28

Chap 8

| Date post: | 01-Jan-2016 |

| Category: |

Documents |

| Upload: | vanna-rodgers |

| View: | 26 times |

| Download: | 0 times |

Chap 8

The Time Value of Money

• Compound interest• Future value and Present value• Annuities• Multiple Cash Flows• NPV and internal rate of return

Compound Interest

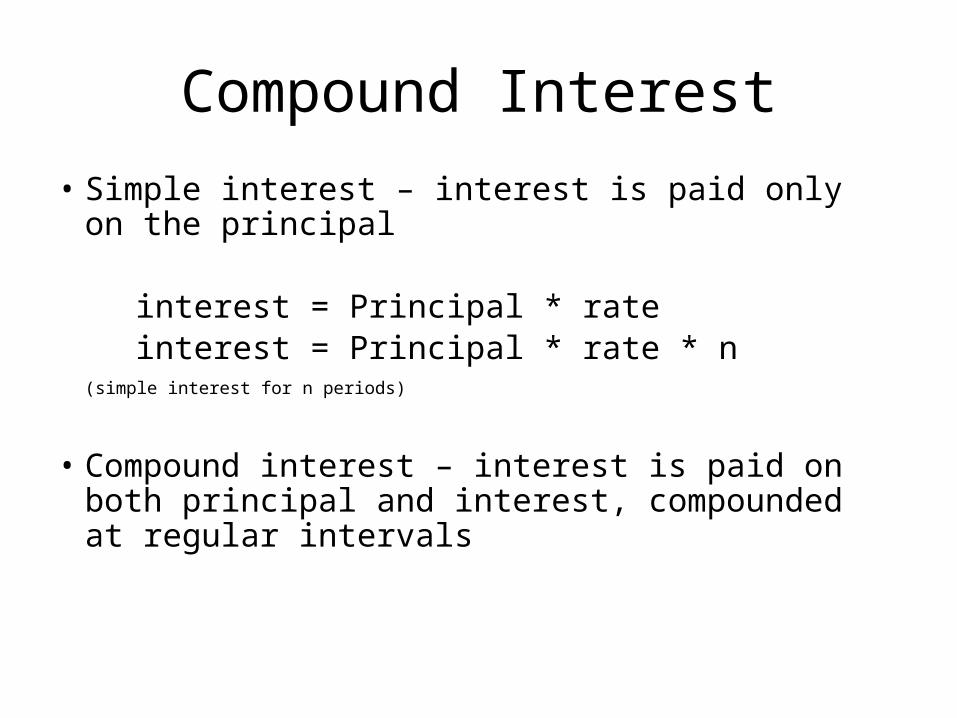

• Simple interest – interest is paid only on the principal interest = Principal * rate interest = Principal * rate * n (simple interest for n periods)

• Compound interest – interest is paid on both principal and interest, compounded at regular intervals

Compound Interest Example

Year Year-begin balance Year-end Interest Year-end balance (FVi)

1 1000 1000*0.1 1000+1000*0.1=1000(1+0.1)

2 1000(1+0.1) 1000(1+0.1)*0.1 1000(1+0.1) + 1000(1+0.1)*0.1=1000(1+0.1)(1+0.1)=1000(1+0.1)^2

3 1000(1+0.1)^2 1000(1+0.1)^2 *0.1 1000(1+0.1)^2+ 1000(1+0.1)^2 *0.1=1000(1+0.1)^3

Example: save $1000 now, with 10% interest, if interest is compounded annually, after 3 years, what will the saving become?

