43

1 1 Business Valuation

11

Business Valuation

22

Learning ObjectivesLearning Objectives

Understand the importance of business Understand the importance of business valuation.valuation.Understand the importance of stock and bond Understand the importance of stock and bond valuation.valuation.Learn to compute the value and yield to Learn to compute the value and yield to maturity of bonds.maturity of bonds.Learn to compute the value and expected yield Learn to compute the value and expected yield on preferred stock and common stock. on preferred stock and common stock. Learn to compute the value of a complete Learn to compute the value of a complete business.business.

33

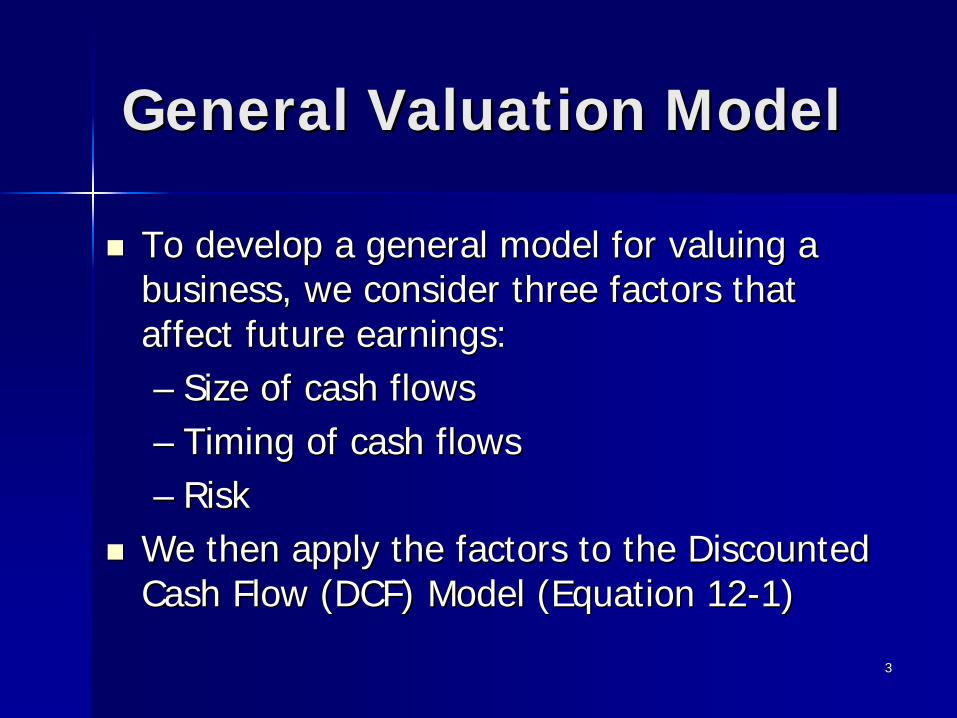

General Valuation ModelGeneral Valuation Model

To develop a general model for valuing a To develop a general model for valuing a business, we consider three factors that business, we consider three factors that affect future earnings:affect future earnings:–– Size of cash flowsSize of cash flows–– Timing of cash flowsTiming of cash flows–– RiskRisk

We then apply the factors to the Discounted We then apply the factors to the Discounted Cash Flow (DCF) Model (Equation 12Cash Flow (DCF) Model (Equation 12--1)1)

44

Bond Valuation ModelBond Valuation Model

Bond Valuation is an application of Bond Valuation is an application of time value model introduced in time value model introduced in chapter 8.chapter 8.The value of the bond is the present The value of the bond is the present value of the cash flows the investor value of the cash flows the investor expects to receive.expects to receive.What are the What are the cashflowscashflows from a bond from a bond investment?investment?

55

Bond Valuation ModelBond Valuation Model

3 Types of Cash Flows3 Types of Cash Flows–– Amount paid to buy the bond (PV)Amount paid to buy the bond (PV)–– Coupon interest payments made to the Coupon interest payments made to the

bondholders (PMT)bondholders (PMT)–– Repayment of Par value at end of BondRepayment of Par value at end of Bond’’s s

life (FV).life (FV).

66

Discount rate (I/YR)

Bond Valuation ModelBond Valuation Model

33 Types of Cash FlowsTypes of Cash Flows–– Amount paid to buy the bond (PV)Amount paid to buy the bond (PV)–– Coupon interest payments made to the Coupon interest payments made to the

bondholders (PMT)bondholders (PMT)–– Repayment of Par value at end of BondRepayment of Par value at end of Bond’’s s

life (FV).life (FV).

