88

Goldstein/Schnieder/Lay: Finite Math & Its Applications 1 Chapter 10 The Mathematics of Finance

| Date post: | 02-Jan-2016 |

| Category: |

Documents |

| Upload: | lillian-schroeder |

| View: | 16 times |

| Download: | 0 times |

Goldstein/Schnieder/Lay: Finite Math & Its Applications 1

Chapter 10

The Mathematics of Finance

Goldstein/Schnieder/Lay: Finite Math & Its Applications 2

Outline

10.1 Interest

10.2 Annuities

10.3 Amortization of Loans

10.4 Personal Financial Decisions

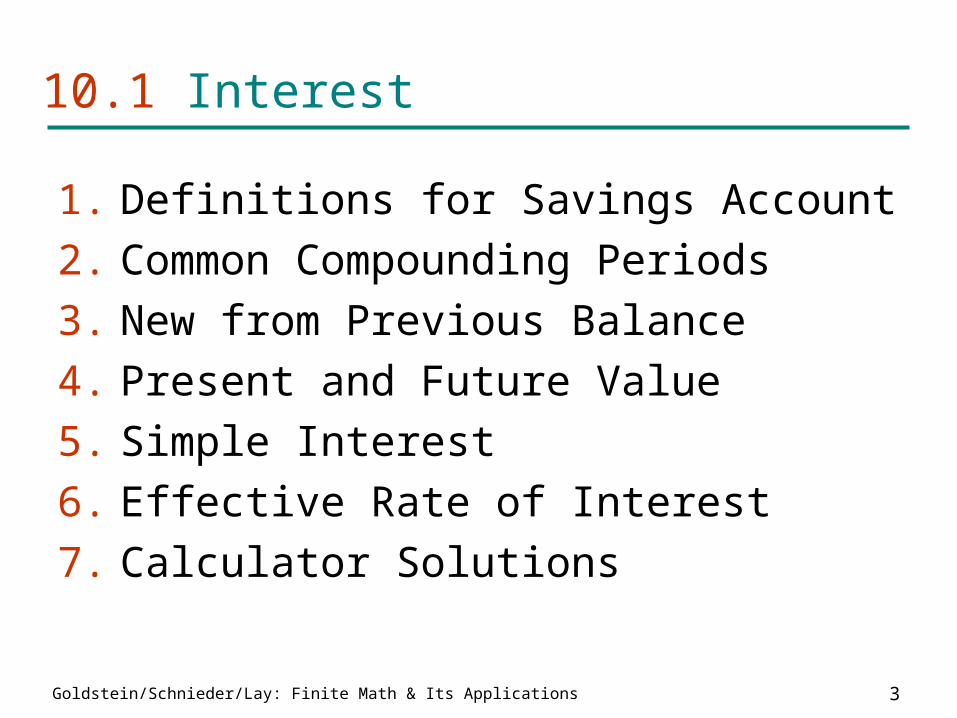

Goldstein/Schnieder/Lay: Finite Math & Its Applications 3

10.1 Interest

1. Definitions for Savings Account

2. Common Compounding Periods

3. New from Previous Balance

4. Present and Future Value

5. Simple Interest

6. Effective Rate of Interest

7. Calculator Solutions

Goldstein/Schnieder/Lay: Finite Math & Its Applications 4

Definitions for Savings Account

Interest is the fee a bank pays for the use of money deposited into a savings account.

The amount deposited is called the principal.

The amount to which the principal grows (after the addition of interest) is called the compound amount or balance.

If interest is compounded m times per year and the annual interest rate is r, then the interest rate per period is i = r/m.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 5

Example Definitions for Savings Account

For the passbook above, determine the principal, compound amount after 1 year, compound interest rate and annual interest rate.

Date Deposits Withdrawals Interest Balance

1/1/05 $100.00 $100.00

4/1/05 $1.00 $101.00

7/1/05 1.01 $102.01

10/1/05 1.02 $103.03

1/1/06 1.03 $104.06

Goldstein/Schnieder/Lay: Finite Math & Its Applications 6

Example Definitions - Savings Account (2)

The principal is $100.00.

The compound amount after 1 year is $104.06.

The compound interest rate is 1% since the interest earned in the first period, $1.00, is 1% of the principal.

Interest is compounded 4 times per year so the annual interest rate is 4·1% = 4%.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 7

Common Compounding Periods

Number of interest periods

per year

Length of each interest period

Interest compounded

1 1 year Annually

2 6 months Semiannually

4 3 months Quarterly

12 1 month Monthly

52 1 week Weekly

365 1 day Daily

Goldstein/Schnieder/Lay: Finite Math & Its Applications 8

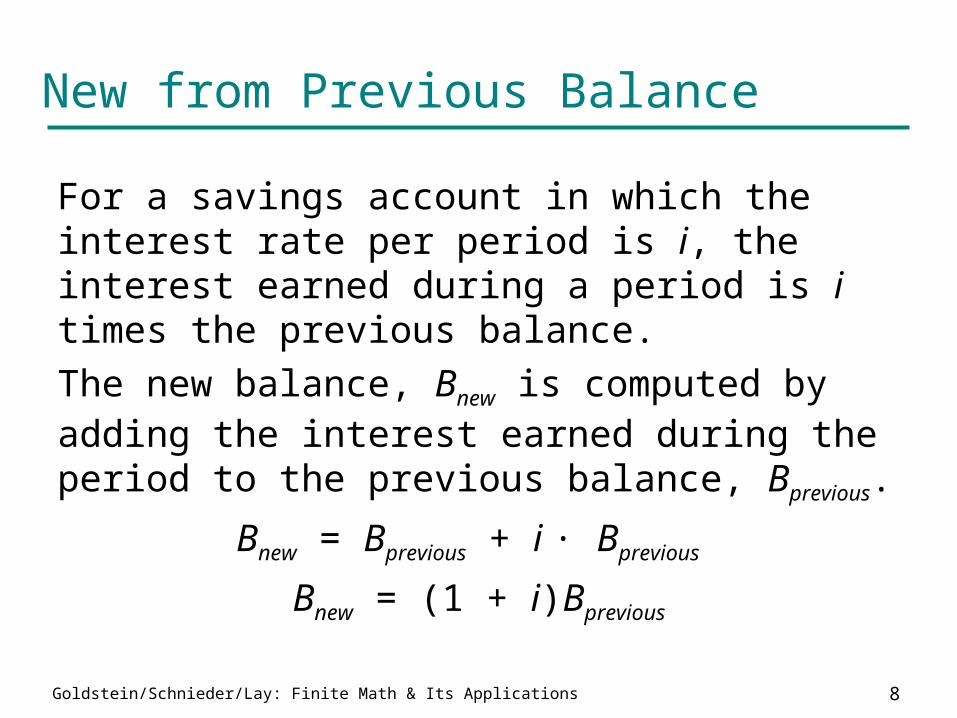

New from Previous Balance

For a savings account in which the interest rate per period is i, the interest earned during a period is i times the previous balance.

The new balance, Bnew is computed by adding the interest earned during the period to the previous balance, Bprevious.

Bnew = Bprevious + i · Bprevious

Bnew = (1 + i)Bprevious

Goldstein/Schnieder/Lay: Finite Math & Its Applications 9

Example New from Previous Balance

Compute the interest and the balance for the first two interest periods for a deposit of $1000 at 4% compounded semiannually.

For semiannually m = 2 so i = (4/2)% = 2% = .02.