Compound Interest

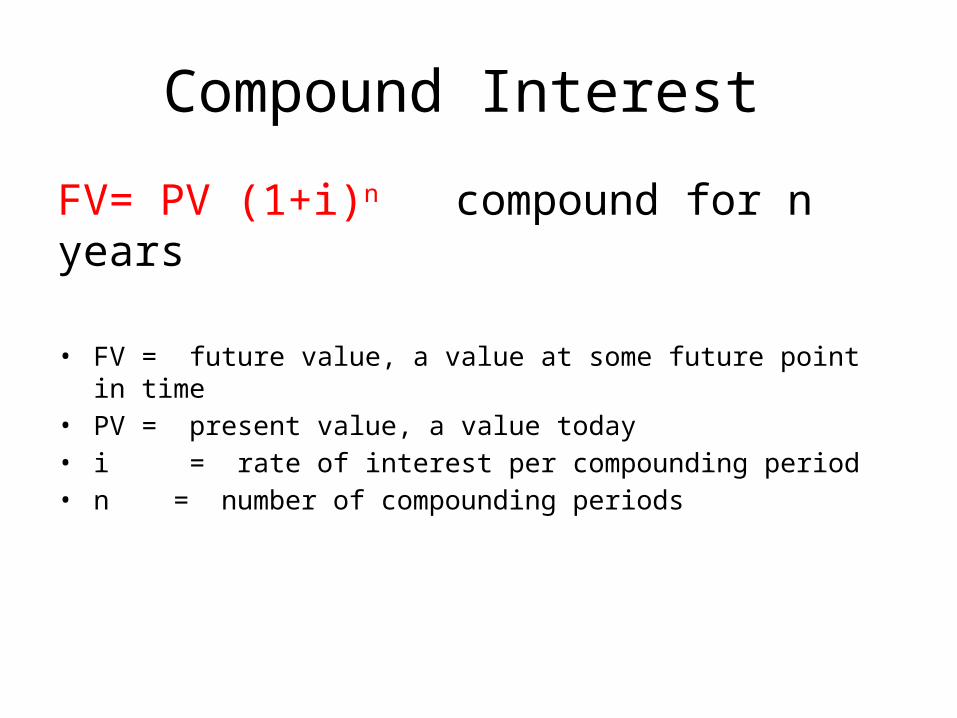

FV= PV (1+i)n compound for n years

• FV = future value, a value at some future point in time• PV = present value, a value today• i = rate of interest per compounding period • n = number of compounding periods

Future Value Example

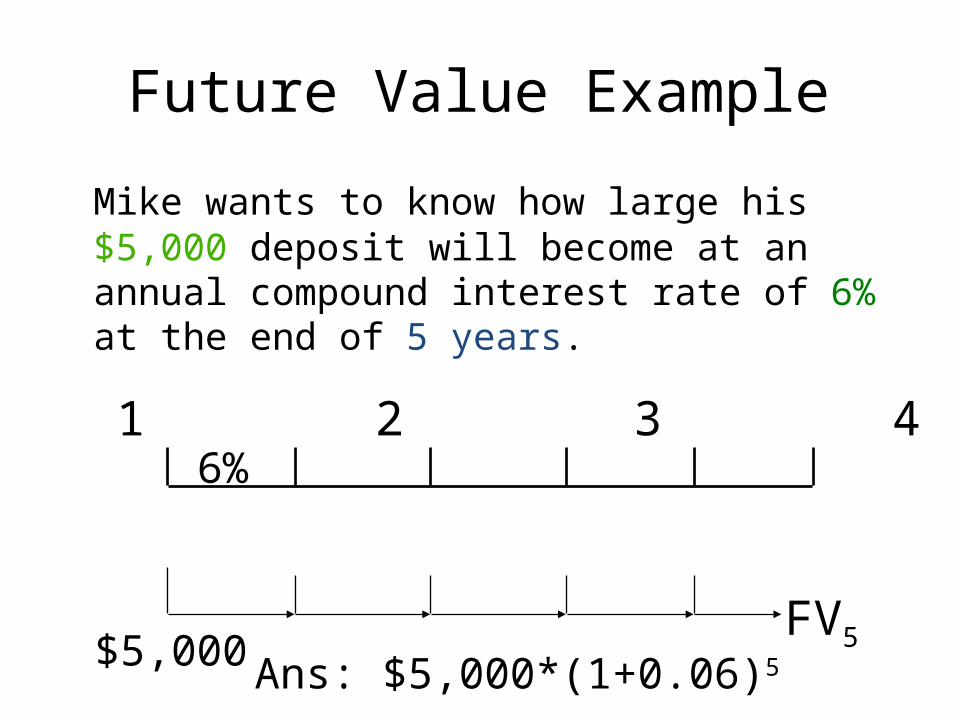

Mike wants to know how large his $5,000 deposit will become at an annual compound interest rate of 6% at the end of 5 years.

