• Equivalent units of production (EUP)– Measures the amount of materials added to or

work done on partially completed units during a period

– Expressed in terms of fully complete units of output

• Conversion costs are the sum of direct labor and manufacturing overhead costs and represent the cost to convert direct materials into finished goods.

• Assume Puzzle Me has 40,000 units that the Assembly Department completed and transferred out.

• Therefore, for units complete and transferred out the equivalent units would be 40,000 units (40,000 units * 100% complete) for both direct materials and conversion costs.

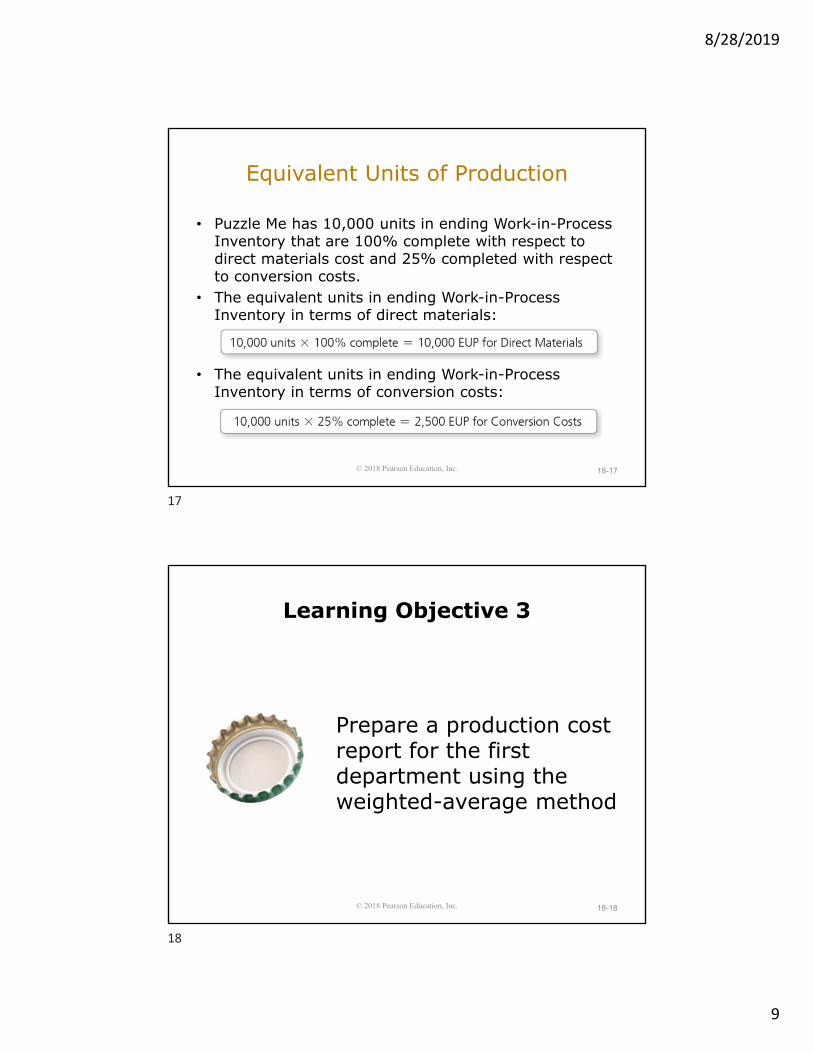

• Puzzle Me has 10,000 units in ending Work-in-Process Inventory that are 100% complete with respect to direct materials cost and 25% completed with respect to conversion costs.

• The equivalent units in ending Work-in-Process Inventory in terms of direct materials:

• The equivalent units in ending Work-in-Process Inventory in terms of conversion costs:

