35

chapter 11 Choices Involving Risk Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | mariano-cliff |

| View: | 217 times |

| Download: | 0 times |

chapter 11

Choices Involving Risk

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-2

Learning Objectives

• Define and measure economic risk.• Illustrate an individual’s risk preferences

graphically.• Explain why people purchase insurance policies.• Analyze why people take certain risks and avoid

others.• Identify and explain several strategies for

managing risk.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-3

Overview

• Many decisions involve risk, and it will be useful to define it and measure it with some precision.

• Consumers can have different preferences toward risk.

• Insurance and other methods of managing risk can make some consumers better off.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-4

Possibilities

• State of nature: one possible way in which events relevant to a risky decision can unfold

• When analyzing a risky decision, economist begin by describing every possible state of nature.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-5

Probability

• Probability: measure of the likelihood that a state of nature will occur

• Objective probability: measure of the likelihood that a state of nature will occur based on the frequency with which it has occurred in the past under comparable conditions

• Subjective probability: measure of the likelihood that an event will occur based on subjective judgment

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-6

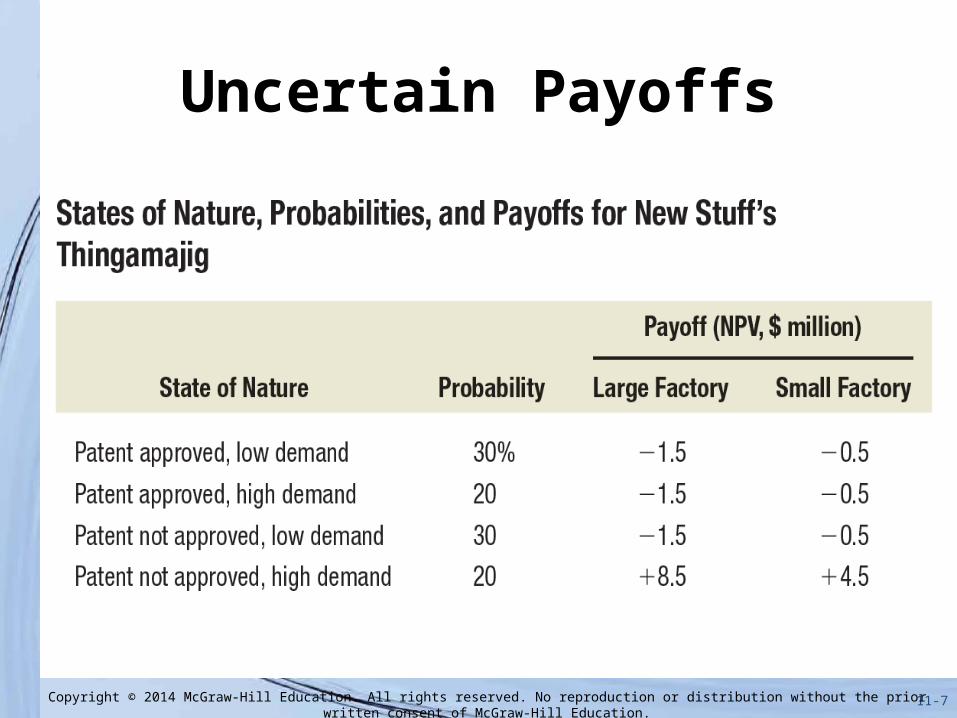

Uncertain Payoffs

• Payoffs are the financial consequences of choices• Probability distribution: the likelihood that each

possible payoff will occur

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-7

Uncertain Payoffs

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-8

Expected Payoff and Variability

• When evaluating a choice with risky financial prospects there are two questions:- What do we expect to gain or lose, on average? Expected

payoff- Do we expect the actual gain or loss to be close to that

average or far from it? Variability

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-9

Expected Payoff

• Expected payoff: weighted average of all the possible payoffs, using the probability of each payoff as its weight

