42

Changes in Securities Trading Since 2000 James J. Angel, Ph.D., CFA Georgetown University

Changes in Securities Trading Since 2000

James J. Angel, Ph.D., CFA Georgetown University

About me At Georgetown since 1991

Former Visiting Academic Fellow NASD 1999-2000

Former Chair, Nasdaq Economic Advisory Board

Visiting Economist Shanghai Stock Exchange 2004

Member, Board of Directors of Direct Edge Stock Exchange since 2010 All comments are mine and not necessarily those of Direct Edge.

Warned US SEC 5 times in writing prior to the Flash Crash that US markets were vulnerable to such events.

Work experience PGandE, BARRA (later part of Morgan Stanley)

Education B.S. Caltech, MBA Harvard, Ph.D. Berkeley

Summary Economics of markets Equity exchanges solve the “prisoners dilemma” of trading Derivative markets guarantee settlement The Network IS the market!

Technology and regulation drive changes Network economics collapses when networks combine Toward a competitive market structure or regulated utility?

US & Europe Open architecture market networks Rise of dark pools

Rise of HFT

Consolidation of exchanges Scale economies in exchange IT

Markets are better, but different Need to understand differences and vulnerabilities

Exchange economics

Why do we have stock exchanges at all? Most goods and services trade quite nicely without a formal

regulated institution. We don’t send orders to The Paperclip Exchange.

Even most financial products trade without an exchange. FX, Debt, OTC derivatives

So why bother with an exchange?

Answer: Information! Information about trading interest is more valuable in equities.

“Prisoner’s dilemma”: Everyone wants to know what everyone else is doing. No one wants to give up their own information.

Everyone better off with some information sharing.

Exchanges force this sharing. Derivative exchanges guarantee settlement.

Network Economics The utility of some products increases when more people use

them.

Telephones, fax machines, computer operating systems

When two incompatible networks compete

The bigger network wins!

Technology format wars

Winner takes all.

Traditional view Exchanges were natural monopolies

Needed to be regulated like old fashioned electric utilities

Non-profit ownership by members also takes care of this.

Role of regulator was to tame the monopoly to achieve competitive results

Just as in telecom, the role of the regulator is to force interconnection between networks that do not want to cooperate.

US: Regulation NMS

Europe: MiFID

Technology changes Better computers

Better communication

New trading systems for exchanges

New ways to trade

New products

New trading technology for traders

New corporate forms of organization

Different regulatory philosophies

Globalization, deregulation, and reregulation

Algorithmic trading has reduced information content Order flow not as informative as it once was.

Many algo traders prefer to split orders across competing limit order books.

No longer a “gravitational pull” that brings everything to one book

Indeed, there is an “electric repulsion” that will drive a permanent fragmentation.

Less dominance for any one node in the network.

OPPORTUNITY FOR ENTRANTS!

Demutualization Transformation from member owned non-profits to

shareholder driven listed companies.

More flexible and efficient exchanges

BUT:

Regulators promote competition to prevent monopolistic abuses.

Government is now the solver of the Prisoner’s Dilemma Rules set by governments for entire network, not by trading

platform companies.

Self regulation is fading away.

Results: Competitive landscape Faster, cheaper markets

.

Merger incentives

Platforms are scalable

Big savings in IT from rationalization of global exchange industry.

Bad news for existing exchanges Easy entry has turned equity trading into a cutthroat commodity

business NYSE Market Share (Feb 2012):

NYSE 20.7% NYSE-ARCA 9.3 NASDAQ 16.7 BATS 9.4 DIRECTEDGE 9.2 Dealers and Darks 34.7

NASDAQ Market Share NASDAQ 29.5% NYSE-ARCA 11.4 BATS 11.7 DIRECTEDGE 10.4 Dealers and Darks 37.0

Source: Barclays

Source: Chi-X

Shifting liquidity from the market of listing in Europe as well

Royal Dutch Shell A, 18th May 2010

Chi-X42.4%

NASDAQ OMX2.9%

Turquoise6.4%

BATS12.1%

LSE36.3%

Royal Dutch Shell B, 6th May 2010

Chi-X46.7%

NASDAQ OMX3.5%Turquoise

6.8%

BATS8.9%

LSE33.2%

NYSE ARCA1.0%

Figures for entire day up to 4.30 pm (closing auction not included)

G4S, 12th May 2010

Chi-X43.1%

NYSE ARCA0.9%

NASDAQ OMX1.3%

Turquoise4.0%

BATS11.0%

LSE39.6%

Lower barriers to entry in equities

There will always be room for another platform at the margin, keeping prices perpetually low.

