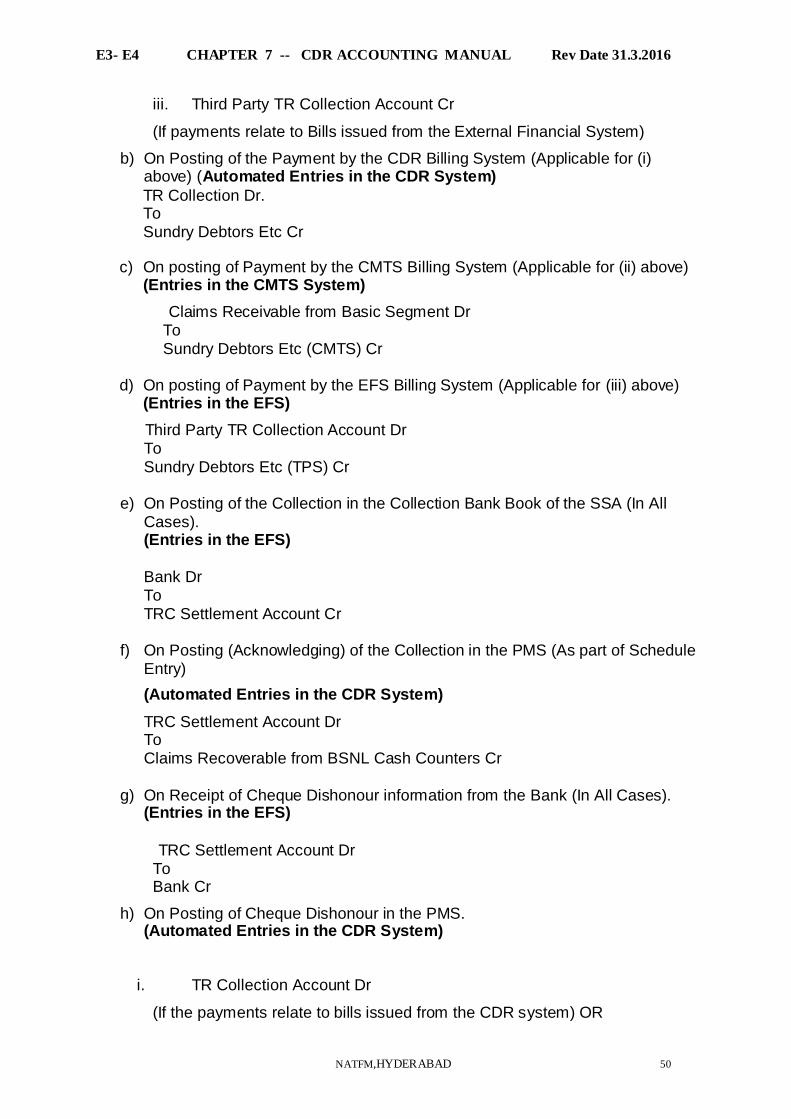

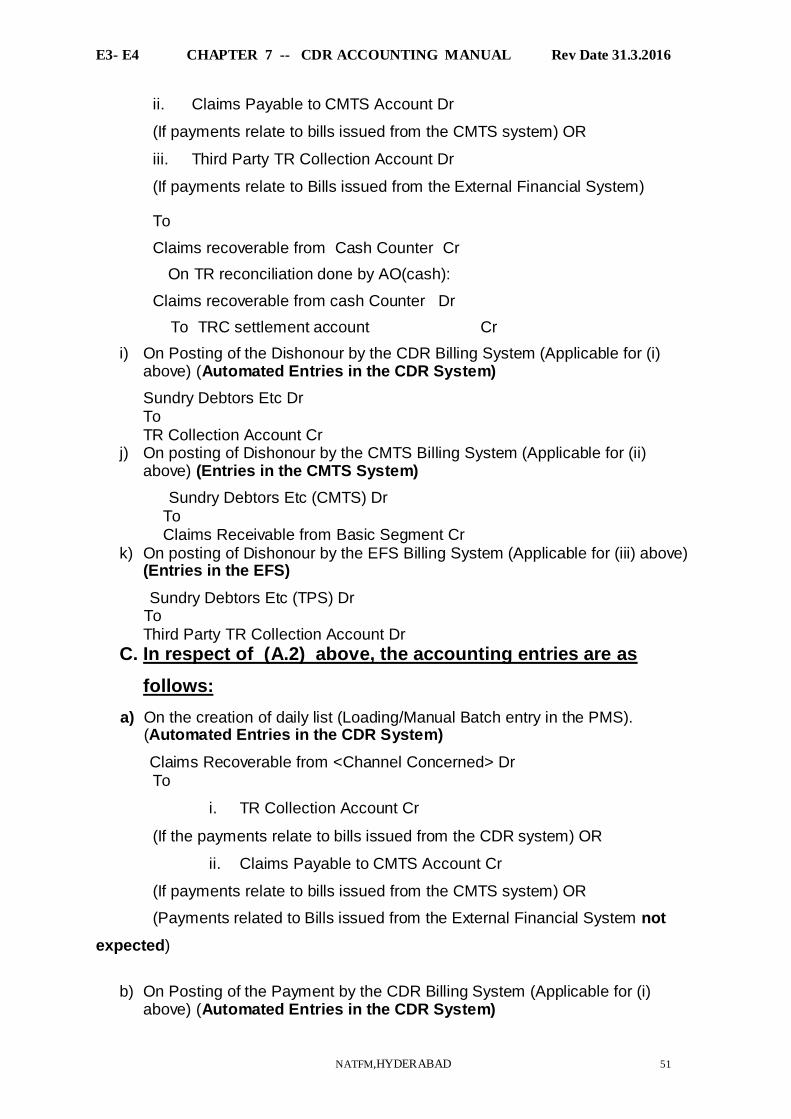

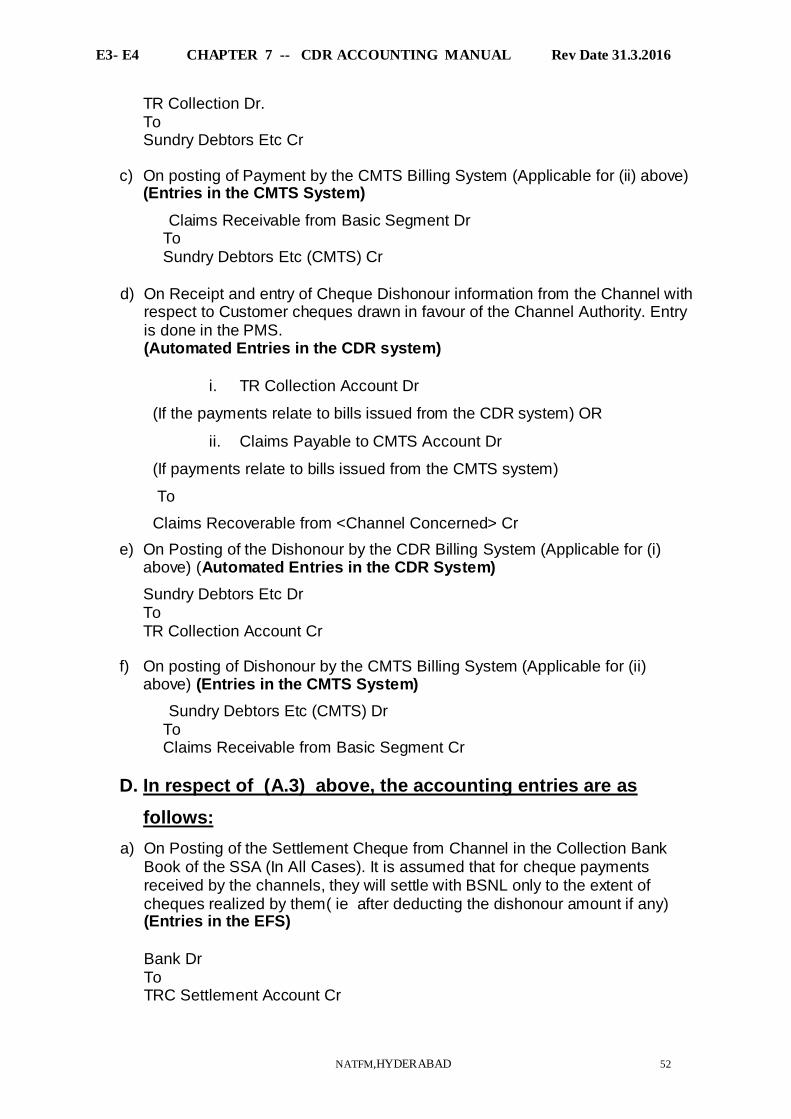

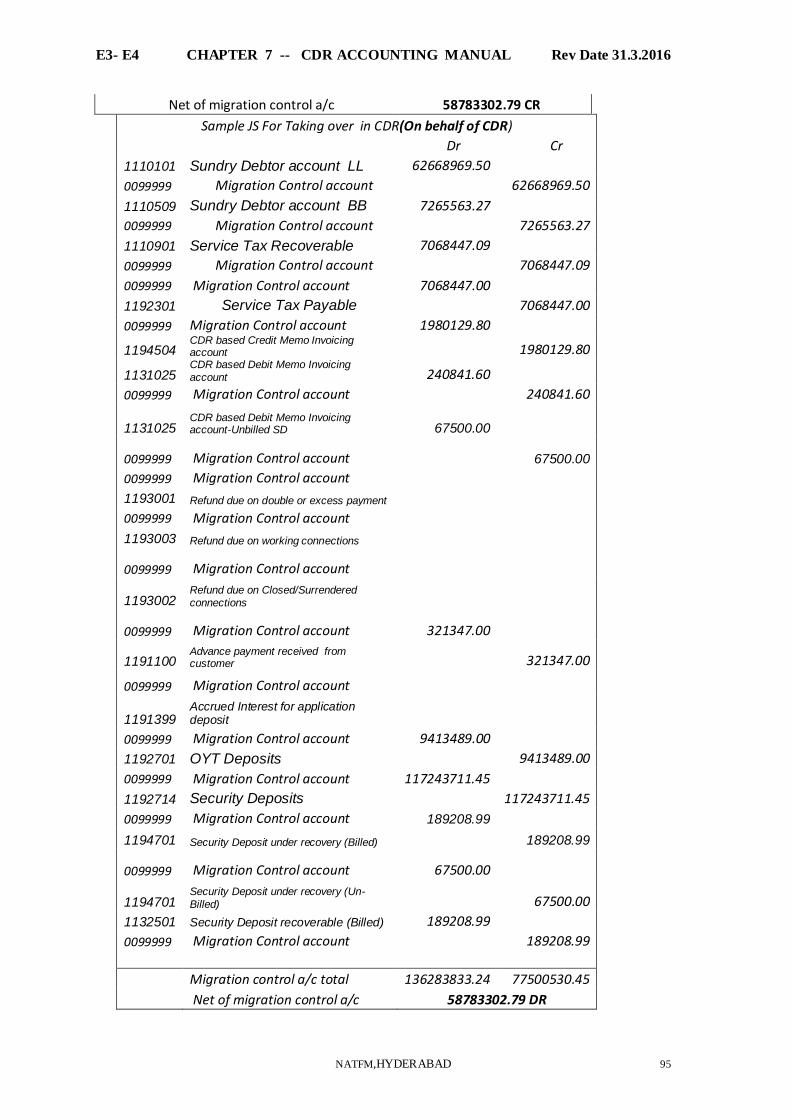

122

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016 NATFM,HYDERABAD 0 Chapter 7 CDR-ACCOUNTING MANUAL

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 0

Chapter 7 CDR-ACCOUNTING MANUAL

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 1

Contents Page No.

1. Introduction to Accounting 3

2. Accounting Scope 4

3. Process Flow 6 4. Chart of Accounts 8

5. Accounting for Invoices and Related Payments 13 a. Invoice Generation and Complete Payment in the same SSA 14 b. Excess/Double Payments when payment is made in the Billing SSA 16

c. Partial Payments made in the Billing SSA 19 d. Remittance to different SSA, Same Circle (Complete payment) 22 e. Remittance to SSA of Same Circle (Partial Payment) 24

f. Remittance to different SSA of same Circle (Excess Payment) 28 g. Remittance to SSA of different Circle (Full Payment) 29 h. Surcharge on delayed payments (Late fee) 30

6. Accounting for GSM Collections 30 a. GSM Invoice of one Circle, Payment in SSA of same Circle 30

b. GSM Invoice of one Circle, Payment in SSA of different Circle 31

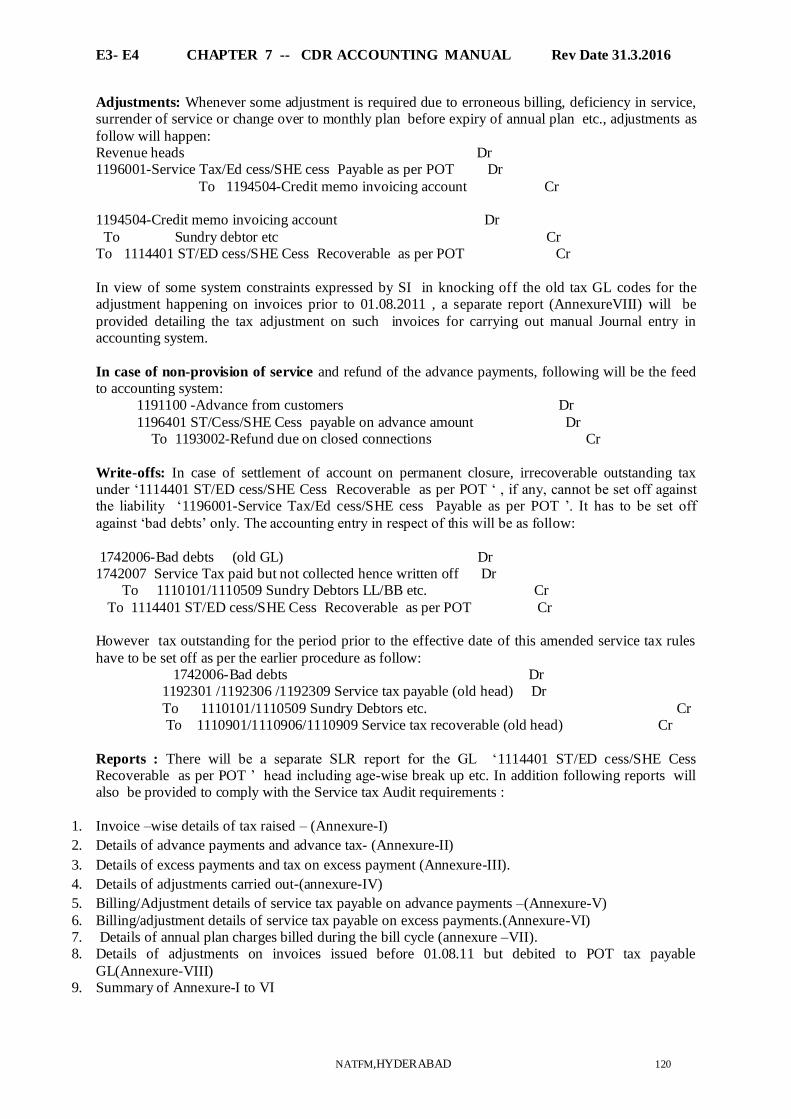

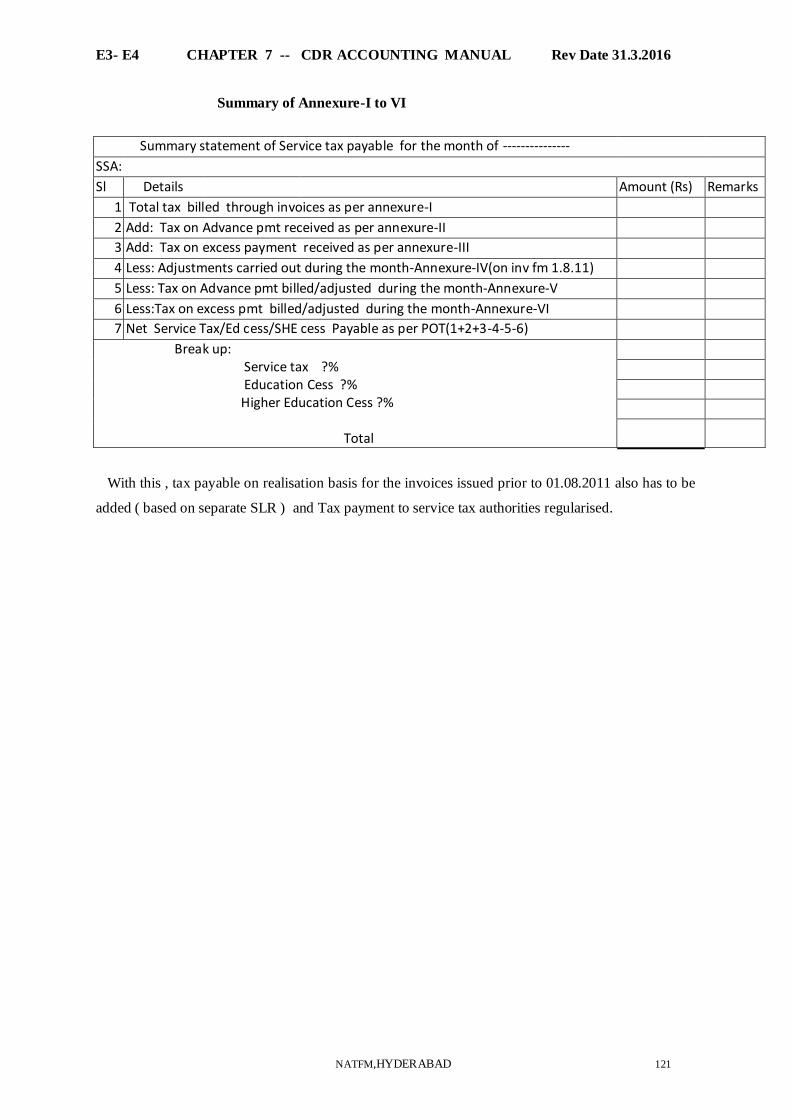

7. Adjustments 32

a. Debit Voucher b. Credit Voucher 34 c. Cancellation of Invoice 36

d. Write off of Bad Debts 36 e. Collection against Write off 37

8. Payments from Various Channels 38 a. Payments on CSR counter 38 b. Payments from Post Offices 39

c. Payments from Banks 40 d. Payments through ECS 42

e. Payments through Bill-desk f. Payments involving units outside the CDR system(ERU) 44

9. Cheque Dishonour Scenario 49

10. Missing Daily Lists Scenario (Unadjusted Credits) 53 11. Reconciliation of channel payments 54 12. Accounting for sale of Pre-paid Cards/Modem through PMS counters 54 13. Accounting for Advance Payments 55

14. Period End Closing Activities 56

a. Income Received in Advance 56

b. Accrued Income 57

c. Interest on Deposits 57 d. Accrued Interest on Deposit 58

15. Refund 61 16. Accounting treatment for OYT rebate in CDR System 63 17. Implementing Bundled PC EMI solution in the CDR system 64

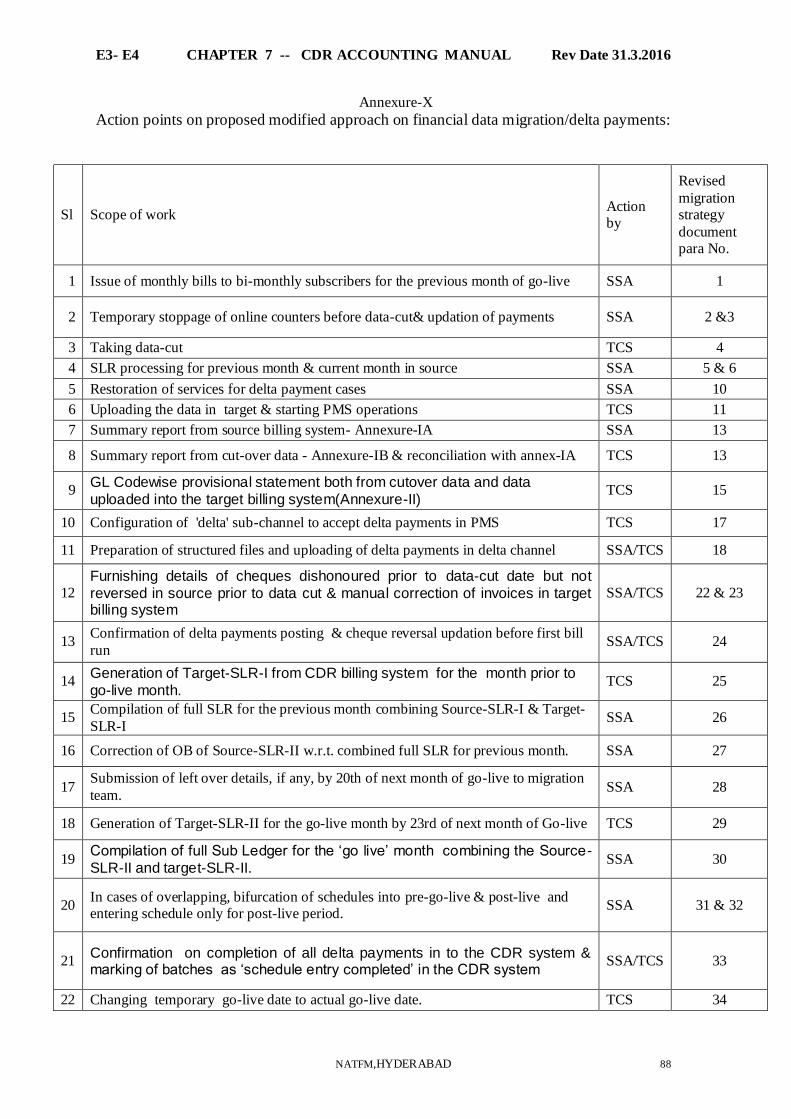

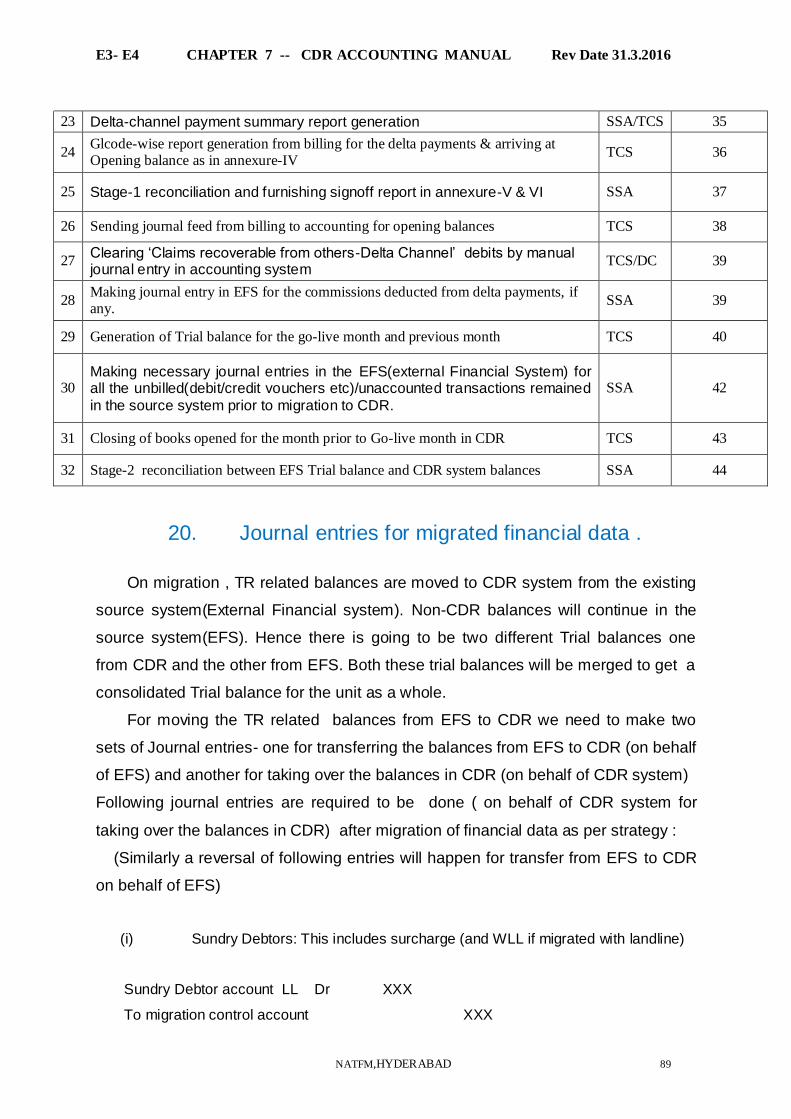

18. Migration Strategy 66 19. Revised Strategy for Financial data/Delta payment Migration 69 20. Journal entries for migrated financial data 89

21. Handling third party vendor payments collected through CDR invoices 96 22. Accounting for Zonal Electronic Stapling(ES) 99 23. Handling of ES discount in CDR Accounting 104

24. Account Settlement procedure 105 25. Accounting module-Oracle applications-Operation guidance 108 26. Accounting for amended Service Tax Rules -Point of Taxation 113

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 2

List of Figures Page No.