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-10

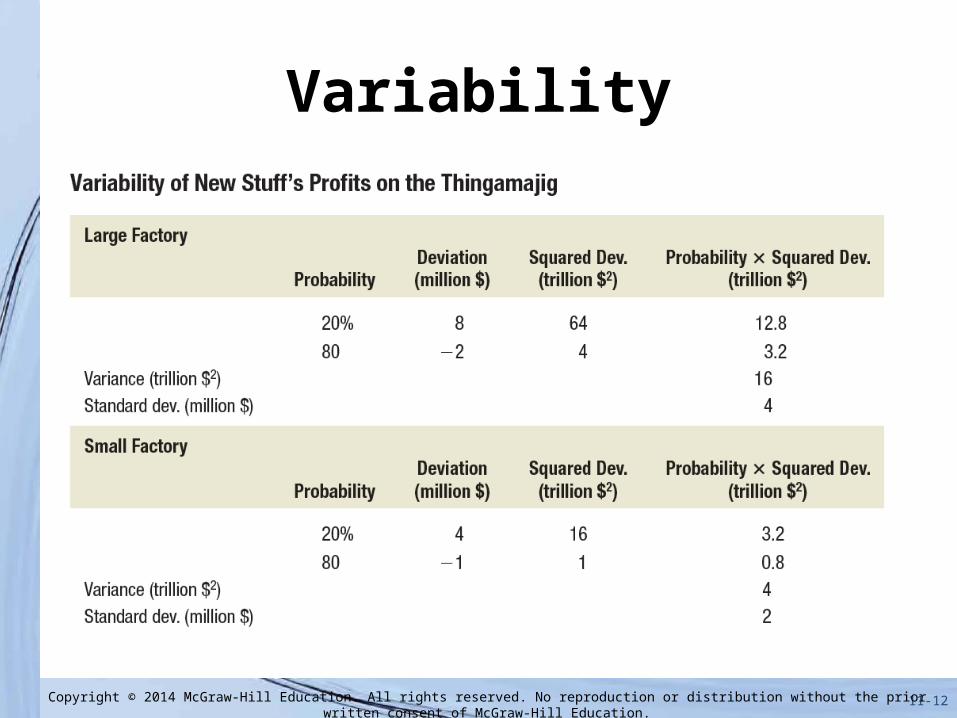

Variability

• Variability: an indication of risk- Little variability: actual payoff is almost always close to the expected payoff- Substantial variability: actual payoff and

expected payoff differ significantly• Deviation: difference between the actual payoff and

the expected payoff• Variance: expected value of a squared deviation• Standard deviation: square root of the variance

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-11

Expected Payoffs and Deviations

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-12

Variability

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-13

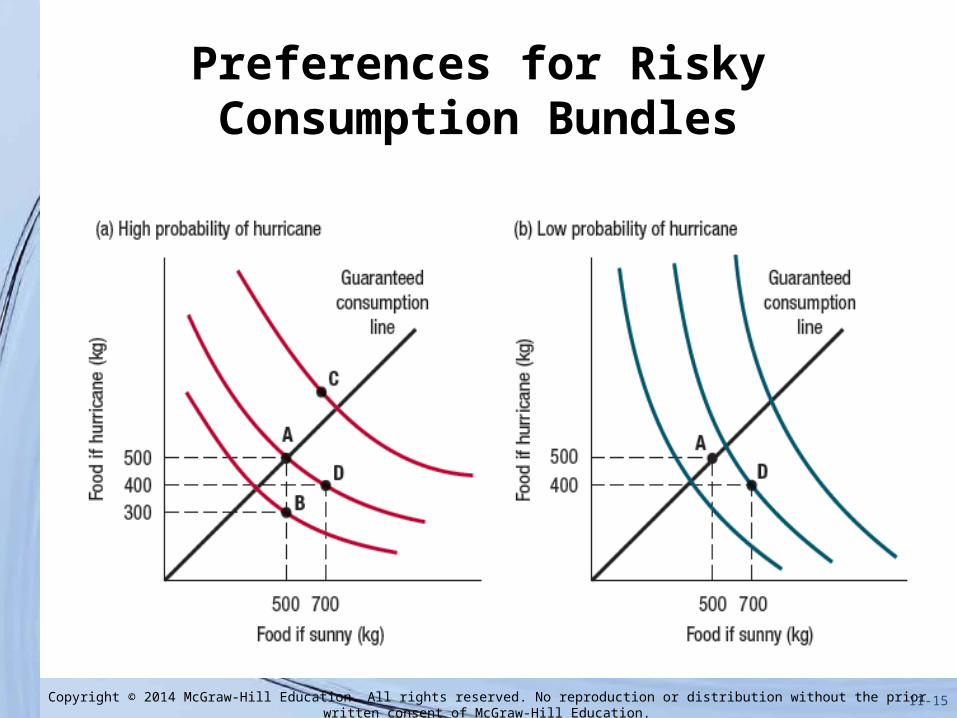

Consumption Bundles

• Guaranteed consumption line: shows the consumption bundles for which the level of consumption does not depend on the state of nature

