Chapter 3-1 C hapter 3-23 A ssets A ssets D ebit/D r. C redit/C r. N orm alBalance N orm alB alance C hapter 3-27 D ebit/D r. C redit/C r. N orm alBalance N orm alB alance Expense Expense Liabilities Liabilities D ebit/D r. C redit/C r. N orm alB alance N orm alB alance C hapter 3-25 D ebit/D r. C redit/C r. N orm alBalance N orm alBalance Equity Equity C hapter 3-26 D ebit/D r. C redit/C r. N orm alBalance N orm alBalance Revenue Revenue Normal Balance Credit Normal Balance Debit Debits and Credits Summary Debits and Credits Summary LO 2 Explain double-entry rules. LO 2 Explain double-entry rules.

Transcript

Chapter 3-1

Chapter 3-23

AssetsAssets

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-27

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

ExpenseExpense

Chapter 3-24

LiabilitiesLiabilities

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

Chapter 3-25

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

EquityEquity

Chapter 3-26

Debit / Dr. Credit / Cr.

Normal BalanceNormal Balance

RevenueRevenue

Normal Balance Credit

Normal Balance Credit

Normal Balance Debit

Normal Balance Debit

Debits and Credits Debits and Credits SummarySummary

Debits and Credits Debits and Credits SummarySummary

LO 2 Explain double-entry rules.LO 2 Explain double-entry rules.

LO 2 Explain double-entry rules.LO 2 Explain double-entry rules.

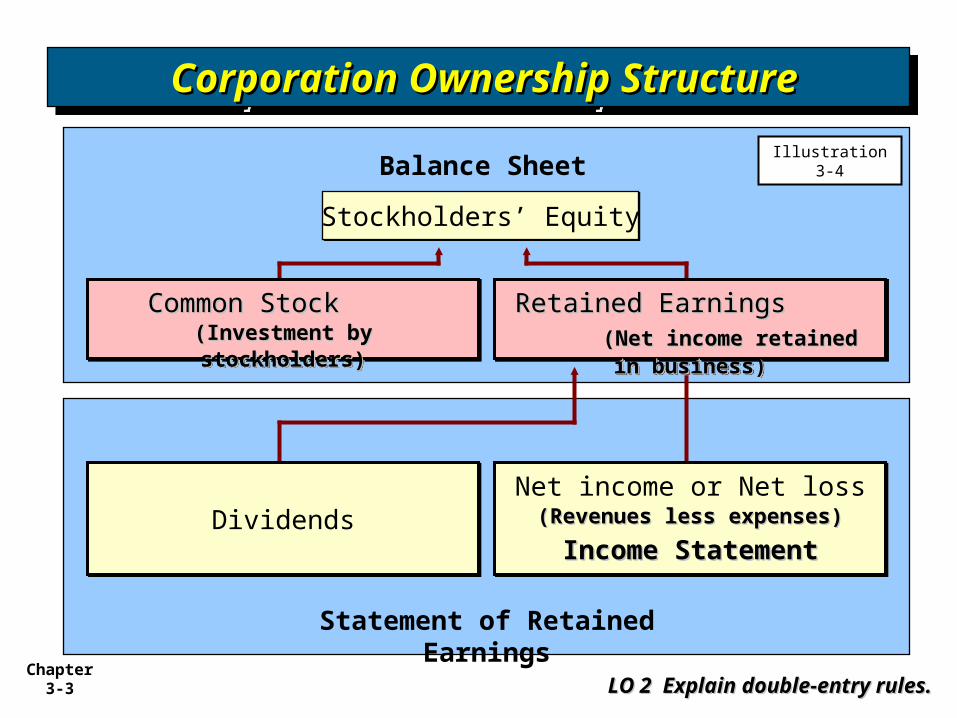

Relationship among the assets, liabilities and Relationship among the assets, liabilities and stockholders’ equity of a business: stockholders’ equity of a business:

The equation must be in balance after every The equation must be in balance after every transaction. For every transaction. For every DebitDebit there must be a there must be a CreditCredit..

