41

CHAPTER Foreign Currency Transactions Fundamentals of Advanced Accounting 1 st Edition Fischer, Taylor, and Cheng 6 6

| Date post: | 03-Jan-2016 |

| Category: |

Documents |

| Upload: | julian-hamilton |

| View: | 218 times |

| Download: | 0 times |

CHAPTER

Foreign Currency Transactions

Fundamentals of Advanced Accounting 1st Edition

Fischer, Taylor, and Cheng

66

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #2

Foreign Currency Exchange Rates

• International monetary systems establish rates of exchange between currencies

• Exchange rate – a measure of how much of one currency can be exchanged for another

• Exchange rates may be quoted direct or indirect

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #3

Direct and Indirect quotes

• Quoted by a foreign currency trader

• Direct quote– How much domestic currency must be

exchanged to receive 1 unit of foreign currency (FC)

– Example: 1 FC = $.25

• Indirect quote– The reciprocal of a direct quote– Example: $1 = 4FC

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #4

Currency Strengthens or Weakens

Currency can “strengthen” or “weaken” against other currency

• Strengthens:– Reduction in a direct quote– Increase in an indirect quote– Domestic unit of currency demands more

FC

• Weakens: opposite– Domestic unit of currency will buy less FC

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #5

Buying and Selling Rates

• Exchange rates may differ depending on whether they are a buying (bid price) or selling (offered price) rate

• Buying/selling rates – what a broker will pay to buy a currency

• Difference between buy/sell rate is a “spread”– Broker’s commission

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #6

Two Primary Groups of Exchange Rates

• Spot rate – currency delivered, bought, sold within 2 business days

• Forward rate – exchange of currencies at a future point in time– Forward Contract: Agreement to

exchange currencies at a specific price at a specific time in the future

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #7

Forward and Spot Rates (continued)

• Both rates change constantly

• Spot rates are revised daily

• Changes in spot rates change forward rates

• At the end of a forward contract, the current forward rate becomes the spot rate– The value of a forward contract changes over

the forward period

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #8

Forward and Spot Rates (continued)

• At inception of a forward contract, the difference between a forward rate and the current spot rate represents:– A premium (forward > spot)– A discount (forward < spot)

• The difference also represents contract expense or income to the contract purchaser