0 1 2 3 4 56%

FV5$5,000 Ans: $5,000*(1+0.06)5

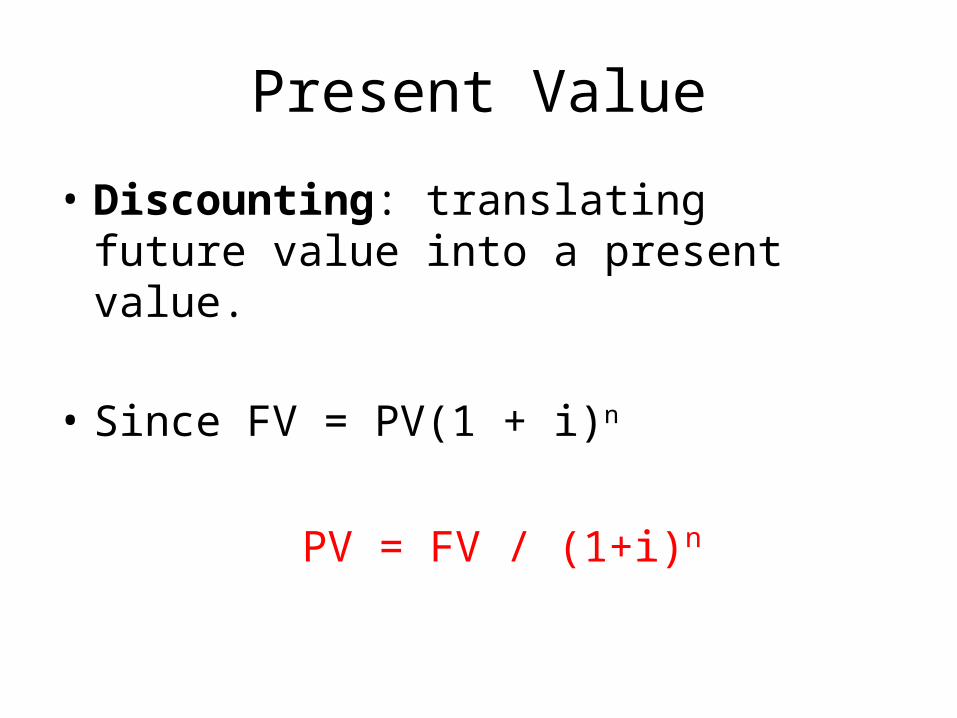

Present Value

• Discounting: translating future value into a present value.

• Since FV = PV(1 + i)n

PV = FV / (1+i)n

Present Value Example

0 1 2 3 4 6%

PV

Assume that you need to have exactly $5,000 saved 4 years from now. How much must you deposit today in an account that pays 6% interest, compounded annually, so that you reach your goal of $5,000 in 4 years?

$5,000

PV= 5000/(1+0.06)4

Frequency of Compounding

• Frequency of Compounding may not be annually, need to use the rate per compounding period as i, and calculate the number of compounding periods as n

• For an annual rate 12%, compounding for 4 years

Frequency i: Rate per period n: Number of Periods

semi-annually 12%/2 4*2

quaterly 12%/4 4*4

monthly 12%/12 4*12

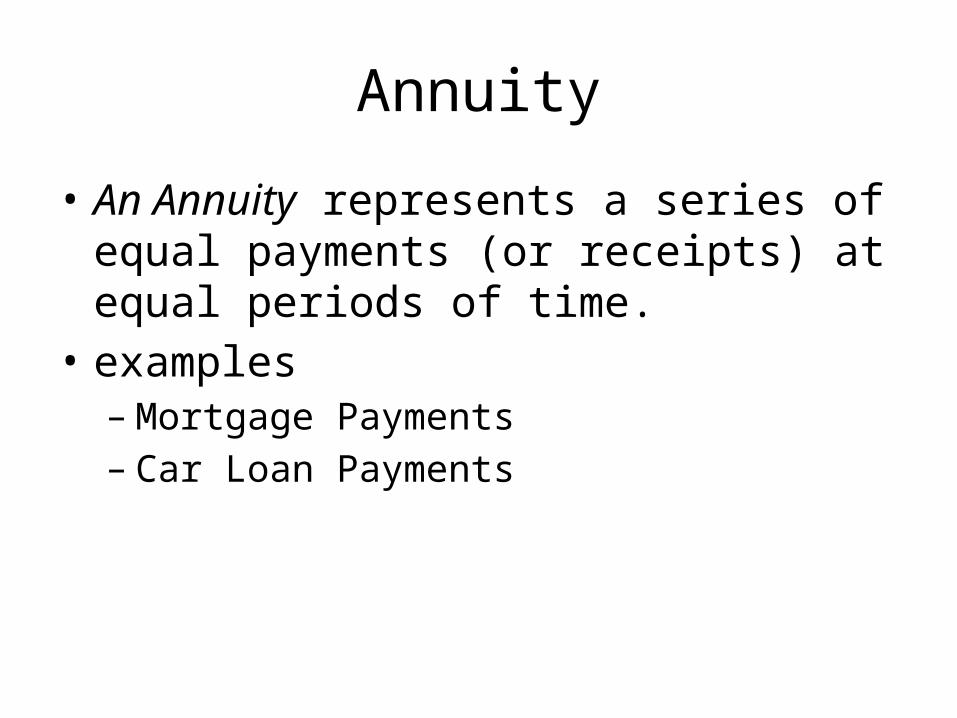

Annuity

• An Annuity represents a series of equal payments (or receipts) at equal periods of time.

