25

Chapter 3 Theoretical Context

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | elyse-collymore |

| View: | 226 times |

| Download: | 4 times |

Chapter 3

Theoretical Context

Financial Information Analysis 2Copyright 2006 John Wiley & Sons Ltd

Financial Analysis

• ‘Extracting significant information’• Purpose?

• Competitors: competitive advantage• Owners: control • Analysts: identify mis-priced shares • Employees, Creditors: security

• Legitimate exercise?• i.e., does it yield advantage?

Financial Information Analysis 3Copyright 2006 John Wiley & Sons Ltd

Usefulness of analysis

• Can accounting info. satisfy these needs?

• Can analysis:• aid control, • identify advantage, etc.?

• What is role of accounting info?

• Is analysis viable, sustainable?

• If not, why proceed?

Financial Information Analysis 4Copyright 2006 John Wiley & Sons Ltd

Theory of financial analysis

• Theory:• explains• predicts• contextualises• legitimises

• “What is relationship between accounting information and market?”

Financial Information Analysis 5Copyright 2006 John Wiley & Sons Ltd

Theoretical approaches

• Objectivism • ‘reality inherent in object’

• Constructionism• ‘reality is in interplay of object and subject’

• Subjectivism• ‘reality is in eye of beholder’

Financial Information Analysis 6Copyright 2006 John Wiley & Sons Ltd

Accounting Theory

• Predominantly Objectivist• Reality exists independently of experience• Firm incorporates certain realities• Reality can be measured

• society has given accountants ‘authority’ to devise rules to this end

• Measures can be interpreted• Interpretation provides insights on reality

Financial Information Analysis 7Copyright 2006 John Wiley & Sons Ltd

Classic (Normative) Theory

• Objectivist worldview • 1950s-1960s• Economic/Finance theory:

• financial instruments (shares) have intrinsic value

• financial accounts verify this value• analysis confirms accounting measure

• ‘Accounting measures capture reality’

Financial Information Analysis 8Copyright 2006 John Wiley & Sons Ltd

Market-based research

• Economic/Finance theory changes• user perspective• market determines reality• constructionist?

• Accounting information:• no intrinsic value• how does it impact upon users?

• Testable by empirical studies

Financial Information Analysis 9Copyright 2006 John Wiley & Sons Ltd

Portfolio Theory

• Finance theory• Risk

• Quantifiable?• Probability-related• Past performance as basis?• Use of mean with standard deviation• Reduced through diversification

• Risk decreases as portfolio increases

Financial Information Analysis 10Copyright 2006 John Wiley & Sons Ltd

Capital Asset Pricing Model

• Relationship between risk and return• Assumptions

• investors are rational and risk-averse• market is perfect with no transaction costs• information has no cost and is free• all can borrow and lend at risk-free rate • Standard Deviation an appropriate

measure of risk

Financial Information Analysis 11Copyright 2006 John Wiley & Sons Ltd

CAPM

• Portfolio built incrementally SD • ‘Relevant’ risk is impact of marginal

investment on portfolio risk• Unsystematic risk

• unique to security• can be diversified away

• Systematic risk

Financial Information Analysis 12Copyright 2006 John Wiley & Sons Ltd

Systematic (Market) Risk

• Cannot be diversified away• How can it be measured?• BETA ()

