44

Chapter 10 The Cost of Capital

| Date post: | 17-Dec-2015 |

| Category: |

Documents |

| Upload: | georgiana-sophia-booker |

| View: | 214 times |

| Download: | 0 times |

Chapter 10

The Cost of Capital

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-2

Learning Goals

1. Understand the key assumptions, the basic concept, and the specific sources of capital associated with the cost of capital.

2. Determine the cost of long-term debt and the cost of preferred stock.

3. Calculate the cost of common stock equity and convert it into the cost of retained earnings and the cost of new issues of commons stock.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-3

Learning Goals (cont.)

4. Calculate the weighted average cost of capital (WACC) and discuss alternative weighting schemes and economic value added (EVA).

5. Describe the procedures used to determine break points and the weighted marginal cost of capital (WMCC).

6. Explain the weighted marginal cost of capital (WMCC) and its use with the investment opportunities schedule (IOS) to make financing and investment decisions.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-4

An Overview of the Cost of Capital

• The cost of capital acts as a link between the firm’s long-term investment decisions and the wealth of the owners as determined by investors in the marketplace.

• It is the “magic number” that is used to decide whether a proposed investment will increase or decrease the firm’s stock price.

• Formally, the cost of capital is the rate of return that a firm must earn on the projects in which it invests to maintain the market value of its stock.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-5

The Firm’s Capital Structure

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-6

Some Key Assumptions

• Business Risk—the risk to the firm of being unable to cover operating costs—is assumed to be unchanged. This means that the acceptance of a given project does not affect the firm’s ability to meet operating costs.

• Financial Risk—the risk to the firm of being unable to cover required financial obligations—is assumed to be unchanged. This means that the projects are financed in such a way that the firm’s ability to meet financing costs is unchanged.

• After-tax costs are considered relevant—the cost of capital is measured on an after-tax basis.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-7

Assume the ABC company has the following investment opportunity:

- Initial Investment = $100,000

- Useful Life = 20 years

- IRR = 7%

- Least cost source of financing, Debt = 6%

Given the above information, a firm’s financial manger would be inclined to accept and undertake the investment.

The Basic Concept

• Why do we need to determine a company’s overall “weighted average cost of capital?”

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-8

Imagine now that only one week later, the firm has another available investment opportunity

- Initial Investment = $100,000

- Useful Life = 20 years

- IRR = 12%

- Least cost source of financing, Equity = 14%

Given the above information, the firm would reject this second, yet clearly more desirable investment opportunity.

The Basic Concept (cont.)

• Why do we need to determine a company’s overall “weighted average cost of capital?”

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-9

The Basic Concept (cont.)

• Why do we need to determine a company’s overall “weighted average cost of capital?”

• As the above simple example clearly illustrates, using this piecemeal approach to evaluate investment opportunities is clearly not in the best interest of the firm’s shareholders.

• Over the long haul, the firm must undertake investments that maximize firm value.

• This can only be achieved if it undertakes projects that provide returns in excess of the firm’s overall weighted average cost of financing (or WACC).

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-10

Specific Sources of Capital: The Cost of Long-Term Debt

• The pretax cost of debt is equal to the the yield-to-maturity on the firm’s debt adjusted for flotation costs.

• Recall that a bond’s yield-to-maturity depends upon a number of factors including the bond’s coupon rate, maturity date, par value, current market conditions, and selling price.

• After obtaining the bond’s yield, a simple adjustment must be made to account for the fact that interest is a tax-deductible expense.

• This will have the effect of reducing the cost of debt.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-11

Duchess Corporation, a major hardware manufacturer, is

contemplating selling $10 million worth of 20-year, 9% coupon

bonds with a par value of $1,000. Because current market

interest rates are greater than 9%, the firm must sell the bonds

at $980. Flotation costs are 2% or $20. The net proceeds to

the firm for each bond is therefore $960 ($980 - $20).

Net Proceeds

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-12

• Before-Tax Cost of Debt

• The before-tax cost of debt can be calculated in any one of three ways:– Using cost quotations

– Calculating the cost

– Approximating the cost

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-13

• Before-Tax Cost of Debt

– Using Cost Quotations

– When the net proceeds from the sale of a bond equal its par value, the before-tax cost equals the coupon interest rate.

– A second quotation that is sometimes used is the yield-to-maturity (YTM) on a similar risk bond.

