1 Reading Chapters 4 and 5 Chapter 4. Financial Planning, Taxation, and the Efficiency of Financial Market 1. The process of financial planning 2. Assets allocation 3. Taxation 4. Pension plans 5. The efficient market hypothesis 2 1. The Process of Financial Planning Financial planning is a process in which the individual Specifies financial goals Identifies financial resources and obligations Allocates assets into a diversified portfolio to meet the goals The process is affected by external factors such as Inflation Taxation Changes in family circumstances 3 Financial Goals and Resources Possible goals: Emergency needs, Large-item purchases, Education, Retirement Consider financial life cycle: Accumulation, Preservation, Use of accumulated assets Identify resources and obligations: Two financial statements A balance sheet: enumerates what is owned (assets) and owed (liability) Textbook Exhibit 4.1 on page 96 shows an example of a balance sheet. A cash budget (income and expense report): enumerates cash receipts (income) and disbursements (expenditures) Textbook Exhibit 4.2 on page 97 shows an example of a cash budget. 4 2. Assets Allocation Once goals are established and resources identified, one needs to construct a portfolio to meet those goals. Optional portfolio is a diversified portfolio that can meet the identified financial goals. The process of constructing such a portfolio is called assets allocation. 5 3. Taxation Taxation occurs at many levels: federal, state, and local We limit discussion here to federal taxation and taxes that affect investment decisions 6

Transcript

1

Reading Chapters 4 and 5

Chapter 4. Financial Planning,

Taxation, and the Efficiency of

Financial Market

1. The process of financial planning

2. Assets allocation

3. Taxation

4. Pension plans

5. The efficient market hypothesis

2

1. The Process of Financial Planning� Financial planning is a process in which the individual

� Specifies financial goals

� Identifies financial resources and obligations

� Allocates assets into a diversified portfolio to meet the goals

� The process is affected by external factors such as

� Consider financial life cycle: � Accumulation, Preservation, Use of accumulated assets

� Identify resources and obligations: Two financial statements� A balance sheet: enumerates what is owned (assets) and owed

(liability)� Textbook Exhibit 4.1 on page 96 shows an example of a balance

sheet.

� A cash budget (income and expense report): enumerates cash receipts (income) and disbursements (expenditures)� Textbook Exhibit 4.2 on page 97 shows an example of a cash budget.

4

2. Assets Allocation� Once goals are established and resources identified,

one needs to construct a portfolio to meet those goals.

� Optional portfolio is a diversified portfolio that can meet the identified financial goals.

� The process of constructing such a portfolio is called assets allocation.

5

3. Taxation� Taxation occurs at many levels: federal, state, and local

� We limit discussion here to federal taxation and taxes that affect investment decisions

6

2

3.1. The Tax Base

� What is taxed – Potentially there are three tax bases� One’s income (e.g. income tax)

� One’s wealth (e.g. property tax, estate tax)

� One’s consumption (e.g. sales tax, gas tax)

� The tax that affects investment decisions the most is income tax

� Tax on investment earnings (interest + capital gains)

7

3.2. The Tax Structure� Different taxing philosophies

� Progressive: Tax rate increases as tax base increases. � Regressive: Tax rate decreases as tax base increases.� Proportional: Tax rate remains constant as tax base increases.

� Hypothetical Example of Progressive, Regressive, and Proportional Taxation

3.3. The Federal Personal Income Tax� In the U.S. the federal income tax structure is

progressive.

� Tax rates (brackets) in 2012: 10% - 35%� http://taxes.about.com/od/Federal-Income-

Taxes/qt/Tax-Rates-For-The-2012-Tax-Year.htm

� Marginal tax: The tax rate paid on an additional last dollar of taxable income. � E.g., If you are filing single and your taxable income is

$27,225 in 2012, your marginal tax rate is 15%. That means if you earn an additional $1 in interest, you pay 15 cents of it as federal income tax.

9

3.4. Tax Shelters� A tax shelter is an asset or investment that

defers, reduces, or avoids taxation.

� Unlike tax fraud, which is illegal, tax shelters are legal. � E.g., Municipal bonds are a tax shelter. By law,

interest earned from municipal bonds are exempt from federal income taxation.

