Chapter 4 1:05 – 2:05pm The Chapter 13 Plan and Saving Your Client’s Home William F. Malaier Jr. Nagler & Malaier, P.S. PowerPoint distributed at the program and also available for download in electronic format: 1. Chapter 13: Overview and Practice Tips Electronic versions of these documents are available on the KCBA website: https://www.kcba.org/cle/EventDetails.aspx?Event=3713

Transcript

Chapter 4

1:05 – 2:05pm

The Chapter 13 Plan and Saving Your Client’s Home

William F. Malaier Jr. Nagler & Malaier, P.S.

PowerPoint distributed at the program and also available for download in electronic format: 1. Chapter 13: Overview and Practice Tips

Electronic versions of these documents are available on the KCBA website:

Unsecured creditors have fewer rights than in Chapter 11----one of Chapter 13’s advantages over Chapter 11

2/28/2013

2

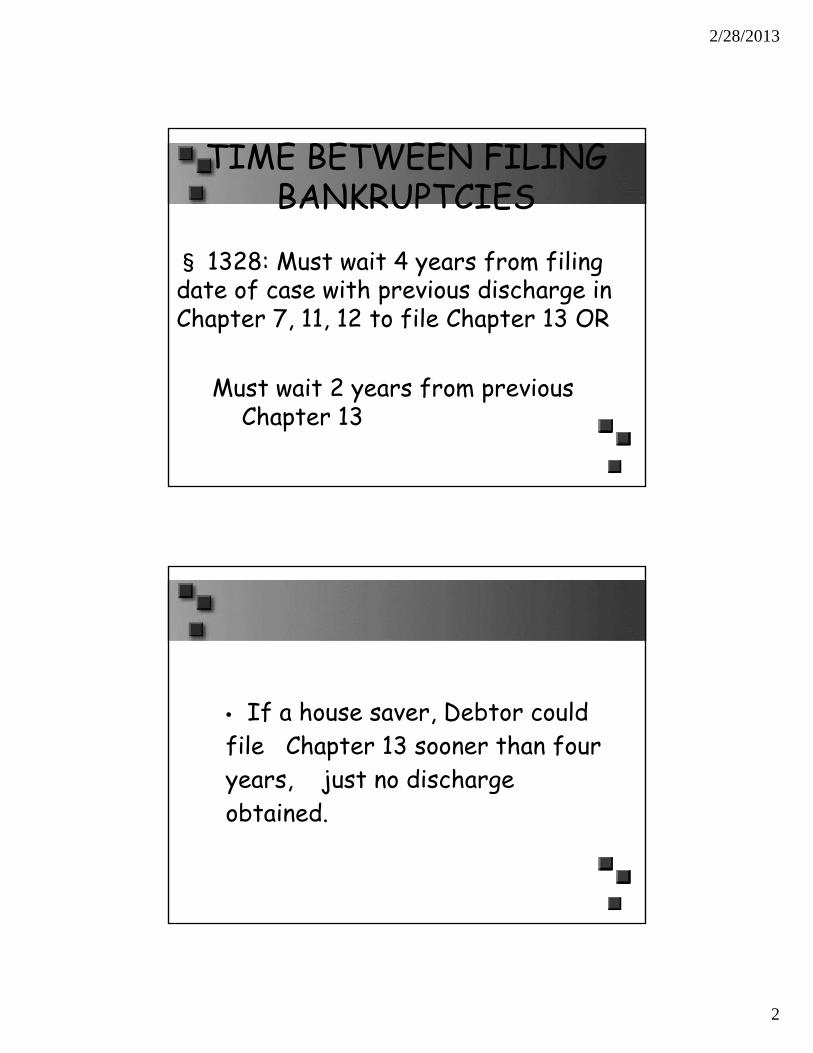

TIME BETWEEN FILING BANKRUPTCIES

§ 1328: Must wait 4 years from filing date of case with previous discharge in Chapter 7, 11, 12 to file Chapter 13 OR

Must wait 2 years from previous Chapter 13

• If a house saver, Debtor could file Chapter 13 sooner than four years, just no discharge b i d obtained.

