Chapter 14: Advanced Derivatives and Strategies. We look at everything. We don’t get scared because of the complexity involved. But we examine it to death. Arvind Sodhani, treasury, Intel Business Week , October 21, 1994, p. 95. Important Concepts in Chapter 14. - PowerPoint PPT Presentation

D. M. Chance An Introduction to Deri vatives and Risk Manage ment, 6th ed. Ch. 14: 1 Chapter 14: Advanced Derivatives and Strategies We look at everything. We don’t get scared because of We look at everything. We don’t get scared because of the complexity involved. But we examine it to death. the complexity involved. But we examine it to death. Arvind Sodhani, treasury, Intel Arvind Sodhani, treasury, Intel Business Week Business Week , October 21, 1994, p. 95 , October 21, 1994, p. 95

Transcript

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 1

Chapter 14: Advanced Derivatives and Strategies

We look at everything. We don’t get scared because of the We look at everything. We don’t get scared because of the complexity involved. But we examine it to death.complexity involved. But we examine it to death.

Arvind Sodhani, treasury, IntelArvind Sodhani, treasury, IntelBusiness WeekBusiness Week, October 21, 1994, p. 95, October 21, 1994, p. 95

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 2

Important Concepts in Chapter 14 The concept of portfolio insurance and its execution using The concept of portfolio insurance and its execution using

puts, calls, futures and t-billsputs, calls, futures and t-bills New and advanced derivatives and strategies such as New and advanced derivatives and strategies such as

equity forwards, warrants, equity-linked debt, structured equity forwards, warrants, equity-linked debt, structured notes, and mortgage securitiesnotes, and mortgage securities

Exotic options such as digital options, chooser options, Exotic options such as digital options, chooser options, Asian options, lookback options, and barrier optionsAsian options, lookback options, and barrier options

Derivatives on electricity and weatherDerivatives on electricity and weather

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 3

Advanced Equity Derivatives and Strategies

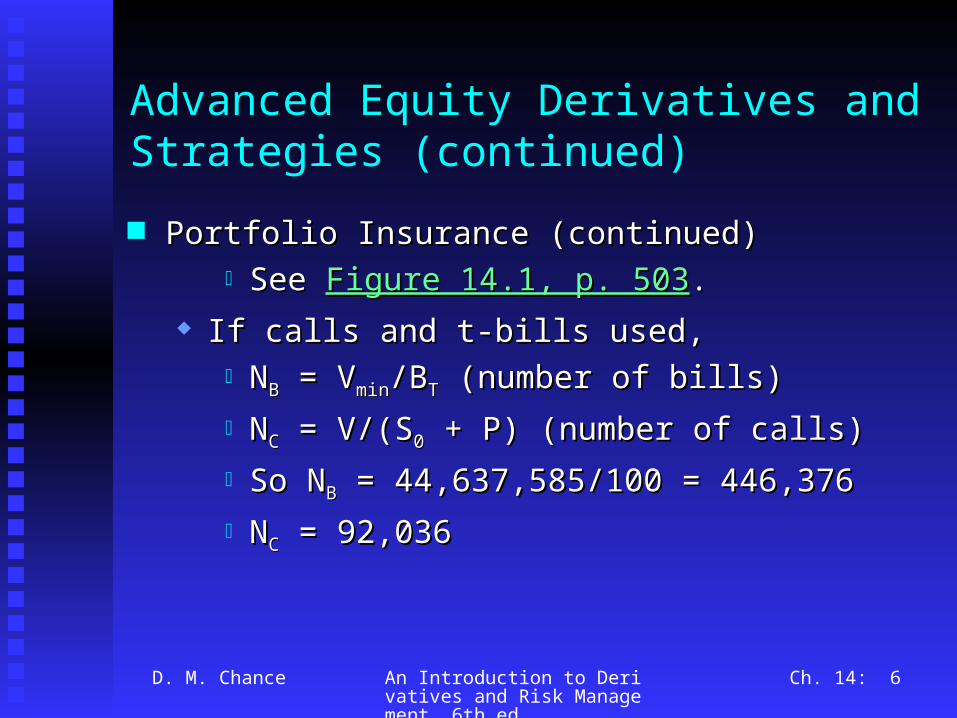

Portfolio InsurancePortfolio Insurance We can insure a portfolio by holding one put for each We can insure a portfolio by holding one put for each

share of stock. For a portfolio worth V, we should holdshare of stock. For a portfolio worth V, we should hold N = V/(SN = V/(S00 + P) puts and shares + P) puts and shares

This will establish a minimum ofThis will establish a minimum of VVminmin = XV/(S = XV/(S00 + P) where X is the exercise price + P) where X is the exercise price

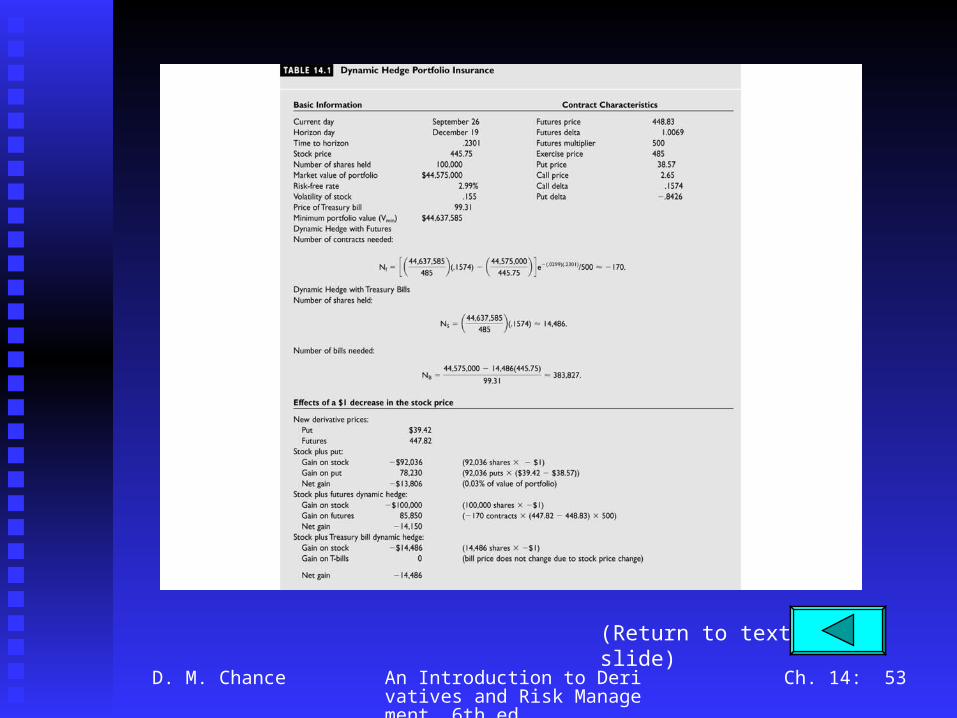

Example: On Sept. 26, market index is 445.75 and Dec Example: On Sept. 26, market index is 445.75 and Dec 485 put is $38.57. Expiration is Dec. 19. Risk-free rate 485 put is $38.57. Expiration is Dec. 19. Risk-free rate is 2.99 % continuously compounded. Volatility is .155.is 2.99 % continuously compounded. Volatility is .155.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 4

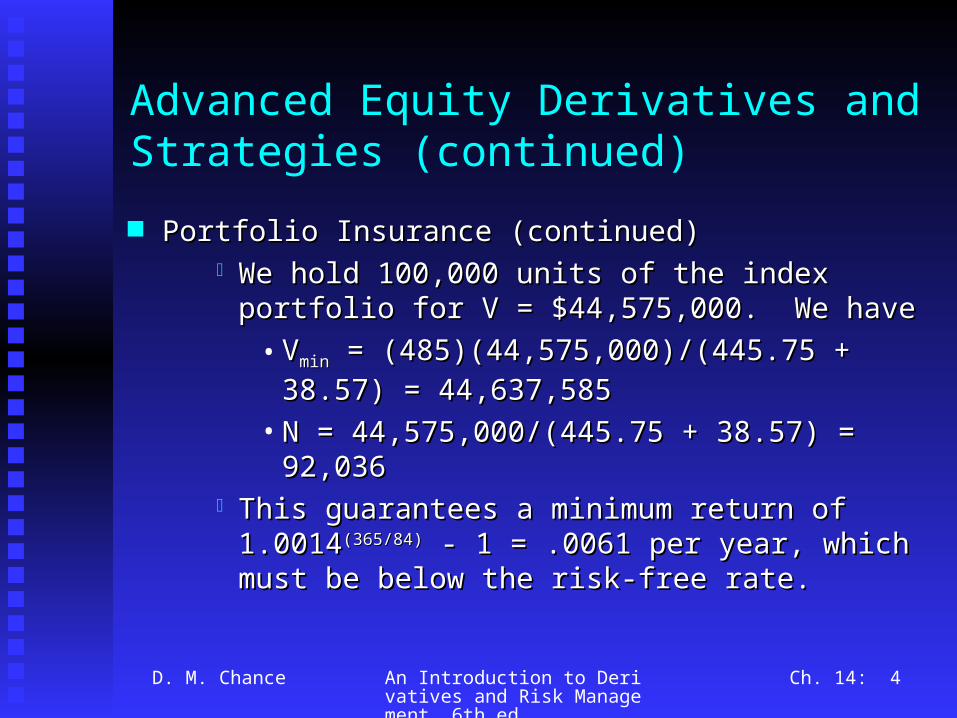

Advanced Equity Derivatives and Strategies (continued)

Portfolio Insurance (continued)Portfolio Insurance (continued) We hold 100,000 units of the index portfolio for V = We hold 100,000 units of the index portfolio for V =

$44,575,000. We have$44,575,000. We have• VVminmin = (485)(44,575,000)/(445.75 + 38.57) = = (485)(44,575,000)/(445.75 + 38.57) =

This guarantees a minimum return of 1.0014This guarantees a minimum return of 1.0014(365/84)(365/84) - - 1 = .0061 per year, which must be below the risk-1 = .0061 per year, which must be below the risk-free rate.free rate.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 5

