37

Chapter 6: Chapter 6: Demand, Supply & Markets Demand, Supply & Markets

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | agatha-harrell |

| View: | 215 times |

| Download: | 2 times |

Chapter 6:Chapter 6:

Demand, Supply & MarketsDemand, Supply & Markets

What is a Market?What is a Market?

• Any network that brings buyers and sellers together so they can exchange goods and services

• Doesn’t have to be a physical place, but can be done over the internet, phone or fax

• Exists wherever supply and demand determine the price and quantity of goods and services sold

DemandDemand

• Is the quantities of a good or service that buyers are willing and able to purchase at various prices

• Demand schedule shows the various prices and quantity demanded at each price

• Chocolate Bar Auction

DemandDemand

• Economists consistently will gather data and put it into a schedule and then to make it visually easier to understand put the schedule into graph form

• Law of Demand: An increase in price will cause a decrease in quantity demanded

The Demand The Demand CurveCurve

Pri

ce

Quantity Demanded

DDP$

Q0

Application QuestionsApplication Questions

• # 1 – 3 pg. 119

• Work in pairs

• Check answers with others at your table

Law of Diminishing Marginal UtilityLaw of Diminishing Marginal Utility

• Each additional unit of a good or service that is consumed brings less satisfaction or “utils” than the previous unit consumed

• This helps explain why the demand curve is downward sloping

Elasticity of DemandElasticity of Demand

• Shows the responsiveness of the quantity demanded to a change in price

• P x Qd = TR (Total Revenue) • Elastic Demand

– %Δ P < %Δ Qd (P TR )

• Inelastic Demand – %ΔP > %ΔQd (P TR )

• Unitary Demand - – %ΔP = %ΔQd (P - TR -)

FACTORS EFFECTING FACTORS EFFECTING ELASTICITY OF DEMANDELASTICITY OF DEMAND

– # of substitutes (e.g. margarine and butter)

– small items in a budget (e.g. pepper, salt)

– essential items (e.g. water, electricity, natural gas)

– time (e.g. gasoline)

Applications of Elasticity of DemandApplications of Elasticity of Demand

• the more inelastic an item the more heavily it can successfully be used to raise tax revenue (e.g. cigarettes, gas & alcohol)