To enter, need:

Faster trading platform

Cheap prices

Good relations/connections with liquidity providers on Day One.

Sustainable competitive advantage

Low cost producer

Technical leader

Niche players

Self cannibalization Exchanges launch new platforms

Different trading rules

Nasdaq relaunched PHLX with size as a secondary priority rule

NYSE and Nasdaq each have three stock exchanges

BATS and DE both have two exchanges

Different pricing models appeal to different market segments

Maker taker pricing versus taker maker pricing

Exchange pricing Rise of “maker taker” pricing

Exchanges pay rebates to limit orders that provide liquidity

Charge full fees to market orders that take liquidity

Provides incentives to post liquidity

Rise of “taker maker” pricing

Pay rebates to market orders that take liquidity

Charge full fees to limit orders that post liquidity

Attractive to traders who want to be first in line for execution.

“Dark” pools fill a need Traders still face traditional problem: Need to reveal some information to find counterparty.

But revealing too much information will result in poor execution.

Trading decisions Size: How much of a large order should be executed at a time?

Aggressiveness How aggressive should the trader be?

Display How much of the trading desire (if any) should be displayed, and to whom?

Displaying only to serious traders reduces information leakage and may result in better execution.

THESE ARE NOT SOLVED PROBLEMS

No “one size fits all” market structure solution.

Dark pool flavors Block trading systems

ITG Posit

Liquidnet

Pipeline

Broker internalization engines

Permits large orders to execute against broker flow

Mostly a way around exchange fee structures

Great if flow uninformed.

Bad if not

Smart traders will sense the lurking order and front run it.

The Rise of High Frequency Trading (HFT)

Computerized trading Most HFT trading follows traditional strategies

Market making

Provides liquidity and lowers trading costs

Arbitrage

Keeps prices in proper alignment

News reaction

Incorporates information in price

Pattern recognition

Try to figure out where market is going

Manipulation

Trigger other people to trade at a loss.

Bluffing, spoofing, order ignition.

The need for speed These strategies are not new.

There has always been a race for speed.

In a race, the second place finisher loses Even if only by a nano-second.

Result: race for speed. Co-location in data centers to avoid signal delays

This is not new!

Traders have traditionally paid up for closer access to trading. Exchange memberships

Offices close to exchange

Even if colo were banned, traders would pay up to place servers next to exchange data center.

Changes in US market quality

US Executions Are Faster

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Sep-

01

Jan-

02

May

-02

Sep-

02

Jan-

03

May

-03

Sep-

03

Jan-

04

May

-04

Sep-

04

Jan-

05

May

-05

Sep-

05

Jan-

06

May

-06

Sep-

06

Jan-

07

May

-07

Sep-

07

Jan-

08

May

-08

Sep-

08

Jan-

09

May

-09

Sep-

09

Market Order Execution Speed

NYSE-listed Nasdaq-listed

Volumes Increased

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Daily U.S. Equity Share Volume