� E.g., Individual retirement arrangements (IRAs) are a tax shelter. By law, interest earned in traditional IRAs are not taxed until one takes the money out for retirement (deferred tax).

10

3.5. Capital Gains and Losses� Many investments are bought and subsequently sold. If the

sale results in a profit, it is called a capital gain. If the sale results in a loss, it is called a capital loss.

� For tax purposes, capital gains and losses are classified into two categories� Short-term: holding period is one year or less.� Long-term: holding period is more than one year.

� Tax rates:� Short-term capital gains tax rate is the investor's marginal tax rate� Long-term capital gains tax rate is lower:, up to 15% depending on

the tax payer’s marginal tax bracket.

11

Capital Gains – Taxed Only Realized.

�Capital gains are only taxed once realized� If your stock has lost (gained) value this

year, but you do not sell it, you only have paper loss (gain), not realized loss (gain).

�May hold an asset indefinitely and avoid capital gain taxes.

12

3

Capital Losses� Capital losses can be used to offset capital gains in

tax filings.

� The order of offsetting gains and losses:� First, short-term losses offset short-term gains

� Second, long-term losses offset long-term gains

� Third, net short-term losses offset long-term gains or net long-term losses offset short-term gains

� Fourth, net short-term or long-term losses are used to offset income from other sources.

13

Capital Losses� If the investor uses a net capital loss to offset income

from other sources, only $3,000 of capital loss is allowed for a given year.

� Losses exceeding $3,000 are carried forward to future years

� E.g., If John and Mary as a couple has a $5,500 net capital loss for this year, they can use $3,000 of this $5,500 to offset their other income. The remaining $2,500 is carried forward to next year to offset next year’s capital gains, or other income if there is no capital gain next year.

14

Capital Gains and Losses – The

Wash Sale Rule� The wash sale rule prevents you from claiming a loss on a

sale of stock if you buy replacement stock within 30 days before or after the sale. Example: � 3/5/2012: Buy 100 shares of ABC stock. Price=$50/share. Total

investment=$5,000.� Share price goes down. � 12/1/2012: Sell 100 shares of ABC stock. Price=$20/share. Total

capital loss = $3,000. � 12/5/2012: Buy 100 shares of ABC stock. Price=$20/share. Total

investment=$2,000. � This is a wash sale. � The wash sale rule dictates that you cannot claim the $3,000

loss as a capital loss for tax purposes because your loss is not actually realized.

15

4.Tax-Advantaged Pension Plans� Traditional IRAs (Deductible IRAs)

� Roth IRAs (Nondeductible IRAs)

� Keogh accounts

� 401(k) plans and 403(b) plans

� SEPs

16

4.1. Deductible Traditional IRAs� Traditional IRA allows you to deduct some or all of your

retirement contributions from your taxable income� Amounts in your IRA, including earnings, generally are not

taxed until distributed.� Penalty for early withdrawal before age 59 ½. � There are contribution limits and income eligibility rules.

� For 2012, contribution limit is $5,000 annually. � For 2012, if a single person’s adjusted gross income (AGI) is

more than $68,000 then s/he is not eligible.

� Assets in the account are selected by the individual.� For details, go to

http://www.irs.gov/publications/p590/ch01.html

17

4.2. Non-deductible Roth IRA� Created in 1997 and named after its sponsor Senator Roth

from Delaware.� Contributions are NOT deductible from income.� However any earnings from investments are tax free at

withdrawal.� Penalty for withdrawal before age 59 ½. � Contribution limit and income eligibility limit apply:

� For 2012, contribution limit is $5,000 annually.� For 2012, if a single person’s adjusted gross income (AGI) is

more than $125,000 then s/he is not eligible.

� For more information please go to http://www.irs.gov/publications/p590/ch02.html

18

4

Traditional (Deductable) Versus the Roth (Non-

deductible) IRA

� Depending on one’s marginal tax rate, both in terms of current rate and tax rate at retirement, one plan can work better for a particular individual than the other. � If your current marginal tax rate is higher than your

retirement rate, then the traditional IRA is better.

� If your current marginal tax rate is lower than your retirement rate, then the Roth IRA is better.

� Different income eligibilities� Roth has a higher income limit than traditional

19

4.3. Keogh Accounts� Keogh accounts are a retirement plan for the self-

employed.� Established in 1962 and named after then U.S.

