30

Chapter 5 Accounting

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | nyla-coate |

| View: | 235 times |

| Download: | 3 times |

Chapter 5Accounting

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Development of systems to collect and report financial information

Analyzing this same information

Making finance-related recommendations to assist management decision making

Record and summarize financial data

Purpose of bookkeeping:

The Accounting Function

Facility Engineering & Maintenance

Controller: The individual responsible for recording, classifying, and summarizing the hotel’s business transactions.

Purpose of accounting:

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Financial management system that collects accounting data from an individual hotel site and combines and analyzes that data at the same siteGM and controller take larger role in preparing financial documents

Financial management system that collects accounting data from an individual hotel(s), then combines and analyzes the data at a central sitePrevails in chain-operated or multiproperty hotel companies;company will likely employ CPA for data analysis

Centralized accounting systems:

Decentralized accounting systems:

The Accounting Function (cont.)

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Rooms available for forecasted period

Estimated rooms for the period

Estimated occupancy rate for period

Total rooms sold/total rooms available = occupancy percent (%)

Estimated ADR (average daily rate) for period

– Total room revenue / Total number of rooms sold = ADR

RevPar (revenue per available room) for forecasted period

– Occupancy % X ADR = RevPar

Rooms revenue forecast should include at minimum:

Revenue Forecasting: Rooms Revenue

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Number of guest rooms sold directly impacts amount of Food and Beverage sales volume

Revenue Forecasting: Food & Beverage Revenue

Controller will forecast sales generated from:

– Room service

– Banquets

– Meeting room Food and Beverage revenue

– Audio visual equipment rental

– Service charges

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Pay-per-view moviesParking chargesInternet access chargesGift shop sales of newspapers, cigarettes, candy, lotion, soda, etc.Telephone (local/long distance calling)Guest laundryCoat check feesGolf feesTennis feesHealth club usage feesPool fees

Typical examples of other revenue sources include:

Revenue Forecasting: Other Revenue

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Allowing management to anticipate/prepare for future business conditions

Providing communication channel whereby hotel objectives are passed to various departments

Encouraging department managers who have participated in budget preparation to establish their own operating objectives, evaluation techniques, and tools

Providing GM with reasonable estimates of future expense levels and serving as tool for determining future room rates

Helping controller and GM to periodically evaluate hotel and its progress toward financial objectives

Important functions of a budget:

Budgeting

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Long-Range

Budgets

Encompass relatively lengthy period, generally 2–5 years or moreUseful for long-term planning, considering wisdom of debt financing, refinancing, and scheduling of capital expenditures

Budgeting (cont.)

Annual Budgets

Must be produced by individual hotels and submitted to central office for review in large, multiunit hotel companiesDeveloped to coincide with calendar year

Monthly Budgets

Helps determine whether maintaining progress toward goals developed in annual budgetGreat use for seasonal hotelIn text, refer to figure showing Waldo hotel property operations and maintenance department operating budget for January

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Known as profit and loss statement

Lists hotel’s revenues, expenses, GOP, and fixed charges for specific time (month, fiscal quarter, or year)

In no case should this period exceed middle of next reporting period

Income statement

Balance sheet

Statement of cash flows

Key financial documents:

Income statement:

Financial Statements: Income Statement

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Income Statement InformationThis Period’s Actual

Revenues

Less Direct operating expense

Equals Department operating income

Less Overhead (undistributed) expense

Equals Net income (GOP)

Less Fixed expense

Equals Income before taxes

Financial Statements: Income Statement (cont).

GM can answer: How did hotel perform during this period?

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Tricolumned Income StatementThis

Period’s Actual

This Period’s

Budgeted

Last Year Same Period

Actual

Revenues

Less Direct operating expense

Equals Department operating income

Less Overhead (undistributed) expense

Equals Net income (GOP)

Less Fixed expense

Equals Income before taxes

Financial Statements: Income Statement (cont).

GM can answer: Hotel performance during this period? Hotel performance compared with performance estimate (budget)? Where did estimates vary significantly? How did hotel perform compared with same period last year? Where were significant changes from last year evident?

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Of all assets, none consider relative value/worth of staff, including the GM, actually operating hotelValue of experienced, well-trained staff not quantified

Provides a point-in-time statement of overall financial position of hotel“Snapshot” of financial health of hotelCaptures the financial condition of hotel on day it is produced, rather than telling how profitable the hotel was in a given accounting period

Functions of balance sheet:

Financial Statements: Income Statement (cont.)