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #9

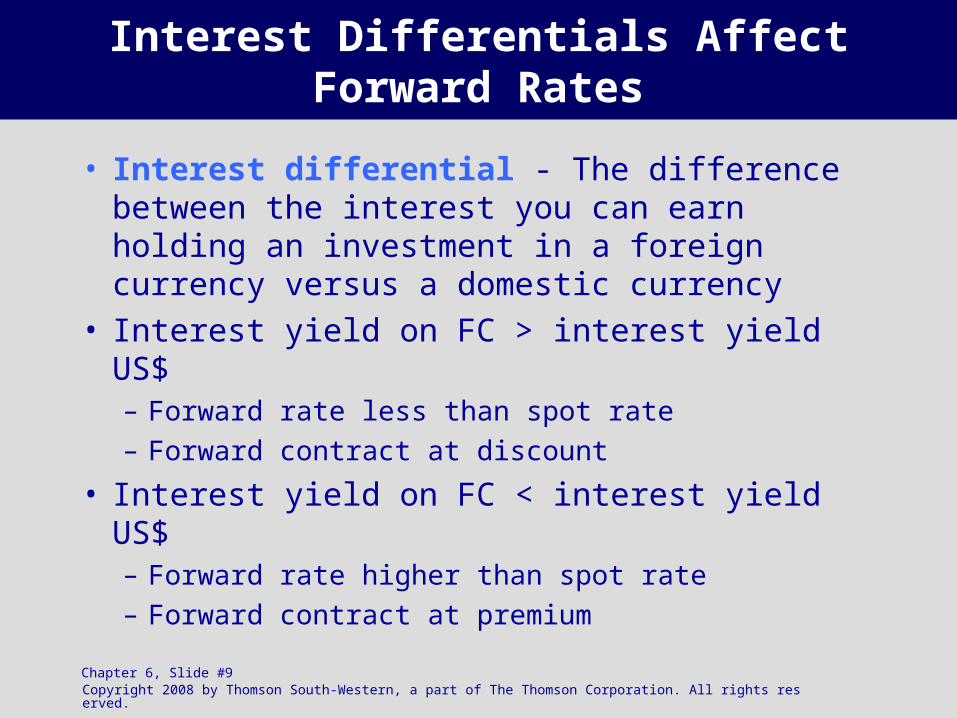

Interest Differentials Affect Forward Rates

• Interest differential - The difference between the interest you can earn holding an investment in a foreign currency versus a domestic currency

• Interest yield on FC > interest yield US$– Forward rate less than spot rate– Forward contract at discount

• Interest yield on FC < interest yield US$– Forward rate higher than spot rate– Forward contract at premium

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #10

Interest Differentials Affect Forward Rates

FactsSpot rate 1 FC = $.60Amount of FC to be sold 1,000 FCForward date 6 months forwardInterest rate on FC 7.25%Interest rate on $ 4.5%

Calculation of forward rate

US $ FC

Value today $600.00 FC 1,000.00Interest for 6 months $ 13.50 FC 36.25Value in 6 months $613.50 FC 1,036.25

Forward rate = $613.50 1036.25 FC = 1 FC = $0.592

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #11

Accounting for Foreign Currency Transactions

• Transactions are denominated in FC and measured in domestic currency

• Changes in exchange rates between the transaction date and the settlement date results in exchange gain or loss to reporting entity– Transactions both denominated and measured in

the reporting entity’s currency are not affected by changes in exchange rates

• If a FC transaction is unsettled at the end of the period, exchange gains/losses should be accrued

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #12

Foreign Currency Unsettled Transaction Example

11/1/X1Transaction

date

Spot Rate: 1 FC = $0.50 1 FC = $0.52 1 FC = $0.55

2/1/X2Settlement

date

Year-end12/31/X1

Journal entries for these dates follow . . .

•US Company purchases inventory on 11/1/20X1 for 1,000 FC.•Purchase to be paid on 2/1/20X2

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #13

Foreign Currency Unsettled Transaction Example (continued)

11/1 Inventory 500Accounts Payable 500

Purchase inventory; rate = $0.50

12/31 Exchange Loss 20Accounts Payable - FC 20

Fiscal year-end; rate = $0.52

2/1 Accounts Payable 500Exchange Loss 30

Cash 550Settlement date; rate = $0.55

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #14

Exposure to FC Exchange Risk

• Certain situations expose domestic companies to FC exchange risk– An existing FC transaction resulting in

recognition of assets or liabilities– A firm commitment to enter into a FC transaction– A forecasted FC transaction that has a high

probability of occurrence– Investment in a foreign subsidiary

• Strategies to hedge risk include derivatives

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #15

Derivatives Defined

• Financial instruments that derive their value from changes in the value of a related asset or liability

