29

1 Chapter 5 Demand Forecasting

| Date post: | 02-Jan-2016 |

| Category: |

Documents |

| Upload: | wendy-cash |

| View: | 20 times |

| Download: | 0 times |

1

Chapter 5

Demand Forecasting

2

1.Importance of Forecasting

Helps planning for long-term growth

Helps in gauging the economic activity (auto sales, new home sales, electricity demand)

Reduces risk and uncertainty in managerial decisions.

3

Types of Forecasts

Qualitative Forecasts- Forecasts based on the survey of experienced managers

Quantitative Forecasts- Forecasts based on statistical analysis (Trend projections)

4

2.Qualitative ForecastsSurveys and opinion polls are used to:

Make short-term forecasts when quantitative data are not available

Supplement quantitative forecasts

Forecast demand for new products for which data do not exist.

5

2:Qualitative Forecasts: Examples

Surveys of business executives plant and equipment expenditure plans

Surveys of plans for inventory change and expectations

Surveys of consumers’ expenditure plans

6

Opinion polls -Executive polling

-Sales force polling

-Consumer intention polling

7

4.Quantitative Forecast Methods

Time Series Analysis - use of past values of an economic variable in order to predict its future value.

Trend Projections (linear trend, growth rate trend).

Types of Time Series Data Fluctuations

Secular trend-long-run upward moments or downward movements

Cyclical fluctuations-fashion, political elections)

Seasonal Fluctuations- Housing starts

Irregular Fluctuations- War, Strikes, disasters

8

9

Cyclical fluctuations - major expansions and contractions in economic data series which recur every several years (Housing construction, auto demand).

Seasonal variation - regular fluctuations in economic activity during each year as caused by weather or social customs (Housing starts, Christmas sales).

10

Irregular or random fluctuations variation in data series due to unique events such as war, natural disaster, and strikes.

11

6. Trend ProjectionExtension of past changes in time series data into the future (sales, interest rate, stock value forecasting)

a)Constant amount of change or growth

Sales = f(time trend)

St = a + bt constant amount

of growth

12

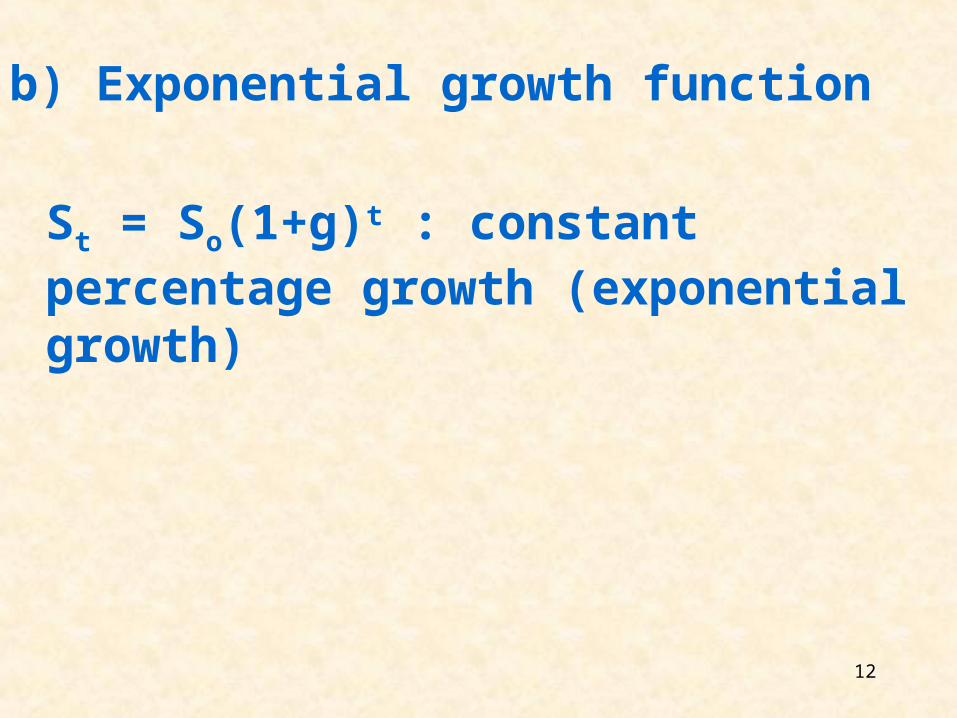

b) Exponential growth function

St = So(1+g)t : constant percentage growth (exponential growth)

13

6a. Linear Trend Projection

14

Demand for Electricity in KWH(million)

Year St t Year St t92-1 11 1 94-1 14 9 -2 15 2 -2 18 10 -3 12 3 -3 15 11 -4 14 4 -4 17 12 93-1 12 5 95-1 15 13 -2 17 6 -2 20 14 -3 13 7 -3 16 15 -4 16 8 -4 19 16

