CHAPTER 2 CHAPTER 2 FINANCIAL STATEMENT AUDITS AND FINANCIAL STATEMENT AUDITS AND AUDITORS’ RESPONSIBILITIES AUDITORS’ RESPONSIBILITIES Fall 2007 Fall 2007 Generally Accepted Auditing Standards Assurance Provided by an Audit Reports on Audited Financial Statements Reports on Internal Controls

Transcript

CHAPTER 2CHAPTER 2FINANCIAL STATEMENT AUDITS AND FINANCIAL STATEMENT AUDITS AND

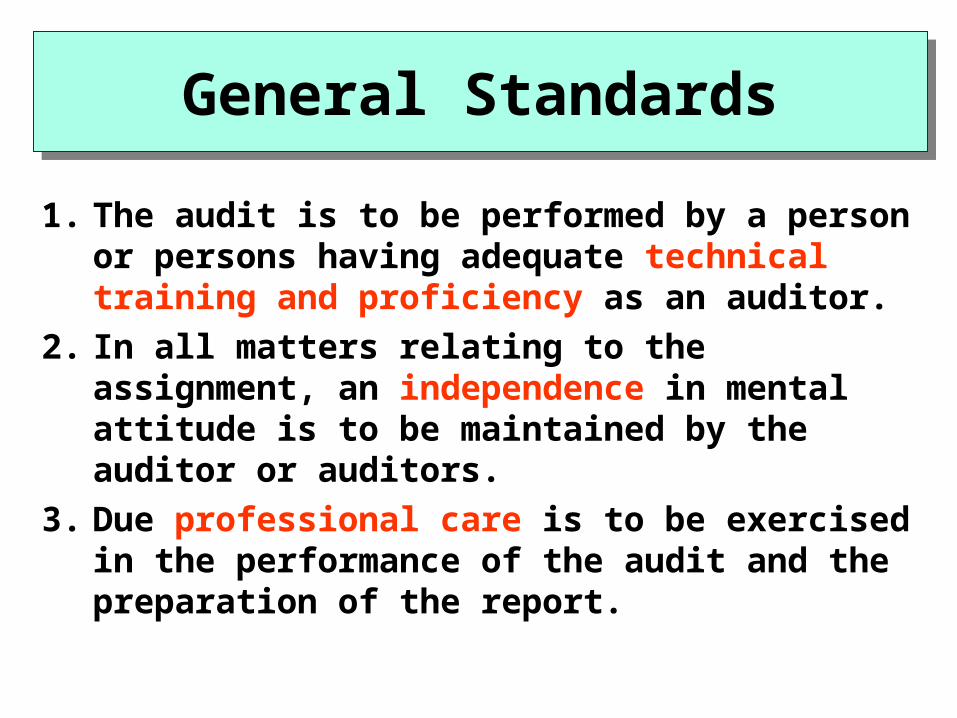

1. The audit is to be performed by a person or persons having adequate technical training and proficiency as an auditor.

2. In all matters relating to the assignment, an independence in mental attitude is to be maintained by the auditor or auditors.

3. Due professional care is to be exercised in the performance of the audit and the preparation of the report.

1. The work is to be adequately planned, and assistants, if any, are to be properly

supervised.2. A sufficient understanding of the internal

control structure is to be obtained to plan the audit and to determine the nature, timing, and extent of tests to be performed.3. Sufficient competent evidential matter is to

be obtained through inspection, observation, inquiries, and confirmations to afford a reasonable basis for an opinion regarding the financial statements under audit.

Standards of Field WorkStandards of Field Work

1. The report shall state whether the financial statements are presented in accordance

with generally accepted accounting principles.2. The report shall identify those circumstances in which such principles have not been

consistently observed in the current period in relation to the preceding period.3. Informative disclosures in the financial

statements are to be regarded as reasonably adequate unless otherwise stated in the report.