• examples– Mortgage Payments– Car Loan Payments

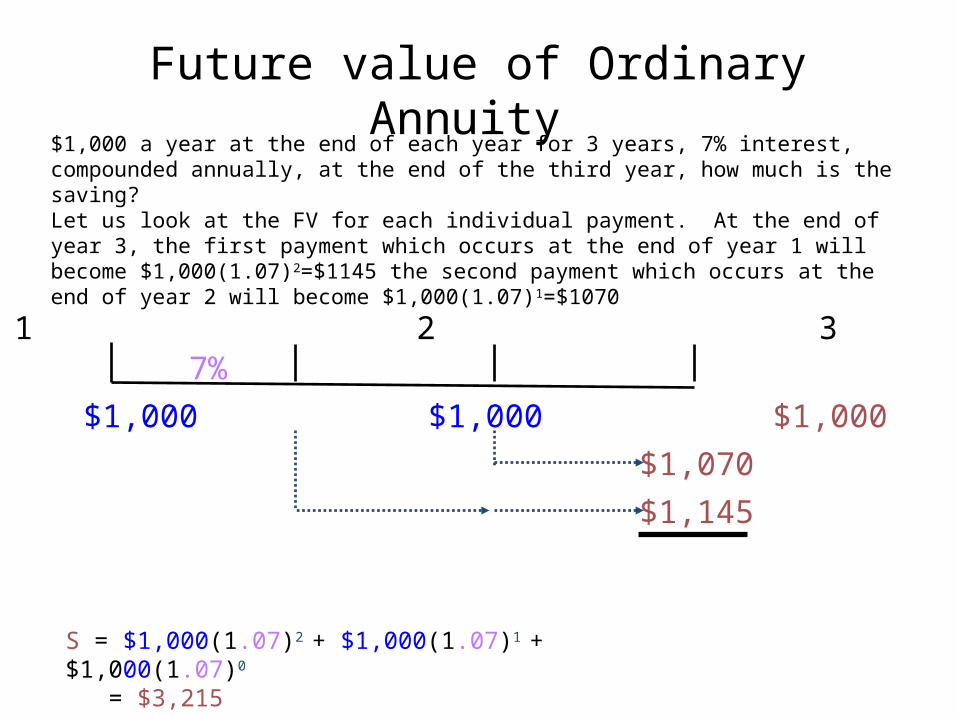

Future value of Ordinary Annuity

$1,000 $1,000 $1,000

0 1 2 3 7%

$1,070

$1,145

S = $1,000(1.07)2 + $1,000(1.07)1 +$1,000(1.07)0 = $3,215

$1,000 a year at the end of each year for 3 years, 7% interest, compounded annually, at the end of the third year, how much is the saving? Let us look at the FV for each individual payment. At the end of year 3, the first payment which occurs at the end of year 1 will become $1,000(1.07)2=$1145 the second payment which occurs at the end of year 2 will become $1,000(1.07)1=$1070

Amount (Future Value) of an Annuity

• Amount of an annuity - S (future value) of n payments of R dollars for n periods at a rate of i per period:

in

n

sRi

iRS

11

Example

• Jenny deposits $2000 at the end of each year in an account earning 10% compounded annually. Determine how much money she has after 25 years. How much interest did she earn?

€

S = 20001+ .10( )

25−1

.10

⎡

⎣ ⎢ ⎢

⎤

⎦ ⎥ ⎥= 2000

9.834706

.10

= $196,694.12

I =196,694.12 − (25 × 2000) = $146,694.12

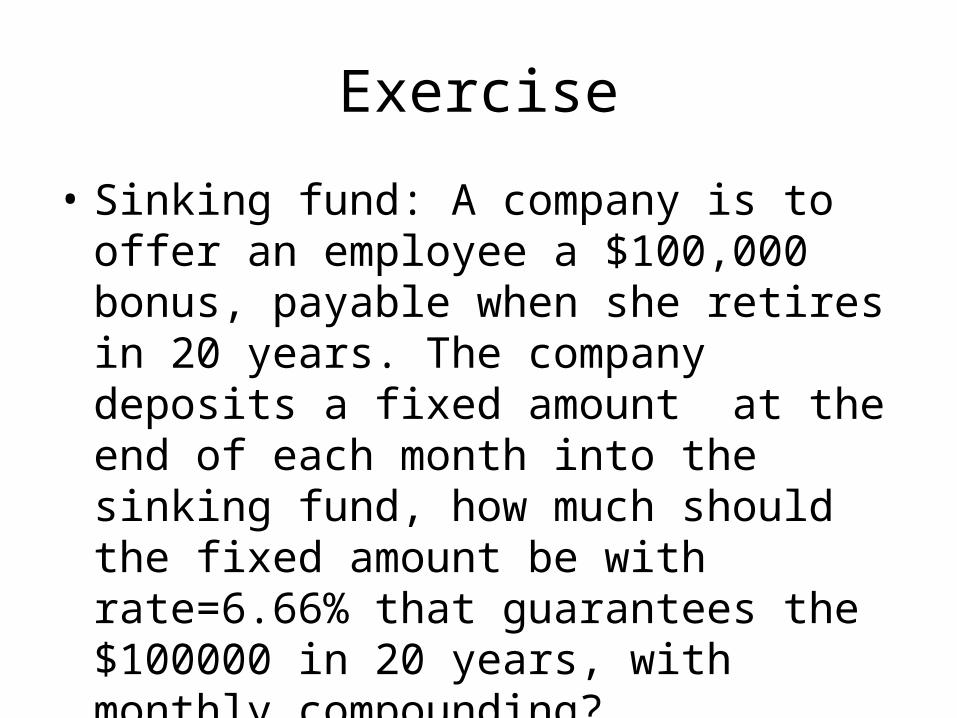

Exercise

• Sinking fund: A company is to offer an employee a $100,000 bonus, payable when she retires in 20 years. The company deposits a fixed amount at the end of each month into the sinking fund, how much should the fixed amount be with rate=6.66% that guarantees the $100000 in 20 years, with monthly compounding?