2/28/2013

3

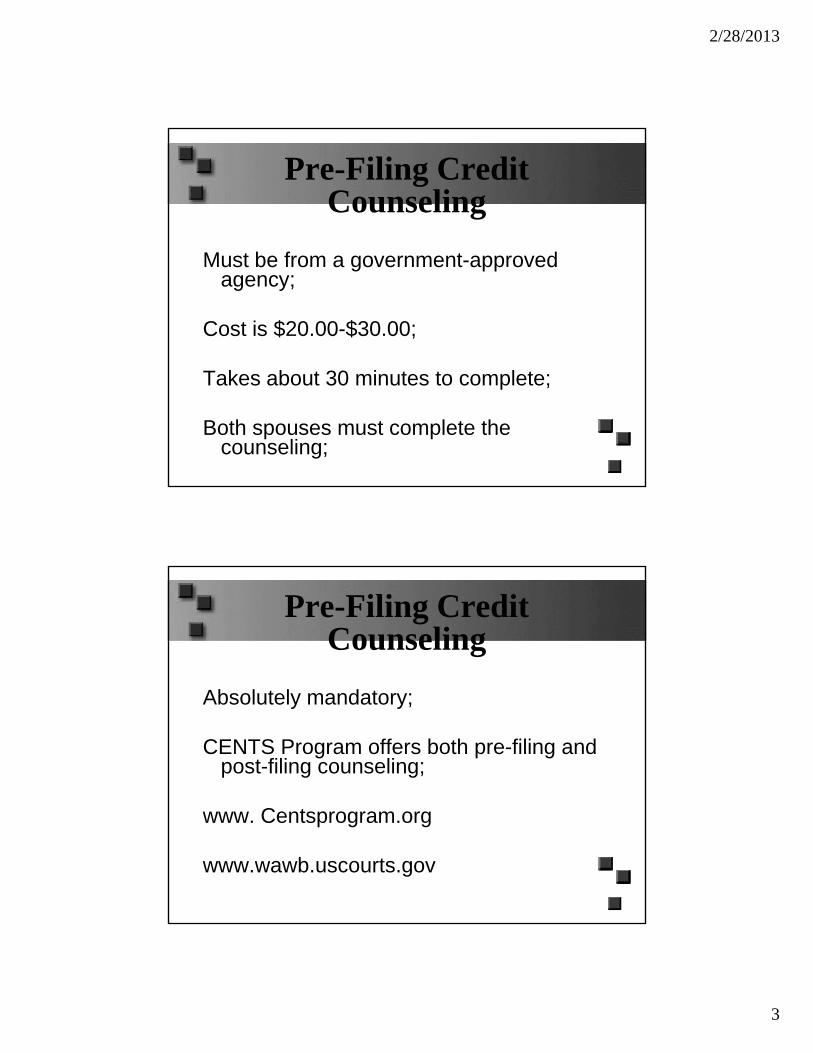

Pre-Filing Credit Counseling

Must be from a government-approved agency;

Cost is $20.00-$30.00;

Takes about 30 minutes to complete;

Both spouses must complete the counseling;

Pre-Filing Credit Counseling

Absolutely mandatory;

CENTS Program offers both pre-filing and post-filing counseling;

www. Centsprogram.org

www.wawb.uscourts.gov

2/28/2013

4

PRE-FILING COUNSELING

• For Chapter 13s, scheduled foreclosure sale will not in itself be sufficient In reWallert 332 be sufficient. In reWallert, 332 B.R. 884 (Bankr. D.Minn. 2005).

PRODUCTION OF CERTAIN DOCUMENTS

§ 521 (a)(1)(B): Debtors must file with their schedules:

Certificate that Debtor was given § 342(b) informational notice;§ 342(b) informational notice;

Copies of all paystubs received within 60 days of filing (email to Trustee);

2/28/2013

5

§ 521 (e)(2)(A): At least 7 days before § 521 (e)(2)(A): At least 7 days before § 341 Meeting Debtor must provide to Trustee or any requesting creditor a copy of most recent federal tax return or transcript of return (email to or transcript of return (email to Trustee)

§ 521 (f)(1)-(3): Debtor must file, at request of party in interest or judge, copies of federal income tax return for tax year ending while Debtor’s case pending AND for tax year within 3 years of case being filed