• index• 2 bases

• risk-free (govt. bond): = 0• market portfolio: = 1

• Past taken as approximation of future

Financial Information Analysis 13Copyright 2006 John Wiley & Sons Ltd

CAPM Formula

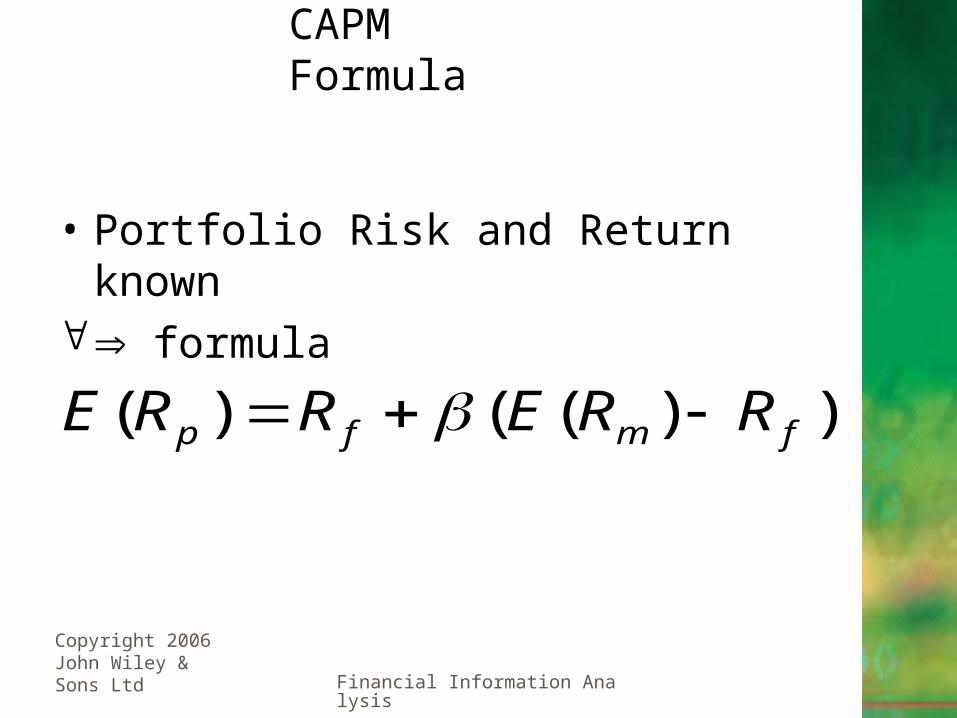

• Portfolio Risk and Return known formula

))(()( fmfp RRERRE

Financial Information Analysis 14Copyright 2006 John Wiley & Sons Ltd

CAPM

• Useful model of expected returns• Empirical tests confirm• Major consequences for accounting

• is accounting information useful?• information regarding future prospects

irrelevant• Fama and French

Financial Information Analysis 15Copyright 2006 John Wiley & Sons Ltd

Arbitrage Pricing Theory (APT)

• Ross - APT

• Multi-index model• macro-economic factors, • interest rate, etc.

• ‘Additional risks incorporated into price to reflect increased risk’

Financial Information Analysis 16Copyright 2006 John Wiley & Sons Ltd

Impact of Changes in Perspective

• CAPM, APT moved focus to market/user• What is impact of accounting data on user?• Is it worthwhile analysing accounting data?• Is it worthwhile producing accounting data?• What is role of accounting, if any?• Is there a better arbiter of value/wealth?

Financial Information Analysis 17Copyright 2006 John Wiley & Sons Ltd

Efficient Market Hypothesis (EMH)

• Focus on market/users• Market as best captor of information• Share price as best measure of wealth• Sources of information other than accounting• All impounded immediately in share price• Stocks valued fairly in light of all available

information

Financial Information Analysis 18Copyright 2006 John Wiley & Sons Ltd

Efficiency

• ‘Share price reflects fairly and immediately all available information’

• Efficiency?• Allocative• Operational• Informational

• How does market react to information?

Financial Information Analysis 19Copyright 2006 John Wiley & Sons Ltd

Weak-form

• ‘Past share movements no guide to future’• Information available: past share prices• Empirical research supports• Random walk• No ‘normal’ value• No advantage in analysing past share price• EMH in weak-form widely accepted

Financial Information Analysis 20Copyright 2006 John Wiley & Sons Ltd

Semi-strong form

• ‘Price reflects all publicly available data’• most Annual Report data probably already

publicly available before issued• i.e., ‘Price impounds information in Annual

Report before issued’ • If no advantage accrues, what is point of:

• Annual Report• Analysis of AR

• Generally supported by empirical tests• Anomalies

Financial Information Analysis 21Copyright 2006 John Wiley & Sons Ltd

Strong form

• Price reflects all data (incl. insider info.)• Testable by identifying market reaction

to insider info.• If all relevant info. impounded then there

should be no effect• In fact research indicates that there is a

reaction• Studies suggest that it is not sustainable

Financial Information Analysis 22Copyright 2006 John Wiley & Sons Ltd

Positive Accounting Theory

• Accounting developed to mediate contracts

• Accounting has role as control mechanism

• Assumes no ‘correct’ approach

• Descriptive, not prescriptive

• Shapes reality as much as describes it

• Useful counter-balance to EMH

• Agency theory

Financial Information Analysis 23Copyright 2006 John Wiley & Sons Ltd

Agency theory

• Natural ally of PAT• People (managers) motivated by self-interest• Control/Monitoring mechanism required• Role for accounting:

• monitoring device• provides language in which to phrase contract• efficient medium through which to operate

firm

Financial Information Analysis 24Copyright 2006 John Wiley & Sons Ltd

Implications for FIA

• EMH fundamentally challenged claims of ‘usefulness’ of accounting information

• ‘Usefulness’ gradually re-asserted by:

• Un-sustainability of Strong form of EMH

• Insights from behavioural finance and economics

• Fundamental Analysis and market research

• Emphasises that accounting information must be:

• considered in broader contexts

• viewed as socially-constructed information

• understood within dynamics of financial markets

Financial Information Analysis 25Copyright 2006 John Wiley & Sons Ltd

Summary

• Market approach challenges notions of:

• usefulness of accounting information

• efficacy of analysis of accounting data

• However, accounting has role as:

• measure of risk

• means of exploiting market anomalies

• source of info. for operational decision-making

• Research has re-established credibility of analysis as means of gaining advantage