First period: interest = .02(1000) = $20

B1 = 1000 + 20 = $1020

Second period: interest = .02(1020) = $20.40

B2 = 1020 + 20.40 = $1040.40

Goldstein/Schnieder/Lay: Finite Math & Its Applications 10

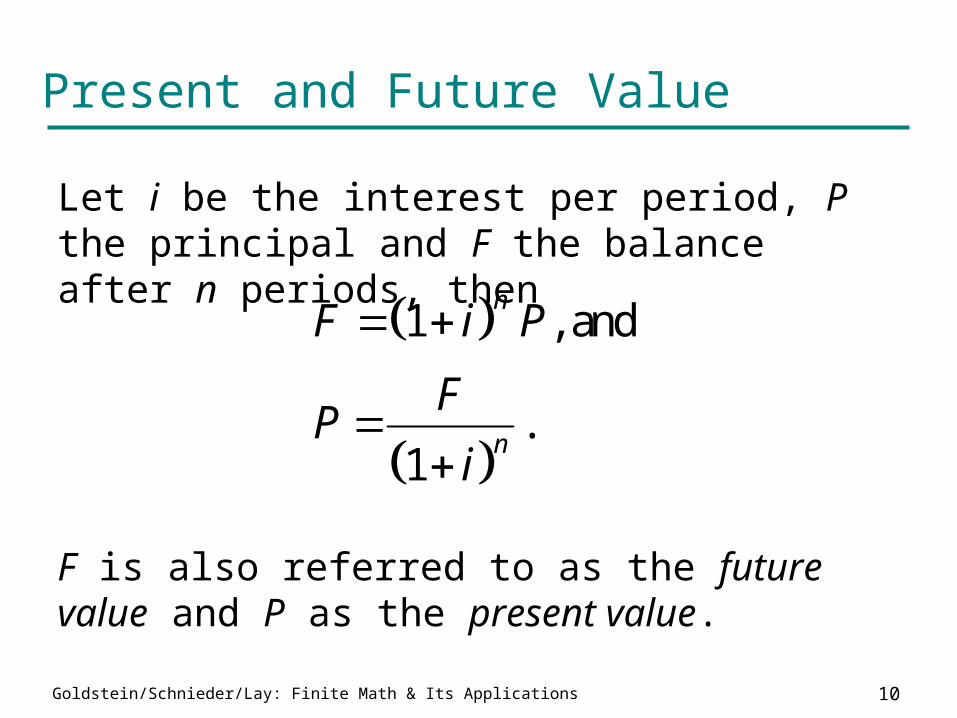

Present and Future Value

Let i be the interest per period, P the principal and F the balance after n periods, then

F is also referred to as the future value and P as the present value.

1 , and

.1

n

n

F i P

FP

i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 11

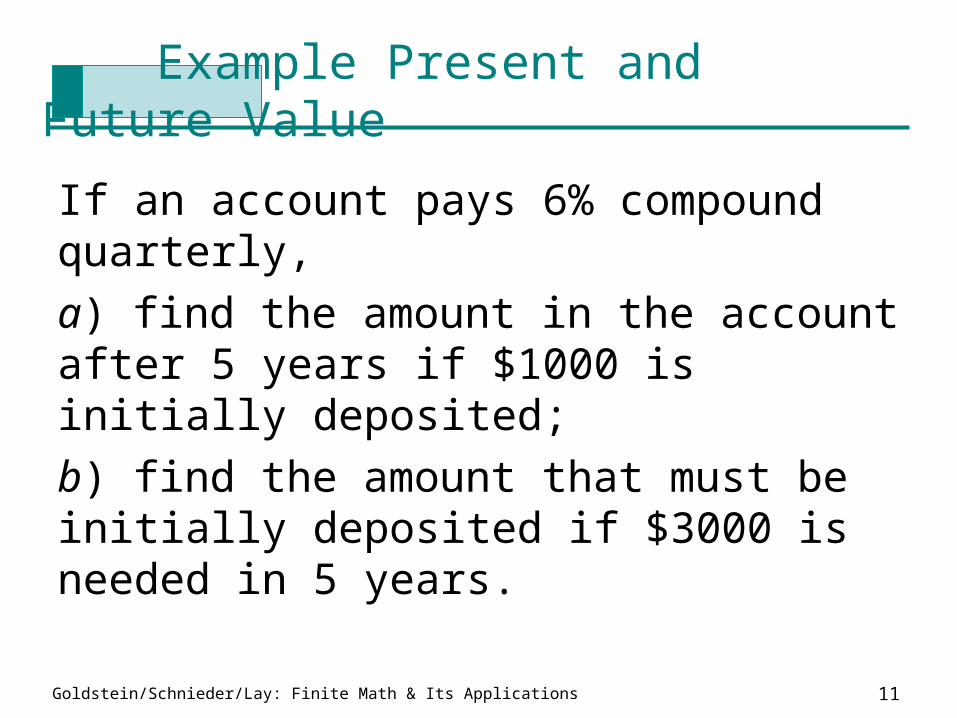

Example Present and Future Value

If an account pays 6% compound quarterly,

a) find the amount in the account after 5 years if $1000 is initially deposited;

b) find the amount that must be initially deposited if $3000 is needed in 5 years.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 12

Example Present and Future Value (2)

Period interest is i = .06/4 = .015.

Number of periods is n = 4*5 = 20.

a) P = $1000 so F = 1000(1 + .015)20 = $1346.86.

b) F = $3000 so 20

3000$2227.41.

(1 .015)P

Goldstein/Schnieder/Lay: Finite Math & Its Applications 13

Simple Interest

Simple interest is earned only on the principal and is not compounded.

If r is the annual percentage rate and n is the number of years, then

Interest = nrP, and

F = P + nrP = (1 + nr)P.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 14

Example Simple Interest

Calculate the amount after 4 years if $1000 is invested at 5% simple interest.

F = (1 + 4(.05))1000 = $1200

Goldstein/Schnieder/Lay: Finite Math & Its Applications 15

Effective Rate of Interest

The effective rate of interest is the simple interest rate that yields the same amount after one year as the annual rate of interest.

If r is the annual interest rate compounded m times a year, then i = r/m and

reff = (1 + i)m – 1.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 16

Example Effective Rate of Interest

Calculate the effective rate of interest for a savings account paying 3.65% compounded quarterly.

reff = (1 + .0365/4)4 - 1 = .037

So the effective rate is 3.7%.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 17

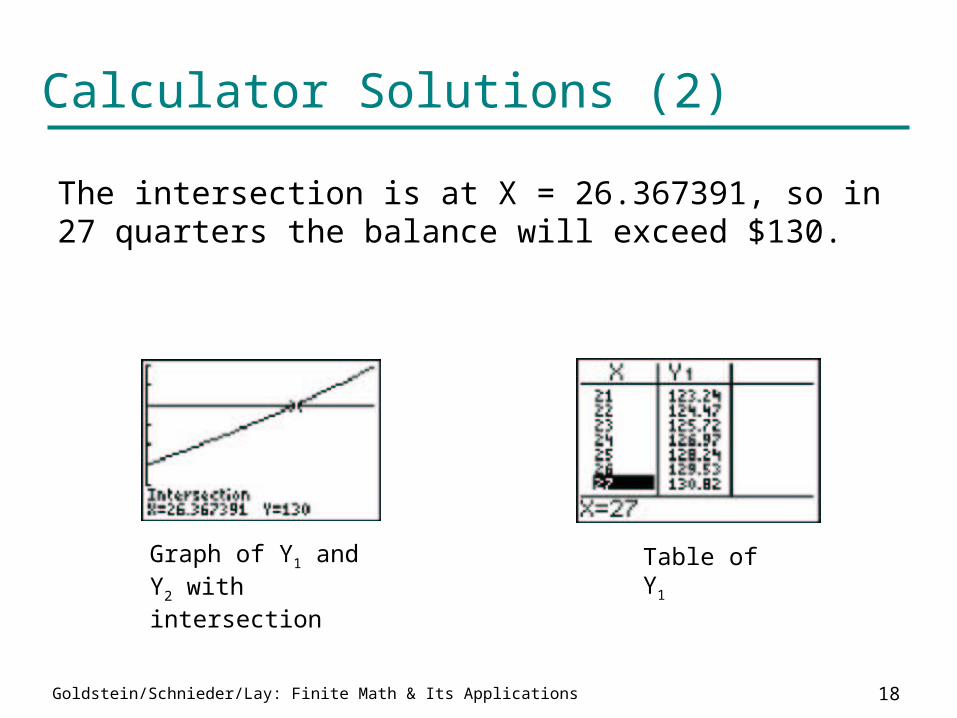

Calculator Solutions

Use a calculator to determine when the balance in a savings account in which $100 is deposited at 4% compounded quarterly reaches $130.

For a TI-83 set

Y1 = (1 + .04/4)^X*100 and

Y2 = 130.

Find the intersection of the two graphs.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 18

Calculator Solutions (2)

The intersection is at X = 26.367391, so in 27 quarters the balance will exceed $130.

