96

Chapter 1: The Shipping Documentation System

| Date post: | 15-Jan-2016 |

| Category: |

Documents |

| Upload: | candace-pearson |

| View: | 221 times |

| Download: | 0 times |

Chapter 1: The Shipping Documentation

System

Module Outline

• 14 Lecturing + Tutorial Sessions (Face-to-face)

• 1 Quiz (10%) lesson 1-5 Week 6• 1 Test (15%) lesson 1- 9 Week 10• 1 group assignment (25%) Week 9• 1 Final written examination (50%)

Total = 100%

At the end of the module, the student is expected to be able to:

• Describe the concept and principles of shipping documentation for import and export

• Explain the nature, type and various bill of lading, this also includes clauses in bill of lading

• Define and differentiate the various International Commercial Terms (INCOTERMS)

• List and explain the various cargo, port and custom documents

1.1 Introduction to shipping documentation

Introduction to shipping documentation

In international settlements, all relevant parties deal with documents, not goods.

1) Banks pay against documents;2) Exporters receive payment by handling over the

required documents;3) Importers pay by virtue of documents. The documents called for by a payment method

differs according to the nature of the transaction, the goods and the countries of exporters and importers, etc..

– functions Evidence for the exporter to fulfill the sale contract; representation of the goods; financing means.

– Requirements: accurate, complete, timely, tidy • Requirements for making documents (Article20b);• Requirements for signatures in documents;• Requirements for the number of original documents and

copies (article20c);• Requirements for authentication (article20d)• Requirements for issuance date (article22).

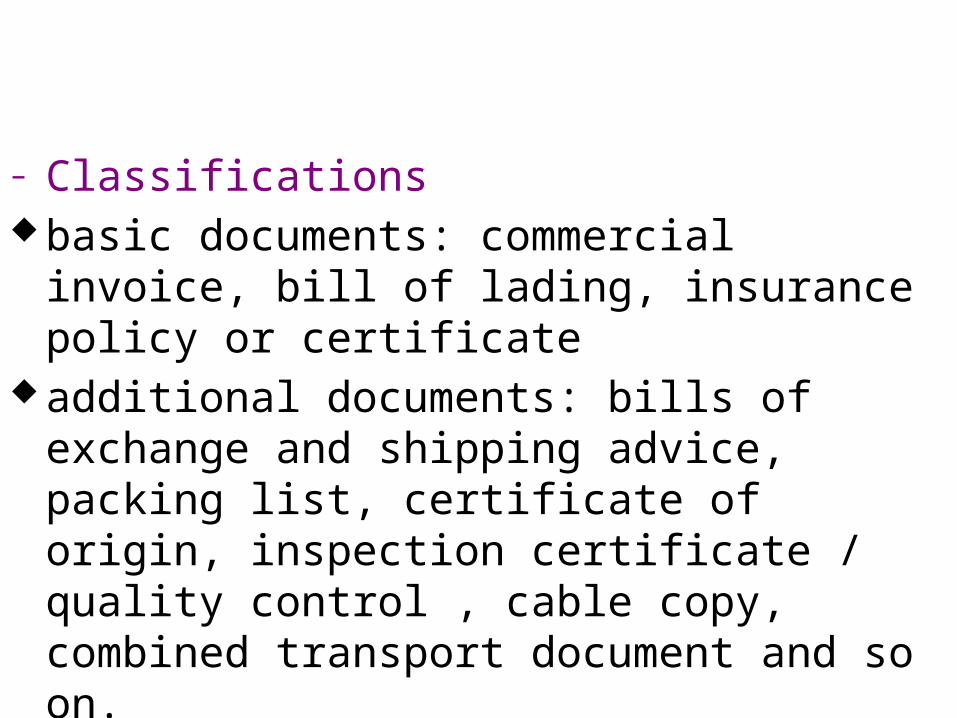

– Classifications basic documents: commercial invoice, bill of lading,

insurance policy or certificate additional documents: bills of exchange and

shipping advice, packing list, certificate of origin, inspection certificate / quality control , cable copy, combined transport document and so on.

Commercial invoice– Definition A commercial invoice is the key accounting

document describing the commercial transaction between the buyer and the seller, which gives details of the goods, service, price, quantity, settlement terms and shipment.

functionsⅠIt is evidence for the importer to check goods and make payment.

• ⅡThe commercial invoice is the basis for the importer’s Customs' identification, classification, duty/tax assessment, and final approval of entry of the goods.

• Ⅲ In the absence of a separate contract of sale , the invoice will take on added importance as the confirmation of the terms of the arrangements between the parties.

• ⅣIn the absence of a separate bill, the importers or the issuing bank will make payments according to the invoice.

• Ⅴ The commercial invoice is the basis for exporters to collect and record.

• Ⅵ The commercial invoice is the basis for the exporter’s foreign Customs' identification, classification, duty/tax assessment, and final approval of delivery of the goods.