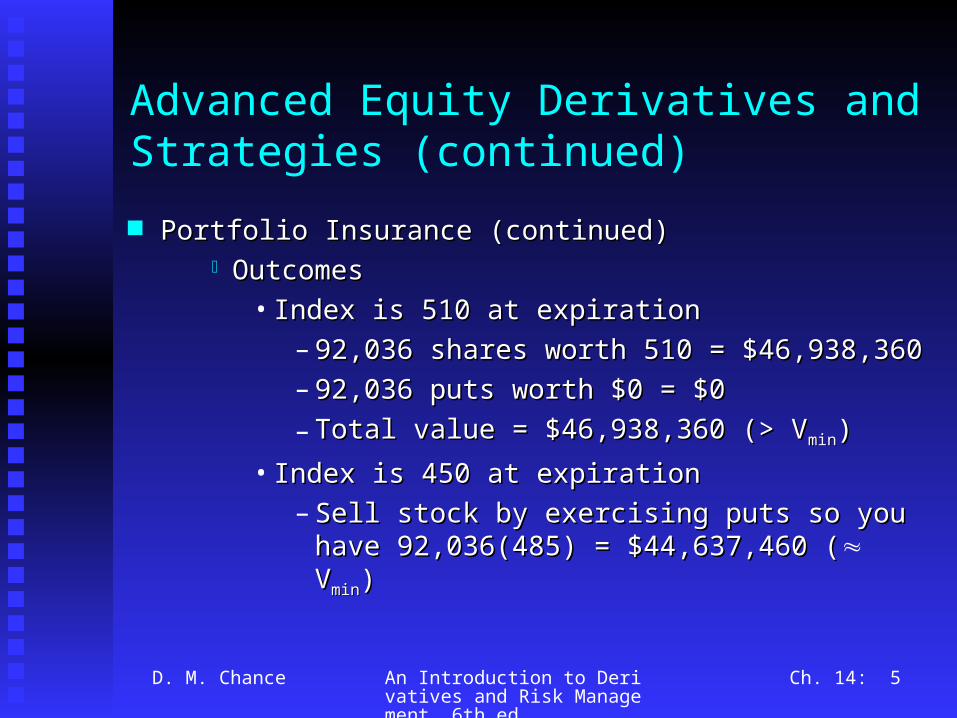

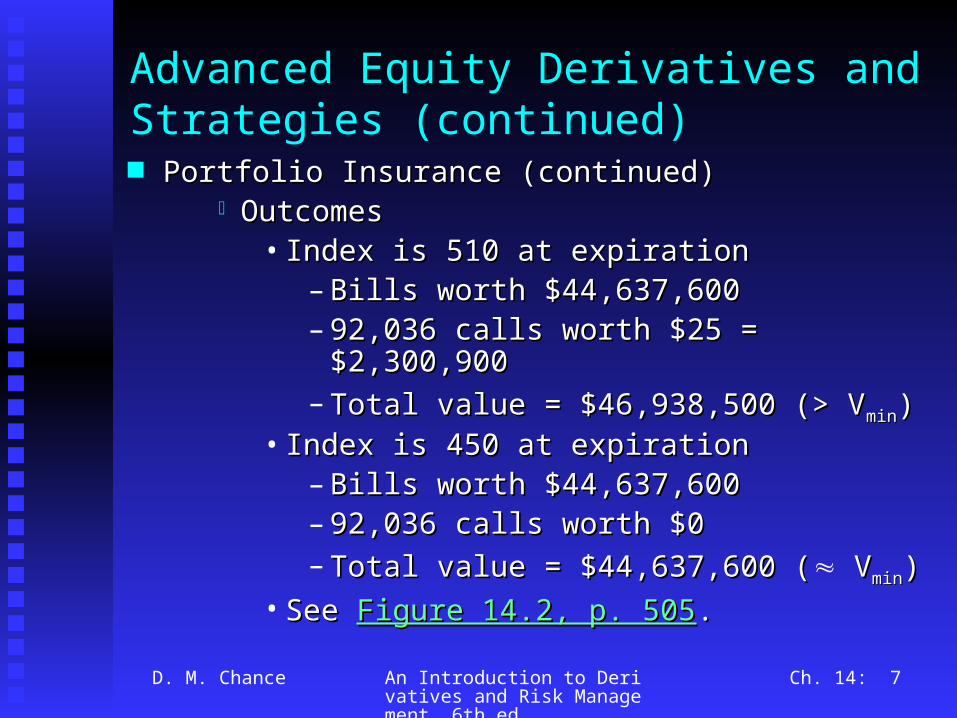

Advanced Equity Derivatives and Strategies (continued)

OutcomesOutcomes• Index is 510 at expirationIndex is 510 at expiration

– Bills worth $44,637,600Bills worth $44,637,600– 92,036 calls worth $25 = $2,300,90092,036 calls worth $25 = $2,300,900– Total value = $46,938,500 (> VTotal value = $46,938,500 (> Vminmin))

• Index is 450 at expirationIndex is 450 at expiration– Bills worth $44,637,600Bills worth $44,637,600– 92,036 calls worth $092,036 calls worth $0– Total value = $44,637,600 (Total value = $44,637,600 ( V Vminmin))

• See See Figure 14.2, p. 505Figure 14.2, p. 505..

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

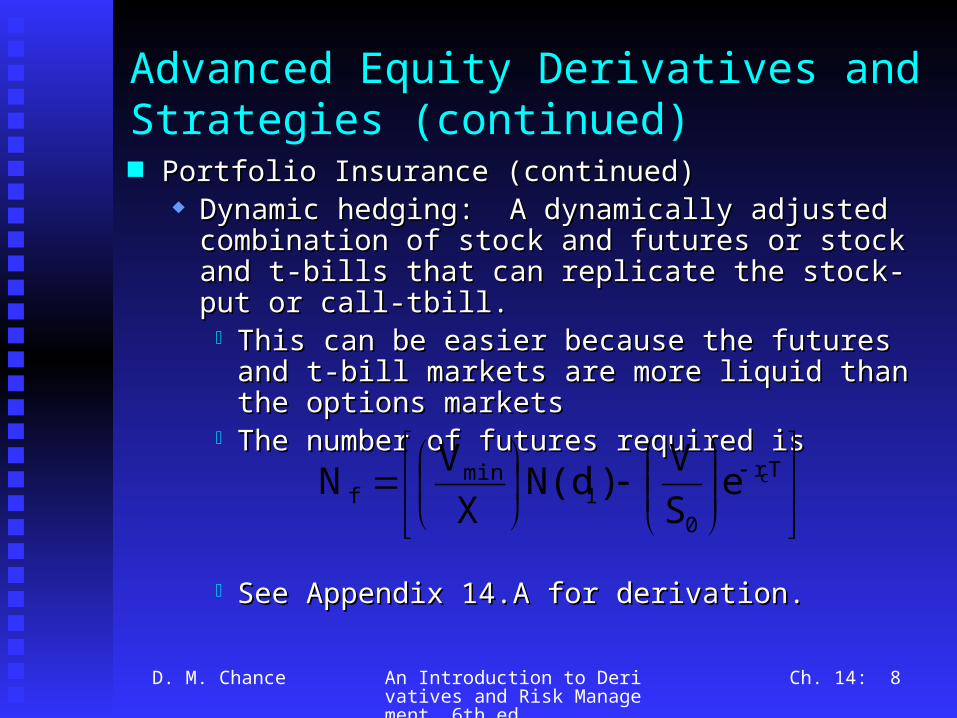

Dynamic hedging: A dynamically adjusted Dynamic hedging: A dynamically adjusted combination of stock and futures or stock and t-bills combination of stock and futures or stock and t-bills that can replicate the stock-put or call-tbill.that can replicate the stock-put or call-tbill. This can be easier because the futures and t-bill This can be easier because the futures and t-bill

markets are more liquid than the options marketsmarkets are more liquid than the options markets The number of futures required isThe number of futures required is

See Appendix 14.A for derivation.See Appendix 14.A for derivation.

Tr

01

minf

ceSV)N(d

XVN

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Alternatively, use stock and t-bills (see Appendix 14.A Alternatively, use stock and t-bills (see Appendix 14.A again for derivation).again for derivation).

See See Table 14.1, p. 507Table 14.1, p. 507 for example of dynamic hedgefor example of dynamic hedge

stock of shares )N(dX

VN

bills- tB

SNVN

1min

S

0SB

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 10

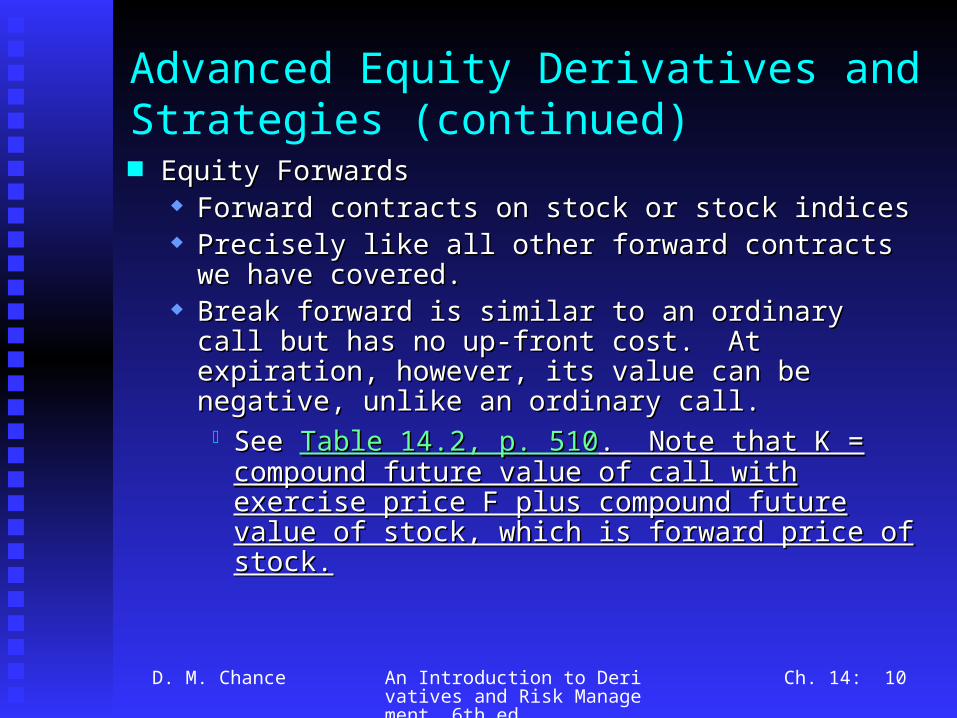

Advanced Equity Derivatives and Strategies (continued) Equity ForwardsEquity Forwards

Forward contracts on stock or stock indicesForward contracts on stock or stock indices Precisely like all other forward contracts we have Precisely like all other forward contracts we have

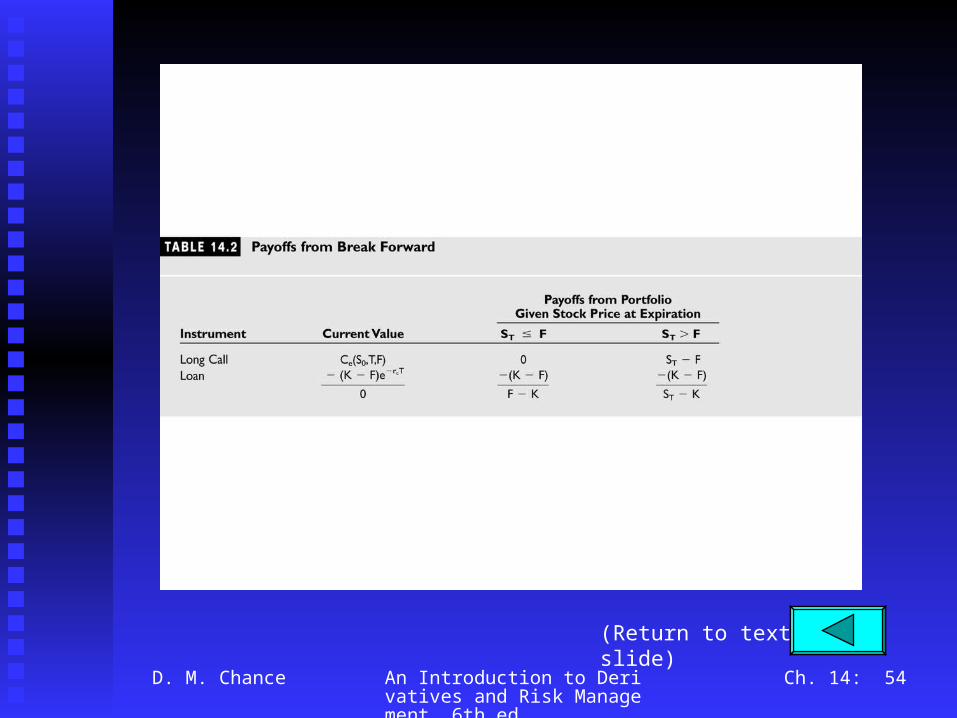

covered.covered. Break forward is similar to an ordinary call but has no Break forward is similar to an ordinary call but has no

up-front cost. At expiration, however, its value can be up-front cost. At expiration, however, its value can be negative, unlike an ordinary call.negative, unlike an ordinary call. See See Table 14.2, p. 510Table 14.2, p. 510. Note that K = compound . Note that K = compound

future value of call with exercise price F plus future value of call with exercise price F plus compound future value of stock, which is forward compound future value of stock, which is forward price of stock.price of stock.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

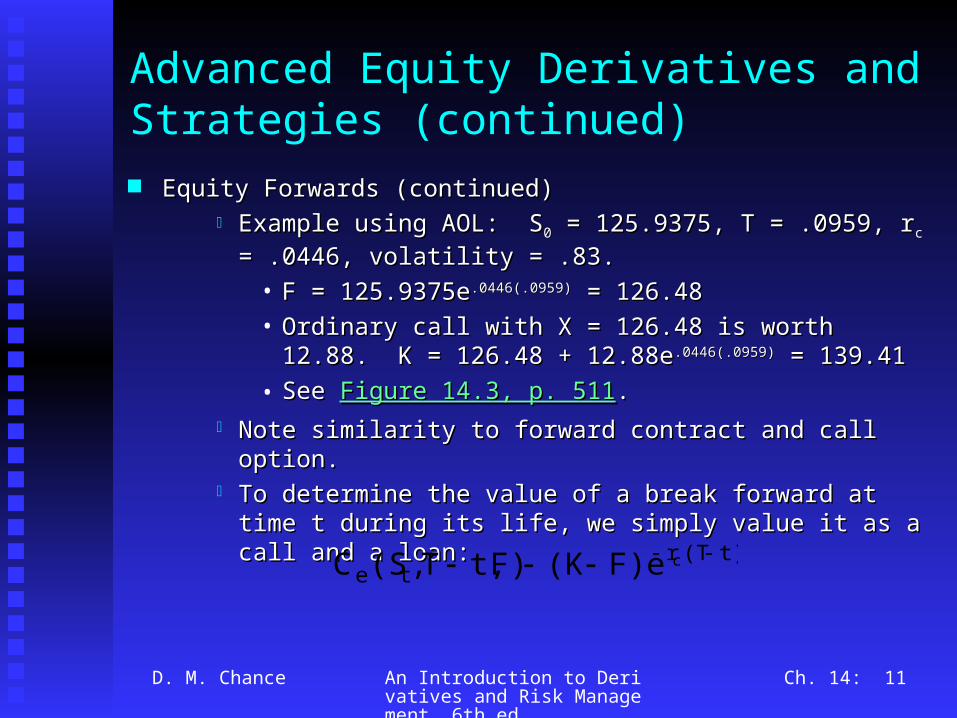

Example using AOL: SExample using AOL: S00 = 125.9375, T = .0959, r = 125.9375, T = .0959, rcc = .0446, = .0446, volatility = .83. volatility = .83.

