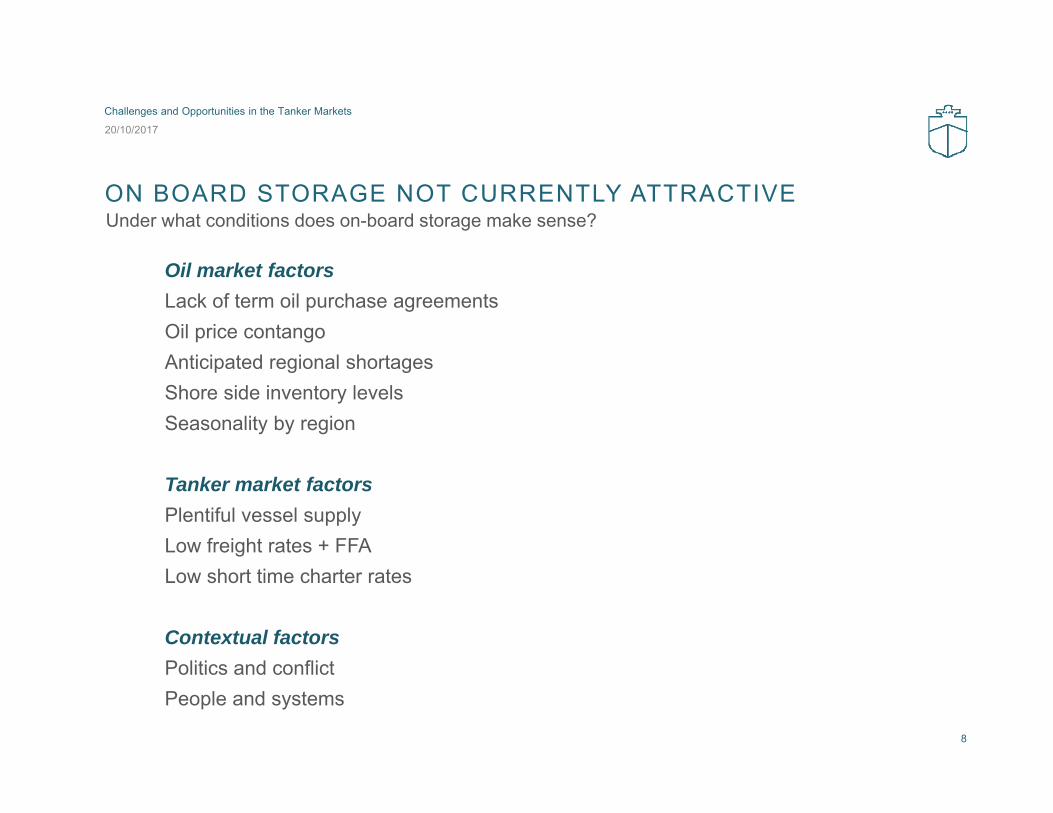

ON BOARD STORAGE NOT CURRENTLY ATTRACTIVE

Oil market factorsLack of term oil purchase agreementsOil price contangoAnticipated regional shortagesShore side inventory levelsSeasonality by region

Tanker market factorsPlentiful vessel supplyLow freight rates + FFALow short time charter rates

Contextual factorsPolitics and conflictPeople and systems

Under what conditions does on-board storage make sense?

20/10/2017

Challenges and Opportunities in the Tanker Markets

8

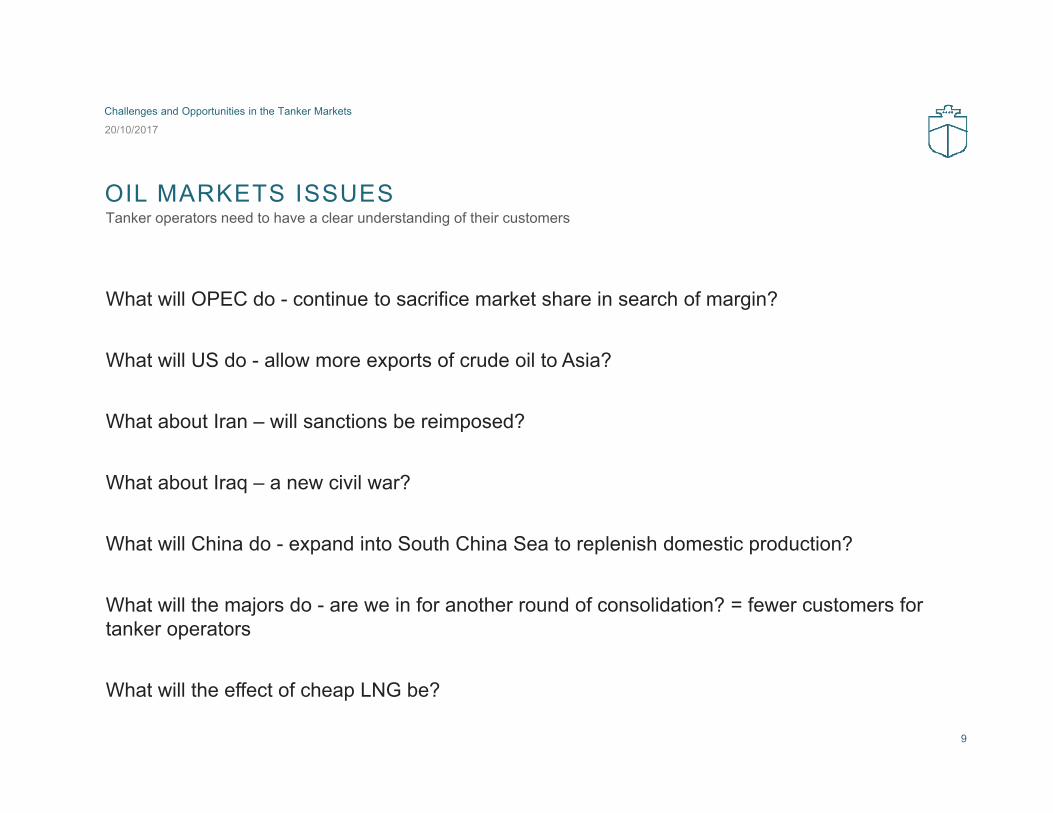

OIL MARKETS ISSUESTanker operators need to have a clear understanding of their customers

20/10/2017

Challenges and Opportunities in the Tanker Markets

9

What will OPEC do - continue to sacrifice market share in search of margin?

What will US do - allow more exports of crude oil to Asia?

What about Iran – will sanctions be reimposed?

What about Iraq – a new civil war?

What will China do - expand into South China Sea to replenish domestic production?

What will the majors do - are we in for another round of consolidation? = fewer customers for tanker operators

What will the effect of cheap LNG be?