2/28/2013

6

St t t id f ltStatute provides for no penalty,• though case can be dismissed or

converted for failure to file returns with tax agencyreturns with tax agency

341 MEETING• Rule 4002(b): Picture i.d., evidence of

Social Security number or written Social Security number or written • statement that no such documentationexists,

evidence of current income (most recent paystub) copies of statements

• for each of debtor's depository • for each of debtor s depository • and investment accounts

2/28/2013

7

341 Meeting

Conducted by Chapter 13 Trustee’s staff attorneys;

As compared to 341 Meeting in Chapter 7, the meeting in Chapter 13 is more involved for the debtor’s attorney;involved for the debtor s attorney;

Be familiar with proposed Plan and schedules, statements and means test;

WHAT WILL MONTHLY PAYMENT WHAT WILL MONTHLY PAYMENT BE:

• The greatest of:

1 Di bl i l l t d • 1. Disposable income, calculated under new Means Test and using IRS standards for expenses, OR

Plan Payment, cont.

• 2. Value of all non-exempt assets (liquidation value) paid over 36 months ORmonths OR

2/28/2013

10

Plan Payment, cont.

3. Payment in full of all priority debts over life of Plan

Duration of Ch. 13 Plan

Duration of Plan depends on Debtor’s “Applicable Commitment Period” as defined in the Bankruptcy Code. 11 USC 1325(b).

Essentially annualized income based onEssentially, annualized income based on all gross income received in the 6 months prior to bankruptcy;

2/28/2013

11

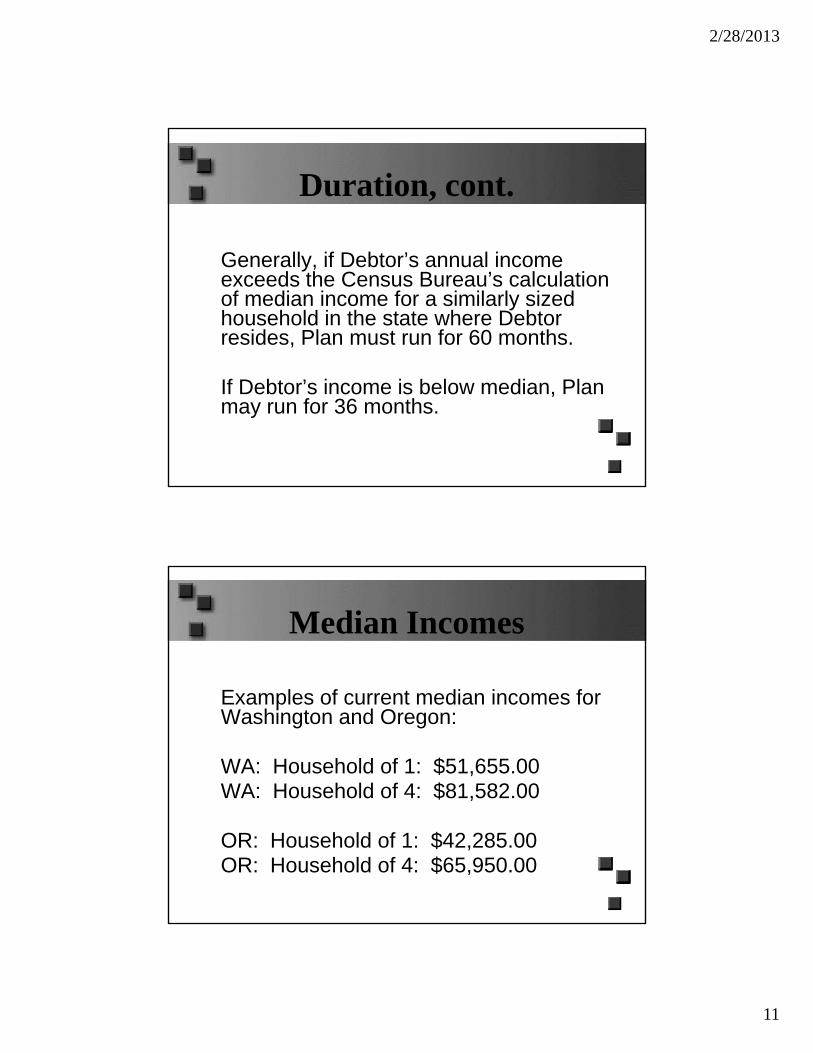

Duration, cont.