– items

• the word “invoice” or “commercial invoice”;• name and address of the exporter, importer, and

consignee, if any;• place and date of issuance;• L/C (Letter of Credit; contract) No. and date;• terms of delivery and payment;

• items relative to shipment: departure date, the name of vessel/flight, the place of receipt and the place of destination;

• shipping marks, goods description, quantity of goods, price and amounts; (article 39)

• signature of the exporter;• other references.

• other types of invoice customs invoice: prepared by exporter for the importing

customs to ascertain the original price and avoid dumping.

consular invoice: an invoice covering a shipment of goods certified in the country of export by a local consul of the country for which the merchandise is destined.

legalized invoice: similar to consular invoice. pro forma invoice: a predecessor of commercial invoice. sample invoice: for the importer to apply for tax reduction

or exemption when importing samples of goods.

packing list– Definition: Packing list (P/L) is an extension of

commercial invoice, which provides the complete packing details of goods.

– Functions the evidence for importers to check and accept

the goods; The evidence for the importer’s customs to check

particular packages.– Classification: packing list, weight memo (list), and

size memo (list).

transport documents– Commercial terms International Rules for the Interpretation of Commercial

Terms, INCOTERMS,1936, 1967, 1976, 1980, 1990, 2000.• functions: the division of transport cost; the division of transport risks; the handling liabilities: furnishing of documents, export

and import clearance, and notifications to the parities concerned.

• Incoterms do not deal with: transfer of property/legal title; breach of contract/deficiency in the merchandise; terms of payment; place of jurisdiction.

• elements the precise point of goods’ transference; a clear definition of the expenses; the time and the place for the actual delivery of goods FrameworkGroup E: EXW, or EX Works means that the seller makes the goods

available to the buyer at the seller’s own premises.Group F: main carriage unpaid, including:

FCA, Free Carrier (…named place), title and risk pass to the buyer including transportations and insurance costs when the seller delivers goods cleared for export to the carrier nominated by the buyer at the named place.

FAS, Free Alongside Ship (…named port of shipment), title and risk pass to the buyer including payment of all transportation and insurance cost when the goods are placed alongside the vessel at the named port of shipment by the seller;

FOB, Free on Board (…named port of shipment), title and risk pass to buyer including payment of all transportation and insurance cost when the goods pass the ship’s rail at the named port of shipment.

• Group C, main carriage paid, including: CFR, Cost and Freight (…named port of destination), the

seller pays the costs and freight necessary to bring the goods to the named port of destination but the risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time of delivery, are transferred from the seller to the buyer;

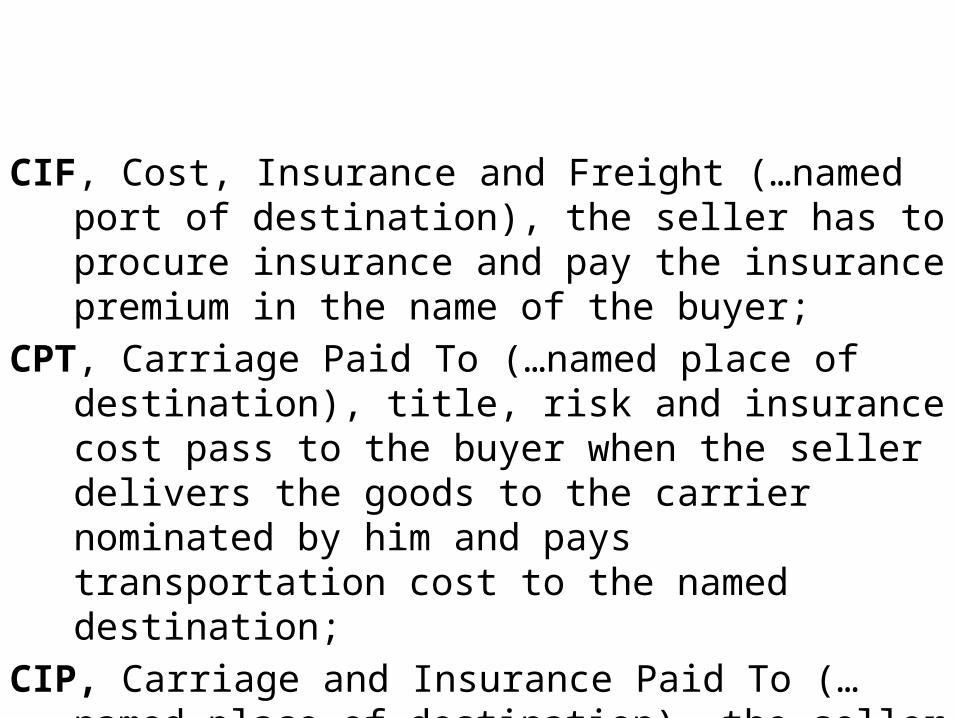

CIF, Cost, Insurance and Freight (…named port of destination), the seller has to procure insurance and pay the insurance premium in the name of the buyer;

CPT, Carriage Paid To (…named place of destination), title, risk and insurance cost pass to the buyer when the seller delivers the goods to the carrier nominated by him and pays transportation cost to the named destination;

CIP, Carriage and Insurance Paid To (…named place of destination), the seller has to procure insurance during the carriage.

