INTRODUCTION : INSURANCE INDUSTRY INDUSTRY PROFILE A thriving insurance sector is of vital importance to every modern economy. Firstly because it encourages the habit of saving, secondly because it provides a safety net to rural and urban enterprises and productive individuals. And perhaps most importantly it generates long- term invisible funds for infrastructure building. The nature of the insurance business is such that the cash inflow of insurance companies is constant while the payout is deferred and contingency related. This characteristic feature of their business makes insurance companies the biggest investors in long-gestation infrastructure development projects in all developed and aspiring nations. This is the most compelling reason why private sector (and foreign) companies, which will spread the insurance habit in the societal and consumer interest are urgently required in this vital sector of the economy. Opening up of insurance to private sector including foreign participation has resulted into various opportunities and challenges in India. 1.1 LIFE INSURANCE MARKET The Life Insurance market in India is an underdeveloped market that was only tapped by the state owned LIC till the entry of private insurers. The penetration of life insurance products was 1

Transcript

INTRODUCTION : INSURANCE INDUSTRY

INDUSTRY PROFILE

A thriving insurance sector is of vital importance to every modern economy. Firstly because it

encourages the habit of saving, secondly because it provides a safety net to rural and urban

enterprises and productive individuals. And perhaps most importantly it generates long- term

invisible funds for infrastructure building. The nature of the insurance business is such that the

cash inflow of insurance companies is constant while the payout is deferred and contingency

related.

This characteristic feature of their business makes insurance companies the biggest investors in

long-gestation infrastructure development projects in all developed and aspiring nations. This is

the most compelling reason why private sector (and foreign) companies, which will spread the

insurance habit in the societal and consumer interest are urgently required in this vital sector of

the economy. Opening up of insurance to private sector including foreign participation has

resulted into various opportunities and challenges in India.

1.1 LIFE INSURANCE MARKET

The Life Insurance market in India is an underdeveloped market that was only tapped by the

state owned LIC till the entry of private insurers. The penetration of life insurance products was

19 percent of the total 400 million of the insurable population. The state owned LIC sold

insurance as a tax instrument, not as a product giving protection. Most customers were under-

insured with no flexibility or transparency in the products. With the entry of the private insurers

the rules of the game have changed.

The 12 private insurers in the life insurance market have already grabbed nearly 9 percent of the

market in terms of premium income. The new business premium of the 12 private players has

tripled to Rs 1000 crore in 2002- 03 over last year. Meanwhile, with regard to state owned LIC's

new premium business has fallen

1

Innovative products, smart marketing and aggressive distribution. That's the triple whammy

combination that has enabled fledgling private insurance companies to sign up Indian customers

faster than anyone ever expected. Indians, who have always seen life insurance as a tax saving

device, are now suddenly turning to the private sector and snapping up the new innovative

products on offer.

The growing popularity of the private insurers is evidenced in other ways. They are coining

money in new niches that they have introduced. The state owned companies still dominate

segments like endowments and money back policies. But in the annuity or pension products

business, the private insurers have already wrested over 33 percent of the market. And in the

popular unit-linked insurance schemes they have a virtual monopoly, with over 90 percent of the

customers. The private insurers also seem to be scoring big in other ways- they are persuading

people to take out bigger policies. For instance, the average size of a life insurance policy before

privatization was around Rs 50,000. That has risen to about Rs 80,000. But the private insurers

are ahead in this game and the average size of their policies is around Rs 1.1 lack to Rs 1.2 lack-

way bigger than the industry average.

Buoyed by their quicker than expected success, nearly all private insurers are fast- forwarding

the second phase of their expansion plans. No doubt the aggressive stance of private insurers is

already paying rich dividends. But a rejuvenated LIC is also trying to fight back to woo new

customers.

1.2 INSURANCE TODAY

In 1993, Malhotra Committee, headed by former Finance Secretary and RBI Governor R. N.

Malhotra, was formed to evaluate the Indian insurance industry and recommend its future

direction. The Malhotra committee was set up with the objective of complementing the reforms

initiated in the financial sector.

With the setup of Insurance Regulatory Development Authority (IRDA) the reforms started in

the Insurance sector. It has became necessary as if we compare our Insurance penetration and per

capita premium we are much behind then the rest of the world. The table above gives the

statistics for the year 2000.

2

With the expected increase in per capita income to 6% for the next 10 year and with the

improvement in the awareness levels the demand for insurance is expected to grow. As per an

independent consultancy company, Monitor Group has estimated a growth form Rs. 218 Billion

to Rs. 1003 Billion by 2008. The estimations seems achievable as the performance of 13 life

Insurance players in India for the year 2002-2003 (up to October, based on the first year

premium) is Rs. 66.683 million being LIC the biggest contributor with Rs. 59,187 million. As of

now LIC has 2050 branches in 7 zones with strong team of 5,60,000 agents

1.3 IMPACT OF GLOBALISATION

While nationalized insurance companies have done a commendable job in extending the volume

of the business, opening up insurance sector to private players was a necessity in the context of

globalization of financial sector. If traditional infrastructural and semipublic goods industries

such as banking, airlines, telecom, power etc., have significant private sector presence,

continuing a state of monopoly in provision of insurance was indefensible and therefore, the

globalization of insurance has been done as discussed earlier. Its impact has to be seen in the

form of creating various opportunities and challenges.

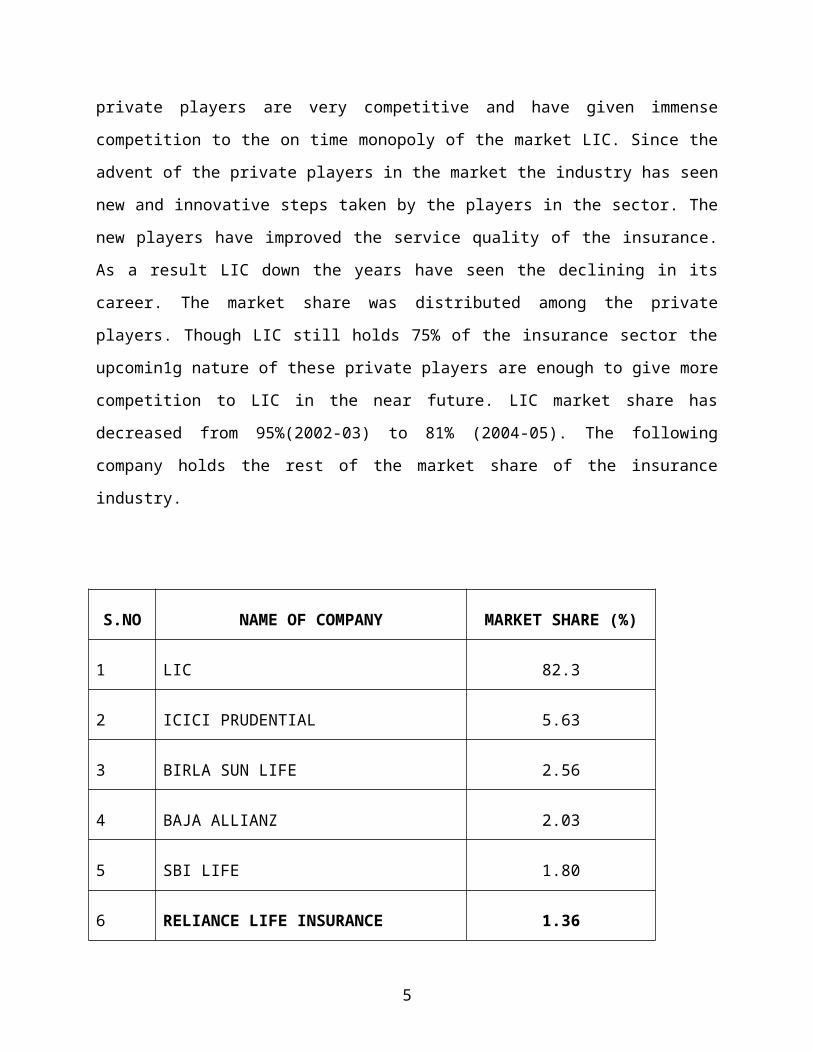

The introduction of private players in the industry has added colours to the dull industry. The

initiatives taken by the private players are very competitive and have given immense competition

to the on time monopoly of the market LIC. Since the advent of the private players in the market

the industry has seen new and innovative steps taken by the players in the sector. The new

players have improved the service quality of the insurance. As a result LIC down the years have

seen the declining in its career. The market share was distributed among the private players.

Though LIC still holds 75% of the insurance sector the upcomin1g nature of these private

players are enough to give more competition to LIC in the near future. LIC market share has

decreased from 95%(2002-03) to 81% (2004-05). The following company holds the rest of the

market share of the insurance industry.