Limitations of balance sheet:

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

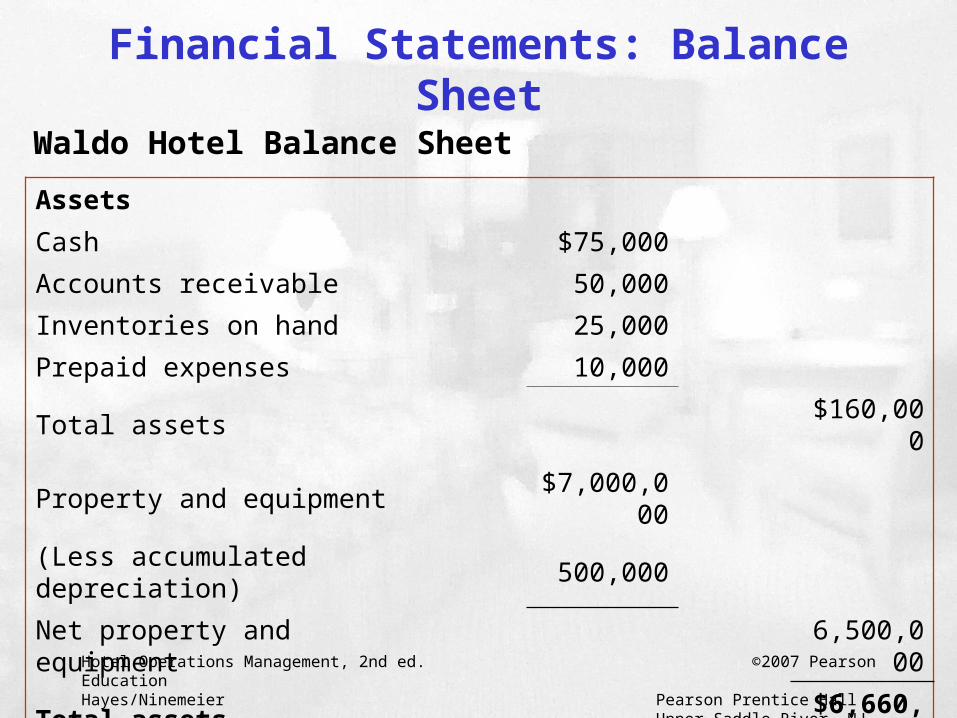

Financial Statements: Balance Sheet

Waldo Hotel Balance Sheet

Assets

Cash $75,000

Accounts receivable 50,000

Inventories on hand 25,000

Prepaid expenses 10,000

Total assets $160,000

Property and equipment $7,000,000

(Less accumulated depreciation) 500,000

Net property and equipment 6,500,000

Total assets $6,660,000

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Financial Statements: Balance Sheet (cont.)

Waldo Hotel Balance Sheet (cont.)

Liabilities and owners’ equity

Current liabilities

Accounts payable $75,000

Wages payable 25,000

Total current liabilities $100,000

Long-term liabilities

Mortgage payable $6,300,000

Total liabilities $6,400,000

Owners’ equity 260,000

Total liabilities and owners’ equity $6,660,000

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

How much cash was provided by hotel’s operation during accounting period?What was hotel’s level of capital expenditure for that period?How much long-term debt did hotel commit to during that period?Will cash be sufficient for next few weeks, or will short-term financing be required?

It is critical that the hotel not only is profitable, but also that it maintains solvency.

Statement of cash flows can answer the following:

Financial Statements: Statement of Cash Flows

It shows cash effects of hotel’s operating, investing, and financing activities.

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

For rooms:– Number of rooms available for sale, number of rooms sold, occupancy rate, ADR, RevPar, and other rooms revenue information

For Food and Beverage:– Restaurant sales, bar and lounge sales, meeting room rentals, banquet sales, and other Food and Beverage revenue information

For other income:– Telephone revenue, in-room movie revenue, no-show billings, and other income

The “Daily”

Controller’s office should provide GM with a timely recap of prior day’s rooms, Food and Beverage, and other revenuesPrepared from data supplied nightly by PMS

Daily Operating Statistics: Manager’s Daily Sales Report

The Daily includes the following:

The more detail you desire, the longer the Daily!

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Rooms availableTotal rooms occupiedRooms occupied by guest typeOccupancy percentTotal ADRADR by guest typeTotal RevPar

Documentation and verification of night auditor’s report is an important function of the controller’s office.

Detailed room revenue report includes:

Night auditor report provides a wealth of info. on room sales.

Daily Operating Statistics: Detailed Room Revenue Statistics

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Adjustments and

Allowances

Reduction in sales revenue credited to guests because of errors in properly recording sales or to appease a guest for property shortcomings.

Daily Operating Statistics: Adjustments and Allowances

Adjustment VoucherADJUSTMENT

NO 348685

(1)

DATE (2) 200xx

NAME (3) ROOM ORACCT.NO. (4)

EXPLANATION (5)

SIGNATURE

X (6)

11-09-0199 (7)

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Employee error in charges– Employee training program, cash sales systems, or guest service techniques

Importance of completion of allowance & adjustment voucher:

Daily Operating Statistics: Adjustments and Allowances (cont.)