• Group D, arrival of the goods, including:DAF, Delivered At Frontier (…named place), title, risk and

responsibility for import clearance pass to buyer when goods are placed at the disposal of the buyer at the named point and place at the frontier;

DES, Delivered Ex Ship (…named port of destination), title, risk and responsibility for vessel discharge and import clearance pass to buyer when the goods are placed at the disposal of the buyer on board the ship at the named port of destination;

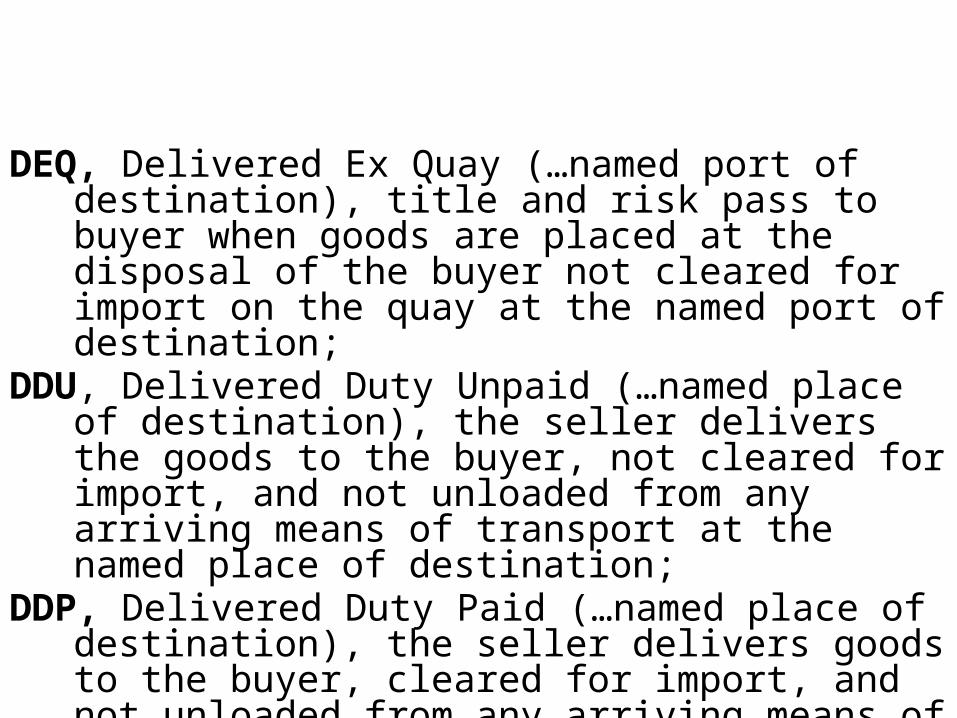

DEQ, Delivered Ex Quay (…named port of destination), title and risk pass to buyer when goods are placed at the disposal of the buyer not cleared for import on the quay at the named port of destination;

DDU, Delivered Duty Unpaid (…named place of destination), the seller delivers the goods to the buyer, not cleared for import, and not unloaded from any arriving means of transport at the named place of destination;

DDP, Delivered Duty Paid (…named place of destination), the seller delivers goods to the buyer, cleared for import, and not unloaded from any arriving means of transport at the named place of destination.

– Definition of transport documents Transport documents are documents that represent the

goods in transport or prove the goods have been received for transport.

– Bill of Lading (B/L)• definition: A bill of lading is a document issued by a carrier to a

shipper, signed by the captain, agent, or owner of a vessel, providing written evidence regarding receipt of the goods, the conditions on which transportation is made, and the engagement to deliver goods at the prescribed port of destination to the lawful holder of the bill of lading.

• Characteristics Requisite in form; Written document; Transferable documents; Documents to deal with goods; Documents with value.• Functions A receipt of goods from the shipping company to the

exporter; Evidence of the transport contract for carriage between the

exporter and the carrier; Document of title.

• itemsitems on the obverse: the carrier; the shipper; the consignee; notify party; vessel, port of loading, port of discharging and

transshipment, if any; marks and No.; description of packages and goods; freight;

place and date of issue; shipment clause; without information clause.Items on the reverse: Definition clause; Jurisdiction clause; Duration of liability; Package and marks; Inaccuracy in particulars furnished by shipper; Lien clause; Transshipment clause; on-deck cargo, live animals and plants.

