26

Challenges in maintaining the momentum of a successful launch Steve Challouma Category Director 19 th October 2011

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | abraham-harrison |

| View: | 215 times |

| Download: | 0 times |

Challenges in maintaining the momentum of a successful launch

Steve Challouma Category Director

19th October 2011

18 April 2023 2

We love our Fish!

• One of the healthiest foods known to man

• In home consumption of Fish and Chips now almost twice as big as takeaway

• For ¾ of us our first taste of Fish is a Fish Finger

• 3.1bn Fish occasion’s a year – half are frozen

• 20 Birds Eye Fish Fingers are eaten every second in the UK

18 April 2023 3

Opportunity: Whilst the biggest brand, the business was dominated by ‘Prepared’ Fish

Famous Kids & Family businesses

£144m

But no foothold in Natural Fish sector

Coated Fish FingersSeafood NakedOthers

£85m sector (pre BTP launch)

Source: Nielsen 52w/e Jan 09

BE = #1 Fish Brand in Frozen

Leading Brand in Frozen & Fish

18 April 2023 4Source: Bluecube Research – Mar 2008

…I lack the skills & know-how

Problem: Consumers have deep-rooted barriers to preparing natural fish

…I don’t know how to use it

…I worry about the quality and freshness

…it’s messy and smelly

I love the idea of eating more fish, but….

...I find the thought of preparing it scary

…it’s not that convenient

18 April 2023 5

The Finest Fish Fillets…….

...topped with herb infused piped butter…

…individually sealed in a Bake PerfectR Foil Bag to

lock in Flavour

Launched in a range of 5 species & flavours

Salmon Haddock King Prawns Pollock Basa

Solution: Perfectly Cooked Fish with No Fuss

18 April 2023 7

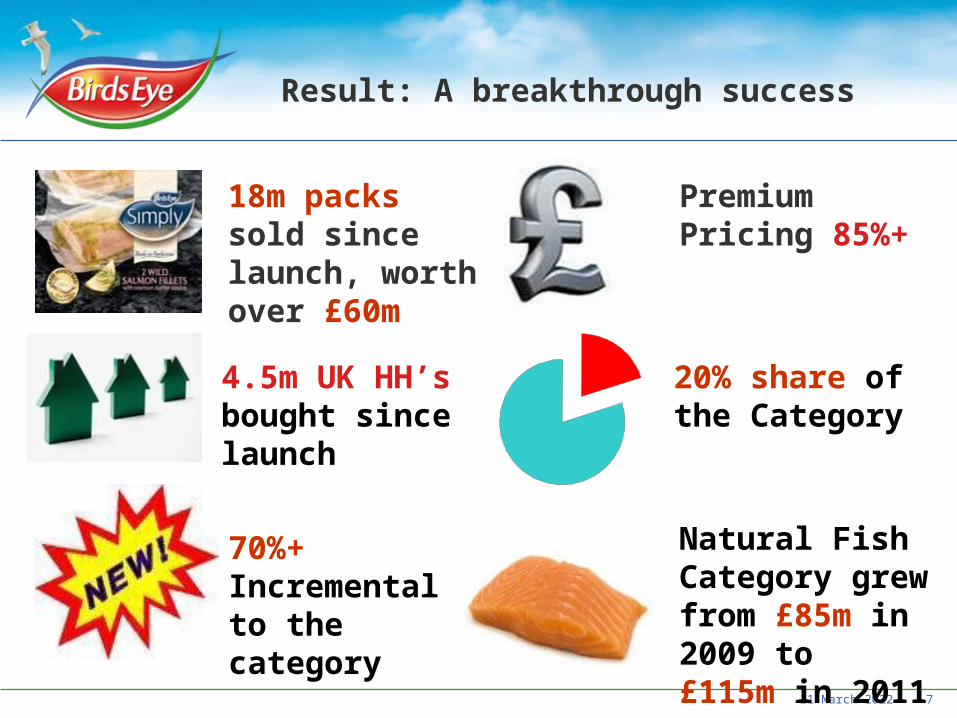

Result: A breakthrough success

18m packs sold since launch, worth over £60m

4.5m UK HH’s bought since launch

Premium Pricing 85%+

20% share of the Category

Natural Fish Category grew from £85m in 2009 to£115m in 2011

70%+ Incremental to the category

18 April 2023 8

63 61

40

2825

7 5

1st yr

RS

V £

mMaking it one of the biggest grocery launches

within the last 15 years

18 April 2023 9

However, whilst the franchise has continued to grow….