Representative Eugene James Keogh� Works just like a traditional IRA – deductible and tax

deferred.� Contribution limit: 25% of net income or $50,000 (in 2012),

whichever is smaller. Limit is adjusted for inflation so it changes every year.

� The concept of net income is a bit confusing. � Net income = Total income – Contribution.� 25% of Net income =20% of Total income� So the effective contribution limit is 20% of total income

20

4.4. 401(k) and 403(b) Plans� Retirement plans offered by an employer. Assets in

the account are chosen from alternatives determined by the employer.

� Participation by employee may be voluntary. Employer may match employee contributions.

� Both the deductable (traditional) or the non-deductable (Roth) types are possible

� 401(k) is typically for for-profit organizations. 403(b) is usually for non-profit organizations, like the University of Utah.

21

4.5. Other Retirement Plans� SEPs: Simplified Employee Plan

� SIMPLE: Savings Incentive Match Plan for Employees of Small Employers

22

4.6. Tax-Deferred Annuities� Annuities are contracts for series of future payments

� E.g., You purchase an annuity for $100,000 that will pay you $10,000 per year for 15 years after you retire.

� Tax-deferred annuities are often sold by life insurance companies.

� Tax-deferred annuity has two components:

� A period in which funds accumulate, tax free, and

� A period in which payments are made by the insurance company to the owner of the annuity. Funds are taxed at the time of distribution.

23

4.7. Life Insurance� Difference between

� Face value: An insurance policy’s death benefits� Cash value: The amount you can receive if you cancel the

policy.

� Growth in cash value not currently taxable. They are taxable only when received. This means this is tax-deferred.

� Death benefits: not taxable to beneficiary

24

5

25

5. The Efficient Market Hypothesis

(EMH)� The Efficient Market Hypothesis is a theory that stock

prices correctly measure the firm’s future earnings and dividends and that investors should not consistently outperform the market on a risk-adjusted basis.

5.1. Assumptions Concerning

Efficient Markets� Three assumptions:

� Large number of competing participants

� Information is readily available

� Transaction costs are small.

� Because these three conditions are generally met, the EMH argues that a stock’s price adjusts rapidly to new information and must reflect all known information concerning the firm.

26

5.2. Random Walk� Because market is efficient and prices adjust rapidly to new

information, day-to-day price changes will follow in a random walk over time. � Random walk is a mathematical formalization of a trajectory

that consists of taking successive random steps.

� Random walk essentially means that � Price changes are unpredictable

� Patterns formed are accidental

� Random walk does not imply stock prices are randomly determined.

� The focus is that day-to-day price changes are random.

27

5.3. The Speed of Price Adjustments

and Degree of Market Efficiency� EMH suggests that prices adjust rapidly to new

information.

� However, if there are inefficiencies in the market, then some investors may be able to take advantages of these inefficiencies.

� Evidence shows that the market is generally efficient. But how efficient?

� There are three forms of the Efficient Market Hypothesis:� the weak form

� the semi-strong form

� the strong form

28

5.3.1. The Weak Form� The weak form implies that

� Technical analysis will not lead to superior investment results.

� Fundamental analysis may still provide excess returns.

� Future price movements are determined by unexpected information and therefore random.

29 30

5.3.2. The Semi-Strong Form� The semi-strong form implies that share prices

adjust to publically available new information very rapidly and in an unbiased fashion, such that no excess returns can be earned by trading on that information.

� Neither technical nor fundamental analyses will be able to reliably produce excess returns.

� However, studying inside information may lead to superior returns.

6

5.3.3. The Strong Form� Share prices reflect all information, public or private,

and no one can earn excess returns.

� Using inside information will not lead to superior investment returns consistently.

31

5.4. Empirical Evidence and

Anomalies� Empirical results generally support:

� the weak form, and the semi-strong form.

� Possible exceptions to the efficient market hypothesis, called anomalies, appear to exist.� The P/E effect� The small firm effect� The January effect� The neglected firm effect� The day-of-the-week effect� The overreaction effect

� The existence of an anomaly does not mean an individual can take advantage of the anomaly due to many reasons, including transaction costs.

