41

Chapter 9 Fundamental Legal Principles

| Date post: | 06-Dec-2015 |

| Category: |

Documents |

| View: | 242 times |

| Download: | 0 times |

Chapter 9

Fundamental Legal Principles

5-2

Outcome

Understand, and be able to apply below principles to insurance contracts

• Principle of Indemnity• Principle of Insurable Interest• Principle of Subrogation• Principle of Utmost Good Faith• Requirements of an Insurance Contract• Distinct Legal Characteristics of Insurance

Contracts• Law and the Insurance Agent

5-3

Principle of IndemnityThe insurer agrees to pay no more than the

actual amount of the loss• Specifies how much one can collect• Purpose:

Q: What would happen if you could insure other people or their property, and when the loss occurs, you could collect the loss?

5-4

Principle of Indemnity

• In property insurance, indemnification is based on the ____________of the property at the time of loss– "actual cash value" is not as easily defined. Some

courts have interpreted the term to mean "fair market value,"

• There are three main methods to determine actual cash value:– Replacement cost less depreciation– Fair market value is the price a willing buyer would

pay a willing seller in a free market– Broad evidence rule means that the determination of

ACV should include all relevant factors an expert would use to determine the value of the property

5-5

Actual Cash Value = Replacement Cost Less Depreciation

ACVloss = [RCloss - DEPloss]

RC = the cost to repair or replace with like kind and quality of materialloss = calculation is performed only on the part that was damagedDEP = A measure of “betterment” Not an accounting concept

Principle of IndemnityActual Cash Value

Q: Can you think of any example that RC or Dep. cost does not make sense?

5-6

ACV calculation

• Purchase price of an old iphone: $4,000• Expected useful life: 4 years• iphone destroyed after 1 year• Current price of similar iphone : $2,800

Q: What is the ACV?

5-7

Scenario• You have a claim to repair an engine that damaged by

water due to flooding in your area. A used engine from the same model year cannot be found. The insurance company says to rebuild the engine a betterment charge will be assessed. – Is it fair?

• Q: Does the case apply to the ACV concept we just learned?• If your automobile is being repaired with newer engine or

parts, your insurance company doesn't have to pay for the _________For example, if your automobile's engine is 8 years old, your insurance company would have to replace it with a _____ old engine. If it cannot be found, a new engine has to be used, but you'd ____ to pay the difference. Of course you can choose not to repair the engine.

5-8

Principle of Indemnity• There are some exceptions to the principle of

indemnity:– A ________pays the face amount of insurance if a

total loss occurs

– Some states have a valued policy law that requires payment of the face amount of insurance to the insured if a total loss to real property occurs from a peril specified in the law• The law forces an insurer to pay the face

amount of the contract when there is a total loss.

5-9

Principle of Indemnity– Replacement cost insurance means there is no

deduction for depreciation in determining the amount paid for a loss• E.g. it would cost HKD2 million to replace your

house and it is insured for HKD1.8 million (80 percent of its replacement value)

• a fire causes HKD200,000 worth of damage, then insurance firm will pay you the full amount of HKD200,000.

– A life insurance contract is a valued policy that pays a stated sum to the beneficiary upon the insured’s death

Q: An antique painting, with insurance, is destroyed in a fire. Should we use ACV for indemnity calculation?

5-10

Principle of Insurable InterestThe insured must stand to __________if a loss occurs

• Specifies who can collect from an insurance contract

• Purpose:

Can I buy a life insurance insuring your life?

• When must insurable interest exist?– Property insurance: at the time of the loss– Life insurance: only at inception of the policy

Let’s read Insurable interest reading.docx

5-11

Corporation Lacking Insurable Interest at Time of Death

• A corporation purchases a $1 million life insurance policy on an officer who was a 20% stockholder in the company. Shortly thereafter, the officer sold his stock and resigned. Two years later he died but the policy owned by the corporation is still in force. The insurer paid the death benefits to the corporation. The deceased insured’s son claimed the corporation’s insurable interest was only temporary. So the son claimed that he, but not the corporation, is entitled to the death benefits.

• Who is entitled for the policy proceeds?

How about those corp. laying off thousands (e.g. Citibank 2008) Or you have worked for a number of companies having life insurance for their employees.Crime?

5-12

Insurable interest

• You have a life insurance contract for your spouse. Even if you were no longer married to that person at the time of their death, the insurance policy would likely still be ???

• Soln: Beneficiaries named as “_________ beneficiaries" => they no longer receive insurance proceeds if an insurable interest is not present at the time the policy proceeds become payable.

5-13

House with insurance sold• You sold a house that would have still been covered by

insurance if you hadn't sold it,• The house was destroyed by a fire after the sale .

Take out a piece of paper and answer the following questions

• Does your insurance company have to pay you? Why? • Does your insurance company have to pay the new

owner? Why?

5-14

Principle of Subrogation

Substitution of the insurer in place of the insured for the purpose of claiming indemnity from a third person for a loss covered by insurance.

• Provides rules as to what happens if the insurer pays you for your loss caused by a negligent party

• Purpose:

It helps speed up the collection process too.