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #16

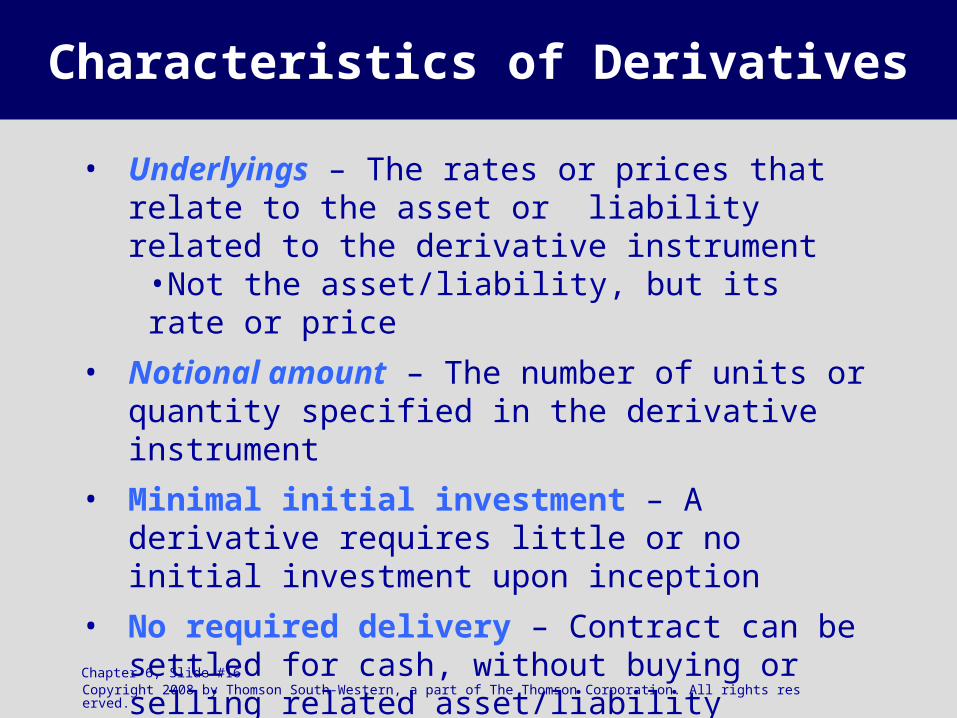

Characteristics of Derivatives

• Underlyings – The rates or prices that relate to the asset or liability related to the derivative instrument

•Not the asset/liability, but its rate or price

• Notional amount – The number of units or quantity specified in the derivative instrument

• Minimal initial investment – A derivative requires little or no initial investment upon inception

• No required delivery – Contract can be settled for cash, without buying or selling related asset/liability

Both the underlying price/rate AND the notional amounts are required to determine total value of the derivative at any point in time!