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-14

• Before-Tax Cost of Debt– Calculating the Cost

– This approach finds the before-tax cost of debt by calculating the internal rate of return (IRR).

– As discussed in earlier in the text, YTM can be calculated using: (a) trial and error, (b) a financial calculator, or (c) a spreadsheet.

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-15

• Before-Tax Cost of Debt– Calculating the Cost

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-16

• Before-Tax Cost of Debt– Calculating the Cost

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-17

• Before-Tax Cost of Debt– Calculating the Cost

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-18

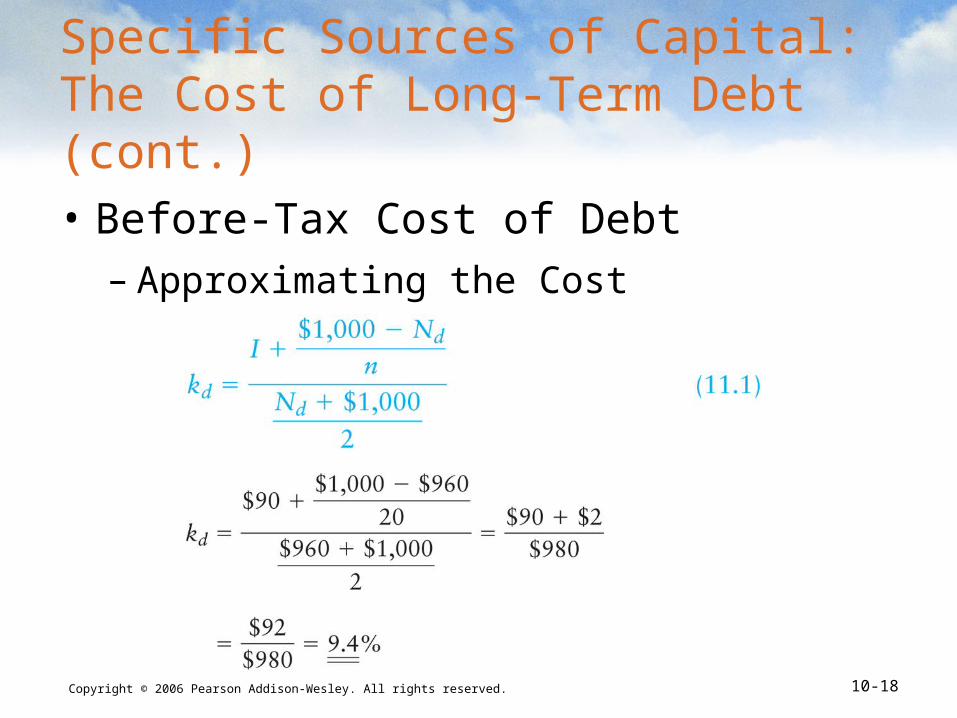

• Before-Tax Cost of Debt– Approximating the Cost

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-19

Find the after-tax cost of debt for Duchess assuming it has a 40% tax rate:

ki = 9.4% (1-.40) = 5.6%

This suggests that the after-tax cost of raising debt capital for Duchess is 5.6%.

Specific Sources of Capital: The Cost of Long-Term Debt (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-20

Duchess Corporation is contemplating the issuance of a 10% preferred stock that is expected to sell for its $87-per share value. The cost of issuing and selling the stock is expected to be $5 per share. The dividend is $8.70 (10% x $87). The net proceeds price (Np) is $82 ($87 - $5).

KP = DP/Np = $8.70/$82 = 10.6%

Specific Sources of Capital: The Cost of Preferred Stock

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-21

Specific Sources of Capital: The Cost of Common Stock

• There are two forms of common stock financing: retained earnings and new issues of common stock.

• In addition, there are two different ways to estimate the cost of common equity: any form of the dividend valuation model, and the capital asset pricing model (CAPM).

• The dividend valuation models are based on the premise that the value of a share of stock is based on the present value of all future dividends.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-22

kS = (D1/P0) + g

kE = rF + b(kM - RF).

• Using the constant growth model, we have:

• We can also estimate the cost of common equity using the CAPM:

Specific Sources of Capital: The Cost of Common Stock (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-23

• The CAPM differs from dividend valuation models in that it explicitly considers the firm’s risk as reflected in beta.

• On the other hand, the dividend valuation model does not explicitly consider risk.

• Dividend valuation models use the market price (P0) as a reflection of the expected risk-return preference of investors in the marketplace.