Figure 1: Process flow for Accounting 3

Figure 2: Billing and complete payment in the same SSA 15

Figure 3: Excess or double payment in the same SSA 16

Figure 4: Excess or Double Payment Adjustment in the next invoice 18

Figure 5: Refund of Excess or Double Payment 19

Figure 6: Refund for closed/surrendered connections 19

Figure 7: Partial payment made in billing SSA 20

Figure 8: Partial Payment adjustment in next cycle 21

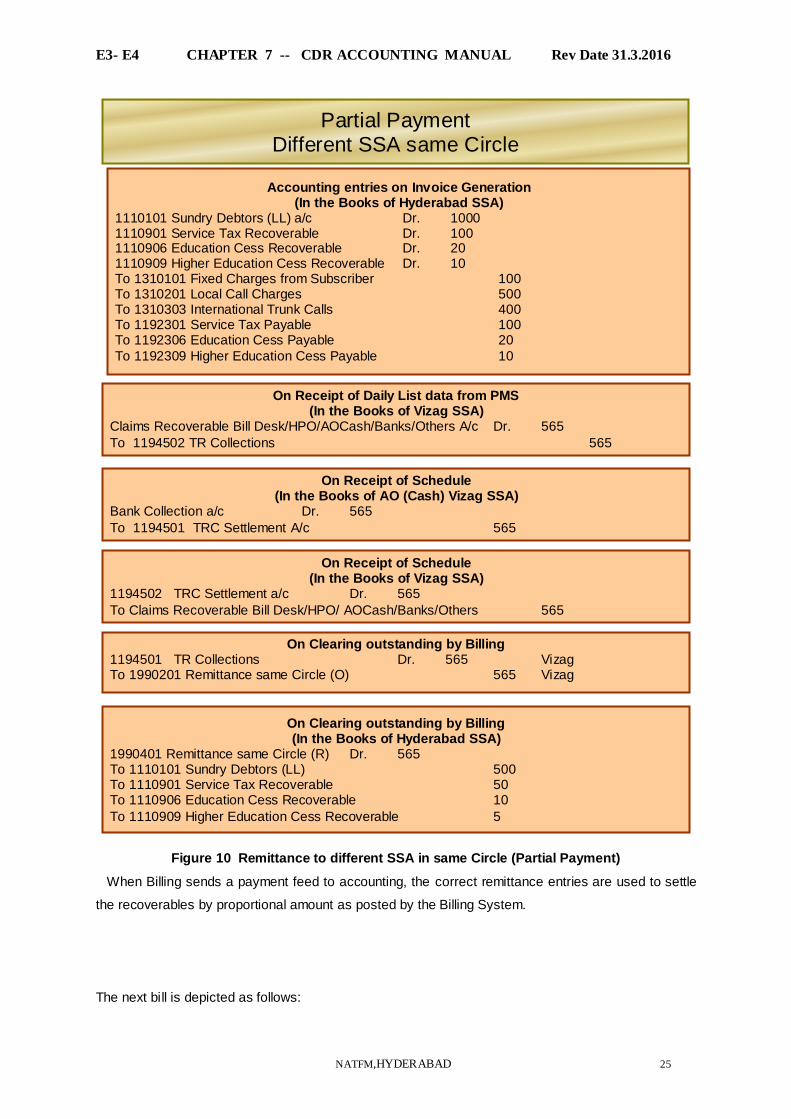

Figure 9: Remittance to different SSA in same circle 23

Figure 10: Remittance to different SSA in same Circle (Partial Payment) 25

Figure 11: Remittance to different SSA in same Circle

(Partial Payment Adjustment) 27

Figure 12: Remittance to different SSA in same circle (excess payment) 28

Figure 13: Remittance to an SSA in different circle (full payment) 29

Figure 14: Surcharge on delayed payments(Late fee) 30

Figure 15: Accounting for GSM Collections: Payment in SSA of same Circle 30

Figure 16: Accounting for GSM Collections: Payment in SSA of diff. Circle 31

Figure 17: Debit Voucher: Settlement of short billed invoice 33

Figure 18: Accounting for debit voucher (Settlement of short billed invoice)

on generation of next invoice 34

Figure 19: Accounting for Credit Voucher where the bill is fully settled 35

Figure 20: Accounting for Credit Voucher on Gen eration of new Invoice 36

Figure 21: Accounting for Write Off of Bad Debts 37

Figure 22: Accounting Entry on Billing 38

Figure 23: Accounting entry on receipt of daily list 38

Figure 24: Accounting entry on receipt of TRC Schedule and Cheque 38 Figure 25: Accounting entry on receipt of daily list from Head Post Office 39

Figure 26: Accounting entry on receipt of TRC Schedule, Cheque from HPO 40 Figure 27: Accounting entry on receipt of payment information from Billing 40

Figure 28: Accounting treatment for Discount on ECS 41

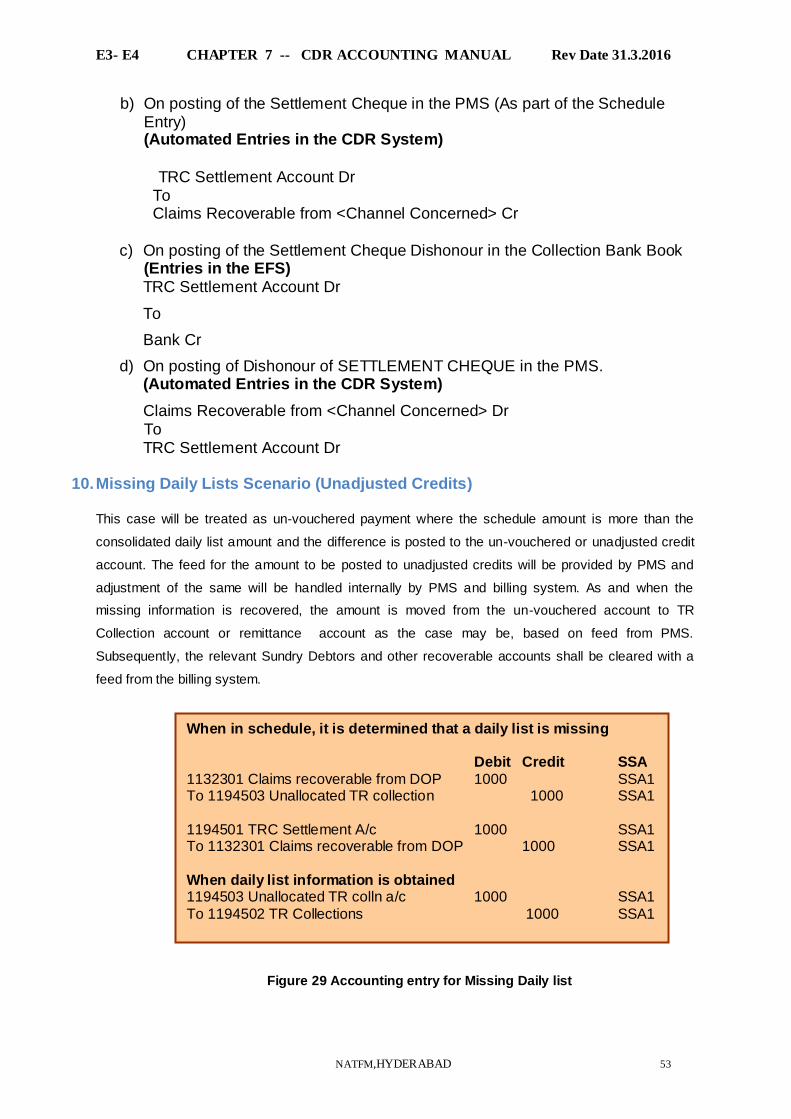

Figure 29: Accounting entry for Missing Daily list 53

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 3

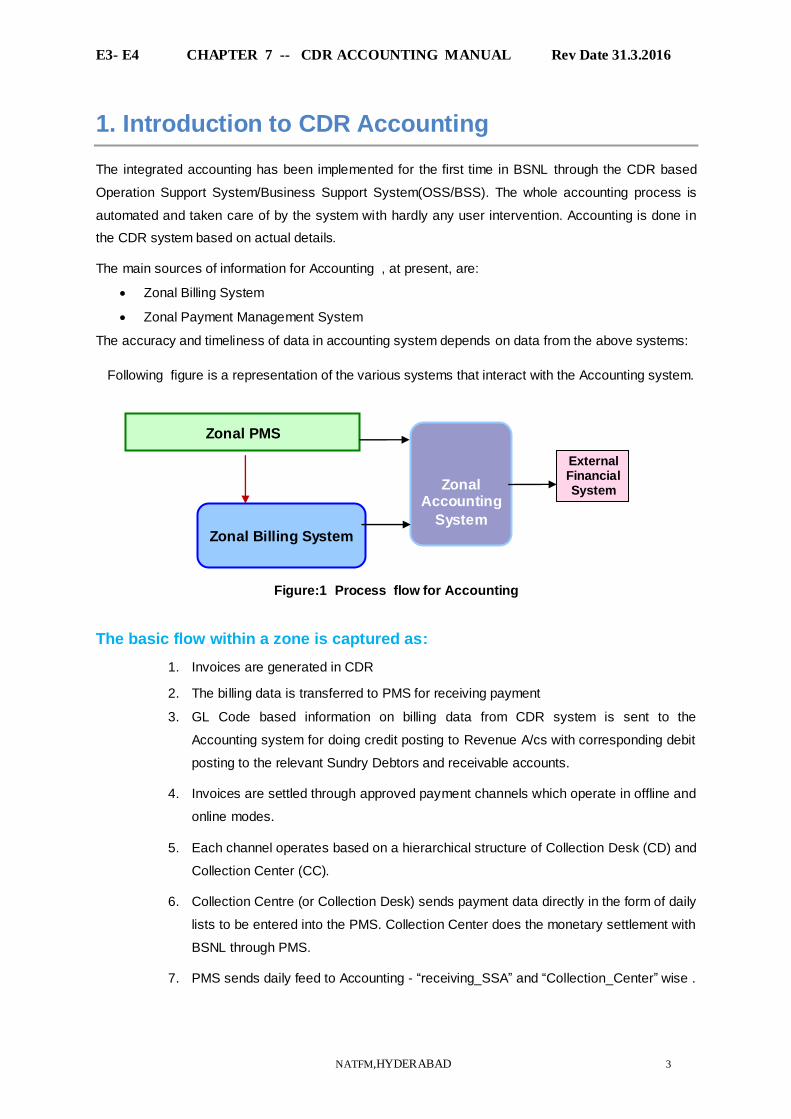

1. Introduction to CDR Accounting

The integrated accounting has been implemented for the first time in BSNL through the CDR based

Operation Support System/Business Support System(OSS/BSS). The whole accounting process is

automated and taken care of by the system with hardly any user intervention. Accounting is done in

the CDR system based on actual details.

The main sources of information for Accounting , at present, are:

Zonal Billing System

Zonal Payment Management System

The accuracy and timeliness of data in accounting system depends on data from the above systems:

Following figure is a representation of the various systems that interact with the Accounting system.

Figure:1 Process flow for Accounting

The basic flow within a zone is captured as:

1. Invoices are generated in CDR

2. The billing data is transferred to PMS for receiving payment

3. GL Code based information on billing data from CDR system is sent to the

Accounting system for doing credit posting to Revenue A/cs with corresponding debit

posting to the relevant Sundry Debtors and receivable accounts.

4. Invoices are settled through approved payment channels which operate in offline and

online modes.

5. Each channel operates based on a hierarchical structure of Collection Desk (CD) and

Collection Center (CC).

6. Collection Centre (or Collection Desk) sends payment data directly in the form of daily

lists to be entered into the PMS. Collection Center does the monetary settlement with

BSNL through PMS.

7. PMS sends daily feed to Accounting - “receiving_SSA” and “Collection_Center” wise .

Zonal PMS

Zonal Billing System

Zonal

Accounting

System

External Financial System

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 4

Based on this ,the Accounting will debit to one of the following accounts:

(i) Claims Recoverable from DoP

(ii) Claims Recoverable from WSC

(iii) Claims Recoverable from Banks

(iv) Claims recoverable from AO (Cash)

(v) Claims recoverable from State Govt IT(E-seva)

(vi) Claims recoverable from EAU(Portal)

(vii) Claims Recoverable from Others etc.

with corresponding credit to “CDR TR Collections account”.

Money from the Collection Center will be received at the prescribed frequency and managed

by AO Cash simultaneously.

8. When money received is entered into the PMS (based on Schedule) and the

information transferred to the accounting system the entry will be to Credit „collection

center (Claims Recoverable from HPO/Banks/AO Cash/Others/Bill Desk etc)‟ and

Debit „TRC Settlement account’ operated within the CDR accounting system

9. PMS sends collection information to the home billing system in the form of lockbox

files in the required format.

10. When CDR billing system does the posting of these payments, it sends the GL Code

based payment information to the accounting system. Accounting system does the

posting of this by debiting „TR Collection Account „ and crediting the relevant „Sundry

Debtors and relevant Tax Recoverable heads ‟ created based on billing data.

Relevant Remittance Accounts will be used in case Receiving and Owning SSA are different

and also when collections belong to external systems like GSM.

2.Accounting Scope

The objective of CDR Accounting is to implement accrual accounting at a consolidated level.

Scope for Accounting:

o Landline and Broadband: Revenue accounting

o GSM: Payment to be collected by zonal PMS, Remittance to be passed to GSM at

circle level.

o Leased Circuits: Payment to be collected by zonal PMS and accounting to be carried

out in EFS (External Financial System) with necessary Journal entry.

o Revenue accounting is to be done based on the feeds from PMS & CDR Billing only

and no other interface is in the scope of accounting at present.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 5

o Accounting system can confirm the consolidated amount received at SSA level and

not at individual transaction level. Reconciliation with individual customer account

(which is maintained at Billing system) is not in accounting scope as only

consolidated entries are done based on feed received from other systems and break

up of these entries are available in the base systems (for payments in PMS and for

cleared and outstanding amount in Billing system). Reconciliation shall be carried out

manually by comparing the accounting output of GL extract and a report from Billing

system.

o Debtors are maintained at consolidated level in Accounting and individual customer

accounts are maintained in relevant billing systems.

o Debtors control account is based on service types eg. Landline and Broadband.

Reporting scope (feed for External Financial System)

o GL Extract (SSA Level; for all accounts in the system)

o Trial Balance (SSA Level)

In the existing system of accounting where SSA is the basic accounting unit, any financial

transaction done by one SSA that affects the accounts of another SSA will be settled

through the operation of “Remittance” heads. The idea of maintaining these heads is that

while no physical exchange of money will take place, the impact of the transaction will be

incorporated into the books of accounts of the SSAs involved. For this purpose, the

following Remittance heads are used

o Remittance same circle (O) and (R)

o Remittance between circles <Circle name> (O) and (R)

Further Remittance heads are used for parking payments received by PMS related to

invoices generated by GSM etc.

Fiscal Year:

o Fiscal year shall be from 1st April to 31st March.

Currency:

o Reporting currency needs to be INR.

o Billing currency for retail customers has to be INR.

It is necessary to keep the accounts of each month open for a sufficient period in the next

month to ensure that all the transactions are entered into the system. In the existing

systems the TR Accounts for the previous month are open until the 25th of the next

month ie upto generation of SLR reports . In the CDR system also it is proposed to close

the accounts by 15th of next month from now onwards.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 6

3. Process Flow

With reference to Figure 1:

Flow from Billing to Accounting:

o Information required Per Billing Cycle:

GL Code wise billed amount of revenue/adjustments for revenue owning

SSAs in each circle, consolidated SSA wise.

Discounts: As they will be adjusted against amount outstanding as a part of

invoice information, posting in accounting to be done GL Code wise like

normal revenue items during bill cycle run with additional line item in invoice.

Excess/Double Payments: For all SSAs in each circle when adjusted in

subsequent invoice. Accounting will capture this as an additional line item

based on the consolidated GL code wise feed received from Billing system.

Adjustment entries for deposits and interest on deposit will be passed based

on the consolidated feed from billing system. The logic for interest and

principal amount break up is to be maintained at billing system level.

Refunds: As and when refund of deposit is due, refund of double/excess

payment and refund on closed/surrendered connections

Either as an adjustment in next invoice

Or refund is given in the form of a cheque

o Information required Daily

Clearing information in order to clear amount outstanding including both

revenue receiving and revenue owning SSA, consolidated based on Owning

and Receiving SSA is received from Billing at end of day.

Adjustments

Debit Voucher information for all SSAs in each circle.

Credit Voucher information for all SSAs in each circle.

Consolidated feed for Interest on deposit for all SSAs in each circle based on

type of deposit to be posted for provisioned connections based on GL Codes.

o Write-offs:

Write offs are manually done in Billing and posted to Accounting on periodic

basis.

Reversal of write-offs not supported

Collections against write-off, if any, will go to „Other Income‟. Posting to be

done by PMS to Accounting.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 7

o At year end, consolidated feed for Interest accrued on interest bearing deposits for all

SSAs in each circle based on type of deposit to be posted for unprovisioned new

connections(prospects) and additional services for existing customers.

o At end of financial year or quarterly as desired, feed file on Accrued Income: Unbilled

revenue items (Earned but not billed) grouped SSA wise upto last day of every

month.

o At end of financial year or quarterly as desired, feed file on Advance Income: eg. Rent

(Billed but unearned) grouped SSA wise, revenue unearned and unbilled grouped

SSA wise

Flow from Payment Management System to Accounting:

o Daily Basis

Payment information combined SSA wise:

Revenue Receiving SSA

Revenue Owning SSA

Collection Centre: Details of payment received from Head Post

offices, Banks, AOCash, Bill Desk etc.

Information about the bounced cheques both Retail cheques and settlement

cheques

Deposit information

For all SSAs in each circle, payment received in the form of deposits.

This information need not be identified as deposits. This identification

will be done by the Billing system

o Periodic Basis (mainly by AO Cash)

Information when schedule is received for Billing System

Consolidated information on amount received.

Collection centre (HPO, Bill Desk etc)

Revenue Receiving SSA

Flow from Accounting to External Financial System

o At period closing, a report containing GL Balances will be generated containing GL

Code, GL Account name, Closing Balance, SSA, Circle.

o An SSA wise trial balance will be obtained.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 8

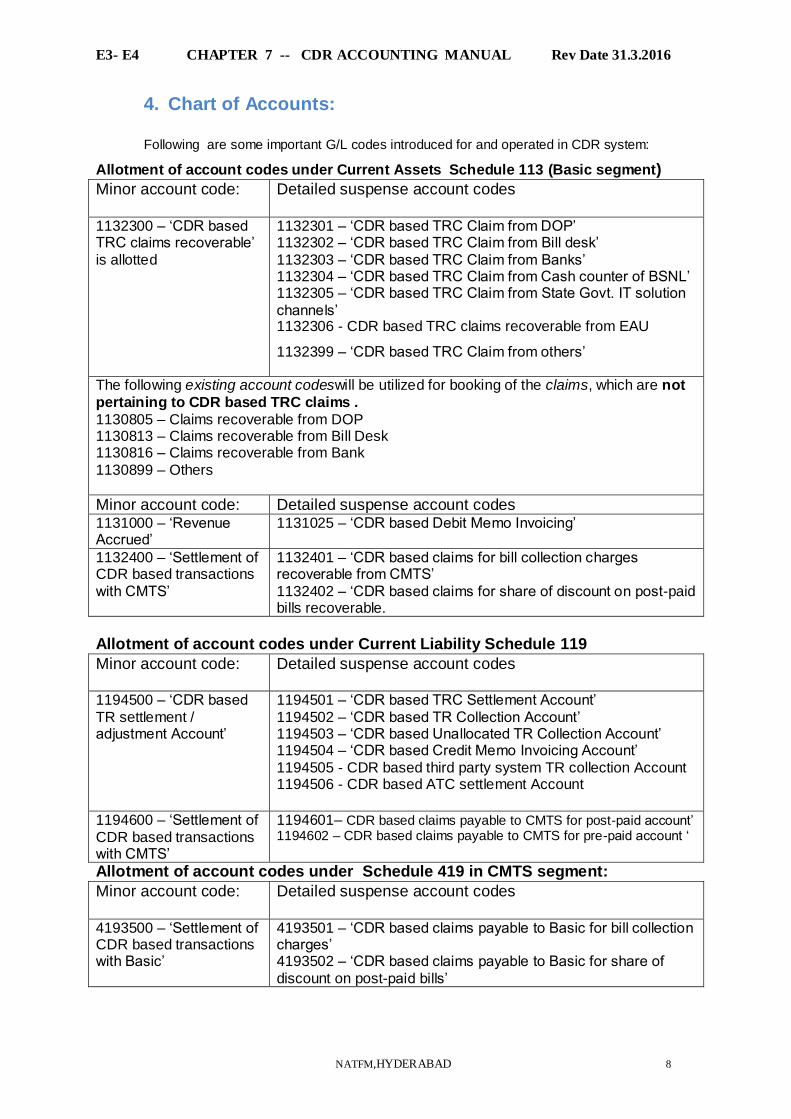

4. Chart of Accounts:

Following are some important G/L codes introduced for and operated in CDR system:

Allotment of account codes under Current Assets Schedule 113 (Basic segment)

Minor account code:

Detailed suspense account codes

1132300 – „CDR based TRC claims recoverable‟

is allotted

1132301 – „CDR based TRC Claim from DOP‟ 1132302 – „CDR based TRC Claim from Bill desk‟

1132303 – „CDR based TRC Claim from Banks‟ 1132304 – „CDR based TRC Claim from Cash counter of BSNL‟ 1132305 – „CDR based TRC Claim from State Govt. IT solution

channels‟ 1132306 - CDR based TRC claims recoverable from EAU

1132399 – „CDR based TRC Claim from others‟

The following existing account codeswill be utilized for booking of the claims, which are not

pertaining to CDR based TRC claims .