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #17

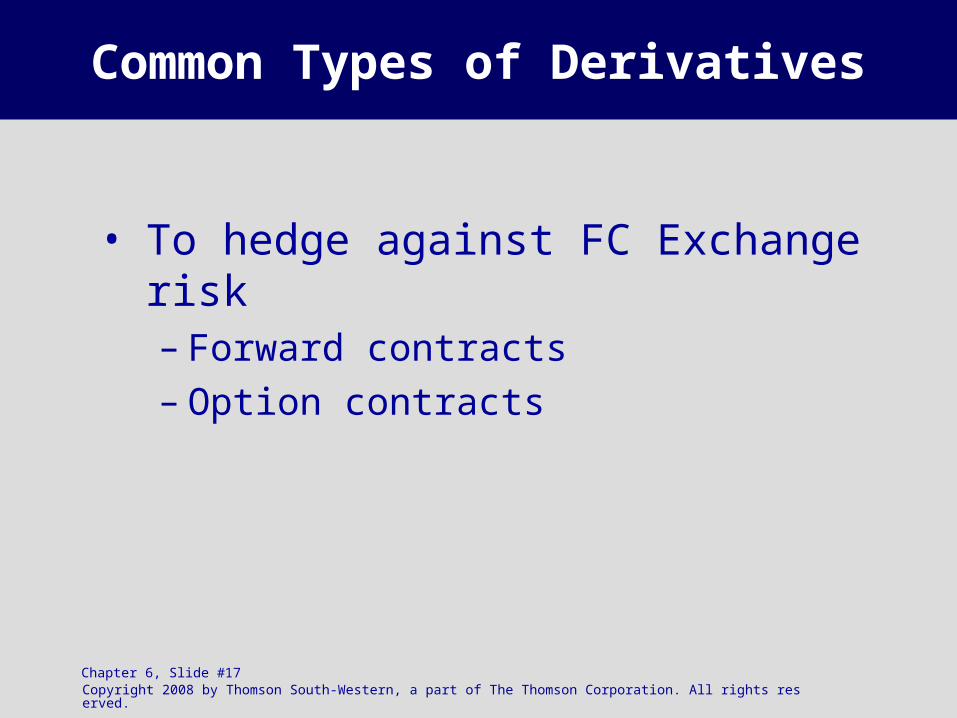

Common Types of Derivatives

• To hedge against FC Exchange risk– Forward contracts– Option contracts

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #18

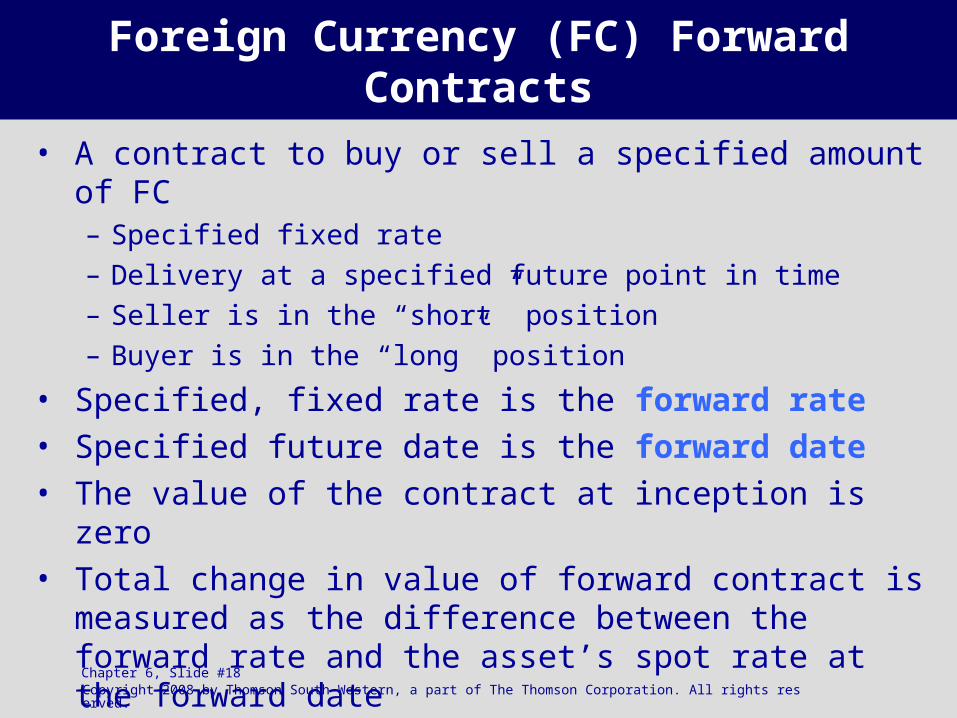

Foreign Currency (FC) Forward Contracts

• A contract to buy or sell a specified amount of FC – Specified fixed rate– Delivery at a specified future point in time– Seller is in the “short” position– Buyer is in the “long” position

• Specified, fixed rate is the forward rate• Specified future date is the forward date• The value of the contract at inception is zero• Total change in value of forward contract is

measured as the difference between the forward rate and the asset’s spot rate at the forward date

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #19

Example - FC Forward Contract

Writerof the

Contract(Seller)

Holderof the

Contract(Buyer)

Convey 1,000,000 FC in 90 days

Pay $160,000 in 90 days

FC at the forward rate in 90 days $ 160,000Assumed spot rate in 90 days 180,000Gain in value to holder $ 20,000

•On 4/1, seller agrees to provide buyer with 1,000,000 FC on 6/29 for $0.16 per FC.