• Applications #4, 6 pgs. 119 – 120

• Work in pairs

• Check answers with others at your table

Effect of an Increase in DemandEffect of an Increase in Demand P

rice

Lev

el

Quantity

DD

Q0

DD11P$

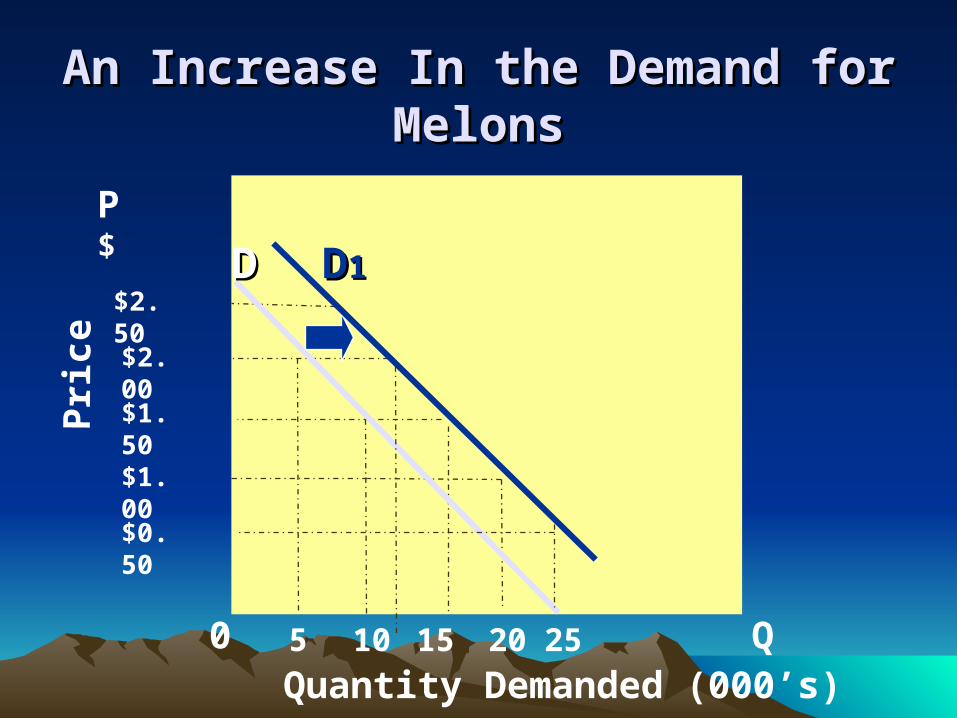

An Increase In the Demand for MelonsAn Increase In the Demand for MelonsP

rice

Quantity Demanded (000’s)0

$1.00

$0.50

15

$1.50

$2.00

$2.50

20 25105

P $

Q

DD DD11

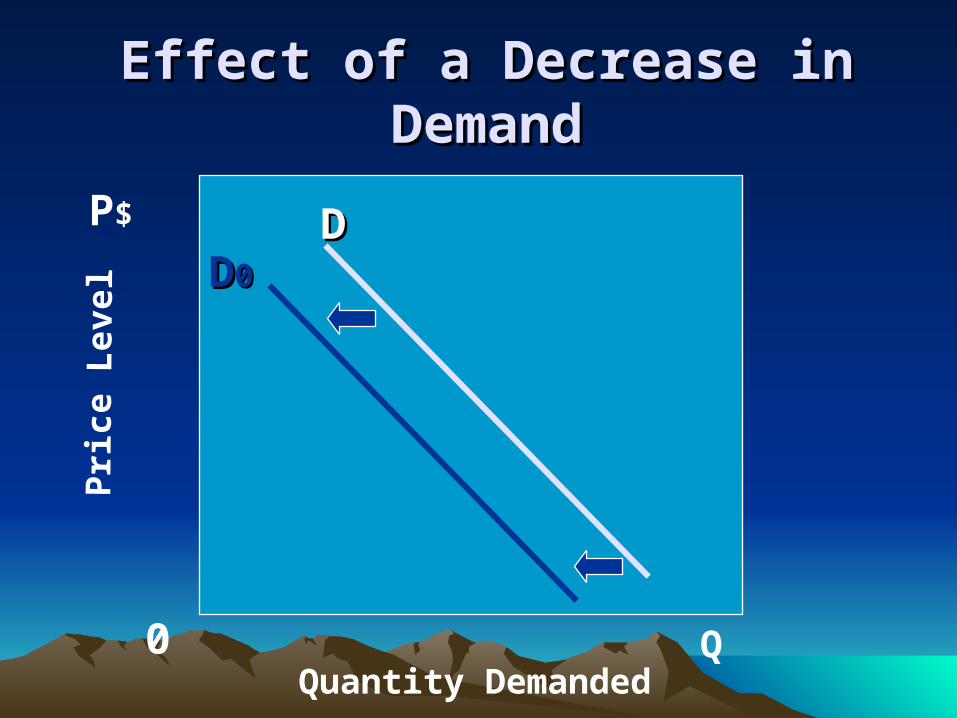