32

5.5. Implications of Efficient

Markets� Stock prices embody known information.

� The playing field is level.

� Specifying financial goals may be more important than seeking undervalued stocks.

� Should investors follow a buy-and-hold strategy?

� The good: Reducing transactions costs

� The bad: Such a strategy ignores changes in financial goals.

� Should do: Reevaluate when financial goals change, but don’t trade if goals are still met.

33

Chapter 5. Risk and Portfolio

Management1. Return

2. Sources of risk

3. Total portfolio risk

4. The measurement of risk

5. Risk reduction through diversification

6. Portfolio theory

7. The Capital Assets Pricing Model (CAPM)

8. Beta coefficients

9. Arbitrage pricing theory

34

1. Return� The purpose of investment is to earn a return.

� Return comes from two sources

� Income: interest, dividend

� Capital gains

� Differences among:

� Expected return: The return one anticipates

� Required return: The return necessary to induce the investor to purchase an asset

� Realized return: The actual return one gets

35

1.1. Expected Return

)()(

)( gEP

DErE +=

%303.025.005.020$

20$25$

20$

1$)(

)()( ==+=

−+=+= gE

P

DErE

� E(r)= the expected return� E(D)= the expected dividend or interest

income� P= purchase price of the asset� E(g)=the expected growth in the value of the

asset (capital gain)

36

Example: An investor buys a stock for $20/share and expects to

earn a dividend of $1/share for the year. He also expects to sell the

stock for $25/share after one year. What is his expected return?

7

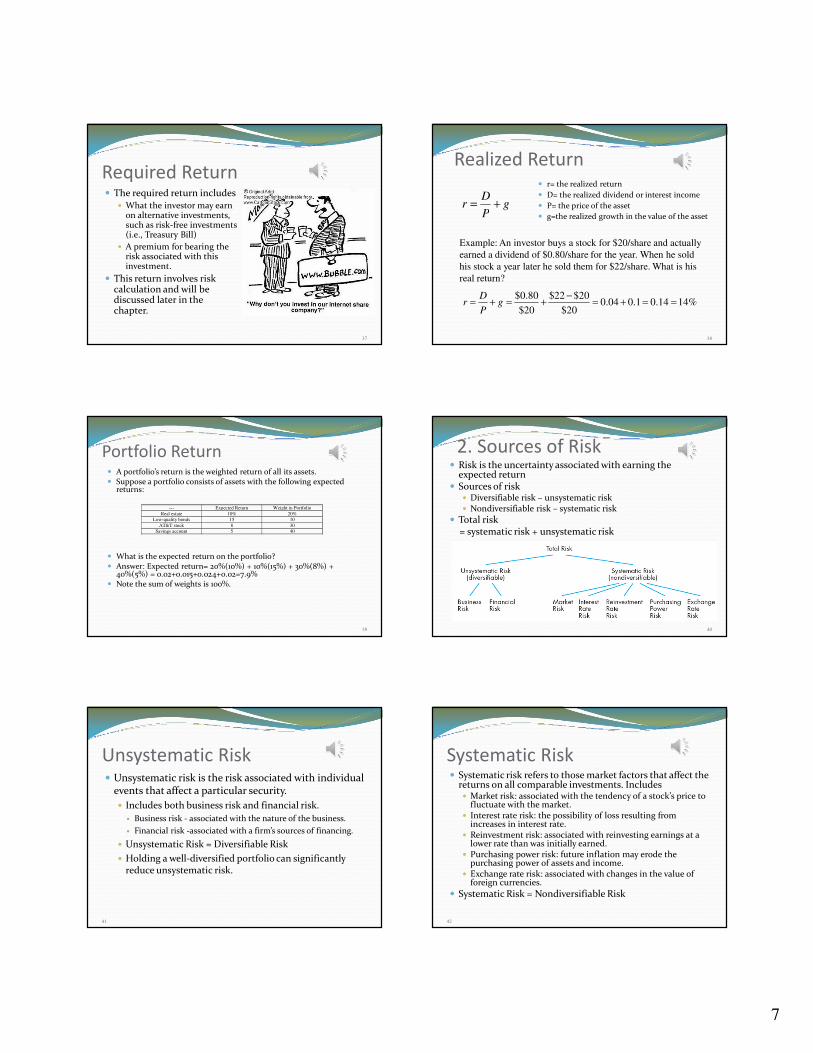

Required Return� The required return includes

� What the investor may earn on alternative investments, such as risk-free investments (i.e., Treasury Bill)

� A premium for bearing the risk associated with this investment.