• Bond’s time to maturity (N)

77

Cur NetBonds Yld Vol Close Chg

AMR6¼24 cv 6 91¼ -1½ATT 8.35s25 8.3 110 102¾ +¼IBM 63/8 05 6.6 228 965/8 -1/8

Kroger 9s99 8.8 74 1017/8 -¼

IBM 63/8 09 6.6 228 965/8 -1/8

Link to Bondtrac Financial Information

IBM Bond Wall Street Journal Information:IBM Bond Wall Street Journal Information:

88

Suppose IBM makes annual coupon payments. The person who buys the bond at the beginning of 2009 for $966.25 will receive 5 annual coupon payments of $63.75 each and a $1,000 principal payment in 5 years (at the end of 2013). Assume t0 is the beginning of 2009.

Suppose IBM makes annual coupon payments. The person who buys the bond at the beginning of 2009 for $966.25 will receive 5 annual coupon payments of $63.75 each and a $1,000 principal payment in 5 years (at the end of 2013). Assume t0 is the beginning of 2009.

IBM Bond Wall Street Journal Information:IBM Bond Wall Street Journal Information:

Cur NetBonds Yld Vol Close Chg

AMR6¼24 cv 6 91¼ -1½ATT 8.35s25 8.3 110 102¾ +¼IBM 63/8 05 6.6 228 965/8 -1/8

Kroger 9s99 8.8 74 1017/8 -¼

IBM 63/8 13 6.6 228 965/8 -1/8

99

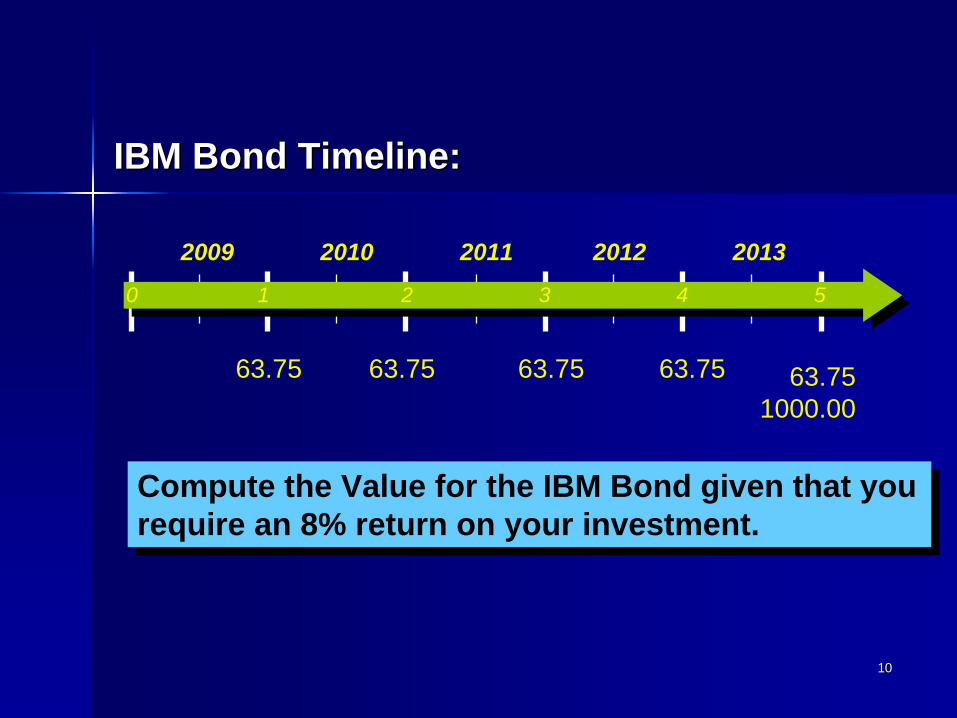

IBM Bond Timeline:IBM Bond Timeline:

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

Suppose IBM makes annual coupon payments. The person who buys the bond at the beginning of 2009 for $966.25 will receive 5 annual coupon payments of $63.75 each and a $1,000 principal payment in 5 years (at the end of 2013).

Suppose IBM makes annual coupon payments. The person who buys the bond at the beginning of 2009 for $966.25 will receive 5 annual coupon payments of $63.75 each and a $1,000 principal payment in 5 years (at the end of 2013).

