46

CHAPTER 16 CHAPTER 16 SPECIAL FINANCING SPECIAL FINANCING VEHICLES VEHICLES

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | kerry-manning |

| View: | 233 times |

| Download: | 6 times |

CHAPTER 16CHAPTER 16

SPECIAL FINANCING SPECIAL FINANCING VEHICLESVEHICLES

CHAPTER OVERVIEWCHAPTER OVERVIEW

I.I. Interest Rate and Currency Interest Rate and Currency SwapsSwaps

II.II. Structured NotesStructured Notes

III.III. Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

IV.IV. International LeasingInternational Leasing

V. V. LDC Debt-Equity SwapsLDC Debt-Equity Swaps

I. Interest Rate and Currency I. Interest Rate and Currency SwapsSwaps

I.I. Interest Rate and Currency SwapsInterest Rate and Currency Swaps

A.A. Basic Features:Basic Features:

1.1. Explosive growth in swap Explosive growth in swap marketmarket

2.2. Two types of swaps:Two types of swaps:

- interest rate- interest rate

Interest Rate SwapsInterest Rate Swaps

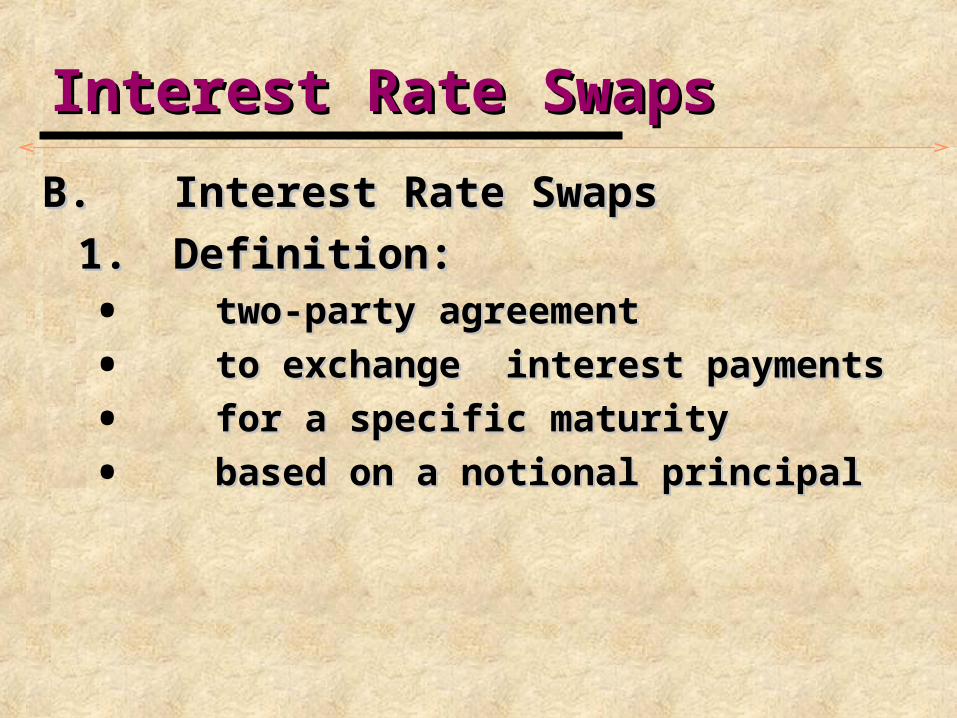

B.B. Interest Rate SwapsInterest Rate Swaps

1.1. Definition:Definition:

• two-party agreementtwo-party agreement

• to exchange interest paymentsto exchange interest payments

• for a specific maturityfor a specific maturity

• based on a notional principalbased on a notional principal

Interest Rate SwapsInterest Rate Swaps

2.2.Notional principalNotional principal

Definition: the reference amount used to Definition: the reference amount used to calculate swap interest paymentscalculate swap interest payments

Not the amount repaid by either Not the amount repaid by either counterpartycounterparty