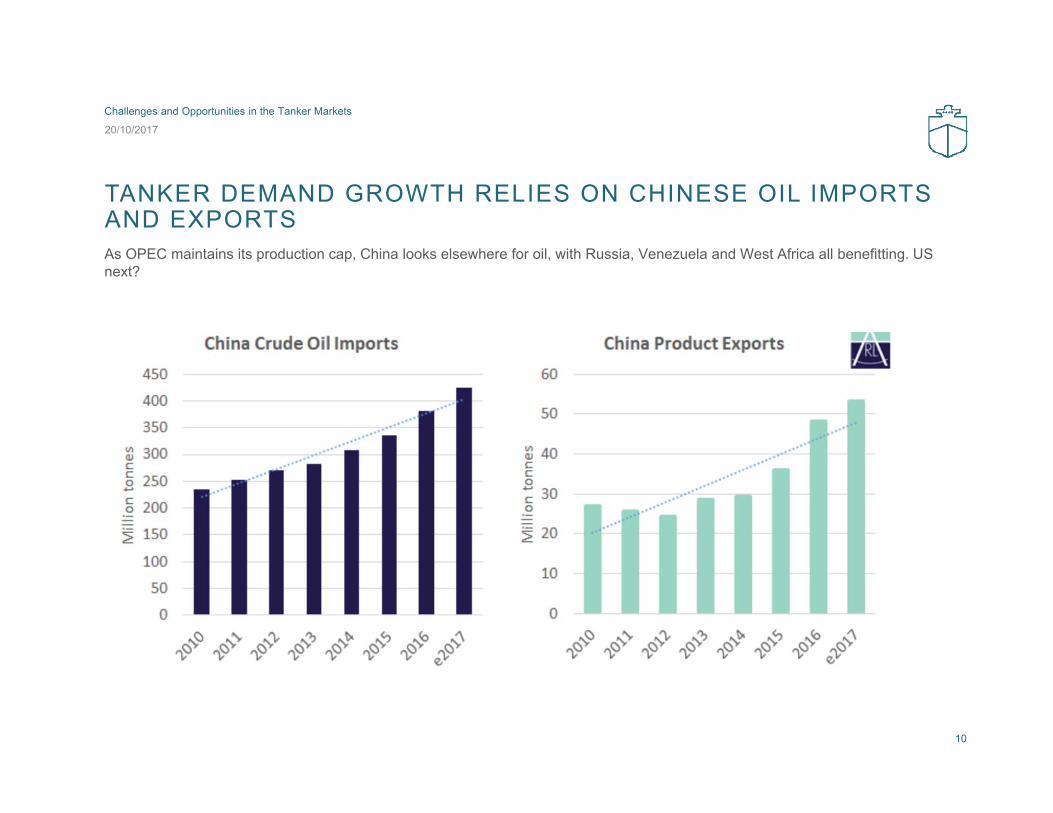

TANKER DEMAND GROWTH RELIES ON CHINESE OIL IMPORTS AND EXPORTSAs OPEC maintains its production cap, China looks elsewhere for oil, with Russia, Venezuela and West Africa all benefitting. US next?

20/10/2017

Challenges and Opportunities in the Tanker Markets

10

MACRO AND GEOPOLITICAL ISSUES

Long Term Climate Change & Policy Response- effects on oil demand

Real Time Pollution control and Ballast Water- ship designs, regulatory push on newbuilding demand

Global Trade - baton passed to China as the guarantor of globalisation

WTO now a dead duck - are we back to an era of bilateralism or is that just for the Trump presidency?

Your 25 year asset faces a number of challenges

20/10/2017

Challenges and Opportunities in the Tanker Markets

11

EMERGING MARKETS TO DRIVE ENERGY DEMANDShell World Energy Model suggests that global oil demand will continue to grow with energy demand

20/10/2017

Challenges and Opportunities in the Tanker Markets

12

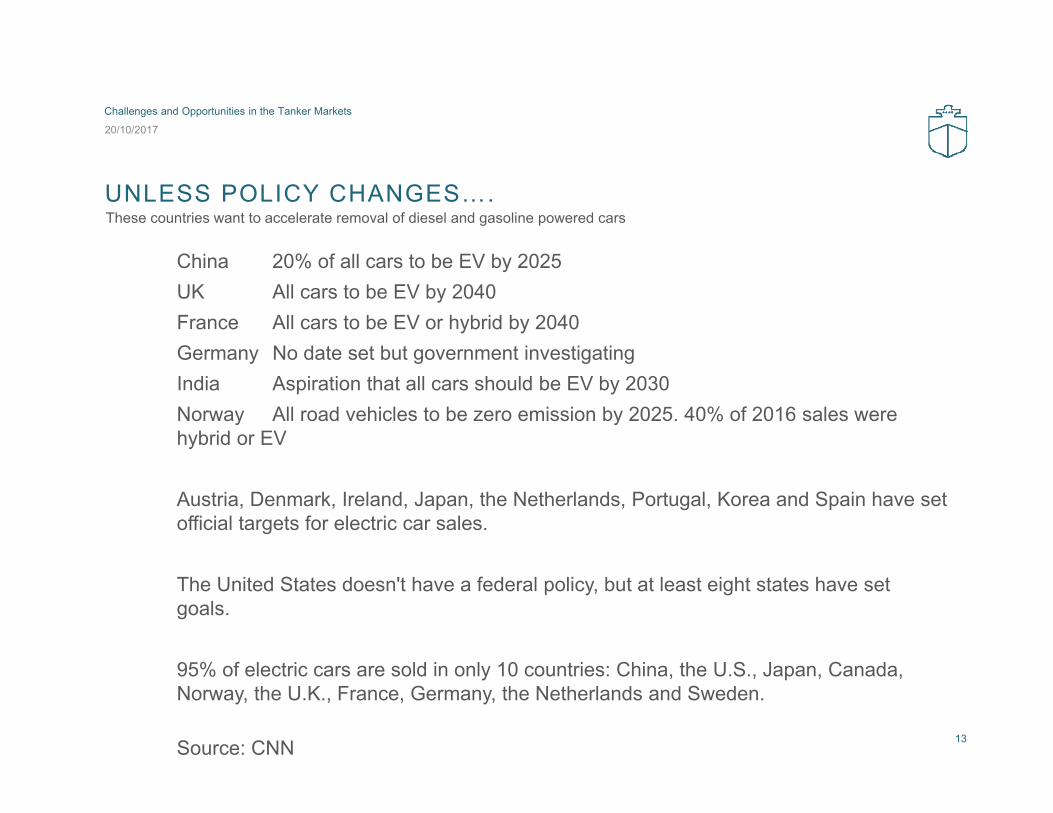

UNLESS POLICY CHANGES….

China 20% of all cars to be EV by 2025UK All cars to be EV by 2040France All cars to be EV or hybrid by 2040Germany No date set but government investigatingIndia Aspiration that all cars should be EV by 2030Norway All road vehicles to be zero emission by 2025. 40% of 2016 sales were hybrid or EV

Austria, Denmark, Ireland, Japan, the Netherlands, Portugal, Korea and Spain have set official targets for electric car sales.

The United States doesn't have a federal policy, but at least eight states have set goals.

95% of electric cars are sold in only 10 countries: China, the U.S., Japan, Canada, Norway, the U.K., France, Germany, the Netherlands and Sweden.

Source: CNN

These countries want to accelerate removal of diesel and gasoline powered cars

20/10/2017

Challenges and Opportunities in the Tanker Markets

13

TANKER FLEET AND ORDERBOOK AT 1ST OCTOBER 2017Supply Side Discipline Anyone?

20/10/2017

Challenges and Opportunities in the Tanker Markets

14

2017 YTD 2017 2018 2019 2020 2021

(Mn Dwt) (Mn Dwt) (No. of Ships) On Order as % of exist. fleet

Handysize 21.9 1.3 36 6.0% 13 9 17 7 3 0Medium Range 75.6 7.5 152 9.9% 57 21 68 49 13 1Panamax / LR1 32.3 2.7 36 8.3% 19 7 19 7 1 2

of which LR1: 27.2 2.4 32 8.7% 16 6 18 5 1 2

Aframax / LR2 109.6 15.5 137 14.2% 58 21 64 33 11 8of which LR2: 38.3 6.2 55 16.3% 32 12 20 12 7 4

Suezmax 86.5 10.4 67 12.0% 50 17 38 10 2 0VLCC 218.4 30.0 97 13.8% 41 12 48 36 1 0

Grand Total 544.2 67.5 525 12.4% 238 87 254 142 31 11

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 2016 Ytd 2017 Ytd 2016 Ytd 2017 YtdHandysize 0 0 0 0 0 0 5 4 7 2Medium Range 15 3 10 7 3 3 19 48 8 9Panamax / LR1 0 2 0 0 1 0 3 3 1 3

of which LR1: 0 1 0 0 1 0 3 2 1 3

Aframax / LR2 6 6 4 8 0 6 14 43 7 15of which LR2: 4 4 4 8 0 4 3 36 1 2

Suezmax 0 2 10 0 6 0 11 18 0 8VLCC 13 13 0 4 0 7 14 46 0 6Grand Total 34 26 24 19 10 16 66 162 23 43

Y-O-Y% change 145% Y-O-Y%

change 87%

Demolition

(No. of Ships)

5981590446

1015

5557134,917

18

New Contracts

52

22

60

2

Fleet Orderbook

Sold for Scrap

372

355

(No. of Vessels)