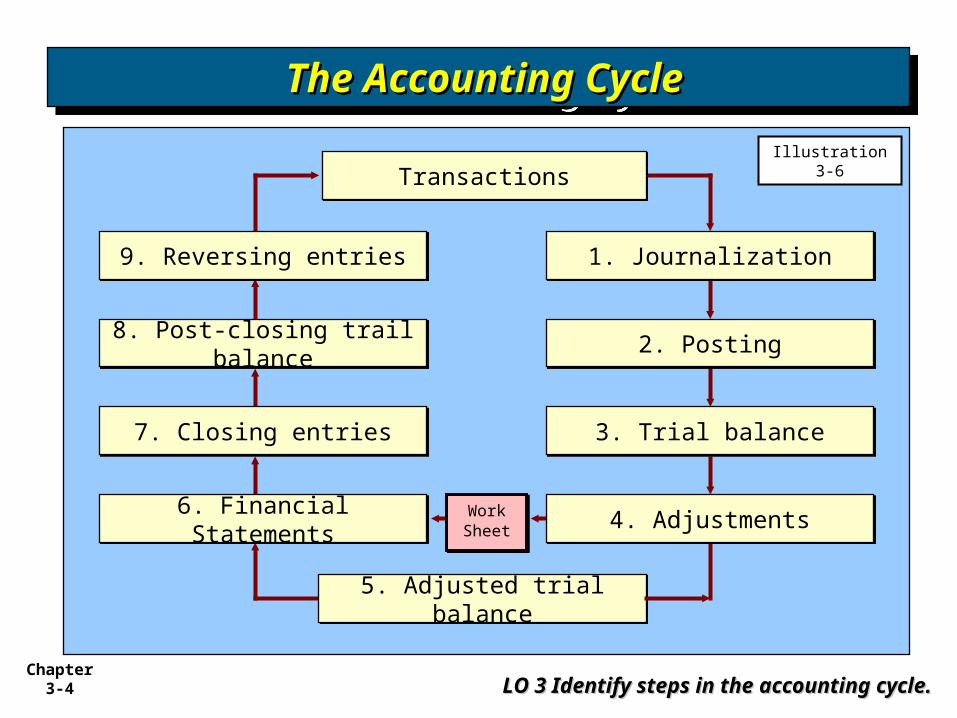

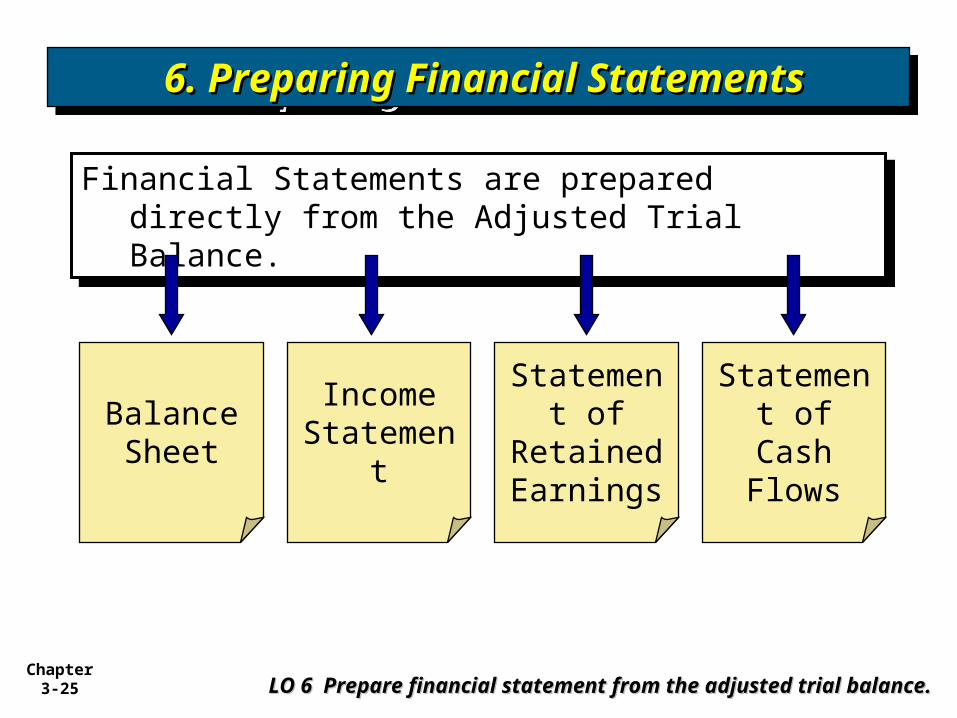

LO 4 LO 4 Record transactions in journals, post Record transactions in journals, post to ledger accounts, and prepare a trial to ledger accounts, and prepare a trial balance.balance.