Effect of a Decrease in DemandEffect of a Decrease in Demand P

rice

Lev

el

Quantity Demanded

DD

Q0

DD00

P$

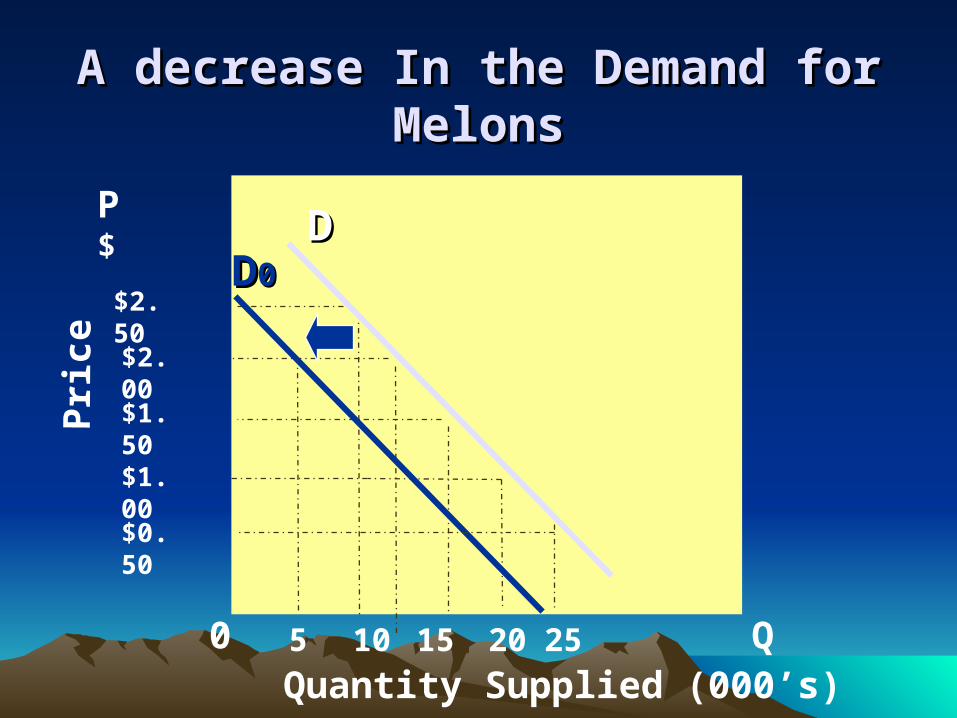

A decrease In the Demand for MelonsA decrease In the Demand for MelonsP

rice

Quantity Supplied (000’s)0

$1.00

$0.50

15

$1.50

$2.00

$2.50

20 25105

P $

Q

DDDD00

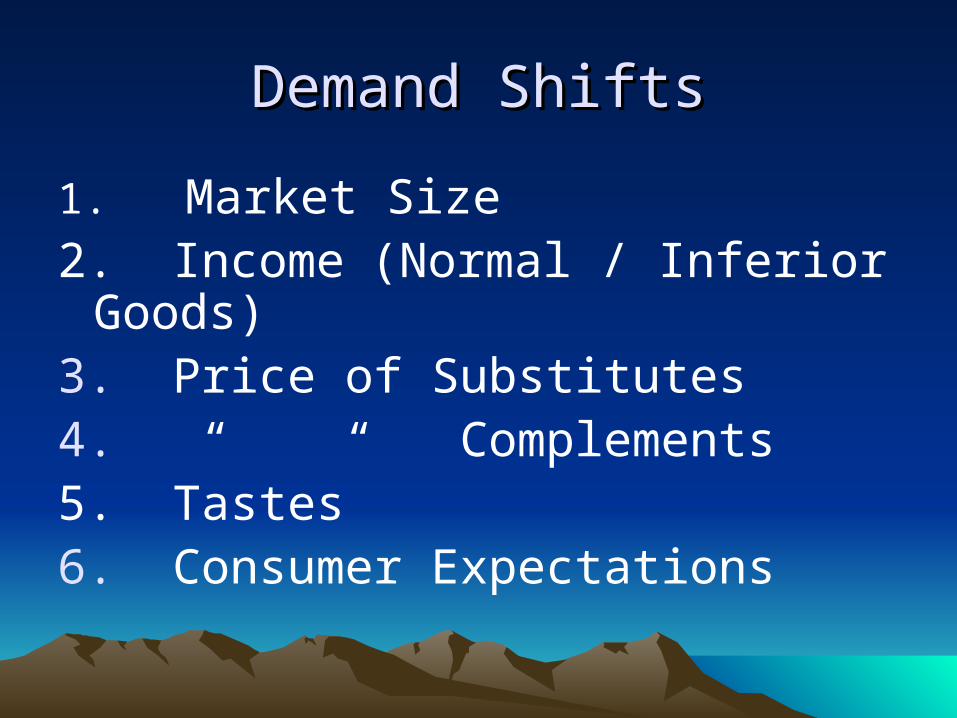

Demand ShiftsDemand Shifts

1. Market Size2. Income (Normal / Inferior Goods)3. Price of Substitutes 4. “ “ Complements5. Tastes6. Consumer Expectations