•Assume a spot rate on 6/29 of $0.18

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #20

Measuring Changes in the Value of a Forward Contract Over Time

• Measure cumulative change in forward value of a contract• Difference between the original forward

value and the remaining forward value• The net present value of the change in

forward value consists of two components:• The change in the spot rates over time • The change in the time value of the

contract (spot – forward differences)

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #21

The Forward Rate

• A function of variables

• As variables change, the value of the forward contract changes

• Current value of the forward contract is determined by present value of future rates

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #22

Example: Change in Value of Forward Contract

Remaining Term of Contract

Forward Rate

Notional Amount

Total Forward

Value

Cumulative Change in Forward Volume

90 days $0.160 1,000,000 $160,00060 days $0.170 1,000,000 $170,000 $10,00030 days $0.170 1,000,000 $170,000 $10,0000 days $0.180 1,000,000 $180,000 $20,000

Assume a 6% discount rate – calculations on next slide

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #23

Example (continued): Change in Value of Forward Contract

60 Days 30 Days Total Life

Cumulative change in forward value $10,000 $10,000 $20,000

Present value of cumulative change:

60 days at 6% $9,901

30 days at 6% $9,950

0 days at 6% $20,000

Previously recognized gain/loss 0 (9,901) (9,950)

Current period gain/loss $9,901 $49 $10,050

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #24

FC Option Contracts

• Represent a right (not an obligation) to either buy or sell FC

• Valid for a specified period of time• Specified buy/sell price

– Referred to as the strike or exercise price – Strike price generally different from FC current value

• Call option – right to buy FC• Put option – right to sell FC• Holder pays nonrefundable cash outlay: premium

– Writer has more risk than holder

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #25

FC Option Contracts (continued)

• Holder will not exercise the option if strike price is greater than fair value– Loss is limited to premium paid at inception– Gain is unlimited

• Options traded on an organized exchange

• Current value quoted in terms of present value

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #26

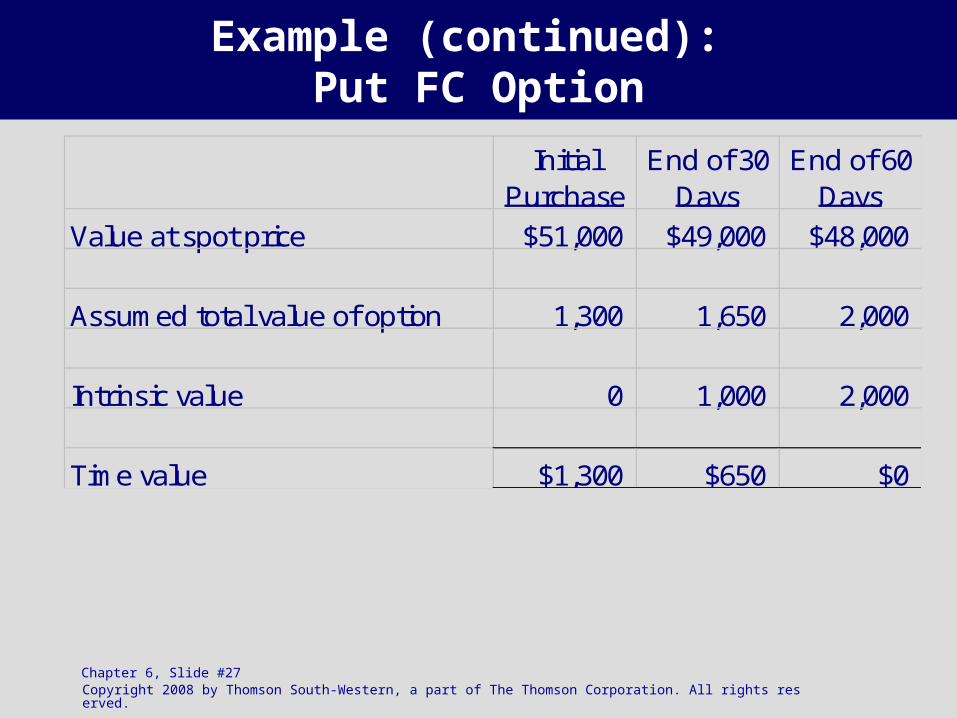

Example of a Put FC Option

OptionWriter

OptionHolder

Sell 100,000 FC @$0.50 per FC

Intrinsic value is the difference between the strike price and the market price

Time value is the value of the option less the intrinsic value

Calculations on next slide….