General Journal

Chapter 3-8

Posting Posting – the process of transferring amounts from the journal to the ledger accounts.

Cash Acct. No. 100

Date Explanation Ref. Debit Credit Balance

General Ledger

Account Title Ref. Debit Credit

J an. 3 Cash 100,000

Common stock 100,000

Date

General Journal

Jan. 3 Sale of stock GJ1 100,000 100,000

100

GJ1

2. Posting2. Posting2. Posting2. Posting

LO 4 LO 4 Record transactions in journals, post Record transactions in journals, post to ledger accounts, and prepare a trial to ledger accounts, and prepare a trial balance.balance.

Chapter 3-9

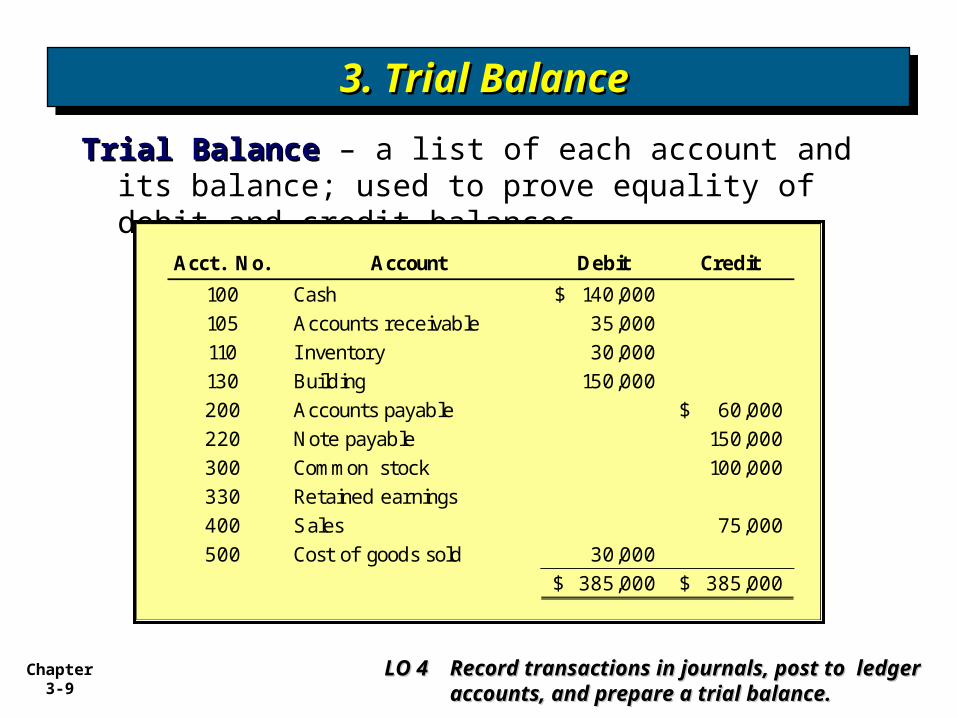

Trial BalanceTrial Balance – a list of each account and its balance; used to prove equality of debit and credit balances.

Acct. No. Account Debit Credit

100 Cash 140,000$ 105 Accounts receivable 35,000 110 I nventory 30,000 130 Building 150,000 200 Accounts payable 60,000$ 220 Note payable 150,000 300 Common stock 100,000 330 Retained earnings400 Sales 75,000 500 Cost of goods sold 30,000

LO 4 LO 4 Record transactions in journals, post Record transactions in journals, post to ledger accounts, and prepare a trial to ledger accounts, and prepare a trial balance.balance.

RevenuesRevenues - recorded in the period in which - recorded in the period in which they are earnedthey are earned.

Expenses Expenses - recognized in the period in which - recognized in the period in which they are incurredthey are incurred.

Adjusting entriesAdjusting entries - needed to ensure that - needed to ensure that the the revenue recognitionrevenue recognition and and matching matching principlesprinciples are followed. are followed.