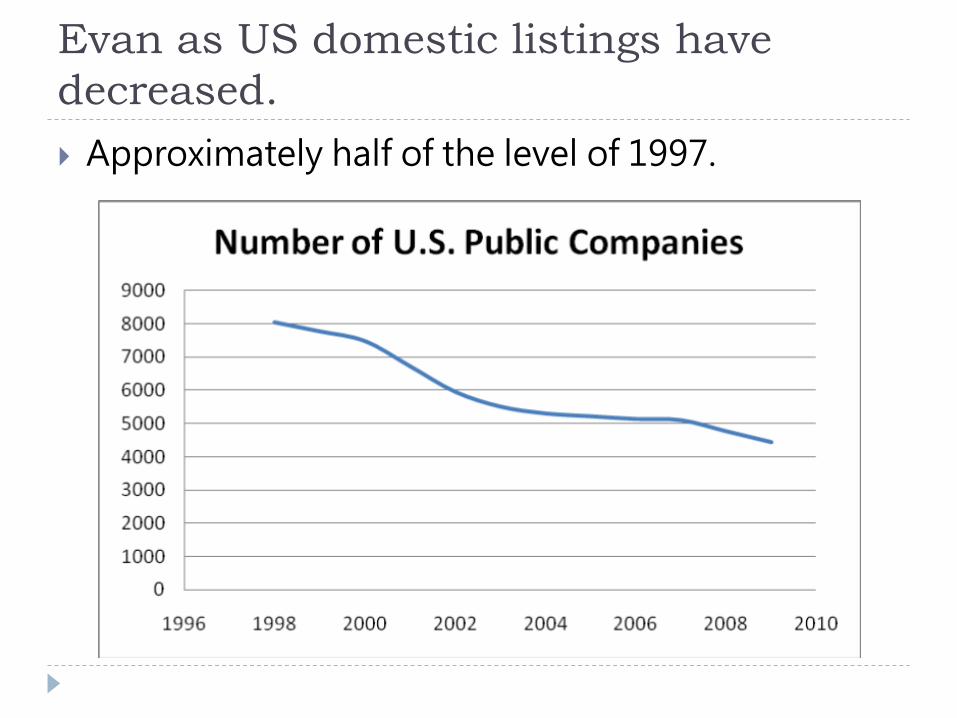

Evan as US domestic listings have decreased. Approximately half of the level of 1997.

Spreads Decreased

-

0.0050

0.0100

0.0150

0.0200

0.0250

0.0300

5/1/

2003

8/1/

2003

11/1

/200

3

2/1/

2004

5/1/

2004

8/1/

2004

11/1

/200

4

2/1/

2005

5/1/

2005

8/1/

2005

11/1

/200

5

2/1/

2006

5/1/

2006

8/1/

2006

11/1

/200

6

2/1/

2007

5/1/

2007

8/1/

2007

11/1

/200

7

2/1/

2008

5/1/

2008

8/1/

2008

11/1

/200

8

2/1/

2009

5/1/

2009

8/1/

2009

11/1

/200

9

$

Median S&P 500 Bid-Ask Spreads

Quotation Sizes Increased

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

11/1

/200

3

2/1/

2004

5/1/

2004

8/1/

2004

11/1

/200

4

2/1/

2005

5/1/

2005

8/1/

2005

11/1

/200

5

2/1/

2006

5/1/

2006

8/1/

2006

11/1

/200

6

2/1/

2007

5/1/

2007

8/1/

2007

11/1

/200

7

2/1/

2008

5/1/

2008

8/1/

2008

11/1

/200

8

2/1/

2009

5/1/

2009

8/1/

2009

11/1

/200

9

Ave

rag

e D

epth

(Bid

+ O

ffer

)

Average Displayed Depth at NBBO

S&P 500 NBBO

Russell 2000 NBBO

All Stocks NBBO

29

Listings are competitive NYSE vs Nasdaq The Official Switch Scoreboard – A Changing Tide Issuer Advisory Group LLC

0

10

20

30

40

50

60

70

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

01020

3040

5060

7080

90

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Number of Companies

Market Cap of Companies ($ in Billions)

NYSE in Blue / Nasdaq in Red IAG Note: To ensure comparability between periods, only companies with greater than $100 million in market cap have been included (eliminates AMEX confusion). Totals also include only the domestic market cap of Vodafone (global mc = $132B).

But there are complaints … Buy side complains Trading more complicated Losing control of executions

Don’t know where order is executed Harder to control information leakage

Phantom liquidity Excessive(?) cancellations

“Predatory” algos Increase market impact

Sell side complains Costly to connect to multiple destinations

Retail suspects new world order is stacked against them Is co-location unfair?

30

Crashes Happen

31

32

Things can go wrong

No human system is perfect. Anything which can go wrong will go wrong.

“Fat fingers” mistakes in trading Computer malfunctions

Misfiring algos Positive feedback loops Hardware failures OS failures

Intentional sabotage Hackers, disgruntled employees, cyber-war, terrorists

System overloads Even though individual entities had filters for “fat fingers” US equity markets had no automated safeguards before the Flash Crash.