Classificationsshipped on board B/L & received for shipment B/L shipped on board B/L: a B/L issued only after the goods

have actually been shipped on board the vessel; received for shipment B/L: a B/L issued to acknowledge

receipt of shipment before cargo loading or before official original bill of lading is issued.

clean B/L & unclean B/L Clean B/L: a B/L in which there is no indication of damage

to the goods and packaging;Unclean B/L: a B/L in which there is indication of damage to

the goods or packaging.

straight B/L, open B/L (blank B/L) & order B/L Straight B/L: a non-transferable B/L which indicates

the carrier will deliver the goods to the consignee. open B/L: a B/L which indicates no specific

consignee and the goods will be delivered to anyone who holds the B/L;

order B/L: a title document to the goods, issued "to the order of" a party, usually the shipper, whose endorsement is required to effect the negotiation.

direct B/L, transshipment B/L, through B/L

direct B/L: issued when goods are shipped from the port of loading directly to the port of discharge without transshipment;

transshipment B/L: issued when the goods are transferred from one ship to another at a named transshipment port; (article 23 b, c)

through B/L: the carriage of goods from the port of loading to the place of destination are taken by two or more than two carriers, and the bill of lading to cover the entire carriage is issued by the first carrier.

liner B/L & charter party B/L Liner B/L: a B/L which indicates that goods are being

transported on a ship that travels on a scheduled route and has a reserved berth at destination;

charter party B/L: a B/L issued by the hirer of a ship to the exporter, subject to the contract of hire between the ship’s owner and hirer.

long form B/L & short form B/L short form B/L: a B/L that doesn’t contain the full details of

the contact of the carriage on the back.

anti-dated B/L, advanced B/L & stale B/L anti-dated B/L: according to the request of shipper, the

carrier signs a B/L in which the date of issuance is earlier than the actual date of shipment in order to comply with the requirements of L/C;

advanced B/L: a shipped on board B/L issued by the carrier when the goods haven’t been shipped on board.

stale B/L: a B/L which arrives after the consignment arrives at the final destination. Because the B/L is not available, the goods cannot be handed over to the consignee.

– other transport documents• sea waybill or ocean waybill: issued by the shipping

company covering port-to-port shipment, not a title document.

• multi-model transport document: a B/L covering two or more models of transport, such as shipping by rail and by sea.

• air transport document: air waybill & house air waybill air waybill: issued by the air carrier, a document evidencing

shipment or dispatch or receipt of goods.

• Road or inland waterway transport documents;• Cargo receipt/railway bill;• Courier receipt and post receipt.

insurance documents– Definition: An insurance document is a contract

whereby the insuer undertakes to indemnify the assured in a manner and to the extent thereby agreed, against certain losses to cargo while in transmit.

– functions:• evidence of insurance contract;• evidence of compensation.

• types:insurance policy: a document issued by an insurance

company, covering the goods being shipped against specified risks during the whole or part of the journey between the seller and the buyer.

insurance certificate: a document issued to the insured certifying that insurance has been effected and the version of the provisions of the policy is abbreviated.

combined certificate or risk note: a stamped invoice as an evidence of insurance.

open policy: an agreement between the insurer and the insured before the goods are shipped in case that the buyer covers the risks lest the insurance might be delayed or missed.

insurance declaration: after the goods are shipped, the buyer should report to the insurer the details of shipment in insurance declaration.

cover note: a document issued to give notice that insurance has been placed pending the production of a policy or a certificate. (article 34 c, d)

• itemsInsurer; (article 34 a)the insured;subject matter;amount insured; (article 34 f)items relative to shipment;conditions: basic risks: free from particular average (F.P.A.), with average (W.A.) & all

risks. General additional risks: theft pilferage and non-delivery, risk of fresh

water rain damage, risk of shortage, risk of inter-mixture contamination, risk of leakage; risk of crash breakage; risk of taint of odor, risk of sweat and heating, risk of hook damage, risk of breakage of packing, risk of rust.

Special additional risks: failure to deliver risk, import duty risk, on deck risk, rejection risk, aflation risk, inspection risk, war risk.

Claim payable at;Surveyor;Date and place of issue. (article 34 e)– other documents• inspection certificate: a document issued by an authority,

as stated in the documentary credit, indicating that goods have been inspected prior to shipment and the results of the inspection.

Key points related to the Inspection Certificate: The description and mark of the goods must be the same

as those mentioned in the commercial invoice and other documents to ascertain that the goods inspected are exactly those exported;

The wording on the inspection certificate must be exactly the same as those mentioned in the invoice and must be in compliance with the terms and conditions of the credit;

The inspection date must be earlier than B/L’s date or conform to that stipulated in the letter of credit.

• origin certificate: a document issued by an authority, as stated in the documentary credit stating the country of origin of goods.

representative form: Generalized System of Preference Certificate of Origin, a certificate used to obtain the treatment of preference customs duty imposed by the developed country in the developing countries.

• Export license: a document prepared by a government authority of a nation granting the right to export a specific quantity of a commodity to a specified country.

• Beneficiary’s statement: a statement issued and signed by the beneficiary, certifying that he has done some work according to the stipulations in the credit.

• Cable copy

– key points in review Incorrect amounts or currency in bill of exchange; Incorrect title in invoice or inconsistence of goods’

description with L/C; Overloading or underloading; Inconsistence of description of goods among documents; Incomplete documents; Omission of signature or stamp in documents; Omission of endorsement; Overdue loading or overdue presenting documents;.