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Chapter 3-11

Classes of Adjusting EntriesClasses of Adjusting EntriesClasses of Adjusting EntriesClasses of Adjusting Entries

1. Prepaid Expenses. Expenses paid in cash and recorded as assets before they are used or consumed.

Prepayments

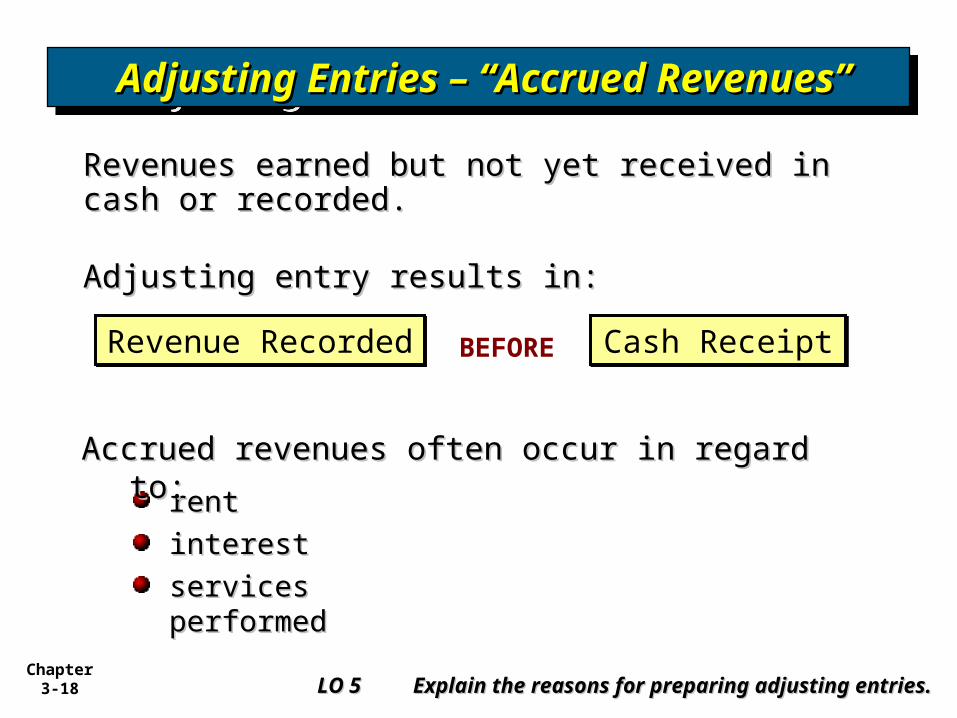

3. Accrued Revenues. Revenues earned but not yet received in cash or recorded.

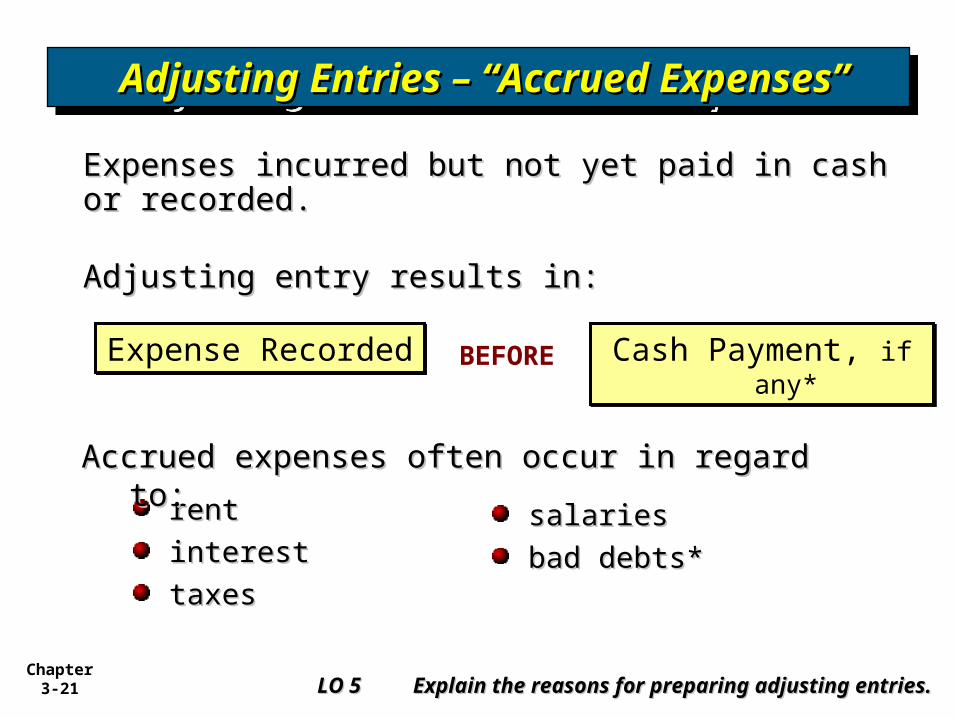

4. Accrued Expenses. Expenses incurred but not yet paid in cash or recorded.

2. Unearned Revenues. Revenues received in cash and recorded as liabilities before they are earned.

Accruals

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Illustration 3-20

Chapter 3-12

Payment of cash that is recorded as an asset because Payment of cash that is recorded as an asset because service or benefit will be received in the future.service or benefit will be received in the future.