1130805 – Claims recoverable from DOP 1130813 – Claims recoverable from Bill Desk 1130816 – Claims recoverable from Bank

1130899 – Others

Minor account code: Detailed suspense account codes 1131000 – „Revenue Accrued‟

1131025 – „CDR based Debit Memo Invoicing‟

1132400 – „Settlement of CDR based transactions

with CMTS‟

1132401 – „CDR based claims for bill collection charges recoverable from CMTS‟

1132402 – „CDR based claims for share of discount on post-paid bills recoverable.

Allotment of account codes under Current Liability Schedule 119

Minor account code:

Detailed suspense account codes

1194500 – „CDR based

TR settlement / adjustment Account‟

1194501 – „CDR based TRC Settlement Account‟

1194502 – „CDR based TR Collection Account‟ 1194503 – „CDR based Unallocated TR Collection Account‟ 1194504 – „CDR based Credit Memo Invoicing Account‟

1194505 - CDR based third party system TR collection Account 1194506 - CDR based ATC settlement Account

1194600 – „Settlement of

CDR based transactions with CMTS‟

1194601– CDR based claims payable to CMTS for post-paid account‟ 1194602 – CDR based claims payable to CMTS for pre-paid account „

Allotment of account codes under Schedule 419 in CMTS segment:

Minor account code:

Detailed suspense account codes

4193500 – „Settlement of CDR based transactions with Basic‟

4193501 – „CDR based claims payable to Basic for bill collection charges‟ 4193502 – „CDR based claims payable to Basic for share of

discount on post-paid bills‟

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 9

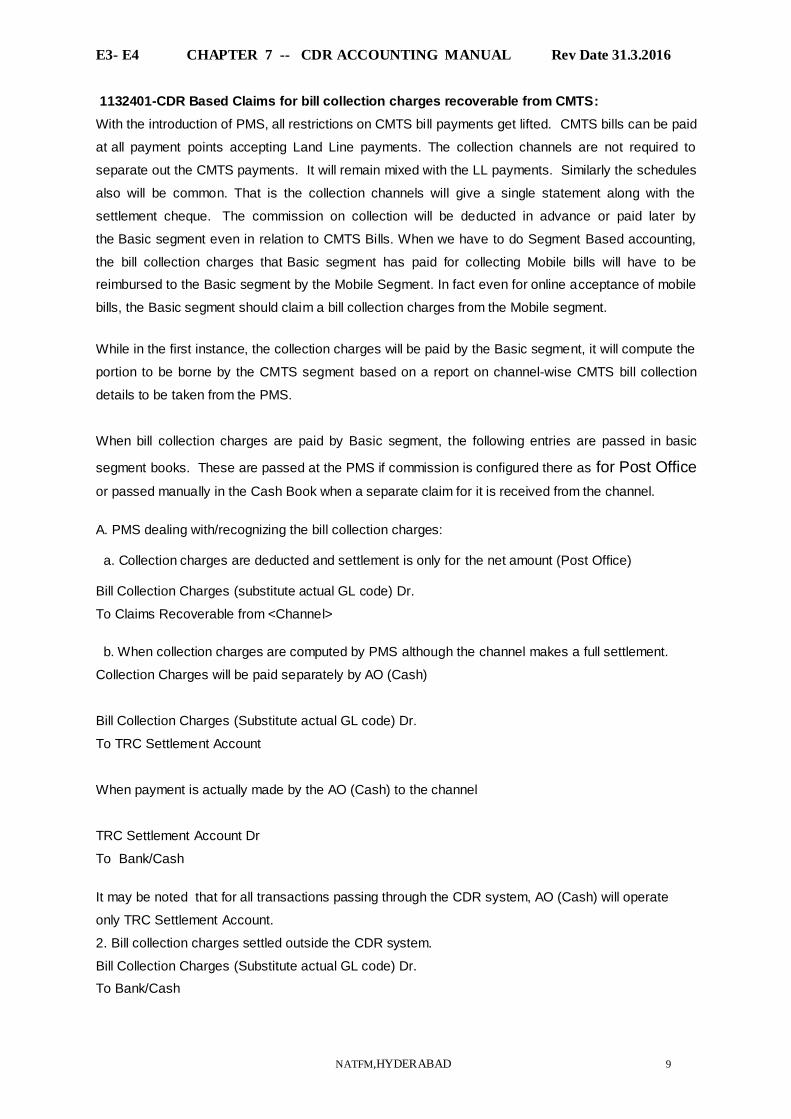

1132401-CDR Based Claims for bill collection charges recoverable from CMTS:

With the introduction of PMS, all restrictions on CMTS bill payments get lifted. CMTS bills can be paid

at all payment points accepting Land Line payments. The collection channels are not required to

separate out the CMTS payments. It will remain mixed with the LL payments. Similarly the schedules

also will be common. That is the collection channels will give a single statement along with the

settlement cheque. The commission on collection will be deducted in advance or paid later by

the Basic segment even in relation to CMTS Bills. When we have to do Segment Based accounting,

the bill collection charges that Basic segment has paid for collecting Mobile bills will have to be

reimbursed to the Basic segment by the Mobile Segment. In fact even for online acceptance of mobile

bills, the Basic segment should claim a bill collection charges from the Mobile segment.

While in the first instance, the collection charges will be paid by the Basic segment, it will compute the

portion to be borne by the CMTS segment based on a report on channel-wise CMTS bill collection

details to be taken from the PMS.

When bill collection charges are paid by Basic segment, the following entries are passed in basic

segment books. These are passed at the PMS if commission is configured there as for Post Office

or passed manually in the Cash Book when a separate claim for it is received from the channel.

A. PMS dealing with/recognizing the bill collection charges: a. Collection charges are deducted and settlement is only for the net amount (Post Office) Bill Collection Charges (substitute actual GL code) Dr.

To Claims Recoverable from <Channel>

b. When collection charges are computed by PMS although the channel makes a full settlement.

Collection Charges will be paid separately by AO (Cash)

Bill Collection Charges (Substitute actual GL code) Dr.

To TRC Settlement Account

When payment is actually made by the AO (Cash) to the channel

TRC Settlement Account Dr

To Bank/Cash

It may be noted that for all transactions passing through the CDR system, AO (Cash) will operate

only TRC Settlement Account.

2. Bill collection charges settled outside the CDR system.

Bill Collection Charges (Substitute actual GL code) Dr.

To Bank/Cash

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 10

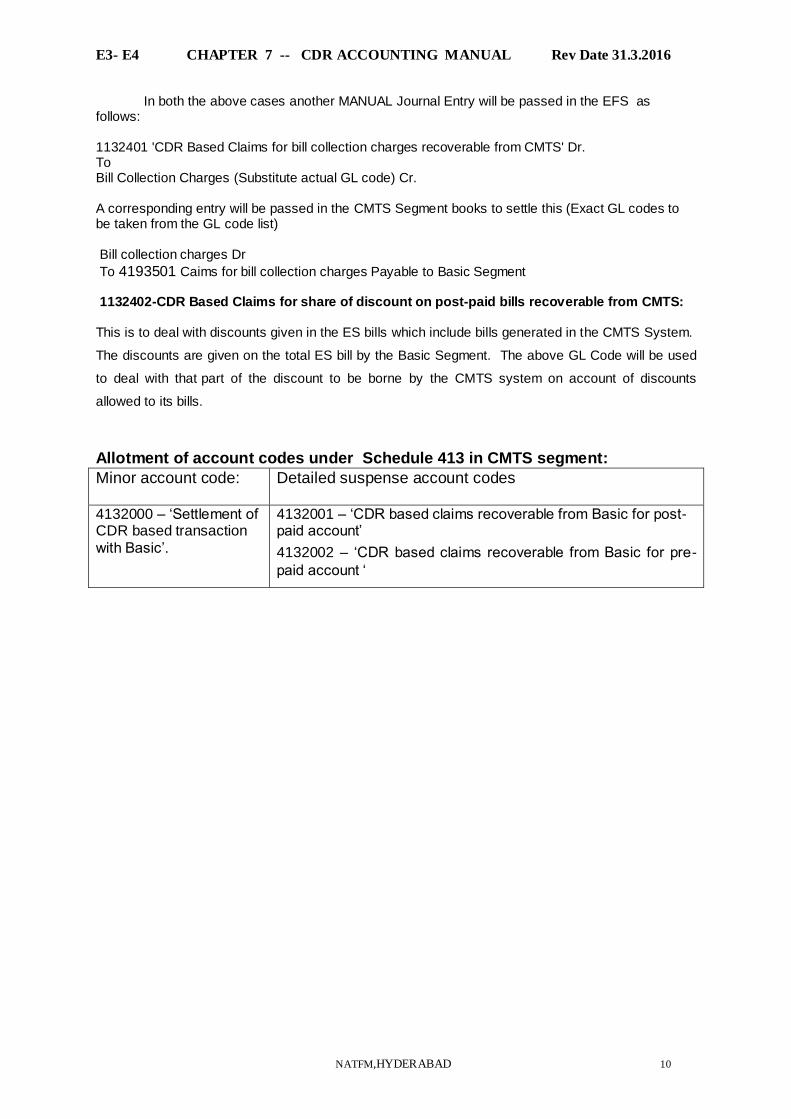

In both the above cases another MANUAL Journal Entry will be passed in the EFS as follows: 1132401 'CDR Based Claims for bill collection charges recoverable from CMTS' Dr. To Bill Collection Charges (Substitute actual GL code) Cr. A corresponding entry will be passed in the CMTS Segment books to settle this (Exact GL codes to be taken from the GL code list) Bill collection charges Dr

To 4193501 Caims for bill collection charges Payable to Basic Segment 1132402-CDR Based Claims for share of discount on post-paid bills recoverable from CMTS: This is to deal with discounts given in the ES bills which include bills generated in the CMTS System.

The discounts are given on the total ES bill by the Basic Segment. The above GL Code will be used

to deal with that part of the discount to be borne by the CMTS system on account of discounts

allowed to its bills.

Allotment of account codes under Schedule 413 in CMTS segment:

Minor account code:

Detailed suspense account codes

4132000 – „Settlement of CDR based transaction

with Basic‟.

4132001 – „CDR based claims recoverable from Basic for post-paid account‟

4132002 – „CDR based claims recoverable from Basic for pre-

paid account „

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 11

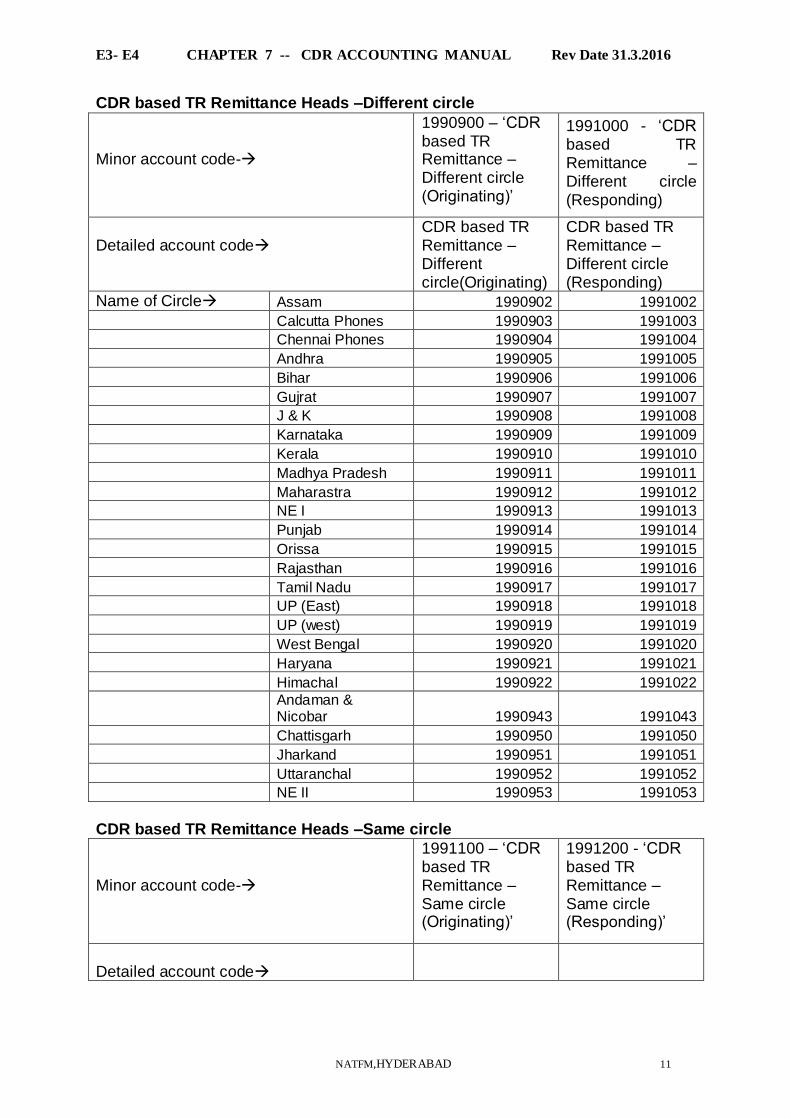

CDR based TR Remittance Heads –Different circle

Minor account code-

1990900 – „CDR based TR Remittance – Different circle (Originating)‟

1991000 - „CDR based TR Remittance – Different circle (Responding)

Detailed account code

CDR based TR Remittance – Different circle(Originating)

CDR based TR Remittance – Different circle (Responding)

Name of Circle Assam 1990902 1991002

Calcutta Phones 1990903 1991003

Chennai Phones 1990904 1991004

Andhra 1990905 1991005

Bihar 1990906 1991006

Gujrat 1990907 1991007

J & K 1990908 1991008

Karnataka 1990909 1991009

Kerala 1990910 1991010

Madhya Pradesh 1990911 1991011

Maharastra 1990912 1991012

NE I 1990913 1991013

Punjab 1990914 1991014

Orissa 1990915 1991015

Rajasthan 1990916 1991016

Tamil Nadu 1990917 1991017

UP (East) 1990918 1991018

UP (west) 1990919 1991019

West Bengal 1990920 1991020

Haryana 1990921 1991021

Himachal 1990922 1991022

Andaman & Nicobar 1990943 1991043

Chattisgarh 1990950 1991050

Jharkand 1990951 1991051

Uttaranchal 1990952 1991052

NE II 1990953 1991053

CDR based TR Remittance Heads –Same circle

Minor account code-

1991100 – „CDR based TR Remittance – Same circle (Originating)‟

1991200 - „CDR based TR Remittance – Same circle (Responding)‟

Detailed account code

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 12

Above remittance heads must not be utilized by any Circle for book transfer of any kind of inter-circle

and intra-circle transactions other than those for TR transactions (revenue and expense) exclusively

generated by CDR based billing system.

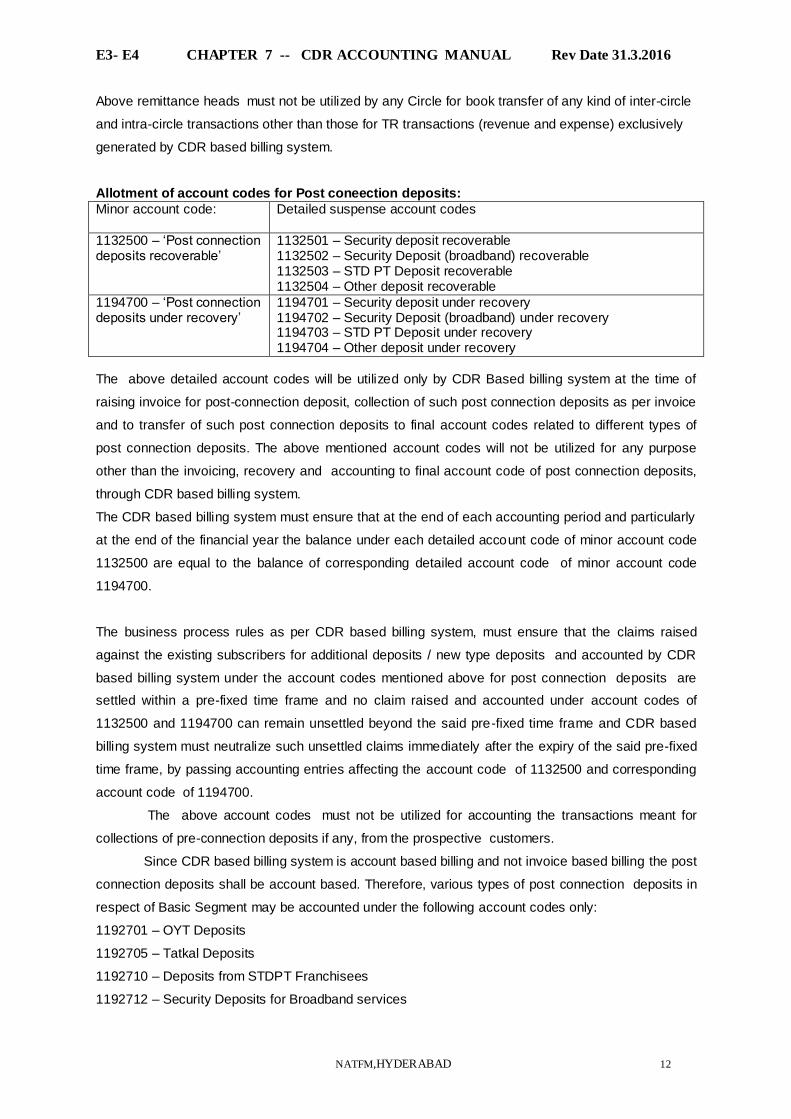

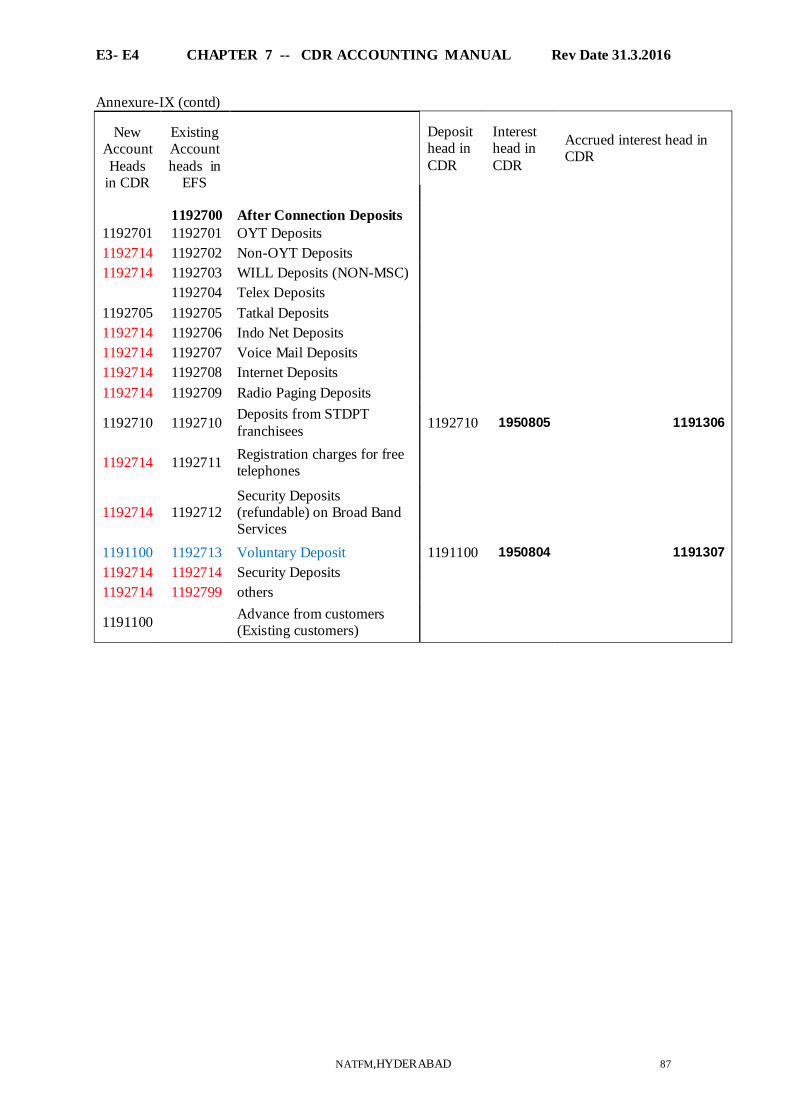

Allotment of account codes for Post coneection deposits:

Minor account code:

Detailed suspense account codes

1132500 – „Post connection deposits recoverable‟

1132501 – Security deposit recoverable 1132502 – Security Deposit (broadband) recoverable 1132503 – STD PT Deposit recoverable 1132504 – Other deposit recoverable

1194700 – „Post connection deposits under recovery‟

1194701 – Security deposit under recovery 1194702 – Security Deposit (broadband) under recovery 1194703 – STD PT Deposit under recovery 1194704 – Other deposit under recovery

The above detailed account codes will be utilized only by CDR Based billing system at the time of

raising invoice for post-connection deposit, collection of such post connection deposits as per invoice

and to transfer of such post connection deposits to final account codes related to different types of

post connection deposits. The above mentioned account codes will not be utilized for any purpose

other than the invoicing, recovery and accounting to final account code of post connection deposits,

through CDR based billing system.

The CDR based billing system must ensure that at the end of each accounting period and particularly

at the end of the financial year the balance under each detailed account code of minor account code

1132500 are equal to the balance of corresponding detailed account code of minor account code

1194700.