Clause as to partial shipment or transshipment is violated; Inconsistence of the freight in transportation documents with trade

terms; Overdraft; Conditional requirements specified in the L/C aren’t satisfied; Corrections in documents haven’t been signed or stamped; Inconsistence of the type of transport documents with L/C; Documents presented obeyed the original L/C after the L/C has

been revised; Inconsistence of issuing date in documents.

A System of payment designed to eliminate the difficulties and risks involved in having large sums of cash, gold or silver always and immediately available and to overcome problems with transporting them over dangerous distances.

Grew out of Merchant practice. Later codified in statute.

All negotiable instruments are transferable….bills of exchange, cheques, bearer debentures, promissory notes, some bonds….but not all things transferable are negotiable….share certificates, money orders, IOUs.

As well as payment method, extensive use in liquidity management (ability to discount) and in financing (commercial bill acceptance or paper facilities).

CONCEPT OF NEGOTIABILITY

Characteristics of Negotiable Instruments

• Title is capable of transfer by mere delivery (or where payable “to order”, by endorsement and then delivery)

• No requirement for notice of transfer to be given to person liable. (Contrast s. 12 Conveyancing Act)

• Holder can sue in his/her own name. • Holder who takes in good faith and for value takes it free of

equities and may obtain better title than transferor. • A presumption of bona fides and consideration.

Negotiable instruments -illustrations of use-payment

DOCUMENTARY COLLECTION FOR AN IMPORTER

What is it? A documentary collection consists of a Bill of Exchange plus various shipping documents relating to the goods you are importing…invoice, bill of lading, other transport documents, insurance policy…delivered to you-via your agent bank. These documents are released to you in exchange for:·On the spot payment (sight documentary collection)·Your endorsing the Bill of exchange as a promise to make payment at a future date, as negotiated and specified in the Bill of exchange (term documentary collection)

•Who initiates it? Your supplier, once terms have been agreed with you usually via their bank to yours.

Documentary collection

2. Shipment

8. Buyer (importer) 3. Seller (exporter)

7. Presenting bank 5. Remitting Bank

1. Contract of Sale

9a. Payment

9b. Shipping documents

4. Lodgement of shipping documents

11. Payment6. Shipping documents

10. Payment

Documentary Collection

1. Contract is negotiated between buyer seller.2. Method of payment -documentary collection, shipment prior to payment.3. Exporter prepares shipping documents, BOE and instructions4. Documents lodged with remitting bank, who acts in accordance with

instructions from exporter5. Remitting bank examines documents 6. Remitting bank dispatches documents to presenting bank.7. Upon receipt shipping documents, presenting bank presents BOE to importer8. Importer will either agree to make payment or refuse9a. If importer agrees to payment, payment or acceptance of BOE9b. Shipping documents released to importer on payment or return of accepted

BOE10. Presenting bank makes payment to remitting bank11. Remitting bank makes payment to exporter.

USING A BILL OF EXCHANGE when structuring

transactions/settlements

A in Australia owes B in NZ AUD 100,000 for goodsB owes C in Australia AUD 100,000 for goods

To satisfy B’s debt to C, B could assign the debt owed to B by A to C by means of the statutory machinery for assignment of choses in action (NSW Conveyancing Act)

Instead of A sending currency to B and B sending money to C, B could send a written order to A to pay C the amount of B’s debt.The drawing of a BofE is distinct from the underlying sale of goods.

1.2 The modern trading system

Trade Policy Development1.2.1. Understanding of trade policy1.2.2 Institutes of the international trade system

Part I Basic Concepts• 1. Definition• international trade: the exchange of goods and

services across national boundaries/borders.

• 2. Major participants in international trade— the buyer that purchases the products

(importer)— the seller that provides the products (exporter)— banks that facilitate the payment of the

transaction

Part I Basic Concepts• 3. Classification– import vs. export (directions of the movement

of commodity traded)– tangible trade vs. intangible trade1) tangible trade: the exchange of tangible goods

(to carry out importing/exporting customs formalities)

2) intangible trade: the exchange of intangible goods, such as services and intellectual property rights

– direct trade vs. indirect trade1) direct trade: the producing country sells the

goods directly to the consuming country. (transit country, transit trade, transit duty)

2) indirect trade: the producing country sells the goods to a third country first and then the third country resells the goods to the consuming country. (middleman, entrepot trade)

4. Policies

• Manchesterism (free trade policy) It is aimed to assure that the market is free to

function in an unconstrained manner by eliminating the restrictions or removing the barriers to effective operation of “invisible hand” of the market and the goods is traded freely between nations to increase the wealth of both the buying and the selling nations.

4. Policies

• Protectionism (protective trade policy) It means a trade policy by which a

government sets up controls over its import trade for the purpose of protecting its economy (esp. agriculture and infant industries) from foreign competition and provides preferential treatment and subsidies to its exporters or exporting firms.

57

1.2.1. Understanding of trade policy

• Question: • What are the key players of

international trade and investments?

58

1.2.1. Understanding of trade policy

• Question: • Do you like

shopping?• Who do you do your

shopping?