3

S.NO NAME OF COMPANY MARKET SHARE (%)

1 LIC 82.3

2 ICICI PRUDENTIAL 5.63

3 BIRLA SUN LIFE 2.56

4 BAJA ALLIANZ 2.03

5 SBI LIFE 1.80

6 RELIANCE LIFE INSURANCE 1.36

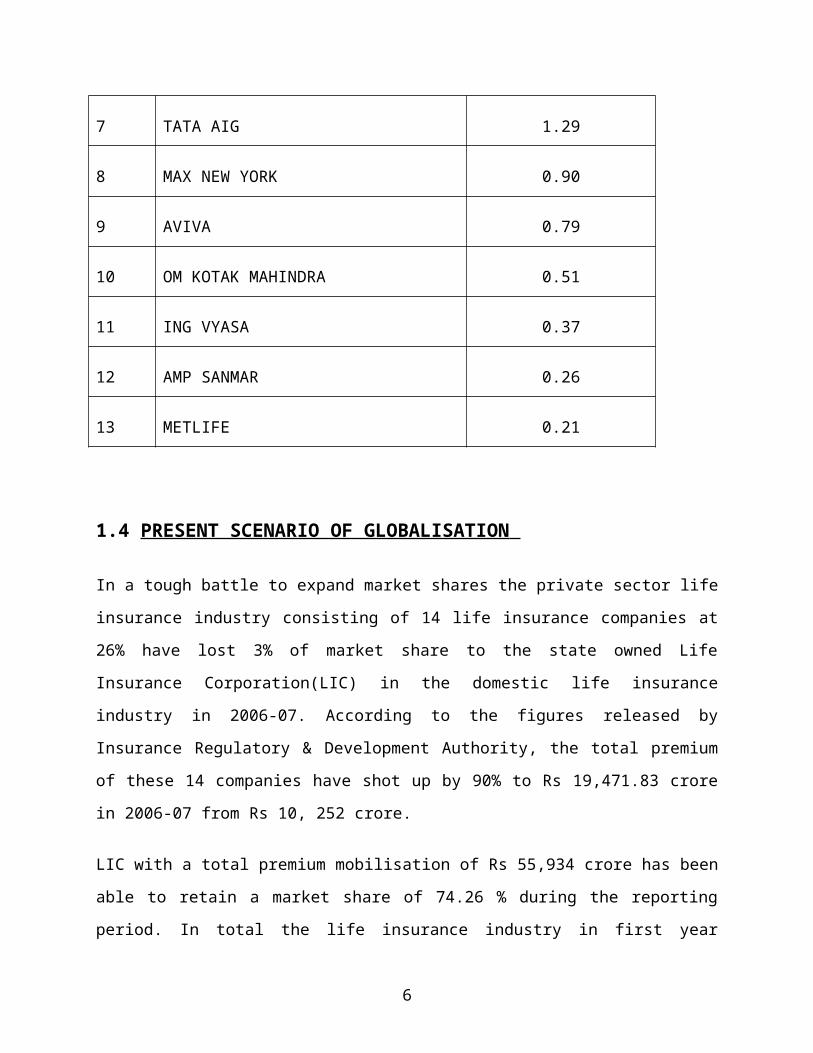

7 TATA AIG 1.29

8 MAX NEW YORK 0.90

9 AVIVA 0.79

10 OM KOTAK MAHINDRA 0.51

11 ING VYASA 0.37

12 AMP SANMAR 0.26

13 METLIFE 0.21

1.4 PRESENT SCENARIO OF GLOBALISATION

In a tough battle to expand market shares the private sector life insurance industry consisting of

14 life insurance companies at 26% have lost 3% of market share to the state owned Life

Insurance Corporation(LIC) in the domestic life insurance industry in 2006-07. According to the

4

figures released by Insurance Regulatory & Development Authority, the total premium of these

14 companies have shot up by 90% to Rs 19,471.83 crore in 2006-07 from Rs 10, 252 crore.

LIC with a total premium mobilisation of Rs 55,934 crore has been able to retain a market share

of 74.26 % during the reporting period. In total the life insurance industry in first year premium

has grown by 110% to Rs 75, 406 crore during 2006-07. The 2006-07 performance has thrown a

few surprises in the ranking among the private sector life insurance companies. New entrants like

Reliance Life and SBI Life had shown a huge growth of over 381% and 210% respectively

during the year. Reliance Life which has become one of the top five companies ended the year

with a premium of Rs 930 crore during the year.

Though ICICI Prudential Life Insurance remained as the No 1 private sector life insurance

company during the year. Bajaj Allianz overtook ICICI Prudential in terms of monthly market

share in March, for the first time ever. Bajaj's market share among private players in non-single

premium for March stood at 29.1% vs. ICICI Prudential's 23.8%. Bajaj gained 4.6 percentage

point market share among private sector players for FY07.

Among other private players, SBI Life and Reliance Life continued to do well, each gaining 4%

market share in FY07. SBI Life's growth was driven by increasing contribution from ULIP

premiums. Another notable developments of the 2006-07 performance has been the expansion of

retail markets by the life insurance comapnies. Bajaj Alliannz Life insurance has added 20 lack

policies while ICICI Prudential has expanded over 19 lack policies during the year.

With the largest number of life insurance policies in force in the world, Insurance happens to be

a mega opportunity in India. It’s a business growing at the rate of 15-20 per cent annually and

presently is of the order of Rs 450 billion. Together with banking services, it adds about 7 per

cent to the country’s GDP. Gross premium collection is nearly 2 per cent of GDP and funds

available with LIC for investments are 8 per cent of GDP.

Yet, nearly 80 per cent of Indian population is without life insurance cover while health

insurance and non-life insurance continues to be below international standards. And this part of

the population is also subject to weak social security and pension systems with hardly any old

5

age income security. This itself is an indicator that growth potential for the insurance sector is

immense.

A well-developed and evolved insurance sector is needed for economic development as it

provides long term funds for infrastructure development and at the same time strengthens the risk

taking ability. It is estimated that over the next ten years India would require investments of the

order of one trillion US dollar. The Insurance sector, to some extent, can enable investments in

infrastructure development to sustain economic growth of the country.

Insurance is a federal subject in India. There are two legislations that govern the sector- The

Insurance Act- 1938 and the IRDA Act- 1999. The insurance sector in India has become a full

circle from being an open competitive market to nationalisation and back to a liberalised market

again. Tracing the developments in the Indian insurance sector reveals the 360 degree turn

witnessed over a period of almost two centuries.

1.5 IMPORTANT MILESTONES IN THE LIFE INSURANCE BUSINESS

IN INDIA

1912: The Indian Life Assurance Companies Act enacted as the first statute to regulate the life

insurance business.`

1928: The Indian Insurance Companies Act enacted to enable the government to collect

statistical information about both life and non-life insurance businesses.

1938: Earlier legislation consolidated and amended to by the Insurance Act with the objective of

protecting the interests of the insuring public.

1956: 245 Indian and foreign insurers and provident societies taken over by the central

government and nationalised. LIC formed by an Act of Parliament- LIC Act 1956- with a capital

contribution of Rs. 5 crore from the Government of India.

6

In a tough battle to expand market shares the private sector life insurance industry consisting 14

life insurance companies at 26% have lost 3% of market share to the state owned Life Insurance

Corporation(LIC) in the domestic life insurance industry in 2006-07. According to the figures

released by Insurance Regulatory & Development Authority the total premium these 14

companies have shot up by 90% to Rs 19,471.83 crore in 2006-07 from Rs 10, 252 crore.

LIC with a total premium mobilisation of Rs 55,934 crore has been able retain a market share of

74.26 % during the reporting period. In total the life insurance industry in first year premium has

grown by 110% to Rs 75, 406 crore during 2006-07. The 2006-07 performance has thrown a few

surprises in the ranking among the private sector life insurance companies. New entrants like

Reliance Life and SBI Life had shown a huge growth of over 381% and 210% respectively

during the year. Reliance Life which has become one of the top five companies ended the year

with a premium of Rs 930 crore during the year.

Though ICICI Prudential Life Insurance remained as the No 1 private sector life insurance

company during the year Bajaj Allianz overtook ICICI Prudential in terms of monthly market

share in March, for the first time ever. Bajaj's market share among private players in non-single

premium for March stood at 29.1% vs. ICICI Prudential's 23.8%. Bajaj gained 4.6 percentage

point market share among private sector players for FY07.. Among other private players, SBI

Life and Reliance Life continued to do well, each gaining 4% market share in FY07. SBI Life's

growth was driven by increasing contribution from ULIP premiums. Another notable

development of the 2006-07 performance has been the expansion of retail markets by the life

insurance companies. Bajaj Alliannz Life insurance has added 20 lack policies while ICICI

Prudential has expanded over 19 lack policies during the year.