0

200

400

600

800

1,000

1,200

Un

its (

000's

)

0

2

4

6

8

10

12

14

16

18

Unit Sales Monthly pen%

Cumulative Pen%

TV Support

Source: Nielsen Scantrack + Kantar 4we to 14.05.11, Total Market

18 April 2023 10

…after 18 months the rate of new consumers coming in slowed, leading to a penetration plateau

0

200

400

600

800

1,000

1,200

4wks

to W

E 21.

03.0

9

4wks

to W

E 16.

05.0

9

4wks

to W

E 11.

07.0

9

4wks

to W

E 05.

09.0

9

4wks

to W

E 31.

10.0

9

4wks

to W

E 26.

12.0

9

4wks

to W

E 20.

02.1

0

4wks

to W

E 17.

04.1

0

4wks

to W

E 12.

06.1

0

4wks

to W

E 07.

08.1

0

4wks

to W

E 02.

10.1

0

4wks

to W

E 27.

11.1

0

4wks

to W

E 22.

01.1

1

4wks

to W

E19.0

3.11

4wks

to W

E 14.

05.11

4wks

to W

E 09.

07.11

Un

its

(000

's)

0

2

4

6

8

10

12

14

16

18

Unit Sales

Monthly pen%

52WK Rolling Penetration

Cumulative Pen%

TVSupport

Source: Nielsen Scantrack + Kantar 4we to 14.05.11, Total Market

18 April 2023 112009 2010 2011

Young’s Fishmongers Choice x2

Sep 2010

Iceland’s Fish in Foil Tray

Jan 2010

Asda Cook in The Bag x5

April 2010

BTP Salmon, Pollock Haddock, Chilli & Basa

March 2009

Young’s Its in the Bag x4 Skus

October 2009

Findus Fresher Taste Launch (2 Poultry/2

Fish)

Oct 2010

With a raft of new competitive launchesThe sincerest form of flattery…

Tesco Simply Bake X 4Apr 2011

JS Bake in the Bag X 3Mar 2011

18 April 2023 12

Keeping your nerve in the face of competitor launches…..

• Not compromising on your value proposition - protect, sustain and build the integrity of your launch

• Understand comparative quality differences and protect what’s distinctive – attention to detail is key

• Customer specific tracking and planning to understand the impact on your sales

• Behave like a confident brand should and demonstrate thought leadership – ensure you have a pipeline of news lined up which keeps up momentum and interest

• Continue to back it and prioritise in the business

18 April 2023 13

Execution is everything - not every distribution point is equal

Distribution Range Space Visibility Overall

Retailer A Room to increase core Strong range 1 facing Mixed Focus on

merch

Retailer B Core skus in full dist

Opps for non-core 2 facings Central at Eye

levelFocus on

range gaps

Retailer C Core skus in high dist

Opps for non-core

2 facings on biggest plan

Central at Eye level

Focus on range gaps

Retailer D Risk to range Risk to range - -Secure &

build range

Retailer ESalmon increase needed

Plans to list Haddock - -

Secure Haddock

listing

Keeping very focused on retailer level execution on the range – just because the product is listed it doesn’t mean there isn’t further room to optimise

18 April 2023 14

Adopters: 0.9m Trialists: 2.7m

Only 25% of trialled have built

it into their repertoire – buying seven times since

launch

But need to go beyond the data to understand they why as well as the what…

Getting quick feedback on how the proposition is being adopted

Total UK Population: 25.5m h/h

Aware: 13m Unaware: 12.5m

Trialled: 3.6m Not trialled: 9.4m

Still a huge remaining

penetration opportunity – only

20% of Category Buyers

18 April 2023 15

Understanding the drivers of consumer valuewhat is working and not working

Identify the shopping and consumption

levers for BTP

Identify the shopping and consumption

levers for BTP

Get a full understanding of both the consumer and the

shopper truths

RegularLight

LapsedConsiderers

Who are they? Demographics and segmentsWhat do they eat/buy? Frozen naked fish? Chilled fish?What do they during they free time? MediaWhat do they believe? Attitude to fish and frozen, etcWhat are their needs? How do they shop for BTP? Planned purchase? Deals? Back up or for a meal this week?