59

1.2.1. Understanding of trade policy

• Answer: • You do your

shopping in order to make decisions to discriminate

60

1.2.1. Understanding of trade policy

Questions of access, protection and discrimination – Discrimination is the basis of choice, that is,

choosing one thing over another thing for whatever reason.

– Most trade policy involves decisions to discriminate: to discriminate between goods or groups domestically or between services suppliers from different countries.

61

1.2.1. Understanding of trade policy

• Trade policy involves – values, – preferences,– priorities, and – an institutional setting and social context

• that can vary from country to country.• Social context, in particular, can have an

important bearing on how national values, preferences and priorities are pursued.

62

1.2.1. Understanding of trade policy

• Commercial Interests - Trade policy is designed to meet a country's commercial interests.

• Question: what are country’s commercial interest? Who decides?

• Social Interests - An increasing reality for trade officials is the need to respond to broader societal interests.

63

1.2.1. Understanding of trade policy

• Legal Norms and Ideas are critical to putting trade policy into practice.

• They involve the implementation of rules and the practice of diplomacy.

64

1.2.1. Understanding of trade policy

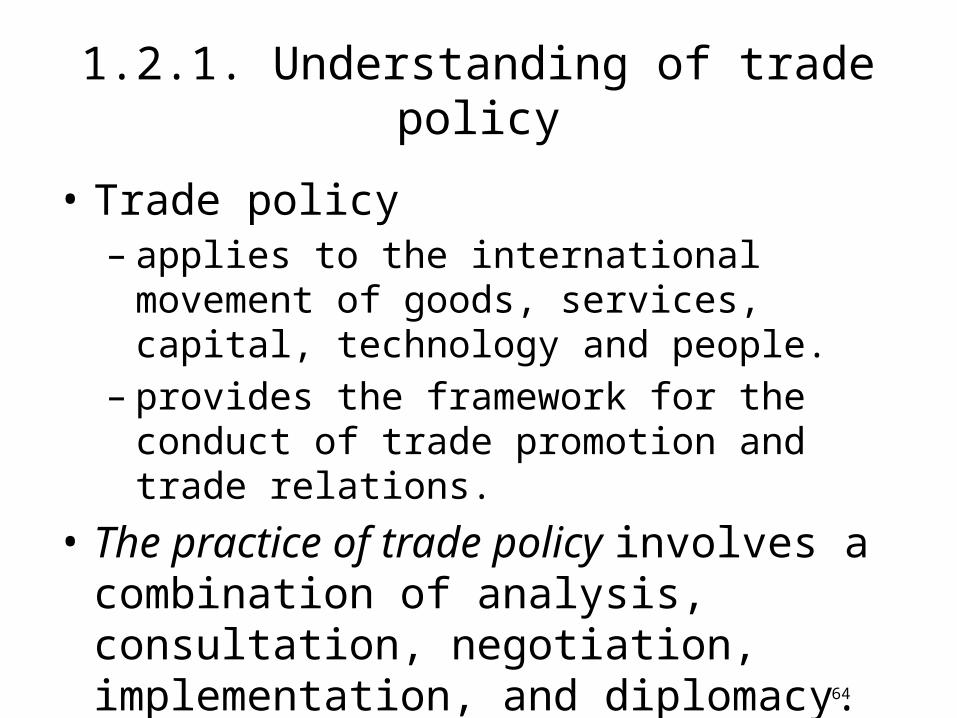

• Trade policy– applies to the international movement of goods,

services, capital, technology and people.– provides the framework for the conduct of trade

promotion and trade relations. • The practice of trade policy involves a

combination of analysis, consultation, negotiation, implementation, and diplomacy.

65

1.2.1. Understanding of trade policy

• Question:– What are the goals of consultation process?

1.2.1. Understanding of trade policy

66

stability and predictability in government policy and trade and investment circumstances

1.2.1. Understanding of trade policy

• Institutional context– Government policy professionals operate

within an institutional setting that influences,

– constrains, and conditions how they address and resolve issues that cross their desk

67

1.2.1. Understanding of trade policy

• Assignment:– compare political and institutional

settings within operate the governments of

• United States,• Canada,• Germany, and • China

68

1.2.1. Understanding of trade policy

• The role of international organizations– International and national institutions

provide permanence and stability in addressing differences and in pursuing competing priorities.

– Positions and approaches adopted by most governments reflect not only their interests, objectives, and preferences, but also the political/institutional setting within which governments operate

69

1.2.1. Understanding of trade policy

• Question:– Why countries enter international trade

agreements/join international organizations?

1. to tell other countries what to do2. because they have week governments and

cannot deal with many issues themselves3. to promote economic growth and

development

70

1.2.1. Understanding of trade policy

• The role of international organizations– Different countries have different objectives —

e.g., Canada/US/Japan/EU/developing countries/Caribbean countries/transitional economies — all have various objectives, approaches, and preferences that may require negotiations to resolve.

– The result is compromise between ideals and reality and the imperfection that is part of reality.

71

72

1.2.1. Understanding of trade policy

The Role of International Organizations• When countries enter into trade agreements

they agree to such broadly-based objectives as increased economic welfare, and promotion of international cooperation.