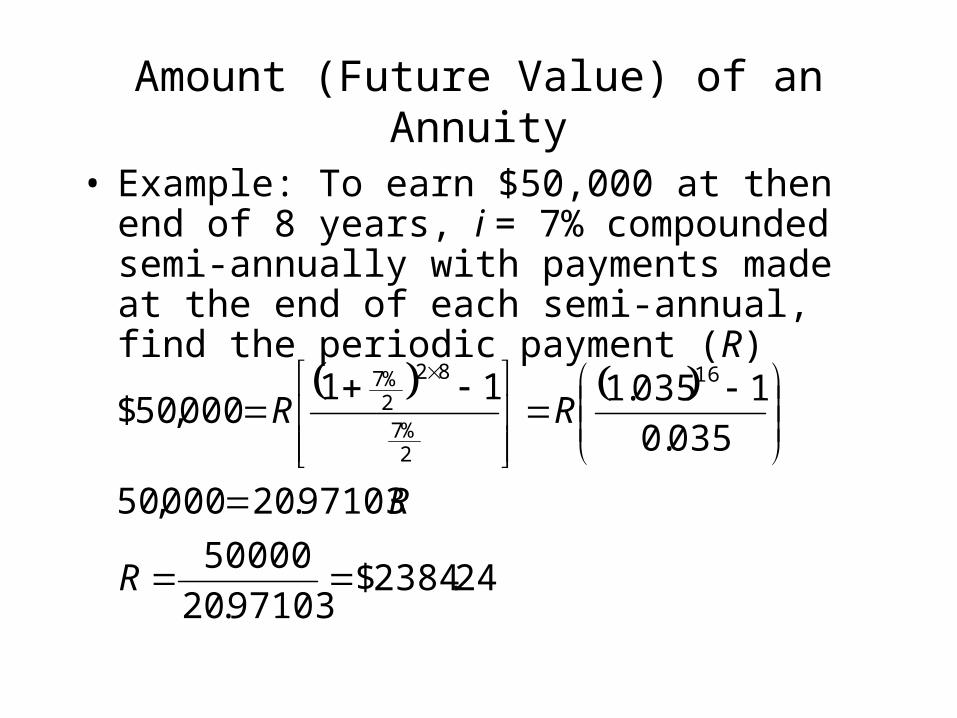

Amount (Future Value) of an Annuity

• Example: To earn $50,000 at then end of 8 years, i = 7% compounded semi-annually with payments made at the end of each semi-annual, find the periodic payment (R)

24.2384$97103.20

50000

97103.20000,50

035.0

1035.111000,50$

16

2%7

82

2%7

R

R

RR

Present Value of Ordinary Annuity

$1,000 $1,000 $1,000

0 1 2 3

$2,624.32 = P

7%

$934.58$873.44 $816.30

P = $1,000/(1.07)1 + $1,000/(1.07)2 + $1,000/(1.07)3 = $2,624.32

If one set up a fund such that it pays $1,000 a year at the end of every year for three years and the discount rate is 7%, how much should one put in the account today?