7

1.6. INSURANCE REGULATORY AND DEVELOPMENT

AUTHORITY

M I S S I O N

To protect the interests of the policyholders, to regulate, promote and ensure orderly growth of

the insurance industry and for matters connected therewith or incidental thereto.

About IRDA

Composition of Authority under IRDA Act, 1999

As per the section 4 of IRDA Act' 1999, Insurance Regulatory and Development Authority

8

(IRDA, which was constituted by an act of parliament)

specify the composition of Authority

The Authority is a ten member team consisting of

(a) a Chairman;

(b) five whole-time members;

(c) four part-time members,

(all appointed by the Government of India)

Duties, Powers and Functions of IRDA

Section 14 of IRDA Act, 1999 lays down the duties, powers and functions of IRDA..

Subject to the provisions of this Act and the time being in force, the Authority shall have

the duty to regulate, promote and ensure orderly growth of the insurance business and re-

insurance business.

Without prejudice to the generality of the provisions contained in sub-section.

Issue to the applicant a certificate of registration, renew, modify, withdraw, suspend or

cancel such registration;

Specifying requisite qualifications, code of conduct and practical training for intermediary

or insurance intermediaries and agents;

Specifying the code of conduct for surveyors and loss assessors; Promoting efficiency in

the conduct of insurance business;

Promoting and regulating professional organisations connected with the insurance and

re-insurance business;

Levying fees and other charges for carrying out the purposes of this Act; calling for

information from, undertaking inspection of, conducting enquiries and investigations

including audit of the insurers, intermediaries, insurance intermediaries and other

9

organisations connected with the insurance business; control and regulation of the rates,

advantages, terms and conditions that may be offered by insurers in respect of general

insurance business not so controlled and regulated by the Tariff Advisory Committee

under section 64U of the Insurance Act, 1938 (4 of 1938);

Specifying the form and manner in which books of account shall be maintained and

statement of accounts shall be rendered by insurers and other insurance Intermediaries;

Regulating investment of funds by insurance companies;

Regulating maintenance of margin of solvency;

Adjudication of disputes between insurers and intermediaries or insurance intermediaries;

Supervising the functioning of the Tariff Advisory Committee;

Specifying the percentage of premium income of the insurer to finance schemes for

promoting and regulating professional organizations.

Specifying the percentage of life insurance business and general insurance business to

undertaken by the insurer in the rural or social sector

10

COMPANY PROFILE : RELIANCE LIFE INSURANCE

2.1 COMPANY PROFILE OF THE ORGANIZATION

Reliance Life Insurance Company Limited is a part of Reliance Capital Ltd. of the Reliance -

Anil Dhirubhai Ambani Group. Reliance Capital is one of India’s leading private sector financial

services companies, and ranks among the top 3 private sector financial services and banking

companies, in terms of net worth. Reliance Capital has interests in asset management and mutual

funds, stock broking, life and general insurance, proprietary investments, private equity and other

activities in financial services.

Reliance Capital Limited (RCL) is a Non-Banking Financial Company (NBFC) registered

with the Reserve Bank of India under section 45-IA of the Reserve Bank of India Act, 1934.

Reliance Capital sees immense potential in the rapidly growing financial services sector in

India and aims to become a dominant player in this industry and offer fully integrated

financial services.

Reliance Life Insurance is another step forward for Reliance Capital Limited to offer need

based Life Insurance solutions to individuals and Corporates.

Reliance capital entered into the life insurance business by acquiring AMP Sanmar in October

2005. The business was thereafter renamed Reliance Life Insurance. Today RLIC has over 20

products - 16 individual plans and 4 employee benefit plans - including the two new innovative

products – Connect to Life and Reliance Money Guarantee Plan - that were launched recently.

11

Reliance Life Insurance Company (RLIC) has been accorded the ISO 9001-2000 certificate for

its best-in-class management systems in Quality, Customer & Process orientation.

With this, RLIC is one of the only two life insurance companies in India to get ISO 9001:2000

certification covering all functional areas.

The scope of the certification covers the entire gamut of business processes ranging from product

design, sales - front-end and back-end operations, customer care and investment, to all business

support functions. The certification has been awarded by internationally acclaimed Bureau

Veritas and is valid till 2010 subject to continued satisfactory operation of RLIC's Quality

Management System.

"This certification is a significant milestone in our continuous quest to offer innovative products,

outstanding services and improved customer satisfaction. It indicates that we have been able to

install systems, processes & performance measures that are in line with the best in the industry

and will form the basis of our business growth in future", said P Nandagopal, CEO, Reliance

Life Insurance Company.

Reliance Life Insurance is the fastest growing life insurance company in India and has an

incremental market share of 4 per cent amongst private insurers. The company has third largest

distribution network in terms of number of agents operating out of 143 locations across the

country

2.2 CORPORATE OBJECTIVE

At Reliance Life Insurance, we strongly believe that as life is different at every stage, life

insurance must offer flexibility and choice to go with that stage. We are fully prepared and

committed to guide you on insurance products and services through our well-trained advisors,

backed by competent marketing and customer services, in the best possible way.

It is our aim to become one of the top private life insurance companies in India and to

become a cornerstone of RLI integrated financial services business in India.

12

2.3 ACHIEVEMENTS

RLIC has been one of the fast gainers in market share in new business premium amongst

the private players with an incremental market share of 4.1% in the Financial Year 2007-

08 – from 3.9% in April 07 to 8% in Feb 08. ( Source: IRDA)

Also continues to be amongst the fast growing Private Life Insurance Companies with a

YOY growth of 195% in new business premium as of Mar’08.

A Company that has crossed 1.7 Million policies in just 2 years of operation, post take

over of AMP Sanmar business.

Initiated Express Life – an Unique ’Over the Counter’ sales process for Unit Linked

Insurance Policies in the Industry.

Accomplished a large distribution ramp-up in the Industry in a short span of time by

opening 600 branches in 10 months taking the overall branch network above 740.

RLIC continues to be one of the two Life Insurance companies in India to be certified

ISO 9001:2000 for all the processes.

Awarded the Jamnalal Bajaj Uchit Vyavahar Puraskar 2007- Certificate of Merit in the

Financial Services category by Council for Fair Business Practices (CFBP).

2.4 ORGANIZATIONAL CHART OF RLIC

13

Vision

Empowering everyone live their dreams.

Mission

Create unmatched value for everyone through dependable, effective, transparent and profitable

life insurance and pension plans.

Our Goal

Reliance Life Insurance would strive hard to achieve the 3 goals mentioned below:

Emerge as transnational Life Insurer of global scale and standard

Create best value for Customers, Shareholders and all Stake holders

14

Achieve impeccable reputation and credentials through best business practices

2.5 MARKETING STRATEGIES OF RELIANCE

Marketing Mix Policies

Different companies can choose to position themselves differently and hence the Marketing Mix

is different. However, there are certain common characteristics that one can cull out from the

possible strategies that companies adopt.

Product:

The development of flexible products to suit individual requirements is what will differentiate

the winners from the also-rans. The key to success is in providing insurance solutions, not

standardized insurance products. The concept of riders/optional benefits has already been a huge

innovation brought about by the new players, which has led to customization of products for

individual needs. However, companies may differentiate themselves on the basis of product

segments that they choose to focus on and excel in.

Place:

Different companies may however choose different channels and different geographies to focus

on. The channel options are - tied agency force, corporate agents and brokers and this is an area

where different companies will make different choices. Many companies like HDFC Standard

Life are focusing on all channels whereas companies like Max New York Life are focusing on

the tied agency force only. Customer interface will be a key challenge for life insurance

companies and includes every that interaction that the customer has with the company, such as

sales, new business underwriting, policy servicing, premium payments, claim processing and so

on. Technology can play a crucial role in delivering the highest standards of service set by the

company and it will be imperative for any serious player to excel in all of these

Price:

Price is a relevant differentiator only in two segments - pure term insurance and in pure

annuities. Here too, service delivery and financial strength will need to be present at a minimum

15

acceptable level for price to be a relevant differentiator. In case of savings oriented products,

long-term returns generated are more relevant than just the price of the product. A focus on

generating good investment performance and keeping a tight control on costs help in generating

good long-term maturity value for customers. Norms have been laid down on all of these by

IRDA and adhering to these while delivering good returns will be a challenge.

Promotion and Advertising:

The level of demand is latent and will have to be activated considerably. The market needs to be

developed. Greater awareness of insurance and the need to have it as a protection tool rather than

as a tax planning measure needs to be appreciated by the Indian people. Various communication

tools including advertising, direct marketing and road shows contribute to all this and different

companies take different approaches on these.