The business process rules as per CDR based billing system, must ensure that the claims raised

against the existing subscribers for additional deposits / new type deposits and accounted by CDR

based billing system under the account codes mentioned above for post connection deposits are

settled within a pre-fixed time frame and no claim raised and accounted under account codes of

1132500 and 1194700 can remain unsettled beyond the said pre-fixed time frame and CDR based

billing system must neutralize such unsettled claims immediately after the expiry of the said pre-fixed

time frame, by passing accounting entries affecting the account code of 1132500 and corresponding

account code of 1194700.

The above account codes must not be utilized for accounting the transactions meant for

collections of pre-connection deposits if any, from the prospective customers.

Since CDR based billing system is account based billing and not invoice based billing the post

connection deposits shall be account based. Therefore, various types of post connection deposits in

respect of Basic Segment may be accounted under the following account codes only:

1192701 – OYT Deposits

1192705 – Tatkal Deposits

1192710 – Deposits from STDPT Franchisees

1192712 – Security Deposits for Broadband services

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 13

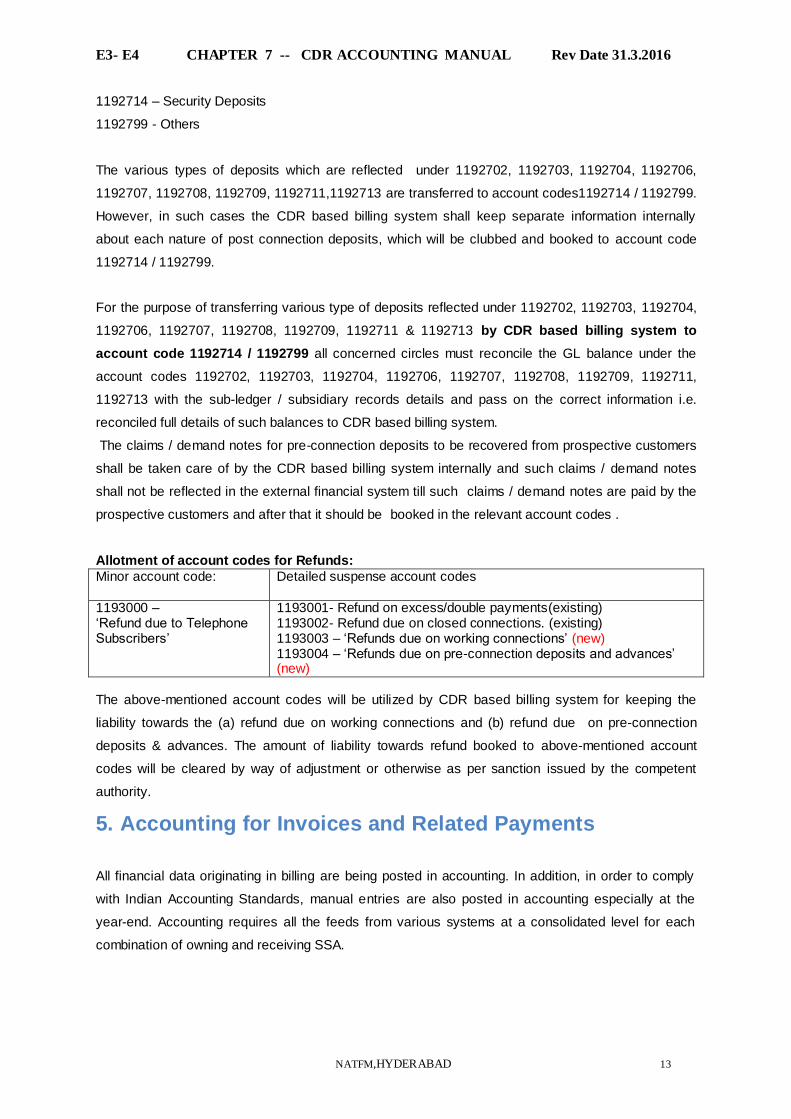

1192714 – Security Deposits

1192799 - Others

The various types of deposits which are reflected under 1192702, 1192703, 1192704, 1192706,

1192707, 1192708, 1192709, 1192711,1192713 are transferred to account codes1192714 / 1192799.

However, in such cases the CDR based billing system shall keep separate information internally

about each nature of post connection deposits, which will be clubbed and booked to account code

1192714 / 1192799.

For the purpose of transferring various type of deposits reflected under 1192702, 1192703, 1192704,

1192706, 1192707, 1192708, 1192709, 1192711 & 1192713 by CDR based billing system to

account code 1192714 / 1192799 all concerned circles must reconcile the GL balance under the

account codes 1192702, 1192703, 1192704, 1192706, 1192707, 1192708, 1192709, 1192711,

1192713 with the sub-ledger / subsidiary records details and pass on the correct information i.e.

reconciled full details of such balances to CDR based billing system.

The claims / demand notes for pre-connection deposits to be recovered from prospective customers

shall be taken care of by the CDR based billing system internally and such claims / demand notes

shall not be reflected in the external financial system till such claims / demand notes are paid by the

prospective customers and after that it should be booked in the relevant account codes .

Allotment of account codes for Refunds:

Minor account code:

Detailed suspense account codes

1193000 – „Refund due to Telephone Subscribers‟

1193001- Refund on excess/double payments(existing) 1193002- Refund due on closed connections. (existing) 1193003 – „Refunds due on working connections‟ (new) 1193004 – „Refunds due on pre-connection deposits and advances‟ (new)

The above-mentioned account codes will be utilized by CDR based billing system for keeping the

liability towards the (a) refund due on working connections and (b) refund due on pre-connection

deposits & advances. The amount of liability towards refund booked to above-mentioned account

codes will be cleared by way of adjustment or otherwise as per sanction issued by the competent

authority.

5. Accounting for Invoices and Related Payments

All financial data originating in billing are being posted in accounting. In addition, in order to comply

with Indian Accounting Standards, manual entries are also posted in accounting especially at the

year-end. Accounting requires all the feeds from various systems at a consolidated level for each

combination of owning and receiving SSA.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 14

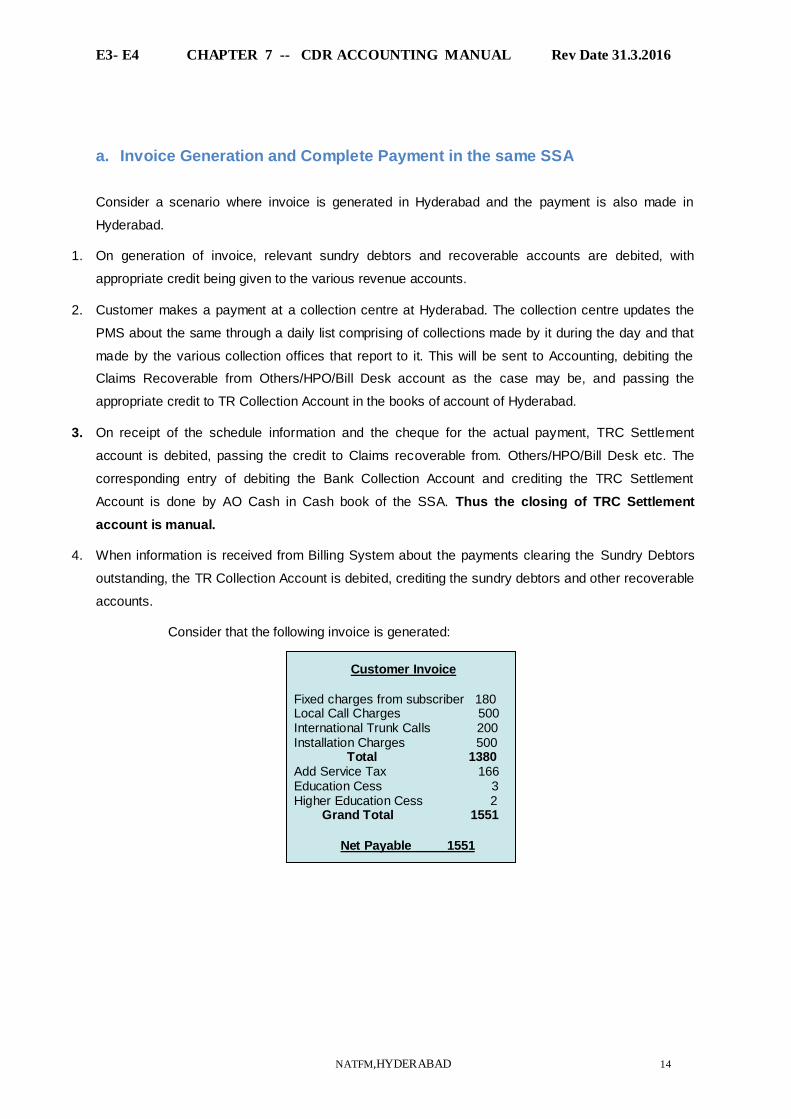

a. Invoice Generation and Complete Payment in the same SSA

Consider a scenario where invoice is generated in Hyderabad and the payment is also made in

Hyderabad.

1. On generation of invoice, relevant sundry debtors and recoverable accounts are debited, with

appropriate credit being given to the various revenue accounts.

2. Customer makes a payment at a collection centre at Hyderabad. The collection centre updates the

PMS about the same through a daily list comprising of collections made by it during the day and that

made by the various collection offices that report to it. This will be sent to Accounting, debiting the

Claims Recoverable from Others/HPO/Bill Desk account as the case may be, and passing the

appropriate credit to TR Collection Account in the books of account of Hyderabad.

3. On receipt of the schedule information and the cheque for the actual payment, TRC Settlement

account is debited, passing the credit to Claims recoverable from. Others/HPO/Bill Desk etc. The

corresponding entry of debiting the Bank Collection Account and crediting the TRC Settlement

Account is done by AO Cash in Cash book of the SSA. Thus the closing of TRC Settlement

account is manual.

4. When information is received from Billing System about the payments clearing the Sundry Debtors

outstanding, the TR Collection Account is debited, crediting the sundry debtors and other recoverable

accounts.

Consider that the following invoice is generated:

Customer Invoice

Fixed charges from subscriber 180 Local Call Charges 500 International Trunk Calls 200 Installation Charges 500 Total 1380 Add Service Tax 166 Education Cess 3 Higher Education Cess 2 Grand Total 1551

Net Payable 1551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 15

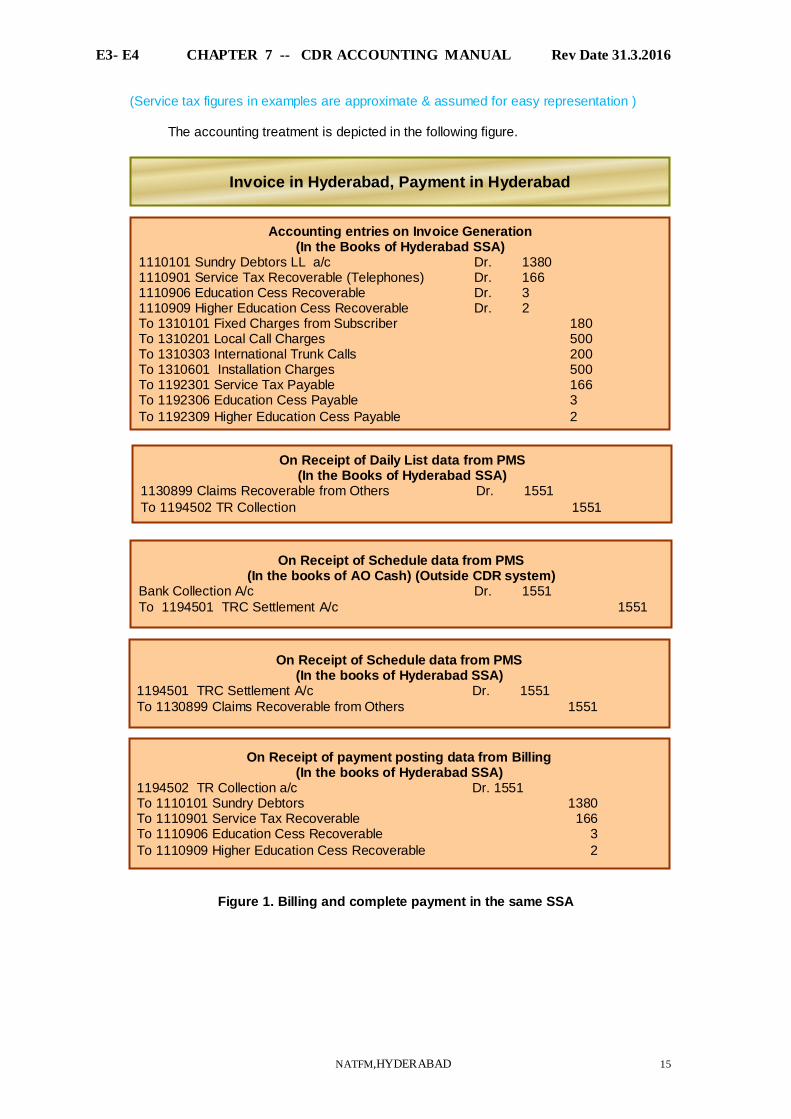

(Service tax figures in examples are approximate & assumed for easy representation )

The accounting treatment is depicted in the following figure.

Figure 1. Billing and complete payment in the same SSA

On Receipt of payment posting data from Billing (In the books of Hyderabad SSA)

1194502 TR Collection a/c Dr. 1551 To 1110101 Sundry Debtors 1380 To 1110901 Service Tax Recoverable 166 To 1110906 Education Cess Recoverable 3

To 1110909 Higher Education Cess Recoverable 2

On Receipt of Schedule data from PMS (In the books of Hyderabad SSA)

1194501 TRC Settlement A/c Dr. 1551

To 1130899 Claims Recoverable from Others 1551

On Receipt of Daily List data from PMS (In the Books of Hyderabad SSA)

1130899 Claims Recoverable from Others Dr. 1551

To 1194502 TR Collection 1551

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors LL a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To 1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3

To 1192309 Higher Education Cess Payable 2

Invoice in Hyderabad, Payment in Hyderabad

On Receipt of Schedule data from PMS (In the books of AO Cash) (Outside CDR system)

Bank Collection A/c Dr. 1551

To 1194501 TRC Settlement A/c 1551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 16

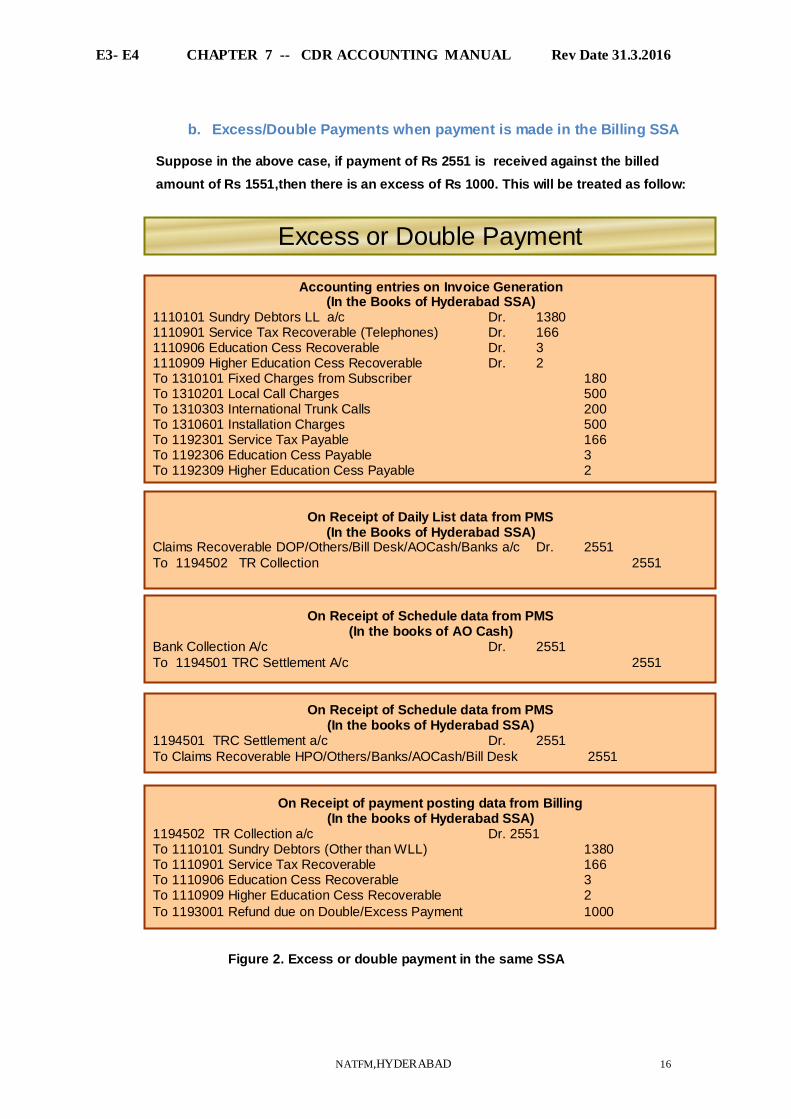

b. Excess/Double Payments when payment is made in the Billing SSA

Suppose in the above case, if payment of Rs 2551 is received against the billed

amount of Rs 1551,then there is an excess of Rs 1000. This will be treated as follow:

Figure 2. Excess or double payment in the same SSA

On Receipt of payment posting data from Billing (In the books of Hyderabad SSA)

1194502 TR Collection a/c Dr. 2551 To 1110101 Sundry Debtors (Other than WLL) 1380 To 1110901 Service Tax Recoverable 166 To 1110906 Education Cess Recoverable 3 To 1110909 Higher Education Cess Recoverable 2

To 1193001 Refund due on Double/Excess Payment 1000

On Receipt of Daily List data from PMS (In the Books of Hyderabad SSA)

Claims Recoverable DOP/Others/Bill Desk/AOCash/Banks a/c Dr. 2551

To 1194502 TR Collection 2551

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors LL a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To 1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3 To 1192309 Higher Education Cess Payable 2

Excess or Double Payment

On Receipt of Schedule data from PMS (In the books of Hyderabad SSA)

1194501 TRC Settlement a/c Dr. 2551

To Claims Recoverable HPO/Others/Banks/AOCash/Bill Desk 2551

On Receipt of Schedule data from PMS (In the books of AO Cash)

Bank Collection A/c Dr. 2551

To 1194501 TRC Settlement A/c 2551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 17

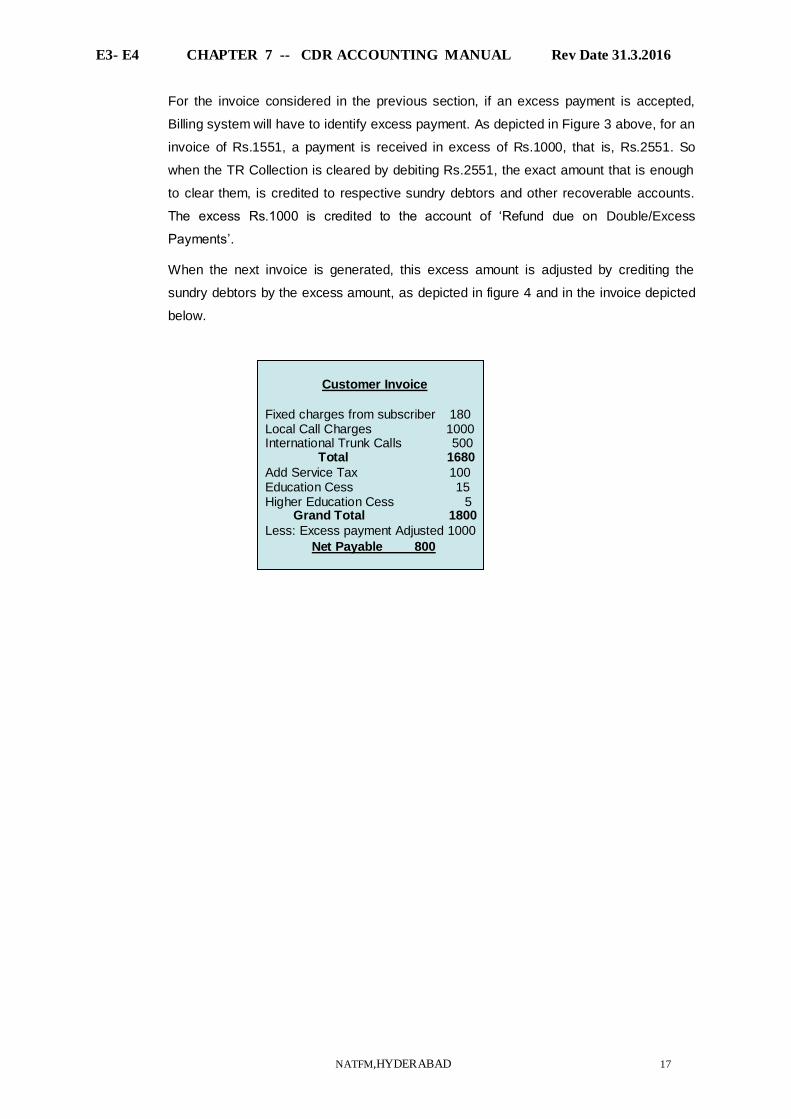

For the invoice considered in the previous section, if an excess payment is accepted,

Billing system will have to identify excess payment. As depicted in Figure 3 above, for an

invoice of Rs.1551, a payment is received in excess of Rs.1000, that is, Rs.2551. So

when the TR Collection is cleared by debiting Rs.2551, the exact amount that is enough

to clear them, is credited to respective sundry debtors and other recoverable accounts.

The excess Rs.1000 is credited to the account of „Refund due on Double/Excess

Payments‟.

When the next invoice is generated, this excess amount is adjusted by crediting the

sundry debtors by the excess amount, as depicted in figure 4 and in the invoice depicted

below.