Cur NetBonds Yld Vol Close Chg

AMR6¼24 cv 6 91¼ -1½ATT 8.35s25 8.3 110 102¾ +¼IBM 63/8 05 6.6 228 965/8 -1/8

Kroger 9s99 8.8 74 1017/8 -¼

IBM 63/8 13 6.6 228 965/8 -1/8

1010

Compute the Value for the IBM Bond given that you require an 8% return on your investment. Compute the Value for the IBM Bond given that you require an 8% return on your investment.

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

IBM Bond Timeline:IBM Bond Timeline:

1111

$63.75 Annuity for 5 years$63.75 Annuity for 5 years

VB = (INT x PVIFAk,n ) + (M x PVIFk,n )

$1000 Lump Sum in 5 years$1000 Lump Sum in 5 years

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

IBM Bond Timeline:IBM Bond Timeline:

1212

VB = (INT x PVIFAk,n ) + (M x PVIFk,n )= 63.75(3.9927) + 1000(.6806)= 254.53 + 680.60 = 935.13

$63.75 Annuity for 5 years$63.75 Annuity for 5 years $1000 Lump Sum in 5 year$1000 Lump Sum in 5 years

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

IBM Bond Timeline:IBM Bond Timeline:

1313

.01 rounding difference

N I/YR PV PMT FV

––935.12935.12

5 8 ? 63.75 1,000

IBM Bond Timeline:IBM Bond Timeline:

$63.75 Annuity for 5 years$63.75 Annuity for 5 years

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

$1000 Lump Sum in 5 years$1000 Lump Sum in 5 years

1414

Most Bonds Pay Interest SemiMost Bonds Pay Interest Semi--Annually:Annually:

e.g. semiannual coupon bond with 5 years to maturity, 9% annual coupon rate.

Instead of 5 annual payments of $90, the bondholder receives 10 semiannual payments of $45.

0 1 2 3 4 5

2009 2010 2011 2012 2013

45 45.001000.00

45 45 45 45 45 45 45 45

1515

Compute the value of the bond given that you require a 10% return on your investment.Compute the value of the bond given that you require a 10% return on your investment.

Since interest is received every 6 months, we need to usesemiannual compounding

VB = 45( PVIFA10 periods,5% ) + 1000(PVIF10 periods, 5% )

10%2

10%2

Semi-AnnualCompounding

Most Bonds Pay Interest SemiMost Bonds Pay Interest Semi--Annually:Annually:

0 1 2 3 4 5

2009 2010 2011 2012 2013

45 45.001000.00

45 45 45 45 45 45 45 45

1616

Most Bonds Pay Interest SemiMost Bonds Pay Interest Semi--Annually:Annually:

= 45(7.7217) + 1000(.6139)= 347.48 + 613.90 = 961.38

Compute the value of the bond given that you require a 10% return on your investment.Compute the value of the bond given that you require a 10% return on your investment.

Since interest is received every 6 months, we need to usesemiannual compounding

VB = 45( PVIFA10 periods,5% ) + 1000(PVIF10 periods, 5% )

0 1 2 3 4 5

2009 2010 2011 2012 2013

45 45.001000.00

45 45 45 45 45 45 45 45

1717

Calculator Solution:

N I/YR PV PMT FV

––961.38961.38

10 5 ? 45 1,000

0 1 2 3 4 5

2009 2010 2011 2012 2013

45 45.001000.00

45 45 45 45 45 45 45 45

1818

Yield to MaturityYield to MaturityIf an investor purchases a 6.375% annual If an investor purchases a 6.375% annual coupon bond today for $966.25 and holds it coupon bond today for $966.25 and holds it until maturity (5 years), what is the expected until maturity (5 years), what is the expected annual rate of return ? annual rate of return ?

-966.25

??

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.75

1000.00

+ ??

966.25966.25

1919

Yield to MaturityYield to Maturity

VVBB = 63.75(PVIFA= 63.75(PVIFA5, x%5, x% ) + 1000(PVIF) + 1000(PVIF5,x%5,x% ))Solve by trial and error.Solve by trial and error.

• If an investor purchases a 6.375% annual coupon bond today for $966.25 and holds it until maturity (5 years), what is the expected annual rate of return ?

-966.25

??

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.75

1000.00

+ ??