Interest Rate SwapsInterest Rate Swaps

C.C. Swap MotivationsSwap Motivations

1.1. Risk-reducing potentialRisk-reducing potential

2.2. Cost savingsCost savings

3.3. Exploit comparative advantages Exploit comparative advantages enjoyed by different borrowers in enjoyed by different borrowers in different financial marketsdifferent financial markets

Interest Rate SwapsInterest Rate Swaps

D.D. Other Interest- Rate Swap Features:Other Interest- Rate Swap Features:

1.1. No principal ever changes handsNo principal ever changes hands

2.2. Maturities:Maturities:

1 - 15 years possible1 - 15 years possible

2 - 10 years typical2 - 10 years typical

Interest Rate SwapsInterest Rate Swaps

3.3. Two Types of Interest-Rate SwapsTwo Types of Interest-Rate Swaps

a.a. Coupon SwapsCoupon Swaps

• one counterparty pays a fixed rateone counterparty pays a fixed rate

• second counterparty pays a floating ratesecond counterparty pays a floating rate

• floating rate resets periodically based on a floating rate resets periodically based on a designated index designated index

Interest Rate SwapsInterest Rate Swaps

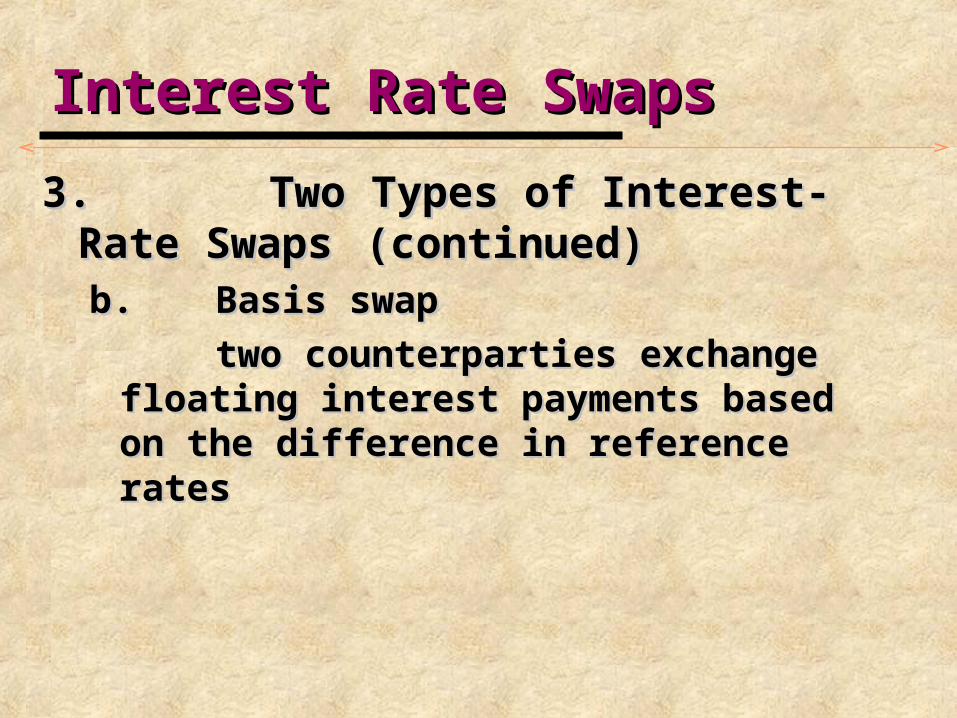

3.3. Two Types of Interest-Rate Swaps Two Types of Interest-Rate Swaps (continued)(continued)

b.b. Basis swapBasis swap

two counterparties exchange floating two counterparties exchange floating interest payments based on the difference interest payments based on the difference in reference ratesin reference rates

Interest Rate SwapsInterest Rate Swaps

E.E. The Classic Swap TransactionThe Classic Swap Transaction

- an example- an example

1.1. AssumptionsAssumptions

Counterparty A: BBB-rated creditCounterparty A: BBB-rated credit

Counterparty B: AAA-rated creditCounterparty B: AAA-rated credit

Fixed-Rates AvailableFixed-Rates Available

For A, 8.5% is best possibleFor A, 8.5% is best possible

For B, 7.0% is best possibleFor B, 7.0% is best possible

Interest Rate SwapsInterest Rate Swaps

1. 1. Assumptions (continued)Assumptions (continued)