• However, countries also enter trade agreements for a variety of specific, subjective reasons that reflect a country's particular political and economic profile.

73

1.2.2. Institutes of international trade system

• Question:– What are the institutions of international trade

system?

74

1.2.2. Institutes of international trade system

• Institutions provide permanence and stability in a changing world, as well as a forum for states to discuss their concerns. Some of the ideas and practices that support modern organizations for international cooperation originated with the League of Nations (which would later emerge as the United Nations).

• There are now some 300 intergovernmental organizations devoted to economic issues alone.

75

1.2.2. Institutes of international trade system

• At the core are the Bretton Woods agreements laid the groundwork for the establishment of:– World Bank – International Monetary Fund (IMF), – International Trade Organization (ITO).

76

1.2.2. Institutes of international trade system

The United Nations has also created a number of specialized and technically oriented institutions to deal with a range of economic issues:

• Labour - International Labour Organization - ILO • Food - Food and Agriculture Organization -FAO • Aviation - International Civil Aviation Organization - ICAO • Customs - World Customs Organization - WCO • Intellectual Property - World Intellectual Property

Organization - WIPO

77

1.2.2. Institutes of international trade system

• The Quad • Some of the most difficult negotiations have

needed an initial breakthrough in talks among the four largest members:

• Canada • European Union • Japan • United States

78

1.2.2. Institutes of international trade system

• European Communities• Association of South East Asian Nations (ASEAN) • MERCOSUR, the Southern Common Market • North American Free Trade Agreement: NAFTA • African Group, • Least-developed countries,• African, Caribbean and Pacific Group (ACP) • Latin American Economic System (SELA).

79

1.2.2. Institutes of international trade system

• The multilateral trade regime is complemented by dozens of regional and bilateral agreements and arrangements. Two regional agreements and arrangements are particularly important: the

• European Union (EU) and the North American Free Trade Agreement (NAFTA), in providing a basis for assessing alternative approaches to integration and liberalization.

• Both of these agreements illustrate various characteristics of regionalism. A wide range of other regional arrangements are currently extant. The WTO catalogs over 200 such arrangements

80

1.2.2. Institutes of international trade system

• Regionalism provides both positive and negative dimension in the further evolution of the global trade regime.

• Trade policy practitioners need to be aware of the dense network of specialized bilateral agreements addressing, e.g., investment, export credits, and double taxation.

81

1.2.2. Institutes of international trade system

• national governments and their related agencies, • private sector organizations (national and

international), • industry associations,• non-governmental organizations (NGOs), • labour unions, • universities and think tanks, • media organizations, • technical regulators and inspectors, • consumers, and many others

1.3 Principles and documentary practices relating to transshipment

Some goods remain in the same mode of transportation when passing through customs territories. Others, though, may be transshipped to other modes of transportation during the process of transit. Article V of the GATT does not currently make a distinction between these two cases. Article V, paragraph 1 states:

• Goods (including baggage), and also vessels and other means of transport, shall be deemed to be in transit across the territory of a contracting party when the passage across such territory, with or without trans-shipment, warehousing, breaking bulk, or change in the mode of transport, is only a portion of a complete journey beginning and terminating beyond the frontier of the contracting party across whose territory the traffic passes.

• “transhipment” means the Customs procedure under which goods are transferred under Customs control from the importing means of transport to the exporting means of transport within the area of one Customs office which is the office of both importation and exportation.

• However, it may be useful to have different requirements for goods in transit without transshipment than for goods in transit with transshipment. In the case of maritime countries, if goods in transit do not involve transshipment into different means of transportation within the Member country, a simple goods declaration and fairly simple set of service fees may be sufficient for transit procedures since there is only a minimal risk that the goods may be released into the transit country, and the services that the transit country authorities provides will be relatively small.

• On the other hand, for goods in transit which involve transshipment within the transit country, there may be a need for additional inspection and security measures to prevent the smuggling of goods in transit into the transit country as well as other illegal activities during the process of transshipment. It seems reasonable for the transit countries to require a minimal amount of additional paperwork and service fees

• In the case of landlocked countries, transit traffic, which may or may not involve trans-shipment, may cross many borders. Given the higher risk of the illegal release of transit goods, it may be necessary for these landlocked countries to implement more sophisticated risk management procedures compared to maritime countries that do not necessarily require border-crossing transits.

• Therefore, it may be useful to discuss the different requirements in each of these circumstances, and devise appropriate customs measures for each of these cases in order to minimize the burdens on the traders engaged in transit traffic, while still maintaining a reasonable degree of safety and order for the countries that these goods pass through.

1.4 Strategy in preparing shipping documents – import and export

• Prepare Shipping DocumentsIt is very important to consider the effects of duties, taxes, port handling fees and other customs charges when determining your shipment's total shipping charges. Depending on the content and the destination country, customs charges will affect the price your recipient is willing to pay for your product. Being able to calculate and communicate the "landed" cost upfront often save yours and your recipient's valuable time and money.