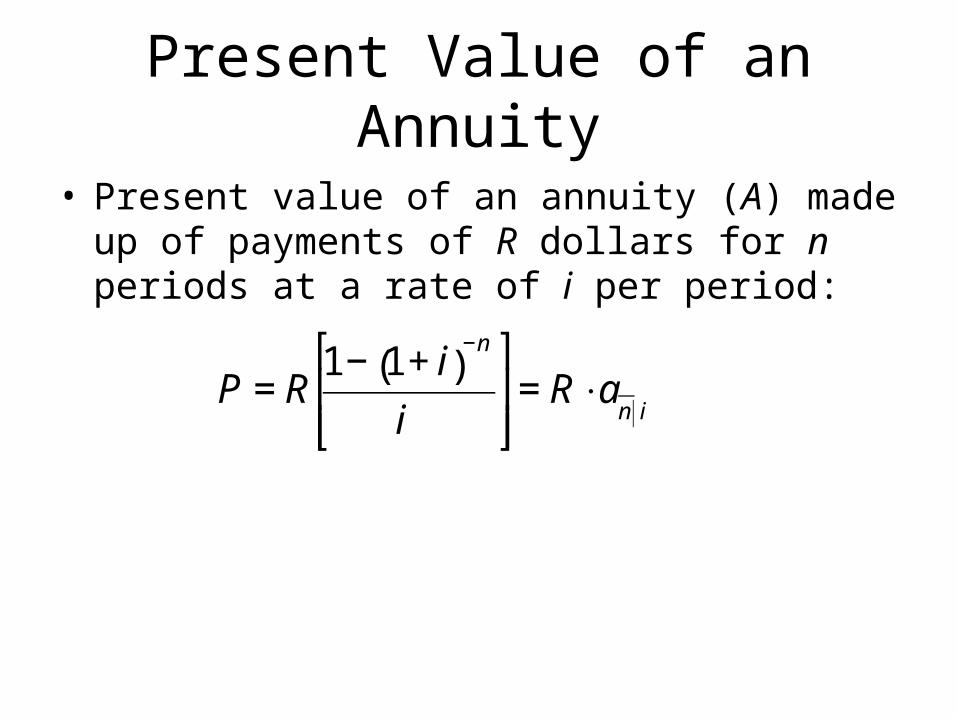

Present Value of an Annuity

• Present value of an annuity (A) made up of payments of R dollars for n periods at a rate of i per period:

€

P = R1− 1+ i( )

−n

i

⎡

⎣ ⎢ ⎢

⎤

⎦ ⎥ ⎥= R ⋅a

n i

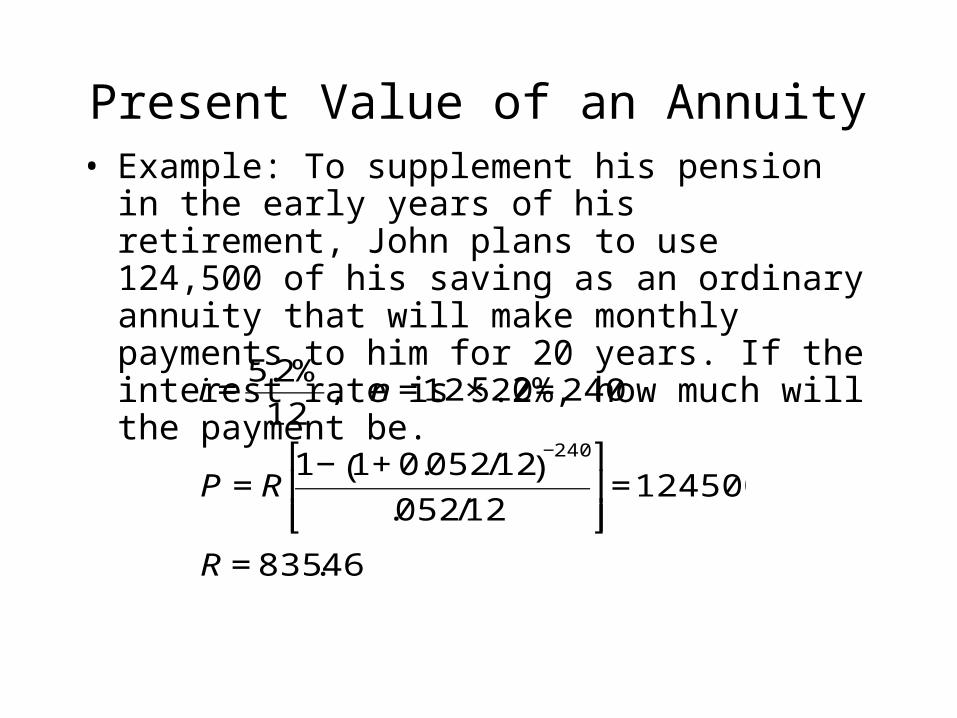

Present Value of an Annuity• Example: To supplement his pension in the early years

of his retirement, John plans to use 124,500 of his saving as an ordinary annuity that will make monthly payments to him for 20 years. If the interest rate is 5.2%, how much will the payment be.

€

i =5.2%

12, n =12 × 20 = 240

P = R1− 1+ 0.052 /12( )