� This return involves risk calculation and will be discussed later in the chapter.

37

Realized Return

gP

Dr +=

%1414.01.004.020$

20$22$

20$

80.0$==+=

−+=+= g

P

Dr

� r= the realized return

� D= the realized dividend or interest income

� P= the price of the asset

� g=the realized growth in the value of the asset

38

Example: An investor buys a stock for $20/share and actually

earned a dividend of $0.80/share for the year. When he sold

his stock a year later he sold them for $22/share. What is his

real return?

Portfolio Return

--- Expected Return Weight in Portfolio

Real estate 10% 20% Low-quality bonds 15 10

AT&T stock 8 30 Savings account 5 40

39

� A portfolio’s return is the weighted return of all its assets. � Suppose a portfolio consists of assets with the following expected

returns:

� What is the expected return on the portfolio? � Answer: Expected return= 20%(10%) + 10%(15%) + 30%(8%) +

40%(5%) = 0.02+0.015+0.024+0.02=7.9%� Note the sum of weights is 100%.

2. Sources of Risk� Risk is the uncertainty associated with earning the

Unsystematic Risk� Unsystematic risk is the risk associated with individual

events that affect a particular security.

� Includes both business risk and financial risk.

� Business risk - associated with the nature of the business.

� Financial risk -associated with a firm’s sources of financing.

� Unsystematic Risk = Diversifiable Risk

� Holding a well-diversified portfolio can significantly reduce unsystematic risk.

41

Systematic Risk� Systematic risk refers to those market factors that affect the

returns on all comparable investments. Includes� Market risk: associated with the tendency of a stock’s price to

fluctuate with the market. � Interest rate risk: the possibility of loss resulting from

increases in interest rate.� Reinvestment risk: associated with reinvesting earnings at a

lower rate than was initially earned.� Purchasing power risk: future inflation may erode the

purchasing power of assets and income. � Exchange rate risk: associated with changes in the value of

foreign currencies.

� Systematic Risk = Nondiversifiable Risk

42

8

3. Total Portfolio Risk� Total Portfolio Risk (Total Risk)

= Systematic Risk + Unsystematic Risk

� By diversification, one reduces unsystematic risk, thus reducing total portfolio risk. � Diversification

� Means investing in a wide spectrum of assets whose returns are not highly correlated.

� Reduces (or eliminates) unsystematic risk. � Does not reduce systematic risk.

� One should allocate one’s assets to achieve diversification in order to reduce unsystematic risk.

43

Illustration: A Portfolio of Three Stocks

44

4. The Measurement of Risk� Note that measurement of risk requires that you have a

good understanding of basic statistics. Please review the concepts of mean, correlation, standard deviation, and variance if needed before you proceed further.

� Two measures:� Standard Deviation (SD) measures the variability of

returns� The larger the SD, the higher the risk

� Beta measures the volatility of returns relative to the overall market return� The larger the Beta, the higher the relative risk compared to

the whole market

45

Standard Deviation as a Measure of Risk:

One Asset

46

Portfolio Standard Deviation� Depends on:

� Each asset’s variability;

� E.g., Stock A has a SD of 1.01 and Stock B has an SD of 3.30.

� Each asset's weight in the portfolio

� E.g., One allocates 70% of assets to Stock A and 30% of assets to Stock B. Thus Stock A has a weight of 70% while stock B has a weight of 30%.

� Covariance between the assets.

� Stocks A and B may move together to some degree due to systematic risk. Correlation coefficient (often denoted as r and is between -1 to +1) is used to measure such correlation.

47

A Portfolio Standard Deviation (SDP) of

Two Assets� Notations:

� SA = Standard Deviation of asset A

� SB = Standard Deviation of asset B

� WA = Portfolio weight of asset A

� WB = Portfolio weight of asset B

� rAB=Correlation coefficient of assets A & B.