Graph of Y1 and Y2 with intersection

Table of Y1

Goldstein/Schnieder/Lay: Finite Math & Its Applications 19

Summary Section 10.1 - Part 1

Money deposited into a savings account earns interest at regular time periods. Interest paid on the initial deposit only is called simple interest. Interest paid on the current balance (that is, on the initial deposit and the accumulated interest) is called compound interest. Successive balances of a savings account with compound interest can be calculated with Bnew = (1 + i)Bprevious.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 20

Summary Section 10.1 - Part 2

P - principal, the initial amount of money deposited into a savings account. P also represents the present value of a sum of money to be received in the future; that is, the amount of money needed to generate the future money. r - annual rate of interest, interest rate stated by the bank and used to calculate the interest rate per period.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 21

Summary Section 10.1 - Part 3

m - number of (compound) interest periods per year, most commonly 1, 4, or 12. i - compound interest rate per period, calculated as r/m. n - number of interest periods.F - future value, compound amount, or balance, value in a savings account. F = (1 + i)nP with compound interest, and F = (1 + nr)P with simple interest.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 22

Summary Section 10.1 - Part 4

reff - effective rate of interest, the simple interest rate that yields the same amount after one year as the annual rate of interest. reff = (1 + i)m – 1

Goldstein/Schnieder/Lay: Finite Math & Its Applications 23

10.2 Annuities

1. Definitions of Annuity

2. Future Value

3. Rent for a Future Value

4. Present Value and Rent

5. Storing andn is

n ia

Goldstein/Schnieder/Lay: Finite Math & Its Applications 24

Definitions of Annuities

An annuity is a sequence of equal payments made at regular intervals of time.

The payments are called rent.

The amount in an increasing annuity gets larger with each payment and the final value is called the future value of the annuity.

The amount in a decreasing annuity gets smaller with each payment and the amount at the beginning is called the present value of the annuity.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 25

Example Definitions of Annuities

Parents decide to deposit $100 at the end of each month into a savings account for the college education of their child. After 216 payments, the account will contain $38,735.32.

You have just sold your house and deposit your profit of $258,627.80 into an account so you can withdraw $5000 at the end of each month for 5 years at which time the balance will be $0.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 26

Example Definitions of Annuities (2)

The first example is of an increasing annuity with rent = $100 and future value = $38,735.32.

The second example is of a decreasing annuity with rent = $5000 and present value = $258,627.80.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 27

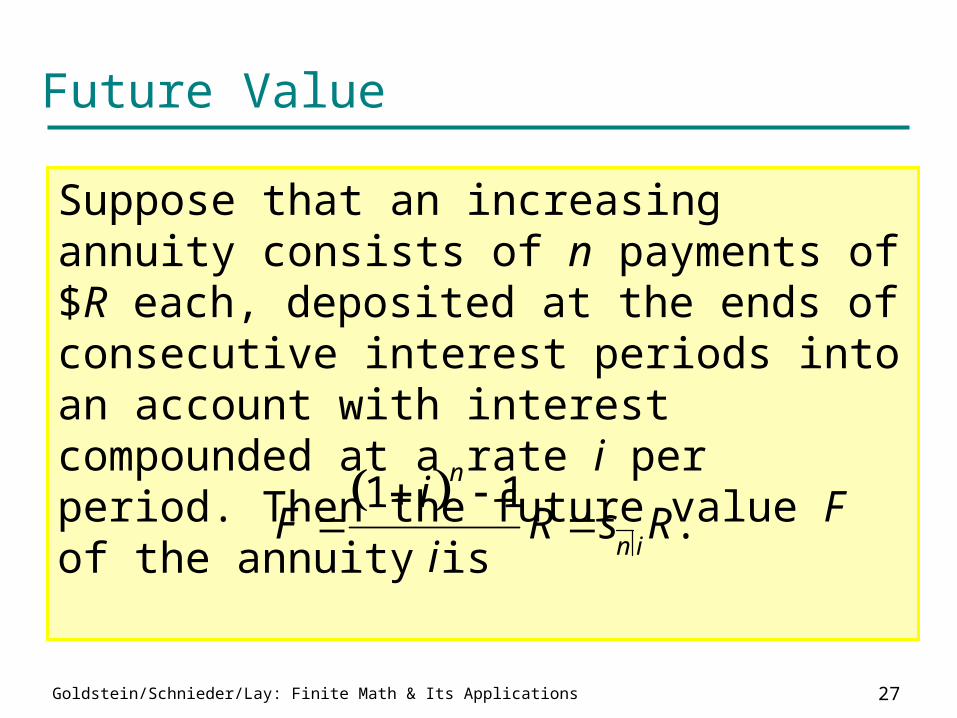

Future Value

Suppose that an increasing annuity consists of n payments of $R each, deposited at the ends of consecutive interest periods into an account with interest compounded at a rate i per period. Then the future value F of the annuity is

1 1.

n

n i

iF R s R

i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 28

Example Future Value

Calculate the future value of an increasing annuity of $100 per month for 2 years at 6% interest compounded monthly.

R = 100, i = .06/12 = .005 and n = 2(12) = 24.

To calculate on a TI-83 calculator, key in

So = 25.43195524.

F = (25.43195524)(100) = $2,543.20.

24 .005s

24 .005s

Goldstein/Schnieder/Lay: Finite Math & Its Applications 29

Rent for a Future Value

Suppose that an increasing annuity of n payments has future value F and has interest compounded at the rate i per period. Then the rent R is

.n i

FR

s

Goldstein/Schnieder/Lay: Finite Math & Its Applications 30

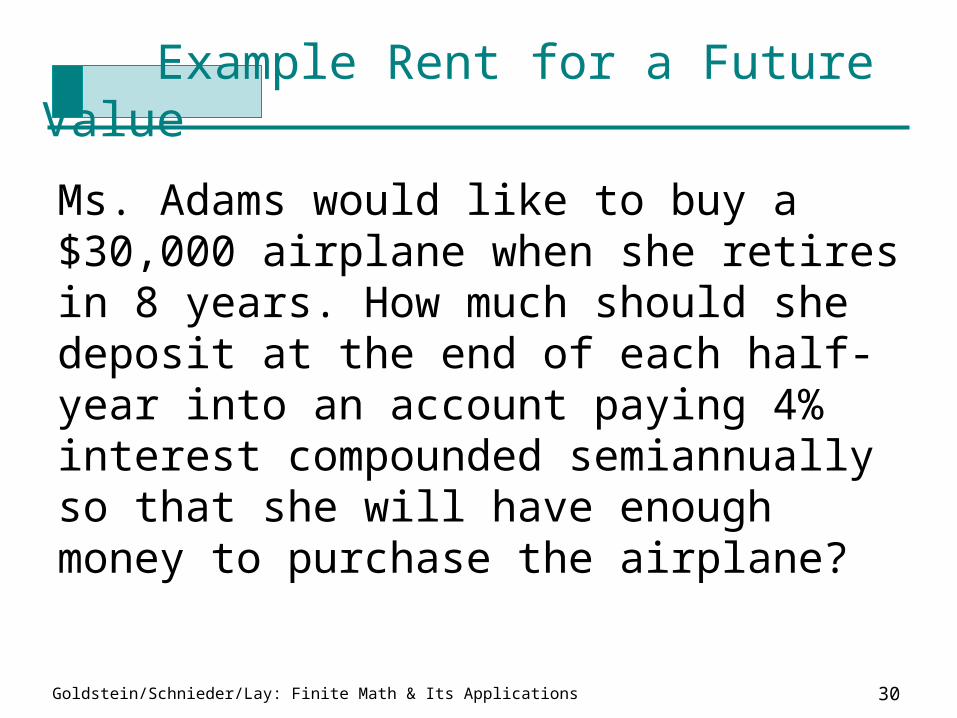

Example Rent for a Future Value

Ms. Adams would like to buy a $30,000 airplane when she retires in 8 years. How much should she deposit at the end of each half-year into an account paying 4% interest compounded semiannually so that she will have enough money to purchase the airplane?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 31

Example Rent for a Future Value (2)

F = 30,000, i = .04/2 = .02 and n = 8(2) = 16.