• For bundles that do not lie on the GCL, the payoff is uncertain

45o line

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-14

Expected Consumption

• Constant expected consumption line: shows all the risky consumption bundles with the same level of expected consumption

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-15

Preferences for Risky Consumption Bundles

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-16

Risk Aversion• When comparing a

riskless bundle with the same level of expected consumption, a risk averse person prefers the riskless bundle (e.g. point A)

• Even a risk averse person may allow for some risk (e.g. point A is preferred to B)

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-17

Certainty Equivalent and the Risk Premium

• Certainty equivalent: the amount of consumption that, if provided with certainty, would make the consumer equally well off

• C is the certainty equivalent of the risky bundle B

• The expected level of consumption is the same at A and B

• Thus, the risk premium is the difference between A and C (expected consumption vs. certainty equivalent)

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-18

Degrees of Risk Aversion• Maria and Arnold are

are both risk averse• Maria would be willing

to swap A for risky bundle D, but Arnold would not– Arnold is more risk

averse than Maria

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-19

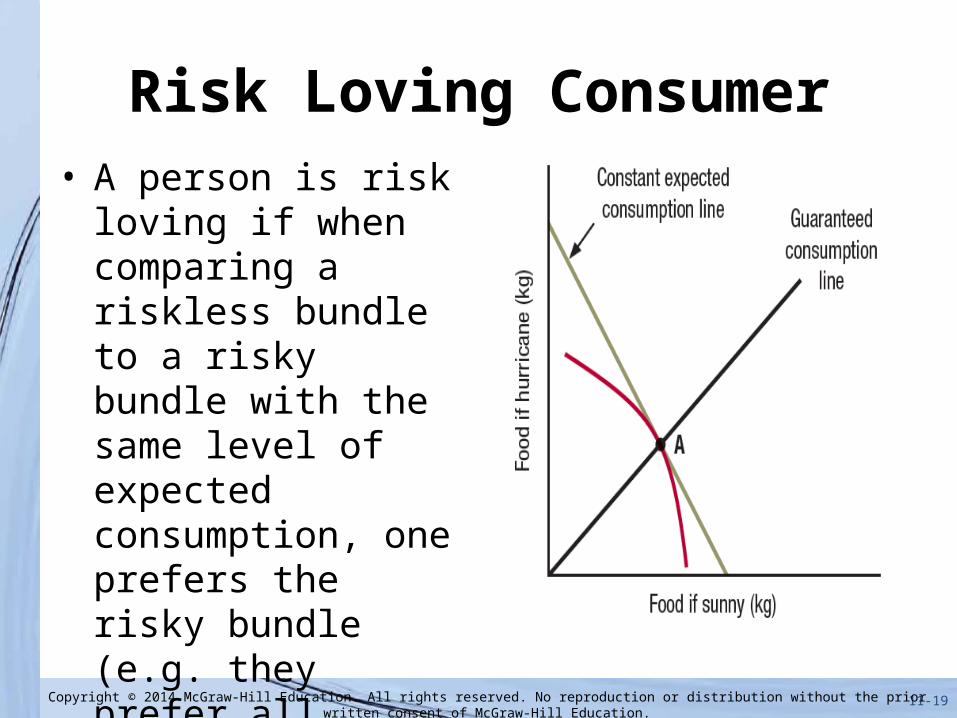

Risk Loving Consumer• A person is risk loving if

when comparing a riskless bundle to a risky bundle with the same level of expected consumption, one prefers the risky bundle (e.g. they prefer all points on this line to point A)

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-20

Risk Neutral Consumer

• Risk neutral: when one is indifferent between all bundles with the same level of expected consumption

• The indifference curves of risk neutral consumers coincide with the constant expected consumption lines