Identifying triggers & barriers

Unlocking BTP potential

and unmet needs

What do they like about BTP and why? What they do not like about BTP and why? How does the product deliver against their expectations? Taste? Filling? Convenience? Etc.What motivates to buy BTP in store? Deals? Awareness of recipes EtcWhat prevent them from buying it? Visibility? Availability? Price?

When do they use BTP? Meal occasion: who, type of meal, What resonates the most? Benefits, needs, comms messagesWhat can make BTP worth paying more for? Species? recipes?

18 April 2023 16

Key Learnings from Engaging with Consumers

We interviewed 1,522 consumers – regular, light & lapsed buyers

Source: U&A research; 1,522 interviews: May ‘11

Consumers don’t know when to eat

BTP & what to eat it with

=+Consumers feel there is a lack of

variety & excitement in the

range

Consumers don’t see BTP as ‘special’

& worth paying more for – see it as

a standby

Need to help consumers…provide them with the inspiration & ideas…to get BTP into their ‘cooking repertoire’

18 April 2023 17

Being prepared to alter the course…

INTENDED STRATEGY REALIZED STRATEGY

DELIBERATE STRATEGY

Source: Mintzberg and Waters (1985)

18 April 2023 18

Being prepared to alter the course…

INTENDED STRATEGY REALIZED STRATEGY

DELIBERATE STRATEGY

UNREALIZED STRATEGY EMERGENT STRATEGY

Source: Mintzberg and Waters (1985)

Direct to realize intentions while at the same time respond to an unfolding pattern of action

18 April 2023 19

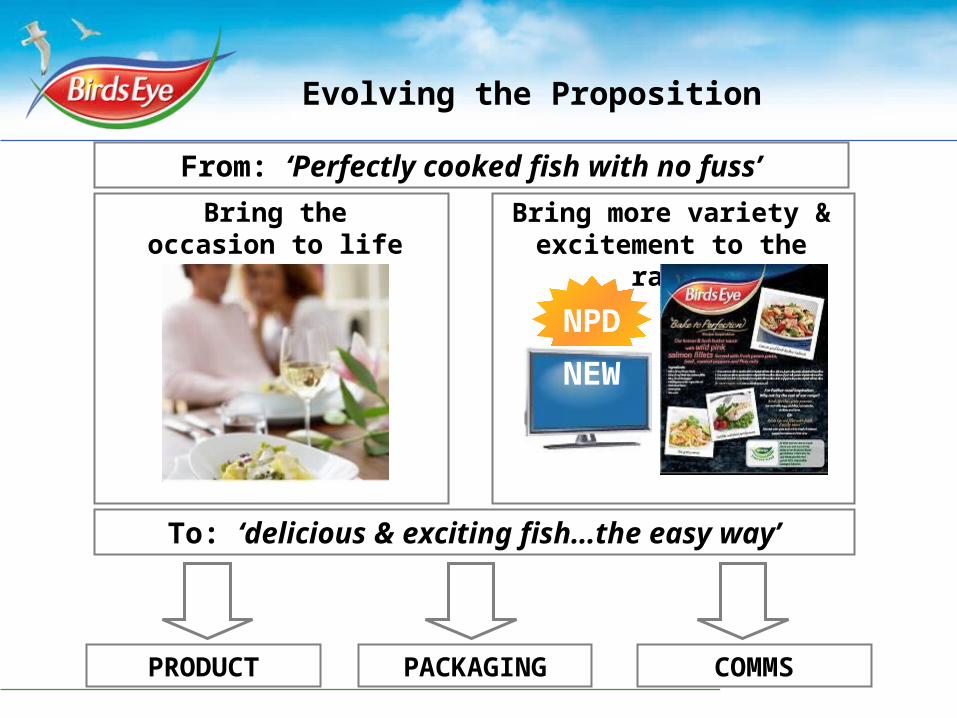

Bring the occasion to life

To: ‘delicious & exciting fish…the easy way’

PRODUCT COMMSPACKAGING

Bring more variety & excitement to the

range

NPD

NEW

From: ‘Perfectly cooked fish with no fuss’