• Duties and TaxesAlmost all shipments crossing international borders are subject to the assessment of duties and taxes imposed by the destination country's government. This is done to generate revenue, protect local industries against foreign competition, or both. The duties and taxes normally must be paid before the goods are released from customs. A shipment's duty and tax amount may be based on:

• Product value• Trade agreements• Country of manufacture• Use of the product• The product's Harmonized System (HS) code

• Customs officials assess duties and taxes based on the declared value and the commodity descriptions provided on the FedEx International Air Waybill and the Commercial Invoice.

• Value Added Tax (VAT) / Goods & Services Tax (GST)A VAT is a form of indirect tax applied to the value of a product. In some countries, including Singapore, Australia, New Zealand and Canada, this tax is known as goods and services tax, or GST. Because it's a tax on consumer expenditure, businesses that are VAT-registered and fully taxable do not bear the final costs of VAT. Every member state of the European Union (EU) has a VAT.

• Responsibility for Paying Duties and TaxesDuties and taxes on your international shipment will automatically be billed to the recipient*, unless the shipper instructs FedEx otherwise. The shipper can usually select either the shipper, recipient or a third party as the payer when you complete the FedEx International Air Waybill or FedEx Expanded Service International Air Waybill. When the recipient is the payer, the FedEx office in the destination country will, in most cases, call to collect or invoice the duties and taxes that have been assessed. We do this to recover the funds that we have advanced on the payer's behalf.

* If the designated recipient refuses to pay the duties and taxes, shipper will be liable to pay any outstanding charges.

• Gathering Duty & Tax informationTo determine duty and tax information for your shipment is to identify the HS code associated with your product. To find the importing country's HS code is to use the Online Tariff Database at http://www.worldtariff.com/Gift Exemption for Duties and TaxesTo qualify for a gift exemption, your shipment must meet the following requirements:

• It must be sent person to person - with no company involvement or indication of involvement on the shipping documentation.

• The shipping documentation must clearly be marked "Unsolicited Gift" in addition to the commodity* name and the detailed description.

• The total value of the shipment must not exceed the values prescribed by the customs.

• *Except dutiable commodities

For more information on gift exemptions, please call FedEx Customer Service.

• Declared Value and Duties and TaxesCustoms officials use a shipment's declared value - the value the shipper declares on the goods being shipped - along with the description of the goods, to determine duties and taxes. This means it's very important to make sure that the declared value on the air waybill and commercial invoice is accurate. Inaccurate declared value is one of the most prevalent reasons for duty and tax disputes. A shipment's declared value represents the selling price or fair market value of the contents of the shipment, even if not sold (e.g. textile samples). This value is identified on the FedEx International Air Waybill and the FedEx Expanded Service International Air Waybill as the "Total Value for Customs" and must agree with the value shown on the Commercial Invoice.

• Temporary ImportsTemporary imports are goods imported for a specific purpose, then either exported back to the country of origin or destroyed. Examples of such shipments include goods to be repaired, trade show displays and tools of trade. Temporary Import Bonds are acceptable under FedEx International Broker Select Option, for initial import only.

• Processing a temporary import. Special procedures and documentation are often necessary to properly process a shipment that is to be imported temporarily. The procedures vary depending upon a number of factors including:

• The origin and destination of the shipment.• The classification of the goods.• The value of the goods.• The origin of the goods (country of manufacture)• Problems with Temporary Import Bond (TIB) shipments.

The two most common errors concerning TIB shipments are: • The failure to indicate on the shipping documentation that a Temporary Import

Bond is required.• The failure to properly document the export or destruction of the articles. When

this happens, the bond or security deposit is forfeited, and the importer bears the duty and tax expense.

• Checklist to Ensure a Dispute-Free Experience• Make sure that the Commercial Invoice and all other international shipping

documents are completed accurately and consistently. The Commercial Invoice is the first international shipping document you should complete, since it is the foundation document for all others and is the most common customs document required for clearing international shipments. Include the following required information: – Shipper's information: Contact name, company name, full address, telephone

number and business registration number.– Recipient's information: Contact name, company name, full address and telephone

number.– International air waybill number.– Country of manufacture: The country of original manufacture for each item in the

shipment.– Accurate and detailed description of shipment contents, including (but not limited

to): • What the item is.• What material the item is made of• What the HS code for the item is• The item's intended use• The part or serial numbers• The item's value per unit and in total

• Checklist to Ensure a Dispute-Free Experience• Make sure that the Commercial Invoice and all other international shipping

documents are completed accurately and consistently. The Commercial Invoice is the first international shipping document you should complete, since it is the foundation document for all others and is the most common customs document required for clearing international shipments. Include the following required information: – Shipper's information: Contact name, company name, full address, telephone

number and business registration number.– Recipient's information: Contact name, company name, full address and telephone

number.– International air waybill number.– Country of manufacture: The country of original manufacture for each item in the

shipment.– Accurate and detailed description of shipment contents, including (but not limited

to): • What the item is.• What material the item is made of• What the HS code for the item is• The item's intended use• The part or serial numbers• The item's value per unit and in total