Application QuestionsApplication Questions

• # 5 pg. 119

• Work in pairs

• Check answers with others at your table

The Supply CurveThe Supply Curve

Supply

•The quantities of a good or service that sellers are willing and able to sell at various prices

•Similar to demand, supply can be shown as a schedule and then as a graph

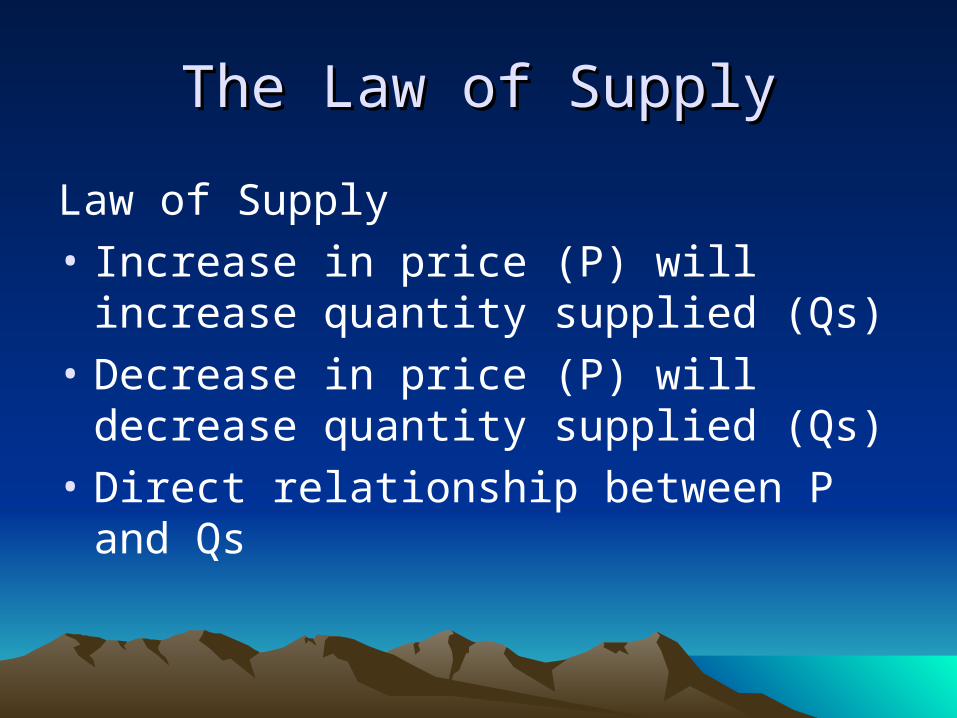

The Law of SupplyThe Law of Supply

Law of Supply

• Increase in price (P) will increase quantity supplied (Qs)

• Decrease in price (P) will decrease quantity supplied (Qs)

• Direct relationship between P and Qs

An Increase In the Supply of MelonsAn Increase In the Supply of MelonsP

rice

Quantity Supplied (000’s)

S

0

$1.00

$0.50

15

$1.50

$2.00

$2.50

20 25105

P $

Q

S1

An Increase In the Supply of MelonsAn Increase In the Supply of Melons

• An increase in supply is represented by a shift in the supply curve to the right (S1).

• At each price point, producers are willing to supply more goods. – For example, at $1.00, producers were

supplying 10,000 units. Now producers are willing to supply 15,000 (an increase of 5,000 units)

A Decrease in the Supply of MelonsA Decrease in the Supply of MelonsP

rice

Quantity Supplied (000’s)