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

rentrent

maintenance on maintenance on equipmentequipment

fixed assetsfixed assets

Prepayments often occur in regard to:Prepayments often occur in regard to:

Chapter 3-13

Example:Example: On Jan. 1On Jan. 1stst, Phoenix Corp. paid $12,000 for , Phoenix Corp. paid $12,000 for 12 months of insurance coverage. Show the journal 12 months of insurance coverage. Show the journal entry to record the payment on Jan. 1entry to record the payment on Jan. 1stst. .

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Debit Credit

Prepaid Insurance

12,00012,000 12,00012,000

Debit Credit

Cash

Chapter 3-14

Example:Example: On Jan. 1On Jan. 1stst, Phoenix Corp. paid $12,000 for , Phoenix Corp. paid $12,000 for 12 months of insurance coverage. Show the 12 months of insurance coverage. Show the adjusting adjusting journal entryjournal entry required at Jan. 31 required at Jan. 31stst. .

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Debit Credit

Prepaid Insurance

12,00012,000 1,0001,000

Debit Credit

Insurance expense

1,0001,000

11,00011,000

Chapter 3-15

Receipt of cash that is recorded as a liability Receipt of cash that is recorded as a liability because the revenue has not been earned.because the revenue has not been earned.

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

magazine subscriptionsmagazine subscriptions

customer depositscustomer deposits

Unearned revenues often occur in regard to:Unearned revenues often occur in regard to:

Chapter 3-16

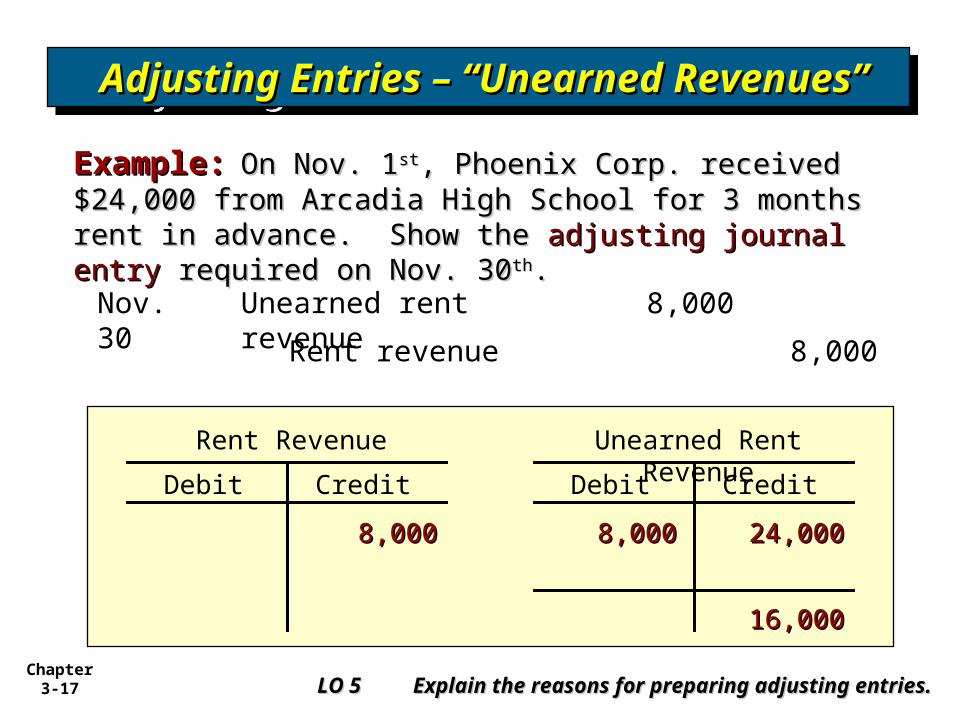

Example:Example: On Nov. 1On Nov. 1stst, Phoenix Corp. received $24,000 , Phoenix Corp. received $24,000 from Arcadia High School for 3 months rent in advance. from Arcadia High School for 3 months rent in advance. Show the journal entry to record the receipt on Nov. 1Show the journal entry to record the receipt on Nov. 1stst. .