1

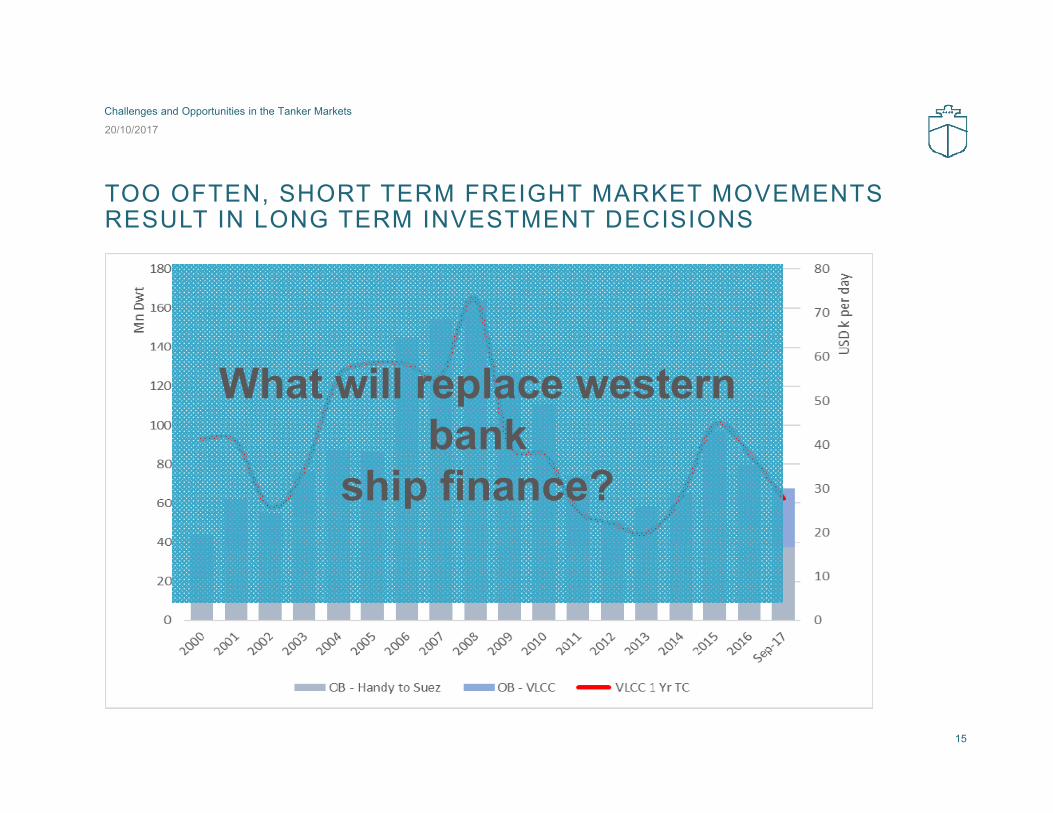

TOO OFTEN, SHORT TERM FREIGHT MARKET MOVEMENTS RESULT IN LONG TERM INVESTMENT DECISIONS

20/10/2017

Challenges and Opportunities in the Tanker Markets

15

What will replace western bank

ship finance?

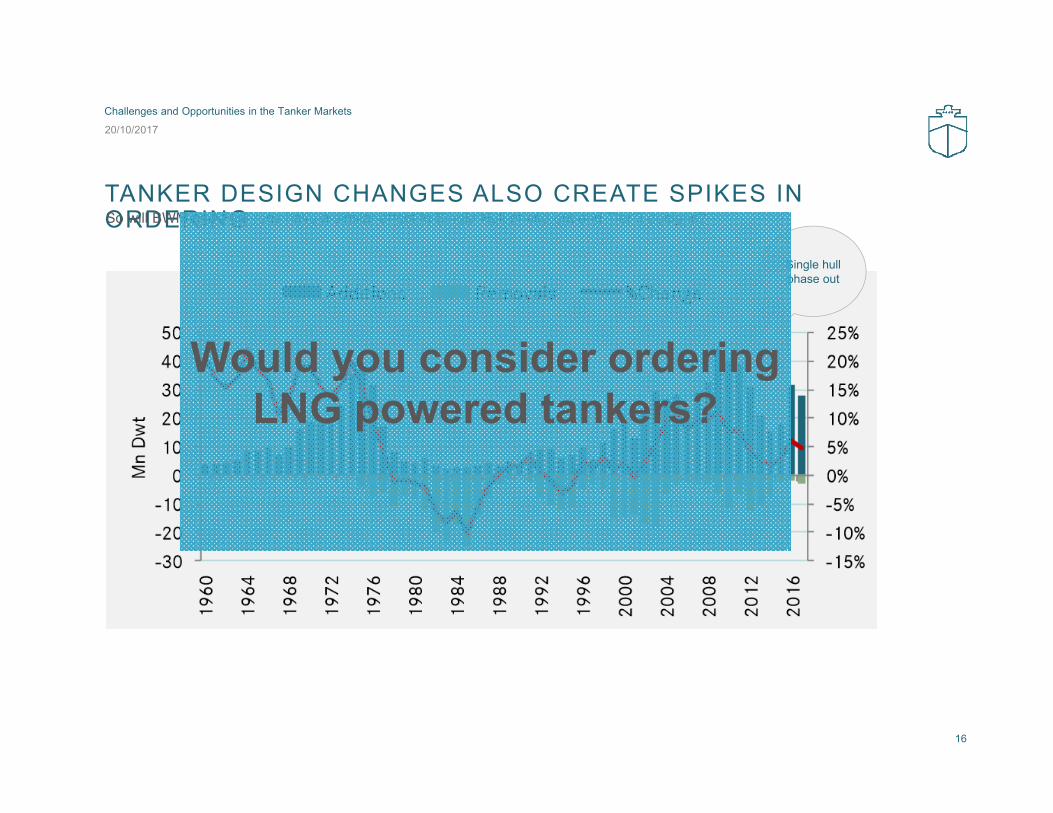

TANKER DESIGN CHANGES ALSO CREATE SPIKES IN ORDERINGSo will BWM and Fuel regs have a similar effect to Single Hull phase out and Tier 3 designs?

20/10/2017

Challenges and Opportunities in the Tanker Markets

16

Single hull phase out

Would you consider ordering LNG powered tankers?

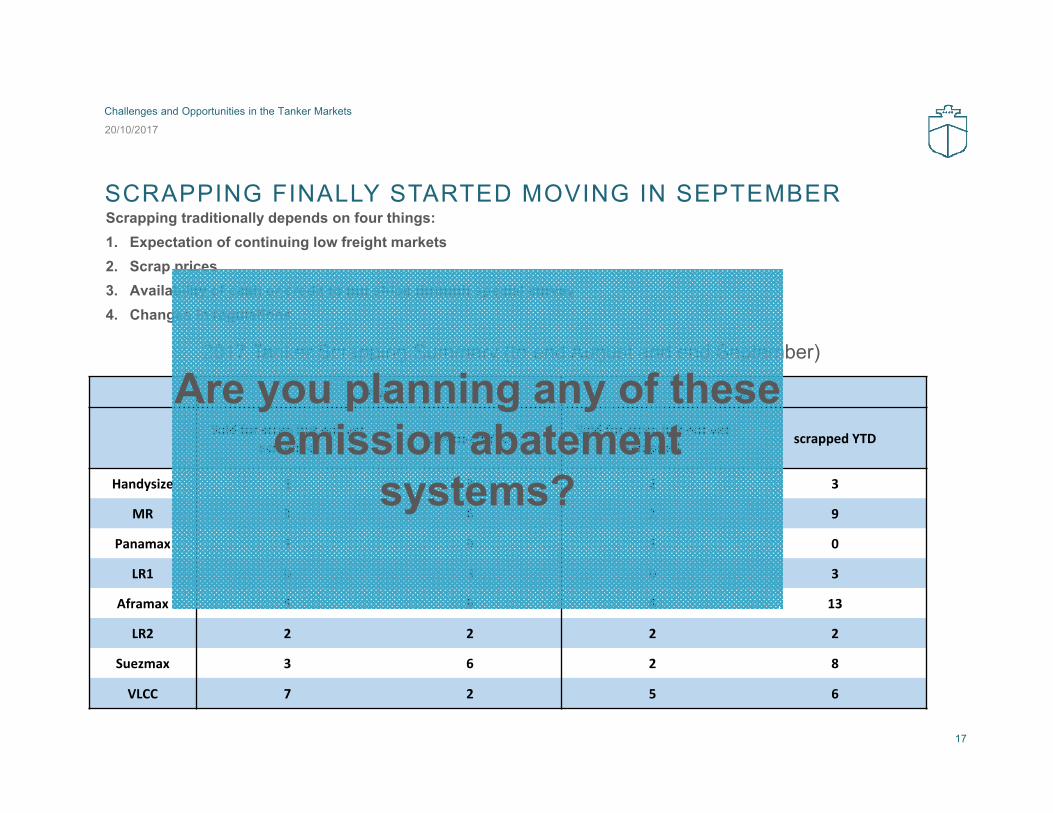

SCRAPPING FINALLY STARTED MOVING IN SEPTEMBERScrapping traditionally depends on four things:1. Expectation of continuing low freight markets2. Scrap prices3. Availability of cash or credit to put ships through special survey4. Changes in regulations

20/10/2017

Challenges and Opportunities in the Tanker Markets

17

2017 Tanker Scrapping Summary (to end August and end September)

Aug Sep

Sold for scrap but not yet scrapped scrapped YTD Sold for scrap but not yet

scrapped scrapped YTD

Handysize 1 3 2 3

MR 3 6 2 9

Panamax 1 0 1 0

LR1 0 3 0 3

Aframax 5 9 4 13

LR2 2 2 2 2

Suezmax 3 6 2 8

VLCC 7 2 5 6

Are you planning any of these emission abatement

systems?