16 .02

30000(.05365013)(30000)

$1609.50

n i

FR

s s

Goldstein/Schnieder/Lay: Finite Math & Its Applications 32

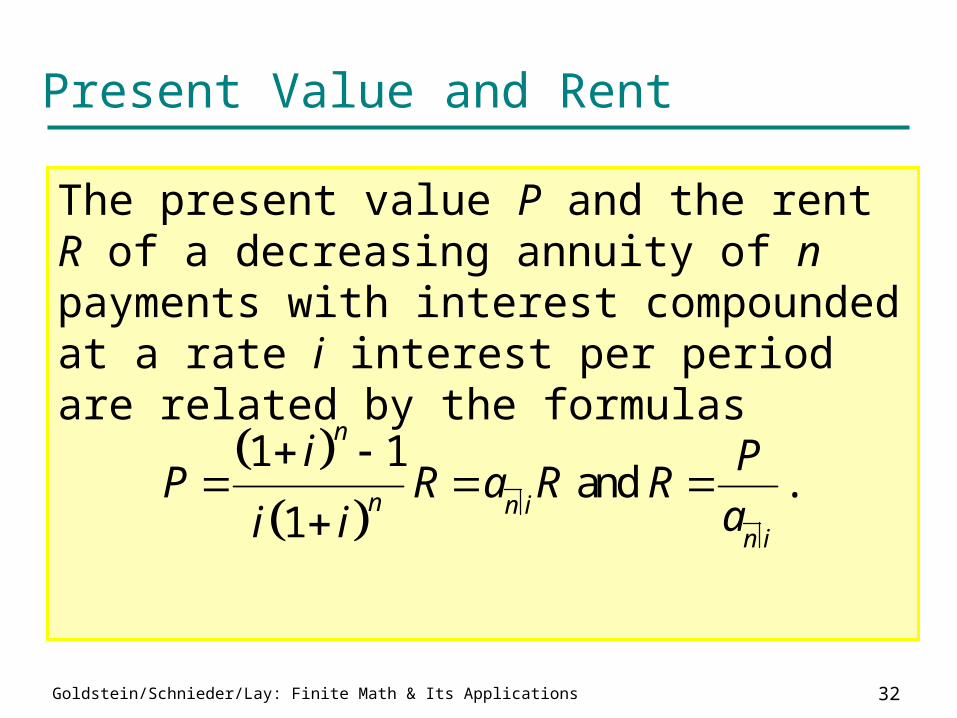

Present Value and Rent

The present value P and the rent R of a decreasing annuity of n payments with interest compounded at a rate i interest per period are related by the formulas

1 1 and .

1

n

n n in i

i PP R a R R

ai i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 33

Example Present Value and Rent

a) How much money must you deposit now at 6% interest compounded quarterly in order to be able to withdraw $3000 at the end of each quarter-year for 2 years?

b) How much money could you withdraw each quarter-year for 2 years if you deposited $24,000 into the same account?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 34

Example Present Value and Rent

a) R = 3000, i = .06/4 = .015 and n = 4(2) = 8.

b) P = 24000, i = .06/4 = .015 and n = 4(2) = 8.

8 .0153000 (7.48592508)(3000)

$22,457.78

P a

8 .015

240000.1335840245 (24000)

$3,206.02

Ra

Goldstein/Schnieder/Lay: Finite Math & Its Applications 35

As a time-saving device, the formulas for

can be assigned to the Y= editor on the TI-83 calculator.

Storing and n i

sn i

a

1 1, , , and

n i n in i n i

s as a

4 5

6 7

1Y , Y ,

1Y , and Y

X IX I

X IX I

ss

aa

Goldstein/Schnieder/Lay: Finite Math & Its Applications 36

Example Calculating Number of Periods

Use a graphing calculator to determine when the balance in an account in which $100 is deposited monthly at 6% interest compounded monthly will exceed $10,000.

Assuming Y4 contains the formula for

store .005 into I on the home screen.

In the Y= menu, define Y1 = 100Y4.

,X I

s

Goldstein/Schnieder/Lay: Finite Math & Its Applications 37

Example Calculating Number of Periods (2)

Scroll down the table for Y1 until Y1 exceeds 10000. This occurs when X = 82.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 38

Summary Section 10.2 - Part 1

An increasing (decreasing) annuity is a sequence of equal deposits (withdrawals) made at the ends of regular time intervals. F - future value, compound amount, or balance, value in an annuity at some point in the future.

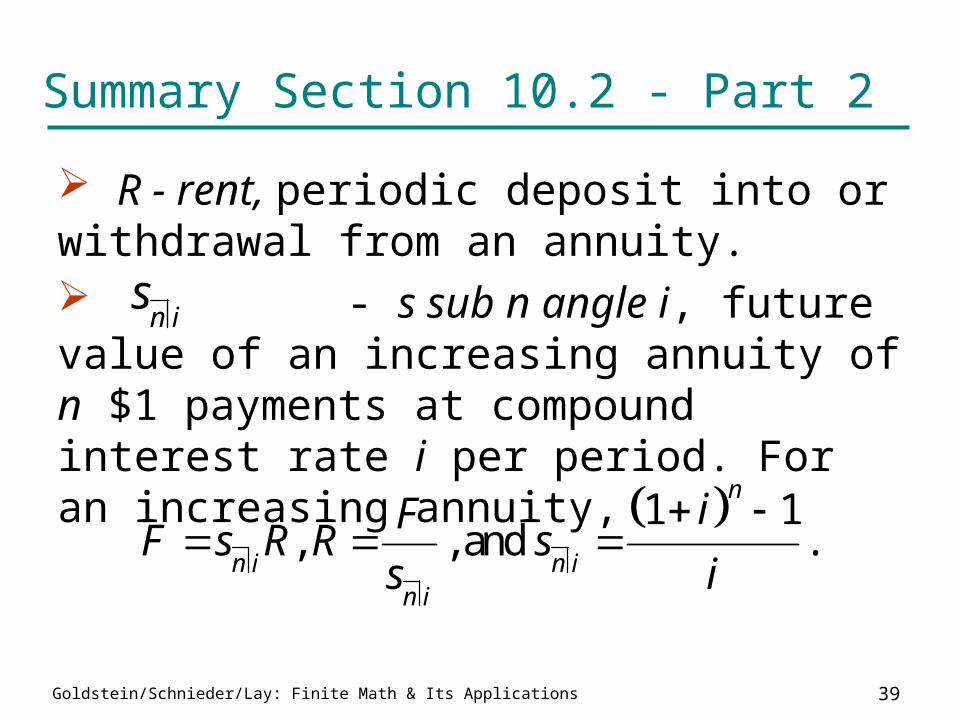

Goldstein/Schnieder/Lay: Finite Math & Its Applications 39

Summary Section 10.2 - Part 2

R - rent, periodic deposit into or withdrawal from an annuity. - s sub n angle i, future value of an increasing annuity of n $1 payments at compound interest rate i per period. For an increasing annuity,

n is

1 1, , and .

n

n i n in i

iFF s R R s

s i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 40

Summary Section 10.2 - Part 3

- a sub n angle i, present value of a decreasing annuity of n $1 payments at compound interest rate i per period. For a decreasing annuity,

n ia

1 1, , and .

1

n

nn i n in i

iPP a R R a

a i i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 41

Summary Section 10.2 - Part 4

Successive balances of an increasing annuity can be calculated with Bnew = (1 + i)Bprevious + R.

Successive balances of a decreasing annuity can be calculated with Bnew = (1 + i)Bprevious - R.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 42

10.3 Amortization of Loans

1. Amortization and Mortgage

2. Repayment Process

3. Unpaid Balance I

4. Unpaid Balance II

5. Balloon Payment

6. Calculator Application

Goldstein/Schnieder/Lay: Finite Math & Its Applications 43

Amortization and Mortgage

Loans under consideration will be repaid in a sequence of equal payments at regular time intervals, with the payment intervals coinciding with the interest periods. The process of paying off such a loan is called amortization.

A mortgage is a long-term loan used to purchase real estate. The real estate is used as collateral to guarantee the loan.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 44

Repayment Process

1. Payments are made at the end of each interest period.

2. The interest to be paid each interest period is the period interest rate, i, times the unpaid balance at the end of the previous interest period.