Generally, if Debtor’s annual income exceeds the Census Bureau’s calculation of median income for a similarly sized household in the state where Debtor resides, Plan must run for 60 months.

If Debtor’s income is below median, Plan may run for 36 months.

Median Incomes

Examples of current median incomes for Washington and Oregon:

WA: Household of 1: $51,655.00WA: Household of 4: $81,582.00

OR: Household of 1: $42,285.00OR: Household of 4: $65,950.00

2/28/2013

12

• First payment is due within 30 First payment is due within 30 days of filing of Plan

• Must be paid in certified funds, or paid via Chapter 13 Trustee paid via Chapter 13 Trustee garnishment/wage order;

Disposable Income

Vast majority of Chapter 13 Plan payments are driven by Debtor’s disposable income as defined under the BK Code.

For over median Debtors “ProjectedFor over-median Debtors, Projected Disposable Income” is determined by Form 22C (the “Means Test”).

Means Test is merely a government-imposed budget framework.

2/28/2013

13

Disposable Income, cont.

Some line-items on Means Test are based on Debtor’s actual expenses.

Most line-items, however, are based on IRS local and national standards for the state and region of the country in whichstate and region of the country in which the Debtor resides.

Disposable Income, cont.

Upon completion of the Means Test, any remaining money is deemed to be a Debtor’s “ Projected Disposable Income”, and must be paid into the Plan.

Be aware however of Hamilton vBe aware, however, of Hamilton v. Lanning, 130 S.Ct. 2464 (2010)

2/28/2013

14

Disposable Income, cont.

If Debtor is below-median, his/her Chapter 13 disposable income is based upon his/her actual current income and expenses. Schedules I and J;

Selected Means Test Deductions

§ 1325(b): Funds used to contribute to § 1325(b) Funds used to contribute to a pension, 401(k) or IRA; Differs from Chapter 7;

§ 1325(f): Pension loan repayments. p yDiffers from Chapter 7;

2/28/2013

15

Means Test and Non-Filing Spouse’s Income

• Spouse's Income: Under § 101(10)(A) and p § ( )( )(B), debtor's spouse's income included in calculation of “current monthly income” only if filing jointly BUT SEE § 707(b)(6)(B) which says that, in calculating CMI in case that is not joint, income of debtor's spouse that is not joint, income of debtor s spouse not included IF they are separated under applicable non-bankruptcy law OR they are living separate and apart, other than for the purpose of evading this section.

Spouse’s Income, cont.•• Our Trustee's Office says don't include • non-filing spouse's income EXCEPT to • extent non-filing spouse makes • contributions to household expenses• contributions to household expenses.

2/28/2013

16

Means Test Deductions, cont.

• Support of elderly, chronically ill • or disabled is an allowed expense, for

household member OR immediate family, so that, for example, grandparent need not be , p , g pliving with Debtor for expense to qualify.

CONFIRMATION AND CONFIRMATION HEARING

§ 1324(b): Hearing must take place no th 20 d d t l t th sooner than 20 days and not later than

45 days after § 341 Meeting.

Court can order earlier hearing if in gbest interests of creditors.§ 1325(a)(8): Plan unconfirmable if Debtor has not paid all postpetition support payments.

2/28/2013

17

Confirmation of Chapter 13 Plan

Binding effect on all creditors who received notice of the bankruptcy case;

Allows the Chapter 13 Trustee to begin disbursing payments to creditors;

Usually a requirement for approval/payment of attorney’s fees;

Confirmation, cont.

Unlike Chapter 11, no voting requirements for confirmation;

As long as plan is proposed in good faith, and complies with requisites for confirmation set forth in 11 U S C 1325confirmation set forth in 11 U.S.C. 1325, plan may be confirmed over objection of creditors;

2/28/2013

18

Selected Requisites for Confirmation

§ 1325(a)(9): Plan unconfirmable if Debtor has not filed all tax returns.

§ 1325(a)(3): Good faith;§ ( )( ) f ;

Requisites for Confirmation, cont.

§ 1325(a)(6): Feasibility; Debtor must be capable of funding plan to completion;

§ 1325(a)(8): Debtor must be current on all post petition domestic support on all post-petition domestic support obligations on a going-forward basis;

2/28/2013

19

Requisites for Confirmation, cont.