BALTIC EXCHANGE DEMOLITION ASSESSMENTS

20/10/2017

Challenges and Opportunities in the Tanker Markets

18

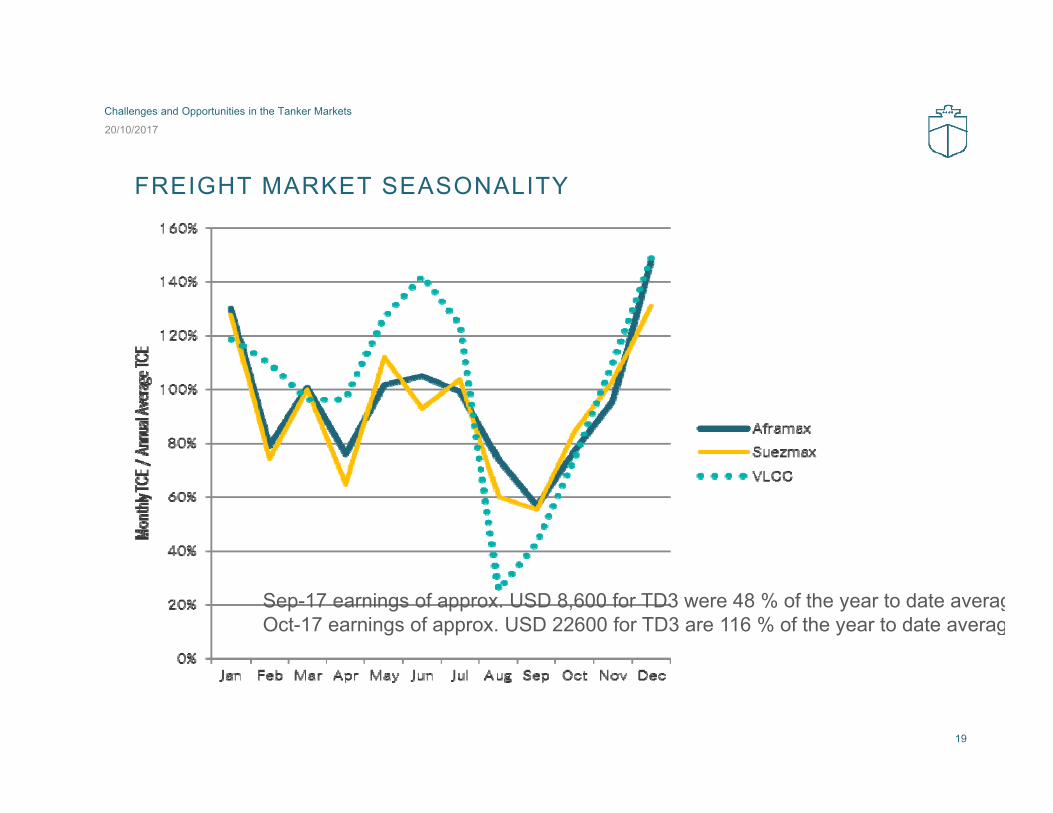

FREIGHT MARKET SEASONALITY

19

20/10/2017

Challenges and Opportunities in the Tanker Markets

Sep-17 earnings of approx. USD 8,600 for TD3 were 48 % of the year to date averagOct-17 earnings of approx. USD 22600 for TD3 are 116 % of the year to date averag