• F = 125.9375eF = 125.9375e.0446(.0959).0446(.0959) = 126.48 = 126.48• Ordinary call with X = 126.48 is worth 12.88. K = 126.48 Ordinary call with X = 126.48 is worth 12.88. K = 126.48

+ 12.88e+ 12.88e.0446(.0959).0446(.0959) = 139.41 = 139.41• See See Figure 14.3, p. 511Figure 14.3, p. 511..

Note similarity to forward contract and call option.Note similarity to forward contract and call option. To determine the value of a break forward at time t during its To determine the value of a break forward at time t during its

life, we simply value it as a call and a loan:life, we simply value it as a call and a loan:t)(Tr

tecF)e(KF)t,T,(SC

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

For example, 15 days later, AOL is at 115.75, T – t = 20/365 = For example, 15 days later, AOL is at 115.75, T – t = 20/365 = 0.0548, and the other inputs are unchanged. We obtain0.0548, and the other inputs are unchanged. We obtain

A more general version of a break forward is a pay-later option. A more general version of a break forward is a pay-later option. In this case, the buyer simply borrows the premium and has to pay In this case, the buyer simply borrows the premium and has to pay it back at expiration. This option is just an ordinary call plus a it back at expiration. This option is just an ordinary call plus a loan of the call premium Cloan of the call premium Cee(S(S00,T,X). At expiration, the buyer ,T,X). At expiration, the buyer decides whether to exercise the call and in either case pays backdecides whether to exercise the call and in either case pays back

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 13

Advanced Equity Derivatives and Strategies (continued)

Equity WarrantsEquity Warrants Warrants issued by firmWarrants issued by firm Warrants trading on over-the-counter markets and Warrants trading on over-the-counter markets and

American Stock Exchange based on various securities American Stock Exchange based on various securities and indices.and indices.

Many of these are quantos, which pay off based on the Many of these are quantos, which pay off based on the performance of a foreign stock index but payment is performance of a foreign stock index but payment is made in a different currency than the one associated made in a different currency than the one associated with the country of the foreign stock index.with the country of the foreign stock index.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 14

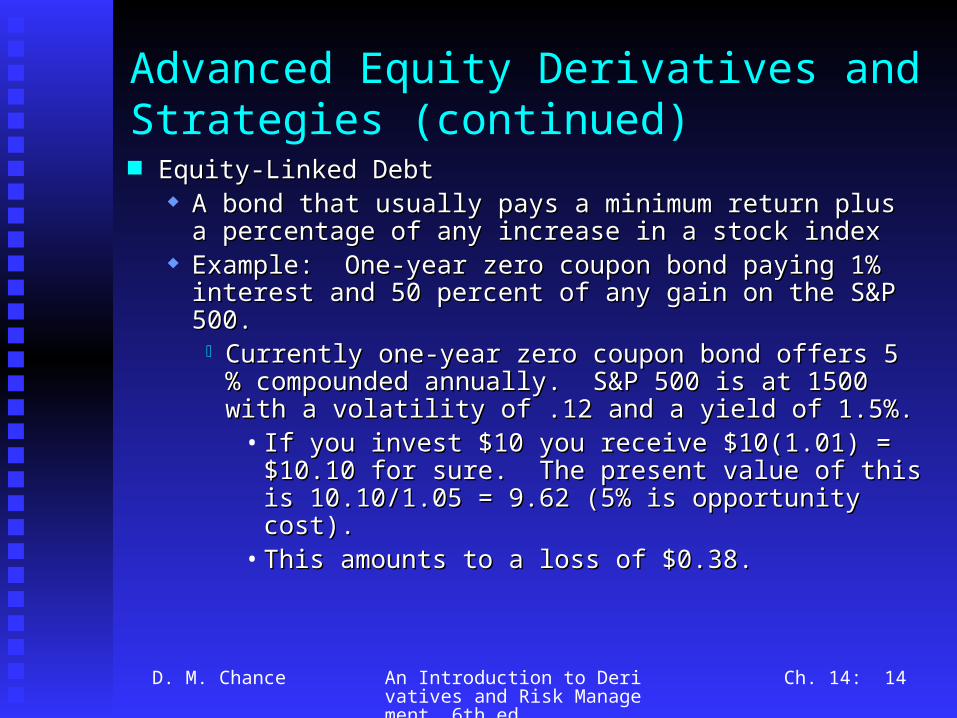

Advanced Equity Derivatives and Strategies (continued) Equity-Linked DebtEquity-Linked Debt

A bond that usually pays a minimum return plus a A bond that usually pays a minimum return plus a percentage of any increase in a stock indexpercentage of any increase in a stock index

Example: One-year zero coupon bond paying 1% Example: One-year zero coupon bond paying 1% interest and 50 percent of any gain on the S&P 500.interest and 50 percent of any gain on the S&P 500. Currently one-year zero coupon bond offers 5 % Currently one-year zero coupon bond offers 5 %

compounded annually. S&P 500 is at 1500 with a compounded annually. S&P 500 is at 1500 with a volatility of .12 and a yield of 1.5%.volatility of .12 and a yield of 1.5%.

• If you invest $10 you receive $10(1.01) = If you invest $10 you receive $10(1.01) = $10.10 for sure. The present value of this is $10.10 for sure. The present value of this is 10.10/1.05 = 9.62 (5% is opportunity cost).10.10/1.05 = 9.62 (5% is opportunity cost).

• This amounts to a loss of $0.38.This amounts to a loss of $0.38.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 15

Advanced Equity Derivatives and Strategies (continued)

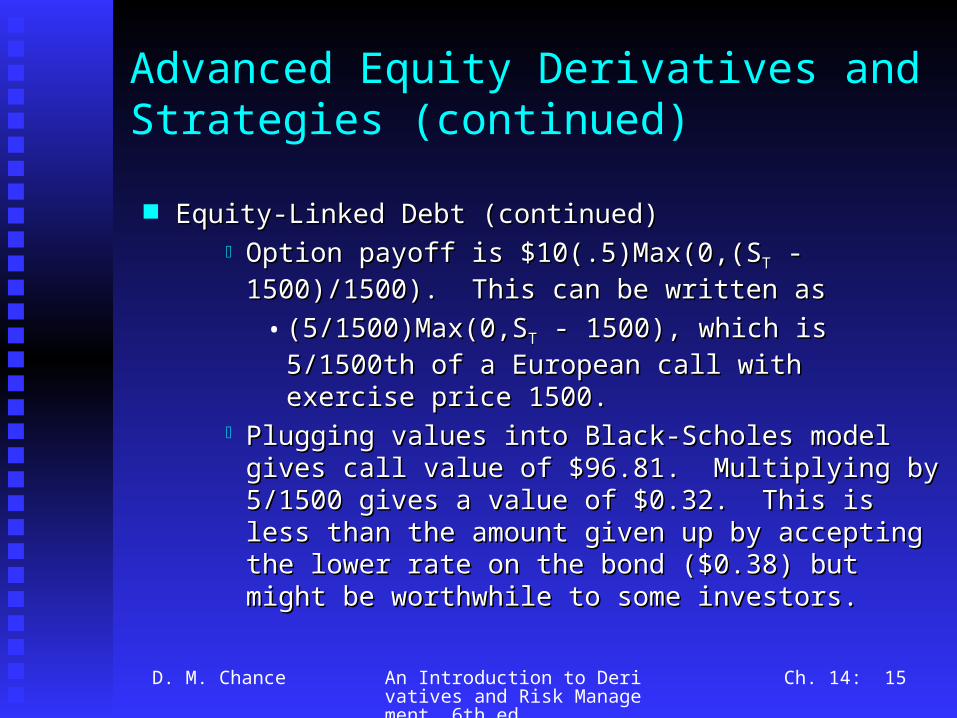

Equity-Linked Debt (continued)Equity-Linked Debt (continued) Option payoff is $10(.5)Max(0,(SOption payoff is $10(.5)Max(0,(STT - 1500)/1500). - 1500)/1500).

This can be written asThis can be written as• (5/1500)Max(0,S(5/1500)Max(0,STT - 1500), which is 5/1500th of - 1500), which is 5/1500th of

a European call with exercise price 1500.a European call with exercise price 1500. Plugging values into Black-Scholes model gives call Plugging values into Black-Scholes model gives call

value of $96.81. Multiplying by 5/1500 gives a value of $96.81. Multiplying by 5/1500 gives a value of $0.32. This is less than the amount given value of $0.32. This is less than the amount given up by accepting the lower rate on the bond ($0.38) up by accepting the lower rate on the bond ($0.38) but might be worthwhile to some investors.but might be worthwhile to some investors.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

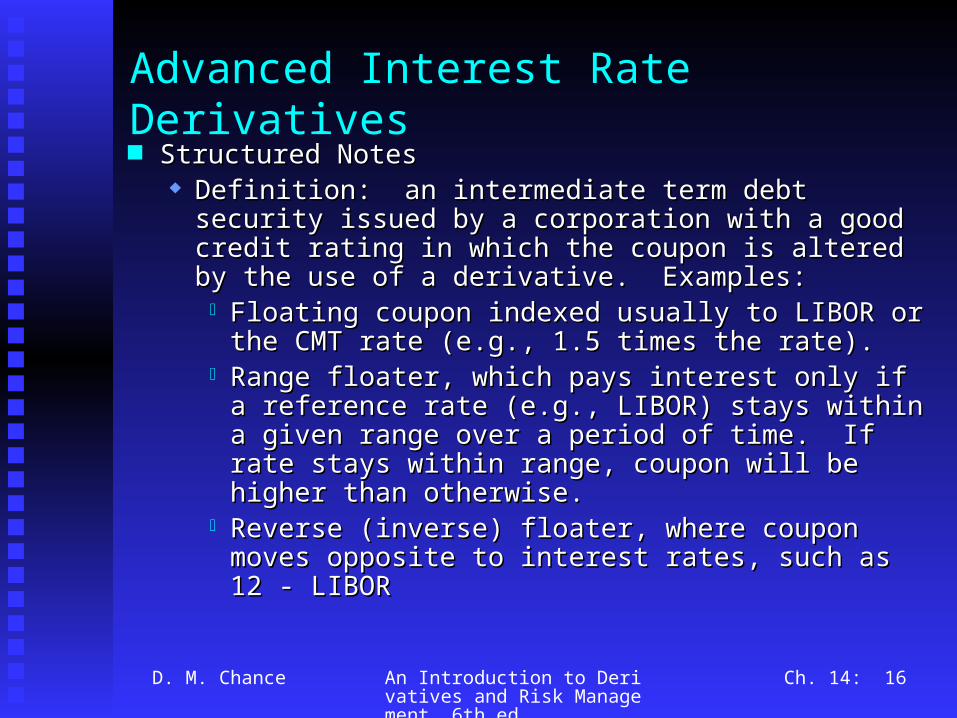

Definition: an intermediate term debt security issued Definition: an intermediate term debt security issued by a corporation with a good credit rating in which the by a corporation with a good credit rating in which the coupon is altered by the use of a derivative. Examples:coupon is altered by the use of a derivative. Examples: Floating coupon indexed usually to LIBOR or the Floating coupon indexed usually to LIBOR or the

CMT rate (e.g., 1.5 times the rate).CMT rate (e.g., 1.5 times the rate). Range floater, which pays interest only if a Range floater, which pays interest only if a

reference rate (e.g., LIBOR) stays within a given reference rate (e.g., LIBOR) stays within a given range over a period of time. If rate stays within range over a period of time. If rate stays within range, coupon will be higher than otherwise.range, coupon will be higher than otherwise.