Process:

Cashless settlement: One of the most defining and customer-friendly changes that we’ve seen in

recent years relates to the way claims settlements are made. The advent of the third-party

administrator (TPA) regime has facilitated the transition to the hugely convenient era of cashless

settlement of health and auto insurance claims. TPAs are entities who process claims on behalf

of insurers: the IRDA licenses them after it is satisfied that they have the financial strength, the

trained manpower, the infrastructure and the skills to undertake this activity.

Likewise, with auto insurance, the TPA ties up with garages and authorized service centers for

cashless settlement of auto insurance claims.

Lower premiums: The spirit of competition and the broadening of the risk experience of

insurance companies have contributed to a fall in premiums over the years. That’s because, other

things being equal, an insurer who covers the lives just of 10 people bears a higher risk than an

insurer who covers the lives of, say, 100 people. Further, a broader base will provide greater

efficiencies on costs such as distribution, management and claims. A broad basing of the

mortality experience, therefore, gives insurers the elbowroom to compete by lowering premiums,

and that trend is expected to continue.

Premium payment flexibility: Insurers have imparted certain flexibility to premium payment

options in order to address this concern. For instance, one now have the option to pay your

16

premiums upfront, which is then carried forward for the tenure of the policy. The yearly

premiums are drawn from the initial corpus. Insurers have also introduced the concept of

‘automatic cover maintenance’ to protect your policy from lapsing owing to your omission to

pay your premium on time. Under this, in the event of your not paying the premium, the insurer

dips into your investment account to the extent of the premium. Of course, this comes with an in-

built drawback: your investment portion diminishes year on year to the extent of the amount paid

to cover your risk.

PLACE

Place is another marketing mix tool, it includes various activities the company undertakes to

make the product accessible and available to the target customer. This element of marketing mix

can be broken down into two clear categories:

• Distribution channel option.

• Physical distribution.

Distribution channels are the alternative method that might be chosen in making the

product/service available to the customer for purchase. In simple terms the channel of

distribution is where the customer will expect to see, and be able to purchase, the product or

services. It is worthwhile breaking channels of distribution down further into two major areas:

1. Direct distribution: many companies choose to distribute their product directly to their

customers without the use of an intervening organization, known alternatively as an intermediary

or middlemen. Companies opt for this distribution channel because of many reasons, few of them

are-

• Maintaining control over all the elements of marketing mix: this will include the way

the product is presented, its selling price, where the product is offered for sale and how the

product is promoted or sold.

• Cost: whether there are cost saving in the marketing directly rather than indirectly will

depend on the product and market circumstances. Superficially there appears to be a saving as

selling direct eliminates the need to pay a percentage amount, in terms of a reduction on

expected selling price, to the intermediary for undertaking some of the marketing tasks.

• Guaranteed outlet: selling directly to ensure a guaranteed outlet of the company’s

product as there are no intervening bodies between the organization and its customer, refusing to

17

take stock or taking from elsewhere and restricting supply. This can be important because of

growing competition and increased intermediary strength.

• Building customer relation: Dealing direct with the end-customer enables the producer

to communicate and build a very close relationship with the customer.

• Focused, specialized attention: a company selling direct can present its product or

services in concentrated and focused way to the customer unhindered by immediate competitor’s

products.

2. Indirect distribution: many companies choose to use middlemen or intermediaries to bring

their products to the market. An intermediary is an organization or an individual, which acts as a

conduit for product or services delivery, between the producer and the end-customer.

There can be one, or more, intermediaries in the distribution chain from the producer to the end-

customer and may purchase the goods either for resale to end-customer or act as some form of

agent, passing on the product to another intermediary.

RELIANCE LIFE INSURANCE makes its product available to its customer through indirect

distribution network with one level of intermediary involved in the chain. The intermediaries are

known as dealers.. RELIANCE LIFE INSURANCE believes that its relationship with the

customer does not end with the purchase of a product. For its inception, RELIANCE LIFE

INSURANCE was committed to provide an excellent network that would facilitate customer in

purchasing products, and getting their claims

Physical distribution is how the product or services actually gets to the customer, once the

choice of channel has been made. It involves planning, implementing and controlling the

physical flow of goods and services from the organization to the customer efficiently,

Effectively and at the lowest possible cost. Physical distribution can be a very costly process, in

some cases it can be as much as 20% of the total cost, it is an area where

18

many companies have managed to make huge savings and gain competitive advantage by

lowering costs and making savings in the method used.

RELIANCE take physical distribution not as cost but as a way in which company can gain

competitive advantage by offering the customer added benefits, better services or lowering prices

through continuous improvements in the methods used.

Physical distribution is making sure that the requisite goods are available when and where the

customer demands. RELIANCE has set its distribution objective in terms of the task that need to

be performed and relate to the overall sales objectives for the product and the channel outlet

chosen. RELIANCE LIFE INSURANCE has clearly identified and broken down

The amount that will need to be delivered to each outlet or delivery point two meet the agreed

sales objective. RELIANCE LIFE INSURANCE has made its objectives:

Specific

Measurable

Achievable

Realistic

PROMOTION

Promotion is the communication element in the marketing mix and it comes into use only when

the other three P’s, product, price, place, have been developed and coordinated and are ready to

meet the needs of the identified target market.

Because products, customers and markets are complex and different the promotional tasks the

need to be undertaken will also be complex and different necessitating the use of many different

types of communication techniques. These different techniques are called Promotion Mix.

Role That Product, Price & Place Play In Promotion

19

If the product, service or brand promises more customer benefits than actually exist or are

perceived to exist, than the customer will be disappointed after trial and no matter how

aggressive and intensive the advertising, the customer will feel aggrieved and even cheated and

so will not purchase again.

Similarly if the price is too high or too low in relation to the product value, or if the chosen

channel of distribution is not at the level expected, then advertising or sales promotion, which

initially creating interest or even purchase, will find that the customer disappointed will militate

against repeat purchase and might also cause long-term corporate damage.

The product, price and place will also communicate a good or bad message to the customer.

RELIANCE LIFE INSURANCE takes care of certain factors while planning a promotional

campaign. These are as follows:

Promotional objective: RELIANCE LIFE INSURANCE decides the promotion

objective i.e. what does the company wants to achieve through the use of communication

techniques;

Promotion strategies: what major methods will be used & why, to achieve these

objectives. This stage will consist of choosing one or more of the promotional mix

techniques. RELIANCE LIFE INSURANCE limited select the best promotional tools-

advertising, sales promotion, publicity etc to promote its products

Target audience: RELIANCE LIFE INSURANCE limited defines the target audience at

which it is going to aim its messages. This also involves constructive detail customer

profile for the target segment.

Message: The message content and the method of presentation is kept in line with the

product positioning statement.

Promotional Tactics: The promotional strategy is broken down into its constituent parts.

For example if above the line advertising strategy is used then the elements of the media

mix are also selected in details. If below the line sales promotion strategy is place then

various methods like free holidays, incentives are studied in detail.

20

Budget: Amount of money is allotted & promotional budgets every year. In the year

2001-02, Rs. 900 million were spend on advertisements, publicity, sales promotion &

business development.

Feedback, Monitoring & Control mechanisms: Feedback, Monitoring & Control

mechanisms are implemented to make certain that agreed promotional objectives

&performance indicators are achieved. This process is operated through the use of some

form of market research.

Integration: Finally all the methods used are integrated in a cohesive, consistent, logical

manner to meet the needs of the target audience.

Promotional mix of RELIANCE LIFE INSURANCE limited

Advertising

Sales promotion

Publicity

Advertising

Any paid form of non personal selling of the company’s product by an identified sponsored is

called as advertisement. Reliance has engaged in many types of advertising campaign which

have successfully helped Reliance India Mobile to get itself established in the Indian

telecommunication society.

Advertising is used by RELIANCE LIFE INSURANCE to

Inform: about the new products launched in the market by RELIANCE LIFE

INSURANCE Limited.

21

Reinforce: give reason (largest service network) why customer should remail with the

brand.

Persuade: customer to buy products.

The media mix is known as “above the line” promotion consists of the major methods

advertising RELIANCE products under the following headings:

Television: it is probably the most recognizable form of advertising. Marketing opportunities

have increased as TV and computers have been combined in the internet and multimedia of

offerings. Television advertising have mass reach, the products are advertised across the whole

country with the potential to reach 95% of the population. No other medium used by RELIANCE

LIFE INSURANCE has the same capability.

Print media: RELIANCE gives print advertising in newspapers, magazines and journals;

RELIANCE uses this medium of advertising less aggressively though it saves a lot of money,

targets accurately.