−240

.052 /12

⎡

⎣ ⎢ ⎢

⎤

⎦ ⎥ ⎥=124500

R = 835.46

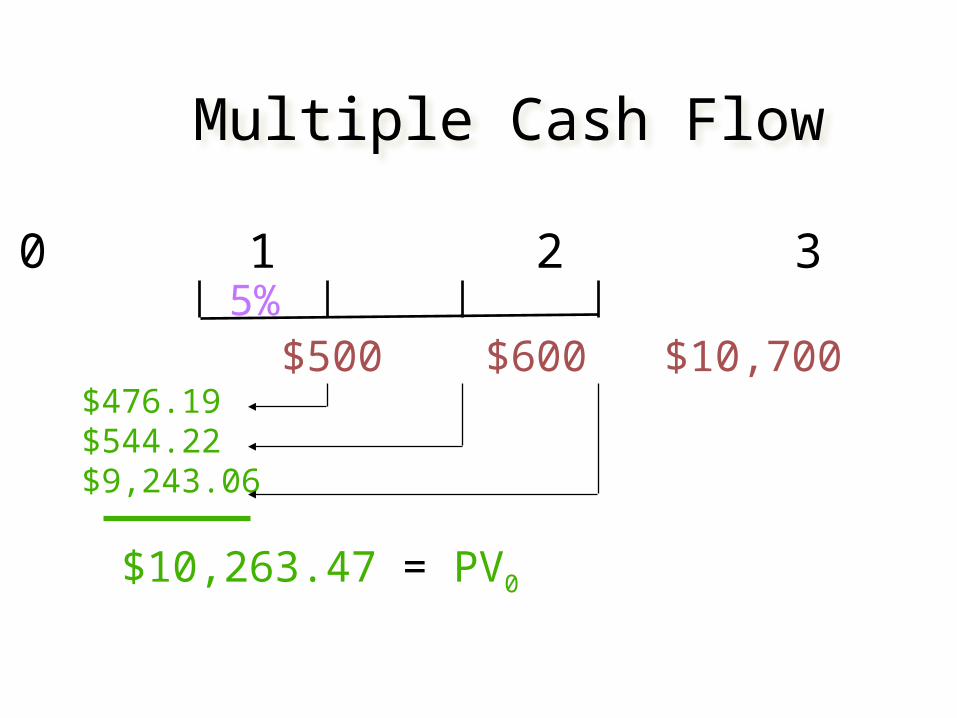

Multiple Cash Flow

0 1 2 3

$500 $600 $10,7005%

$476.19$544.22$9,243.06

$10,263.47 = PV0

To compare amounts of money at different times

• Discount amounts to present values • Calculate a net present value: Net present value = sum of discounted revenues – sum of discounted costs

Figure 8.8 Calculation of net present values for the three projects in worked example 8.9

Figure 8.10 Iterative calculation of IRR, the internal rate of return which make NPV to be 0, and standard function, in worked example 8.11

Figure 8.12 Depreciated value of vans at Hamil Leasing in worked example 8.13

Summary of Formulae

• Future value of a lump sum: FV = PV(1 + i)n

• Present value of a lump sum: PV = FV / (1+i)n

• Future value of annuity

• Present value of annuity

in

n

sRi

iRS

11

€

P = R1− 1+ i( )