S

0

$1.00

$0.50

15

$1.50

$2.00

$2.50

20 25105

P $

Q

S0

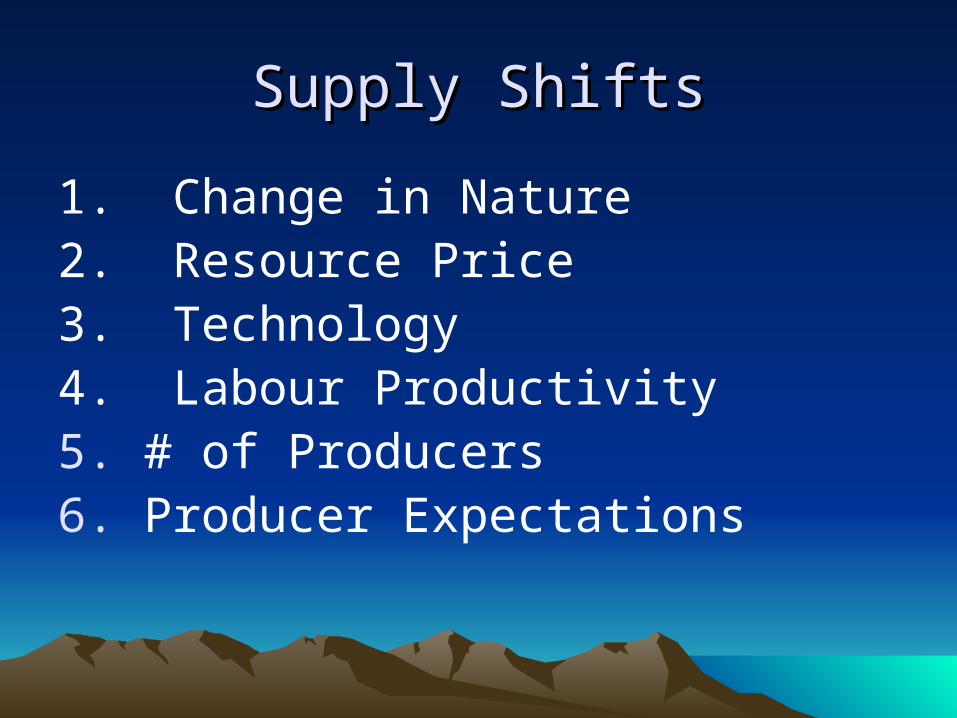

Supply ShiftsSupply Shifts

1. Change in Nature2. Resource Price3. Technology4. Labour Productivity5. # of Producers6. Producer Expectations

Application QuestionsApplication Questions

• #3 pgs. 134 – 135

• Work in pairs

• Check answers with others at your table

• Supply – Demand Game

Demand & Supply Curve ShiftsDemand & Supply Curve Shifts

Demand Causes