Cinema: research has shown that there is a clear customer segment that regularly goes to cinema

and it is good media to advertise the product. RELIANCE advertisements are also shown in

premier cinema halls.

Outdoor: outdoor posters are used as reinforcement to the primary medium such as TV or print.

RELIANCE has been extensively using this medium of advertising.

Sales promotion

The second major promotional mix method used by RELIANCE, is the use of sales promotion

also known as “below the line” promotion. Sales promotions are short term incentives used to

boost sales. It takes the form of some kind of extra value that is added to the product for the

period of promotional campaign. The RELIANCE sales promotion strategy is to increase sales,

either overall or on specific models. Most of the schemes of sales promotion are at national level.

Local level scheme are formulated and implemented by regional offices. RELIANCE does its

sales promotion in three different ways:

22

Consumer sales promotion: RELIANCE promotion is usually a short term incentive

that urgently trumpets the message to the consumer ‘buy now rather than later otherwise

it will be too late and the opportunity will be lost. Also customers are offered free

holiday packages to various destinations within and outside India, discount coupons, free

magazines subscription, etc.

Dealer sales promotion: most of the sales promotion schemes are for dealers. Generally

incentives are given to dealers are based on the target achievement.

Finance company sales promotion: RELIANCE gives incentives to finance companies

& financial institutions as subvention on certain models, which they use to incentives

customers.

Publicity: The next major promotional mix technique used by RELIANCE is the use of

publicity. Publicity is any form of planned, unpaid for media exposure that promotes the

company or its products in favorable light. This consists of items of news or stories that

appears in newspapers, magazines and on the television about the organization, their

products, their directors, their employees etc. RELIANCE understands the value of good

publicity. Marketing department of RELIANCE is concerned in using public relations

and publicity as a planned element of the promotion mix specifically to communicate

favorable message to its customer about the organizations existing & new products.

The tool of publicity

The press or news release: the press is probably most widely used by RELIANCE LIFE

INSURANCE for gaining free coverage in the national press. Information is sent to the

newspaper to be printed.

Press and news conference: the news conference is another method of building

relationship and publicity, by RELIANCE. Journalist from both TV and press release are

invited to hear some new development in the organization. After the conference there is

time allowed for question and answer session.

23

Events: RELIANCE plans staging of activity knowing that it will be reported in the

media.

Public service activity: RELIANCE LIFE INSURANCE has been actively involved in

providing medical support and welfare education and training, taking steps towards

conserving energy resources and a host of other activities in the development of a

healthier community life and proving welfare need. RELIANCE LIFE INSURANCE has

been constructing and maintaining roads in Gurgaon.

Exhibitions: an exhibition takes many forms and is seen as a marketplace for both

displaying products & services and as a way of getting producers and customers together.

The mounting of an exhibition includes all the elements of the promotional mix.

RELIANCE takes part in various trade as well as consumer exhibition.

The objective in taking part in exhibition is:

- To build goodwill, inform and educate; and pave the way of future sales.

- To communicate corporate image.

- To meet competitors.

- To make appointments and take sales leads.

Sponsorship: is giving of some form of support, usually money, in return for an

advertising, sales promotion, publicity or sales opportunity. There has been enormous

growth in this media form over the last decades and this look to continue into the future

1. RELIANCE LIFE Insurances a serious sponsor of golf &polo tournaments. The

auto flagship has sponsored the hole-in-one concept in pro-Am Golf Tournament.

2. RELIANCE LIFE Insurances extensively sponsoring various programmes in both

TV as well as Radio.

3. Reliance Life Insurance has been sponsoring various charity shoes. Recently they

had a show for Gujarat Relief Fund.

2.6 MARKETING DEPARTMENT

24

The Marketing Department is responsible for creating a “customer pull” for RELIANCE

products. The main functions of this department are:

Advertising research

Product Advertising and Promotion

Corporate Advertising

Formulating Corporate Identify Guidelines

Organizing sales training for dealers

Organizing exhibitions and rallies

Developing Socially Relevant Campaigns

Providing Support to dealers on advertising, promotion and showroom up-gradation.

2.7 REGIONAL OFFICES

In order to manage the sales and service network, RELIANCE has divided the country into five

regions, which are further into territories. It has five Regional Offices located in Delhi, Bombay,

Calcutta, Chennai and Chandigarh and Area Offices located at Lucknow, Hyderabad & Mumbai.

Each dealership operated in one territory, but does not have exclusive selling rights in the

territory. The dealer is expected to service the entire territory through his dealership.

The Regional Offices (RO) has the primary responsibility of managing, monitoring and

supporting the network in a region. The RO has field staff for sales and services. A Regional

Manager (RM) heads each RO. The sales staff has primary responsibility for all sales related

issues, and report to RM. The services engineering’s look after the workshops in the region, and

report to the Regional Service Representative (RSR).

2.8 BRAND AMBASSADOR OF RLIC

The Indian Insurance Industry seems to have caught the Nike-fever of hiring sports stars as brand

ambassadors. Aviva Life Insurance Company’s brand ambassador is Sachin Tendulkar. Sanmar

AMP Life Insurance Company, which has now been taken over by Reliance Life Insurance

Company, earlier had Australian cricket captain Steve Waugh as its brand ambassador. Sunil

Shetty and Viral Kohli would be the brand ambassadors of RLIC in the year 2010-11.

25

2.9 PRODUCTS OF RELIANCE LIFE INSURANCE

A. Market Return Plan

With Reliance Market Return plan you can have the twin advantage of insurance protection as

well as reaping the benefits of investment growth. It is a flexible plan which works all through

your life and meets the changing requirements like additional protection, liquidity through cash,

option to invest in different asset class, steady golden years and many more.

Key Features – Reliance Market Return Plan:

Twin benefit of market linked return and insurance protection

A Unit Linked Plan, different form traditional Life Insurance products, with maximum

maturity age of 80 years

Option to create your own portfolio depending on your risk appetite

Choose from 4 different investment funds

Flexibility to switch between funds

Option to pay regular as well as single premium & Top-ups

Option to package with Accidental riders

Flexibility to increase the Sum Assured

Liquidity through partial withdrawals

Benefits

Life Cover Benefit: You can choose the basic Sum Assured within the minimum and

maximum levels mentioned below

Minimum Sum Assured:

Regular Premium: Annualized Premium for 5 years or for half the Policy term

Single Premium: 125% of the single premium

Maximum Sum Assured : No Limit (Rs 500,000 for age up to 12 years)

26

In case of unfortunate loss of life, your Beneficiary will get sum Assured or Unit Account Value

whichever is higher.

Maturity Benefit : On survival, at maturity the value of your Unit Account will be paid out

Rider Benefit: You can add the Accidental Death & Accidental Total and Permanent

Disablement Benefit Rider (available only with regular premium option).

This benefit doubles the life coverage in case of accidental death or accidental total and

permanent disablement at a very nominal additional cost. The maximum cover is Rs. 50, 00,000

per life.

B. Money Guarantee Plan

For the select few like you, the Reliance Money Guarantee Plan is a Unit Linked product

addressing comprehensive need to strike that perfect balance of Protection and Savings, that you

deserve as you grow successfully. The Reliance Money Guarantee Plan is a Regular Premium

Unit Linked Policy which guarantees the entire premium (including premiums for top- ups) paid

by you. This is a plan which helps you reap all the benefits of a rising market simultaneously

protecting you from the downside risk of the market.

Key Features

Capital Guarantee The sum of all premiums paid is guaranteed on maturity or on death

before the maturity.

Capital Guarantee is available on both the basic premiums as well as on top-up premiums

Unique Return Shield feature to protect your returns

Choice to invest from 3 pre-packaged investment fund options

Unmatched flexibility through our ‘Exchange Option’ to move between the Reliance

Money Guarantee suite of products offered, as you grow up the ladder

Liquidity in the form of partial withdrawals from top-up fund

27

Option to package with Accidental Death & Disability and Term Insurance riders

The Funds Options are:

a. Funds available in respect of Basic Plan and top-up premium:

The plan offers three funds for Basic Plan and top-ups - Fund D, Fund E and Fund F. You

have the option to decide your own fund mix with respect to premiums under the Basic

Plan and top-ups.

b. Funds available in respect of Return Shield Option:

Return Shield Fund will be available if Return Shield Option is selected. The returns

earned under the Basic Plan and top-ups will be transferred to Return Shield Fund if

Return Shield option is selected.

c. Funds available during settlement period:

If you have opted for the settlement option, then Fund C would apply by default during

the settlement period

C. Reliance Whole Life Plan

You always loved your family. As a loving person you also wanted to be rest assured in the

knowledge that they will be happy, even if something were to happen to you. With Reliance

Whole Life Plan you can be sure that your family will receive that timely financial support they

need. Go ahead, live your today to the fullest without a worry about tomorrow.