3. The unpaid balance at the end of the interest period is the previous unpaid balance plus the interest owed for the current interest period minus the payment.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 45

Unpaid Balance I

For a loan amortized over n payments with payments R, the unpaid balance at the end of the kth payment is the present value of a decreasing annuity with the same i and R but with n - k payments.

unpaid balance after paymentsn k i

k a R

Goldstein/Schnieder/Lay: Finite Math & Its Applications 46

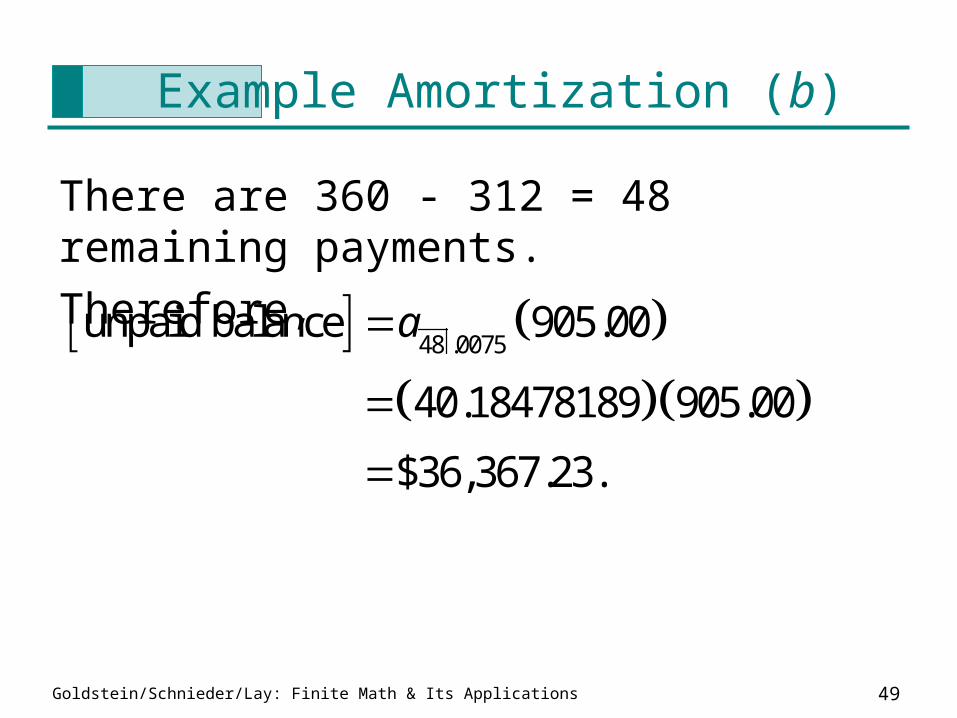

Example Amortization

On Dec. 31, 1990, a house was purchased with the buyer taking out a 30-year, $112,475 mortgage at 9% interest, compounded monthly. The mortgage payments are made at the end of each month.

a) Calculate the amount of the monthly payment.

b) Calculate the unpaid balance of the loan on Dec. 31, 2016, just after the 312th payment.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 47

Example Amortization - continued

c) How much interest will be paid during the month of January 2017?

d) How much of the principal will be paid off during the year 2016?

e) How much interest will be paid during the year 2016?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 48

Example Amortization (a)

A mortgage is a decreasing annuity. P = 112475, i = .09/12 = .0075 and n = (30)(12) = 360.

360 .0075

1112475 .00804623 112475

$905.00

Ra

Goldstein/Schnieder/Lay: Finite Math & Its Applications 49

Example Amortization (b)

There are 360 - 312 = 48 remaining payments.

Therefore,

48 .0075unpaid balance 905.00

40.18478189 905.00

$36,367.23.

a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 50

Example Amortization (c)

The interest paid during January 2017 is i times the unpaid balance at the end of December 2016 which was calculated in (b).

Interest = .0075(36367.23) = $272.75.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 51

Example Amortization (d)

The principal paid off during 2016 is equal to the unpaid balance at the end of 2015 minus the unpaid balance at the end of 2016.

The unpaid balance at the end of 2016 was calculated in (b). At the end of 2015, there are 360 - 300 = 60 payments left.

60 .0075principal repaid 905.00 36367.23

43596.90 36367.23 $7229.67

a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 52

Example Amortization (e)

The interest paid during 2016 is the total amount paid during 2016 minus that part of the payment used to repay the principal during 2016 which was calculated in (d).

interest during 2016 12 905.00 7229.67

$3630.33

Goldstein/Schnieder/Lay: Finite Math & Its Applications 53

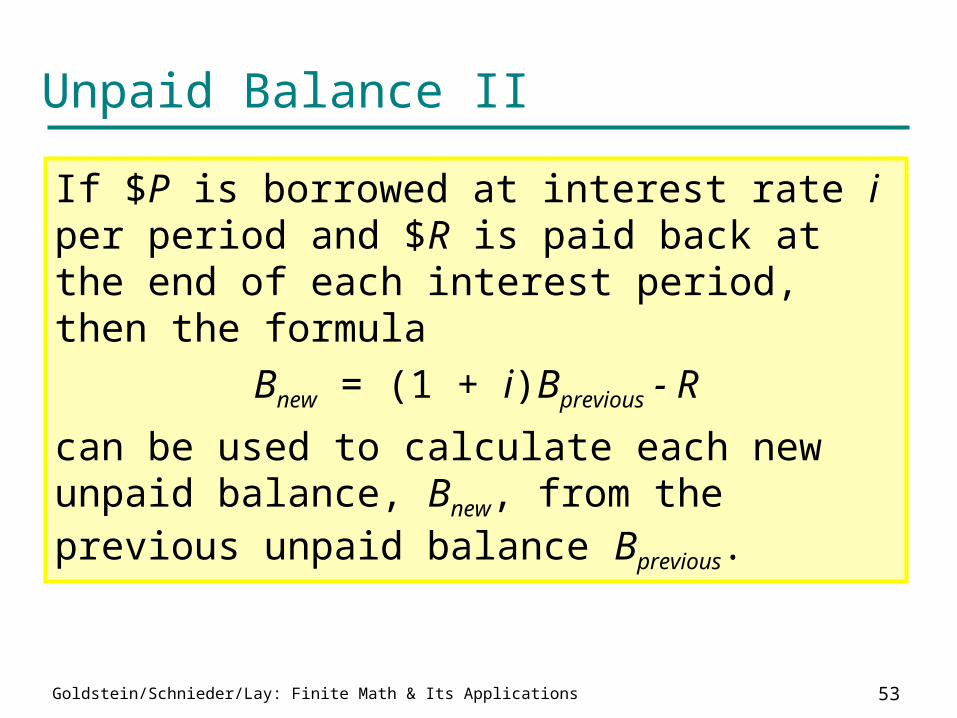

Unpaid Balance II

If $P is borrowed at interest rate i per period and $R is paid back at the end of each interest period, then the formula

Bnew = (1 + i)Bprevious - R

can be used to calculate each new unpaid balance, Bnew, from the previous unpaid balance Bprevious.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 54

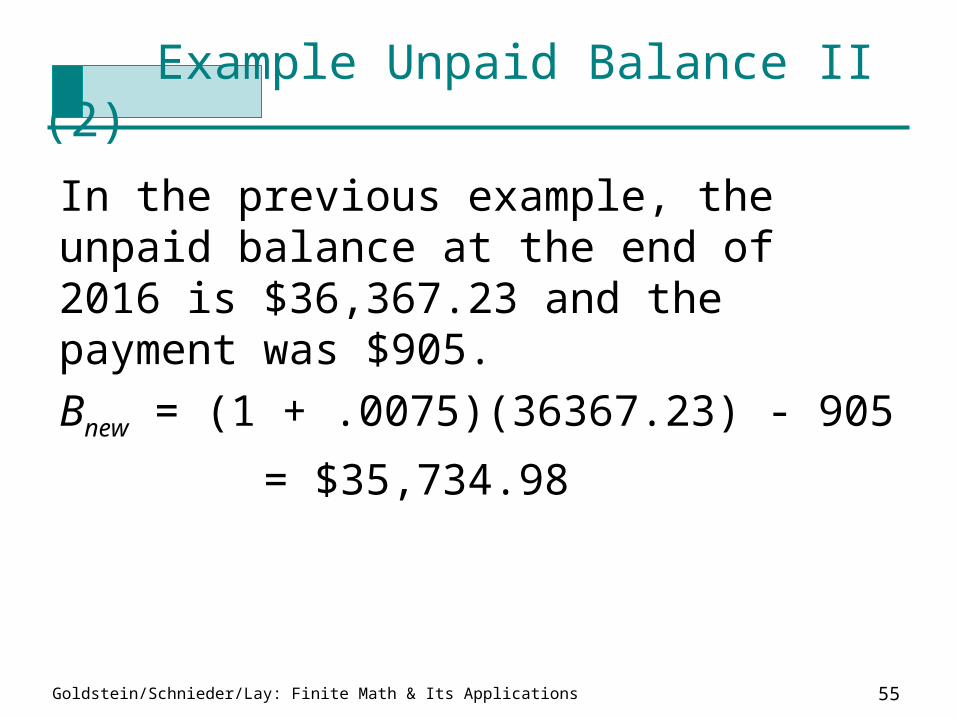

Example Unpaid Balance II

On Dec. 31, 1990, a house was purchased with the buyer taking out a 30-year , $112,475 mortgage at 9% interest, compounded monthly. The mortgage payments are made at the end of each month.