5-15

Principle of Subrogation

• the injured is reimbursed by the insurer• the insurer is substituted for the injured and obtains the

rights of recovery to the amount that it was paid for • if injured gets $9000 after paying the $1000 deductible while the

insurers recovers $10000, the insurer has to pay the injured $1000

Insurerpays

InjuredInsured

Negligentparty

Subrogates againstnegligent party

5-16

Principle of SubrogationPrinciple of Subrogation

Insured has $10,000 loss andrecovers $7,000from insurer

Insurer pays$8,000 less $1,000Deductible

Negligent Partypays $5,000

subrogates

injury

$3,000 to insured$2,000 to insurer

5-17

Principle of Subrogation

• The insurer is entitled only to the amount it has paid under the policy

• The insured cannot impair the insurer’s subrogation rights

• Subrogation does not apply to life insurance and to most individual health insurance contracts– any examples?

• The insurer cannot subrogate against its own insureds

• Subrogation does not exist where the principle of indemnity does not apply –

5-18

Principle of Utmost Good FaithA higher degree of honesty is imposed on both

parties to an insurance contract than is imposed on parties to other contracts

• Provides guidance for when a party breaches the Utmost Good Faith standard.

• Supported by three legal doctrines:– _____________ are statements made by the applicant for

insurance– A concealment is intentional failure of the applicant for

insurance to reveal a material fact to the insurer– A warranty is a statement that becomes part of the

insurance contract and is guaranteed by the maker to be true in all respects

• Statements made by applicants are considered representations, not warranties. So insurer cannot deny liability for a claim if a misrepresentation is not material.

5-19

Example: A warranty in an insurance policy is a promise by the insured party that statements affecting the legality of the contract are true. Most insurance contracts require the insured to make certain warranties.

Health Insurance policy: an insured party may have to warrant that he does not suffer from a terminal disease. If the warranty is violated, the insurer may cancel the policy or refuse to cover claims. Let’s refer to “A warranty in an insurance policy.doc”

5-20

Representations• Statements made before a contract starts to induce a

party to enter the contract

– Oral or written statements

• A contract is voidable if the representation is material, false, and relied on by the insurer

• An innocent misrepresentation of a material fact, if relied on by the insurer, makes the contract voidable– Do you think it is fair?

5-21

• Material Misrepresentation Tests– False - not true at the time of the statement– Material - would the insurer have declined

the contract, changed the wording, or priced it differently if the truth were known

• Example: Gender-material?

• Statement of opinions are not sufficient to avoid the contract– a person stated that he was free of cancer

– this was the truth to the best of her knowledge

– later it was found that (undiagnosed) cancer had been present for three years this would be an opinion because there was no ___________ involved.

Material Misrepresentations

5-22

In class exercise

• misrepresentation in class exercise.doc

5-23

• Silence when there is an obligation to speak

• Utmost good faith imposes a duty to voluntarily disclose material information

• When a material fact is concealed the insurer cannot avoid the contract

• Generally involves an element of deception

Principle of Utmost Good Faith Concealments

5-24

Element of deception?• Did the insured know of a certain fact?• Was the fact material?• Was the insurer ignorant of the fact?

Tests for Concealment

5-25

Warranties

• A warranty creates a condition in a contract• Any breach of warranty, even if not

material, will allow the insurer to avoid the contract (strict interpretation), but modifications were made.

5-26

Types of Warranties

• Express - written• Implied - not written, understood by all• Promissory - condition to continue

throughout contract period• Affirmative - exists at contract’s inception;

promises nothing about the future

5-27

Warranties - Examples

• Express affirmative

• Express promissory

• Implied affirmative

– Seaworthiness

• The ability of a ship (or other vessel, liner container, etc.) to make a sea voyage with probable safety: there is, in every insurance, whether on ship or goods, an implied warranty that the ship shall be worthy when she sails on the voyage insured

• Implied promissory– Legality e.g.

5-28

• Commonly referred to as a ‘bad faith claim’

• Used when the insured feels the insurer is not acting in ‘good faith’ and dealing fairly

• Used to force insurance companies to perform according to the contract

Breach of Utmost Good Faith

What if staff got extra bonus of rejecting a claim.

5-29

The duty of the utmost good faith• It requires insurers to act with due regard to the

insured's interests in situations where there is a conflict of interest. – E.g. The insurer must disclose any relevant policy terms that

have major consequences (such as denial of claims).– E.g. Insurer must not misrepresent facts about the policy

• an agent explains a promise in the policy of a benefit that’s being provided, and the representation is more explicit than what the policy stated

– E.g. Insurer must draft its policies in clear, plain English so that the policy can be easily understood by the insured.

– E.g.decline claims only with reasonable evidence or belief

• It also requires the insured to act honestly when dealing with the insurer.

5-30

Requirements of an Insurance Contract

• To be legally enforceable, an insurance contract must meet four requirements:– Offer and acceptance of the terms of the

contract• contract law: to determine whether an agreement

exists between two parties.