Evolving the Proposition

18 April 2023 20

NPD Solution: Taste Inspiration Recipes

Olive Oil, Rosemary & Tomato

White Wine, Wholegrain

Mustard & Spring Onion

18 April 2023 21

Ongoing plan: Using NPD and refreshment to drive interest and uplift across the range

18 April 2023 23

Summary: Evolution of the Proposition

Drive Expansion

• Objective: Drive excitement & expand recipe offerings

• Strategy: Occasion led advertising, new & inspiring flavour combinations

• Plan: New ‘taste inspiration’ recipes and occasion-based advertising

• Objective: Easy to understand concept, recipes for everybody

• Strategy: Effective product led advertising, traditional recipes / flavours

• Plan: Functional ad explaining BTP technology on “butter & herb” fish & prawn range

• Objective: Build the franchise, expand the shopper base

• Strategy: New product benefits, recipes based on consumer needs

• Plan: Next generation concepts that drive the platform further

Embed InspirationLaunch Concept

18 April 2023 24

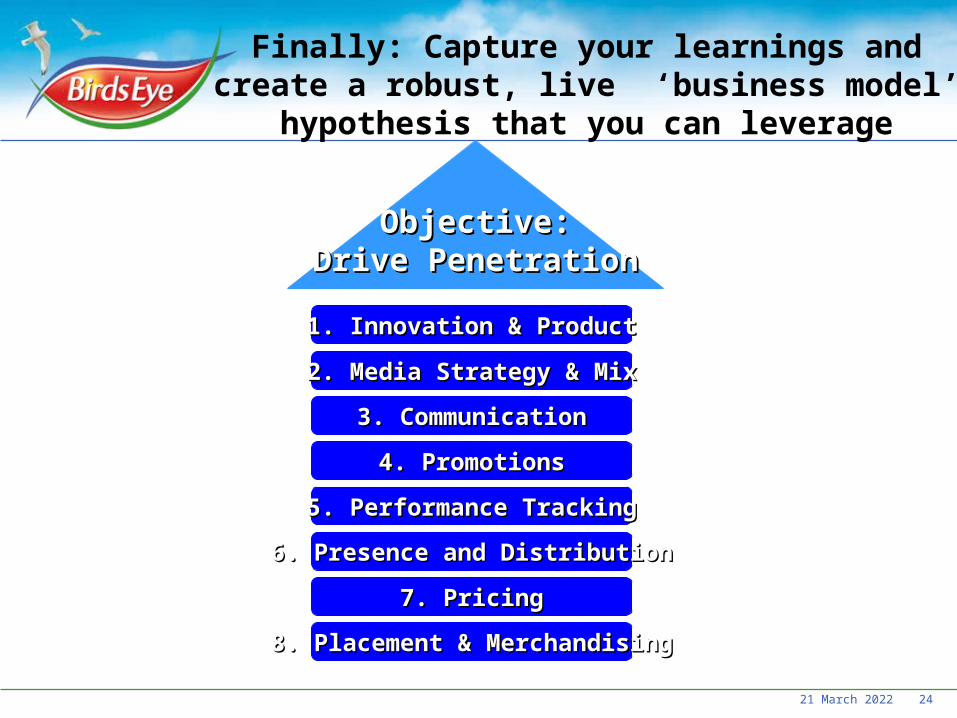

Finally: Capture your learnings and create a robust, live ‘business model’ hypothesis that you can leverage

1. Innovation & Product1. Innovation & Product

6. Presence and Distribution6. Presence and Distribution

7. Pricing7. Pricing

2. Media Strategy & Mix2. Media Strategy & Mix

8. Placement & Merchandising8. Placement & Merchandising

4. Promotions4. Promotions

3. Communication3. Communication

Objective:Objective:Drive PenetrationDrive Penetration

5. Performance Tracking5. Performance Tracking

18 April 2023 25

Providing a ‘Blueprint’ for rolling into new territories

18 April 2023 26

Summary

• Expect success to be copied - but don’t let it un-nerve you or compromise your standards

• Keep razor sharp focus on in-store execution

• Get quick feedback to understand what’s working and not

• Be prepared to evolve the proposition to get to next step change of growth

• Capture and leverage your experience