1. Market Size2. Income (Normal / Inferior Goods)

3. Price of Substitutes 4. “ “ Complements5. Tastes

6. Consumer Expectations

Supply Causes

1. Change in Nature2. Resource Price3. Technology4. Labour Productivity5. # of Producers6. Producer Expectations

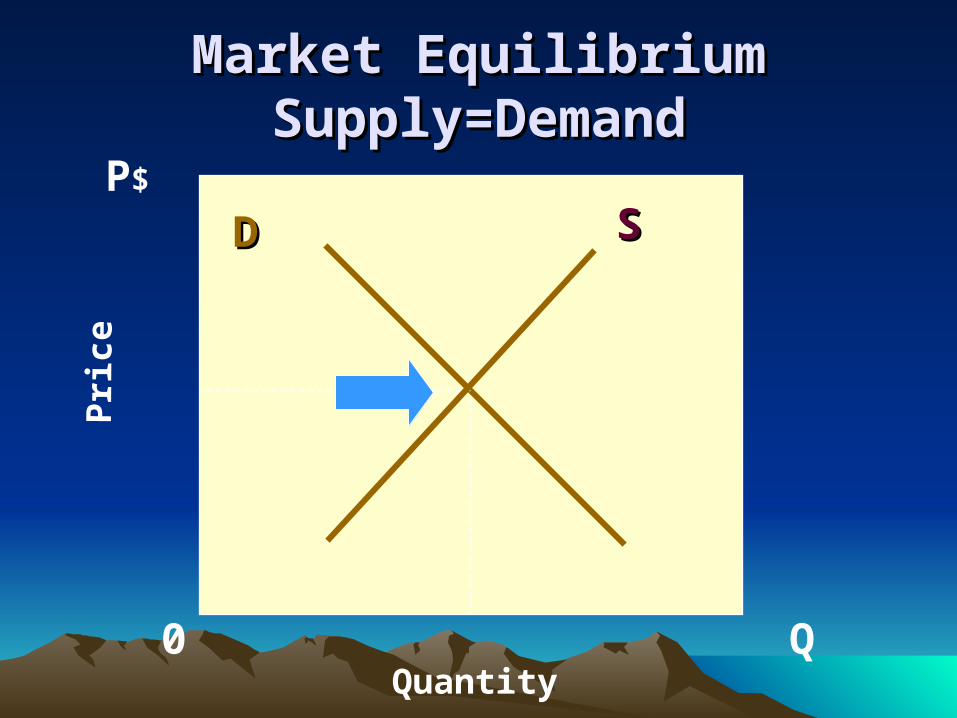

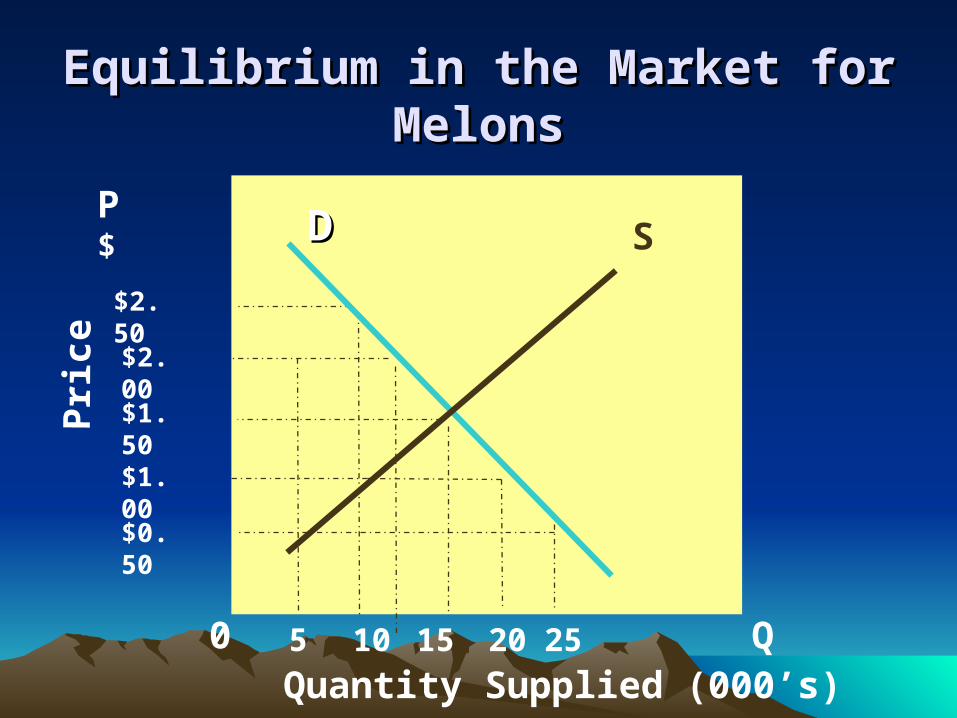

Market EquilibriumMarket Equilibrium

• The point where the supply curve and the demand curve intersect

• At this point, Qd = Qs– (Quantity Demanded = Quantity Supplied)