15

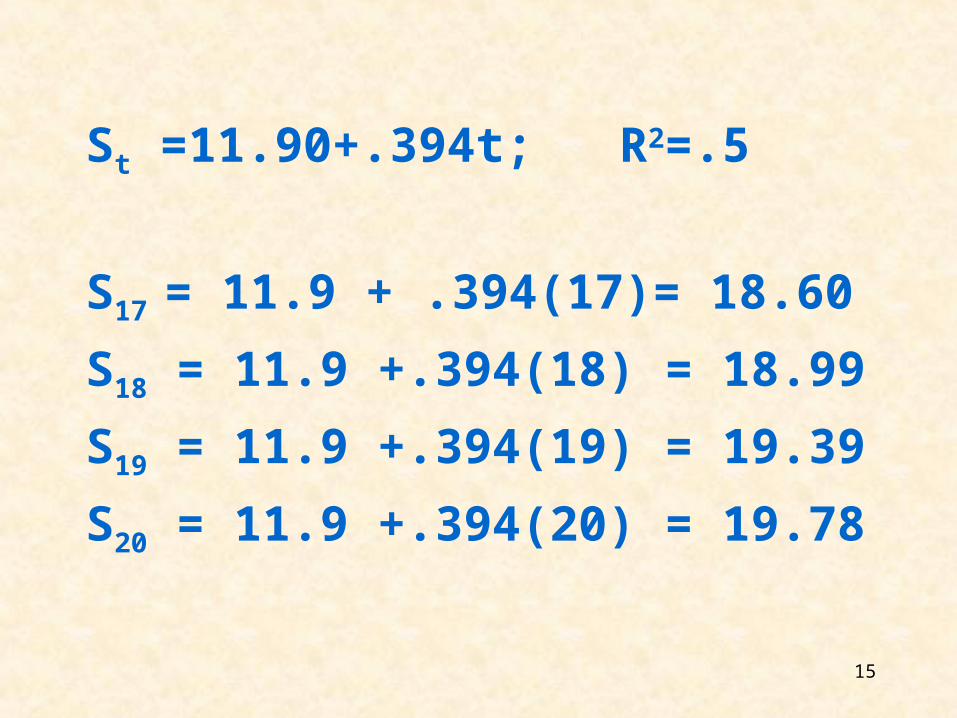

St =11.90+.394t; R2=.5

S17 = 11.9 + .394(17)= 18.60

S18 = 11.9 +.394(18) = 18.99

S19 = 11.9 +.394(19) = 19.39

S20 = 11.9 +.394(20) = 19.78

16

6b. Exponential Growth ProjectionModel: St = S0 ( 1 +g)t

ln St = lnS0 + t ln(1 + g)

Year lnSt t

92.1 2.398 1

. . .

. . .

. . .

95.4 2.944 16

17

ln St = 2.49 + .026t

Taking the antilog of both sides yields,

St= 12.06(1.026)t; R2= .5

S17 = 12.06(1.026)17 = 18.76

S18 = 12.06(1.026)18 = 19.14

S19 = 12.06(1.026)19 = 19.64

S20 = 12.06(1.026)20 = 20.15

tt gSS )1(0

18

Notice that forecasts based on linear trend model tend to be less accurate the further one forecasts into the future.

19

7.Methods of Incorporating Seasonal Variation

a.Ratio to trend methodGroup the data by quartersGet a forecasted value for each quarter by using the trend model

Calculate the actual/forecast ratio for each season or each month.

Find the average of the actual/forecast ratio for each season over the entire period of the study.

20

b. The dummy variable methodMultiply each unadjusted forecasted value of the economic variable by its corresponding seasonal adjusting factor.

Include n-1 dummy variables in the trend equation and run the regression.

21

Time-Series Growth Patterns

Y

tt ̂

Time(t)

tt g)1(ˆ

0

Y

Time(t) Time(t)

Y

2ˆ cttt

(a)Linear trend (b)Exponential growth trend

(c)Declining rate of growth trend

22

8.Some shortcomings of Time Series Analysis

Assumes that past behaviors will be repeated in the future

Cannot forecast turning pointsDoes not examine the underlying causes of fluctuations in economic variables.

23

9.Smoothing Techniques (Irregular Time Series Data)

Refer to the methods of predicting future values of a time series on the basis of an average of its past values only

They are used when the data show irregular variation (random).

24

a. Moving Averages Help to generate acceptable future period

value of a variable when the time series are subject to random fluctuations.

-See, Table 5-5 in the handout 3-quarter vs 5-quarter Moving Average

Forecasts and Comparison

Objective: Forecast 13th quarter value,

given time series data for the previous 12 quarters

25

Choose the appropriate period based on the lowest RMSE.

RMSE= At = actual value of the time series in period t.

Ft = the forecasted value of the time series in period t.

Problem: Gives equal weight to

each period

nFA tt /)( 2

26

b. Exponential smoothing

- a smoothing technique in which the forecast for period t+1 is a weighted average of the actual (At)and forecasted values(Ft) of the time series in period t.

27

Ft+1 = wAt + (1-w)Ft

where Ft+1 = the forecast of F in period t +1.

w= the weight assigned to the

actual value of the time

series, 0<w<1.

1-w = the weight assigned to

the forecasted value of

the time series.

28

10. Using Econometric Models to Forecast

AdvantagesSeek to explain the economic phenomenon being forecasted- i.e. enables mgt to assess the impact of changes in policies (price, Ad)

Predict the direction and magnitude of change

29

Models can be modified based on the comparison of actual and forecast value.

Examples:

Comment: The above advantages have to be weighed against the difficulties of getting the forecast values of each of the explanatory variables.