� Portfolio SDP of assets A and B is

ABBABABBAAPrSSWWSWSWSD 22222 ++=

48

Note this formulas is the same as Equation 6.4 from the

textbook page 159 because CovAB = SASBrAB.

9

SDP of Two Assets with Perfect Negative

Correlation (rAB=-1)

� Assume� SA = 1.5

� SB = 2.0

� WA = 70%

� WB = 30%

� rAB= -1

� Portfolio SDP of assets A and B is

45.026.136.01025.1

)1(*0.2*5.1*3.0*7.0*20.2*3.05.1*7.0

2

2222

2222

=−+=

−++=

++=

KK

KK

ABBABABBAAP rSSWWSWSWSD

49

SDP of Two Assets with No Correlation

(rAB=0)

� Assume� SA = 1.5

� SB = 2.0

� WA = 70%

� WB = 30%

� rAB= 0

� Portfolio SDP of assets A and B is

21.1036.01025.1

0*0.2*5.1*3.0*7.0*20.2*3.05.1*7.0

2

2222

2222

=++=

++=

++=

KK

KK

ABBABABBAAPrSSWWSWSWSD

50

SDP of Two Assets with Perfect

Correlation (rAB=1)� Assume

� SA = 1.5

� SB = 2.0

� WA = 70%

� WB = 30%

� rAB= 1

� Portfolio SDP of assets A and B is

65.126.136.01025.1

1*0.2*5.1*3.0*7.0*20.2*3.05.1*7.0

2

2222

2222

=++=

++=

++=

KK

KK

ABBABABBAAP rSSWWSWSWSD

51

Compare Three Scenarios� When the correlation between A and B is perfect at r=1, the

portfolio risk is the highest. In this case unsystematic risk is not reduced at all.

� When the correlation between A and B is completely negative at r=-1, the portfolio risk is the lowest. In this case unsystematic risk is completely eliminated.

� Rule: The smaller the correlation between the returns of assets in one’s portfolio, the lower the total portfolio risk.

� Diversification is achieved when one has several assets in the portfolio that have small correlation with each other.

52

5. Risk Reduction through Diversification

� Often diversification is about holding a variety of different kind of assets such as bonds, stocks, real estate, etc., instead of just several kinds of stocks.

� Historical data on correlation coefficients for returns from various types of assets.

53

6. Portfolio Theory

– The Markowitz Model

�The optimal portfolio choice is made by combing two factors:

�The efficient frontier

�The investor's willingness to bear risk– the indifference map

54

10

The Efficient Frontier� All portfolios (e.g., B) on line

XY are "efficient“� All points on XY yield the

highest possible expected return for the level of risk

� Any portfolio below line XY (e.g., A) is inefficient - offers a lower return for the level of risk

� Any portfolio above line XY (e.g., C) is unobtainable

� The portfolio efficient frontier represents all acceptable and attainable choices to the investor.

55

Investor’s Willingness to Take

Risk: Indifference Map� The graph to the left is an

indifference map.� The investor is equally happy

with the combination of (δp1and r1, lower risk lower expected return), or the combination of (δp2 and r2, higher risk higher expected return)

� Any points on I2 represents a higher expected return for the same risk, compared to points on I1. So the investor is happier (or has higher satisfaction) while on I2 than on I1.

� By the same token, I3 is even better than I2.

56

Optimal Portfolio Choice� Superimposing the

indifference curves on the efficient frontier determines the investor's optimal portfolio.

� On the graph, at Point O (tangent point), the investor attains the highest level of satisfaction for the efficient portfolio choices available to him or her.

57

Differences in Individuals� Different individuals have

different preferences. Some may be more risk seeking while others are more risk averse.

� Flatter indifference curves -> more risk seeking.

� Investor B is more risk-seeking than Investor A.

� These two investors can face the same efficient frontier, but they will make different choices, with Investor B choosing a more risky portfolio than Investor A

58

7. The Capital Asset Pricing Model

(CAPM)� The gist of CAPM

� It replaces portfolio efficient frontier with a related but different concept called “Capital Market Line.”

� Investors maximize their satisfaction by choosing optimal portfolios for their levels of risk preference while facing the constraints of the Capital Market Line.

59

The Capital Market Line

� The capital market line redefines the efficient frontier XY and is marked as AB.