966.25966.25

2020

Yield to MaturityYield to Maturity

Calculator Solution:

N I/YR PV PMT FV

7.203%7.203%

5 ? -966.25 63.75 1,000

-966.25

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

2121

If YTM > Coupon Rate bond Sells at a DISCOUNT

If YTM < Coupon Rate bond Sells at a PREMIUM

Yield to MaturityYield to Maturity

-966.25

0 1 2 3 4 5

2009 2010 2011 2012 2013

63.75 63.75 63.75 63.75 63.751000.00

2222

Interest Rate RiskInterest Rate Risk

Bond Prices fluctuate over TimeBond Prices fluctuate over Time–– As interest rates in the economy change, As interest rates in the economy change,

required rates on bonds will also change required rates on bonds will also change resulting in changing market prices.resulting in changing market prices.

Interest Rates VVBB

2323

• Bond Prices fluctuate over Time– As interest rates in the economy change,

required rates on bonds will also change resulting in changing market prices.

Interest Rates VVBB

Interest Rate RiskInterest Rate Risk

Interest Rates VVBB

2424

Valuing Preferred StockValuing Preferred Stock

P0 = Value of Preferred Stock

= PV of ALL dividends discounted at investor’s Required Rate of Return

52 Weeks Yld Vol NetHi Lo Stock Sym Div % PE 100s Hi Lo Close Chg

s 42½ 29 QuakerOats OAT 1.14 3.3 24 5067 35 34¼ 34¼ -¾s 36¼ 25 RJR Nabisco RN .08p ... 12 6263 29¾ 285/8 287/8 -¾

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

7¼ 5½ RJR Nab pfC .60 9.4 ... 2248 6½ 6¼ 63/8 -1/8

0 1 2 3 ∞

P0 =23.75 D1 =2.31 D2 =2.31 D3 =2.31 D∞ =2.31

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

2525

Valuing Preferred StockValuing Preferred Stock

P0 = + + +···2.31 (1+ kp )

2.31 (1+ kp )2

2.31 (1+ kp )3 ∞

52 Weeks Yld Vol NetHi Lo Stock Sym Div % PE 100s Hi Lo Close Chg

s 42½ 29 QuakerOats OAT 1.14 3.3 24 5067 35 34¼ 34¼ -¾s 36¼ 25 RJR Nabisco RN .08p ... 12 6263 29¾ 285/8 287/8 -¾

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

7¼ 5½ RJR Nab pfC .60 9.4 ... 2248 6½ 6¼ 63/8 -1/8

0 1 2 3 ∞

P0 =23.75 D1 =2.31 D2 =2.31 D3 =2.31 D∞ =2.31

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

2626

Valuing Preferred StockValuing Preferred Stock

P0 = Dpkp

= 2.31 .10

= $23.10

P0 = + + +···2.31 (1+ kp )

2.31 (1+ kp )2

2.31 (1+ kp )3 ∞

52 Weeks Yld Vol NetHi Lo Stock Sym Div % PE 100s Hi Lo Close Chg

s 42½ 29 QuakerOats OAT 1.14 3.3 24 5067 35 34¼ 34¼ -¾s 36¼ 25 RJR Nabisco RN .08p ... 12 6263 29¾ 285/8 287/8 -¾

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

7¼ 5½ RJR Nab pfC .60 9.4 ... 2248 6½ 6¼ 63/8 -1/8

0 1 2 3 ∞

P0 =23.75 D1 =2.31 D2 =2.31 D3 =2.31 D∞ =2.31

237/8 20 RJR Nab pfB 2.31 9.7 ... 966 24 235/8 23¾ ...

2727

Valuing Individual Shares Valuing Individual Shares of Common Stockof Common Stock

P0 = PV of ALL expected dividends discounted at investor’s Required Rate of Return

Not like Preferred Stock since D0 = D1 = D2 = D3 = DN , therefore the cash flows are no longer an annuity. Not like Preferred Stock since D0 = D1 = D2 = D3 = DN , therefore the cash flows are no longer an annuity.

P0 = + + +···∞D1(1+ ks )

D2(1+ ks )2

D3(1+ ks )3

D1 D2 D3P0 D∞

0 1 2 3 ∞

2828

Valuing Individual Shares Valuing Individual Shares of Common Stockof Common Stock

P0 = PV of ALL expected dividends discounted at investor’s Required Rate of Return

Investors do not know the values of D1 , D2 , .... , DN . The future dividends must be estimated.