Unearned rent revenue

24,000

Cash 24,000

Nov. 1

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Example:Example: On Nov. 1On Nov. 1stst, Phoenix Corp. received $24,000 , Phoenix Corp. received $24,000 from Arcadia High School for 3 months rent in advance. from Arcadia High School for 3 months rent in advance. Show the Show the adjusting journal entryadjusting journal entry required on Nov. 30 required on Nov. 30thth. .

Rent revenue 8,000

Unearned rent revenue 8,000Nov. 30

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

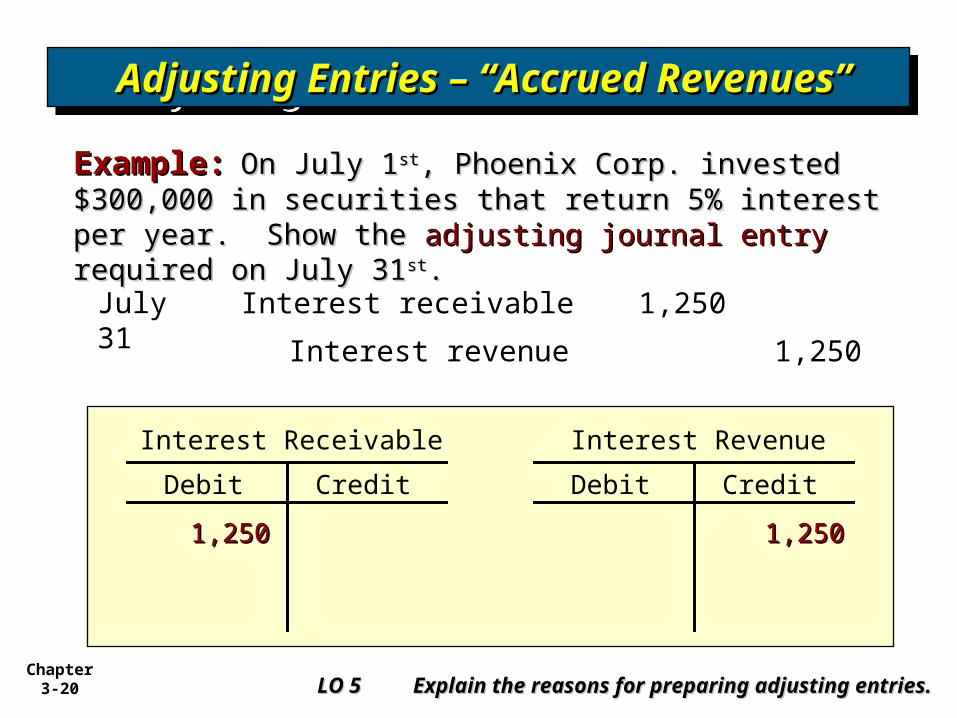

Example:Example: On July 1On July 1stst, Phoenix Corp. invested $300,000 , Phoenix Corp. invested $300,000 in securities that return 5% interest per year. Show the in securities that return 5% interest per year. Show the journal entry to record the investment on July 1journal entry to record the investment on July 1stst. .

Cash 300,000

Investments 300,000

July 1

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

Example:Example: On July 1On July 1stst, Phoenix Corp. invested $300,000 , Phoenix Corp. invested $300,000 in securities that return 5% interest per year. Show the in securities that return 5% interest per year. Show the adjusting journal entryadjusting journal entry required on July 31 required on July 31stst. .

