Chapter 1 Notes Economics - the study of how people seek to satisfy their needs and wants by making choices. I NEED it, or I WANT it! Need is food, shelter, clothes, water, etc… something for your survival. Want is cable TV, cell phone, laptop, Coach bag… something not

Transcript

Chapter 1 NotesEconomics- the study of how people seek to satisfy their needs and wants by making choices.

I NEED it, or I WANT it!

Need is food, shelter, clothes, water, etc… something for your survival.

Want is cable TV, cell phone, laptop, Coach bag… something not needed for survival

Chapter 1 NotesScarcity versus Shortage:

Scarcity implies limited quantities of resources to meet unlimited needs.

Shortage occurs when producers will not or cannot offer goods or services at current prices.

Basically scarcity always exists b/c resources are limited and shortage is like the hot item during the holiday shopping season…they are always out!

Chapter 1 NotesThe factors of production:

1) Land- natural resources used to produce

2) Labor- effort devoted to work

3) Capital- anything used to produce goods1) Physical Capital-building, tools, etc.

2) Human Capital-knowledge, skills, etc.

Chapter 1 NotesEntrepreneurs

An ambitious person who combines land, labor, and capital to create and market new goods and services.

Bill Gates, Henry Ford, or even the new store owner around the corner are all examples.

Chapter 1 NotesAt its core, Economics is about solving the

problem of scarcity.

EX:The amount of land, labor, and capital to make French

Fries can determine how many pairs of jeans you make. Each one takes all three factors of production. But each one is limited.

An entrepreneur will have to determine how much land to use for the jeans (cotton) and how much to use for the fries (potatoes), and….. You get the picture?

Chapter 1 NotesOpportunity Cost

1) Individual- spending more time at school/work means less time watching TV.

2) Business- Farmer planting cauliflower cannot use the same land at the same time to grow broccoli.

3) Society- Guns or Butter… the steel used to make a tank (guns) is no longer available for building the dairy equipment to make butter (butter).

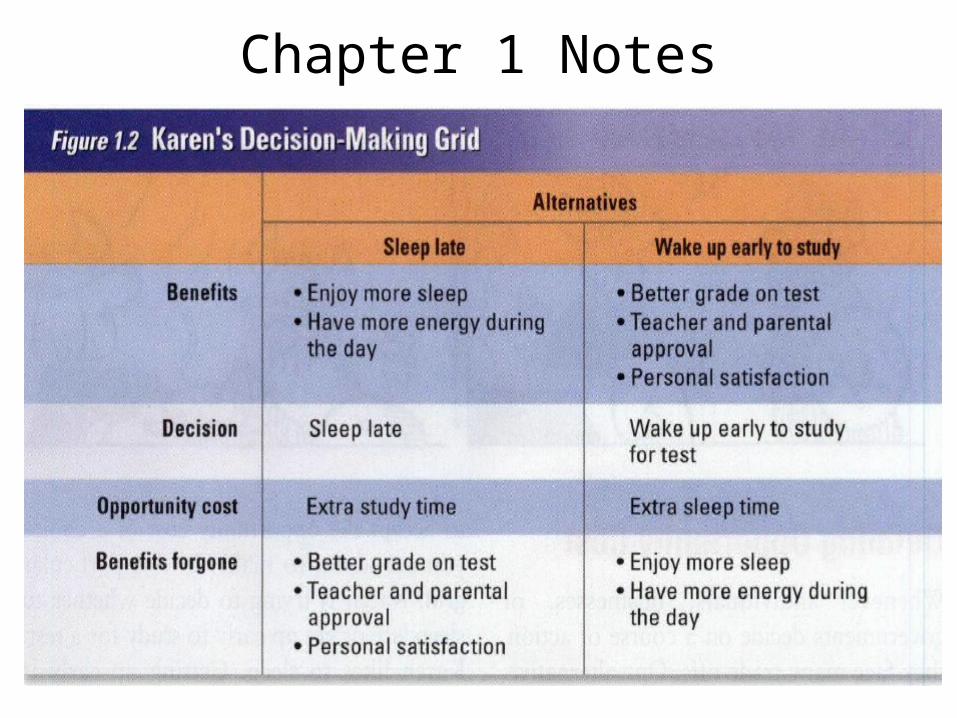

Chapter 1 NotesOpportunity cost- the most desirable

alternative given up as a result of a decision.

If a government decides to produce more “guns,” then “butter” is the opportunity cost.

Basically it is whatever you were willing to sacrifice between two more decisions…that is your opportunity cost.

Chapter 1 Notes

Chapter 1 Notes

Thinking at the Margin- deciding whether to do or use one additional unit of some resource.

So, what you could have got done with that extra hour of study or that extra hour of sleep…or what you didn’t get done with that extra hour of sleep or that 1 less hour of study.

Now you are making a Decision on the Margin.

Chapter 1 Notes

Chapter 1 Notes

Production Possibilities Curve

A graph that shows alternative ways to use an economy’s resources.

So, this is a graph that tells you how many shoes and watermelons you can make together or just one of each.

Chapter 1 Notes

Chapter 1 Notes• Production Possibilities Frontier

– The line on a production possibilities graph that shows the maximum possible output.

Once you are given a set of data saying what products and how many of each is capable of being produced, then you can plot your points, and find the Productions Possibilities Frontier.

Chapter 1 Notes

Chapter 1 Notes• A production possibilities frontier means the

economy is running at maximum efficiency.

– Efficiency- using resources in such a way as to maximize the production of goods and services.

• Any point inside the production possibilities curve means an underutilization of resources.

– Underutilization- using fewer resources than an economy is capable. Not at highest potential!