Customer Invoice

Fixed charges from subscriber 180 Local Call Charges 1000 International Trunk Calls 500 Total 1680

Add Service Tax 100 Education Cess 15 Higher Education Cess 5 Grand Total 1800

Less: Excess payment Adjusted 1000

Net Payable 800

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 18

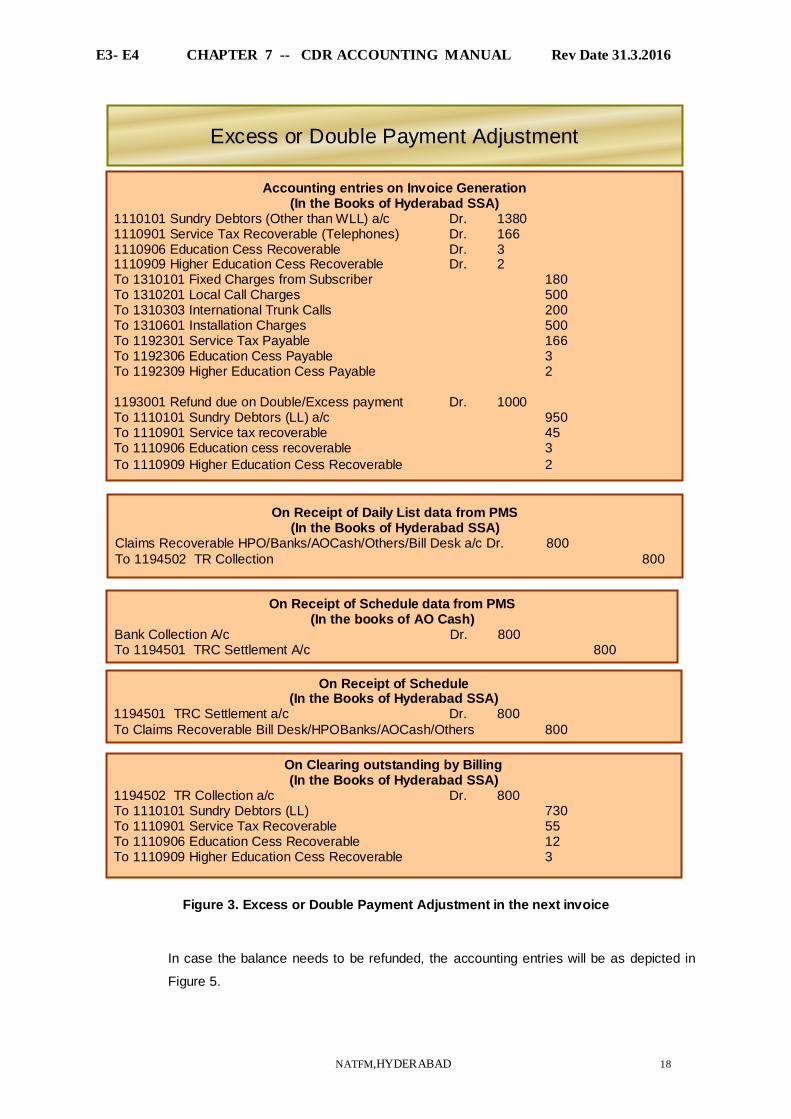

Figure 3. Excess or Double Payment Adjustment in the next invoice

In case the balance needs to be refunded, the accounting entries will be as depicted in

Figure 5.

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1194502 TR Collection a/c Dr. 800 To 1110101 Sundry Debtors (LL) 730 To 1110901 Service Tax Recoverable 55 To 1110906 Education Cess Recoverable 12 To 1110909 Higher Education Cess Recoverable 3

On Receipt of Schedule (In the Books of Hyderabad SSA)

1194501 TRC Settlement a/c Dr. 800

To Claims Recoverable Bill Desk/HPOBanks/AOCash/Others 800

On Receipt of Daily List data from PMS (In the Books of Hyderabad SSA)

Claims Recoverable HPO/Banks/AOCash/Others/Bill Desk a/c Dr. 800

To 1194502 TR Collection 800

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (Other than WLL) a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To 1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3 To 1192309 Higher Education Cess Payable 2 1193001 Refund due on Double/Excess payment Dr. 1000 To 1110101 Sundry Debtors (LL) a/c 950 To 1110901 Service tax recoverable 45 To 1110906 Education cess recoverable 3

To 1110909 Higher Education Cess Recoverable 2

Excess or Double Payment Adjustment

On Receipt of Schedule data from PMS (In the books of AO Cash)

Bank Collection A/c Dr. 800 To 1194501 TRC Settlement A/c 800

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 19

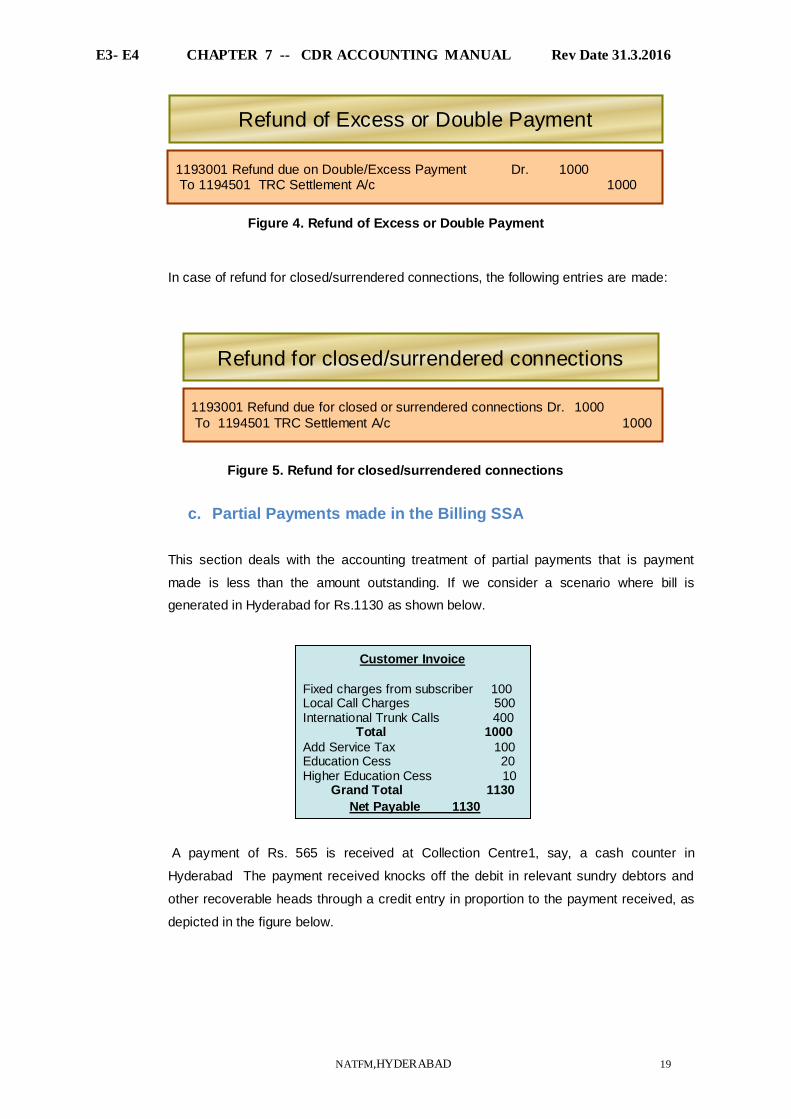

Figure 4. Refund of Excess or Double Payment

In case of refund for closed/surrendered connections, the following entries are made:

Figure 5. Refund for closed/surrendered connections

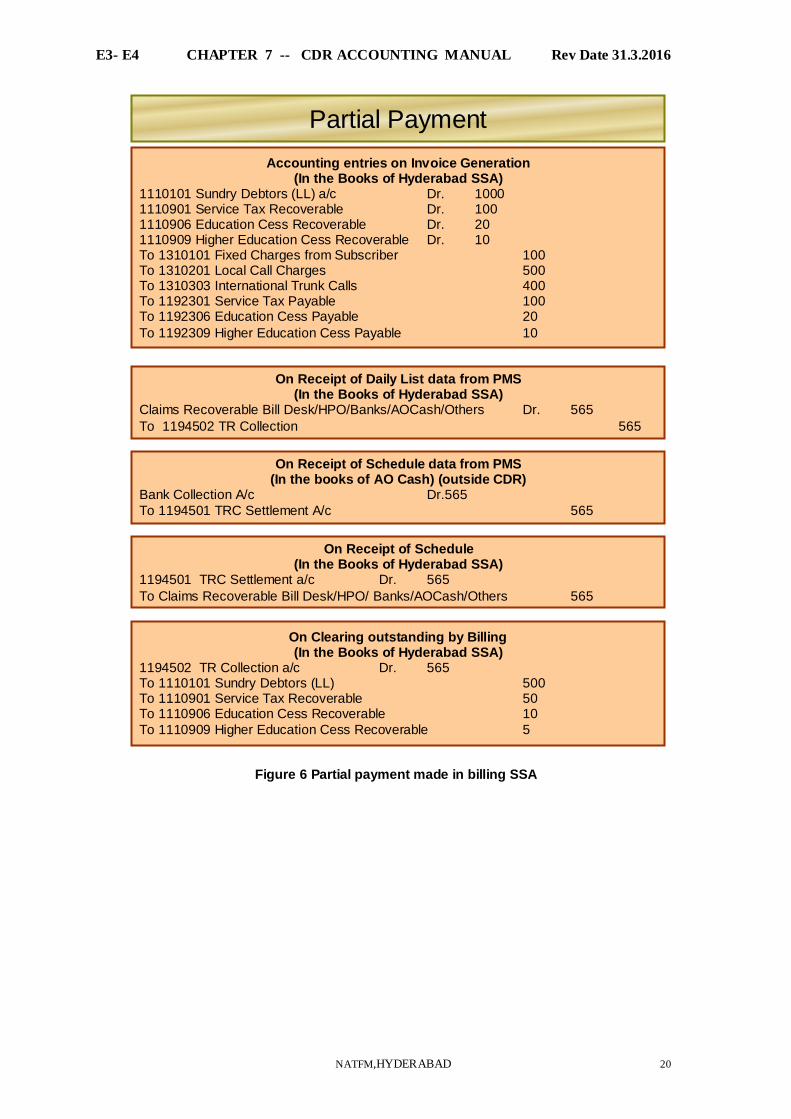

c. Partial Payments made in the Billing SSA

This section deals with the accounting treatment of partial payments that is payment

made is less than the amount outstanding. If we consider a scenario where bill is

generated in Hyderabad for Rs.1130 as shown below.

A payment of Rs. 565 is received at Collection Centre1, say, a cash counter in

Hyderabad The payment received knocks off the debit in relevant sundry debtors and

other recoverable heads through a credit entry in proportion to the payment received, as

depicted in the figure below.

1193001 Refund due for closed or surrendered connections Dr. 1000

To 1194501 TRC Settlement A/c 1000

Refund for closed/surrendered connections

1193001 Refund due on Double/Excess Payment Dr. 1000 To 1194501 TRC Settlement A/c 1000

Refund of Excess or Double Payment

Customer Invoice

Fixed charges from subscriber 100 Local Call Charges 500 International Trunk Calls 400 Total 1000

Add Service Tax 100 Education Cess 20 Higher Education Cess 10 Grand Total 1130

Net Payable 1130

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 20

Figure 6 Partial payment made in billing SSA

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1194502 TR Collection a/c Dr. 565 To 1110101 Sundry Debtors (LL) 500 To 1110901 Service Tax Recoverable 50 To 1110906 Education Cess Recoverable 10

To 1110909 Higher Education Cess Recoverable 5

On Receipt of Schedule (In the Books of Hyderabad SSA)

1194501 TRC Settlement a/c Dr. 565

To Claims Recoverable Bill Desk/HPO/ Banks/AOCash/Others 565

On Receipt of Daily List data from PMS (In the Books of Hyderabad SSA)

Claims Recoverable Bill Desk/HPO/Banks/AOCash/Others Dr. 565

To 1194502 TR Collection 565

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (LL) a/c Dr. 1000 1110901 Service Tax Recoverable Dr. 100 1110906 Education Cess Recoverable Dr. 20 1110909 Higher Education Cess Recoverable Dr. 10 To 1310101 Fixed Charges from Subscriber 100 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 400 To 1192301 Service Tax Payable 100 To 1192306 Education Cess Payable 20

To 1192309 Higher Education Cess Payable 10

Partial Payment

On Receipt of Schedule data from PMS (In the books of AO Cash) (outside CDR)

Bank Collection A/c Dr.565

To 1194501 TRC Settlement A/c 565

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 21

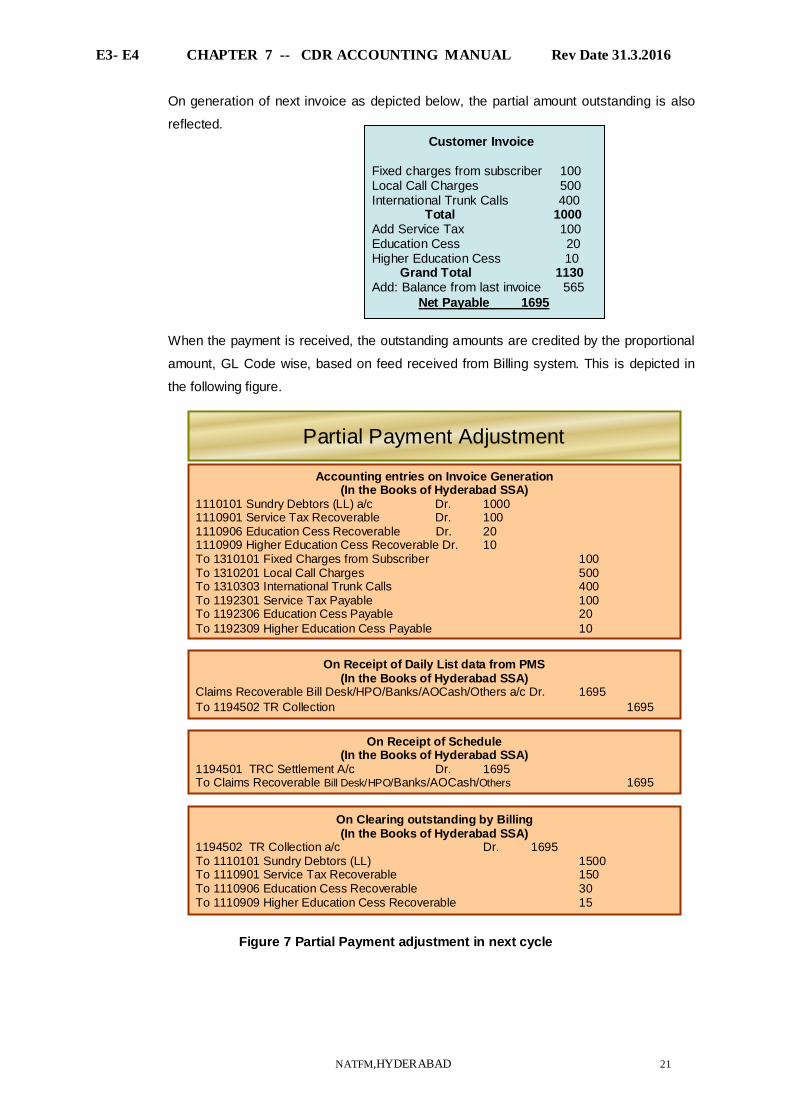

On generation of next invoice as depicted below, the partial amount outstanding is also

reflected.

When the payment is received, the outstanding amounts are credited by the proportional

amount, GL Code wise, based on feed received from Billing system. This is depicted in

the following figure.

Figure 7 Partial Payment adjustment in next cycle

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1194502 TR Collection a/c Dr. 1695 To 1110101 Sundry Debtors (LL) 1500 To 1110901 Service Tax Recoverable 150 To 1110906 Education Cess Recoverable 30 To 1110909 Higher Education Cess Recoverable 15

On Receipt of Schedule (In the Books of Hyderabad SSA)

1194501 TRC Settlement A/c Dr. 1695 To Claims Recoverable Bill Desk/HPO/Banks/AOCash/Others 1695

On Receipt of Daily List data from PMS (In the Books of Hyderabad SSA)

Claims Recoverable Bill Desk/HPO/Banks/AOCash/Others a/c Dr. 1695

To 1194502 TR Collection 1695

Partial Payment Adjustment

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (LL) a/c Dr. 1000 1110901 Service Tax Recoverable Dr. 100 1110906 Education Cess Recoverable Dr. 20 1110909 Higher Education Cess Recoverable Dr. 10 To 1310101 Fixed Charges from Subscriber 100 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 400 To 1192301 Service Tax Payable 100 To 1192306 Education Cess Payable 20

To 1192309 Higher Education Cess Payable 10

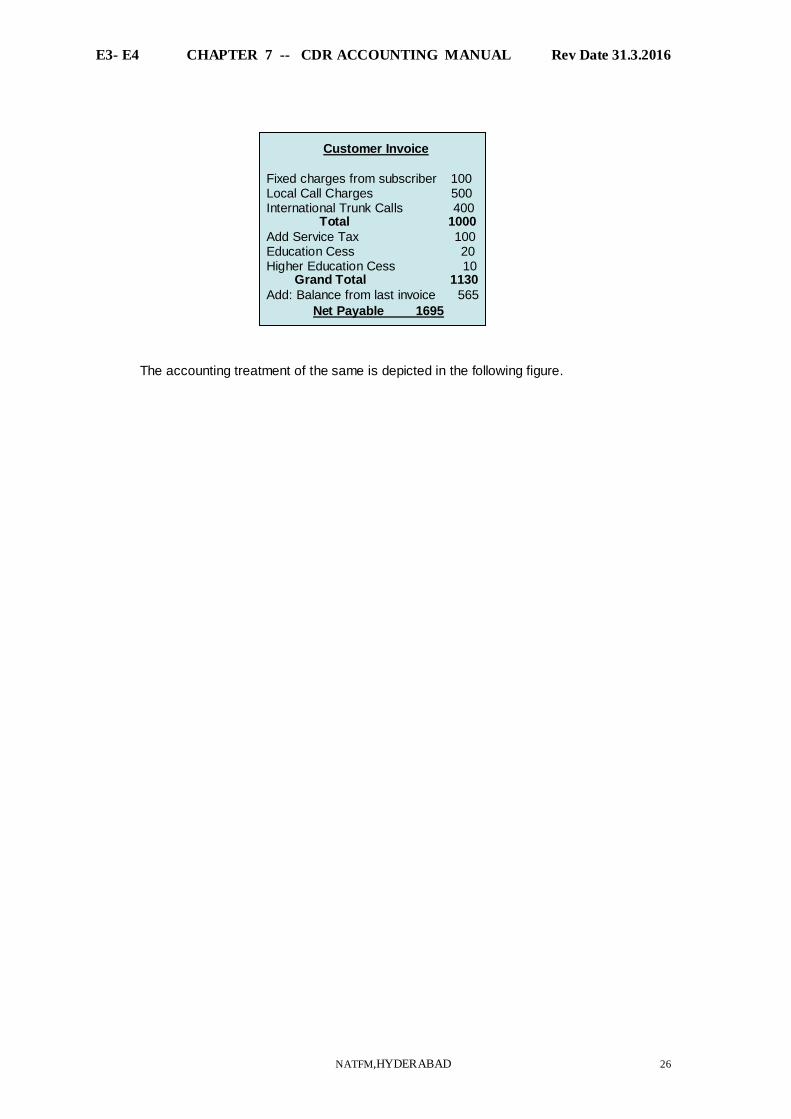

Customer Invoice Fixed charges from subscriber 100 Local Call Charges 500 International Trunk Calls 400 Total 1000 Add Service Tax 100 Education Cess 20 Higher Education Cess 10 Grand Total 1130 Add: Balance from last invoice 565

Net Payable 1695

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 22

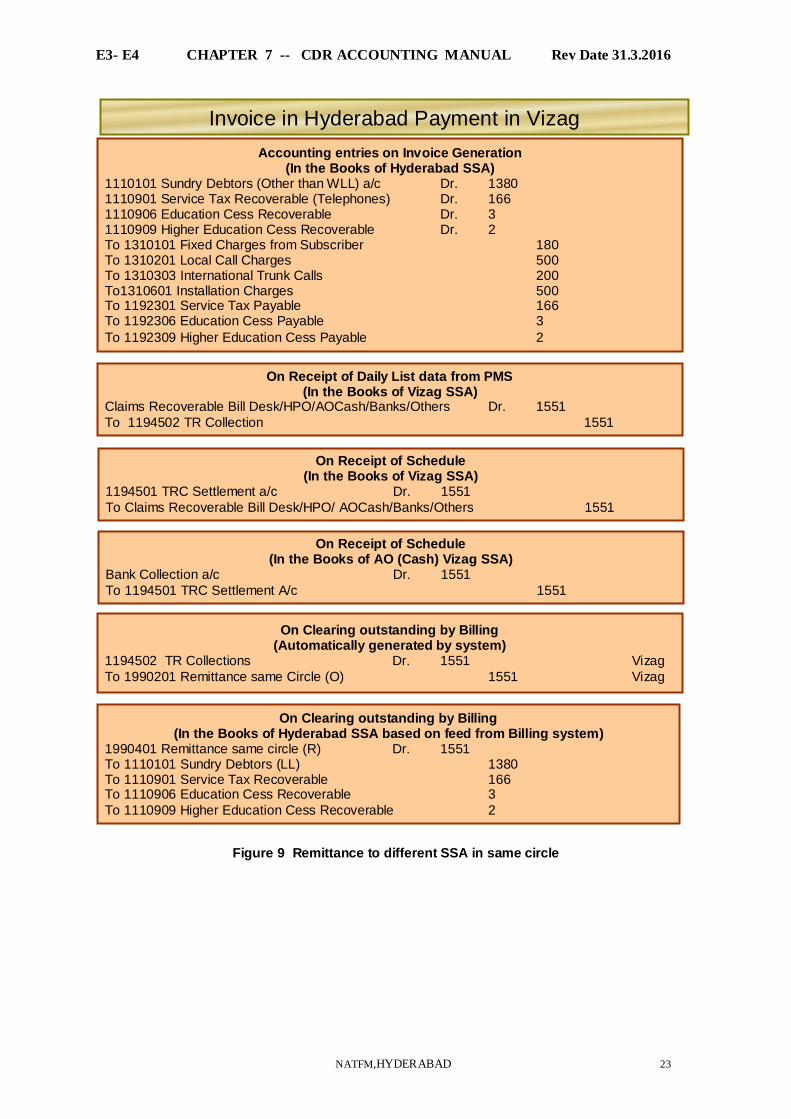

d. Remittance to different SSA, Same Circle (Complete payment)

In cases where the SSA where the payment is made is different than the SSA where the

Bill has been generated, we need to pass a remittance entry from the revenue receiving

SSA to the revenue owning SSA.

Accounting System is capable of generating remittance accounting entries for payments

received in SSA other than revenue owning SSA. Revenue owning and revenue

receiving SSAs can be in different Circles in the same Zone.

In order to comply with this requirement it is essential that Billing provides SSA

information for revenue at the time of billing as well as information on revenue owning

and revenue receiving SSA at the time of payment adjustment against outstanding.

In the following figure, a scenario is considered where Invoice is generated in Hyderabad

and payment is made in Vizag, that is both SSAs belong to the same circle. On receipt of

daily list information by PMS, Claims recoverable from collection centre a/c is debited by

the amount received, in the books of accounts of the receiving SSA that is Vizag here,

crediting the TR Collection Account.

When Schedule information and cheque is received by PMS, TRC Settlement account is

debited, thus clearing the outstanding Claims recoverable a/c in the revenue receiving

SSA. On payment feed from Billing system, the correct remittance entries are determined

and posted. TR Collection Account is debited and Originating Remittance same circle

credit entry is made in the books of accounts of revenue receiving, here Vizag. The

responding remittance entry in revenue owning SSA (Hyderabad in this case) is used to

clear the debtors outstanding and other recoverable accounts in revenue owning SSA.