Market EquilibriumMarket EquilibriumSupply=DemandSupply=Demand

Pri

ce

Quantity

DDP$

Q

SS

0

Equilibrium in the Market for MelonsEquilibrium in the Market for MelonsP

rice

Quantity Supplied (000’s)0

$1.00

$0.50

15

$1.50

$2.00

$2.50

20 25105

P $

Q

DD S

D2

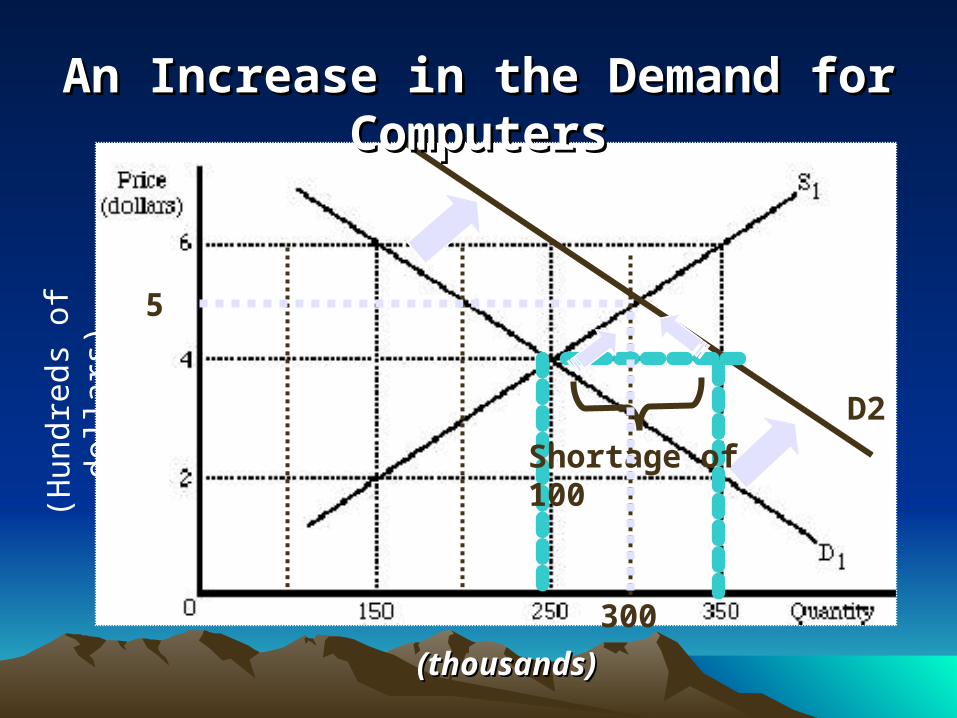

An Increase in the Demand for ComputersAn Increase in the Demand for Computers

Shortage of 100

5

300

(thousands)(thousands)

(Hun

dred

s of

dol

lars

)

D0

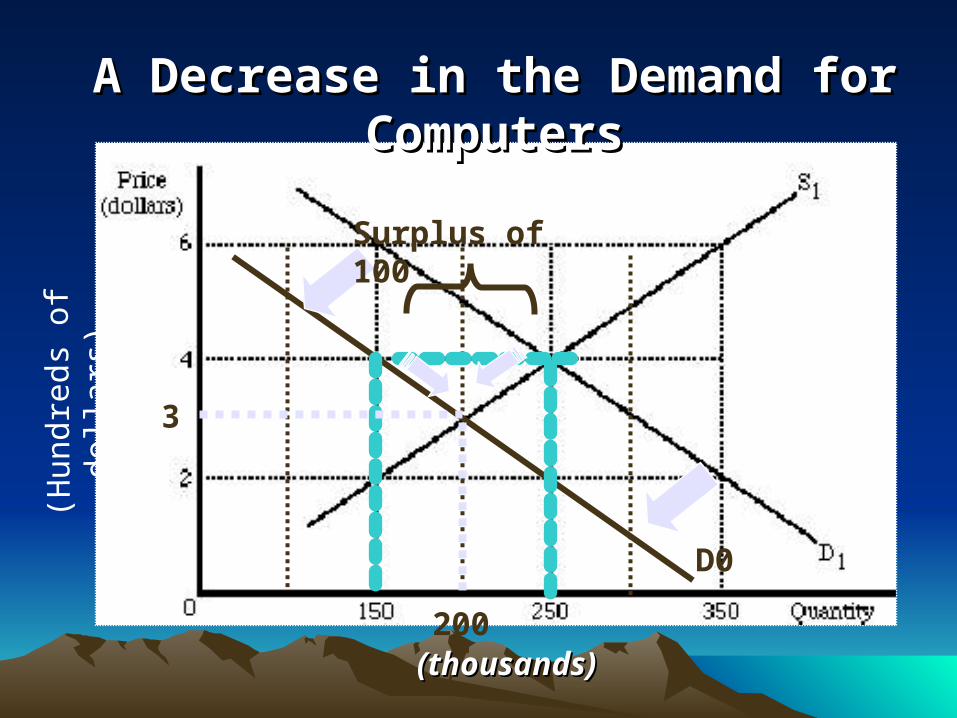

A Decrease in the Demand for ComputersA Decrease in the Demand for Computers

Surplus of 100

3

200(thousands)(thousands)