– Consideration – the values that each party exchange

– Legally competent parties, with legal capacity to enter into a binding contract

– The contract must exist for a legal purpose

5-31

Distinct Legal Characteristics of Insurance Contracts

• Aleatory: values exchanged are not equal

• Unilateral: only the insurer makes a legally enforceable promise

• Conditional: policyowner must comply with all policy provisions to collect for a covered loss

• Personal: property insurance policy cannot be validly assigned to another party without the insurer's consent

• Contract of adhesion: since the insured must accept the entire contract as it is written, any ambiguities are construed against the insurer

5-32

Law and the Insurance Agent• An agent is someone who has the authority to act

on behalf of a principal (the insurer)• Several laws govern the actions of agents and their

relationship to insureds– There is no presumption of an agency relationship– An agent must be authorized to represent the

principal• Authority is either express, implied, or apparent

– Knowledge of the agent is presumed to be knowledge of the principal with respect to matters within the scope of the agency relationship

– Insurers can place limitations on the power of agents by adding a nonwaiver clause to the application or policy

5-33

Law and the Insurance Agent

• Waiver is defined as the voluntary relinquishment of a known legal right

• Estoppel occurs when a representation of fact made by one person to another person is reasonably relied on by that person to such an extent that it would be inequitable to allow the first person to deny the truth of the representation

5-34

Estoppel

• Dictionary.com: a bar or impediment preventing a party from asserting a fact or a claim inconsistent with a position that party previously took, either by conduct or words, especially where a representation has been relied or acted upon by others.

• In other words, Estoppel prevents a person or organization from adopting a position, action or attitude inconsistent with an earlier position if it would result in an injury to another person.

5-35

Estoppel

• Different than waiver. • Is a rule of fair play.

5-36

Another example

• Your insurance company knows that you are no longer disabled but

• it continues to pay you disability benefits,

Q: Waiver or Estoppel?

5-37

Case

• Insurance company frequently accept late payments from policyholders (may be due to auto-pay problems)

• Can the insurance company assert a policy’s cancellation provision against its policyholder?

5-38

Case• You apply for a life insurance of HK$ 2

million. You send out the filled application form together with a check for the premium today.

• You take a physical/medical examination two days later, then you go to sky diving and got killed.

• Does the insurer have to pay?– If you pass the medical examination and the

agent said that the effective date will be the date you signed the application form.

5-39

Waiver or Estoppel?

• You inform your agent about your health problem but the agent assures you that you do not have to state it in your application for medical insurance.

• The insurer cannot deny your claim on the grounds that you did not include this information.

5-40

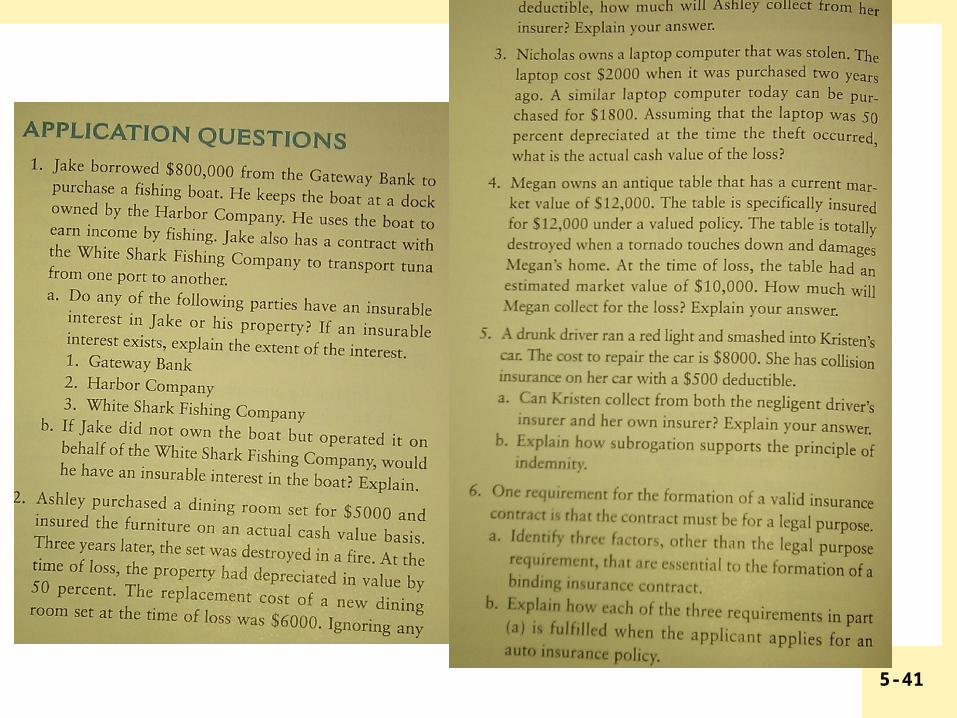

Exercises

• How does the concept of actual cash value support the principle of indemnity?

• What is a valued policy?• Why is valued policy used?• What is insurable interest?• Why is insurable interest required in

insurance contract?• What are the four requirements for a valid

insurance contract?• Application questions: 1, 3, 4,5 and 6 (p. 199)

5-41