Customer Invoice Fixed charges from subscriber 180 Local Call Charges 500 International Trunk Calls 200 Installation Charges 500 Total 1380 Add Service Tax 166 Education Cess 3 Higher Education Cess 2 Grand Total 1551 Net Payable 1551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 23

Figure 9 Remittance to different SSA in same circle

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (Other than WLL) a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3

To 1192309 Higher Education Cess Payable 2

On Receipt of Daily List data from PMS (In the Books of Vizag SSA)

Claims Recoverable Bill Desk/HPO/AOCash/Banks/Others Dr. 1551

To 1194502 TR Collection 1551

On Receipt of Schedule (In the Books of Vizag SSA)

1194501 TRC Settlement a/c Dr. 1551

To Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others 1551

On Clearing outstanding by Billing (In the Books of Hyderabad SSA based on feed from Billing system)

1990401 Remittance same circle (R) Dr. 1551 To 1110101 Sundry Debtors (LL) 1380 To 1110901 Service Tax Recoverable 166 To 1110906 Education Cess Recoverable 3

To 1110909 Higher Education Cess Recoverable 2

Invoice in Hyderabad Payment in Vizag

On Clearing outstanding by Billing (Automatically generated by system)

1194502 TR Collections Dr. 1551 Vizag

To 1990201 Remittance same Circle (O) 1551 Vizag

On Receipt of Schedule (In the Books of AO (Cash) Vizag SSA)

Bank Collection a/c Dr. 1551

To 1194501 TRC Settlement A/c 1551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 24

e. Remittance to SSA of Same Circle (Partial Payment)

This section deals with the accounting treatment of a scenario of Partial payment made in

some other SSA of the same circle in which invoice has been generated. Consider a

scenario where Bill is generated in Hyderabad (AP Circle) and payment is made in Vizag

(AP Circle).

Consider the bill to be the following:

The accounting treatment of the same will be as depicted in the figure below.

Customer Invoice Fixed charges from subscriber 100 Local Call Charges 500 International Trunk Calls 400 Total 1000 Add Service Tax 100 Education Cess 20 Higher Education Cess 10 Grand Total 1130

Net Payable 1130

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 25

Figure 10 Remittance to different SSA in same Circle (Partial Payment)

When Billing sends a payment feed to accounting, the correct remittance entries are used to settle

the recoverables by proportional amount as posted by the Billing System.

The next bill is depicted as follows:

Partial Payment Different SSA same Circle

On Receipt of Daily List data from PMS (In the Books of Vizag SSA)

Claims Recoverable Bill Desk/HPO/AOCash/Banks/Others A/c Dr. 565

To 1194502 TR Collections 565

On Receipt of Schedule (In the Books of Vizag SSA)

1194502 TRC Settlement a/c Dr. 565

To Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others 565

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (LL) a/c Dr. 1000 1110901 Service Tax Recoverable Dr. 100 1110906 Education Cess Recoverable Dr. 20 1110909 Higher Education Cess Recoverable Dr. 10 To 1310101 Fixed Charges from Subscriber 100 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 400 To 1192301 Service Tax Payable 100 To 1192306 Education Cess Payable 20

To 1192309 Higher Education Cess Payable 10

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1990401 Remittance same Circle (R) Dr. 565 To 1110101 Sundry Debtors (LL) 500 To 1110901 Service Tax Recoverable 50 To 1110906 Education Cess Recoverable 10

To 1110909 Higher Education Cess Recoverable 5

On Clearing outstanding by Billing 1194501 TR Collections Dr. 565 Vizag To 1990201 Remittance same Circle (O) 565 Vizag

On Receipt of Schedule (In the Books of AO (Cash) Vizag SSA)

Bank Collection a/c Dr. 565

To 1194501 TRC Settlement A/c 565

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 26

The accounting treatment of the same is depicted in the following figure.

Customer Invoice

Fixed charges from subscriber 100 Local Call Charges 500 International Trunk Calls 400 Total 1000

Add Service Tax 100 Education Cess 20 Higher Education Cess 10 Grand Total 1130

Add: Balance from last invoice 565

Net Payable 1695

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 27

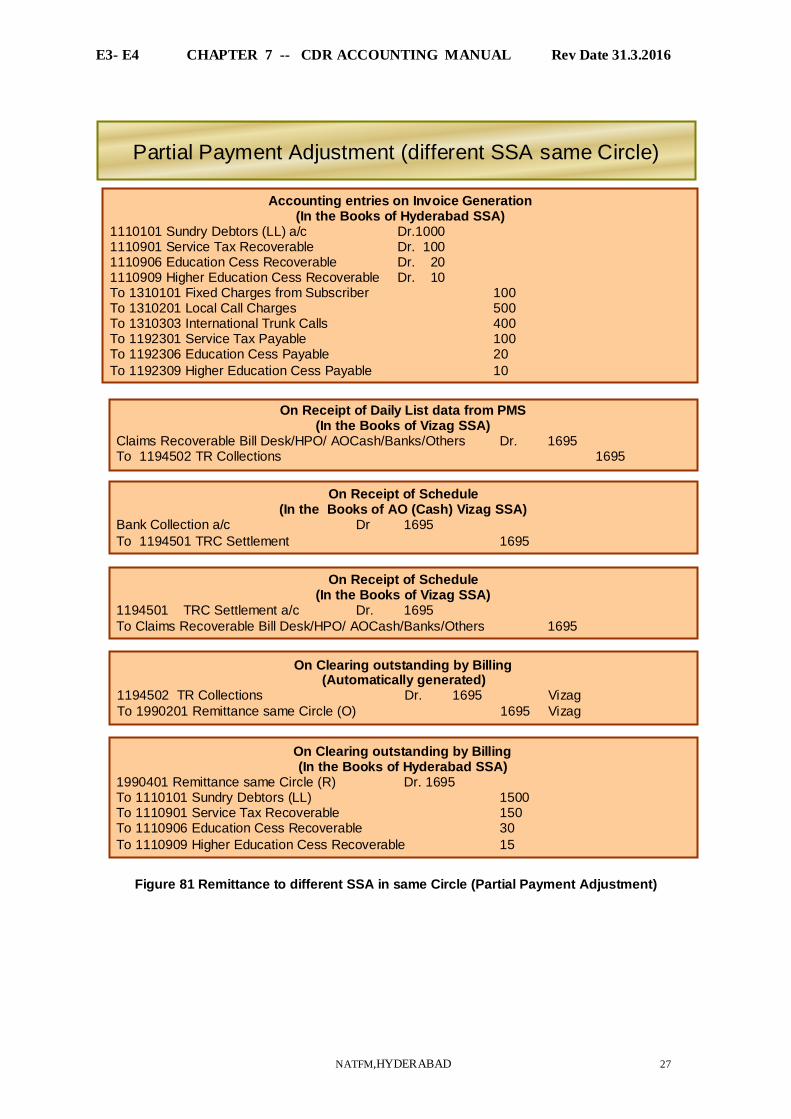

Figure 81 Remittance to different SSA in same Circle (Partial Payment Adjustment)

Partial Payment Adjustment (different SSA same Circle)

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (LL) a/c Dr.1000 1110901 Service Tax Recoverable Dr. 100 1110906 Education Cess Recoverable Dr. 20 1110909 Higher Education Cess Recoverable Dr. 10 To 1310101 Fixed Charges from Subscriber 100 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 400 To 1192301 Service Tax Payable 100 To 1192306 Education Cess Payable 20

To 1192309 Higher Education Cess Payable 10

On Receipt of Daily List data from PMS (In the Books of Vizag SSA)

Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others Dr. 1695 To 1194502 TR Collections 1695

On Receipt of Schedule (In the Books of Vizag SSA)

1194501 TRC Settlement a/c Dr. 1695

To Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others 1695

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1990401 Remittance same Circle (R) Dr. 1695 To 1110101 Sundry Debtors (LL) 1500 To 1110901 Service Tax Recoverable 150 To 1110906 Education Cess Recoverable 30

To 1110909 Higher Education Cess Recoverable 15

On Clearing outstanding by Billing (Automatically generated)

1194502 TR Collections Dr. 1695 Vizag

To 1990201 Remittance same Circle (O) 1695 Vizag

On Receipt of Schedule (In the Books of AO (Cash) Vizag SSA)

Bank Collection a/c Dr 1695

To 1194501 TRC Settlement 1695

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 28

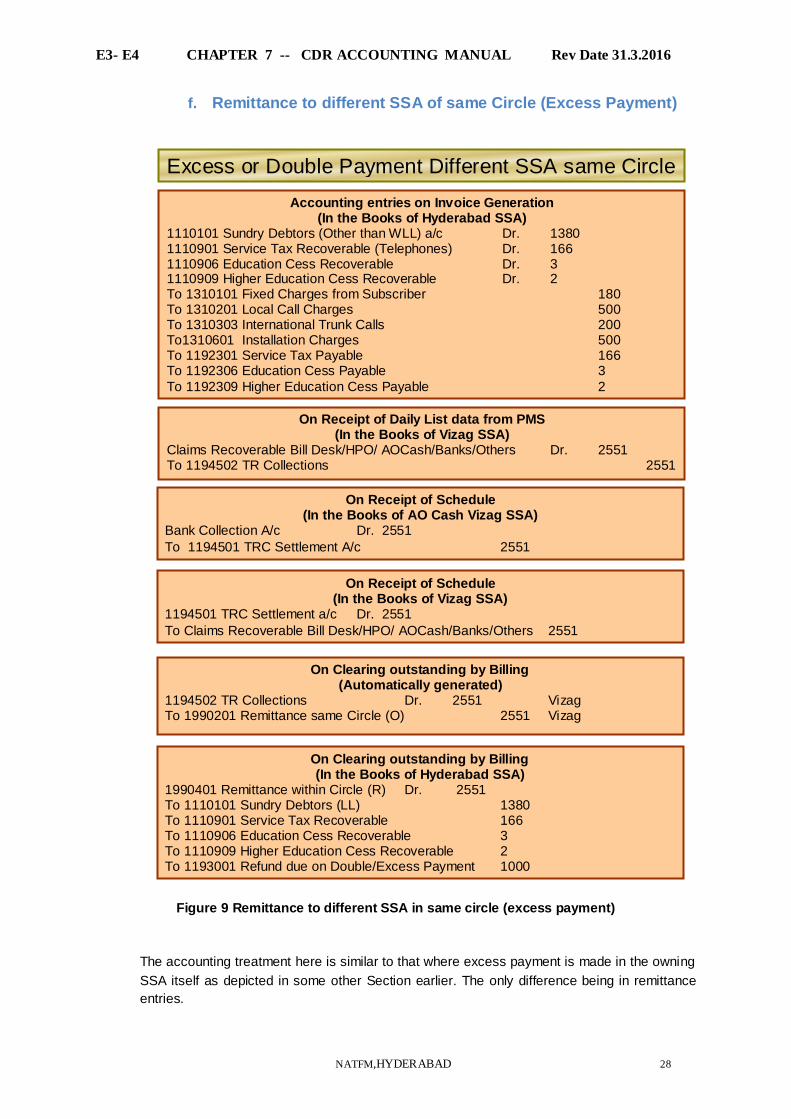

f. Remittance to different SSA of same Circle (Excess Payment)

Figure 9 Remittance to different SSA in same circle (excess payment)

The accounting treatment here is similar to that where excess payment is made in the owning

SSA itself as depicted in some other Section earlier. The only difference being in remittance

entries.

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (Other than WLL) a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3

To 1192309 Higher Education Cess Payable 2

Excess or Double Payment Different SSA same Circle

On Receipt of Daily List data from PMS (In the Books of Vizag SSA)

Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others Dr. 2551 To 1194502 TR Collections 2551

On Receipt of Schedule (In the Books of Vizag SSA)

1194501 TRC Settlement a/c Dr. 2551

To Claims Recoverable Bill Desk/HPO/ AOCash/Banks/Others 2551

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1990401 Remittance within Circle (R) Dr. 2551 To 1110101 Sundry Debtors (LL) 1380 To 1110901 Service Tax Recoverable 166 To 1110906 Education Cess Recoverable 3 To 1110909 Higher Education Cess Recoverable 2 To 1193001 Refund due on Double/Excess Payment 1000

On Clearing outstanding by Billing (Automatically generated)

1194502 TR Collections Dr. 2551 Vizag To 1990201 Remittance same Circle (O) 2551 Vizag

On Receipt of Schedule (In the Books of AO Cash Vizag SSA)

Bank Collection A/c Dr. 2551

To 1194501 TRC Settlement A/c 2551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 29

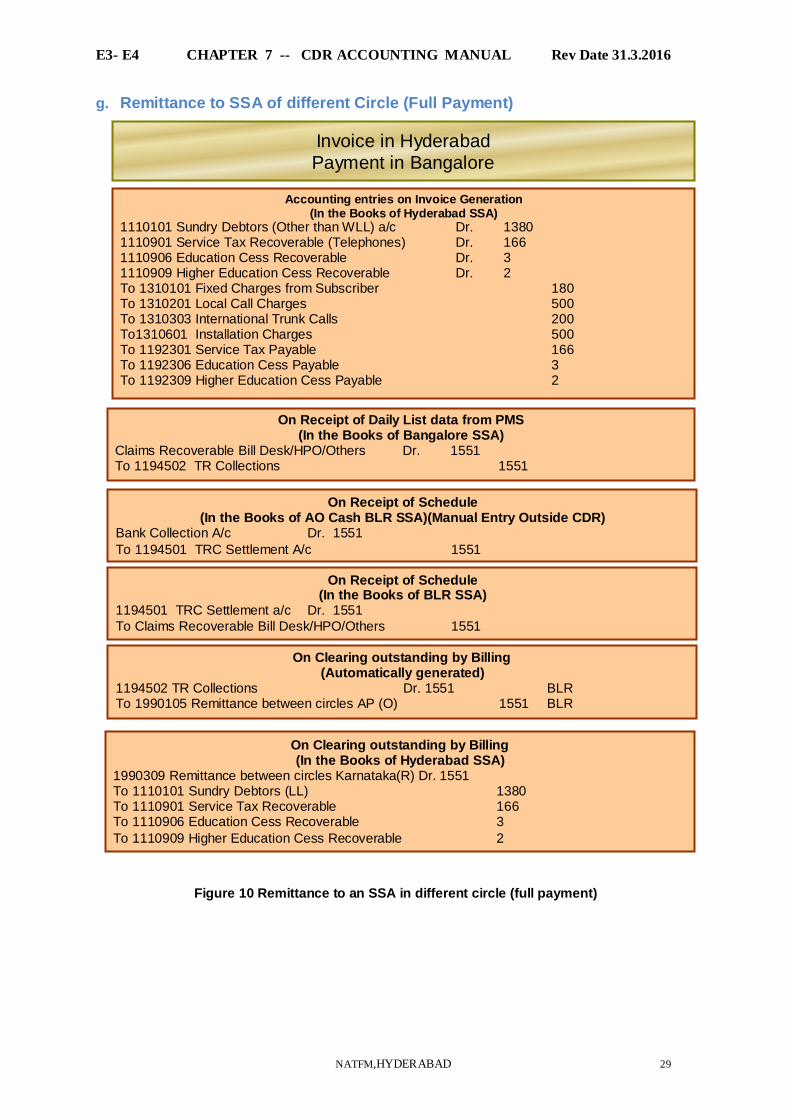

g. Remittance to SSA of different Circle (Full Payment)

Figure 10 Remittance to an SSA in different circle (full payment)

On Receipt of Daily List data from PMS (In the Books of Bangalore SSA)

Claims Recoverable Bill Desk/HPO/Others Dr. 1551 To 1194502 TR Collections 1551

On Clearing outstanding by Billing (In the Books of Hyderabad SSA)

1990309 Remittance between circles Karnataka(R) Dr. 1551 To 1110101 Sundry Debtors (LL) 1380 To 1110901 Service Tax Recoverable 166 To 1110906 Education Cess Recoverable 3

To 1110909 Higher Education Cess Recoverable 2

Invoice in Hyderabad Payment in Bangalore

Accounting entries on Invoice Generation (In the Books of Hyderabad SSA)

1110101 Sundry Debtors (Other than WLL) a/c Dr. 1380 1110901 Service Tax Recoverable (Telephones) Dr. 166 1110906 Education Cess Recoverable Dr. 3 1110909 Higher Education Cess Recoverable Dr. 2 To 1310101 Fixed Charges from Subscriber 180 To 1310201 Local Call Charges 500 To 1310303 International Trunk Calls 200 To1310601 Installation Charges 500 To 1192301 Service Tax Payable 166 To 1192306 Education Cess Payable 3 To 1192309 Higher Education Cess Payable 2

On Clearing outstanding by Billing (Automatically generated)

1194502 TR Collections Dr. 1551 BLR To 1990105 Remittance between circles AP (O) 1551 BLR

On Receipt of Schedule (In the Books of BLR SSA)

1194501 TRC Settlement a/c Dr. 1551

To Claims Recoverable Bill Desk/HPO/Others 1551

On Receipt of Schedule (In the Books of AO Cash BLR SSA)(Manual Entry Outside CDR)

Bank Collection A/c Dr. 1551

To 1194501 TRC Settlement A/c 1551

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 30

In the previous figure , a scenario is considered where Invoice is generated in Hyderabad and

payment is made in Bangalore, that is both SSAs belong to different circles in the same zone.

On receipt of daily list information by PMS, Claims recoverable from collection centre a/c is

debited by the amount received, in the books of accounts of the receiving SSA that is

Bangalore here. TR Collection Account is credited by the same amount. When Schedule

information and cheque is received by PMS, TRC Settlement account is debited, thus clearing

the outstanding Claims recoverable from CC(HPO/Bill Desk/Others) a/c in the revenue

receiving SSA. On payment feed from Billing system, TR Collection account is debited, The

corresponding originating Remittance credit entry is made in the books of accounts of

receiving SSA. The responding remittance entry is used to clear the debtors outstanding and

other recoverable accounts in revenue owning SSA. The remittance account used here is

Remittance between circles.

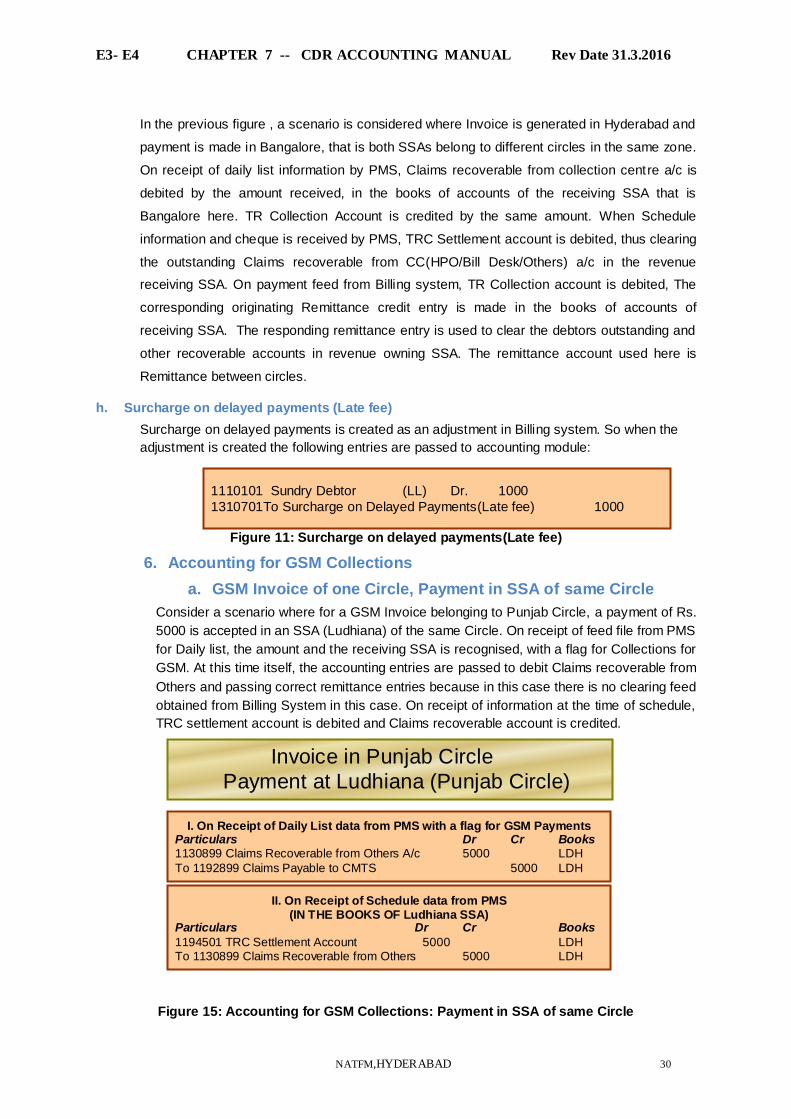

h. Surcharge on delayed payments (Late fee)

Surcharge on delayed payments is created as an adjustment in Billing system. So when the

adjustment is created the following entries are passed to accounting module:

Figure 11: Surcharge on delayed payments(Late fee)

6. Accounting for GSM Collections

a. GSM Invoice of one Circle, Payment in SSA of same Circle

Consider a scenario where for a GSM Invoice belonging to Punjab Circle, a payment of Rs.

5000 is accepted in an SSA (Ludhiana) of the same Circle. On receipt of feed file from PMS

for Daily list, the amount and the receiving SSA is recognised, with a flag for Collections for

GSM. At this time itself, the accounting entries are passed to debit Claims recoverable from

Others and passing correct remittance entries because in this case there is no clearing feed

obtained from Billing System in this case. On receipt of information at the time of schedule,

TRC settlement account is debited and Claims recoverable account is credited.

Figure 15: Accounting for GSM Collections: Payment in SSA of same Circle

I. On Receipt of Daily List data from PMS with a flag for GSM Payments Particulars Dr Cr Books 1130899 Claims Recoverable from Others A/c 5000 LDH

To 1192899 Claims Payable to CMTS 5000 LDH

II. On Receipt of Schedule data from PMS (IN THE BOOKS OF Ludhiana SSA)

Particulars Dr Cr Books

1194501 TRC Settlement Account 5000 LDH To 1130899 Claims Recoverable from Others 5000 LDH

Invoice in Punjab Circle

Payment at Ludhiana (Punjab Circle) (Full Payment)

1110101 Sundry Debtor (LL) Dr. 1000

1310701To Surcharge on Delayed Payments(Late fee) 1000

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 31

The credit entry to TRC Settlement A/c is made in the books of AO Cash with a debit to Bank Collection A/c on receipt of schedule.