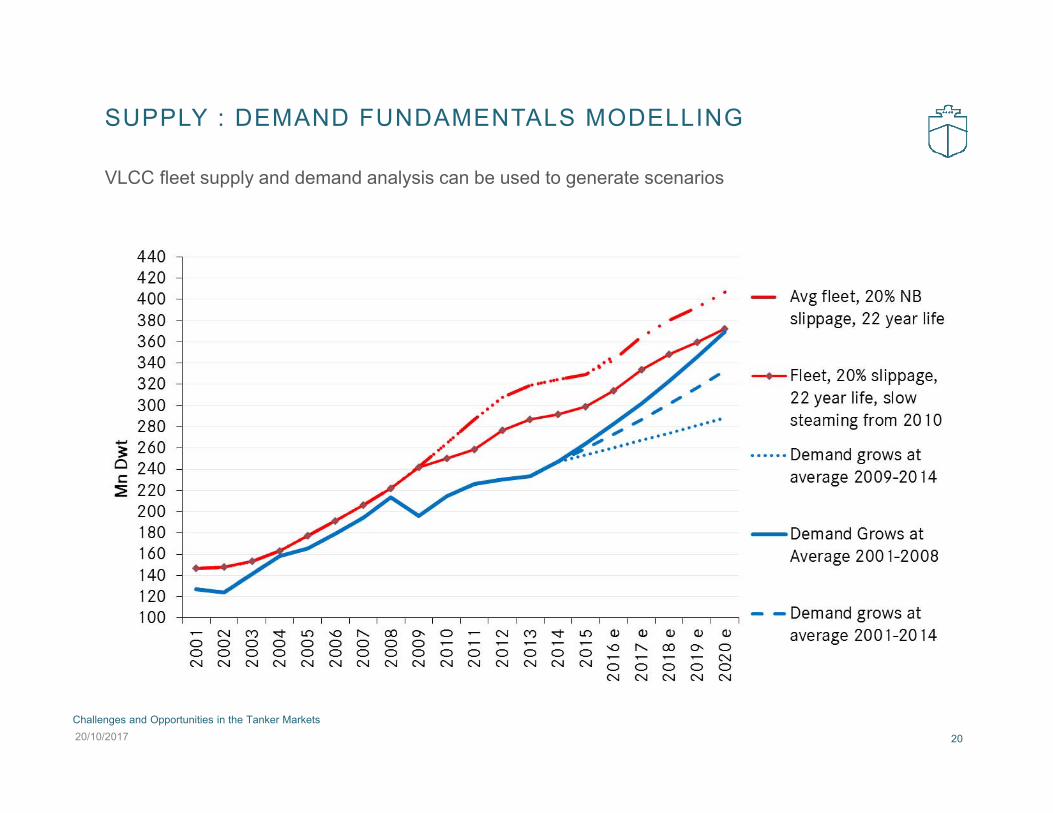

SUPPLY : DEMAND FUNDAMENTALS MODELLING

VLCC fleet supply and demand analysis can be used to generate scenarios

Challenges and Opportunities in the Tanker Markets

2020/10/2017

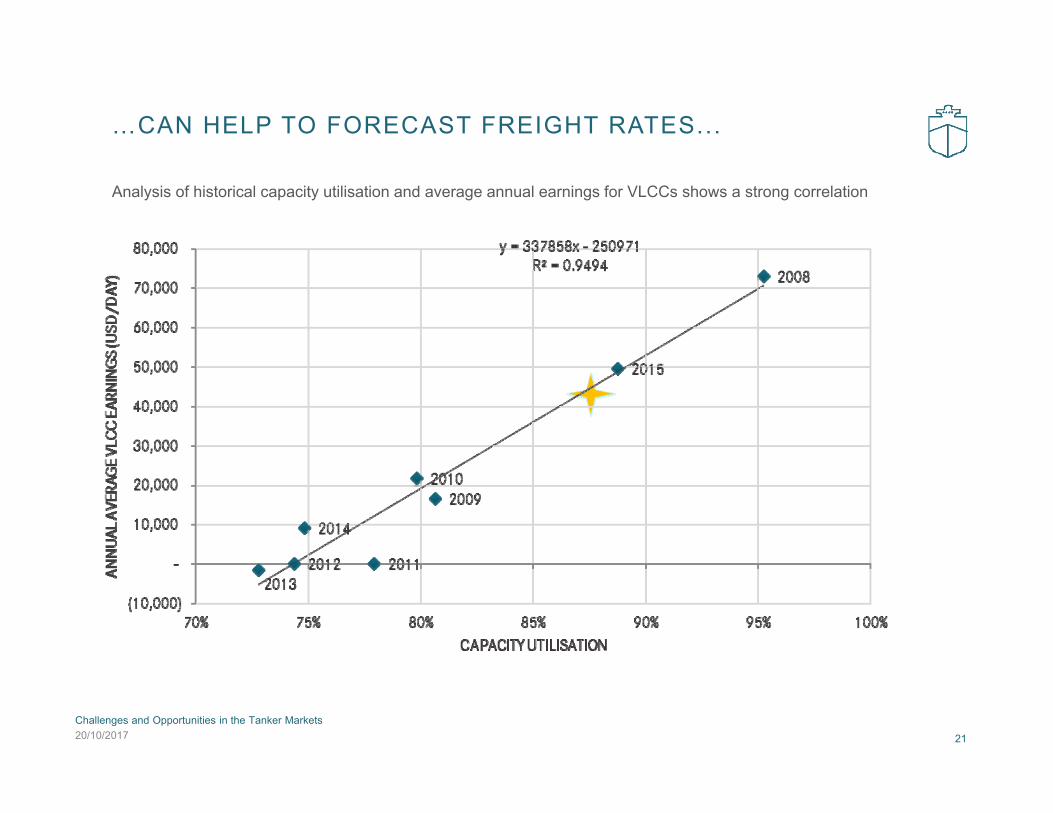

…CAN HELP TO FORECAST FREIGHT RATES...

Analysis of historical capacity utilisation and average annual earnings for VLCCs shows a strong correlation

Challenges and Opportunities in the Tanker Markets

2120/10/2017

NO SUCH THING AS A GOOD FORECAST, BUT HERE ARE SOME SCENARIOSThis is our forecast from January 2017…why did the market underperform?

20/10/2017

Challenges and Opportunities in the Tanker Markets

22

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

60%

65%

70%

75%

80%

85%

90%

95%

100%

105%

2001 2003 2005 2007 2009 2011 2013 2015 2017 e 2019 e 2021 e

ALL CR

UDE

OIL TAN

KERS

TCE

, USD

/ DA

Y

CAPA

CITY UTILISA

TION

Worst Case Capacity utilisation Base Case Capacity Utilisation historic average utilisation rate

Best Case Capacity utllisation Historic Average BDTI

20/10/2017

Challenges and Opportunities in the Tanker Markets

23

How will 2018 be compared to 2017?

TECH TRENDS AND TANKER SHIPPING

Maersk’s acquisition of Cargometrics suggests that there is some value in this Big Data concept. Better data can lead to better analysis and better insights delivering value to operators through commercial optimisation.

Not certain yet how Industry 4.0 will impact tanker shipping but let's suggest that it shortens global supply chains. Once you no longer need search for offshored cheap labour, then you don't need to put manufacturing far away from consumers. Will industrial demand for oil be disrupted?

Internet of things - self driving cars could hugely reduce car use, cutting oil demand, let alone self driving ships optimising utilisation and disrupting the freight market which relies on information asymmetry.

Alternative fuels, not just for ships but for everyone - we touched on effects of cheap natgasearlier. Oilco investment in gas is significant. Road and rail freight to gas and personal transport to EVs?

Good news is that nobody knows how to run ships as well as ship owners do. The opportunity is to slot into the midstream and become indispensable.

Big Data, Industry 4.0 and the Internet of Things

20/10/2017

Challenges and Opportunities in the Tanker Markets

24

DOES YOUR COMPANY HAVE A DATA STRATEGY?

CONCLUSIONS…UNANSWERABLE QUESTIONS…

What will replace petroleum products for transport, if they can be replaced at all?

Is the unmanned vessel viable? Is it desirable?

How will the rise of renewables and recycling industries affect oil shipping?

Is there any advantage to being the first mover or an early adopter of new shipping technology?

If manufacturing automation negates the need for offshored manufacturing labour, what happens to globalized supply chains?

Can better data mean better supply side discipline?

Who will pay for the next generation of tanker ships, if banks are exiting ship finance?

20/10/2017

Challenges and Opportunities in the Tanker Markets

25

LPG COMMENTS

LPG MARKET OUTLOOK

Global population and incomegrowth are key drivers to thegrowing demand for energy.

Increasing levels of carbonemissions have accelerated theneed for cleaner energy.

LPG is a clean energy sourceused by millions of consumersworldwide.

The boom in shale gas extractionhas increased the supply of LPGwhich is used in a range ofapplications in business, industry,transportation, farming, powergeneration, cooking, heating andfor recreational purposes.

With the world’s populationestimated to increase byapproximately 1.5 Bn people by2035, energy consumption isestimated to increase by 34%between 2014 and 2035.

Growth in the world’s population drives higher consumption of energy

20/10/2017

Challenges and Opportunities in the Tanker Markets

27

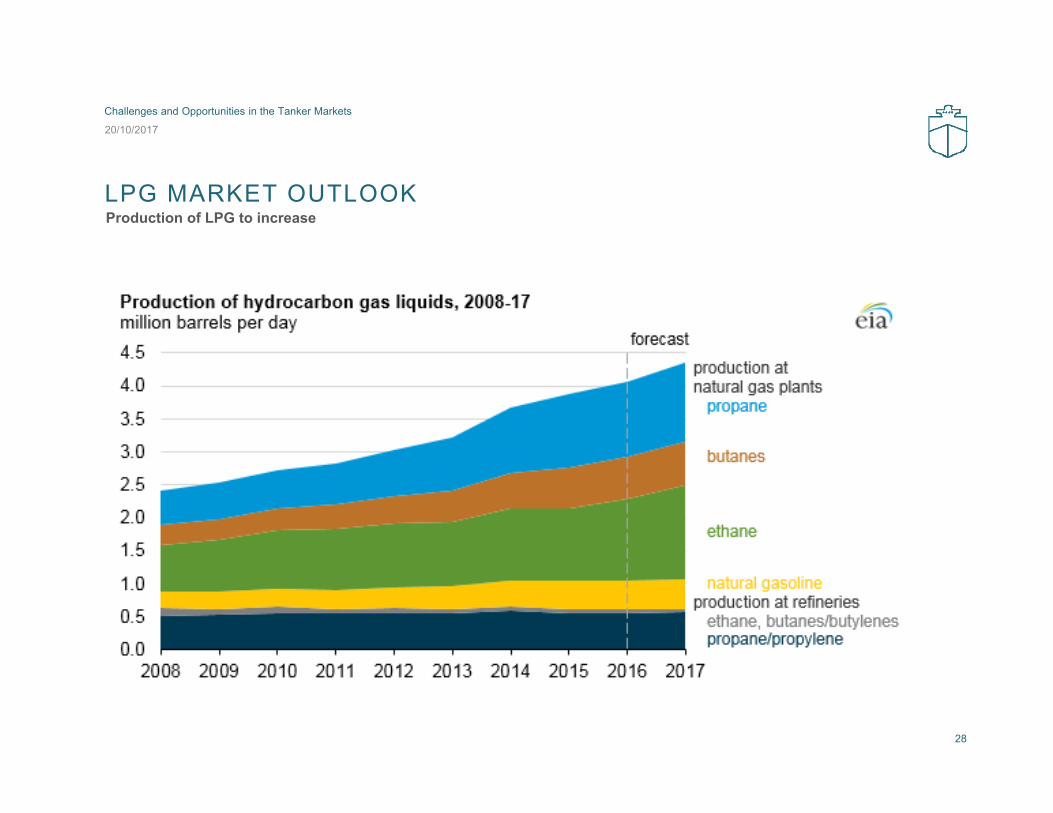

LPG MARKET OUTLOOKProduction of LPG to increase

20/10/2017

Challenges and Opportunities in the Tanker Markets

28

LPG MARKET OUTLOOK

Propane export capacityhas exceeded supplygrowth over the pastseveral years As supply has grown

exports have increased to45 per cent of total supplyin 2016 Propane Exports will

exceed 50 per cent ofsupply by 2019

Growth in the world’s population drives higher consumption of energy

20/10/2017

Challenges and Opportunities in the Tanker Markets

29

LPG IS COST EFFECTIVE AND ABUNDANT

US Propane is cheaper than Brentcrude oil, making it a cost effectivesolution

With the continued stream ofshale gas resources, anestablished supply chain andmarket structures, global LPGconsumption increased by 4% in2016 to 293 million metric tonnes,31% of which is seaborne.