Specific Sources of Capital: The Cost of Common Stock (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-24

• Although both are theoretically equivalent, dividend valuation models are often preferred because the data required are more readily available.

• The two methods also differ in that the dividend valuation models (unlike the CAPM) can easily be adjusted for flotation costs when estimating the cost of new equity.

• This will be demonstrated in the examples that follow.

Specific Sources of Capital: The Cost of Common Stock (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-25

ks = D1/P0 + g

For example, assume a firm has just paid a dividend of

$2.50 per share, expects dividends to grow at 10%

indefinitely, and is currently selling for $50.00 per share.

First, D1 = $2.50(1+.10) = $2.75, and

kS = ($2.75/$50.00) + .10 = 15.5%.

Specific Sources of Capital: The Cost of Common Stock (cont.)

• Cost of Retained Earnings (kE)

– Constant Dividend Growth Model

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-26

ks = rF + b(kM - RF).

For example, if the 3-month T-bill rate is currently 5.0%,

the market risk premium is 9%, and the firm’s beta is

1.20, the firm’s cost of retained earnings will be:

ks = 5.0% + 1.2 (9.0%) = 15.8%.

• Cost of Retained Earnings (kE)

– Security Market Line Approach

Specific Sources of Capital: The Cost of Common Stock (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-27

The previous example indicates that our estimate of the

cost of retained earnings is somewhere between 15.5%

and 15.8%. At this point, we could either choose one or

the other estimate or average the two.

Using some managerial judgement and preferring to err

on the high side, we will use 15.8% as our final estimate

of the cost of retained earnings.

Specific Sources of Capital: The Cost of Common Stock (cont.)

• Cost of Retained Earnings (kE)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-28

kn = = D1/Nn - g

Continuing with the previous example, how much would it

cost the firm to raise new equity if flotation costs amount

to $4.00 per share?

kn = [$2.75/($50.00 - $4.00)] + .10 = 15.97% or 16%.

• Cost of New Equity (kn)

– Constant Dividend Growth Model

Specific Sources of Capital: The Cost of Common Stock (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-29

WACC = ka = wiki + wpkp + wskr or n

The weights in the above equation are intended to

represent a specific financing mix (where wi = % of

debt, wp = % of preferred, and ws= % of common).

Specifically, these weights are the target percentages

of debt and equity that will minimize the firm’s overall

cost of raising funds.

The Weighted Average Cost of Capital

• Capital Structure Weights

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-30

WACC = ka = wiki + wpkp + wskr or n

The Weighted Average Cost of Capital

• Capital Structure Weights

One method uses book values from the firm’s balance

sheet. For example, to estimate the weight for debt,

simply divide the book value of the firm’s long-term

debt by the book value of its total assets.

To estimate the weight for equity, simply divide the total

book value of equity by the book value of total assets.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-31

A second method uses the market values of the firm’s debt

and equity. To find the market value proportion of debt,

simply multiply the price of the firm’s bonds by the number

outstanding. This is equal to the total market value of the

firm’s debt.

Next, perform the same computation for the firm’s equity

by multiplying the price per share by the total number of

shares outstanding.

WACC = ka = wiki + wpkp + wskr or n

The Weighted Average Cost of Capital

• Capital Structure Weights

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-32

WACC = ka = wiki + wpkp + wskr or n

The Weighted Average Cost of Capital

• Capital Structure Weights

Finally, add together the total market value of the firm’s

equity to the total market value of the firm’s debt. This

yields the total market value of the firm’s assets.

To estimate the market value weights, simply dividend

the market value of either debt or equity by the market

value of the firm’s assets .

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-33

WACC = ka = wiki + wpkp + wskr or n

The Weighted Average Cost of Capital

• Capital Structure Weights

For example, assume the market value of the firm’s debt is $40

million, the market value of the firm’s preferred stock is $10

million, and the market value of the firm’s equity is $50 million.

Dividing each component by the total of $100 million gives us

market value weights of 40% debt, 10% preferred, and 50%

common.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-34

WACC = ka = wiki + wpkp + wskr or n

The Weighted Average Cost of Capital

• Capital Structure Weights

Using the costs previously calculated along with the

market value weights, we may calculate the weighted

average cost of capital as follows:

WACC = .40(5.67%) + .10(9.62%) + .50(15.8%)

= 11.13%

This assumes the firm has sufficient retained earnings to

fund any anticipated investment projects.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-35

The Weighted Average Cost of Capital: Economic Value Added (EVA®)

• EVA is a popular measure used by firms to determine whether an investment contributes to owners’ wealth.