Floating Rates AvailableFloating Rates Available

For A For A 6-month LIBOR + 0.5%6-month LIBOR + 0.5%

For BFor B 6-month LIBOR6-month LIBOR

Interest Rate SwapsInterest Rate Swaps

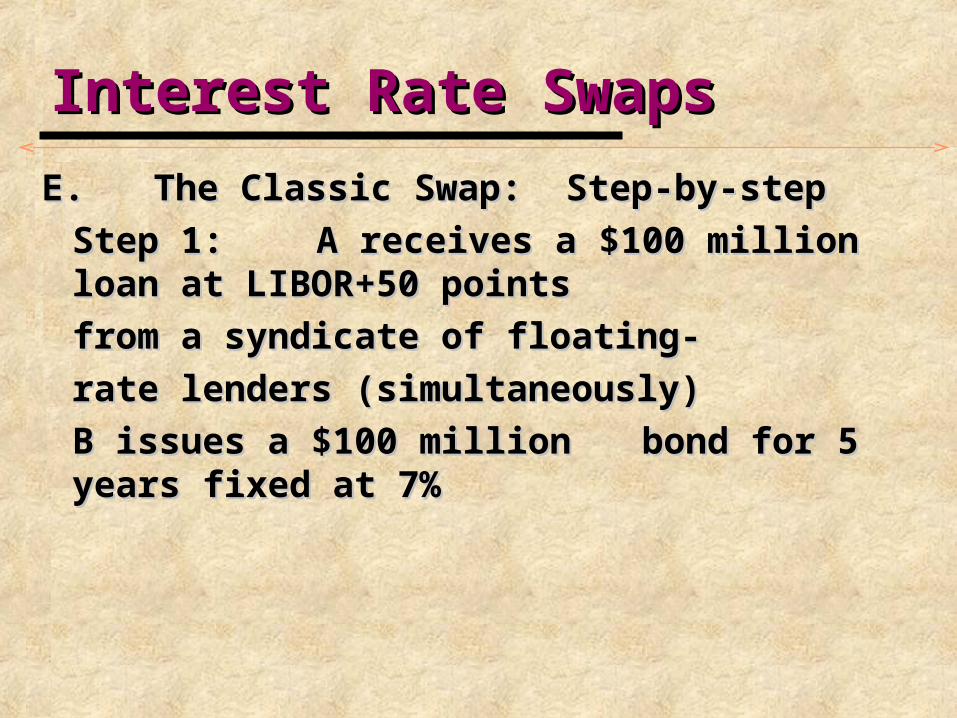

E.E. The Classic Swap: Step-by-stepThe Classic Swap: Step-by-step

Step 1: Step 1: A receives a $100 million A receives a $100 million loan at LIBOR+50 pointsloan at LIBOR+50 points

from a syndicate of floating-from a syndicate of floating-

rate lenders (simultaneously)rate lenders (simultaneously)

B issues a $100 million B issues a $100 million bond for 5 years fixed at 7%bond for 5 years fixed at 7%