Growth in the world’s population drives higher consumption of energy

20/10/2017

Challenges and Opportunities in the Tanker Markets

30

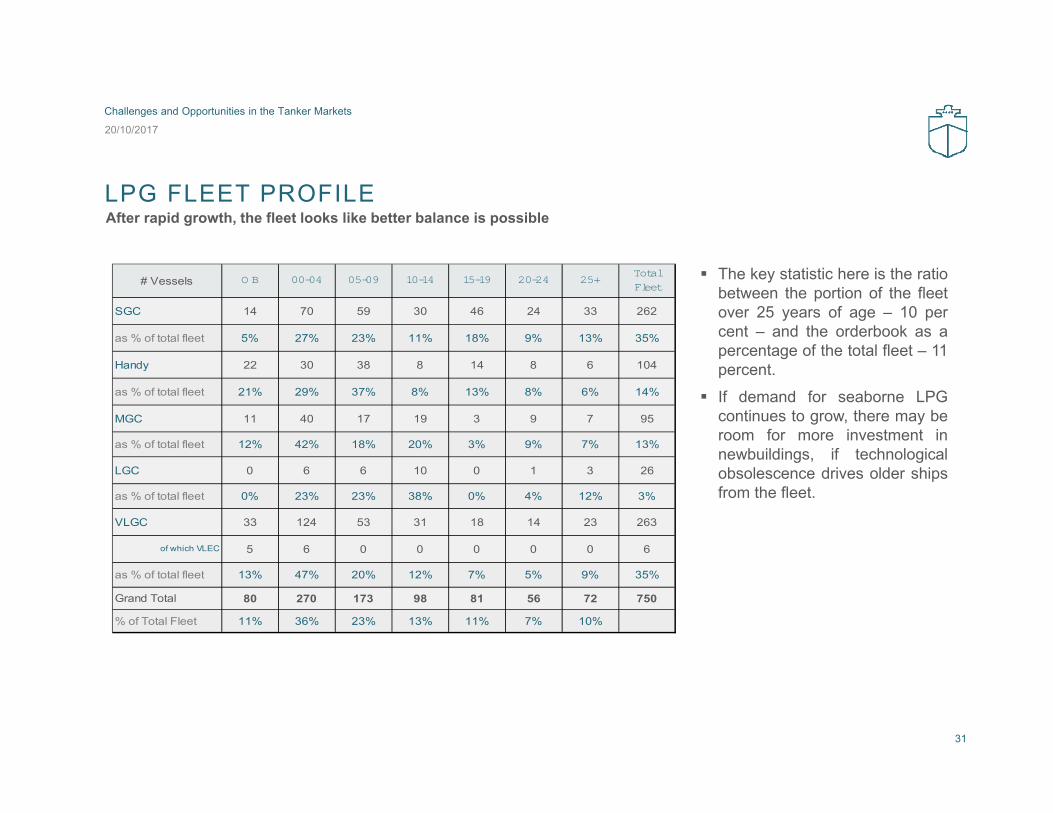

LPG FLEET PROFILE

The key statistic here is the ratiobetween the portion of the fleetover 25 years of age – 10 percent – and the orderbook as apercentage of the total fleet – 11percent.

If demand for seaborne LPGcontinues to grow, there may beroom for more investment innewbuildings, if technologicalobsolescence drives older shipsfrom the fleet.