Reverse (inverse) floater, where coupon moves Reverse (inverse) floater, where coupon moves opposite to interest rates, such as 12 - LIBORopposite to interest rates, such as 12 - LIBOR

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 17

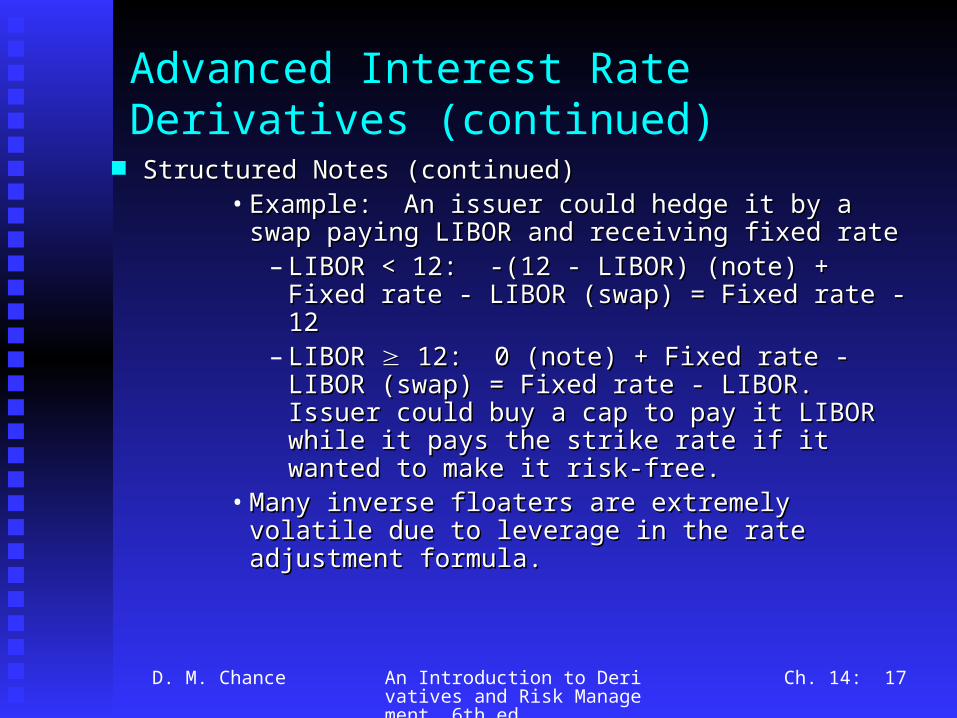

Advanced Interest Rate Derivatives (continued)

Structured Notes (continued)Structured Notes (continued)• Example: An issuer could hedge it by a swap Example: An issuer could hedge it by a swap

(swap) = Fixed rate - LIBOR. Issuer could (swap) = Fixed rate - LIBOR. Issuer could buy a cap to pay it LIBOR while it pays the buy a cap to pay it LIBOR while it pays the strike rate if it wanted to make it risk-free.strike rate if it wanted to make it risk-free.

• Many inverse floaters are extremely volatile due Many inverse floaters are extremely volatile due to leverage in the rate adjustment formula.to leverage in the rate adjustment formula.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Securities constructed by offering claims on a portfolio Securities constructed by offering claims on a portfolio of mortgages, a process called securitization.of mortgages, a process called securitization.

Mortgage-backed securities are subject to prepayment Mortgage-backed securities are subject to prepayment risk.risk.

Mortgage pass-throughs and stripsMortgage pass-throughs and strips Mortgage pass-through: a security in which the Mortgage pass-through: a security in which the

holder receives the principal and interest payments holder receives the principal and interest payments made on a portfolio of mortgages.made on a portfolio of mortgages.

Mortgage strip: a claim on either the principal or Mortgage strip: a claim on either the principal or interest on a mortgage pass-through. Called interest on a mortgage pass-through. Called principal only (PO) or interest only (IO)principal only (PO) or interest only (IO)..

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Example: Assume a mortgage-backed security Example: Assume a mortgage-backed security representing a single $100,000 mortgage at 9.75 % for representing a single $100,000 mortgage at 9.75 % for 30 years. Assume annual payments for simplicity. 30 years. Assume annual payments for simplicity. See See Table 14.3, p. 516Table 14.3, p. 516 for amortization schedule. for amortization schedule.

Annual payment would be Annual payment would be • $100,000/[(1-(1.0975)$100,000/[(1-(1.0975)-30-30)/.0975] = $10,387.)/.0975] = $10,387.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

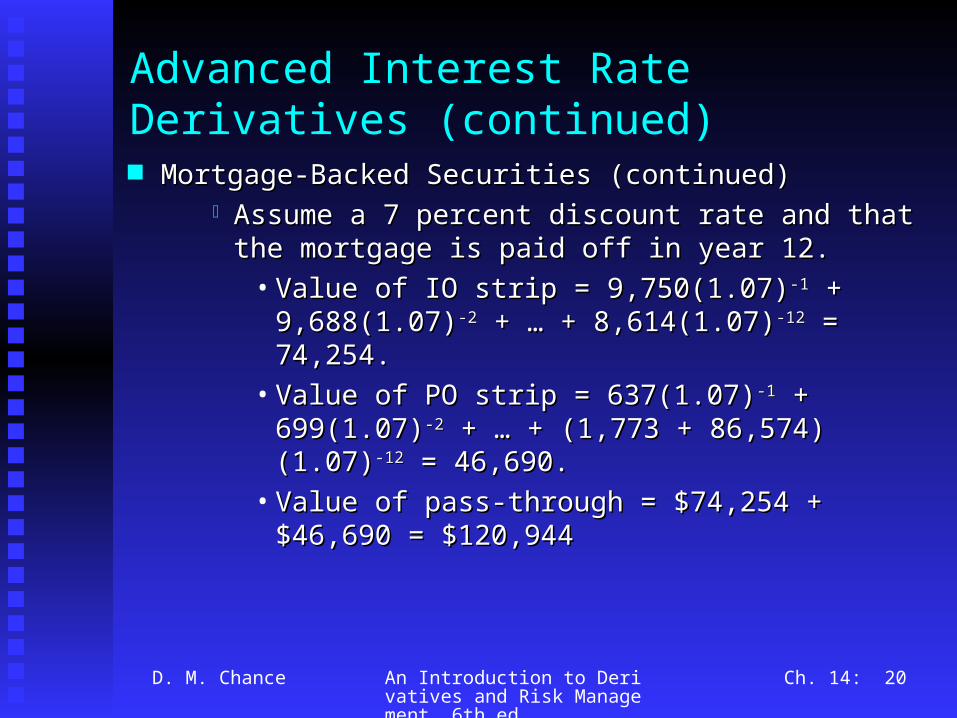

Assume a 7 percent discount rate and that the Assume a 7 percent discount rate and that the mortgage is paid off in year 12.mortgage is paid off in year 12.

• Value of IO strip = 9,750(1.07)Value of IO strip = 9,750(1.07)-1-1 + 9,688(1.07) + 9,688(1.07)-2-2 + … + 8,614(1.07)+ … + 8,614(1.07)-12-12 = 74,254. = 74,254.

• Value of PO strip = 637(1.07)Value of PO strip = 637(1.07)-1-1 + 699(1.07) + 699(1.07)-2-2 + + … + (1,773 + 86,574)(1.07)… + (1,773 + 86,574)(1.07)-12-12 = 46,690. = 46,690.

• Value of pass-through = $74,254 + $46,690 = Value of pass-through = $74,254 + $46,690 = $120,944$120,944

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Let discount rate drop to 6 % and assume Let discount rate drop to 6 % and assume homeowner pays off two years from now. homeowner pays off two years from now.

• Value of IO = $9,750(1.06)Value of IO = $9,750(1.06)-1-1 + $9,688(1.06) + $9,688(1.06)-2-2 = = $17,820, loss of 76%$17,820, loss of 76%

• Value of PO = $637(1.06)Value of PO = $637(1.06)-1-1 + ($699 + $98,663) + ($699 + $98,663)(1.06)(1.06)-2-2 = $89,033, gain of 91% = $89,033, gain of 91%

• Value of pass-through = $17,820 + $89,034 = Value of pass-through = $17,820 + $89,034 = $106,854, loss of 12%$106,854, loss of 12%

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

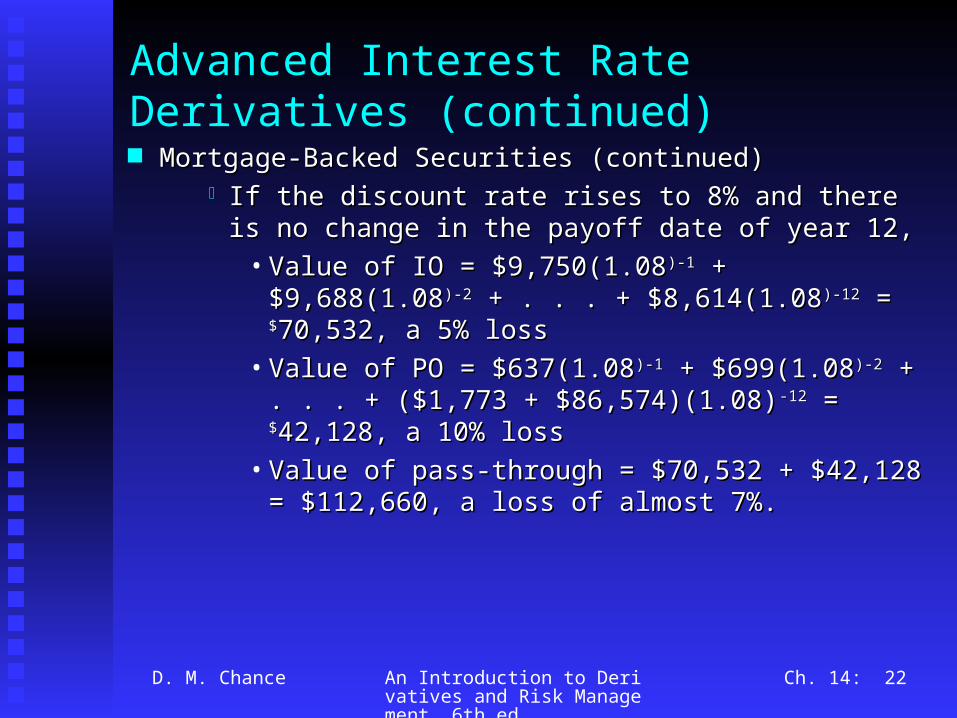

If the discount rate rises to 8% and there is no If the discount rate rises to 8% and there is no change in the payoff date of year 12,change in the payoff date of year 12,

• Value of IO = $9,750(1.08Value of IO = $9,750(1.08)-1)-1 + $9,688(1.08 + $9,688(1.08)-2)-2 + . . . + $8,614(1.08+ . . . + $8,614(1.08)-12)-12 = = $$70,532, a 5% loss70,532, a 5% loss

• Value of PO = $637(1.08Value of PO = $637(1.08)-1)-1 + $699(1.08 + $699(1.08)-2)-2 + . . . + . . . + ($1,773 + $86,574)(1.08)+ ($1,773 + $86,574)(1.08)-12-12 = = $$42,128, a 10% 42,128, a 10% lossloss

• Value of pass-through = $70,532 + $42,128 = Value of pass-through = $70,532 + $42,128 = $112,660, a loss of almost 7%.$112,660, a loss of almost 7%.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