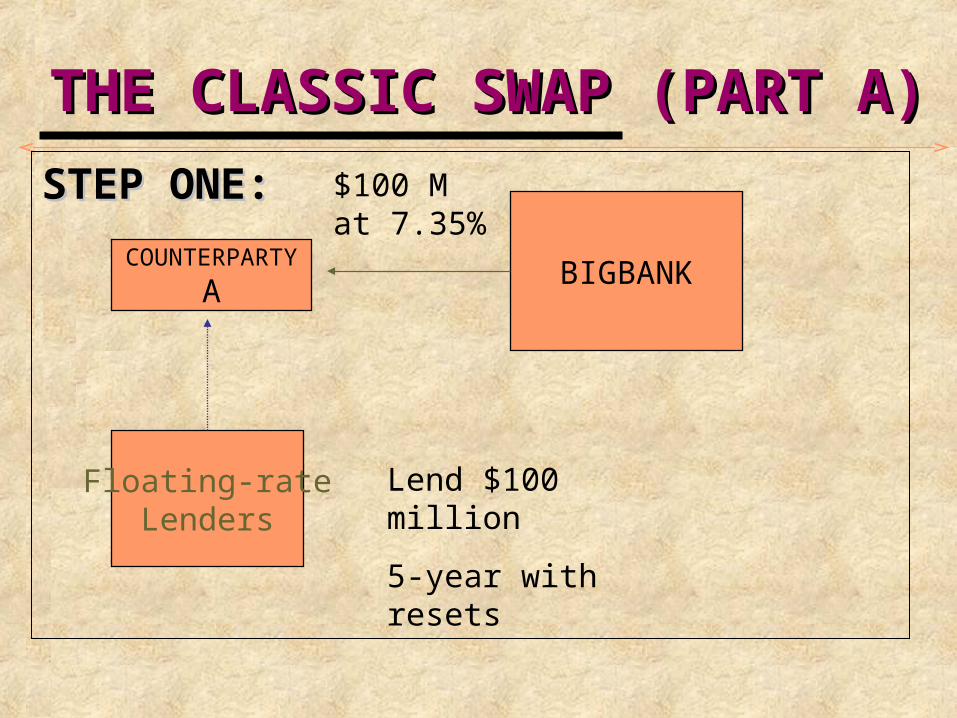

THE CLASSIC SWAP (PART A)THE CLASSIC SWAP (PART A)

STEP ONE:STEP ONE:

Floating-rateLenders

COUNTERPARTYA

Lend $100 million

5-year with resets

BONDMARKET

COUNTERPARTYB

Issue $100 million @7%for 5 years

Interest Rate SwapsInterest Rate Swaps

Step 2: The Swap Agreement (Part A)Step 2: The Swap Agreement (Part A)A borrows $100 million from A borrows $100 million from BigBank and agrees to pay BigBank and agrees to pay 7.35% for 5 years 7.35% for 5 years (.0735 x $100 million)(.0735 x $100 million)

THE CLASSIC SWAP (PART A)THE CLASSIC SWAP (PART A)

STEP ONE:STEP ONE:

Floating-rateLenders

COUNTERPARTY

A

Lend $100 million

5-year with resets

BIGBANK

$100 Mat 7.35%

Interest Rate SwapsInterest Rate Swaps

In exchange for depositing its In exchange for depositing its

$100 million floating-rate loan $100 million floating-rate loan proceeds with BigBank, the proceeds with BigBank, the Bank agrees to pay Bank agrees to pay Counterparty A at the 6-month Counterparty A at the 6-month LIBOR rate (resets to match LIBOR rate (resets to match

the the original loan resets)original loan resets)

THE CLASSIC SWAP (PART A)THE CLASSIC SWAP (PART A)

STEP ONE:STEP ONE:

Floating-rateLenders

COUNTERPARTY

A

Lend $100 million

5-year with resets

BIGBANK

$100 Mat 7.35%

Depositearns 6-moLIBOR

Interest Rate SwapsInterest Rate Swaps

The results from Part A:The results from Part A:

Counterparty A has effectively borrowed Counterparty A has effectively borrowed

at a fixed rate of 7.35% when otherwise at a fixed rate of 7.35% when otherwise

the best the could have received in the the best the could have received in the

fixed-rate market was 8.5%fixed-rate market was 8.5%

Interest Rate SwapsInterest Rate Swaps

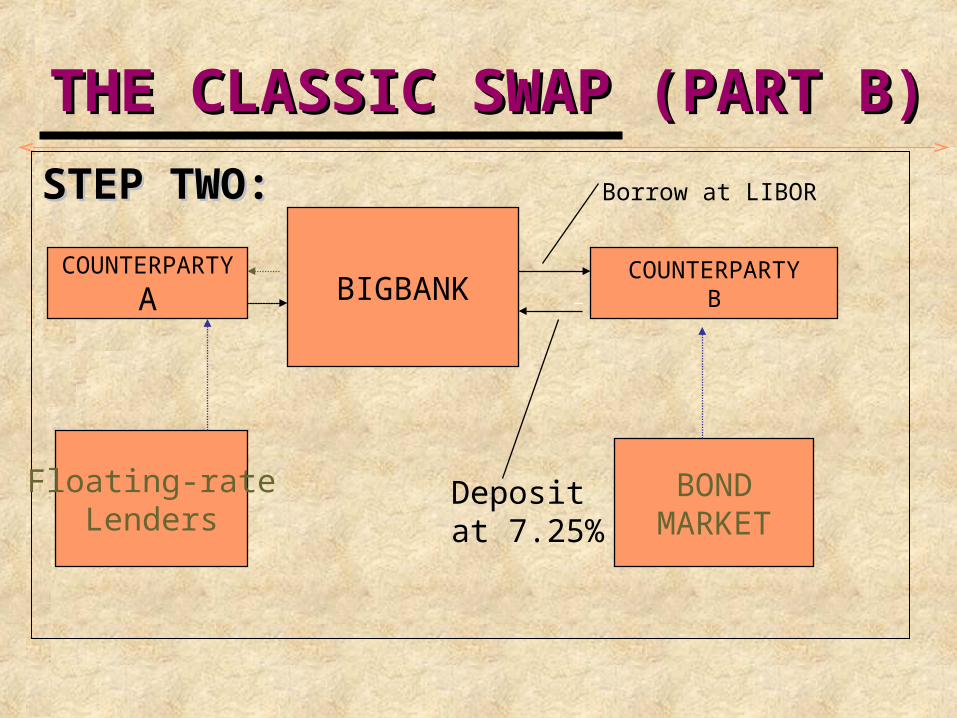

Step 2: The Swap Agreement (Part B)Step 2: The Swap Agreement (Part B)

B borrows from BigBank at the B borrows from BigBank at the 6 6 month LIBOR floating rate for month LIBOR floating rate for 5 5 yearsyears

In exchange for the deposit of In exchange for the deposit of B’s bond proceeds of $100 B’s bond proceeds of $100 million, BigBank agrees to pay million, BigBank agrees to pay

B B at 7.25%at 7.25%

THE CLASSIC SWAP (PART B)THE CLASSIC SWAP (PART B)

STEP TWO:STEP TWO:

Floating-rateLenders

COUNTERPARTY

A BIGBANK

BONDMARKET

COUNTERPARTYB

Borrow at LIBOR

Depositat 7.25%

Interest Rate SwapsInterest Rate Swaps

The Result from Part B:The Result from Part B:

Counterparty B has swapped a fixed-Counterparty B has swapped a fixed-rate loan for a floating-rate loan with an rate loan for a floating-rate loan with an effective cost of LIBOR - .25% when effective cost of LIBOR - .25% when otherwise the best the could have otherwise the best the could have obtained in the floating-rate market was obtained in the floating-rate market was a LIBOR-only loan.a LIBOR-only loan.

Interest Rate SwapsInterest Rate Swaps

Part C: Part C: The Gains to BigBank from the The Gains to BigBank from the SwapsSwaps

BigBank:BigBank:ReceivesReceives 7.35% 7.35% PaysPays (7.25%) (7.25%)ReceivesReceives LIBORLIBORPaysPays (LIBOR) (LIBOR)

NetsNets .01%.01%

Interest Rate SwapsInterest Rate Swaps

Part C: Part C: The Gains to BigBank from the The Gains to BigBank from the Swap (continued)Swap (continued)

BigBank receivesBigBank receives

.001 x the notional principal.001 x the notional principal

($100 million)($100 million)