Standards of ReportingStandards of Reporting

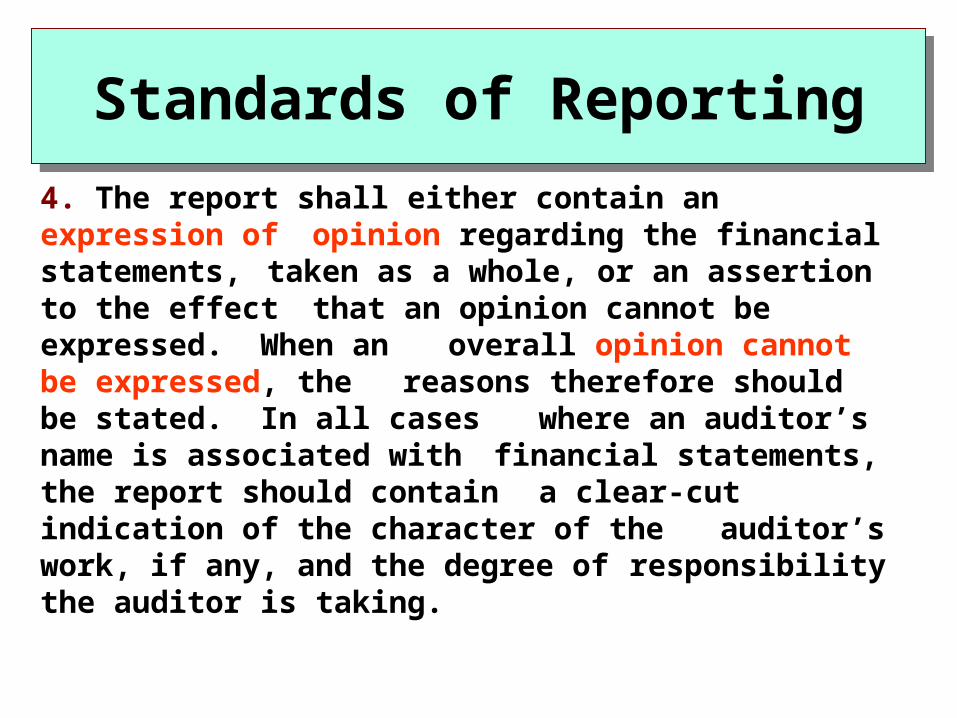

4. The report shall either contain an expression of opinion regarding the financial statements,

taken as a whole, or an assertion to the effect that an opinion cannot be expressed. When an overall opinion cannot be expressed, the reasons therefore should be stated. In all cases where an auditor’s name is associated with financial statements, the report should contain a clear-cut indication of the character of the

auditor’s work, if any, and the degree of responsibility the auditor is taking.

Standards of ReportingStandards of Reporting

Auditor’s Standard F/S Auditor’s Standard F/S ReportReport

Auditor’s Standard F/S Auditor’s Standard F/S ReportReport

Basic Elements of Auditor’s Standard Report

Title Addressee

Introductory Paragraph

Scope Paragraph

Opinion Paragraph

Firm’s SignatureDate

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

1. Auditor Independence– Independent in fact and appearance

2. Reasonable Assurance about F/S– Relates to limitations of an audit

3. Evaluation of Internal Control– Public companies

• Design & operation effective at year end• Inherent limitations of internal control

– Non-public companies• None

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

4. Fraud– Includes:

• Fraudulent financial reporting • Misappropriation of assets

– Assess risk of fraud – SAS No. 99– Design plan to provide reasonable assurance

that fraud does not exist that is material to the financial statements based on risk assessment.

– Reporting Fraud• Employee fraud• Management fraud• Confidential client information

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

Assurance Provided Assurance Provided by a F/S Auditby a F/S Audit

5. Illegal Client Acts– Define

• Direct and material • Indirect

– Responsibility

6. Assurance About a Going Concern- Ability to continue for the next 12 months- Does the auditor have “substantial doubt”?

Types of Auditors’ Reports Types of Auditors’ Reports and Circumstancesand Circumstances

Figure 2-4Figure 2-4

Types of Auditors’ Reports Types of Auditors’ Reports and Circumstancesand Circumstances

Figure 2-4Figure 2-4

Types of Auditors’ Reports on F/STypes of Auditors’ Reports on F/Sand Circumstancesand Circumstances

Figure 2-4Figure 2-4

Types of Auditors’ Reports on F/STypes of Auditors’ Reports on F/Sand Circumstancesand Circumstances

Figure 2-4Figure 2-4

Standard Report with Explanatory LanguageStandard Report with Explanatory Language

• Reason for Report– The financial statements present fairly in

all material respects– Used with

• Changes in accounting principles• Material uncertainties• Emphasis of a matter• Going concern matters

• Form of Report– 4th paragraph to explain issue and refer to

note in the financial statements

Qualified OpinionQualified Opinion

• Reason for Opinion– Material departure from GAAP– Material scope limitation (circumstance)– Except for the qualification, the financial

statements present fairly.

• Form of Report– 3rd paragraph before the opinion to explain the

exception its impact on the financial statements– 4th paragraph is opinion paragraph. “In our

opinion, except for ….