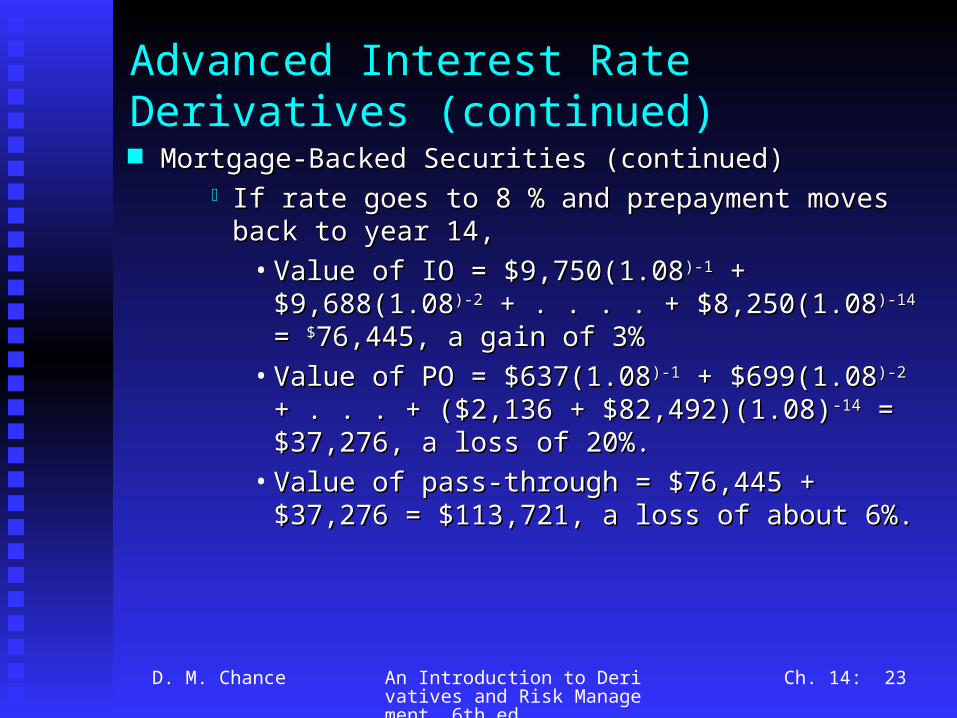

If rate goes to 8 % and prepayment moves back to If rate goes to 8 % and prepayment moves back to year 14, year 14,

• Value of IO = $9,750(1.08Value of IO = $9,750(1.08)-1)-1 + $9,688(1.08 + $9,688(1.08)-2)-2 + . . . . + $8,250(1.08+ . . . . + $8,250(1.08)-14)-14 = = $$76,445, a gain of 3%76,445, a gain of 3%

• Value of PO = $637(1.08Value of PO = $637(1.08)-1)-1 + $699(1.08 + $699(1.08)-2)-2 + . . . + . . . + ($2,136 + $82,492)(1.08)+ ($2,136 + $82,492)(1.08)-14-14 = $37,276, a loss = $37,276, a loss of 20%.of 20%.

• Value of pass-through = $76,445 + $37,276 = Value of pass-through = $76,445 + $37,276 = $113,721, a loss of about 6%.$113,721, a loss of about 6%.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

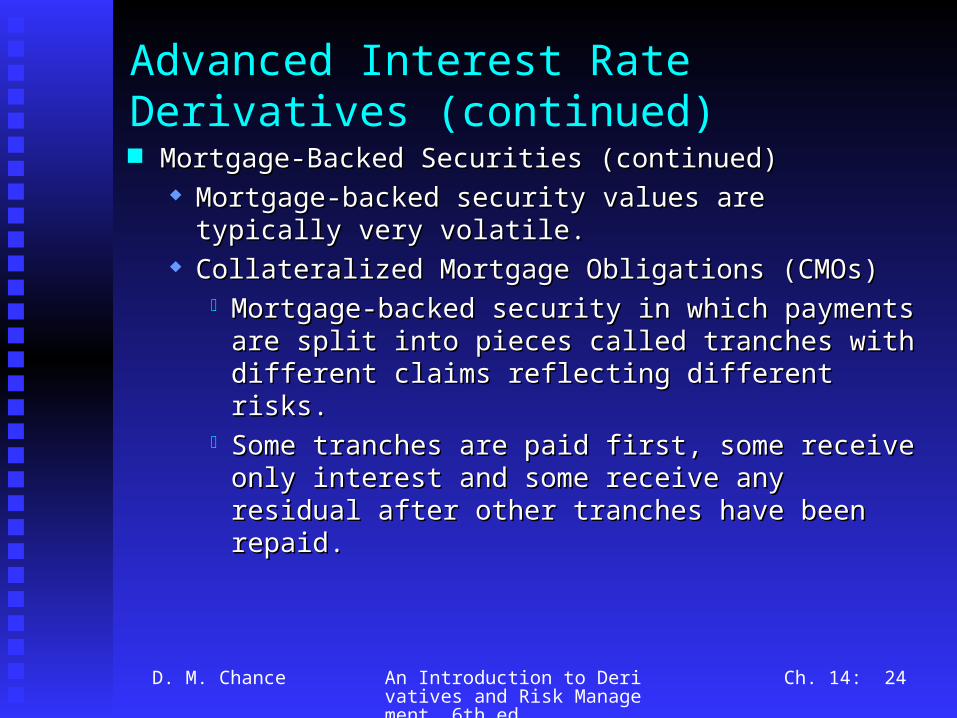

Mortgage-backed security values are typically very Mortgage-backed security values are typically very volatile.volatile.

Collateralized Mortgage Obligations (CMOs)Collateralized Mortgage Obligations (CMOs) Mortgage-backed security in which payments are Mortgage-backed security in which payments are

split into pieces called tranches with different claims split into pieces called tranches with different claims reflecting different risks.reflecting different risks.

Some tranches are paid first, some receive only Some tranches are paid first, some receive only interest and some receive any residual after other interest and some receive any residual after other tranches have been repaid.tranches have been repaid.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

(continued)(continued) The different tranches receive interest, principal and The different tranches receive interest, principal and

prepayments according to different priorities.prepayments according to different priorities. Some CMO tranches are extremely volatile and Some CMO tranches are extremely volatile and

others have low volatility.others have low volatility. A CMO is generally a fairly complex security.A CMO is generally a fairly complex security.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 26

Exotic Options

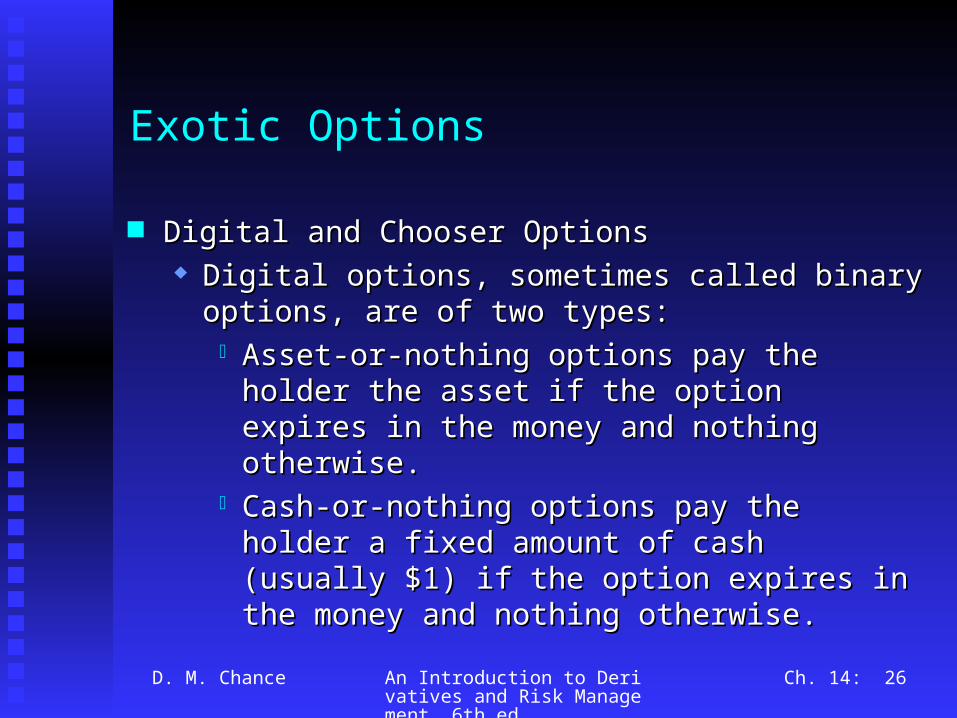

Digital and Chooser OptionsDigital and Chooser Options Digital options, sometimes called binary options, are of Digital options, sometimes called binary options, are of

two types:two types: Asset-or-nothing options pay the holder the asset if Asset-or-nothing options pay the holder the asset if

the option expires in the money and nothing the option expires in the money and nothing otherwise.otherwise.

Cash-or-nothing options pay the holder a fixed Cash-or-nothing options pay the holder a fixed amount of cash (usually $1) if the option expires in amount of cash (usually $1) if the option expires in the money and nothing otherwise.the money and nothing otherwise.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 27

Exotic Options (continued)

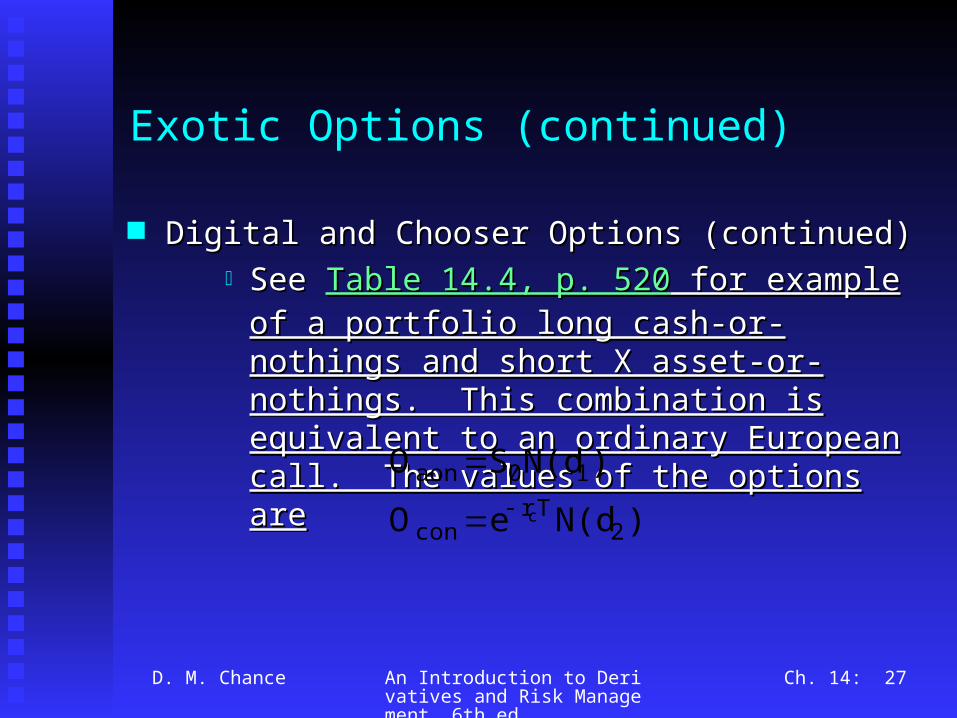

Digital and Chooser Options (continued)Digital and Chooser Options (continued) See See Table 14.4, p. 520Table 14.4, p. 520 for example of a portfolio for example of a portfolio

long cash-or-nothings and short X asset-or-nothings. long cash-or-nothings and short X asset-or-nothings. This combination is equivalent to an ordinary This combination is equivalent to an ordinary European call. The values of the options areEuropean call. The values of the options are

)N(deO

)N(dSO

2Tr

con

10aon

c

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 28

Exotic Options (continued)

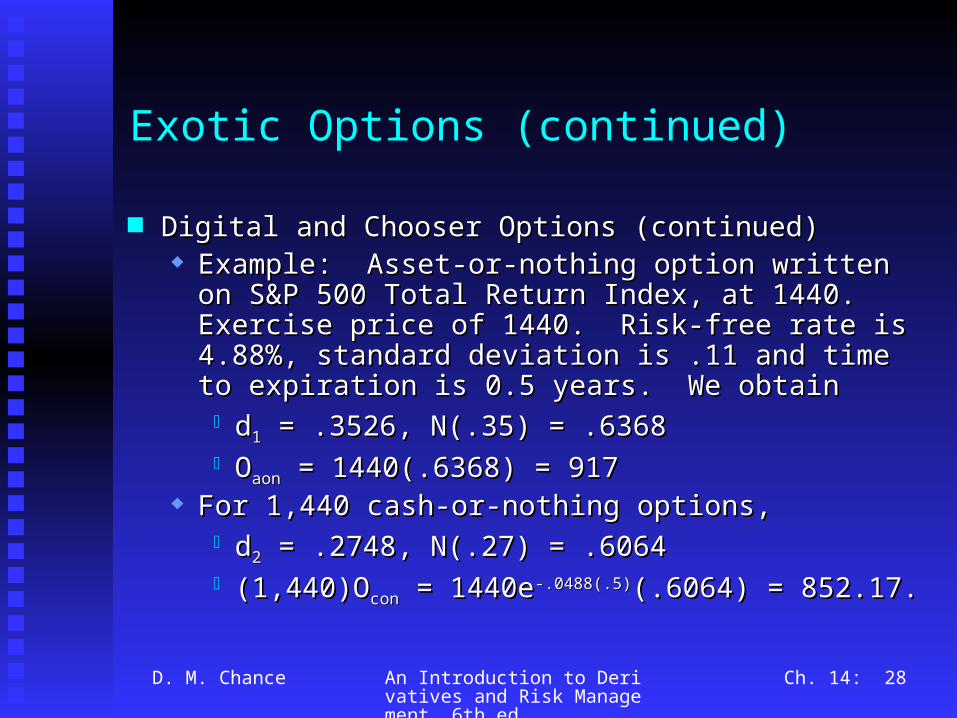

Digital and Chooser Options (continued)Digital and Chooser Options (continued) Example: Asset-or-nothing option written on S&P 500 Example: Asset-or-nothing option written on S&P 500