in 60 days

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #27

Example (continued): Put FC Option

Initial Purchase

End of 30 Days

End of 60 Days

Value at spot price $51,000 $49,000 $48,000

Assumed total value of option 1,300 1,650 2,000

Intrinsic value 0 1,000 2,000

Time value $1,300 $650 $0

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #28

Derivatives Designated as a Hedge

• Derivatives designated as a hedge are classified as

– fair value hedge

– cash flow hedge

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #29

Fair Value Hedges

• Used to offset changes in fair value of items with fixed exchange price or rates– Recognized FC asset or liability– Unrecognized FC firm commitment

• Prices or rates are fixed– Subsequent changes in the price or rates affect

the fair value

• The derivative instrument can be used as a hedge against exchange risk

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #30

Fair Value Hedges (continued)

• Fair value hedges receive special accounting treatment if certain criteria are satisfied– Formal documentation of the hedging

relationship– Ongoing assessment of hedge effectiveness – Other criteria must also be satisfied

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #31

Special Accounting Treatment for Fair Value Hedges

Special accounting treatment:• The gain or loss on the derivative instrument

is recognized currently in earnings• The gain or loss on the hedged item is also

recognized currently in earnings• Recognizing both changes in value in

current earnings gives recognition to the offsetting nature of the hedge

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #32

Special Accounting Treatment for Fair Value Hedges (continued)

Changes in the time value of a derivative are may be excluded from assessment of hedge effectiveness and recognized in current earnings

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #33

Cash Flow Hedges

• Used to establish fixed prices when future cash flows can vary due to changes in prices and rates.

• Include hedges against change in cash flows from:

– Forecasted FC transaction– Forecasted functional-currency-equivalent cash

flows associated with recognized asset/liability– Unrecognized FC firm commitment

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #34

Cash Flow Hedges (continued)

• Receive special accounting treatment if certain criteria are met– Formal documentation of the hedging relationship– Ongoing assessment of hedge effectiveness – Other criteria must also be satisfied

• Effective portion of gain/loss recognized in other comprehensive income (OCI).

• Ineffective portion recognized in current earnings

• Amounts reported in OCI will be transferred to current earnings in the same period that the hedged item affects earnings