Hotel-related problems– Equipment inspection programs, guest service training

Guest-related problems– Total monthly allowance and adjustments / total room revenue = room

allowance and adjustment %

– This percentage varies based on hotel age, quality of staff and training

programs, and type of guest typically served

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Charging guests’ credit cards for items not purchased, then keeping money from erroneous charges

Changing totals on credit card charges after guest has left, or imprinting additional credit card charges and pocketing cash difference

Mis-adding legitimate charges to create higher-than-appropriate total, with intent to keep the overcharge

Charging higher-than-authorized prices for products/services, recording proper price, and keeping the overcharge

Giving/selling credit card numbers to unauthorized individuals outside hotel

Credit card-related techniques used to defraud guests:

Internal Controls: Cash

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Cashier training programs

Sales revenue recording systems

Cash overage/shortage monitoring systems

Enforcement of employee disciplinary procedures for noncompliance

Methods of evaluating cash control systems:

Internal Controls: Cash (cont.)

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Facility Engineering & Maintenance

Accounts Receivable (AR): Money owed to hotel because of sales made on credit.

Internal Controls: Accounts Receivable

Facility Engineering & Maintenance

Direct Bill: An arrangement whereby a guest is allowed to purchase hotel services and products on credit.

Guest seeking credit would complete a “Direct Bill Application” (refer to figure in text).

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Which guests are allowed to purchase goods/services on credit

How promptly those guests will receive bills

What is total amount owed to hotel, and how long have those monies have been owed

Controller’s job to establish:

Internal Controls: Accounts Receivable (cont.)

Facility Engineering & Maintenance

A controller, together with a GM, should establish credit policies that maximize number of guests doing business with hotel yet minimize hotel’s risk of creating uncollectable accounts receivable.

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Accounts Receivable Aging Report

Waldo Hotel: Accounts Receivable Aging Report for January, 200X

Total amount receivable $100,000.00

Number of days past due

Less than 30 30–60 60–90 90+

$50,000

$30,000

$15,000

_____ _____ _____ $5,000

_____ _____ _____

_____ _____ _____

Total $50,000 $30,000 $15,000 $5,000

% of Total 50% 30% 15% 5%

Internal Controls: Accounts Receivable (cont.)

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Payment of proper amounts

Payments made in a timely manner

Payment records properly maintained

Payment totals assigned to appropriate departments

Charge for goods/services used by hotel, invoiced by vendor, not yet paid

Sum total of all invoices owed by hotel to its vendors for credit purchases made by hotel

Accounts Payable (AP):

Internal Controls: Accounts Payable

Four major concerns in AP systems:

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Use a system of coding to assign actual costs to predetermined cost centers

Implement functioning expenses coding system

Create system whereby total payments to vendors match vendor billings exactly

Maintain good relations with vendors by prompt payment of invoices

Take advantage of discounts offered by vendors for prompt payment

Ensure legitimate invoices are paid only for amount actually due

Invoices, and payments for those invoices, should be checked by at least two people

Payment of proper amounts:

Internal Controls: Accounts Payable (cont.)

Payments made in a timely manner:

Payment records properly maintained:

Payment totals assigned to appropriate departments:

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Ensuring payment is made to vendors only for goods/services actually received

Internal Controls: Purchasing and Receiving

Payment should be withheld if all services have not been performed

Before AP invoice is paid, check terms of sale, product prices quoted by vendor, and list of products against actual vendor’s invoices

Devise payment system that ensures member of property management team has:– Preauthorized work– Confirmed cost of work– Verified work is satisfactorily completed

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Internal Controls: Inventories

Facility Engineering & Maintenance

Secure accurate inventory from each department where monthly inventories are taken (refer to monthly income statement).

Beginning period value of towel inventory+ Towel purchases

= Cost of towels available

– Ending period value of towel inventory

Cost of towels used in period

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Proper payment of employees’ salaries and wages is an important function of the controller’s office

Keep detailed, department-specific (individual) payroll info.– Important due to fluid nature of labor usage in hotel

Advice to GM about prevailing wage rates, worker productivity, variation from budget, and future labor needs

Internal Controls: Payroll

Hotel Operations Management, 2nd ed. ©2007 Pearson EducationHayes/Ninemeier Pearson Prentice Hall

Upper Saddle River, NJ 07458

Internal Audit

Independent verification of financial records performed by organization operating hotelCost-effective in multiunit hotels

Audits

Facility Engineering & Maintenance

Auditor: The individual conducting independent verification of financial records.

External Audit

Independent verification of financial records performed by accountants employed by organization operating the hotel