It has happened before computers There are numerous accounts in financial history

of market gyrations. Jitters over financial conditions Stocks drop rapidly. Confusion in market over price

Latency and data integrity issues are not new! Ticker tape running late

33

Many times… May 2, 1906

34

NY Times. August 8,

1919

35

36

More historical parallels

Market mechanisms broke down at previous times of high stress October 1929 May 29, 1962

Ticker ran 2 hours 29 minutes after market closed. IBM fell 5.3% in 19 minutes

October 19, 1987 “Large scale breakdowns in automated trading systems”

http://www.sec.gov/news/studies/tradrep.htm

Printers jammed on NYSE floor Phones unanswered at brokers

Dendreon: April 28, 2009

37

38

What happened on “Tornado The The “Flash Crash”

Not one but three ****storms

Three major problems on May 6 Tornado in S&P futures

Large sell order in E-minis? Index quickly recovered from downdraft. Arbitrage activity spilled into cash market for S&P500

Flood of market data overwhelmed participants Market centers became disconnected Data integrity issues pushed liquidity providers off line

Erroneous trades in non S&P stocks Arca-listed ETFs bore brunt of damage ACN at a penny

39

40

Chronology of May 6, 2010

Market already jittery because of concerns over Greece. Down day with very heavy volume Reports of data problems in various places 2:00- 2:30 Over 200 NYSE stocks hit LRPs

NYSE slow motion mode

2:30 – 3:00 E-mini volume 10x ADV 2:32 “Large trader” starts to sell 75,000 E-mini contracts 2:37 NASDAQ invokes “self help” against NYSE Arca

BATS, NSE, and BSE also invoke self-help Apparently ARCA was not responding quickly enough to other exchanges.

Fault of ARCA or data linkages between exchanges?

2:40 PM decline accelerates 2:45:28 CME halts E-mini for 5 seconds

Stop logic functionality

Spread widens dramatically as depth drops on E-mini 78,412 E-mini contracts trade during that minute!

2:45- 2:55 Armageddon and rebound 2:47 Accenture trades at 1 cent on CBOE

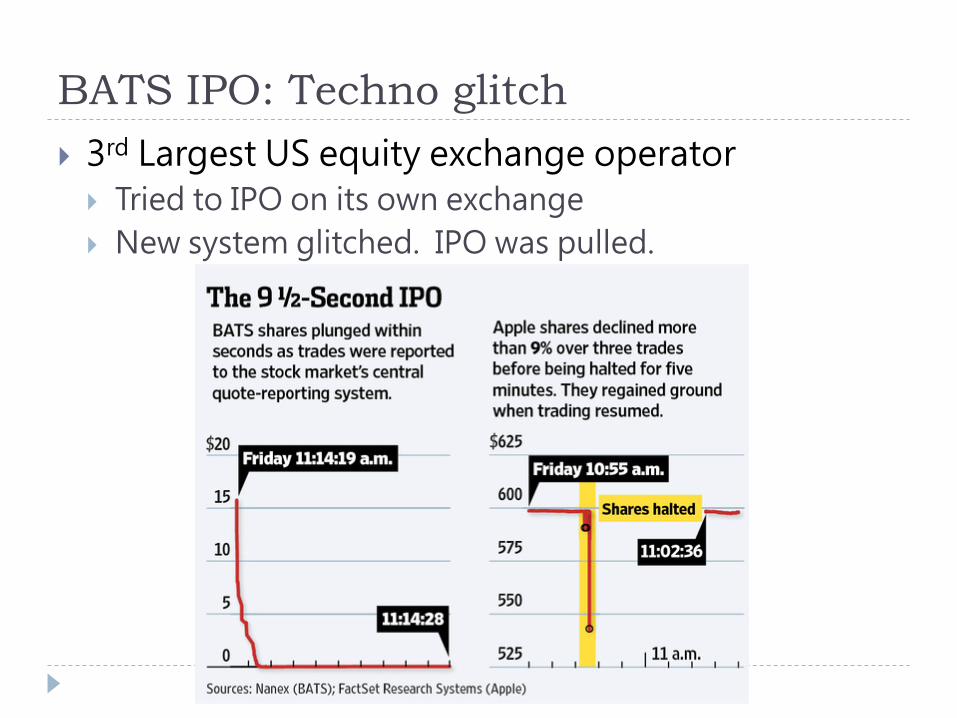

BATS IPO: Techno glitch 3rd Largest US equity exchange operator Tried to IPO on its own exchange New system glitched. IPO was pulled.

Summary Technology has changed. Electronic trading and private ownership From natural monopolies to competitive networks

Our markets are mostly better We need to be prepared for glitches

42