Investors do not know the values of D1 , D2 , .... , DN . The future dividends must be estimated.

Link to Quote.com

D1 D2 D3P0 D∞

0 1 2 3 ∞

P0 = + + +···∞D1(1+ ks )

D2(1+ ks )2

D3(1+ ks )3

2929

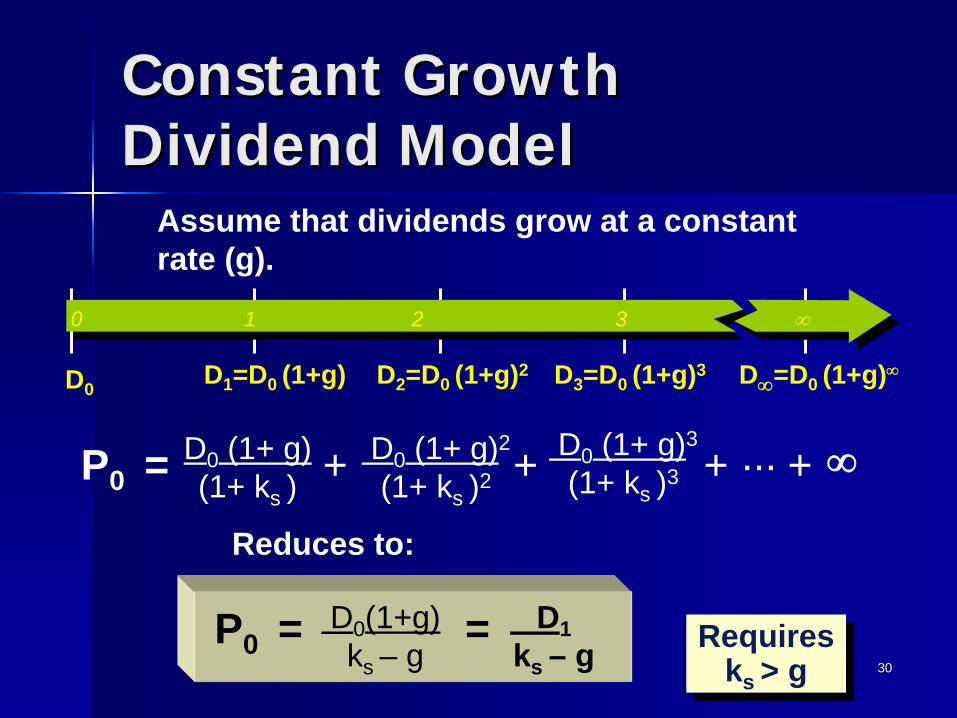

Assume that dividends grow at a constant rate (g).

D1 =D0 (1+g)D0 D2 =D0 (1+g)2 D3 =D0 (1+g)3 D∞=D0 (1+g)∞

0 1 2 3 ∞

Constant Growth Constant Growth Dividend ModelDividend Model

3030Requires

ks > g Requires

ks > g

Reduces to:

P0 = + + + ··· + D0 (1+ g)(1+ ks )

D0 (1+ g)2

(1+ ks )2D0 (1+ g)3

(1+ ks )3 ∞

P0 = =D0 (1+g) ks – g

D1ks – g

Assume that dividends grow at a constant rate (g).

D1 =D0 (1+g)D0 D2 =D0 (1+g)2 D3 =D0 (1+g)3 D∞=D0 (1+g)∞

0 1 2 3 ∞

Constant Growth Constant Growth Dividend ModelDividend Model

3131

P0 = = $30.50 1.14(1+.07) .11 – .07

What is the value of a share of common stock if themost recently paid dividend (D0 ) was $1.14 per share anddividends are expected to grow at a rate of 7%?Assume that you require a rate of return of 11% on this investment.

P0 = =D0 (1+g) ks – g

D1ks – g

Constant Growth Constant Growth Dividend ModelDividend Model

3232

Valuing Total Valuing Total StockholdersStockholders’’ EquityEquity

The Free Cash Flow DCF ModelThe Free Cash Flow DCF Model–– Free Cash Flow is the amount that is Free Cash Flow is the amount that is

““freefree”” to be distributed to debt holders, to be distributed to debt holders, preferred stockholders and common preferred stockholders and common stockholders.stockholders.