Total Return Index, at 1440. Exercise price of 1440. Total Return Index, at 1440. Exercise price of 1440. Risk-free rate is 4.88%, standard deviation is .11 and Risk-free rate is 4.88%, standard deviation is .11 and time to expiration is 0.5 years. We obtaintime to expiration is 0.5 years. We obtain dd11 = .3526, N(.35) = .6368 = .3526, N(.35) = .6368 OOaonaon = 1440(.6368) = 917 = 1440(.6368) = 917

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 29

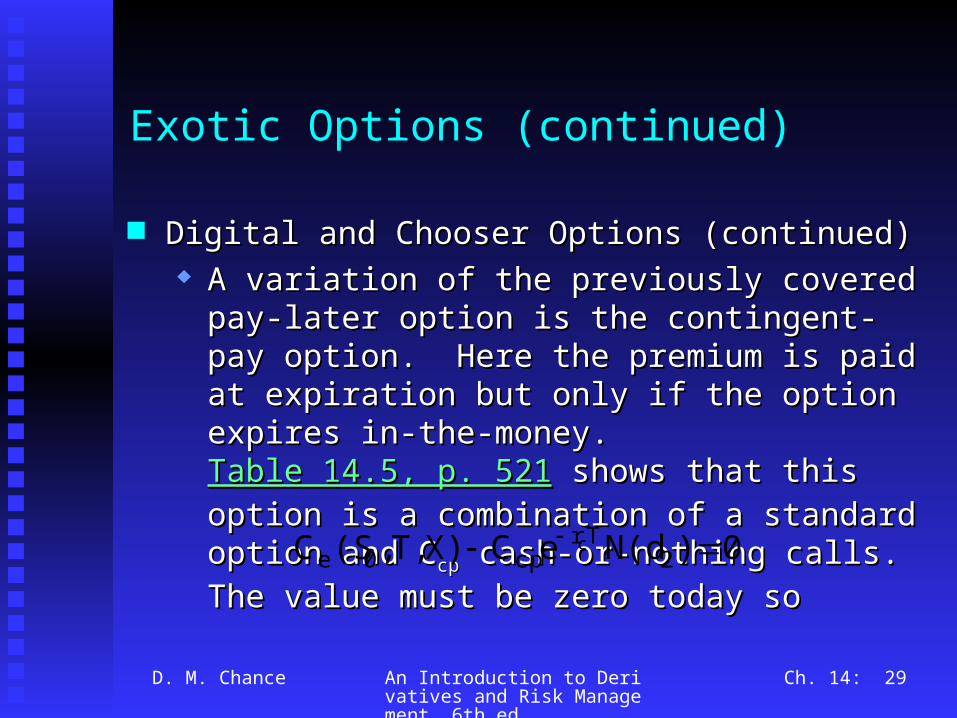

Exotic Options (continued)

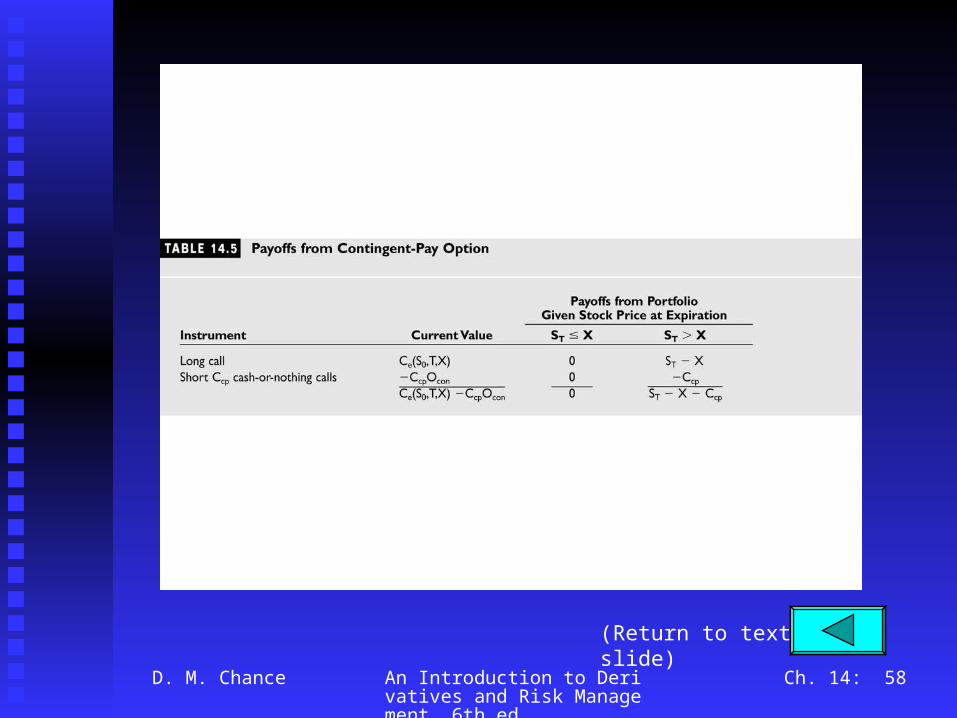

Digital and Chooser Options (continued)Digital and Chooser Options (continued) A variation of the previously covered pay-later option A variation of the previously covered pay-later option

is the contingent-pay option. Here the premium is paid is the contingent-pay option. Here the premium is paid at expiration but only if the option expires in-the-at expiration but only if the option expires in-the-money. money. Table 14.5, p. 521Table 14.5, p. 521 shows that this option is a shows that this option is a combination of a standard option and Ccombination of a standard option and Ccpcp cash-or- cash-or-nothing calls. The value must be zero today sonothing calls. The value must be zero today so

0)N(deCX)T,,(SC 2Tr

cp0ec

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 30

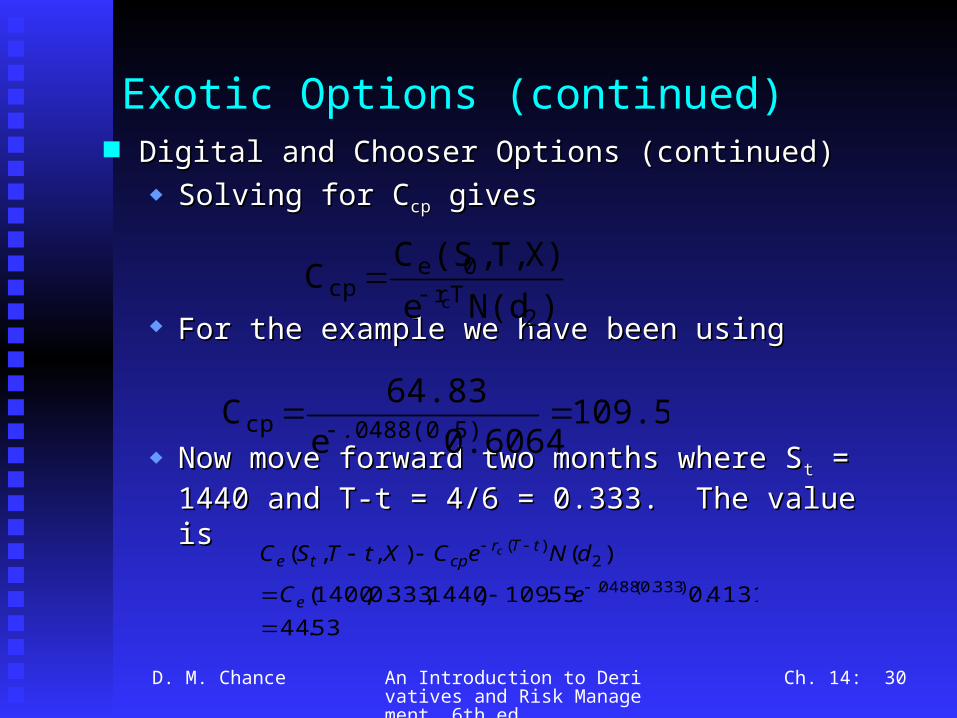

Exotic Options (continued) Digital and Chooser Options (continued)Digital and Chooser Options (continued)

Solving for CSolving for Ccpcp gives gives

For the example we have been usingFor the example we have been using

Now move forward two months where SNow move forward two months where Stt = 1440 and T- = 1440 and T-t = 4/6 = 0.333. The value is t = 4/6 = 0.333. The value is

)N(deX)T,,(SC

C2

Tr0e

cpc

109.550.6064e

64.83C .0488(0.5)cp

53.444131.055.109)1440,333.0,1400(

)(),,()333.0(0488.

2)(

eC

dNeCXtTSC

e

tTrcpte

c

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 31

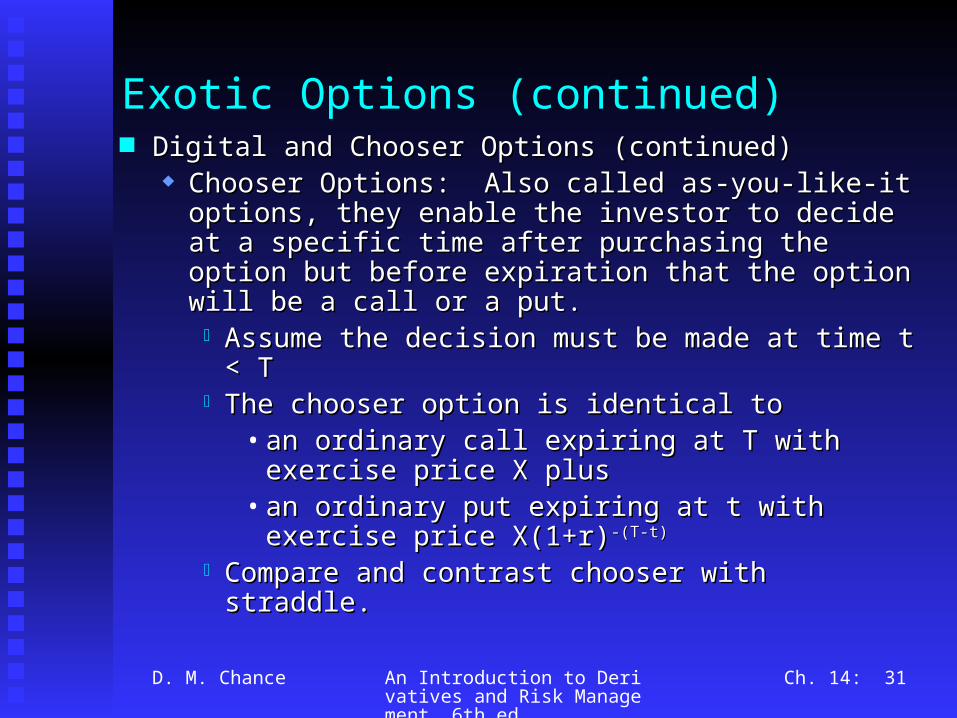

Exotic Options (continued) Digital and Chooser Options (continued)Digital and Chooser Options (continued)

Chooser Options: Also called as-you-like-it options, Chooser Options: Also called as-you-like-it options, they enable the investor to decide at a specific time they enable the investor to decide at a specific time after purchasing the option but before expiration that after purchasing the option but before expiration that the option will be a call or a put.the option will be a call or a put. Assume the decision must be made at time t < TAssume the decision must be made at time t < T The chooser option is identical to The chooser option is identical to