After rapid growth, the fleet looks like better balance is possible

20/10/2017

Challenges and Opportunities in the Tanker Markets

31

# Vessels O B 00-04 05-09 10-14 15-19 20-24 25+Total Fleet

SGC 14 70 59 30 46 24 33 262

as % of total fleet 5% 27% 23% 11% 18% 9% 13% 35%

Handy 22 30 38 8 14 8 6 104

as % of total fleet 21% 29% 37% 8% 13% 8% 6% 14%

MGC 11 40 17 19 3 9 7 95

as % of total fleet 12% 42% 18% 20% 3% 9% 7% 13%

LGC 0 6 6 10 0 1 3 26

as % of total fleet 0% 23% 23% 38% 0% 4% 12% 3%

VLGC 33 124 53 31 18 14 23 263

of which VLEC 5 6 0 0 0 0 0 6

as % of total fleet 13% 47% 20% 12% 7% 5% 9% 35%

Grand Total 80 270 173 98 81 56 72 750

% of Total Fleet 11% 36% 23% 13% 11% 7% 10%

20/10/2017

Challenges and Opportunities in the Tanker Markets

32

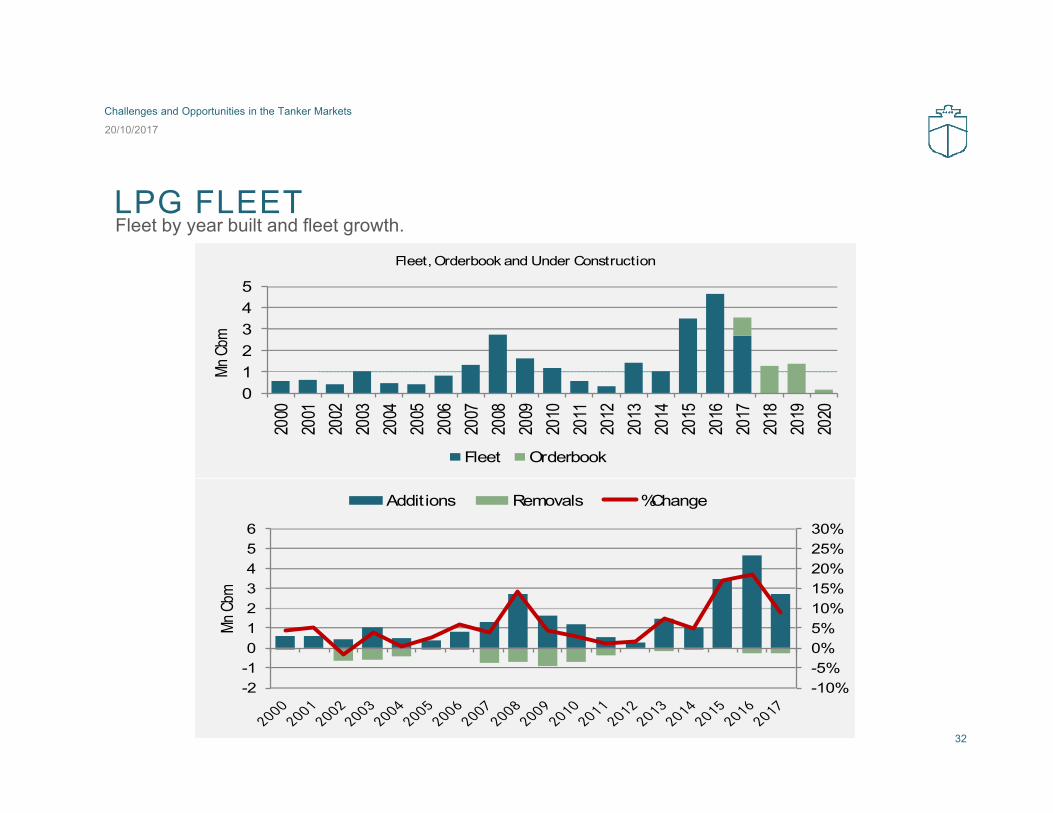

Fleet by year built and fleet growth. LPG FLEET

012345

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Mn C

bm

Fleet, Orderbook and Under Construction

Fleet Orderbook

-10%-5%0%5%10%15%20%25%30%

-2-10123456

Mn C

bm

Additions Removals %Change

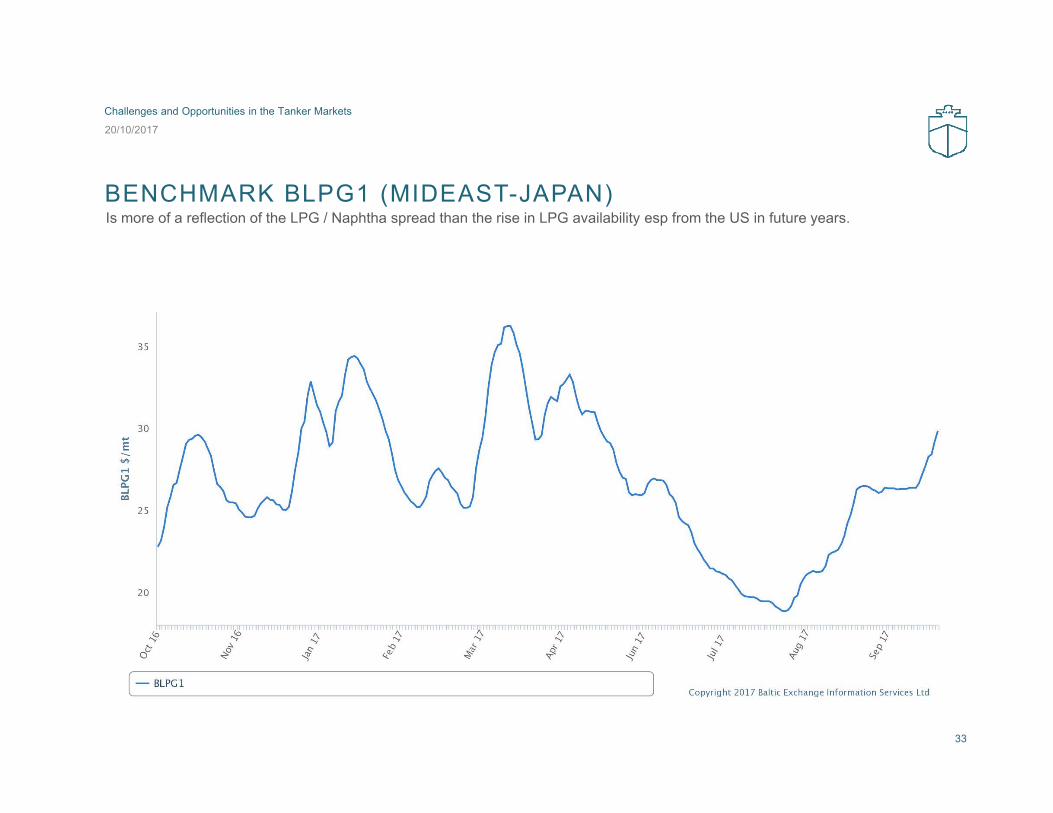

BENCHMARK BLPG1 (MIDEAST-JAPAN) Is more of a reflection of the LPG / Naphtha spread than the rise in LPG availability esp from the US in future years.

20/10/2017

Challenges and Opportunities in the Tanker Markets

33

LNG COMMENTS

In H1 2017 143 Mn T of LNG were exported, up 12% from H1 2016• Australia and the US produced an incremental 12 Mn T (H1-17 vs

H1-16)• This trend is expected to continue with existing trains ramping-up

capacity and new projects (Cameron LNG, Wheatstone LNG)coming online

• Malaysia contributed an additional 1.7 Mn T of supply growth in H12017. Petronas successfully commissioned Train 9 at Bintulu LNGcomplex in Q4 2016 and achieved its first cargo with the PFLNGSatu in March 2017

• LNG production at Trinidad and Tobago’s liquefaction facilitydeclined by 0.6 Mn T compared to the first half 2016. LNGproduction has been shrinking for more than a year due to gasshortages in the country

• Angola LNG continues to ramp up production after the plant’srestart last year. An additional 1.4 Mn T were exported in H1 2017versus H1 2016

US & AUSTRALIA INCREASE LNG EXPORTS

35Source: Affinity, Reuters

+6.8

+5.3+0.3

+3.7-0.5

+0.1

120

130

140

150Mt LNG

Incremental LNG Exports by Region, H1 2017 vs H1 2016 (million tons)

Incremental LNG Exports by Region, H1 2017 vs H1 2016 (million tons)

Incremental LNG Exports by Country, H1 2017 vs H1 2016 (million tons)

-1.1

-0.6

-0.5

-0.4

0.3

0.4

0.5

1.3

1.4

1.7

5.3

6.8

Indonesia

Trinidad

Norway

Brunei

⁞

Papua New Guinea

Equatorial Guinea

Egypt

Nigeria

Angola

Malaysia

United States

Australia

Note: LNG exports do not include re-exports and indigenous exports

+12% +5%

-0.5

+0.6

-1.8

-0.5

-0.4

0.6

0.6

0.7

0.9

1.0

1.2

2.7

4.0

4.3

United Kingdom

Brazil

United Arab Emirates

⁞

Portugal

Pakistan

Italy

France (Northern)

Turkey

Spain

South Korea

Japan

China

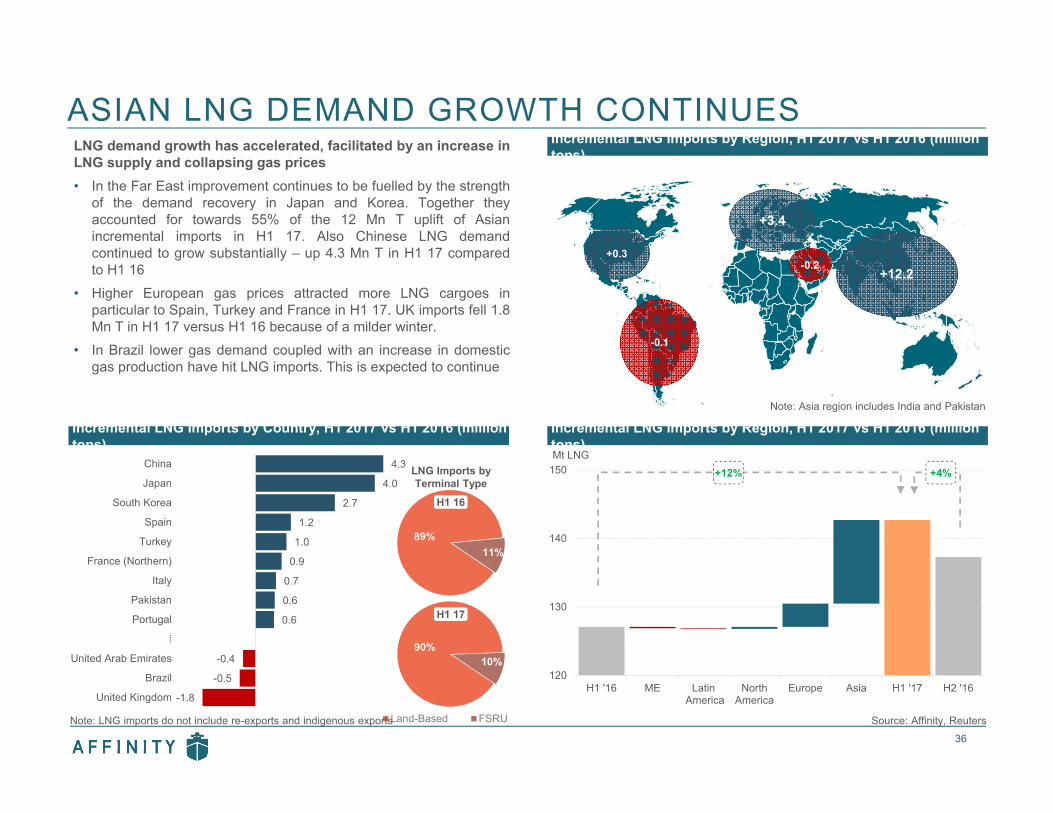

ASIAN LNG DEMAND GROWTH CONTINUES

36Source: Affinity, Reuters

90%10%

Land-Based FSRU

LNG Imports by Terminal Type

89%11%

H1 16

H1 17

Incremental LNG Imports by Region, H1 2017 vs H1 2016 (million tons)

Incremental LNG Imports by Region, H1 2017 vs H1 2016 (million tons)

Incremental LNG Imports by Country, H1 2017 vs H1 2016 (million tons)

LNG demand growth has accelerated, facilitated by an increase inLNG supply and collapsing gas prices• In the Far East improvement continues to be fuelled by the strength

of the demand recovery in Japan and Korea. Together theyaccounted for towards 55% of the 12 Mn T uplift of Asianincremental imports in H1 17. Also Chinese LNG demandcontinued to grow substantially – up 4.3 Mn T in H1 17 comparedto H1 16

• Higher European gas prices attracted more LNG cargoes inparticular to Spain, Turkey and France in H1 17. UK imports fell 1.8Mn T in H1 17 versus H1 16 because of a milder winter.