(Hun

dred

s of

dol

lars

)

S2

An Increase in the Supply of ComputersAn Increase in the Supply of Computers

Surplus of 100

3

300

(thousands)(thousands)

(Hun

dred

s of

dol

lars

)

S0

A Decrease in the Supply of ComputersA Decrease in the Supply of Computers

Shortage of 100

5

200(thousands)(thousands)

(Hun

dred

s of

dol

lars

)

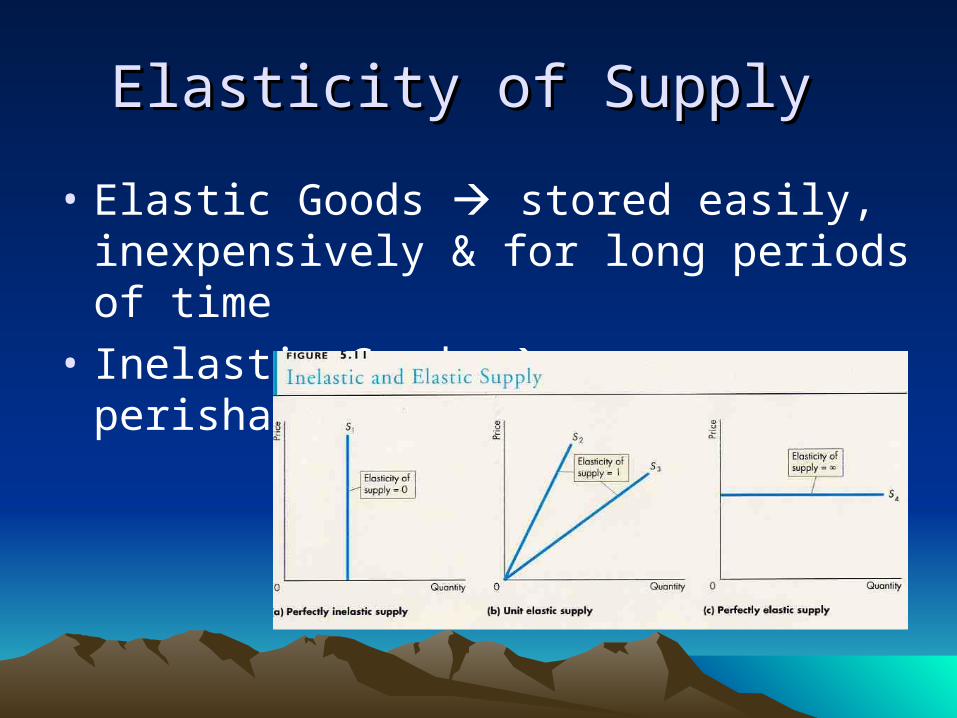

Elasticity of SupplyElasticity of Supply

• similar to Demand

• shows the responsiveness of the quantity supply to a change in price

• key factor effecting supply elasticity is time. – Given more time a producer can supply more

of a product in response to higher prices

Elasticity of SupplyElasticity of Supply

• Elastic Goods stored easily, inexpensively & for long periods of time

• Inelastic Goods more perishable

Gov’t Involvement in the MarketGov’t Involvement in the Market

• at times the market system is unfair • so in our mixed market system the government

steps in to make the situation more fair• if government feels the price is too high make

the price legally lower. • called a ceiling price problem is Qd > Qs

– Excess Demand / Shortage

Gov’t Intervention in the MarketGov’t Intervention in the Market

• If the government feels the price is too low then they make the price legally higher

• called a floor price problem is Qs > Qd– Excess Supply / Surplus

Shortages & SurplusesShortages & Surpluses

Application QuestionsApplication Questions

• #7 pg. 121

• #1 – 2 pg. 134

• #4 – 5 pg. 135

• Work in pairs

• Check answers with others at your table