= $100,000 annually for 5 years= $100,000 annually for 5 years

Interest Rate SwapsInterest Rate Swaps

F.F. Cost SavingsCost Savings

CounterpartyCounterparty NormalNormal SwapSwap NetNet

AA 8.5%8.5% 7.857.85 .65.65

BB LIBORLIBOR L-.25L-.25 .25.25

BigBankBigBank .10.10

Total 1.00Total 1.00

Currency SwapsCurrency Swaps

G.G. Currency SwapsCurrency Swaps

1.1. Definition: Definition:

• an exchange of debt-service obligationsan exchange of debt-service obligations

• denominated in one currency denominated in one currency

• purpose:purpose: for the service on an agreed upon principal for the service on an agreed upon principal

amount of debt denominated in anotheramount of debt denominated in another

Currency SwapsCurrency Swaps

2.2. Motivation for Currency SwapsMotivation for Currency Swaps

a.a. Replaces parallel loanReplaces parallel loan

b.b. Solve two potential problems:Solve two potential problems:

1.) 1.) If no right of offset, defaultIf no right of offset, default

by one party does not by one party does not release the other from release the other from making payments. making payments.

• Swaps have right of offset.Swaps have right of offset.

Currency SwapsCurrency Swaps

2).2). Parallel loans remain on the Parallel loans remain on the balance sheet whereas a balance sheet whereas a currency swap does notcurrency swap does not

Currency SwapsCurrency Swaps

3.3. Difference between interest-rate Difference between interest-rate andand

Currency swaps:Currency swaps:

a.a. Currency swaps have an Currency swaps have an exchange of principal at exchange of principal at predetermined exchange predetermined exchange ratesrates

Interest-Rate and Currency SwapsInterest-Rate and Currency Swaps

H.H. Economic Advantages of SwapsEconomic Advantages of Swaps

1.1. Overcome barriers when they Overcome barriers when they exist to effective arbitrage such exist to effective arbitrage such asas

• legal restrictions on forwardslegal restrictions on forwards

• different perceptions by investors of the different perceptions by investors of the creditworthiness of the two counterpartiescreditworthiness of the two counterparties

• tax differentialstax differentials

Interest-Rate and Currency SwapsInterest-Rate and Currency Swaps

H.H. Economic Advantages of Swaps Economic Advantages of Swaps (continued)(continued)

2.2. They provide long-term They provide long-term financing in foreign currenciesfinancing in foreign currencies

II.II. Structured NotesStructured Notes

II.II. Structured NotesStructured Notes

A.A. Definition:Definition:

interest-bearing securities interest-bearing securities whose interest payments are whose interest payments are

by by a a formulaformula set in advance set in advance

B.B. FormulaFormula

may be tied to a variety of may be tied to a variety of different often complex factorsdifferent often complex factors

Structured NotesStructured Notes

C.C. Purpose of Structured NotesPurpose of Structured Notes

1.1. They allow firms to speculate They allow firms to speculate onon

the direction, range, and the direction, range, and volatility of interest ratesvolatility of interest rates

2.2. They also can be used for They also can be used for hedging purposeshedging purposes

Structured NotesStructured Notes

D. Types of Structured NotesD. Types of Structured Notes

1.1. Inverse floatersInverse floaters

2.2. Step-upsStep-ups

3.3. Step-downsStep-downs

III.III. Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

III.III. Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

A.A. Include:Include:

1. 1. Forward forwardsForward forwards

2.2. Forward rate agreementsForward rate agreements

3.3. Eurodollar futuresEurodollar futures

Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

B.B. Forward ForwardsForward Forwards

1.1. Definition:Definition:

a contract that fixes an interest a contract that fixes an interest rate today on a future loan or rate today on a future loan or

depositdeposit

2. 2. Contract specifiesContract specifies– interest rateinterest rate–principal amountprincipal amount–start and ending dates of future interest start and ending dates of future interest

rate periodrate period

Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

C.C. Forward Rate AgreementsForward Rate Agreements

1.1. Definition:Definition:

a cash-settled, over-the-countera cash-settled, over-the-counter

forward contract that allowsforward contract that allows–a fixed interest rate a fixed interest rate – the rate to be applied in the future on the rate to be applied in the future on

some notional principal amountsome notional principal amount– the parties to exchange interest the parties to exchange interest

paymentspayments

Interest Rate Forwards and Interest Rate Forwards and FuturesFutures

D.D. Eurodollar FuturesEurodollar Futures

1.1. Definition:Definition:

a cash-settled futures contract a cash-settled futures contract on a three-month, $1 million on a three-month, $1 million Eurodollar deposit that pays Eurodollar deposit that pays LIBORLIBOR