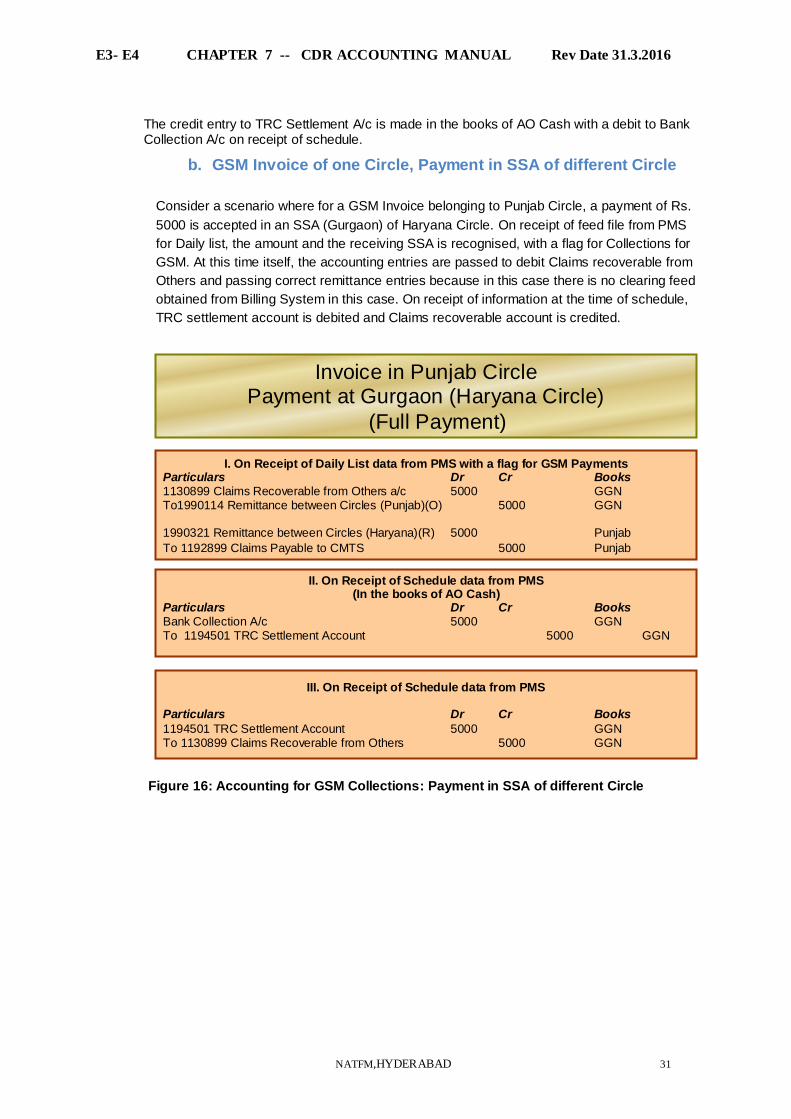

b. GSM Invoice of one Circle, Payment in SSA of different Circle

Consider a scenario where for a GSM Invoice belonging to Punjab Circle, a payment of Rs.

5000 is accepted in an SSA (Gurgaon) of Haryana Circle. On receipt of feed file from PMS

for Daily list, the amount and the receiving SSA is recognised, with a flag for Collections for

GSM. At this time itself, the accounting entries are passed to debit Claims recoverable from

Others and passing correct remittance entries because in this case there is no clearing feed

obtained from Billing System in this case. On receipt of information at the time of schedule,

TRC settlement account is debited and Claims recoverable account is credited.

Figure 16: Accounting for GSM Collections: Payment in SSA of different Circle

I. On Receipt of Daily List data from PMS with a flag for GSM Payments Particulars Dr Cr Books 1130899 Claims Recoverable from Others a/c 5000 GGN To1990114 Remittance between Circles (Punjab)(O) 5000 GGN 1990321 Remittance between Circles (Haryana)(R) 5000 Punjab

To 1192899 Claims Payable to CMTS 5000 Punjab

II. On Receipt of Schedule data from PMS (In the books of AO Cash)

Particulars Dr Cr Books Bank Collection A/c 5000 GGN To 1194501 TRC Settlement Account 5000 GGN

Invoice in Punjab Circle Payment at Gurgaon (Haryana Circle)

(Full Payment)

III. On Receipt of Schedule data from PMS Particulars Dr Cr Books

1194501 TRC Settlement Account 5000 GGN To 1130899 Claims Recoverable from Others 5000 GGN

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 32

7. Adjustments

The adjustment would update customer balance in billing system and appear on

subsequent bill. The adjustment voucher is required from the billing system to post

accounting entry. Also, when the amount is included in the next invoice, the relevant GL

Code based information will flow from Billing to accounting as depicted in the following

sections.

a. Debit Voucher A debit voucher on account of revenue would arise on account of the following reasons.

Detection of short billing on a previous invoice

Detection of non-billing for any previous period.

To create cheque dishonour charges, if any.

To create late fee to be incorporated into the next invoice.

To deal with special charges to be levied for bold entry in telephone directory etc.

When the billing is done in the above cases, the revenue being invoiced would be

belonging to a previous bill cycle falling within the same fiscal (Accounting) year or an

accounting period in respect of which final accounts have already been closed. In the

former case, no accounting issues are involved and the revenue would be billed as

current year income. In the latter case, we have to follow the accounting policy on dealing

with “prior period income”.

Based on this the amount would be booked either as income in the current year or as

prior period income. Booking of Prior Period income will be done in accounting as a

manual journal entry.

Take an example where short billing on a previous invoice is detected. For recovery of

charges subsequent to generation of bill, a debit is posted in the Billing System. The debit

voucher updates customer account balance in Billing system and appear in subsequent

bill. The debit voucher is posted in accounting simultaneously.The debit voucher is

required from the billing system to post accounting entry. The taxation part of the debit

entries will be taken care of at the time of actual billing. Only the basic amount will be

entered as a debit voucher. This is depicted in following Figure .

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 33

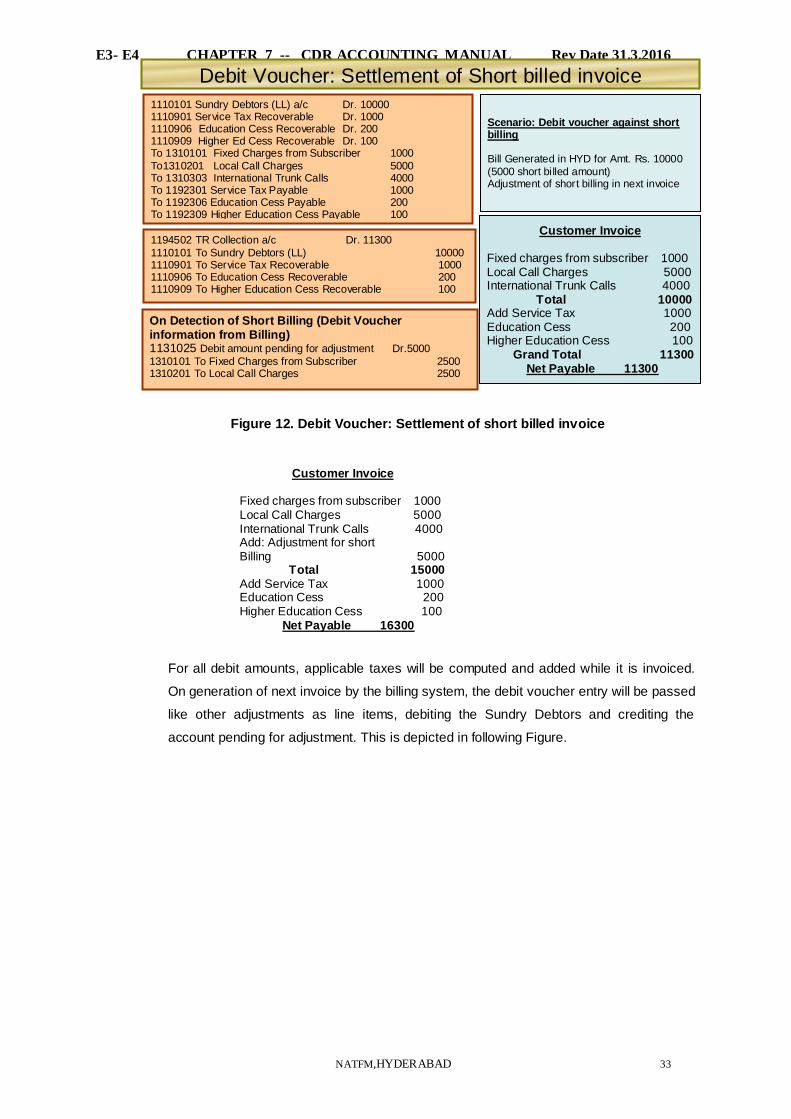

Figure 12. Debit Voucher: Settlement of short billed invoice

Customer Invoice Fixed charges from subscriber 1000 Local Call Charges 5000 International Trunk Calls 4000 Add: Adjustment for short Billing 5000 Total 15000 Add Service Tax 1000 Education Cess 200 Higher Education Cess 100 Net Payable 16300

For all debit amounts, applicable taxes will be computed and added while it is invoiced.

On generation of next invoice by the billing system, the debit voucher entry will be passed

like other adjustments as line items, debiting the Sundry Debtors and crediting the

account pending for adjustment. This is depicted in following Figure.

Debit Voucher: Settlement of Short billed invoice

Scenario: Debit voucher against short billing Bill Generated in HYD for Amt. Rs. 10000

(5000 short billed amount) Adjustment of short billing in next invoice

Customer Invoice Fixed charges from subscriber 1000 Local Call Charges 5000 International Trunk Calls 4000 Total 10000 Add Service Tax 1000 Education Cess 200 Higher Education Cess 100 Grand Total 11300 Net Payable 11300

1194502 TR Collection a/c Dr. 11300

1110101 To Sundry Debtors (LL) 10000 1110901 To Service Tax Recoverable 1000 1110906 To Education Cess Recoverable 200 1110909 To Higher Education Cess Recoverable 100

1110101 Sundry Debtors (LL) a/c Dr. 10000 1110901 Service Tax Recoverable Dr. 1000 1110906 Education Cess Recoverable Dr. 200 1110909 Higher Ed Cess Recoverable Dr. 100 To 1310101 Fixed Charges from Subscriber 1000

To1310201 Local Call Charges 5000 To 1310303 International Trunk Calls 4000 To 1192301 Service Tax Payable 1000 To 1192306 Education Cess Payable 200 To 1192309 Higher Education Cess Payable 100

On Detection of Short Billing (Debit Voucher information from Billing) 1131025 Debit amount pending for adjustment Dr.5000

1310101 To Fixed Charges from Subscriber 2500 1310201 To Local Call Charges 2500

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

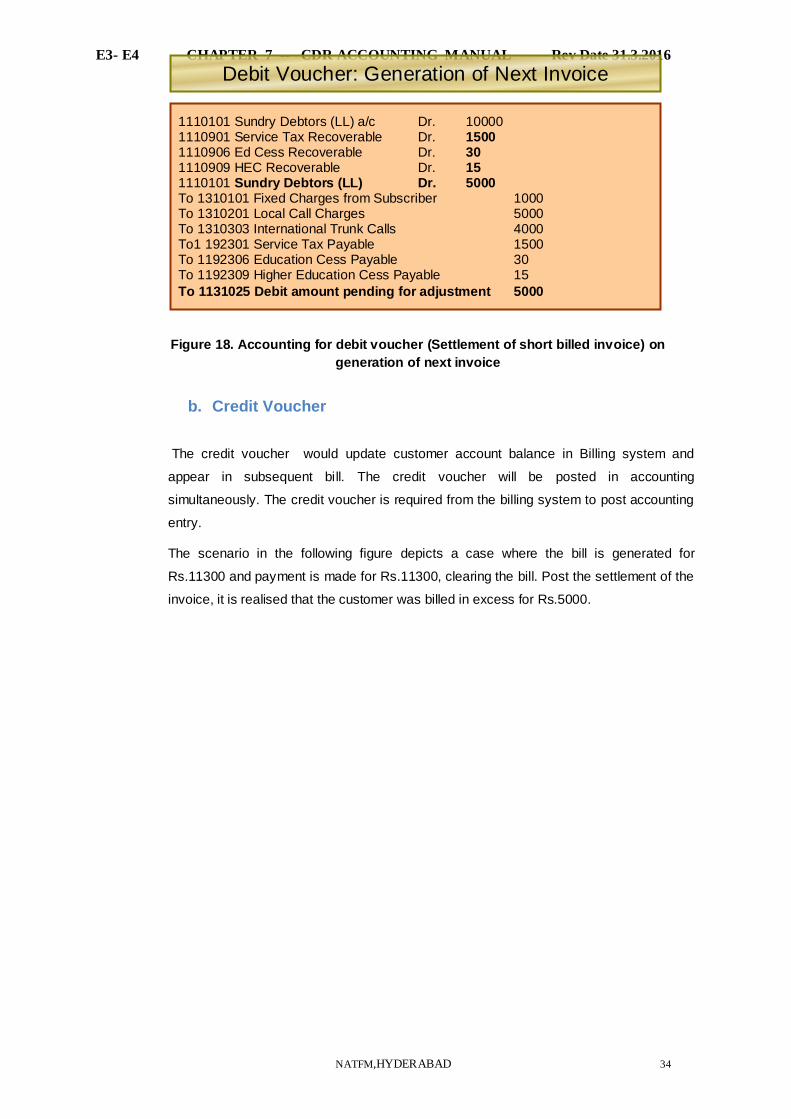

NATFM,HYDERABAD 34

Figure 18. Accounting for debit voucher (Settlement of short billed invoice) on

generation of next invoice

b. Credit Voucher

The credit voucher would update customer account balance in Billing system and

appear in subsequent bill. The credit voucher will be posted in accounting

simultaneously. The credit voucher is required from the billing system to post accounting

entry.

The scenario in the following figure depicts a case where the bill is generated for

Rs.11300 and payment is made for Rs.11300, clearing the bill. Post the settlement of the

invoice, it is realised that the customer was billed in excess for Rs.5000.

Debit Voucher: Generation of Next Invoice

1110101 Sundry Debtors (LL) a/c Dr. 10000 1110901 Service Tax Recoverable Dr. 1500 1110906 Ed Cess Recoverable Dr. 30 1110909 HEC Recoverable Dr. 15 1110101 Sundry Debtors (LL) Dr. 5000 To 1310101 Fixed Charges from Subscriber 1000 To 1310201 Local Call Charges 5000 To 1310303 International Trunk Calls 4000 To1 192301 Service Tax Payable 1500 To 1192306 Education Cess Payable 30 To 1192309 Higher Education Cess Payable 15

To 1131025 Debit amount pending for adjustment 5000

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 35

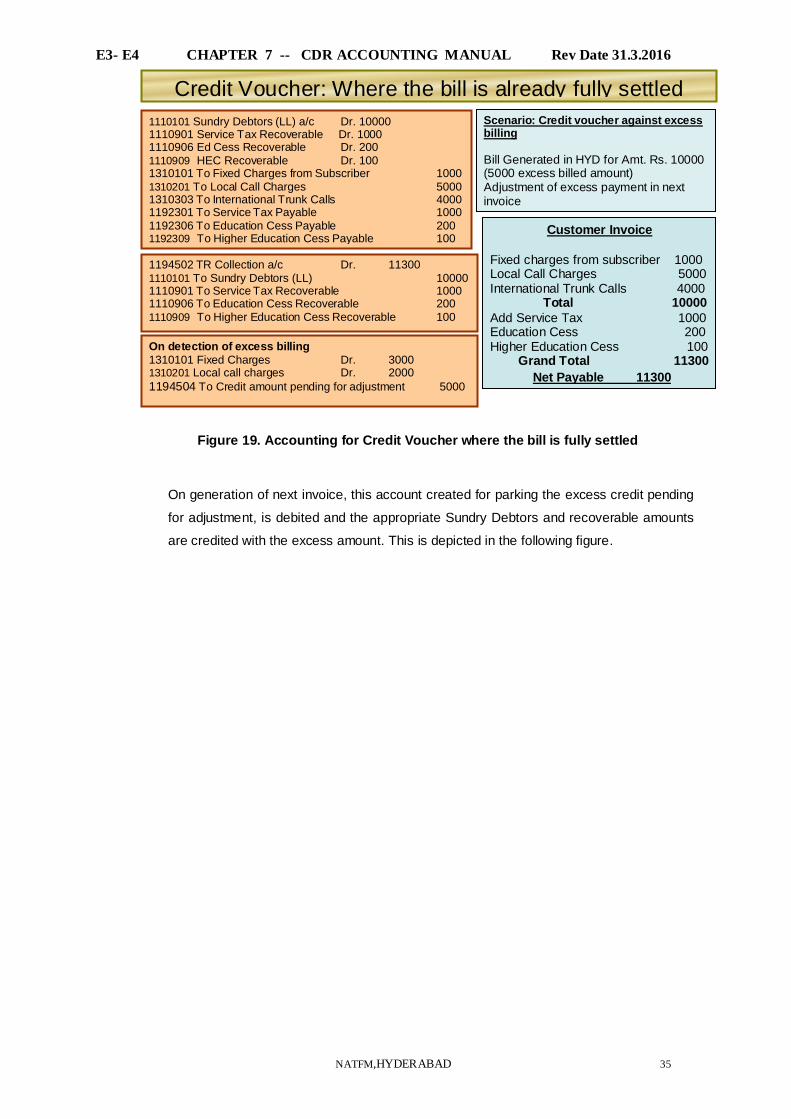

Figure 19. Accounting for Credit Voucher where the bill is fully settled

On generation of next invoice, this account created for parking the excess credit pending

for adjustment, is debited and the appropriate Sundry Debtors and recoverable amounts

are credited with the excess amount. This is depicted in the following figure.

Scenario: Credit voucher against excess billing

Bill Generated in HYD for Amt. Rs. 10000 (5000 excess billed amount) Adjustment of excess payment in next invoice

Customer Invoice

Fixed charges from subscriber 1000 Local Call Charges 5000 International Trunk Calls 4000 Total 10000

Add Service Tax 1000 Education Cess 200 Higher Education Cess 100 Grand Total 11300

Net Payable 11300

On detection of excess billing 1310101 Fixed Charges Dr. 3000 1310201 Local call charges Dr. 2000

1194504 To Credit amount pending for adjustment 5000

1194502 TR Collection a/c Dr. 11300 1110101 To Sundry Debtors (LL) 10000 1110901 To Service Tax Recoverable 1000 1110906 To Education Cess Recoverable 200 1110909 To Higher Education Cess Recoverable 100

1110101 Sundry Debtors (LL) a/c Dr. 10000 1110901 Service Tax Recoverable Dr. 1000 1110906 Ed Cess Recoverable Dr. 200 1110909 HEC Recoverable Dr. 100 1310101 To Fixed Charges from Subscriber 1000 1310201 To Local Call Charges 5000 1310303 To International Trunk Calls 4000 1192301 To Service Tax Payable 1000 1192306 To Education Cess Payable 200 1192309 To Higher Education Cess Payable 100

Credit Voucher: Where the bill is already fully settled

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 36

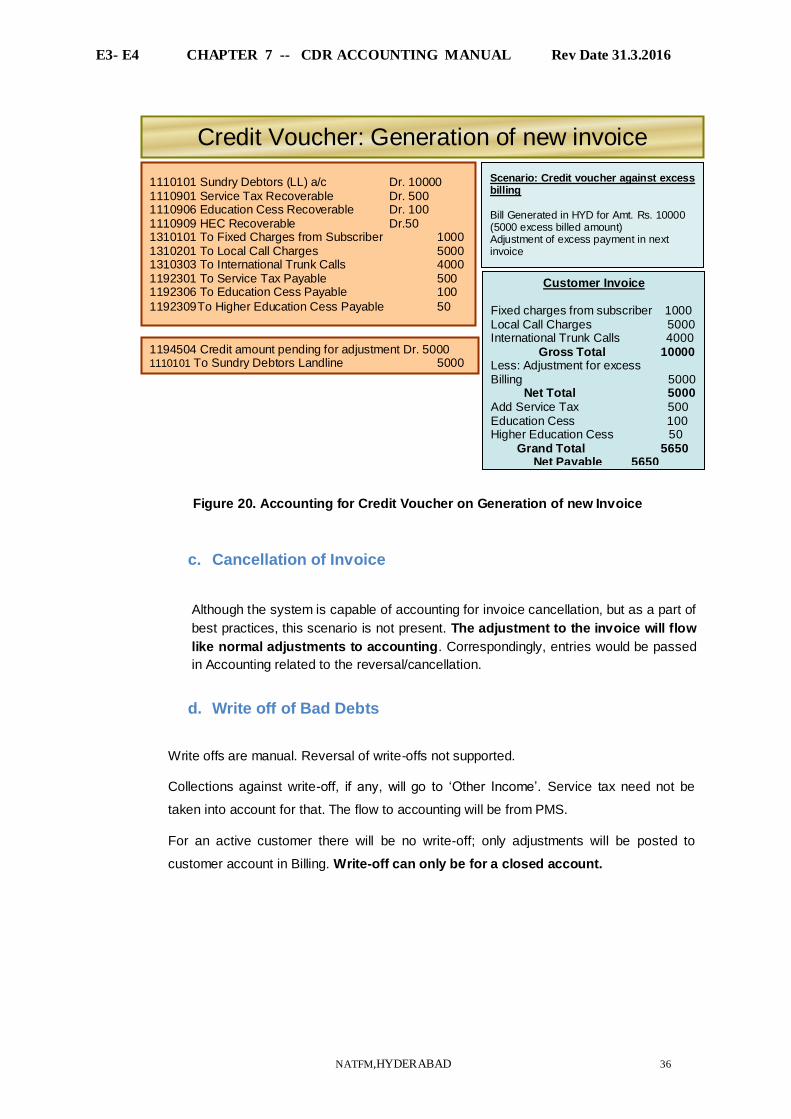

Figure 20. Accounting for Credit Voucher on Generation of new Invoice

c. Cancellation of Invoice

Although the system is capable of accounting for invoice cancellation, but as a part of

best practices, this scenario is not present. The adjustment to the invoice will flow

like normal adjustments to accounting. Correspondingly, entries would be passed

in Accounting related to the reversal/cancellation.