−n

i

⎡

⎣ ⎢ ⎢

⎤

⎦ ⎥ ⎥= R ⋅a

n i

Break Even Point

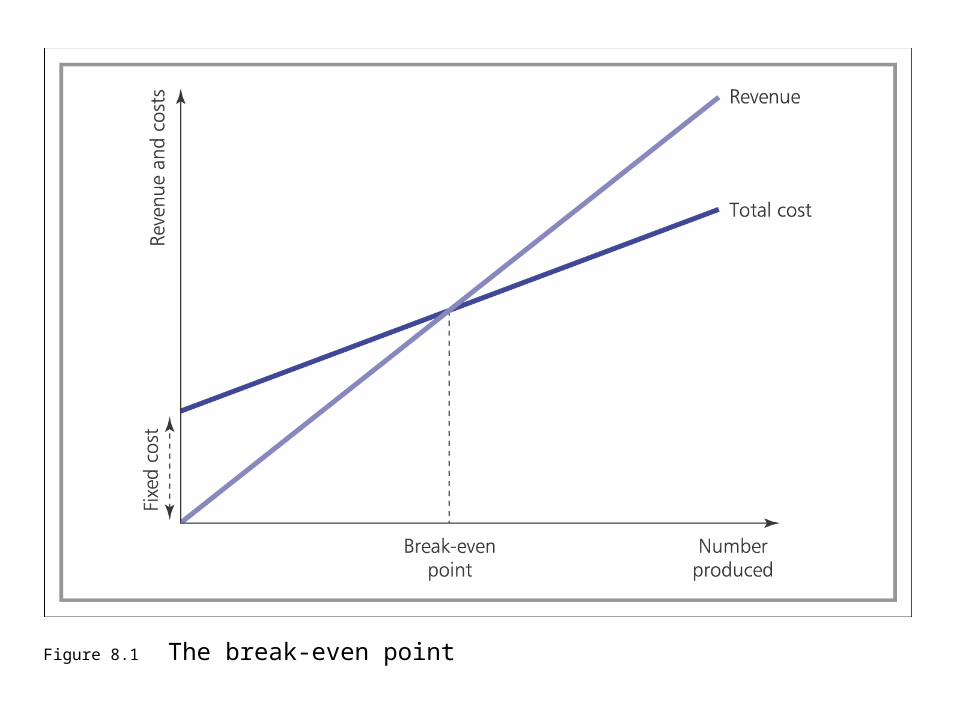

Figure 8.1 The break-even point

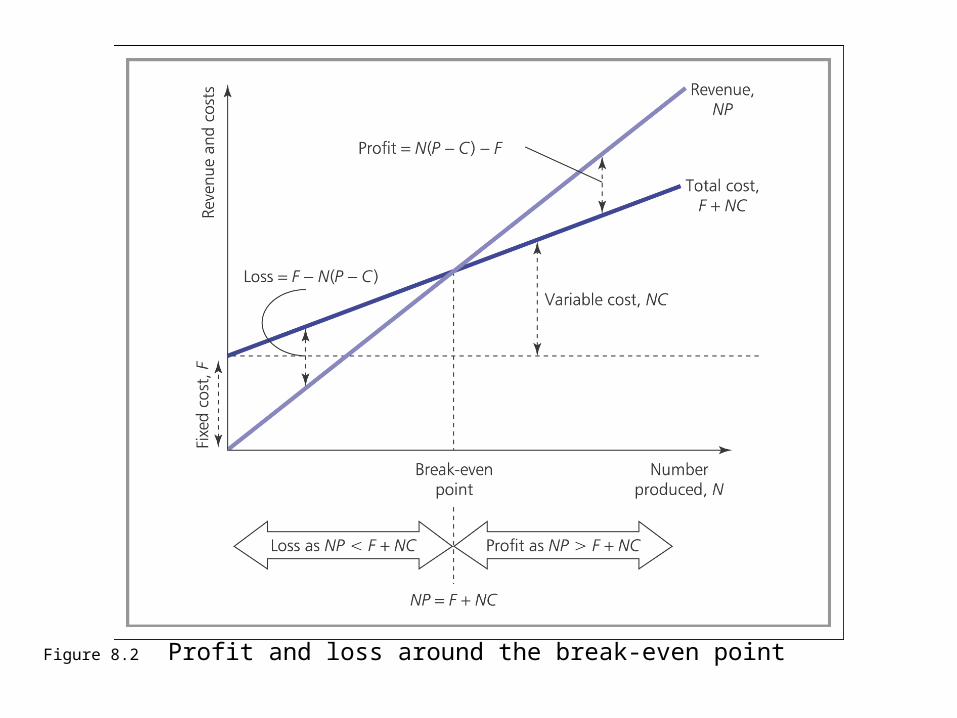

Figure 8.2 Profit and loss around the break-even point

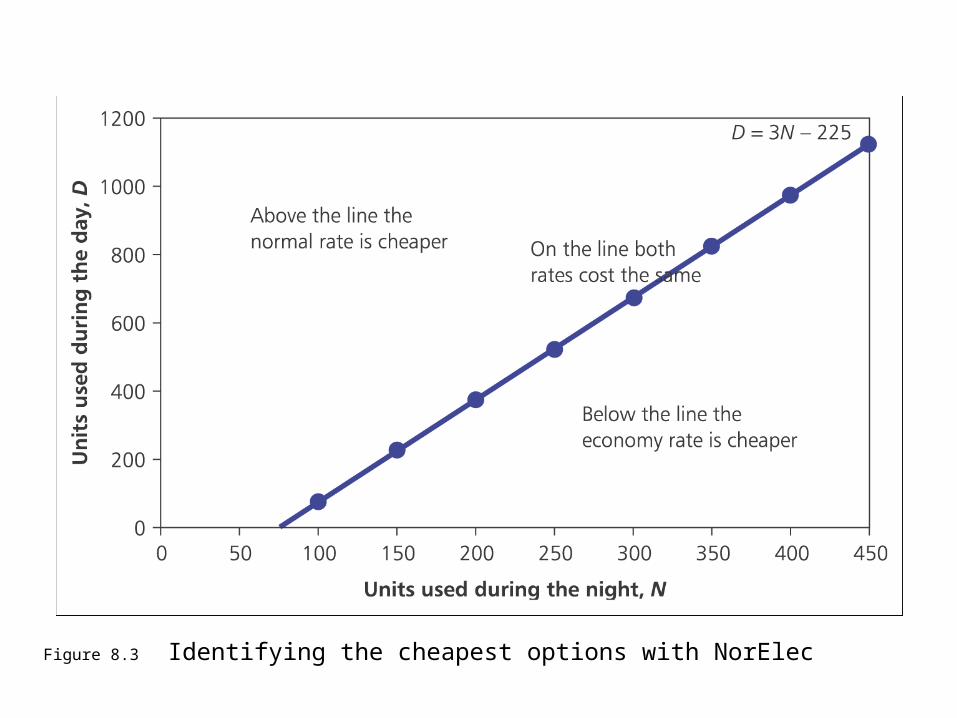

Figure 8.3 Identifying the cheapest options with NorElec