Interest revenue 1,250

Interest receivable 1,250July 31

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

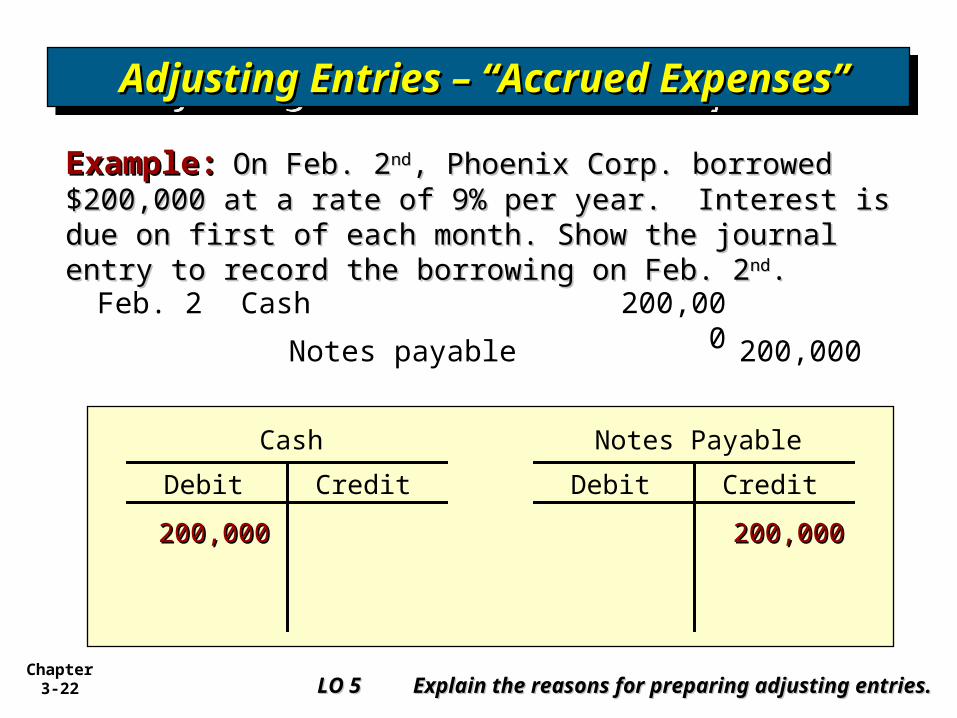

Example:Example: On Feb. 2On Feb. 2ndnd, Phoenix Corp. borrowed $200,000 , Phoenix Corp. borrowed $200,000 at a rate of 9% per year. Interest is due on first of each at a rate of 9% per year. Interest is due on first of each month. Show the journal entry to record the borrowing on month. Show the journal entry to record the borrowing on Feb. 2Feb. 2ndnd..

Chapter 3-23

Example:Example: On Feb. 2On Feb. 2ndnd, Phoenix Corp. borrowed $200,000 , Phoenix Corp. borrowed $200,000 at a rate of 9% per year. Interest is due on first of each at a rate of 9% per year. Interest is due on first of each month. Show the month. Show the adjusting journal entryadjusting journal entry required on Feb. required on Feb. 2828thth..

Interest payable 1,500

Interest expense 1,500Feb. 28

LO 5 LO 5 Explain the reasons for preparing adjusting Explain the reasons for preparing adjusting entries.entries.

LO 7 Prepare closing LO 7 Prepare closing entries.entries.

To reduce the balance of the income To reduce the balance of the income statement (statement (revenuerevenue and and expenseexpense) accounts ) accounts to zero. to zero.

To transfer net income or net loss to owner’s To transfer net income or net loss to owner’s equity.equity.

Balance sheet (Balance sheet (assetasset, , liabilityliability, and , and equityequity) ) accounts are not closed.accounts are not closed.

Dividends are closed directly to the Retained Dividends are closed directly to the Retained Earnings account.Earnings account.

LO 7 Prepare closing LO 7 Prepare closing entries.entries.