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-21

Expected Utility Functions

• An expected utility function assigns a benefit level to each possible state of nature based only on what is consumed, and then takes the expected value of those benefits

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-22

Expected Utility for a Risk-Averse Consumer

• FH: food when hurricane

• FS: food when sunny• C: risky bundle• E: certainty

equivalent• D: riskless bundle

with same expected consumption on C

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-23

Expected Utility and the Degree of Risk Aversion

• Arnold is more risk averse than Maria

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-24

Nature of Insurance

• Insurance policy: a contract that reduces the financial loss associated with some risky event

• Insurance premium (M): amount of money the policyholder pays for the insurance policy

• Insurance benefit (B): amount of money a policyholder receives if a specific loss occurs

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-25

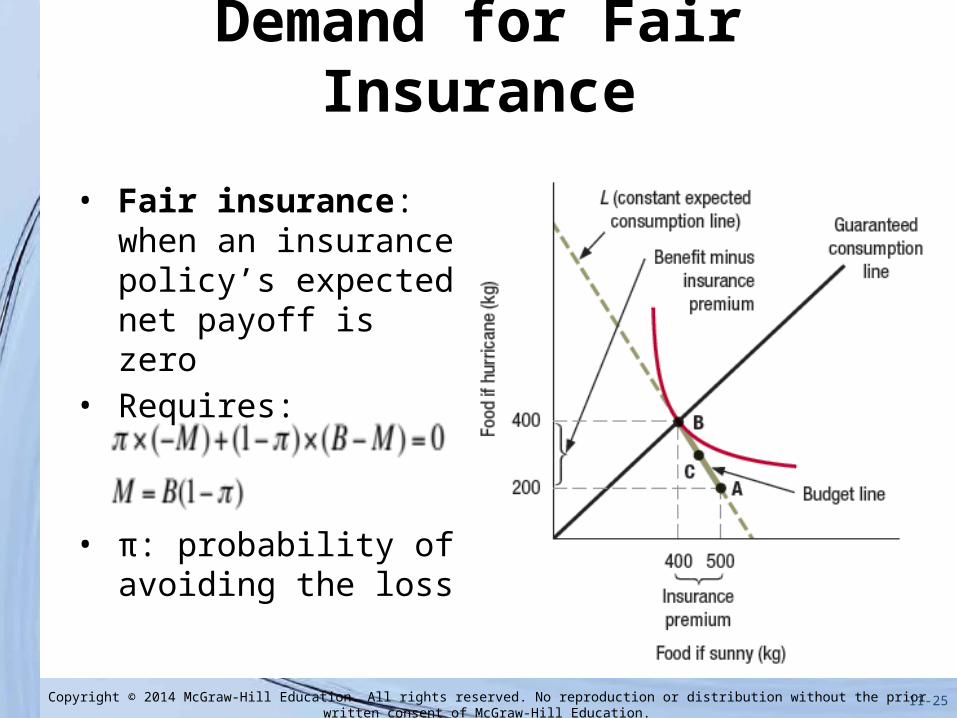

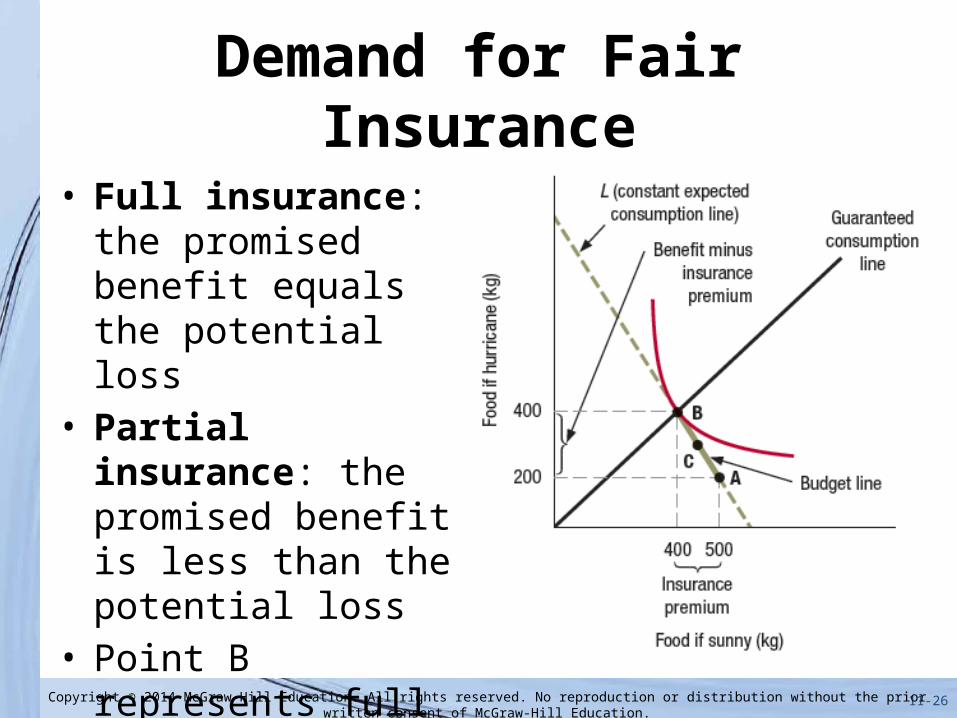

Demand for Fair Insurance

• Fair insurance: when an insurance policy’s expected net payoff is zero

• Requires:

• π: probability of avoiding the loss

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-26

Demand for Fair Insurance

• Full insurance: the promised benefit equals the potential loss

• Partial insurance: the promised benefit is less than the potential loss

• Point B represents full insurance

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-27

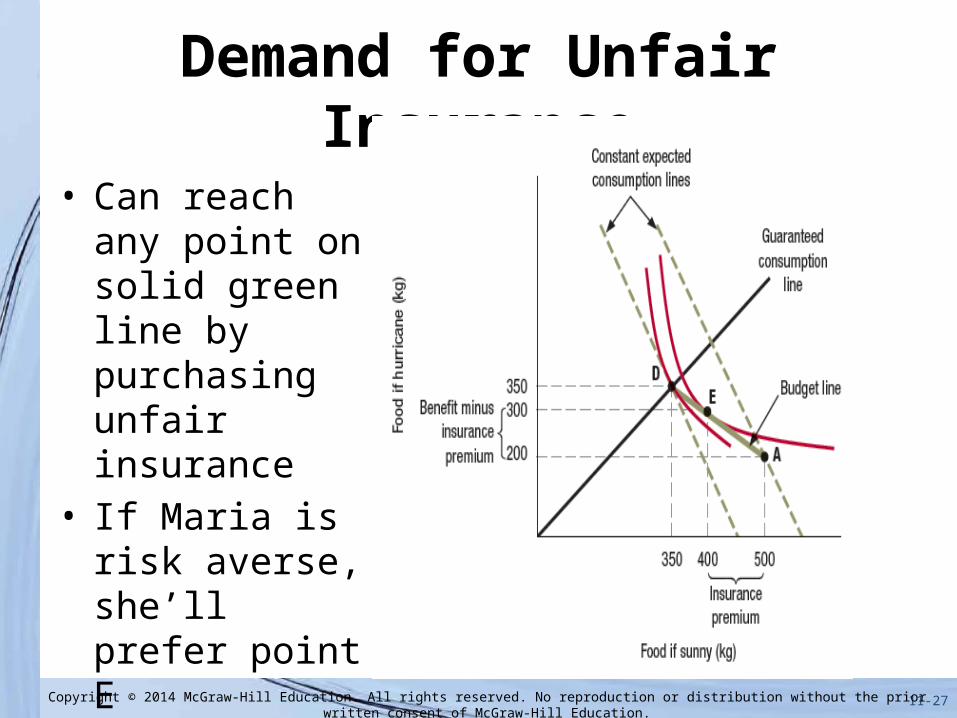

Demand for Unfair Insurance

• Can reach any point on solid green line by purchasing unfair insurance

• If Maria is risk averse, she’ll prefer point E

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-28

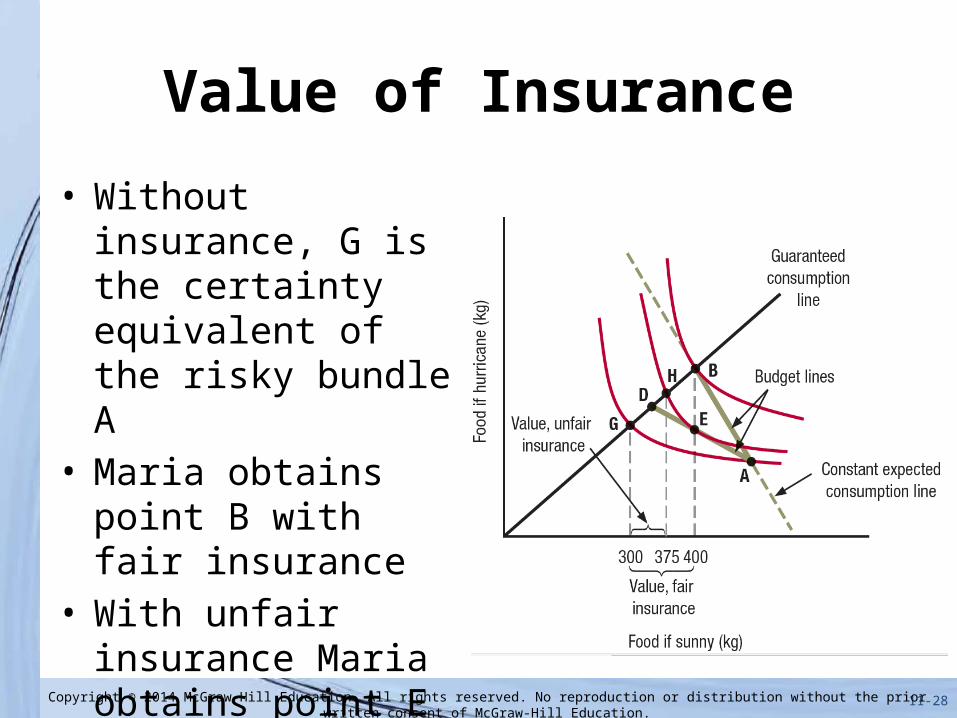

Value of Insurance

• Without insurance, G is the certainty equivalent of the risky bundle A

• Maria obtains point B with fair insurance

• With unfair insurance Maria obtains point E

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-29

Other Methods of Managing Risk

• Risk management: making risky activities more attractive by taking steps to moderate the potential losses while preserving much of the potential gains

1. Risk sharing2. Hedging3. Diversification4. Information acquisition

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-30

Risk Sharing• Risk sharing: dividing a risky

prospect among several people• Maria can make an investment

to swap A for risky bundle B, which provides higher expected consumption

• However, Maria prefers A to B, given her risk aversion

• If Maria finds partners to share the profits and the risk she can be anywhere on the green line in particular reaching D (preferred to A)