Key Features

Insurance protection till age 85

28

Choose to extend your insurance coverage till age 99

Convenient Premium Payment Term Wealth creation through bonus additions

More value for your money by way of High Sum Assured Rebate

Get Sum Assured plus bonuses in case of your unfortunate death

Option to add two riders – Critical Illness and Accidental Death Benefit & Total &

Permanent Disablement Rider

Policy Loan available after three full years’ premium payment

D.Reliance Automatic Investment Plan:

The Key benefits of Reliance Automatic Investment Plan are as follows:

A smart plan which adapts to your changing risk profile with increasing age

Option to lower the average cost of units through systematic transfer of your funds

Flexibility to switch between funds and plans

Options for additional Insurance cover available through riders

Key Features Reliance Automatic Investment Plan

Two plan options to choose from Ready-made and Tailor-made

Life Stage asset allocation to ensure automatic change in investment patterns, under the

Ready-made Plan option

Freedom to decide your own fund mix based on your risk profile under the Tailor-made

Plan

Regular, limited, single premium paying options

Unmatched flexibility through our ‘Exchange Option’

Liquidity in the form of partial withdrawal

Option to avail of Accidental Death Benefit, Accidental Total, Premium Disability and

Term Insurance riders

E. Reliance Golden Year Plan:

29

The Reliance Golden Years Plan Value gives you the right kind of solution. A retirement plan

that allows you to save systematically to generate a much needed corpus to make your olden

years look golden.

UNDER THIS PLAN THE INVESTMENT RISK IN THE INVESTMENT PORTFOLIO IS

BORNE BY THE POLICYHOLDER.

Key Features

Invest systematically and secure your golden years

Four different investment funds to choose from

Flexibility to advance your Vesting Age

Tax free commutation of up to one third of fund value at vesting age

Life cover and optional Accidental rider

F. RELIANCE ENDOWEMENT PLAN:

Reliance Endowment Plan gives you just the financial independence to realize your dreams in

the future. It lets you decide how much you would like to set as your sum assured based on your

current financial position and your expected future expenses.

Key Features:

On maturity receive Sum Assured plus bonuses

Wealth creation through bonus additions

More value for your money by way of High Sum Assured Rebate

Increase your insurance protection by adding Term Cover

Choose to pay regular or single premium

Choose to add the benefit of two riders - Critical Illness Rider and Accidental Death

Benefit & Total and Permanent Disablement Rider

Choose to avail of a Policy Loan after three full years’ of premium payment

30

Benefits:

Maturity Benefit: On maturity you get Sum Assured plus accumulated bonuses (if any) till that

date.

Life Cover Benefit: In the unfortunate event of loss of life, your family will receive the Sum

Assured plus accumulated bonuses (if any) till that date.

Rider Benefit: You also have the option to add three additional benefits to customize the Policy

as per your needs for the regular premium plan

a. Term Life Insurance Benefit Rider

b. Accidental Death Benefit & Total and Permanent Disablement Rider

c. Critical Illness Rider

Term Life Insurance Benefit Rider:

Add the advantage of the Term Life Insurance Benefit rider to your basic Policy and increase

risk coverage. In the event of unfortunate loss of life the Term Life Insurance Benefit is payable

and the amount payable is equal to the rider Sum Assured. There is no Maturity Benefit.

Term Insurance

Minimum / Maximum Age at

entry 18 / 59

Maximum Age at expiry 64 yrs (policy anniversary immediately following age)

Sum Assured Rs 1,00,000 Equal to basic policy sum assured

Policy Term Equal to basic policy term

Minimum Policy Term: 5 years

31

Maximum Policy Term: Regular Premium - 35 years (Single)

Premium 15 years

The Policy Term:

Minimum Policy Term: 5 years

Maximum Policy Term: Regular Premium – 35 years (Single)

Premium 15 years

Entry age:

Minimum age at

entry: 5 years

Maximum age at

entry:65 years

Minimum age at

maturity:18 years

Maximum age at

maturity:75 years

The Sum Assured:

Minimum Sum

Assured:

Regular Premium – Rs 25,000 For

Single

Premium it is

determined by the minimum premium

Maximum Sum

Assured:Entry age below 18 years - Rs 5,00,000

Entry age 18 years and

above No Limit

32

Surrendering the policy:

You have the option to Surrender your Policy and receive the Surrender Value. If your Policy

has accumulated any bonuses, then you will also receive the cash value of that total amount upon

surrendering your Policy. Your single premium plan acquires a surrender value as soon as you

pay your premium. We guarantee a minimum surrender value of 70% of the single premium paid

excluding any extra premium plus the cash surrender value of any vested bonuses.

Your regular premium plan acquires a surrender value after 3 years’ premium has been paid and

after three years have elapsed from date of commencement of Policy. We guarantee a minimum

surrender value of 30% of the total premiums paid (excluding any extra premiums and premiums

for additional benefits) subsequent to the first year premium, plus the cash surrender value of any

vested bonuses. On surrender, the insurance protection provided under the policy will also cease.

2.10 COMPETITION INFORMATION

1. HDFC Standard Life Insurance Company Ltd.

HDFC Standard Life Insurance Company Ltd. is one of India’s leading private life insurance

companies, which offers a range of individual and group insurance solutions. It is a joint venture

between Housing Development Finance Corporation Limited (HDFC Ltd.), India’s leading

housing finance institution and The Standard Life Assurance Company, a leading provider of

financial services from the United Kingdom. Their cumulative premium income, including the

first year premiums and renewal premiums is Rs. 672.3 for the financial year, Apr-Nov 2005.

They have managed to cover over 11,00,000 individuals out of which over 3,40,000 lives have

been covered through our group business tie-ups.

2. Max New York Life Insurance Co. Ltd.

33

Max New York Life Insurance Company Limited is a joint venture that brings together two large

forces - Max India Limited, a multi-business corporate, together with New York Life

International, a global expert in life insurance. With their various Products and Riders, there are

more than 400 product combinations to choose from. They have a national presence with a

network of 57 offices in 37 cities across India.

3. ICICI Prudential Life Insurance Company Ltd.

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank, a premier

financial powerhouse and Prudential plc, a leading international financial services group

headquartered in the United Kingdom. ICICI Prudential was amongst the first private sector

insurance companies to begin operations in December 2000 after receiving approval from

Insurance Regulatory Development Authority (IRDA). The company has a network of about

56,000 advisors; as well as 7 bank assurance and 150 corporate agent tie-up

4. Om RELIANCE Mahindra Life Insurance Co. Ltd.

RELIANCE Mahindra Old Mutual Life Insurance Ltd. is a joint venture between RELIANCE

Mahindra Bank Ltd. (KMBL), and Old Mutual plc.

5.Birla Sun Life Insurance Company Ltd.

Birla Sun Life Insurance Company is a joint venture between Aditya Birla Group and Sun Life

financial Services of Canada.

6.SBI Life Insurance

SBI Life Insurance is a joint venture between the State Bank of India and BNP Paribas

Assurance. SBI Life Insurance is registered with an authorized capital of Rs 2000 crores and a

34

Paid-up capital of Rs 1000 Crores. SBI owns 74% of the total capital and BNP Paribas

Assurance the remaining 26%.

State Bank of India enjoys the largest banking franchise in India. Along with its 7 Associate

Banks, SBI Group has the unrivalled strength of over 14,500 branches across the country,

arguably the largest in the world. BNP Paribas Assurance is the insurance arm of BNP Paribas -

Euro Zone’s leading Bank. BNP Paribas, part of the world's top 10 group of banks by market

value and part of Europe top 3 banking companies, is one of the oldest foreign banks with a

presence in India dating back to 1860. BNP Paribas Assurance is the forth largest life insurance

company in France, and a worldwide leader in Creditor insurance products offering protection to

over 50 million clients. BNP Paribas Assurance operates in 42 countries mainly through the bank

assurance and partnership model.

SBI Life has a unique multi-distribution model encompassing Bank assurance, Agency and

Group Corporates.

SBI Life extensively leverages the SBI Group as a platform for cross-selling insurance products

along with its numerous banking product packages such as housing loans and personal loans.

SBI’s access to over 100 million accounts across the country provides a vibrant base for

insurance penetration across every region and economic strata in the country ensuring true

financial inclusion.

7. Allianz Bajaj Life Insurance Company Ltd.

Bajaj Allianz Life Insurance Company Limited is a Union between Allianz SE, one of the

world’s largest Life Insurance companies and Bajaj Auto, one of the biggest 2- &- 3 wheeler

manufacturers in the world.