• In Brazil lower gas demand coupled with an increase in domesticgas production have hit LNG imports. This is expected to continue

120

130

140

150

H1 '16 ME Latin America

NorthAmerica

Europe Asia H1 '17 H2 '16

Mt LNG

+12.2+0.3

-0.2

-0.1

+3.4

Note: LNG imports do not include re-exports and indigenous exports

Note: Asia region includes India and Pakistan

+12% +4%

(150)

(100)

(50)

-

50

100

150

200

250

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2017 2018 2019 2020 2021

# Vesselsnormalized to 165m3 Vessel Demand Vessel Supply Shipping Balance

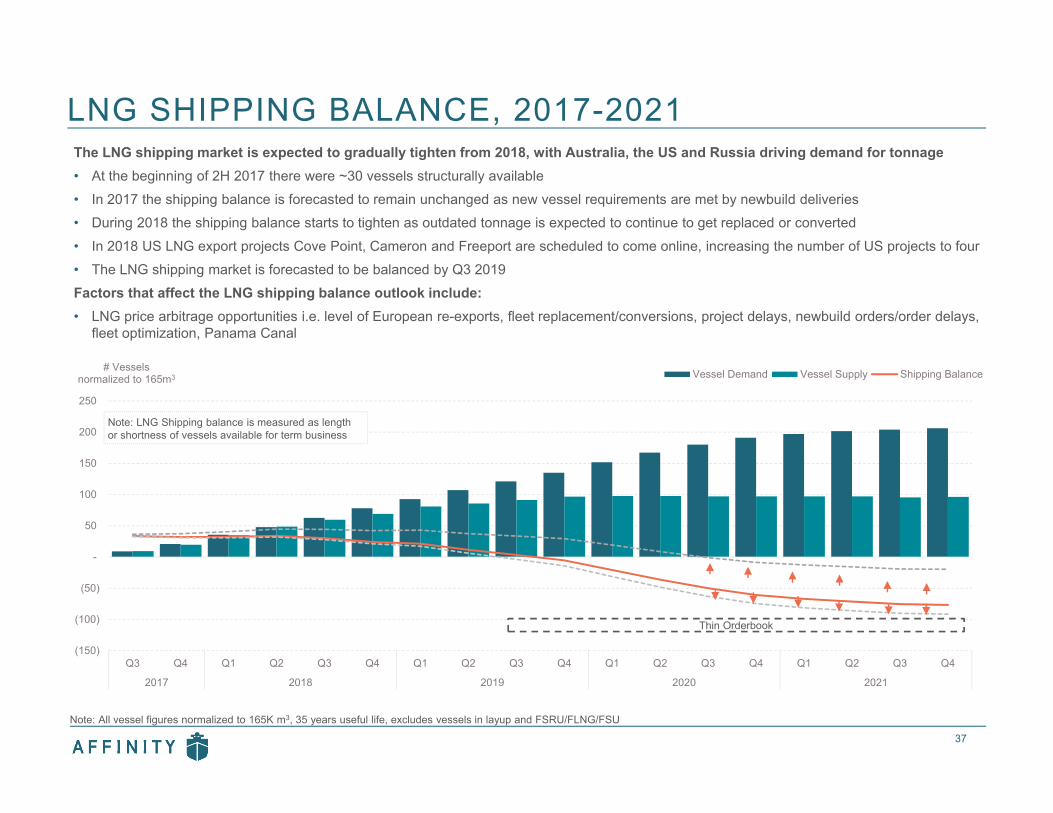

LNG SHIPPING BALANCE, 2017-2021

37

Note: LNG Shipping balance is measured as length or shortness of vessels available for term business

Note: All vessel figures normalized to 165K m3, 35 years useful life, excludes vessels in layup and FSRU/FLNG/FSU

Thin Orderbook

The LNG shipping market is expected to gradually tighten from 2018, with Australia, the US and Russia driving demand for tonnage• At the beginning of 2H 2017 there were ~30 vessels structurally available• In 2017 the shipping balance is forecasted to remain unchanged as new vessel requirements are met by newbuild deliveries• During 2018 the shipping balance starts to tighten as outdated tonnage is expected to continue to get replaced or converted• In 2018 US LNG export projects Cove Point, Cameron and Freeport are scheduled to come online, increasing the number of US projects to four• The LNG shipping market is forecasted to be balanced by Q3 2019Factors that affect the LNG shipping balance outlook include:• LNG price arbitrage opportunities i.e. level of European re-exports, fleet replacement/conversions, project delays, newbuild orders/order delays,

fleet optimization, Panama Canal

-

20

40

60

80

100

120

140

160US$ ‘000/day ST Assessed Spot Charter Rates TFDE Assessed Spot Charter Rates

Term Fixtures: Existing Tonnage Term Fixtures: Newbuild Tonnage

LNG SHIPPING MARKET - OVERVIEW

38

(60) (40) (20)

- 20 40 60

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 Jan-20

# VesselsPeriod of low to zero structural

availability

Speculative orders get delivered Thin Orderbook

245212 202 202 201 209 205 200 185

-

50

100

150

200

250US$ million

Minimum 26-Month Construction Time

New

build

Pric

esSt

ruct

ural

Ava

ilabi

lity

Spot

& T

erm

Rat

es

Uncommitted NB Deliveries

1 3 1 1 2 1 -

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q42008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Earliest Delivery

Only 9 uncommitted Newbuilds

on the Orderbook

Shipping market starts

to tighten

183

NB Prices lowest since

2008

Trend

Trend

Trend

DISCLAIMERThe information contained within this report is given in good faith based on the current market situation at the time of preparing this report and as such is specific to that point only. While all reasonable care has been taken in the preparation and collation of information in this report Affinity (Shipping) LLP (and all associated and affiliated companies) does not accept any liability whatsoever for any errors of fact or opinion based on such facts.Some industry information relating to the shipping industry can be difficult to find or establish. Some data may not be available and may need to be estimated or assessed and where such data may be limited or unavailable subjective assessment may have to be used.No market analysis can guarantee accuracy. The usual fundamentals may not always govern the markets, for example psychology, market cycles and external events (such as acts of god or developments in future technologies) could cause markets to depart from their natural/usual course. Such

external events have not been considered as part of this analysis. Historical market behaviour does not predict future market behaviour and shipping is an inherently high risk business. You should therefore consider a variety of information and potential outcomes when making decisions based on the information contained in this report.All information provided by Affinity (Shipping) LLP is without any guarantee whatsoever. Affinity (Shipping) LLP or any of its subsidiaries or affiliates will not be liable for any consequences thereof.This report is intended solely for the information of the email recipient account and must not be passed or divulged to any third parties whatsoever without the written permission of Affinity (Shipping) LLP. Affinity (Shipping) LLP accepts no liability to any third parties whatsoever. If permission is granted, you must disclose the full report including all disclaimers, and not selected excerpts which may be taken out of context.

© 2017 Affinity Research LLPAffinity Research London

T. +44 20 3142 0100E. [email protected]

20/10/2017

Challenges and Opportunities in the Tanker Markets

39

AFFINITY GLOBAL OFFICES

40

LONDON

H

SYM

P

Dry Cargo

Tankers LNG

Sale & Purchase

Newbuilding

Research

SEOUL

Sale & Purchase Newbuilding

S INGAPORE

Dry Cargo Sale & Purchase

SYDNEY, MELBOURNE & PERTH

Dry Cargo

HOUSTON

Tankers

SI

BEIJ ING

Tankers Dry Cargo

LNG

Finance Valuations

Tankers

LB

SE

SANTIAGO

Dry Cargo

Tankers

SA

H

20/10/2017

Challenges and Opportunities in the Tanker Markets