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-31

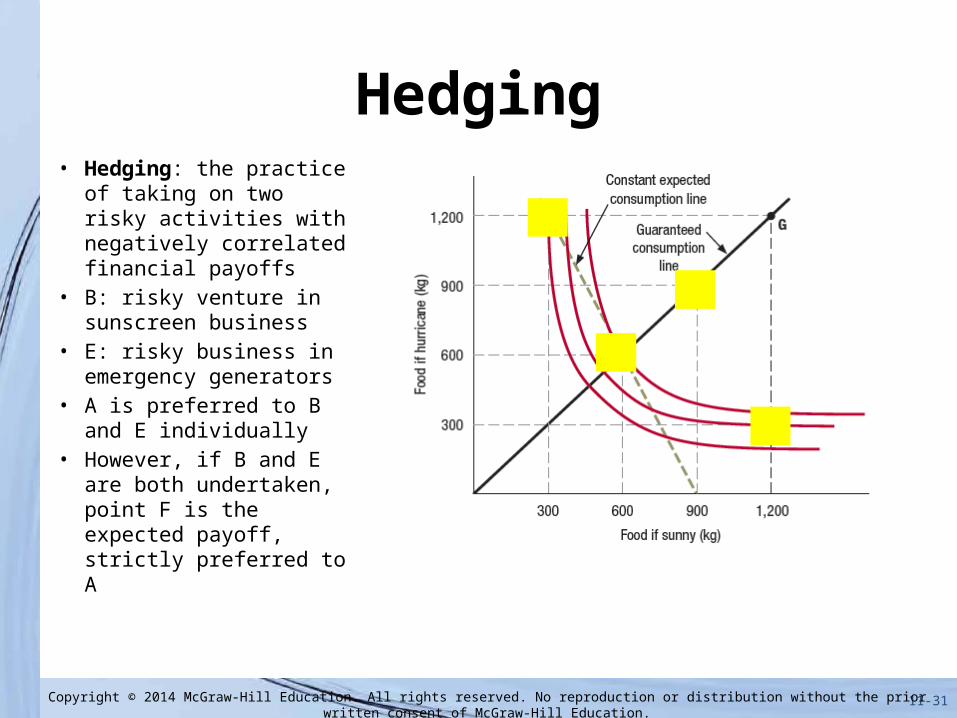

Hedging• Hedging: the practice of

taking on two risky activities with negatively correlated financial payoffs

• B: risky venture in sunscreen business

• E: risky business in emergency generators

• A is preferred to B and E individually

• However, if B and E are both undertaken, point F is the expected payoff, strictly preferred to A

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-32

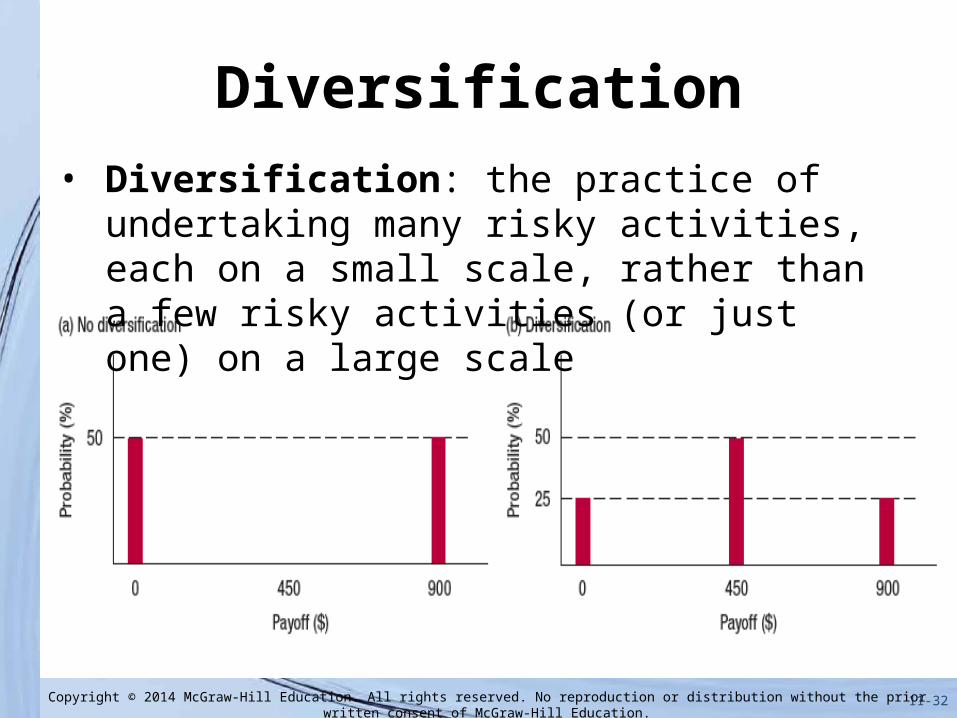

Diversification• Diversification: the practice of undertaking many

risky activities, each on a small scale, rather than a few risky activities (or just one) on a large scale

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-33

Information Acquisition • Individuals often try

to reduce or eliminate risk by acquiring information

• With perfect information about weather, Maria could reach point G

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-34

Review

• A risk averse consumer’s preferred point on any constant expected consumption line lies on the guaranteed consumption line.

• If insurance is actuarially fair, a risk-averse consumer will always purchase full insurance.

• The amount of less-than-actuarially-fair insurance purchased depends on the degree of risk aversion. Those that are not very risk averse will purchase no insurance.

• Risk sharing, hedging, diversification, and information acquisition reduce risk.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

11-35

Looking Forward

• Next we will switch gears, analyzing strategic decisions – situations where the effects of your actions depend on the actions and reactions of other people.

• In particular, we will learn of a specific approach called game theory that is useful in many economic interactions.

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.