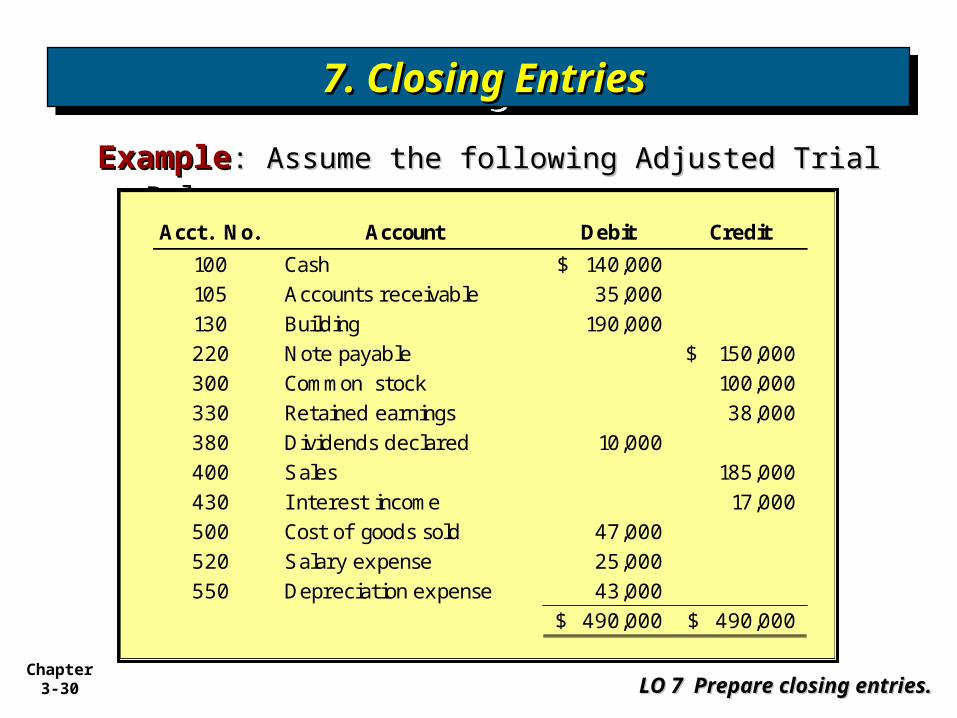

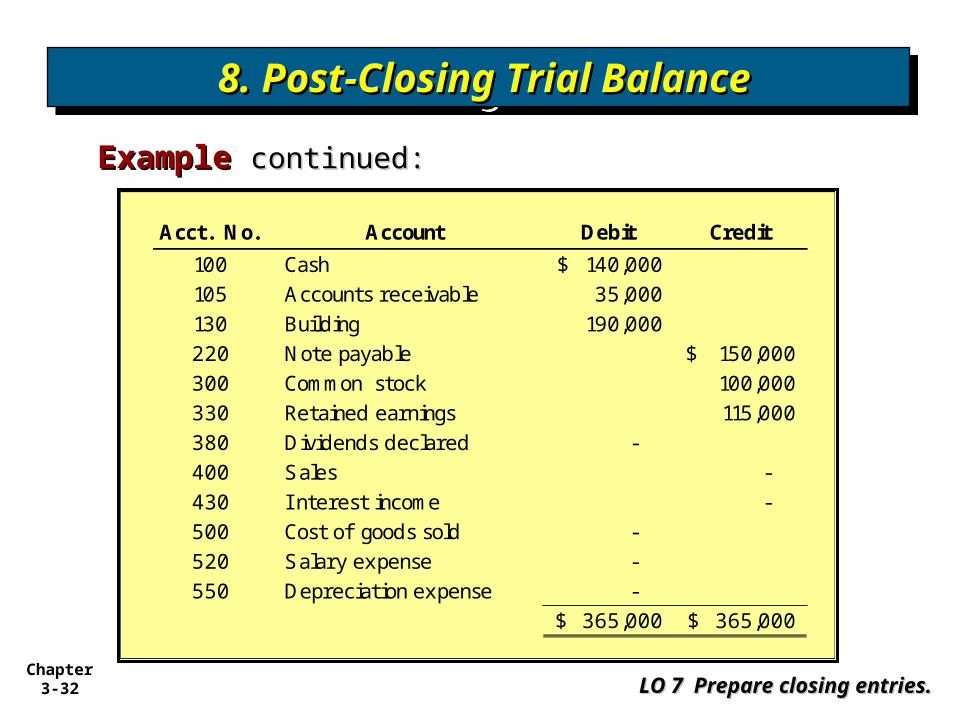

ExampleExample: Assume the following Adjusted Trial : Assume the following Adjusted Trial BalanceBalanceAcct. No. Account Debit Credit

100 Cash 140,000$ 105 Accounts receivable 35,000 130 Building 190,000 220 Note payable 150,000$ 300 Common stock 100,000 330 Retained earnings 38,000 380 Dividends declared 10,000 400 Sales 185,000 430 I nterest income 17,000 500 Cost of goods sold 47,000 520 Salary expense 25,000 550 Depreciation expense 43,000

490,000$ 490,000$

Chapter 3-31

Example:Example: Prepare the Prepare the Closing journal entryClosing journal entry from the from the adjusted trial balance on the previous slide.adjusted trial balance on the previous slide.

LO 7 Prepare closing LO 7 Prepare closing entries.entries.

Reversing entries is an Reversing entries is an optional stepoptional step that a company may perform at the that a company may perform at the beginning of the next accounting beginning of the next accounting period.period.