• an ordinary call expiring at T with exercise price an ordinary call expiring at T with exercise price X plusX plus

• an ordinary put expiring at t with exercise price an ordinary put expiring at t with exercise price X(1+r)X(1+r)-(T-t)-(T-t)

Compare and contrast chooser with straddle.Compare and contrast chooser with straddle.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 32

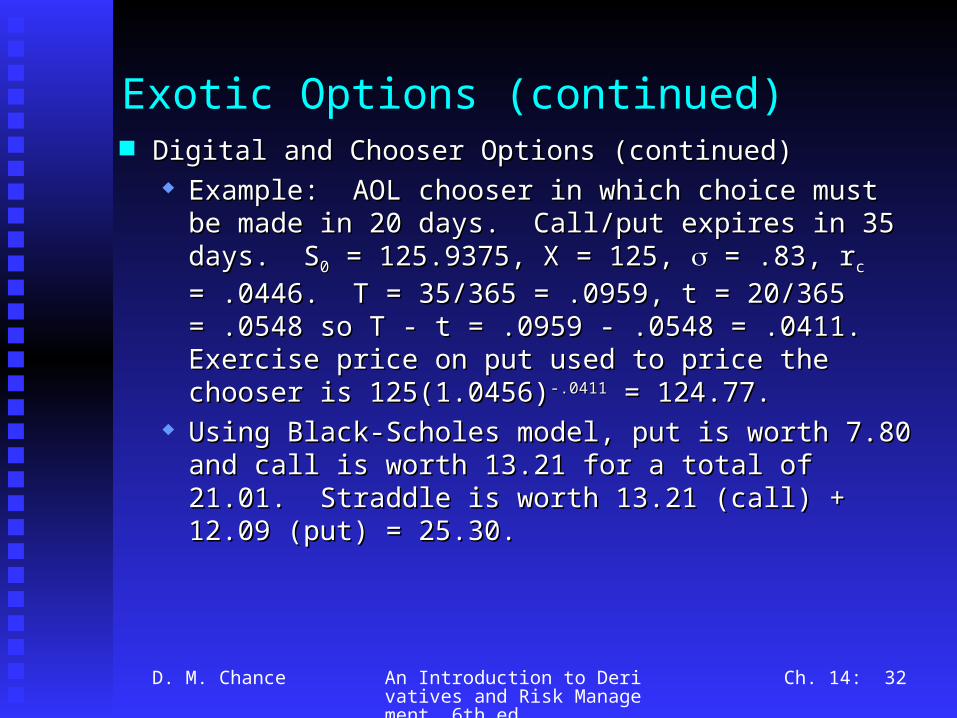

Exotic Options (continued) Digital and Chooser Options (continued)Digital and Chooser Options (continued)

Example: AOL chooser in which choice must be made Example: AOL chooser in which choice must be made in 20 days. Call/put expires in 35 days. Sin 20 days. Call/put expires in 35 days. S00 = 125.9375, = 125.9375, X = 125, X = 125, = .83, r = .83, rcc = .0446. T = 35/365 = .0959, t = = .0446. T = 35/365 = .0959, t = 20/365 = .0548 so T - t = .0959 - .0548 = .0411. 20/365 = .0548 so T - t = .0959 - .0548 = .0411. Exercise price on put used to price the chooser is Exercise price on put used to price the chooser is 125(1.0456)125(1.0456)-.0411-.0411 = 124.77. = 124.77.

Using Black-Scholes model, put is worth 7.80 and call Using Black-Scholes model, put is worth 7.80 and call is worth 13.21 for a total of 21.01. Straddle is worth is worth 13.21 for a total of 21.01. Straddle is worth 13.21 (call) + 12.09 (put) = 25.30.13.21 (call) + 12.09 (put) = 25.30.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 33

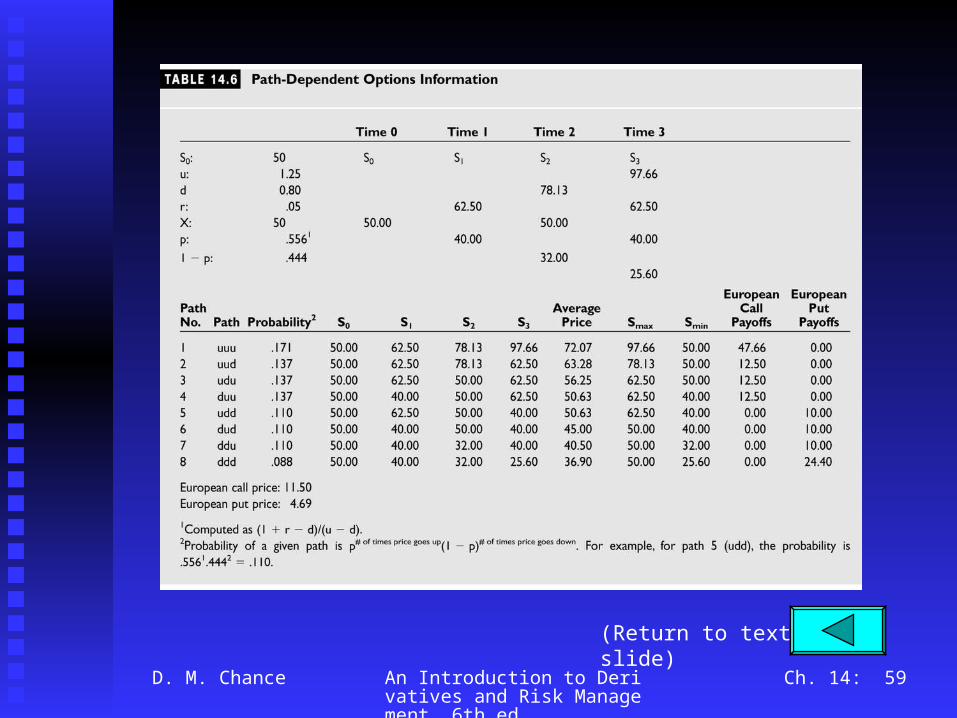

Exotic Options (continued)

Path-Dependent OptionsPath-Dependent Options Path-dependent options are options in which the payoff Path-dependent options are options in which the payoff

is determined by the sequence of prices followed by the is determined by the sequence of prices followed by the asset and not just by the price of the asset at expiration.asset and not just by the price of the asset at expiration.

We shall price these options using a binomial We shall price these options using a binomial framework. See framework. See Table 14.6, p. 523Table 14.6, p. 523 which shows a which shows a three-period problem. Note eight paths, and the three-period problem. Note eight paths, and the average, maximum, and minimum prices of each path average, maximum, and minimum prices of each path are computed.are computed.

Note how the probabilities are calculated.Note how the probabilities are calculated. In practice the binomial model is difficult to use for In practice the binomial model is difficult to use for

path-dependent options. Monte Carlo simulation (see path-dependent options. Monte Carlo simulation (see Appendix 15.B) is often used.Appendix 15.B) is often used.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 34

Exotic Options (continued)

Path-Dependent Options (continued)Path-Dependent Options (continued) Asian option: an option in which the final payoff is Asian option: an option in which the final payoff is

determined by the average price of the asset during the determined by the average price of the asset during the option’s life. Some are average price options because option’s life. Some are average price options because the average price substitutes for the asset price at the average price substitutes for the asset price at expiration. Others are average strike options because expiration. Others are average strike options because the average price substitutes for the exercise price at the average price substitutes for the exercise price at expiration. Can be calls or puts. Useful for hedging or expiration. Can be calls or puts. Useful for hedging or speculating when the average is acceptable as a speculating when the average is acceptable as a measure of the underlying risk. Also useful for cases measure of the underlying risk. Also useful for cases where market can be manipulated.where market can be manipulated.

See See Table 14.7, p. 525Table 14.7, p. 525 for example of pricing Asian for example of pricing Asian options.options.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 35

Exotic Options (continued)

Path-Dependent Options (continued)Path-Dependent Options (continued) Lookback option: Also called a no-regrets option, it Lookback option: Also called a no-regrets option, it

permits purchase of the asset at its lowest price during permits purchase of the asset at its lowest price during the option’s life or sale of the asset at its highest price the option’s life or sale of the asset at its highest price during the option’s life. during the option’s life.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Lookback options (continued):Lookback options (continued): Four different types.Four different types.

• lookback call: exercise price set at minimum lookback call: exercise price set at minimum price during option’s lifeprice during option’s life

• lookback put: exercise price set at maximum lookback put: exercise price set at maximum price during option’s lifeprice during option’s life

• fixed-strike lookback call: payoff based on fixed-strike lookback call: payoff based on maximum price during option’s life (instead of maximum price during option’s life (instead of final price) compared to fixed strikefinal price) compared to fixed strike

• fixed-strike lookback put: payoff based on fixed-strike lookback put: payoff based on minimum price during option’s life (instead of minimum price during option’s life (instead of final price) compared to fixed strikefinal price) compared to fixed strike

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Barrier Options: Options that either terminate early if Barrier Options: Options that either terminate early if the asset price hits a certain level, called the barrier, or the asset price hits a certain level, called the barrier, or activate only if the asset price hits the barrier. The activate only if the asset price hits the barrier. The former are called knock-out options (or simply out-former are called knock-out options (or simply out-options)options) and the latter are called knock-in optionsand the latter are called knock-in options (or (or simply in-options). If the barrier is above the current simply in-options). If the barrier is above the current price, it is called an up-option. If the barrier is below price, it is called an up-option. If the barrier is below the current price, it is called a down-option. the current price, it is called a down-option. See See Table 14.9, p. 528Table 14.9, p. 528 for example of pricing. for example of pricing. Barrier options are normally cheaper than ordinary Barrier options are normally cheaper than ordinary

options because they provide payoffs for fewer options because they provide payoffs for fewer outcomes than ordinary options.outcomes than ordinary options.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 39

Exotic Options (continued)

Path-Dependent Options (continued)Path-Dependent Options (continued) Other Exotic Options:Other Exotic Options:

compound and installment optionscompound and installment options multi-asset options, exchange options, min-max multi-asset options, exchange options, min-max

options (rainbow options), alternative options, options (rainbow options), alternative options, outperformance optionsoutperformance options

shout, cliquet and lock-in optionsshout, cliquet and lock-in options contingent premium, pay-later and deferred strike contingent premium, pay-later and deferred strike

optionsoptions forward-start and tandem optionsforward-start and tandem options

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 40

Some Important New Derivatives

Electricity DerivativesElectricity Derivatives Electricity is a non-storable assetElectricity is a non-storable asset These derivatives are difficult to priceThese derivatives are difficult to price

Weather DerivativesWeather Derivatives Measures of weather activityMeasures of weather activity

Heating degree days and cooling degree daysHeating degree days and cooling degree days Quantity of rain or snowQuantity of rain or snow Financial loss caused by weatherFinancial loss caused by weather

Pricing is difficult but not impossible; a lot of data are Pricing is difficult but not impossible; a lot of data are available on weatheravailable on weather

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 41

Summary

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 42

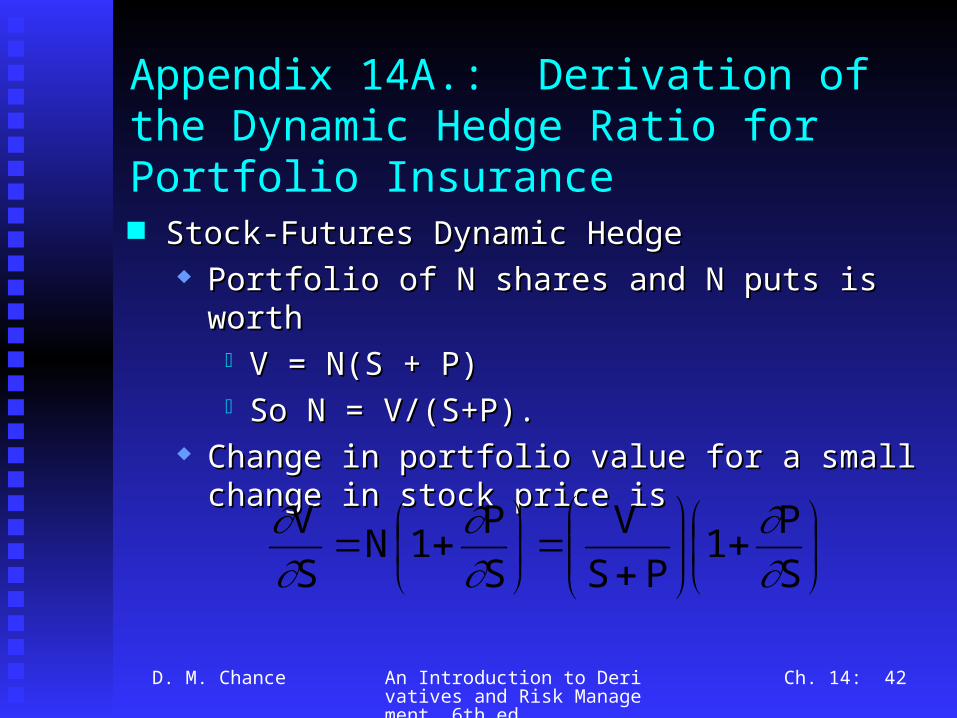

Appendix 14A.: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance

Stock-Futures Dynamic HedgeStock-Futures Dynamic Hedge Portfolio of N shares and N puts is worthPortfolio of N shares and N puts is worth

V = N(S + P)V = N(S + P) So N = V/(S+P). So N = V/(S+P).