2.2. Features are similar to Features are similar to currency currency futuresfutures

IV.IV. International LeasingInternational Leasing

IV.IV. International LeasingInternational Leasing

A.A. PurposesPurposes

1.1. To defer and avoid taxesTo defer and avoid taxes

2.2. To safeguard firm’s To safeguard firm’s

foreign foreign subsidiary assetssubsidiary assets

3.3. To avoid currency To avoid currency

controlscontrols

International LeasingInternational Leasing

B.B. Types of LeasesTypes of Leases

1. Operating Lease (true lease)1. Operating Lease (true lease)• ownership and the use of the ownership and the use of the

asset are separatedasset are separated• agreement covers only part of the agreement covers only part of the

useful life of the assetuseful life of the asset

International LeasingInternational Leasing

B.B. Types of LeasesTypes of Leases

2.2. Financial leaseFinancial lease• extends over most of the economic life extends over most of the economic life

of the assetof the asset• noncancelablenoncancelable• if cancelable, it requires substantial if cancelable, it requires substantial

penalty to the lessorpenalty to the lessor• in effect, lessor borrows money and in effect, lessor borrows money and

then purchases the assetthen purchases the asset

if a financial lease, lessee allowed if a financial lease, lessee allowed tax depreciation for the purchase tax depreciation for the purchase price price tax deduction for the interest factortax deduction for the interest factorlessor not entitled to tax benefitslessor not entitled to tax benefits

International Leasing International Leasing

3.3. Tax FactorsTax Factors

a lease that qualifies as a true lease a lease that qualifies as a true lease for tax purposes is called a tax-for tax purposes is called a tax-oriented lease entitling lessee tooriented lease entitling lessee to

deduct full value of lease paymentsdeduct full value of lease payments

International LeasingInternational Leasing

if a financial lease, lessee allowed if a financial lease, lessee allowed

• tax depreciation for the purchase price tax depreciation for the purchase price

• tax deduction for the interest factortax deduction for the interest factor

• lessor not entitled to tax benefitslessor not entitled to tax benefits

V. V. LDC Debt-Equity SwapsLDC Debt-Equity Swaps

V. V. LDC Debt-Equity SwapsLDC Debt-Equity Swaps

A. A. The LDC Debt-Equity MarketThe LDC Debt-Equity Market

1.1. enables investors to purchase enables investors to purchase the external debt of less-the external debt of less-developed countries (LDC) todeveloped countries (LDC) to

acquire equity or domestic acquire equity or domestic

currency in those same currency in those same marketsmarkets

LDC Debt-Equity SwapsLDC Debt-Equity Swaps

B.B. Types of Debt Swaps and RationaleTypes of Debt Swaps and Rationale

1.1. LDC loans sell at deep LDC loans sell at deep discounts discounts to their face valueto their face value

2.2. Substantial variation can Substantial variation can occur occur across countriesacross countries

LDC Debt-Equity SwapsLDC Debt-Equity Swaps

3.3. Investors buy loans in Investors buy loans in expectation that credit ratings expectation that credit ratings will increasewill increase

4.4. Arbitrage opportunities occur. Arbitrage opportunities occur. The market offers a more The market offers a more favorable exchange rate that favorable exchange rate that

do do official currency markets. official currency markets.

LDC Debt-Equity SwapsLDC Debt-Equity Swaps

C.C. Costs and Benefits of Debt SwapsCosts and Benefits of Debt Swaps

1.1. Debt swaps and inflationDebt swaps and inflation

2.2. Impact on capital FormationImpact on capital Formation

3.3. Effect on privatizationEffect on privatization