§ 1325(b)(1): Must dedicate all Projected Disposable Income (means test) to non-priority, unsecured claims for duration of Plan (36-60 months);

Requisites for Confirmation, cont.

•§ 1325(A)(4): best interests of Creditors •§ 1325(A)(4): best interests of Creditors Tests

•Regarding liquidation analysis, Debtor and Trustee must now be familiar with exemption sch m s in ll st t s b c us f 730 d rul schemes in all states because of 730-day rule mandated by § 522(b)(3)(A).

2/28/2013

20

LEASES & STAY§ 365(p)(3): If personal property lease is not assumed in Chapter 13 Plan by conclusion not assumed in Chapter 13 Plan by conclusion of confirmation hearing, lease is deemed rejected and stay and co-debtor stay are terminated as to the property.

Must be assumed by motion, not just by Plan provision

Leases, cont.

•§ 365(d)(4): Now extends time to assume nonresidential real property lease to 120 days after filing BUT must be done prior to confirmation order even if confirmation order confirmation order even if confirmation order is entered prioi to 120-day period. The 120-day period can be extended by order ONCE without lessor's consent.

2/28/2013

21

BAR DATE FOR TAX CLAIMS

502(b)(9): In Chapter 13, bar date for tax claims is 60 days after filing y gof any return required to be filed by § 1308

Treatment of Secured Claims in Chapter 13

Plan must provide for retention of secured creditor’s lien until payment in full or discharge Section full or discharge. Section 1325(a)(5)(B)(I).

2/28/2013

22

Treatment of Secured Claims in Chapter 13, cont.

Post-confirmation payments to secured creditors must “adequately protect” secured claim. Section 1325(a)(5)(B)(I).

“Cram-down”

Bifurcation of a secured claim into two distinct claim characterizations, one secured and the other unsecured.

B.A.P.C.P.A. has imposed some limits on Debtor’s ability to cram down securedDebtor s ability to cram-down secured claims on vehicles.

2/28/2013

23

“Cram-down”, cont.

Secured component of a bifurcated claim must be paid in full over the life of the Chapter 13 Plan.

In re: Enewally, 368 F.3d 1165 (9th

Cir 2004)Cir.2004).

Balloon payment at end of plan not acceptable (eg. cramdown on rental real estate).

“Cram-down”, cont.

Special rules for PMSI’s in autos Special rules for PMSI s in autos purchased within 910 days of filing or anything of value purchased within one year of filing; no cram down if objected to. Section j1325(a)

2/28/2013

24

Per Local Rule, Debtors must pay all vehicle claims through the Chapter 13 Plan. No exceptions.

Lien Stripping

Done by adversary proceeding;

Debtor may not strip an undersecuredlien on his/her residence. Nobleman v. American Savings Bank, 113 S.Ct. 2106 (1993)(1993).

2/28/2013

25

Lien Stripping, cont.

Debtor may strip a lien only in 2 instances:

1. Lien to be stripped is ENTIRELY unsecured; OR

2. Lienholder has other collateral;

In re: Zimmer, 313 F.3d 1220 (9th

Cir.2002)

Lien Stripping, cont.

Bankruptcy Code does not allow modification of mortgages secured by Debtor’s primary residence.

Cannot force a mortgage-modification upon a lender.

2/28/2013

26

Priority Claims

Must be paid in full over life of the Chapter 13 Plan.

Payment in full of such claims is a condition of discharge.

Priority Claims, cont.§ 507(a): Debtor’s domestic support obligations will have first priority in obligations will have first priority in distribution, subject to administrative expenses of Trustee. Support obligations assigned to government entities are subordinated to unassigned support bli tiobligations.

2/28/2013

27

Priority Claims, cont.

§ 507(a)(10): New priority for claims for death or personal injury from drunk-driving or use of drugs while driving.

Priority Claims, cont.

§ 507(a)(8): Most recent taxes;

Taxes for which return was timely filed and due within 3 years prior to bankruptcy filing;

2/28/2013

28

PAYMENT OF SUPPORT CLAIMS IN CHAPTER 13

1325( ) Ch 13 Pl b § 1325(a): Chapter 13 Plan cannot be confirmed unless Debtor is current with postpetition support payments

PAYMENT OF SUPPORT CLAIMS IN CHAPTER 13,

cont.