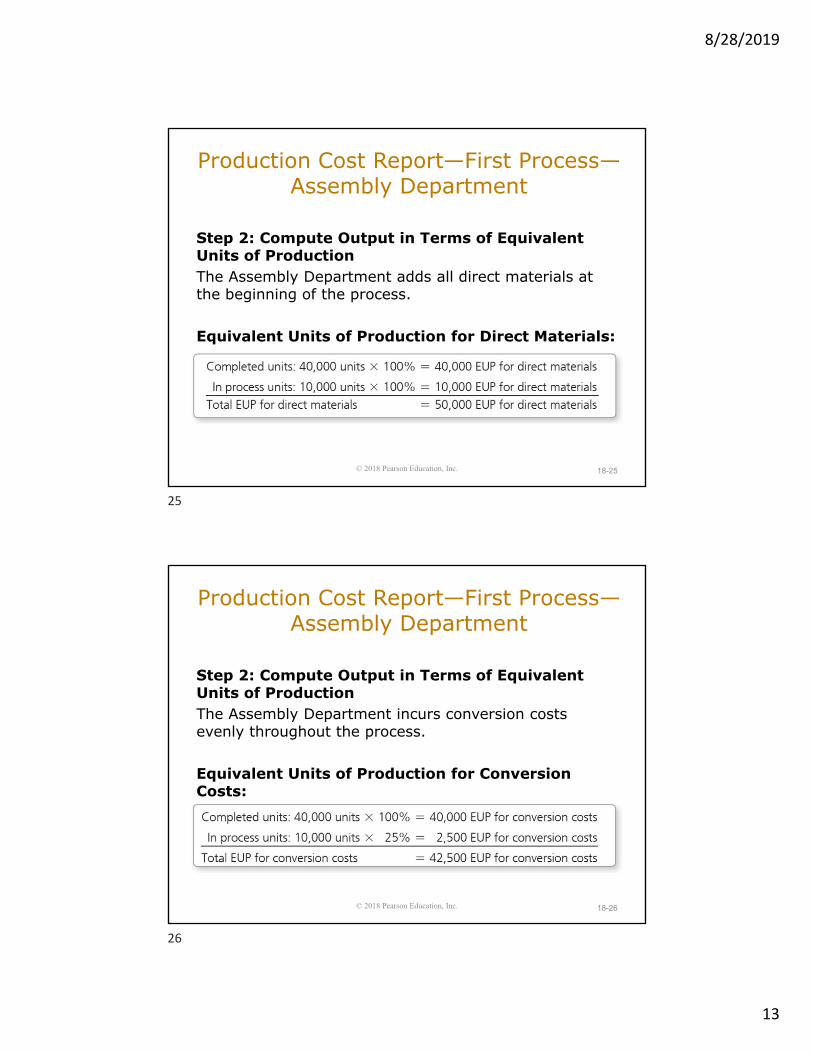

Production Cost Report—First Process—Assembly Department

The Assembly Department applies glue to the cardboard and then presses a picture onto the cardboard. Operations for this department include two inputs:• The direct materials (glue

and cardboard) are added at the beginning of the process.

• The conversion costs are added evenly throughout the process.

Production Cost Report—First Process—Assembly Department

Step 1: Summarize the Flow of Physical Units The physical units are the actual units that the company will account for during the period. The Assembly Department had 8,000 units in process on July 1 and started 42,000 units during the month.

Production Cost Report—First Process—Assembly Department

Step 3: Compute the Cost per Equivalent Unit of ProductionThe Assembly Department has to account for costs associated with the following:• Work done last month on the 8,000 partially

completed units (beginning work-in-process)• Work done this month to complete the 8,000 partially

completed units• Work done this month on the 42,000 units that were

Production Cost Report—First Process—Assembly Department

Step 4: Assign Costs to Units Completed and Units in ProcessThe costs must be divided between two outputs:• The 40,000 completed puzzle boards that have been

transferred out to the Cutting Department.• The 10,000 partially completed puzzle boards

remaining in the Assembly Department’s ending Work-in-Process Inventory.

This is accomplished by multiplying the cost per equivalent unit of production (Step 3) by the equivalent units of production (Step 2).

• The Cutting Department receives the puzzle boards from the Assembly Department and cuts the boards into puzzle pieces before inserting the pieces into the box at the end of the process. – Glued puzzle boards with pictures are transferred

in from the Assembly Department at the beginning of the Cutting Department’s process.

– The Cutting Department’s conversion costs are added evenly throughout the process.

– The Cutting Department’s direct materials are added at the end of the process.

Step 1: Summarize the Flow of Physical Units The Cutting Department has 5,000 units in process on July 1 and receives 40,000 units during the month from the Assembly Department.

The Cutting Department completes the cutting and boxing process on 38,000 of the 45,000 units to account for and transfers those units to Finished Goods Inventory.

Production Cost Report—Second Process—Cutting Department

Step 2: Compute Output in Terms of Equivalent Units of Production The Cutting Department starts with the units transferred in from the Assembly Department. The equivalent units of production for transferred in are always 100%.

Equivalent Units of Production for Transferred In:

Production Cost Report—Second Process—Cutting Department

Step 3: Compute the Cost per Equivalent Unit of ProductionThe Cutting Department has three inputs and therefore must make three calculations for cost per equivalent unit of production.

Production Cost Report—Second Process—Cutting Department

Step 4: Assign Costs to Units Completed and Units in ProcessThe $233,040 total costs accounted for by the Cutting Department should be assigned to the following:• The 38,000 completed puzzles that have been

transferred out to Finished Goods Inventory• The 7,000 partially completed puzzle boards

remaining in the Cutting Department’s ending Work-in-Process Inventory

Production Cost Report—Second Process—Cutting Department

During July, Puzzle Me assigns direct materials to the two production departments: $130,200 to the Assembly Department and $19,000 to the Cutting Department; $2,000 in indirect materials is accumulated in Manufacturing Overhead.

During the month, Puzzle Me assigns $22,090 in direct labor costs to the Assembly Department and $3,840 in direct labor costs to the Cutting Department. $1,500 in indirect labor costs are accumulated in Manufacturing Overhead.

Puzzle Me incurs $30,000 in machinery depreciation and $19,000 in indirect costs that were paid in cash. These costs are accumulated in the Manufacturing Overhead account.