Allianz SE is a leading insurance conglomerate globally and one of the largest asset managers in

the world, managing assets worth over a Trillion Euros (Over R. 55,00,000 crores). Allianz SE

has over 115 years of financial experience in over 70 countries.

35

Bajaj Auto is one of the most trusted name is Indian auto for over 55 years. At Bajaj Allianz

customer delight is our guiding principle. Ensuring world-class solutions by offering customized

products with transparent benefits, supported by best technology is our business philosophy.

OTHER PLAYERS:

Tata AIG Life Insurance Company Ltd

ING Vysya Life Insurance Company Private Limited

Met life India Insurance Company Pvt. Ltd.

AMP SANMAR Assurance Company Ltd.

Dabur CGU Life Insurance Company Pvt. Ltd.

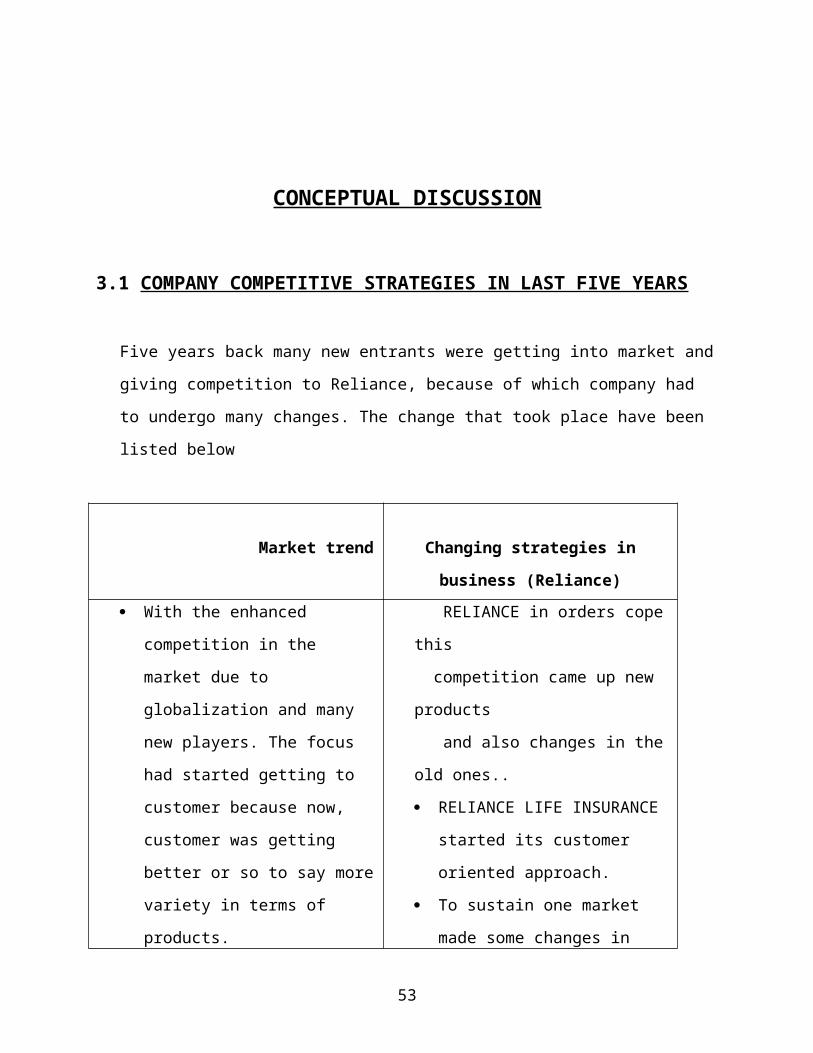

CONCEPTUAL DISCUSSION

3.1 COMPANY COMPETITIVE STRATEGIES IN LAST FIVE YEARS

Five years back many new entrants were getting into market and giving competition to

Reliance, because of which company had to undergo many changes. The change that took

place have been listed below

Market trend Changing strategies in business

(Reliance)

With the enhanced competition in RELIANCE in orders cope this

36

the market due to globalization and

many new players. The focus had

started getting to customer because

now, customer was getting better or

so to say more variety in terms of

products.

competition came up new products

and also changes in the old ones..

RELIANCE LIFE INSURANCE

started its customer oriented

approach.

To sustain one market made some

changes in one market strategy as

well as making advertisement

which would show one deep

association of RELIANCE LIFE

INSURANCE with Indians and at

the same time reflect technological

changes.

Customer was getting aware with

the availability of choice to him

thus he now asked value for every

penny is spent.

RELIANCE in this course of time

launched new products well within

on reach of common man.

RELIANCE LIFE INSURANCE

makes the product to suit the

Indian pockets

RELIANCE LIFE INSURANCE

came up with easy financing

schemes. They made the tie-ups

with big financing companies such

as GE financing and country wide

financing.

RELIANCE LIFE INSURANCE

started giving the accidental

Insurance coverage for its

customers

But the best thing the RELIANCE

37

got into was buying & selling of

cars.

Technological improvements- The

competitors were convincing with

better technology which made them

cut cost and sell cheap, thus

assuring higher technology.

Changes at HDFC- RELIANCE

LIFE INSURANCE Limited could

not just sit back and see its

competitors rising and acquiring the

market share. Hence they also

improved upon technology with one

changing times. In fact they are

always on the move for new and

better technology.

For the betterment of the society

and environment they started

complying with EURO-II norms.

Another change was done in terms

of Recruitment and Selection policy

i.e. RELIANCE now started

recruiting more technical staff who

would be specialist in their fields.

Quality Assurance- There was a

need for quality order to sustain the

market share and provide better

service to the customer.

Changes incorporated by

RELIANCE- following the

customer oriented approach.

RELIANCE now focused itself by

providing after sales services.

There was increase in number of

branches and offices .

First few services required after

specific KMs was provided free.

38

Forecasting the changes in the

market five year down the line

was a tough job in term of

increasing competition.

We are gradually moving towards

the customer oriented market,

where customer very soon would

be termed as “King of the

Market”.

Customer will drive the marketing

strategy.

Market would be fragmented on

the basis of different segments for

new customers,

RELIANCE LIFE INSURANCE

would keep customer as prime

factor.

There is possibility that

RELIANCE LIFE INSURANCE

starts with the customization of

products i.e. make

Customer would like to have the

product with higher cost

effectiveness. Money being a

major consideration in current

scenario and which is expected to

raise furthermore cars need to

higher in terms of high

growth ,return and savings

RELIANCE would solve this

problem by taking following

steps:

Buying back facilities.

Easy financing and financing 0%

interest or very low rate.

More tie-ups with financial

institutional % insurance agencies

in the near futures.

Higher Technology and

innovation in terms of style, looks

and utility too would induce the

customer to buy

RELIANCE plans technology

infusion in terms of quality and

standard

Plans to use 100% Indian parts to

be used for production.

Diversification in production and

adoption of new methods for

cutting cost.

39

Company who could build the

brand in one market would sell

more.

RELIANCE- thus would adopt

both rational as well as emotional

appeal to sell their vehicle i.e.

would produce better quality of

car with assurance and also do one

advertising on the emotional

grounds to appeal the customers.

Competition – players in the

market. Not everybody would be

leader. Thus the leader would be

the one who caters the customer

need at most competitive prices

and satisfying one rule and norms

laid by the systems.

Understood the definition of the

leader and wants to be the leader

in the industry

RESEARCH METHODOLOGY

4.1 RESEARCH OBJECTIVES

The search for knowledge through objective and systematic method of finding solution to

problem is research.

The primary objective of the project is to study the changing marketing trend of reliance life

insurance

The secondary objectives of the research are as follows:

To study the securities market industry as a whole.

To know the profile of reliance life insurance.

The study deals with Reliance Life Insurance in focus and the various segments that

it caters to.

40

To study the various services and features offered by changing trend of reliance life

insurance.

The study then goes on to evaluate and analyse the findings so as to present a clear

picture of trends in the Insurance sector.

4.2 RESEARCH DESIGN

A research design is the arrangement of conditions for collections and analysis of data in a

manner that aims to combine relevance to the research problem with economies in a procedure.

I have used descriptive research design for my research.

Descriptive Research

Descriptive research includes surveys and fact findings enquiries of different kinds. It basically

gives a description of the state of affairs as it exists at present. A researcher has no control over

the variables so they can only report what has happened or what is happening. We can also use

the survey method for this purpose.

4.3 DATA SOURCES

A research design is one, which simplifies the framework of plan for the study and adds itself in

the quick collection and analysis of the data. It is a blue print that has been filled in completing

the study. Data sources are:

Primary data

The primary data are those which are collected fresh for the first time and thus happen to be

original in character. In other words, it is obtained by design to fulfill the data are original in

character and are also generated in a large number of surveys conducted mostly by government

and also by institution and research bodies.