Change in portfolio value for a small change in stock Change in portfolio value for a small change in stock price isprice is

SP1

P SV

SP1N

SV

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 43

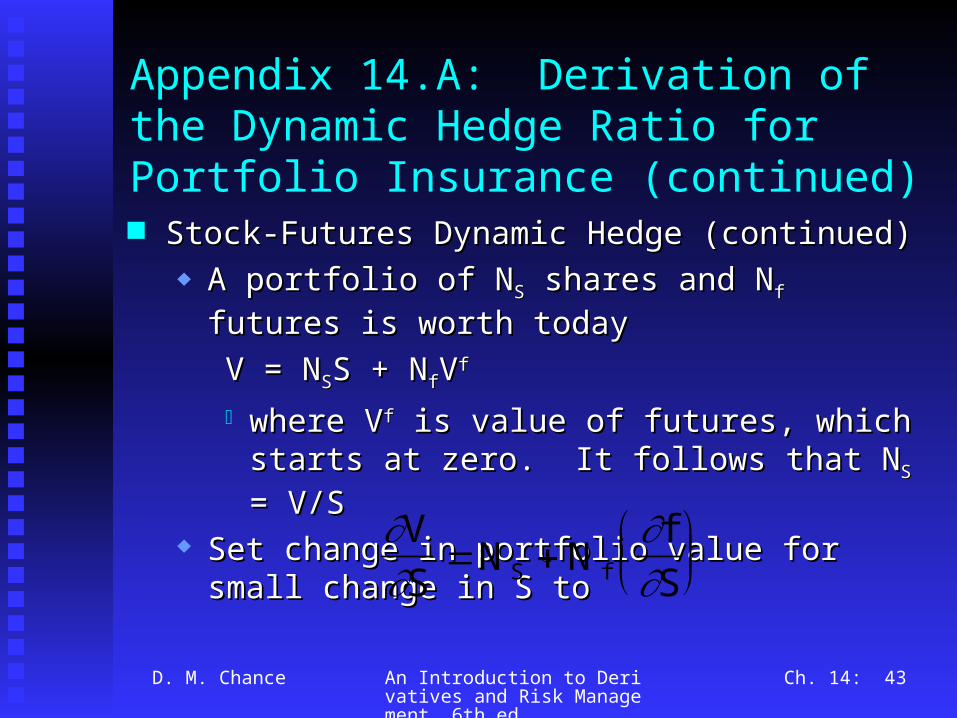

Appendix 14.A: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance (continued) Stock-Futures Dynamic Hedge (continued)Stock-Futures Dynamic Hedge (continued)

A portfolio of NA portfolio of NSS shares and N shares and Nff futures is worth today futures is worth today

V = NV = NSSS + NS + NffVVff

where Vwhere Vff is value of futures, which starts at zero. It is value of futures, which starts at zero. It follows that Nfollows that NSS = V/S = V/S

Set change in portfolio value for small change in S toSet change in portfolio value for small change in S to

VS

N NfSS f

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 44

Appendix 14.A: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance (continued) Stock-Futures Dynamic Hedge (continued)Stock-Futures Dynamic Hedge (continued)

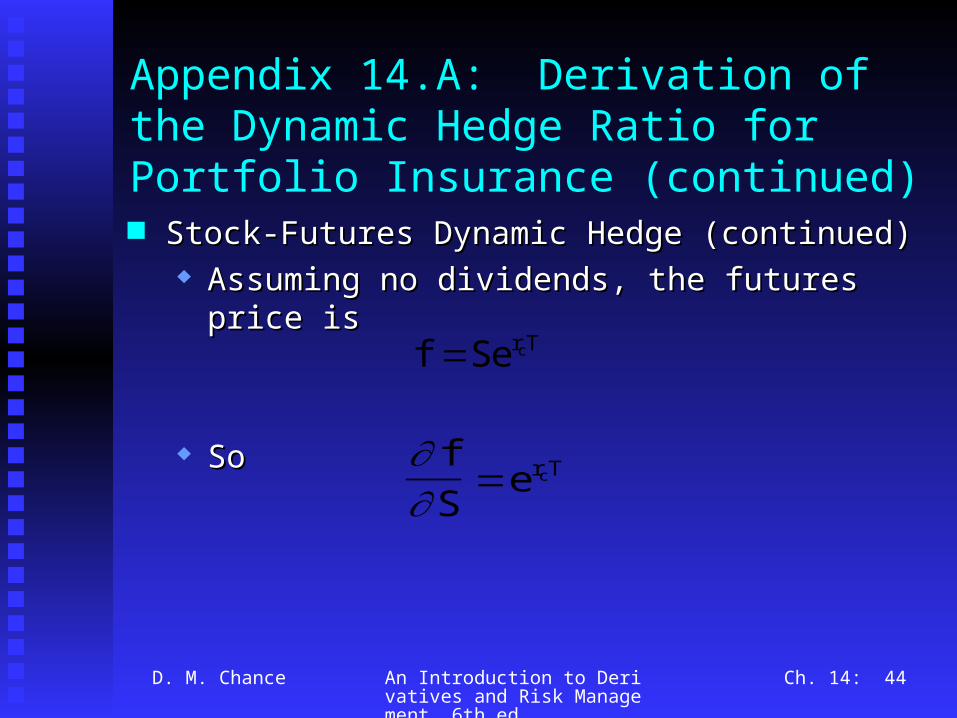

Assuming no dividends, the futures price isAssuming no dividends, the futures price is

So So

f Se r Tc

fS

e r Tc

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 45

Appendix 14.A: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance (continued) Stock-Futures Dynamic Hedge (continued)Stock-Futures Dynamic Hedge (continued)

After substituting, setting the two partial derivatives of After substituting, setting the two partial derivatives of V with respect to S equal to other, recognizing that 1 + V with respect to S equal to other, recognizing that 1 + P/ S is C/ S and N(d N(d11) is ) is C/ S, we obtain the we obtain the number of futures contracts asnumber of futures contracts as

Tr1

minf

ceSV)N(d

XVN

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 46

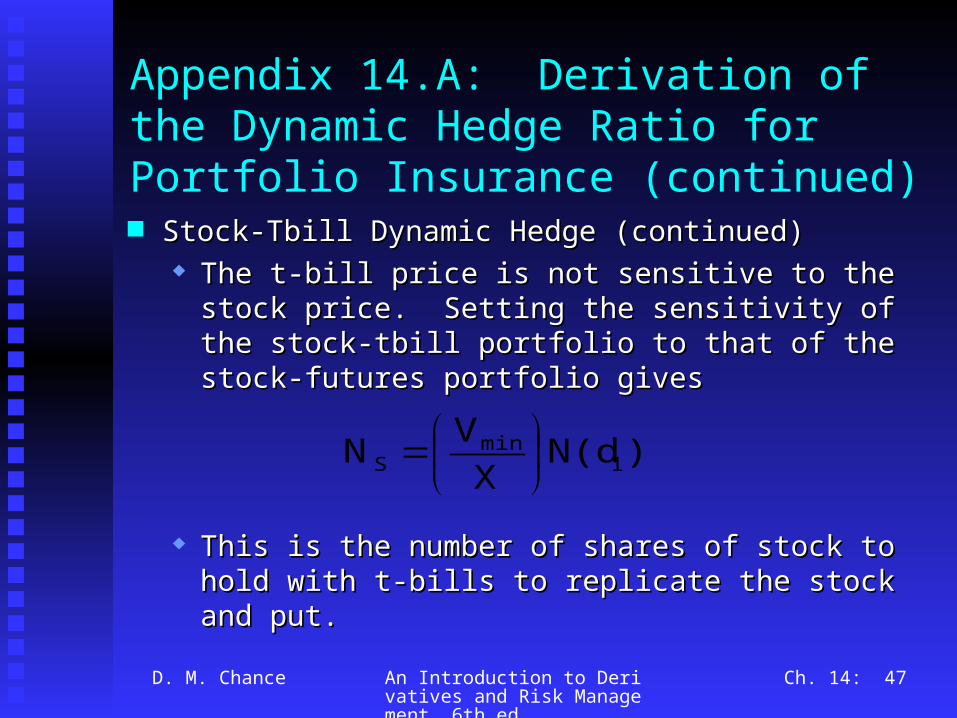

Appendix 14.A: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance (continued) Stock-Tbill Dynamic Hedge Stock-Tbill Dynamic Hedge

A portfolio of stock and tbills is worthA portfolio of stock and tbills is worth

Its sensitivity to a change in S isIts sensitivity to a change in S is

V N S N BS B

VS

NS

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 47

Appendix 14.A: Derivation of the Dynamic Hedge Ratio for Portfolio Insurance (continued) Stock-Tbill Dynamic Hedge (continued) Stock-Tbill Dynamic Hedge (continued)

The t-bill price is not sensitive to the stock price. The t-bill price is not sensitive to the stock price. Setting the sensitivity of the stock-tbill portfolio to that Setting the sensitivity of the stock-tbill portfolio to that of the stock-futures portfolio givesof the stock-futures portfolio gives

This is the number of shares of stock to hold with t-This is the number of shares of stock to hold with t-bills to replicate the stock and put.bills to replicate the stock and put.

)N(dX

VN 1min

S

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 48

Appendix 14.B: Monte Carlo Simulation A method of using random numbers designed to simulate A method of using random numbers designed to simulate

the random observations of prices of an asset. The the random observations of prices of an asset. The simulated series of asset prices at expiration is then simulated series of asset prices at expiration is then converted to an equivalent series of option prices at converted to an equivalent series of option prices at expiration.expiration.

Then the current option price is the discounted average of Then the current option price is the discounted average of the option prices obtained at expiration from the the option prices obtained at expiration from the simulation.simulation.

Random prices can be simulated by drawing a standard Random prices can be simulated by drawing a standard normal random variable, normal random variable, , and inserting into the formula

S Sr t S tc

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 49

Appendix 14.B: Monte Carlo Simulation (continued)

where where t is the length of the time interval over which t is the length of the time interval over which the stock price change occurs. the stock price change occurs.

Note: simulating a standard normal random variable Note: simulating a standard normal random variable can be done approximately as the sum of twelve unit can be done approximately as the sum of twelve unit uniform random numbers (in Excel, “=Rand( )”) minus uniform random numbers (in Excel, “=Rand( )”) minus 6.0.6.0.

Each simulated stock price is treated as the stock price at Each simulated stock price is treated as the stock price at expiration; thus, expiration; thus, t is the maturity in years of the option. For each simulated stock price, compute the option For each simulated stock price, compute the option

price at expiration using the intrinsic value.price at expiration using the intrinsic value.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 50

Appendix 14.B: Monte Carlo Simulation (continued)

Take the average of all of the option prices at Take the average of all of the option prices at expiration.expiration.

Discount the average over the life of the option at the Discount the average over the life of the option at the risk-free rate. This is the estimate of the current option risk-free rate. This is the estimate of the current option price.price.

This procedure will probably require at least 50,000 This procedure will probably require at least 50,000 random numbers for a standard option and more for exotic random numbers for a standard option and more for exotic and complex options and derivatives.and complex options and derivatives.

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 51

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 52

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 53

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 54

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 55

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 56

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 57

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 58

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 59

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 60

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.

Ch. 14: 61

(Return to text slide)

D. M. Chance An Introduction to Derivatives and Risk Management, 6th ed.