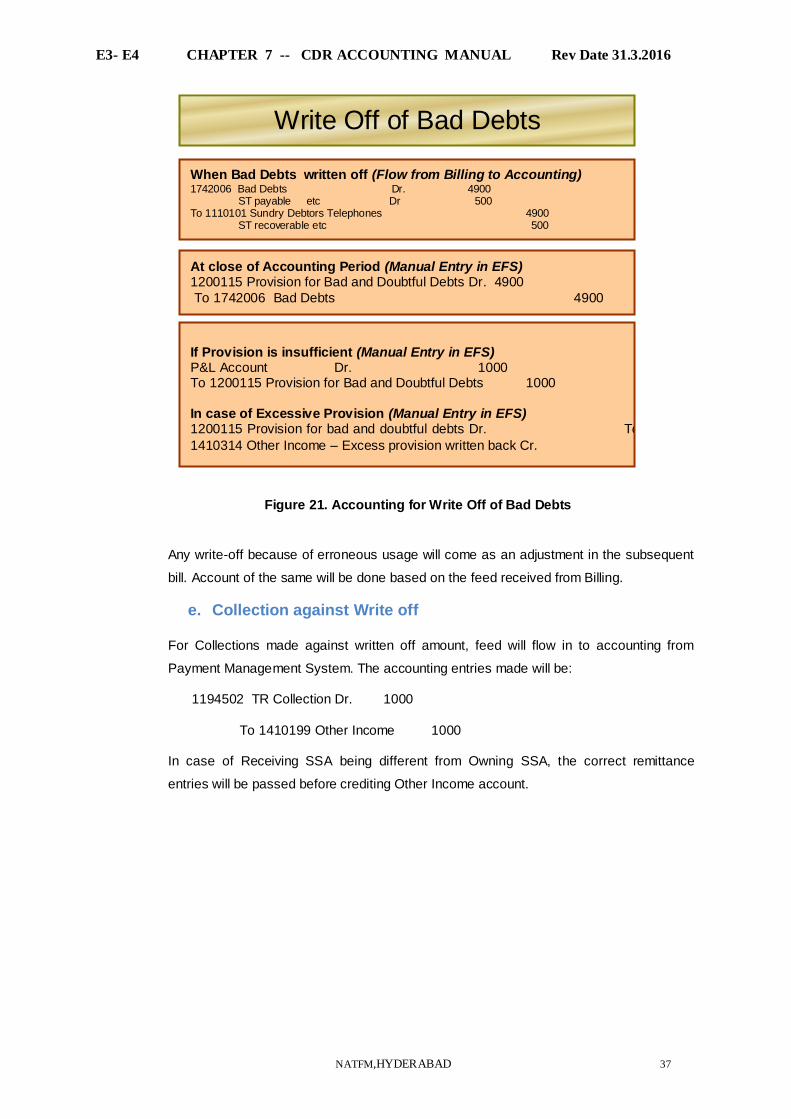

d. Write off of Bad Debts

Write offs are manual. Reversal of write-offs not supported.

Collections against write-off, if any, will go to „Other Income‟. Service tax need not be

taken into account for that. The flow to accounting will be from PMS.

For an active customer there will be no write-off; only adjustments will be posted to

customer account in Billing. Write-off can only be for a closed account.

Credit Voucher: Generation of new invoice

Scenario: Credit voucher against excess billing

Bill Generated in HYD for Amt. Rs. 10000 (5000 excess billed amount) Adjustment of excess payment in next invoice

Customer Invoice Fixed charges from subscriber 1000 Local Call Charges 5000 International Trunk Calls 4000 Gross Total 10000 Less: Adjustment for excess Billing 5000 Net Total 5000 Add Service Tax 500 Education Cess 100 Higher Education Cess 50 Grand Total 5650 Net Payable 5650

1110101 Sundry Debtors (LL) a/c Dr. 10000 1110901 Service Tax Recoverable Dr. 500 1110906 Education Cess Recoverable Dr. 100 1110909 HEC Recoverable Dr.50 1310101 To Fixed Charges from Subscriber 1000 1310201 To Local Call Charges 5000 1310303 To International Trunk Calls 4000 1192301 To Service Tax Payable 500 1192306 To Education Cess Payable 100

1192309 To Higher Education Cess Payable 50

1194504 Credit amount pending for adjustment Dr. 5000 1110101 To Sundry Debtors Landline 5000

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 37

Figure 21. Accounting for Write Off of Bad Debts

Any write-off because of erroneous usage will come as an adjustment in the subsequent

bill. Account of the same will be done based on the feed received from Billing.

e. Collection against Write off

For Collections made against written off amount, feed will flow in to accounting from

Payment Management System. The accounting entries made will be:

1194502 TR Collection Dr. 1000

To 1410199 Other Income 1000

In case of Receiving SSA being different from Owning SSA, the correct remittance

entries will be passed before crediting Other Income account.

Write Off of Bad Debts

When Bad Debts written off (Flow from Billing to Accounting) 1742006 Bad Debts Dr. 4900 ST payable etc Dr 500 To 1110101 Sundry Debtors Telephones 4900 ST recoverable etc 500

At close of Accounting Period (Manual Entry in EFS) 1200115 Provision for Bad and Doubtful Debts Dr. 4900

To 1742006 Bad Debts 4900

If Provision is insufficient (Manual Entry in EFS) P&L Account Dr. 1000 To 1200115 Provision for Bad and Doubtful Debts 1000 In case of Excessive Provision (Manual Entry in EFS) 1200115 Provision for bad and doubtful debts Dr. To To

1410314 Other Income – Excess provision written back Cr.

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 38

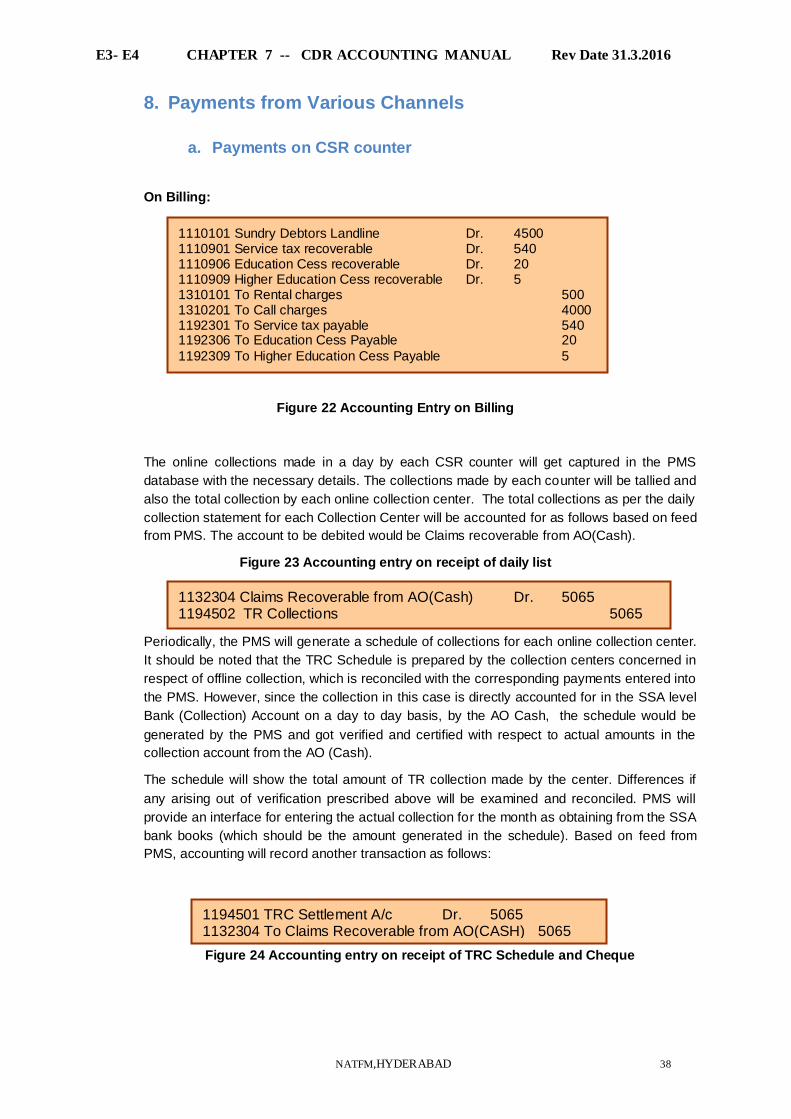

8. Payments from Various Channels

a. Payments on CSR counter

On Billing:

Figure 22 Accounting Entry on Billing

The online collections made in a day by each CSR counter will get captured in the PMS

database with the necessary details. The collections made by each counter will be tallied and

also the total collection by each online collection center. The total collections as per the daily

collection statement for each Collection Center will be accounted for as follows based on feed

from PMS. The account to be debited would be Claims recoverable from AO(Cash).

Figure 23 Accounting entry on receipt of daily list

Periodically, the PMS will generate a schedule of collections for each online collection center.

It should be noted that the TRC Schedule is prepared by the collection centers concerned in

respect of offline collection, which is reconciled with the corresponding payments entered into

the PMS. However, since the collection in this case is directly accounted for in the SSA level

Bank (Collection) Account on a day to day basis, by the AO Cash, the schedule would be

generated by the PMS and got verified and certified with respect to actual amounts in the

collection account from the AO (Cash).

The schedule will show the total amount of TR collection made by the center. Differences if

any arising out of verification prescribed above will be examined and reconciled. PMS will

provide an interface for entering the actual collection for the month as obtaining from the SSA

bank books (which should be the amount generated in the schedule). Based on feed from

PMS, accounting will record another transaction as follows:

Figure 24 Accounting entry on receipt of TRC Schedule and Cheque

1110101 Sundry Debtors Landline Dr. 4500 1110901 Service tax recoverable Dr. 540 1110906 Education Cess recoverable Dr. 20 1110909 Higher Education Cess recoverable Dr. 5 1310101 To Rental charges 500 1310201 To Call charges 4000 1192301 To Service tax payable 540 1192306 To Education Cess Payable 20

1192309 To Higher Education Cess Payable 5

1132304 Claims Recoverable from AO(Cash) Dr. 5065 1194502 TR Collections 5065

1194501 TRC Settlement A/c Dr. 5065 1132304 To Claims Recoverable from AO(CASH) 5065

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 39

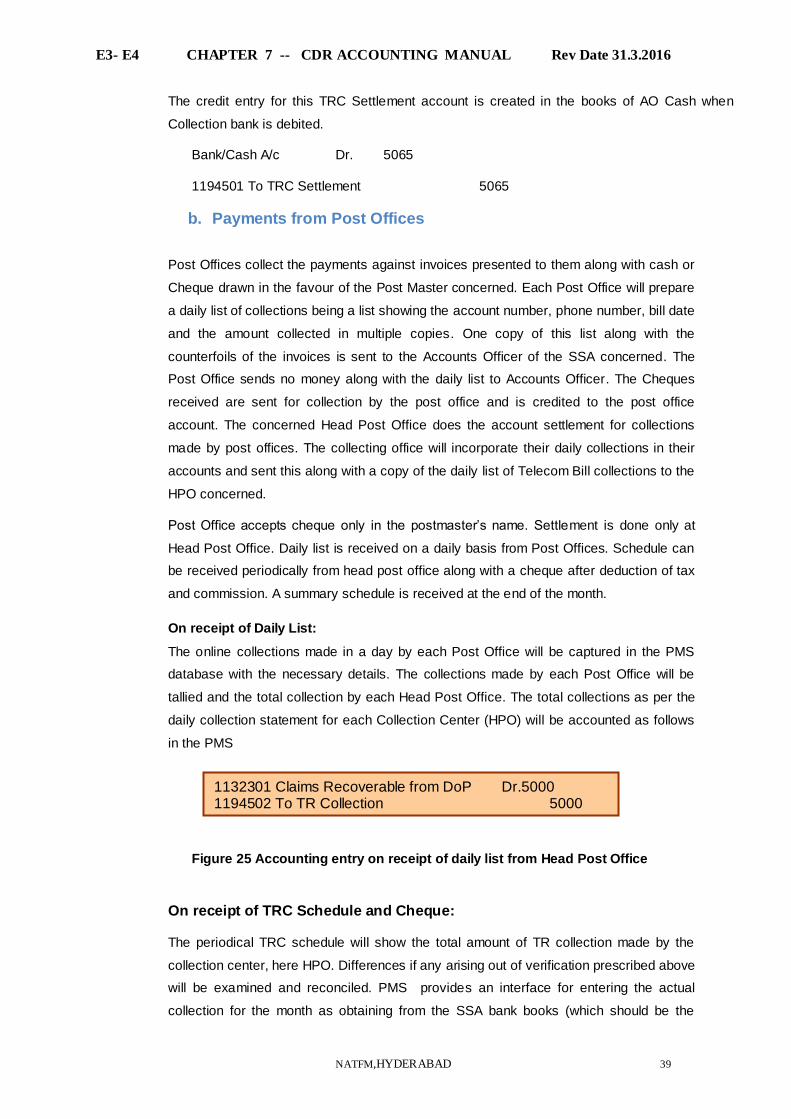

The credit entry for this TRC Settlement account is created in the books of AO Cash when

Collection bank is debited.

Bank/Cash A/c Dr. 5065

1194501 To TRC Settlement 5065

b. Payments from Post Offices

Post Offices collect the payments against invoices presented to them along with cash or

Cheque drawn in the favour of the Post Master concerned. Each Post Office will prepare

a daily list of collections being a list showing the account number, phone number, bill date

and the amount collected in multiple copies. One copy of this list along with the

counterfoils of the invoices is sent to the Accounts Officer of the SSA concerned. The

Post Office sends no money along with the daily list to Accounts Officer. The Cheques

received are sent for collection by the post office and is credited to the post office

account. The concerned Head Post Office does the account settlement for collections

made by post offices. The collecting office will incorporate their daily collections in their

accounts and sent this along with a copy of the daily list of Telecom Bill collections to the

HPO concerned.

Post Office accepts cheque only in the postmaster‟s name. Settlement is done only at

Head Post Office. Daily list is received on a daily basis from Post Offices. Schedule can

be received periodically from head post office along with a cheque after deduction of tax

and commission. A summary schedule is received at the end of the month.

On receipt of Daily List:

The online collections made in a day by each Post Office will be captured in the PMS

database with the necessary details. The collections made by each Post Office will be

tallied and the total collection by each Head Post Office. The total collections as per the

daily collection statement for each Collection Center (HPO) will be accounted as follows

in the PMS

Figure 25 Accounting entry on receipt of daily list from Head Post Office

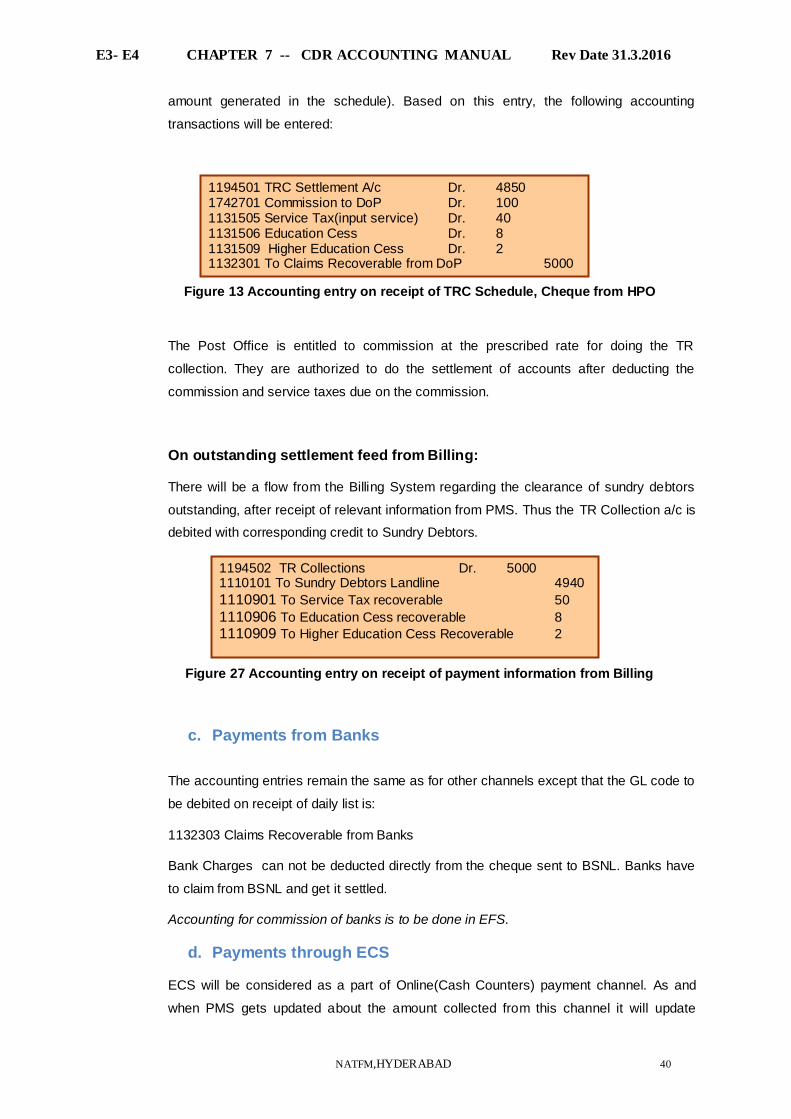

On receipt of TRC Schedule and Cheque:

The periodical TRC schedule will show the total amount of TR collection made by the

collection center, here HPO. Differences if any arising out of verification prescribed above

will be examined and reconciled. PMS provides an interface for entering the actual

collection for the month as obtaining from the SSA bank books (which should be the

1132301 Claims Recoverable from DoP Dr.5000 1194502 To TR Collection 5000

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 40

amount generated in the schedule). Based on this entry, the following accounting

transactions will be entered:

Figure 13 Accounting entry on receipt of TRC Schedule, Cheque from HPO

The Post Office is entitled to commission at the prescribed rate for doing the TR

collection. They are authorized to do the settlement of accounts after deducting the

commission and service taxes due on the commission.

On outstanding settlement feed from Billing:

There will be a flow from the Billing System regarding the clearance of sundry debtors

outstanding, after receipt of relevant information from PMS. Thus the TR Collection a/c is

debited with corresponding credit to Sundry Debtors.

Figure 27 Accounting entry on receipt of payment information from Billing

c. Payments from Banks

The accounting entries remain the same as for other channels except that the GL code to

be debited on receipt of daily list is:

1132303 Claims Recoverable from Banks

Bank Charges can not be deducted directly from the cheque sent to BSNL. Banks have

to claim from BSNL and get it settled.

Accounting for commission of banks is to be done in EFS.

d. Payments through ECS

ECS will be considered as a part of Online(Cash Counters) payment channel. As and

when PMS gets updated about the amount collected from this channel it will update

1194501 TRC Settlement A/c Dr. 4850 1742701 Commission to DoP Dr. 100 1131505 Service Tax(input service) Dr. 40 1131506 Education Cess Dr. 8 1131509 Higher Education Cess Dr. 2 1132301 To Claims Recoverable from DoP 5000

1194502 TR Collections Dr. 5000 1110101 To Sundry Debtors Landline 4940

1110901 To Service Tax recoverable 50

1110906 To Education Cess recoverable 8

1110909 To Higher Education Cess Recoverable 2

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 41

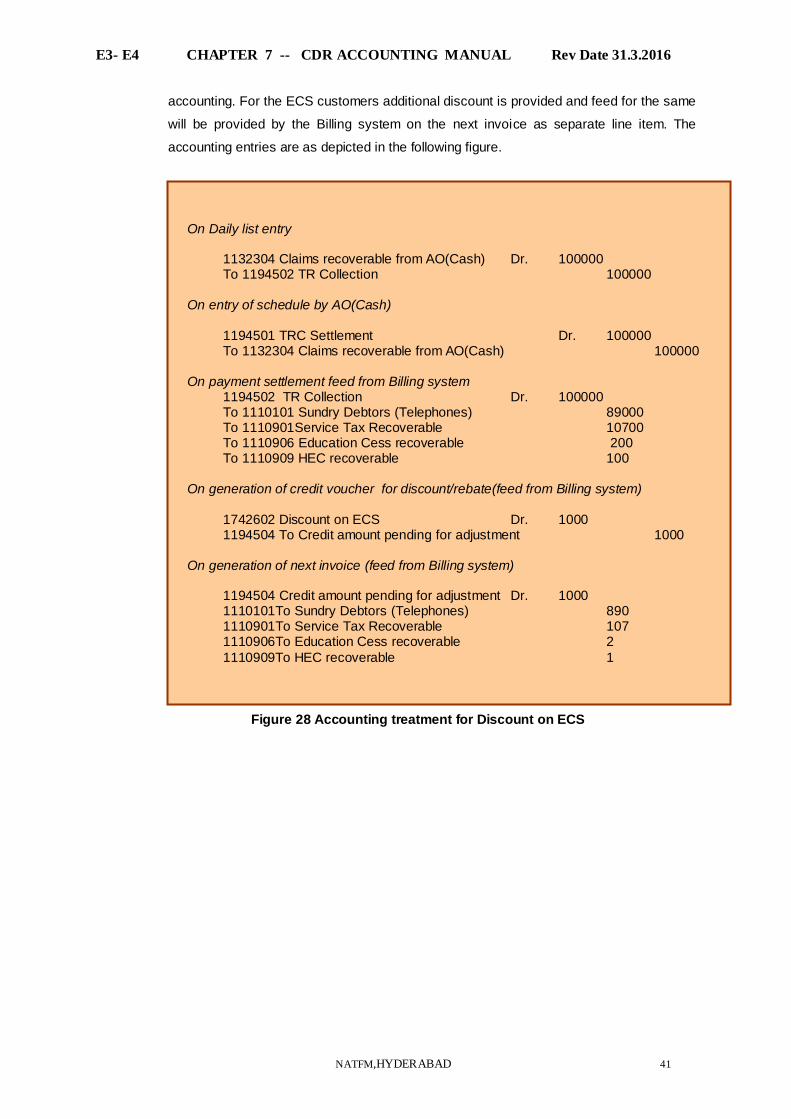

accounting. For the ECS customers additional discount is provided and feed for the same

will be provided by the Billing system on the next invoice as separate line item. The

accounting entries are as depicted in the following figure.

Figure 28 Accounting treatment for Discount on ECS

On Daily list entry 1132304 Claims recoverable from AO(Cash) Dr. 100000 To 1194502 TR Collection 100000 On entry of schedule by AO(Cash) 1194501 TRC Settlement Dr. 100000

To 1132304 Claims recoverable from AO(Cash) 100000 On payment settlement feed from Billing system 1194502 TR Collection Dr. 100000

To 1110101 Sundry Debtors (Telephones) 89000 To 1110901Service Tax Recoverable 10700 To 1110906 Education Cess recoverable 200 To 1110909 HEC recoverable 100

On generation of credit voucher for discount/rebate(feed from Billing system)

1742602 Discount on ECS Dr. 1000 1194504 To Credit amount pending for adjustment 1000

On generation of next invoice (feed from Billing system)

1194504 Credit amount pending for adjustment Dr. 1000 1110101To Sundry Debtors (Telephones) 890 1110901To Service Tax Recoverable 107 1110906To Education Cess recoverable 2

1110909To HEC recoverable 1

E3- E4 CHAPTER 7 -- CDR ACCOUNTING MANUAL Rev Date 31.3.2016

NATFM,HYDERABAD 42

e. Payments through Bill-desk: We are dealing with the collections made by "BILL DESK" payment aggregator in THREE

different ways.

1. Online Web based payments made by CDR system customers through the Web Self-Care

portal of the CDR system. This is online payment from the CDR system perspective in that

the invoice data is accessed by the portal directly from the CDR system and the payment

processing is done online without any manual intervention.

(This is under implementation stage)

2.Web based payments made by CDR customers through BSNL All India Portal. This is

NOT an online payment from the CDR system perspective since the invoice or payment data