Calculate the unpaid balance of the loan on Jan. 31, 2017, just after the 313th payment.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 55

Example Unpaid Balance II (2)

In the previous example, the unpaid balance at the end of 2016 is $36,367.23 and the payment was $905.

Bnew = (1 + .0075)(36367.23) - 905

= $35,734.98

Goldstein/Schnieder/Lay: Finite Math & Its Applications 56

Balloon Payment

Sometimes amortized loans stipulate a balloon payment at the end of the term.

The present value, P, of a loan with n payments of R at an interest per period of i and a balloon payment of D at the end of the loan is

.

1nn i

DP a R

i

Goldstein/Schnieder/Lay: Finite Math & Its Applications 57

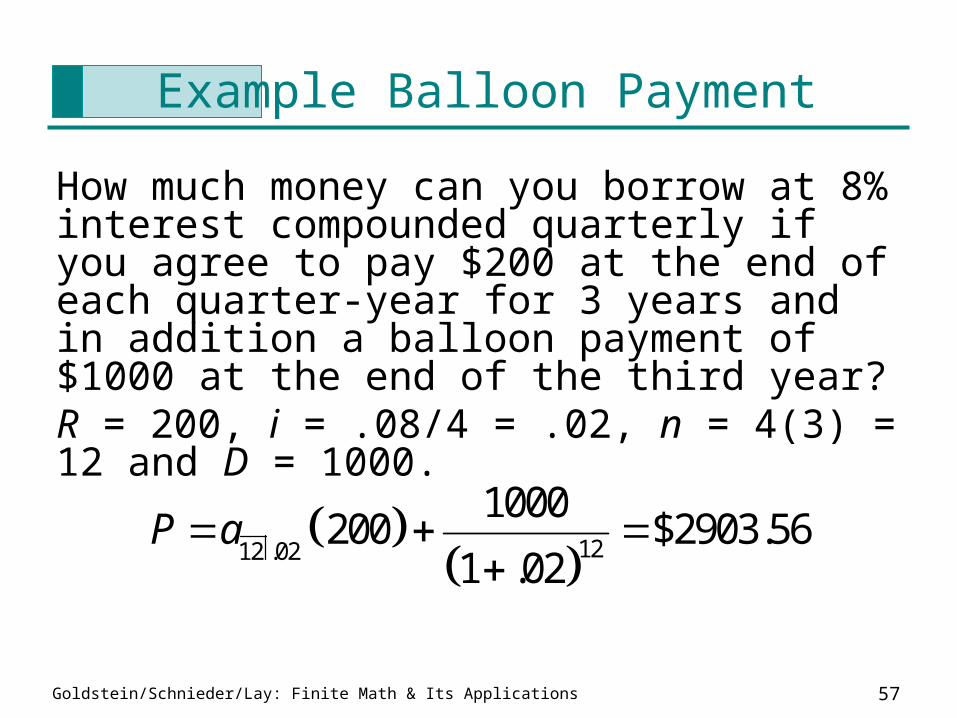

Example Balloon Payment

How much money can you borrow at 8% interest compounded quarterly if you agree to pay $200 at the end of each quarter-year for 3 years and in addition a balloon payment of $1000 at the end of the third year?R = 200, i = .08/4 = .02, n = 4(3) = 12 and D = 1000.

1212 .02

1000200 $2903.56

1 .02P a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 58

Example Calculator Application

Consider a loan of $112,475 at 9% interest compounded monthly and repaid with 360 monthly payments of $905. When will the debt-reduction portion of the payment surpass the interest portion?

On a TI-83, store the unpaid balance in Y1, the interest in Y2 and the debt-reduction portion of the payment in Y3.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 59

Example Calculator Application (2)

Store .0075 into I.

In the Y= menu, set

Y1 = Y6(360-X)*905, Y2 = I*Y1(X-1) and

Y3 = 905-Y2

where the formula for was stored in Y6.

Graph Y2 and Y3 and find their intersection.

X Ia

Goldstein/Schnieder/Lay: Finite Math & Its Applications 60

Example Calculator Application (3)

The intersection is at X = 268.23423.

So the debt-reduction portion of all payments starting with the 269th payment is greater than the interest.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 61

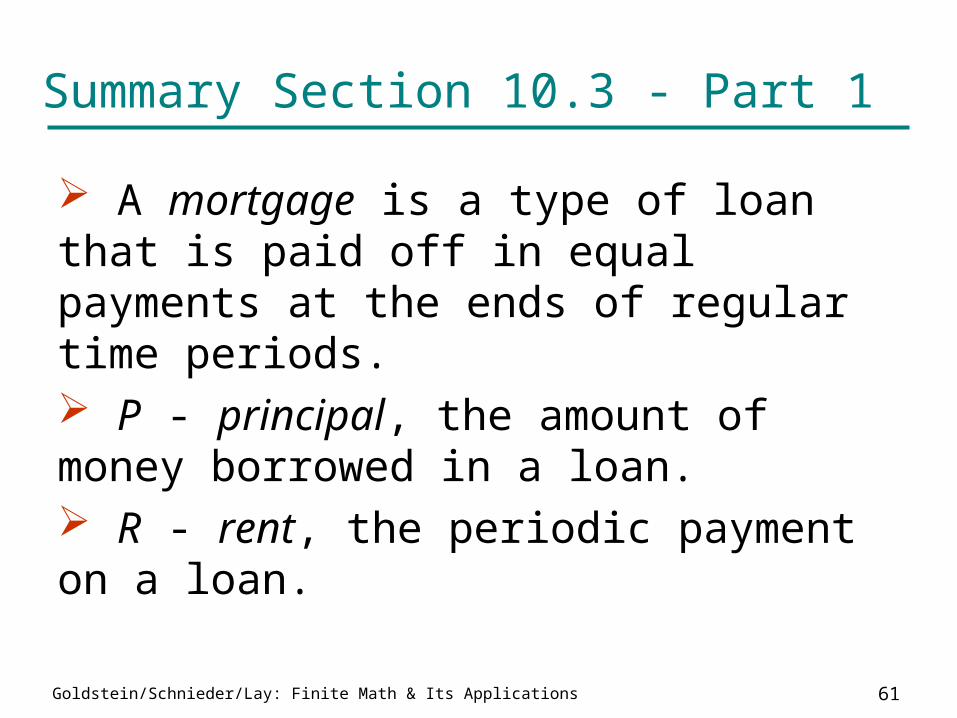

Summary Section 10.3 - Part 1

A mortgage is a type of loan that is paid off in equal payments at the ends of regular time periods. P - principal, the amount of money borrowed in a loan. R - rent, the periodic payment on a loan.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 62

Summary Section 10.3 - Part 2

At any time, the balance of a loan is the amount of money needed to retire (that is, pay off) the loan. It is calculated as the present value of all future payments. A payment used to retire a loan is called a balloon payment. Successive balances of a loan can be calculated with Bnew = (1 + i)Bprevious - R.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 63