Puzzle Me uses a predetermined overhead allocation rate to allocate indirect costs to the departments: $42,000 to the Assembly Department and $11,000 to the Cutting Department.

Transaction 6—Transfer from the Assembly Department to the Cutting Department

18-59

At the end of July, when the production cost report for the Assembly Department is prepared, Puzzle Me assigns $176,000 to the 40,000 units transferred from the Assembly Department to the Cutting Department.

Transaction 7—Transfer from Cutting Department to Finished Goods Inventory

18-60

At the end of July, when the production cost report for the Cutting Department is prepared, Puzzle Me assigns $201,400 to the 38,000 units transferred from the Cutting Department to Finished Goods Inventory. This is the cost of goods manufactured.

Transaction 8—Puzzles SoldDuring July, Puzzle Me sells 35,000 puzzles. The total production cost of manufacturing a puzzle is $5.30. The cost of 35,000 puzzles is $185,500 (35,000 puzzles × $5.30 per puzzle). The puzzles are sold on account for $8.00 each, which is a total of $280,000 (35,000 puzzles × $8.00 per puzzle).

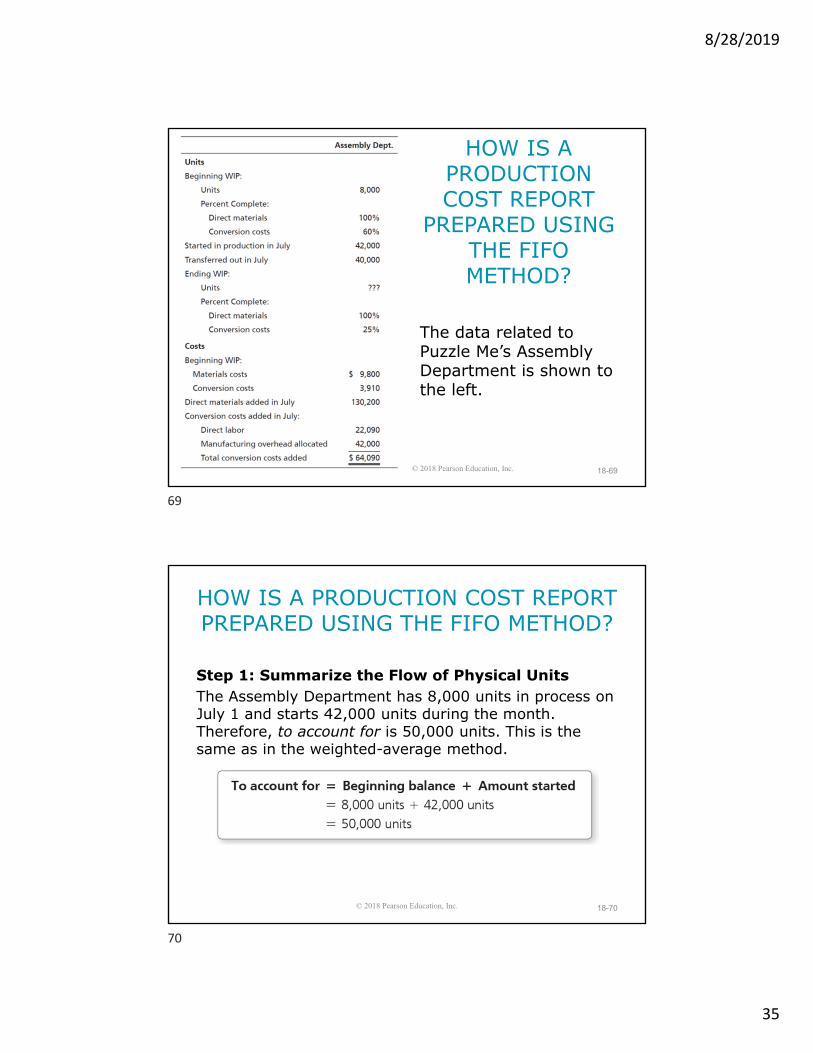

Step 1: Summarize the Flow of Physical Units The Assembly Department has 8,000 units in process on July 1 and starts 42,000 units during the month. Therefore, to account for is 50,000 units. This is the same as in the weighted-average method.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

Step 1: Summarize the Flow of Physical UnitsIf 40,000 units are completed and transferred, this includes the 8,000 units in beginning inventory plus another 32,000 units started in July. We must account for 50,000 units. If 40,000 are transferred out, then that leaves 10,000 still in process at the end of July.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?

Step 4: Assign Costs to Units Completed and Units in ProcessThe $208,000 total costs must be assigned to:• The 8,000 puzzle boards from beginning inventory

that have now been completed and transferred to the Cutting Department.

• The 32,000 started and completed puzzle boards that have also been transferred to Cutting Department.

• The 10,000 partially completed puzzle boards remaining in the Assembly Department’s ending Work-in-Process Inventory.

HOW IS A PRODUCTION COST REPORT PREPARED USING THE FIFO METHOD?