–– Cash remaining after accounting for Cash remaining after accounting for expenses, taxes, capital expenditures expenses, taxes, capital expenditures and new net working capital.and new net working capital.

3333

Calculating Free Cash Flow Calculating Free Cash Flow

Calculating Free Cash Flow:Calculating Free Cash Flow:Cash Revenue Cash Revenue -- Cash Expense = EBITDA Cash Expense = EBITDA **EBITDA (Earnings Before Interest, Taxes, Depreciation and **EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization)Amortization)

EBITDA EBITDA –– Depreciation Depreciation -- Amortization = EBITAmortization = EBIT**EBIT (Earnings Before Interest, and Taxes)**EBIT (Earnings Before Interest, and Taxes)

EBIT EBIT –– Federal and State Income Tax = NOPATFederal and State Income Tax = NOPAT**NOPAT (Net Operating Profit After Taxes)**NOPAT (Net Operating Profit After Taxes)

NOPAT + Depreciation + Amortization NOPAT + Depreciation + Amortization –– Capital Expenditures Capital Expenditures –– New Net Working Capital = New Net Working Capital = FREE CASH FLOWFREE CASH FLOW

3434

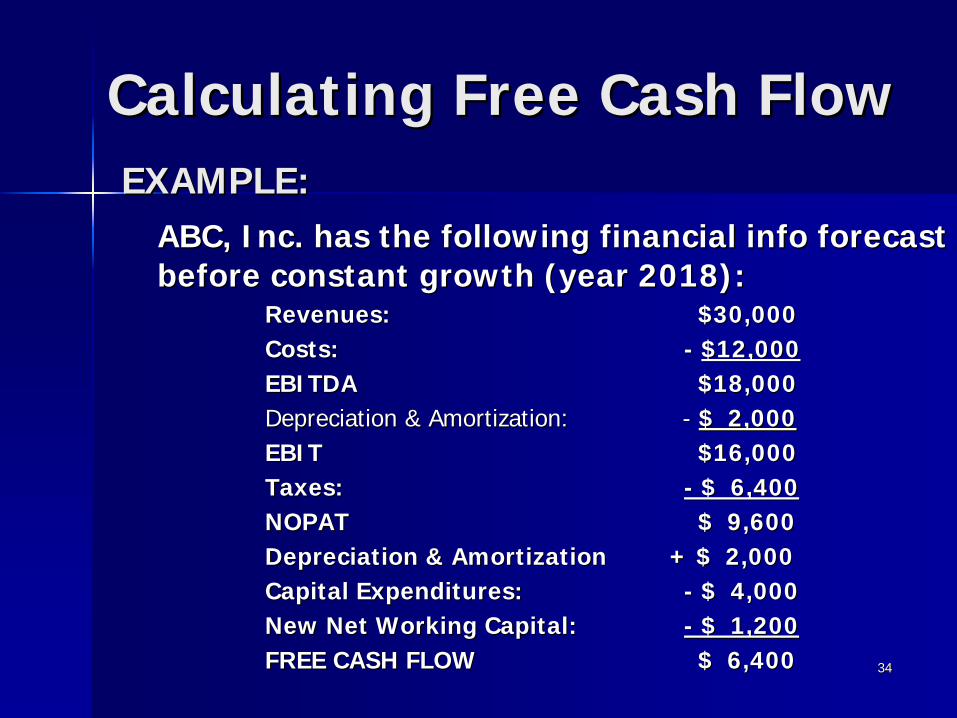

Calculating Free Cash FlowCalculating Free Cash FlowEXAMPLE:EXAMPLE:

ABC, Inc. has the following financial info forecast ABC, Inc. has the following financial info forecast before constant growth (year 2018):before constant growth (year 2018):

Revenues: Revenues: $30,000$30,000Costs:Costs: -- $12,000$12,000EBITDAEBITDA $18,000$18,000Depreciation & Amortization: Depreciation & Amortization: -- $ 2,000$ 2,000EBITEBIT $16,000$16,000Taxes:Taxes: -- $ 6,400$ 6,400NOPATNOPAT $ 9,600$ 9,600Depreciation & Amortization + $ 2,000Depreciation & Amortization + $ 2,000Capital Expenditures:Capital Expenditures: -- $ 4,000$ 4,000New Net Working Capital:New Net Working Capital: -- $ 1,200$ 1,200FREE CASH FLOWFREE CASH FLOW $ 6,400$ 6,400