10.4 Personal Financial Decisions

1. IRA

2. Equivalence of IRAs

3. Consumer Loans

4. Mortgages with Discount Points

5. Calculating APR

6. Calculating Effective Mortgage Rates

7. Significance of Discount Points

Goldstein/Schnieder/Lay: Finite Math & Its Applications 64

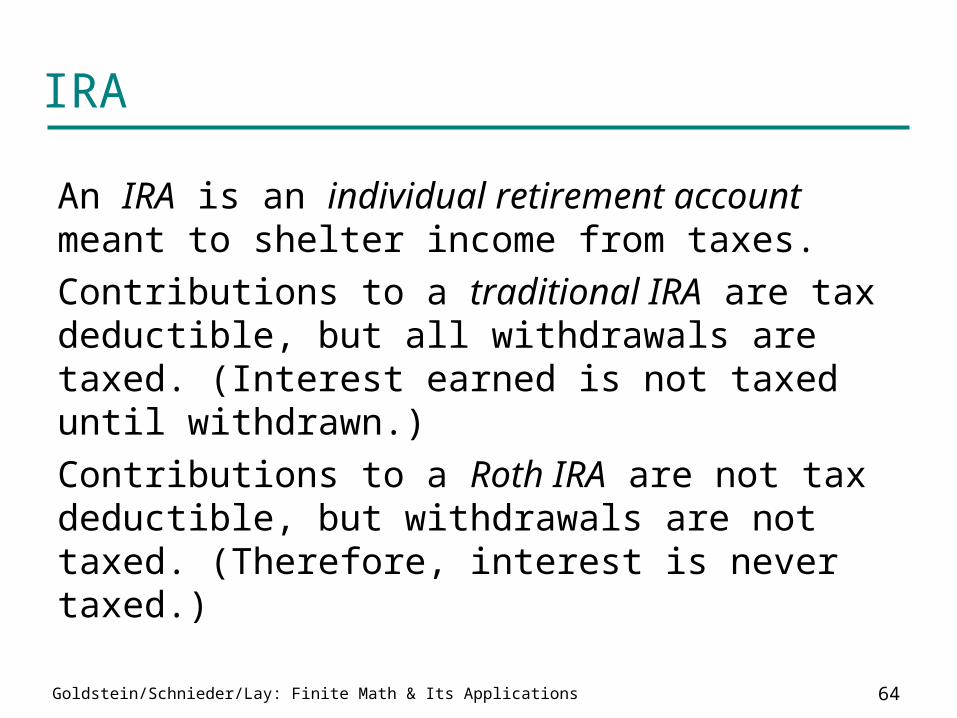

IRA

An IRA is an individual retirement account meant to shelter income from taxes.

Contributions to a traditional IRA are tax deductible, but all withdrawals are taxed. (Interest earned is not taxed until withdrawn.)

Contributions to a Roth IRA are not tax deductible, but withdrawals are not taxed. (Therefore, interest is never taxed.)

Goldstein/Schnieder/Lay: Finite Math & Its Applications 65

Example IRA

In 2006 you deposit $4000 of earned income into a traditional IRA on Jan. 1 which earns an annual interest rate of 6% compounded annually and suppose you are in the 30% marginal tax bracket for the duration of the account.a) How much income tax on earnings will you save for the year 2006?b) Making no more deposits, how much will you have after 48 years and after taxes are paid on the money?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 66

Example IRA (2)

a) [income tax saved] = [tax bracket] [amount]

= .30 (4000)

= $1200.

b) [balance after 48 years] = 4000(1 + .06)48

= $65,575.49.

[amount after taxes] = .70(65575.49)

= $45,902.84.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 67

Equivalence of IRAs

Equivalence of traditional and Roth IRAs With the assumption that your tax bracket does not change, the net earnings upon withdrawal from contributing P dollars into a traditional IRA account is the same amount as would result from paying taxes on the P dollars but then contributing the remaining money into a Roth IRA.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 68

Example IRA

Earl and Larry each begin full-time jobs in Jan. 2006 and plan to retire in Jan. 2054 after working for 48 years. Assume that any money they deposit into IRAs earns 6% interest compounded annually.a) Earl opens a traditional IRA account immediately and deposits $4000 into his account at the end of the next twelve years. Then he makes no more deposits. How much money will Earl have in his account when he retires?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 69

Example IRA - continued

b) Larry waits 12 years before opening his IRA and then deposits $4000 into the account at the end of each year until he retires. How much money will Larry have in his account when he retires?

c) Who paid the most money into his IRA?

d) Who had the most money in his account upon retirement?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 70

Example IRA (a)

a) At the end of 12 years, the account's balance is

After the first 12 years, the money earns compound interest for the final 36 years.

12 .064000 $67,479.76.F s

36[amount in account] 1 .06 67479.76

$549,774.61

Goldstein/Schnieder/Lay: Finite Math & Its Applications 71

Example IRA (b, c, d)

b) Larry's account only earns interest for 36 years.

c) Earl pays 12(4000) = $48,000.

Larry pays 36(4000) = $144,000.

d) Even though Larry paid more, he has less in his account upon retirement than Earl.

36 .064000 $476,483.47F s

Goldstein/Schnieder/Lay: Finite Math & Its Applications 72

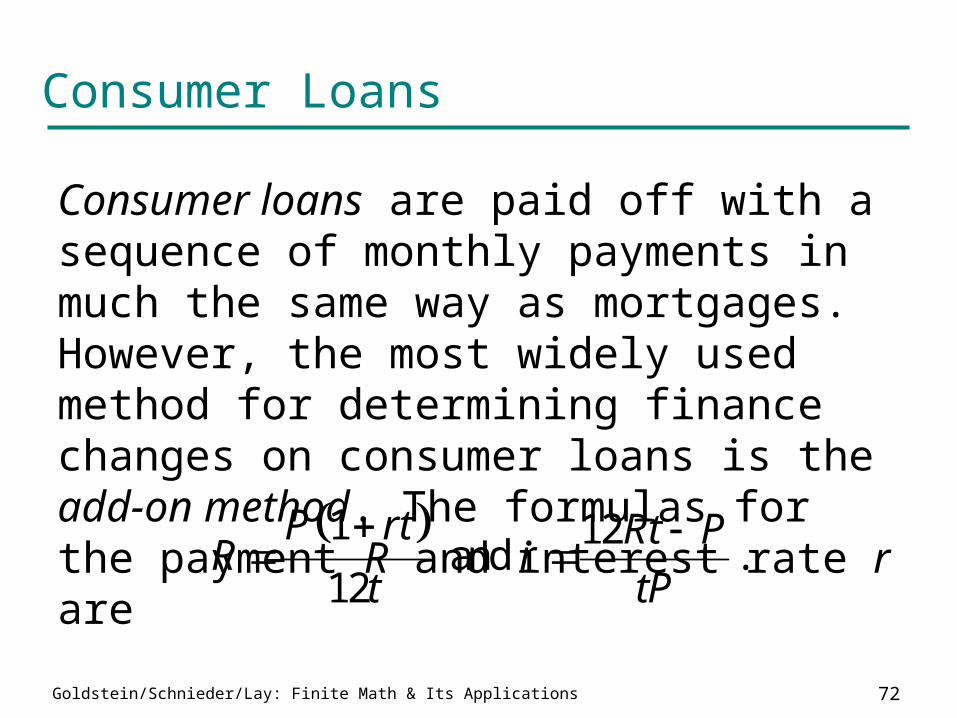

Consumer Loans

Consumer loans are paid off with a sequence of monthly payments in much the same way as mortgages. However, the most widely used method for determining finance changes on consumer loans is the add-on method. The formulas for the payment R and interest rate r are 1 12

and .12

P rt Rt PR r

t tP

Goldstein/Schnieder/Lay: Finite Math & Its Applications 73

Example Consumer Loans

You take out a 2-year consumer loan of $1000 at an annual interest rate of 6% using the add-on method.

a) What is the monthly payment?

b) What would the monthly payment be if computed as a mortgage?

c) What is the APR (annual percentage rate)?

Goldstein/Schnieder/Lay: Finite Math & Its Applications 74

Example Consumer Loans (a and b)

a) P = 1000, r = .06 and t = 2.

b) P = 1000, i = .06/12 = .005 and n = 24.

1000 1 .06 2= $46.67

12 2R

24 .005

1000= $44.32R

a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 75

Example Consumer Loans (c)

c) Using a TI-83, the period interest rate X is the intersection of the lines Y1 = 1000 and Y2 = ((1+X)^24-1)/(X(1+X)^24)*46.67.