§ 1328(a): Debtor will not receive Chapter 13 discharge until Debtor certifies that all postpetition support payments are currentpayments are current

2/28/2013

29

Payment of Support Claims in Chapter 13, cont.

§ 1307(c)(11): Failure to stay current with postpetition support payments is now a basis for dismissal or conversion of Chapter 13

At time of discharge, trustee must notify holder of claim and DSHS of the Debtor’s holder of claim and DSHS of the Debtor s last known address, employer, the names of creditors holding non-discharged debts (523(a)(2), (4) or (14)), and all reaffirmed debts. Section 1302(d).

2/28/2013

30

Support, cont.

Child support claim holder may request the last known address of a Debtor from a creditor holding a debt excepted from discharge. Section 1302(d)(2).

CONTRIBUTIONS TO EMPLOYEE PLANS

§ 541(b)(7): ERISA-qualified § 541(b)(7): ERISA qualified retirement plans, deferred compensation plans, tax-deferred annuities and health insurance plans NOT property of the estateNOT property of the estate

2/28/2013

31

MISAPPLIED PAYMENTS

§ 524(I): Willful failure of § 524(I): Willful failure of creditor to apply Debtor’s payments pursuant to Plan is violation of discharge injunction f g jif caused material injury to Debtor.

INTEREST ON NONDISCHARGEABLE DEBT

§ 1322(b)(10): Plan may § 1322(b)(10): Plan may provide for payment of interest on nondischargeable debt only if 100% Plan.y f .

2/28/2013

32

CREDITOR REMEDIES

Debtor’s burden to prove that Debtor s burden to prove that filing was in good faith; must be demonstrated to confirm Plan. Section 1325(a).

Grounds for dismissal: failure to timely file a tax return. Section 1307(e);

failure to timely pay domestic support obligations. Section 1307(c)(11).

2/28/2013

33

Creditor Remedies, cont.

Relief from Stay:

1. Must be secured;

2. Creditor has burden of proof;p ;

3. Most common bases are “Cause” or “Lack of Adequate Protection”

FINANCIAL EDUCATION

§ 1328( ) N di h til § 1328(g): No discharge until debtors complete approved financial education program

2/28/2013

34

FINAL REPORT OF TRUSTEE

• § 704(a)(9): Trustee now required to file”final report” at end of Plan. The report must list, among other things, p , g g ,defaults under the Plan.

CONVERSION

348(f)(1)(B) U i f § 348(f)(1)(B): Upon conversion from Chapter 13, valuations of property & of allowed secured claims apply only if conversion is to Chapter 11 or 12, not Chapter 7.p

2/28/2013

35

Conversion, cont.

§ 348(f)(1)(C)(I): Upon conversion from Chapter 13, secured creditor continues to be secured unless full amount of claim was paid before conversion, notwithstanding any valuation of allowed claim during Chapter 13.g p

Nondischargeable Debts

11 U.S.C. 523

1. Fraud or use of false financial statements; Section 523(a)(2)

2. Fraud or defalcation by a fiduciary, b l t l S tiembezzlement or larceny; Section

523(a)(4)

3. Intentional injury to persons; 523(a)(6)

2/28/2013

36

Nondischargeable Debts, cont.

4. Unscheduled creditors; 523(a)(3)

5. Domestic support obligations; 523(a)(5)

Various other debts, including student loans, most taxes, government fines and penalties, restitution, damages arising from DUI, post-petition HOA or condo dues/assessments;

Nondischargeable Debts, cont.

Most nondischargeable debts are t ti ll di h blautomatically nondischargeable.

Some, however, require that dischargeability be litigated by way of adversary proceeding:

Fraud or misrepresentation; 523(a)(2)

Fraud or defalcation by fiduciary; 523(a)(4)

2/28/2013

37

Super-Discharge

Chapter 13 grants Debtors a broader discharge than would be otherwise available under Chapters 7 or 11:

1. Debts arising from a divorce decree or separation agreement;separation agreement;

2. Willful and malicious injury to another’s property (as opposed to bodily injury);