• EVA can be calculated as the difference between Net Operating Profits After Taxes (NOPAT) and the cost of funds used to finance the investment.

• The cost of funds is found by multiplying the dollar amount of funds used to finance the investment by the firm’s WACC.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-36

For Example, the EVA® of an investment of $3.75 million

by a firm with a WACC of 10% in a project expected to

generate NOPAT of $410,000 would be:

EVA® = $410,000 – (10% x $3,750,000) = $35,000

Because the EVA® is positive, the proposed investment

is expected to increase owner wealth and is therefore

acceptable.

The Weighted Average Cost of Capital: Economic Value Added (EVA®)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-37

The Marginal Cost & Investment Decisions

• The Weighted Marginal Cost of Capital (WMCC)– The WACC typically increases as the volume of new

capital raised within a given period increases.

– This is true because companies need to raise the return to investors in order to entice them to invest to compensate them for the increased risk introduced by larger volumes of capital raised.

– In addition, the cost will eventually increase when the firm runs out of cheaper retained equity and is forced to raise new, more expensive equity capital.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-38

Finding the break points in the WMCC schedule will allow us to determine at what level of new financing the WACC will increase due to the factors listed above.

BPj = AFj/wj

where:

BPj = breaking point form financing source j

AFj = amount of funds available at a given cost

wj = target capital structure weight for source j

The Marginal Cost & Investment Decisions (cont.)

• The Weighted Marginal Cost of Capital (WMCC)– Finding Break Points

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-39

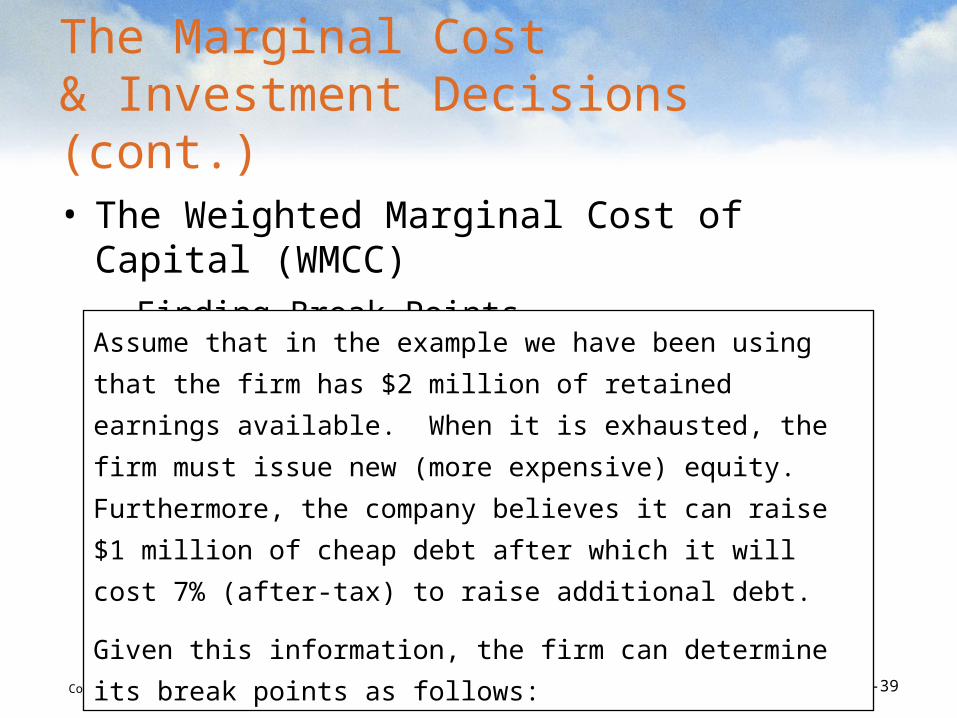

The Marginal Cost & Investment Decisions (cont.)

• The Weighted Marginal Cost of Capital (WMCC)– Finding Break Points

Assume that in the example we have been using that the firm

has $2 million of retained earnings available. When it is

exhausted, the firm must issue new (more expensive) equity.

Furthermore, the company believes it can raise $1 million of

cheap debt after which it will cost 7% (after-tax) to raise

additional debt.

Given this information, the firm can determine its break points as

follows:

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-40

The Marginal Cost & Investment Decisions (cont.)