A questionnaire was prepared for the respondents, where there views were collected.

Secondary data

41

The secondary data are those which have already been collected for some purpose other than the

problem in hand and passed through the statistical process. In other words, data that are not

originally collected rather obtained from Published and Unpublished Sources.

The secondary data has been collected through various sources:

Internet

Books

Newspaper

Magazines

Brochure

Journals

Websites

4.4 QUESTIONNAIRE DESIDN / FORMULATION

Questionnaires: - A questionnaire consists of a set of questions presented to respondent for their

answers. It can be Closed Ended of Open Ended.

Open Ended: - Allows respondents to answer in their own words & are difficult to

Interpret and Tabulate.

Close Ended: - Pre-specify all the possible answers & are easy to Interpret and Tabulate.

Types of question included:

Dichotomous questions: - Which has only two answers “Yes” or “No”.

Multiple choice questions: - Where respondent is offered more than two choices.

Importance scale: - A scale that rates the importance of some attribute.

Rating scale:- A scale that rates some attribute from “highly satisfied ” to “highly

unsatisfied “ and “very inefficient” to “very efficient

42

But in this project report, the questionnaire includes only closed type questions because it saves

respondents time and helps them to understand easily.

4.5 SAMPLE DESIGN

A sample design is a definite plan for obtaining a sample from given population. It refers to the

techniques or procedures, the researcher would adopt in selecting items for the sample.

i. Sample element /unit

The primary data was collected through survey that was systematically carried in north-east

region of Delhi. The data was collected through questionnaire. The responses of the

respondents were recorded in the questionnaire prepared for them.

ii. Extent

Extent refers to the area from the respondents belong. We have conducted the research

mainly on the people of Delhi, that too specifically, north-east region.

iii. Time frame

Time frame is the time spent on research. The time frame for our research is 8 weeks.

iv. Sampling technique

Sampling technique refers to the technique or procedure the researcher would adopt in

selecting items for the sample. We have used judgmental sampling for our research because

gathering information from every individual is not possible.

v. Sample size

Sample size refers to the number of respondents. To get a clear view we have conducted

our research on 100 people.

4.6 LIMITATIONS OF THE RESEARCH

• Since the sampling was done in Delhi only it does not represent the entire picture of

Indian market.

43

• The questionnaire might have been filled without much attention to the questions due to

lack of time by the respondents.

• Incase of Primary data, respondents were not very much interested in filling the

questionnaire and sometimes it was difficult to contact or meet the clients, because of

their work schedules and personal reasons.

• There may be biasness against some personal preferences and which would have led to

unjustified responses from the respondents.

• Personally contacting the clients involved time and cost.

• Secondary data when collected was invaluable but due to passage of time and with many

dynamic changes taking place in the markets, the information losses its value in the

current scenario.

• As gathering information from every individual was not possible so we have to take

judgmental sampling.

DATA ANALYSIS AND INTERPRETATION

Q1. Age Group?

1 Age group 25-30

2 Age group 30-35

3 Age group 35-40

4 Above age 40

S.NO TYPE OF CHOICE % AGE

1 Age group 25-30 15

2 Age group 30-35 40

3 Age group 35-40 30

44

4 Above age 40 15

INTERPRETATION:

From the above pie chart, we can understand that age group of 25 to 30 are more then other three

age groups.

Q2. Gender ?

1 Male

2 Female

S.NO TYPE OF CHOICE

1 Male 65

2 Female 35

15%

40%30%

15%

1 Age group 25-30

2 Age group 30-35

3 Age group 35-40

4 Above age 40

45

65%

35%

1 Male

2 Female

INTERPRETATION:

From the above pie chart, we can understand that males are more investing in insurance company

rather then females

Q3. Occupation?

1) Businessmen

2) Service

3) Housewife

4) Others

S.NO TYPE OF CHOICE

1 Businessmen 40

2 Service 30

3 Housewife 10

4 Others 20

46

40%

30%

10%

20%

1 Businessmen

2 Service

3 Housewife

4 Others

INTERPRETATION:

From the above pie chart, we can see businessmen, service are more then housewives and others.

Q4. Annual income?

1 50,000-1,00,000

2 1,00,000-2,50,000

3 2,50,000-3,00,000

4 Above 3,00,000

S.NO TYPE OF CHOICE

1 50,000-1,00000 15

2 1,00000-2,50000 35

3 2,50000-300000 40

4 Above 3,00000 10

47

INTERPRETATION:

From the above pie chart, it is clear 40 % ratio of the people have annual income between

2,50000-300000 as compared to the 35 % ratio of the people whose annual income falls between

1,00000-2,50000 .

Q5.Are you insured or not?

1 Yes

2 No

S.NO TYPE OF CHOICE

1 Yes 80

2 No 20

15%

35%40%

10%

1. 50,000-1,00000

2. 1,00000-2,50000

3. 2,50000-300000

4. Above 3,00000

48

80%

20%

1 Yes

2 No

INTERPRETATION:

To get the clear picture of the survey we have taken , much of who have insurance as they are

aware of various things related to insurance

6.From where you have taken insurance?

1 Public sector

2 Private sector

S.NO TYPE OF CHOICE

1 Public sector 25

2 Private sector 75

49

25%

75%

1 Public sector

2 Private sector

INTERPRETATION:

From the above pie chart, it is clear that 75 % of the people have taken insurance from private

sector and 25 % of people from public sector.

7. In your view which is the Best private sector company?

1 Reliance life insurance

2 ICICI Prudential

3 HDFC SLIC

4 Others

50

40%

25%

20%

15%

1 RELIANCE Life Insurance

2 ICICI Prudential

3 HDFC SLIC

4 Others

S.NO TYPE OF CHOICE

1 RELIANCE Life Insurance 40

2 ICICI Prudential 25

3 HDFC SLIC 20

4 Others 15

INTERPRETATION:

From the above pie chart, it is clear that about 40 % of the people prefer Reliance life insurance

as compared to the 25 % of the people which prefer ICICI prudential as their best private sector

company .

Q8. Are you satisfied with your present company?

1 Completely Satisfied

2 Partially Satisfied

3 Dissatisfied

4 Partially Dissatisfied

51

S.NO TYPE OF CHOICE % AGE

1 Completely satisfied 20

2 Partially Satisfied 40

3 Dissatisfied 25

4 Partially Dissatisfied 15

INTERPRETATION:

From the above pie chart, it is clear that about 40 % of the people are satisfied with their present

life insurance company as compared to the 25 % ratio of the people which are not satisfied.

However 15 % of the people are dissatisfied .

Q9.Which features do you think RELIANCE Life Insurance Company have

better a part from other companies?

1 Cheaper Price

2 Wide Distribution of Products

20%

40%

25%

15%1 Completely satisfied

2 partially Satisfied

3 Dissatisfied

4 partially Dissatisfied

52

3 Good Claim

4 Others

35%

15%30%

20%

1 Cheaper price

2 Wide distribution of products

3 Good claim procedure

4 Others

S.NO TYPE OF CHOICE

1 Cheaper price 35

2 Wide distribution of products 15

3 Good claim procedure 30

4 Others 20

INTERPRETATION:

From the above pie chart, it is clear 35 % of the people like the cheaper price as the unique

feature which the company should have as compared to the 30 % ratio of the people which thinks

that the claim procedure should be good and fast.

Q10. Which product do you prefer the most ?

1 ULIP Plans

2 Children Plans

3 Pension Plans

4 Endowment plans

53

20%

40%

15%

25%

1 ULIP plans

2 Children Plans

3 Pension Plans

4 Endow ment plans

S.NO TYPE OF CHOICE

1 ULIP plans 20

2 Children Plans 40

3 Pension Plans 15

4 Endowment plans 25

INTERPRETATION:

From the above pie chart, it is clear that 40 % of the people think that children plans are the best

selling product in the life insurance company as compared to the 25 % of the people which

thinks that endowment plans are best selling plans.

Q11. Which marketing strategy of the RELIANCE life Insurance attracts you

the most?

1 Advertising Strategy

2 Place Distribution Strategy

3 Making Exhibitions

4 Others

54

46%

25%

14%

15%

1 Advertising Strategy

2 Place distribution strategy

3 Making Exhibitions

4 Others

S.NO TYPE OF CHOICE

1 Advertising Strategy 46

2 Place distribution strategy 25

3 Making Exhibitions 14

4 Others 15

INTERPRETATION:

From the above pie chart, it is clear that about 46 % of the thinks that the advertising strategy of

the company attracts most of the customers as compared to the 25 % ratio of the people which

thinks that the place distribution strategy is the best strategy