The solution is i = X = .0092782 so r = 12(.0092782) = .1113384 or 11.13%.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 76

Mortgages with Discount Points

Home mortgages have a stated interest rate, called the constant rate. However, some loans also carry points or discount points. Each point requires that you pay up-front additional interest equal to 1% of the stated loan amount. This has the effect of reducing the actual loaned amount.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 77

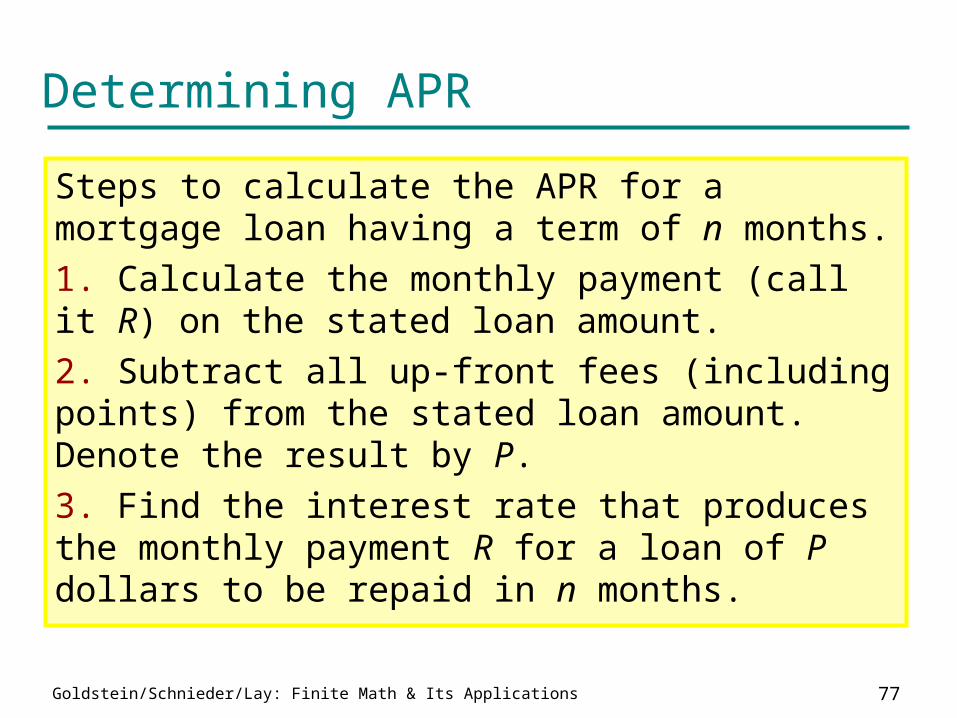

Determining APR

Steps to calculate the APR for a mortgage loan having a term of n months.

1. Calculate the monthly payment (call it R) on the stated loan amount.

2. Subtract all up-front fees (including points) from the stated loan amount. Denote the result by P.

3. Find the interest rate that produces the monthly payment R for a loan of P dollars to be repaid in n months.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 78

Example Determining APR

For a mortgage of $200,000 at 6% compounded monthly that carries 1 point, find the APR.

Following the 3 steps:

1) P = 200000, i = .06/12 = .005 and

n = 12(30) = 360.

360 .005

200000$1199.10R

a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 79

Example Determining APR (2)

2) P = 200000 - .01(200000) = $198,000

3) Technology is the best way to calculate the interest rate. Using the Excel RATE(n,-R,P,0) function, APR = 12*RATE(360,-1199.10,198000,0)

= .06094 = 6.094%.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 80

Effective Mortgage Rate

The APR is of limited use because it is relevant only for loans that are kept for their full terms. The average mortgage is refinanced or terminated after around 5 years. The effective mortgage rate takes into account the length of time the loan will be held and the unpaid balance at that time.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 81

Effective Mortgage Rate (2)

Steps to calculate the effective mortgage rate for a mortgage loan expected to be held for m months.

1. Calculate the monthly payment (call it R) on the stated loan amount.

2. Subtract all up-front fees (including points) from the stated loan amount. Denote the result by P.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 82

Effective Mortgage Rate (3)

3. Determine the unpaid balance on the stated loan amount after m months. Denote the result by B.

4. Find the interest rate that causes a decreasing annuity with beginning balance P dollars and monthly payment R to decline to B dollars after m months.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 83

Example Effective Mortgage Rate

For a mortgage of $200,000 at 6% compounded monthly that carries 1 point, find the effective mortgage rate assuming the mortgage will be held for 5 years.

Use the 4-step process:

1. R = 1199.10 as calculated previously.

2. P = 198000 as calculated previously.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 84

Example Effective Mortgage Rate (2)

3. The mortgage has 360 - 60 = 300 months to go. Therefore

4. Using the Excel RATE(m, -R,P,-B) function, the effective rate is 12*RATE(60,-1199.10,198000,-186108.55) = .0624069 or 6.25%.

300 .0051199.10 $186,108.55.B a

Goldstein/Schnieder/Lay: Finite Math & Its Applications 85

Significance of Discount Points

Rule of thumb for the significance of discount pointsLifetime Difference between effective mortgage rate

and stated interest rate, per discount point

1 year 1 percentage point

2 years 1/2 percentage point

3 years 1/3 percentage point

4 to 6 years 1/4 percentage point

7 to 9 years 1/6 percentage point

10 to 12 years 1/7 percentage point

More than 12 years 1/8 percentage point

Goldstein/Schnieder/Lay: Finite Math & Its Applications 86

Summary Section 10.4 - Part 1

An individual retirement account (IRA) is an increasing annuity in which the annual interest earned is either tax free (Roth IRA) or tax-deferred (traditional IRA). Contributions are tax deductible only with a traditional IRA. When finance charges on a consumer loan are calculated with the add-on method, the interest paid each month is a fixed percentage of the principal, rather than a fixed percentage of the current balance.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 87

Summary Section 10.4 - Part 2

For each discount point accompanying a mortgage loan, you must pay additional interest up-front equal to 1% of the amount borrowed. The APR and the effective mortgage rate, which take up-front fees into account, are often more useful than the contract interest rate in appraising a loan. Each of them makes use of the reduced loan amount obtained by subtracting the up-front fees from the stated loan amount.

Goldstein/Schnieder/Lay: Finite Math & Its Applications 88

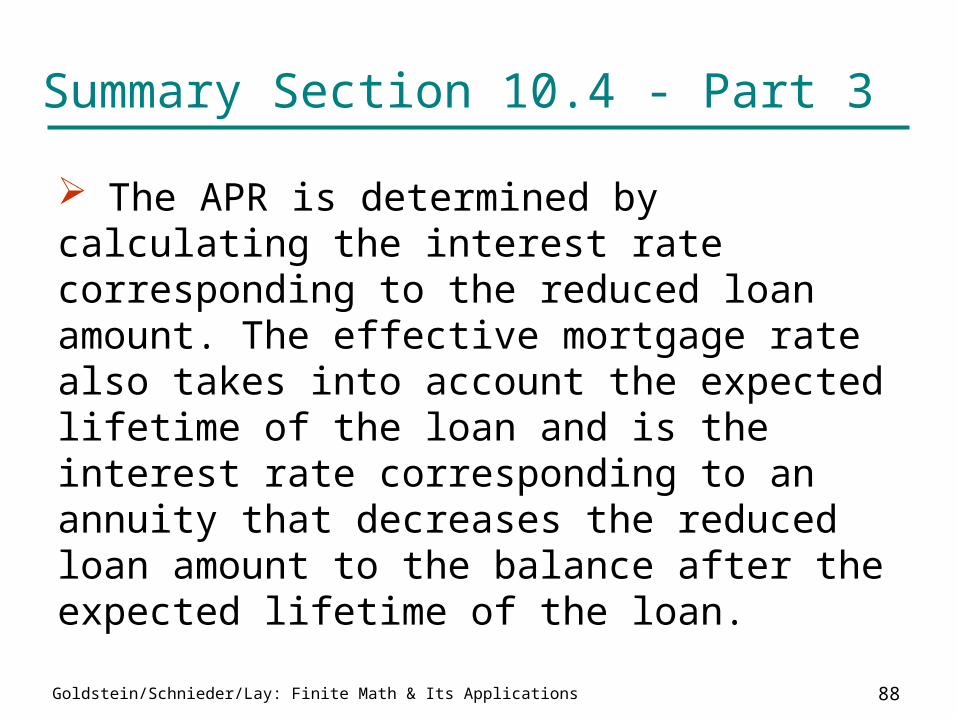

Summary Section 10.4 - Part 3

The APR is determined by calculating the interest rate corresponding to the reduced loan amount. The effective mortgage rate also takes into account the expected lifetime of the loan and is the interest rate corresponding to an annuity that decreases the reduced loan amount to the balance after the expected lifetime of the loan.