� The intercept is rf, = risk free return.

� Z is the point of tangency on XY.

60

11

Different Optimal Portfolios for Different

Investors

� This graph shows two investors, R more risk tolerant than C, choosing different optimal portfolios.

61

A Pragmatic Capital Market Line� The graph shows a practical application of the

Capital Market Line: risk and return relationship of different types of assets.

62

The CAPM and Beta Coefficients

� The second part of CAPM is the specification of the relationship between risk and return for the individual asset (such as a stock).

� The relationship between risk and return for the individual asset is called the Security Market Line(SML). � Earlier we mentioned two ways of measuring risk:

Standard Deviation and the Beta (β) coefficient.

� Risk measurement is different for Capital Market Line and for Security Market Line. � Capital Market Line: Standard Deviation measure

� Security Market Line: Beta coefficient measure

63

8. Beta Coefficient� Beta coefficient is an index of volatility of an asset

relative to the volatility of the market. � Notation:

� βi = Beta of asset i� σi = Standard Deviation of return on asset i� σM = Standard Deviation of return on the market� riM=correlation coefficient between the return on

asset i and the return on the market

iM

M

i

i r×=σ

σβ

64

Examples of Beta Coefficients

� ABC stock standard deviation is 4%, and the correlation coefficient between ABC stock return and the market return is 0.8. Then the Beta coefficient for ABC stock is

� XYZ stock standard deviation is 20%, and the correlation coefficient between stock return and the market return is 0.7. Then the Beta coefficient for XYZ stock is

32.08.0%10

%4* =×=×= MABC

M

ABC

ABC rσ

σβ

4.17.0%10

%20* =×=×= MXYZ

M

XYZXYZ r

σ

σβ

65

•Suppose the market standard deviation of return is 10%. Interpretation of Beta� Interpretation

� Beta = 1.0: the same volatility as the market return.

� Beta > 1.0: more volatile than the market return.

� Beta < 1.0: less volatile than the market return.

� Depending on the data used, the time period covered, individual stock betas may vary over time and across different sources.

� Historical data show a tendency of beta to move toward 1.0, the market beta.

66

12

Beta Coefficients and

The Security Market Line� The return on a stock

depends on� The risk free rate (rf)� The return on the market

(rM)� The stock's beta (β)

� The return on a stock is� rs= rf + (rM - rf)β� E.g. If rM=6%, rf=3%, stock

ABC β is 1.2. � Then return on stock ABC

is� rs= 3% + (6% - 3%)x1.2

=6.6%

67

Portfolio Betas� Weighted average of the individual asset's betas

� May be more stable than individual stock betas

� E.g. If a portfolio consists of these three stocks

Stock % of Portfolio Beta

XXX 20% 0.8

YYY 30% 1.2

ZZZ 50% 1.5

68

βP=20%*0.8+30%*1.2+50%*1.5=1.27

9. Arbitrage Pricing Theory (APT)� APT is developed as an alternative to the CAPM.

� Arbitrage means buying in one market and simultaneously selling in another market to take advantage of price differentials.

� This process ensures that � There can only be one price for the same security at a

given time

� Portfolios with the same risk will have the same returns

� In APT, security returns (rs) are considered as the result of arbitrage as investors seek to take advantage of perceived differences in prices of risk exposure.

69

Determinants of Return on Stock (rs)� rs=re+b1F1+b2F2+b3F3+b4F4+e

� re= the expected return� F1 to F4 are a series of factors that may affect security prices,

such as� Unexpected inflation� Unexpected changes in industrial production� Unanticipated shifts in risk premiums� Unanticipated changes in the structure of yields

� b1 to b4 are how the individual stock responds to unanticipated changes in those factors

� e is random error. � APT model is being further developed. It is supposed to be

more flexible than CAPM because it allows more than two factors.

![Arnold and Commissioner of Taxation (Taxation) … and Commissioner of Taxation (Taxation) [2017] AATA 1318 PAGE 2 OF 26 CATCHWORDS TAXATION AND REVENUE – appeal …](https://static.documents.pub/doc/80x56/5af2c9387f8b9ac2469120bc/arnold-and-commissioner-of-taxation-taxation-and-commissioner-of-taxation.jpg)