Adverse OpinionAdverse Opinion

• Reason for Opinion– Departures from GAAP are so material and so

pervasive to the financial statement that the auditor concludes that the financial statement do not present fairly …

• Form of Report– 3rd paragraph before the opinion to explain the

exception its impact on the financial statements– 4th paragraph is opinion paragraph. “In our

opinion,… the financial statements referred to above do not present fairly….

Disclaimer of OpinionDisclaimer of Opinion

• Reason for Opinion– The auditor is unable to obtain sufficient

evidence to form an opinion on the financial statements

– Client imposed scope restrictions

• Form of Opinion– Omit 2nd scope paragraph– 3rd paragraph before the opinion to explain the

reason for the disclaimer of opinion– 4th paragraph is opinion paragraph. “… the

scope of our work was not sufficient to enable us to express, and we do not express, an opinion on the financial statements.

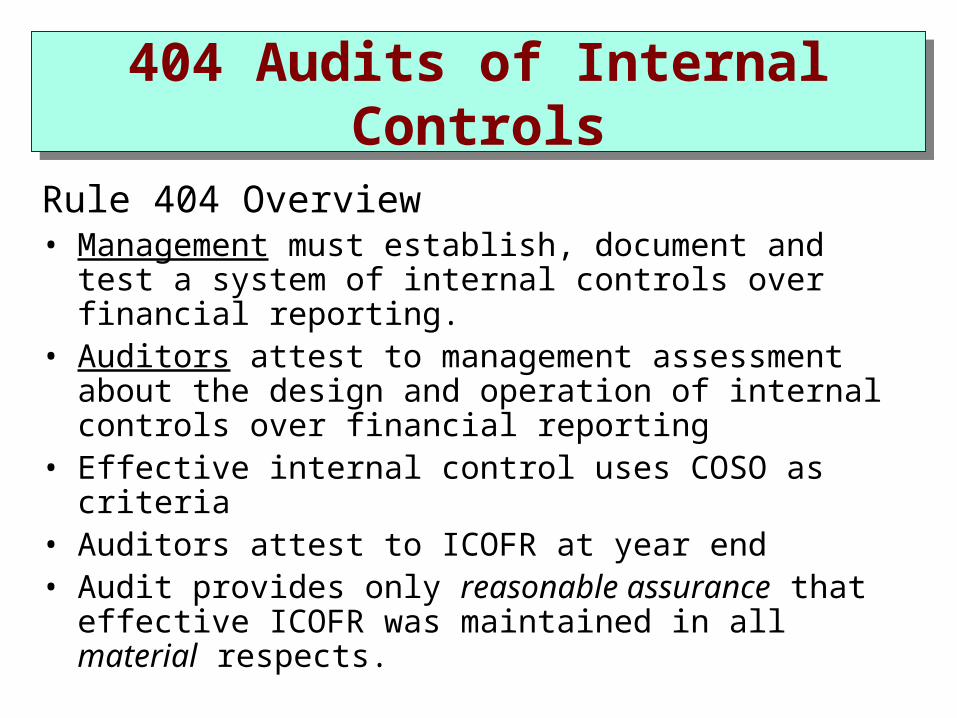

404 Audits of Internal Controls

404 Audits of Internal Controls

Rule 404 Overview• Management must establish, document and test a

system of internal controls over financial reporting.• Auditors attest to management assessment about

the design and operation of internal controls over financial reporting

• Effective internal control uses COSO as criteria• Auditors attest to ICOFR at year end• Audit provides only reasonable assurance that

effective ICOFR was maintained in all material respects.

404 Audits: AS5 “Sanity in SOX”

404 Audits: AS5 “Sanity in SOX”

• Effective FY ending 11/15/07• Main idea: “Focus on the jugular” (Christopher

Cox, SEC Chairman)– No longer assess mgm’t assessments of ICOFR– Assess the design of ICOFR, then test risk areas– Focus on highest risk areas where ICOFR may not

find a misstatement that is material to the f/s– Emphasize f/s fraud controls– Audit should plan to find material weaknesses

• Material weakness: a deficiency, or a combination of deficiencies, in ICOFR such that there is a reasonable possibility that a material misstatement of the registrant’s annual or interim financial statements will not be prevented or detected on a timely basis

• Significant deficiency: less severe than a material weakness

Audits of Internal ControlsAudits of Internal Controls

• Rule 404 Reports – may be separate from or integrated with report on audited f/s– Similar to f/s audit report but also includes definition and

limitations paragraph– Departures:

• Material weakness Adverse opinion• Significant deficiency Unqualified opinion, but report to BOD• Circumstance imposed scope limitation withdraw, disclaim or

qualified opinion• Management imposed scope limitation withdraw or disclaim

• Question: how can a company receive a clean opinion on their f/s but not on internal controls?