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #35

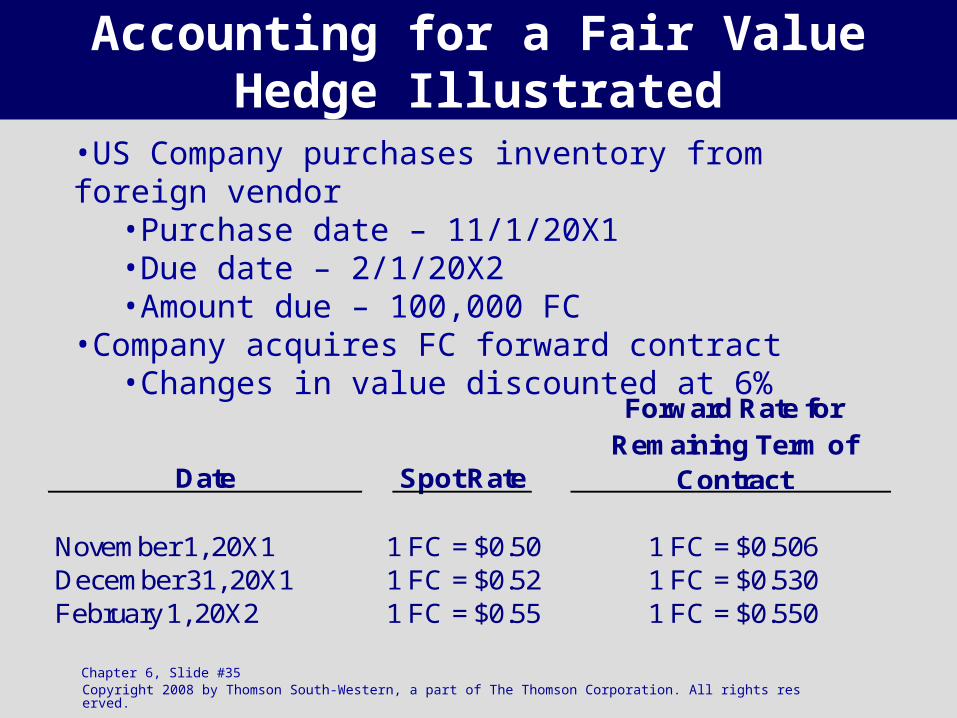

Accounting for a Fair Value Hedge Illustrated

•US Company purchases inventory from foreign vendor•Purchase date – 11/1/20X1•Due date – 2/1/20X2•Amount due – 100,000 FC

•Company acquires FC forward contract•Changes in value discounted at 6%

Date Spot Rate

Forward Rate for Remaining Term of

Contract

November 1, 20X1 1 FC = $0.50 1 FC = $0.506December 31, 20X1 1 FC = $0.52 1 FC = $0.530February 1, 20X2 1 FC = $0.55 1 FC = $0.550

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #36

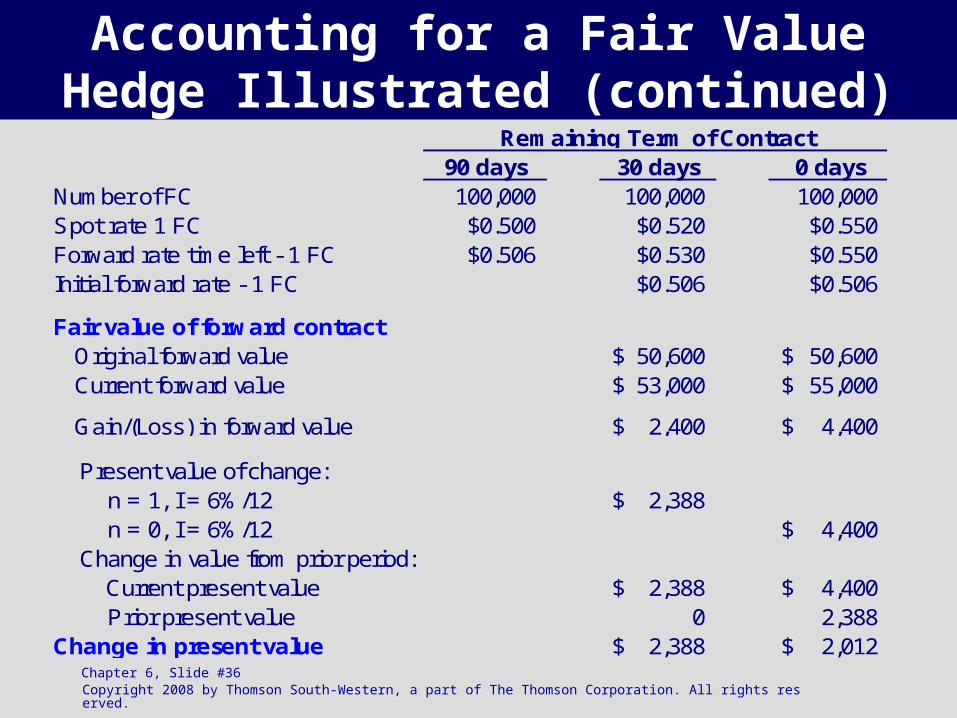

Accounting for a Fair Value Hedge Illustrated (continued)

90 days 30 days 0 daysNumber of FC 100,000 100,000 100,000 Spot rate 1 FC $0.500 $0.520 $0.550Forward rate time left - 1 FC $0.506 $0.530 $0.550Initial forward rate - 1 FC $0.506 $0.506

Fair value of forward contract Original forward value 50,600$ 50,600$ Current forward value 53,000$ 55,000$

Gain/(Loss) in forward value 2,400$ 4,400$

Present value of change: n = 1, I = 6%/12 2,388$ n = 0, I = 6%/12 4,400$ Change in value from prior period:

Current present value 2,388$ 4,400$ Prior present value 0 2,388

Change in present value 2,388$ 2,012$

Remaining Term of Contract

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #37

Assessing the Effectiveness of a Fair Value Hedge

Without the With the Hedge Hedge

Hedging gain (loss) on contract 4,400$ Exchange loss on FC asset/liability (5,000) (5,000)Net effect on earings (5,000)$ (600)$

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #38

Journal entries – 11/1/20X1

Inventory 50,000

Accounts payable – FC50,000

(to record purchase of inventory)

Forward contract receivable - FC 50,000

Forward contract payable - $50,600

(to record purchase of FC forward contract)

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #39

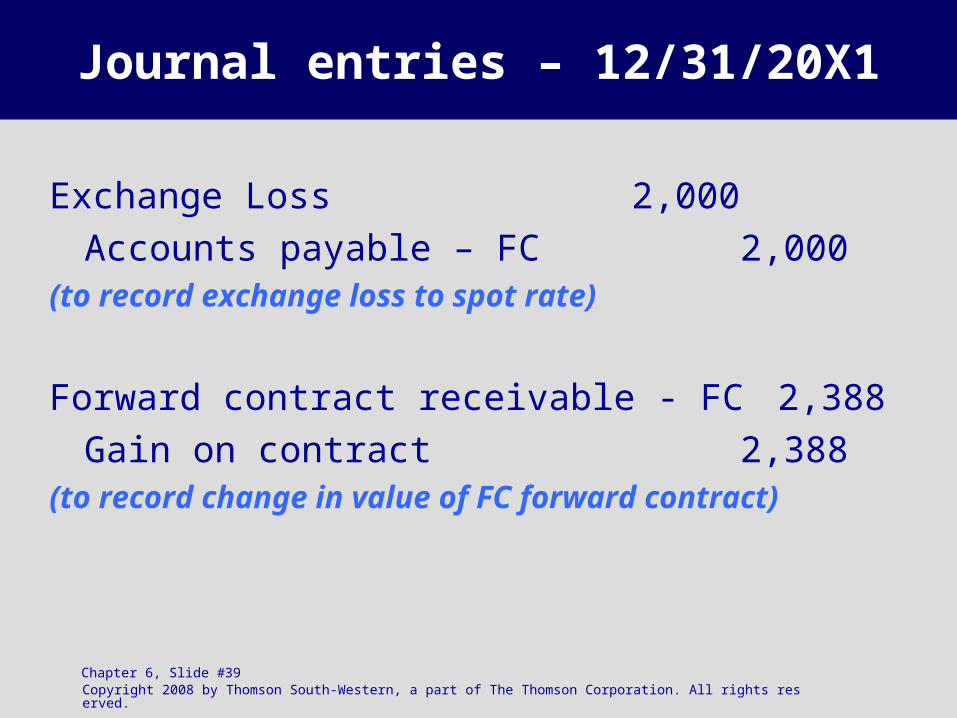

Journal entries – 12/31/20X1

Exchange Loss 2,000

Accounts payable – FC2,000

(to record exchange loss to spot rate)

Forward contract receivable - FC 2,388

Gain on contract2,388

(to record change in value of FC forward contract)

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #40

Journal entries – 2/1/20X2

Accounts payable 52,000Exchange Loss 3,000

FC 55,000(to record payment)

Forward contract receivable - FC 2,012Gain on contract 2,012

(to record change in value of FC forward contract)

FC 55,000FC receivable 55,000

FC payable 50,600Cash 50,600

(to record settlement of FC forward contract)

Copyright 2008 by Thomson South-Western, a part of The Thomson Corporation. All rights reserved.Chapter 6, Slide #41

Additional Illustrations

• The previous example was hedging with an FC forward contract

• Additional fair value examples are similar and detailed in the text– Hedging with an FC option– Hedging an FC firm commitment

• Cash flow hedges are also detailed in the text