• The Weighted Marginal Cost of Capital (WMCC)– Finding Break Points

BPequity = $2,000,000/.50 = $4,000,000

BPdebt = $1,000,000/.40 = $2,500,000

This implies that the firm can fund up to $4 million of new investment before it is forced to issue new equity and $2.5 million of new investment before it is forced to raise more expensive debt.

Given this information, we may calculate the WMCC as follows:

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-41

Range of total Source of Weighted

New Financing Capital Weight Cost Cost

$0 to $2.5 million Debt 40% 5.67% 2.268%

Preferred 10% 9.62% 0.962%

Common 50% 15.80% 7.900%

WACC 11.130%

$2.5 to $4.0 million Debt 40% 7.00% 2.800%

Preferred 10% 9.62% 0.962%

Common 50% 15.80% 7.900%

WACC 11.662%

over $4.0 million Debt 40% 7.00% 2.800%

Preferred 10% 9.62% 0.962%

Common 50% 16.00% 8.000%

WACC 11.762%

WACC for Ranges of Total New Financing

The Marginal Cost & Investment Decisions (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-42

$2.5 $4.0 Total Financing (millions)

11.75%

11.25%

11.50%

WMCC11.76%

11.66%

11.13%

The Marginal Cost & Investment Decisions (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-43

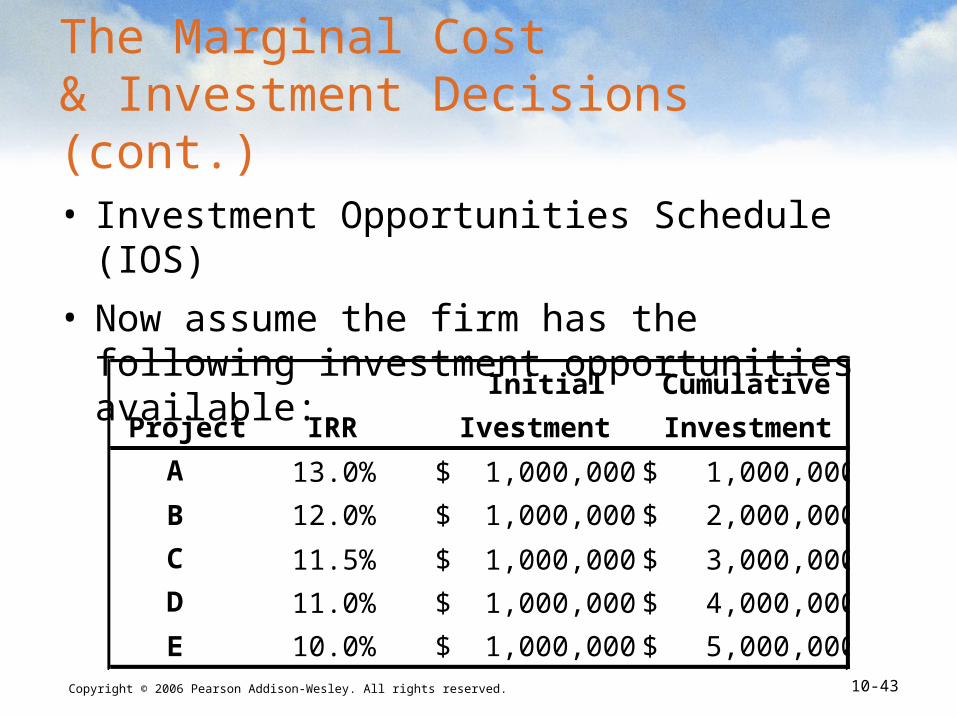

Initial Cumulative

Project IRR Ivestment Investment

A 13.0% 1,000,000$ 1,000,000$

B 12.0% 1,000,000$ 2,000,000$

C 11.5% 1,000,000$ 3,000,000$

D 11.0% 1,000,000$ 4,000,000$

E 10.0% 1,000,000$ 5,000,000$

The Marginal Cost & Investment Decisions (cont.)

• Investment Opportunities Schedule (IOS)

• Now assume the firm has the following investment opportunities available:

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 10-44

$2.5 $4.0 Total Financing (millions)

WMCC

11.66%

11.13%

$1.0

13.0% AB

$2.0 $3.0

C

D

11.5%

11.0%

12.0%

This indicates

that the firm can

accept only

Projects A & B.

The Marginal Cost & Investment Decisions (cont.)