3535

Step 1Step 1-- Calculate PV of free cash flows in Calculate PV of free cash flows in each year up to terminal value point in time.each year up to terminal value point in time.Example:Example:Free Cash Flows for ABC, Inc.Free Cash Flows for ABC, Inc.Assume tAssume t00 = 2009 and k = 10%= 2009 and k = 10%

2009: (500) 2009: (500) 2014: 3,200 2014: 3,200 2010: 1,2002010: 1,200 2015: 4,300 2015: 4,300 2011: 1,900 2011: 1,900 2016: 5,1002016: 5,1002012: 2,100 2012: 2,100 2017: 5,8002017: 5,8002013: 2,500 2013: 2,500 2018: 6,400 2018: 6,400

The Free Cash Flow DCF ModelThe Free Cash Flow DCF Model

3636

Example (cont):Example (cont):PV of Free Cash Flows for ABC, Inc.PV of Free Cash Flows for ABC, Inc.

2009: (500) 2009: (500) 2014: 1,987 2014: 1,987 2010: 1,0912010: 1,091 2015: 2,427 2015: 2,427 2011: 1,570 2011: 1,570 2016: 2,6172016: 2,6172012: 1,578 2012: 1,578 2017: 2,7062017: 2,7062013: 1,708 2013: 1,708 2018: 2,7142018: 2,714

The Free Cash Flow DCF ModelThe Free Cash Flow DCF Model

3737

Terminal ValueTerminal ValueForecasts free cash flows once company is Forecasts free cash flows once company is expected to grow at a constant rate.expected to grow at a constant rate.

Vfcf t =FCFt (1 + g)

k - gVfcf t = the value of future free cash flows at time t

FCFt = free cash flow at time t

k = the discount rate

g = the long term constant growth rate of free cash flows

3838

Terminal ValueTerminal ValueEXAMPLEEXAMPLE

TV2018 = $6,400 (1 +.05)

.10 - .05

ABC, Inc. has free cash flow of $6,400. The discount rate is 10% and they are expected to have a constant growth rate of 5%.

TV2018 = $6,720 / .05 = $134,400

PV2009 = $134,400 / (1+.10)9 = $56,999

3939

Example (cont):Example (cont):Step 2 Step 2 -- Add PV of Cash Flows to get PV of current Add PV of Cash Flows to get PV of current operations:operations:

(500) + 1,091 + 1,570 + 1,578 + 1,708 + 1,987 + (500) + 1,091 + 1,570 + 1,578 + 1,708 + 1,987 + 2,427 + 2,617 + 2,706 + 2,714 + 56,999 =2,427 + 2,617 + 2,706 + 2,714 + 56,999 =

The Free Cash Flow DCF ModelThe Free Cash Flow DCF Model

$74,897

4040

Total PV of Company operationsTotal PV of Company operations $74,897$74,897Plus current assetsPlus current assets 50,00050,000Less Current LiabilitiesLess Current Liabilities 3,5003,500Less Long Term DebtLess Long Term Debt 2,0002,000Less Preferred StockLess Preferred Stock 00Net Market Value of Common Equity $119,397Net Market Value of Common Equity $119,397

Example (cont):Step 3 - Calculate market value of common equity

The Free Cash Flow DCF ModelThe Free Cash Flow DCF Model

4141

Yield, or Total Return on Yield, or Total Return on Common StockCommon Stock

ks = D0 (1+g) P0

+ g

What is the yield on stock when D0 = .08, g=.20, and current price (P0 ) = $28.875

Link to Financial Web

Link to Yahoo Finance

4242

Yield, or Total Return on Yield, or Total Return on Common StockCommon Stock

ks = .08(1+.2) 28.875 + .20

= .0033 + 0.20

= 20.33%

ks = D0 (1+g) P0

+ g

What is the yield on stock when D0 = .08, g=.20, and current price (P0 ) = 28.875

4343

Valuing Complete BusinessesValuing Complete Businesses

The Free Cash Flow DCF Model Applied The Free Cash Flow DCF Model Applied to a Complete Business:to a Complete Business:Example, for ABC:Example, for ABC:Total PV of Company Total PV of Company

operations...$74,897operations...$74,897Plus current assets.......................... Plus current assets..........................

50,00050,000= Complete Business Value of = Complete Business Value of ABC..$124,897ABC..$124,897