ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM IV - 1 R 04/03 CASHIERING INTRODUCTION The Cashiering function consists of processing employer contribution payments, including the following major tasks: Receive employer contribution payments Prepare contribution payments for deposit Deposit contribution payments into clearing account(s) Record all contribution payment deposit information Post contribution payments to employer accounts Transfer monies to the Unemployment Trust Fund (UTF) PRIMARY OBJECTIVE The primary objective of Cashiering is the prompt and accurate processing of employer contribution payments. To achieve this, the Cashiering function must: 1. Process all contribution payments accurately and record deposit activities accurately (Accuracy and Completeness) 2. Deposit all contribution payments promptly and transfer monies to the UTF timely (Timeliness) Accuracy and Completeness Timeliness To determine the accuracy and completeness of processing employer contribution payments and recording deposit activities, a Program Review will be conducted to determine the existence of necessary internal controls and to determine whether or not such controls are functioning properly. To assess the promptness with which the State deposits contribution payments into the clearing account, an Estimation Sample will be conducted. (Timeliness of the transfer of monies from the clearing account into the UTF

Transcript

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 1 R 04/03

CASHIERING INTRODUCTION

The Cashiering function consists of processing employer contribution payments, including the following major tasks:

Receive employer contribution payments

Prepare contribution payments for deposit

Deposit contribution payments into clearing account(s)

Record all contribution payment deposit information

Post contribution payments to employer accounts

Transfer monies to the Unemployment Trust Fund (UTF) PRIMARY OBJECTIVE The primary objective of Cashiering is the prompt and accurate processing of employer contribution payments. To achieve this, the Cashiering function must:

1. Process all contribution payments accurately and record deposit activities accurately (Accuracy and Completeness)

2. Deposit all contribution payments promptly and transfer monies to the

UTF timely (Timeliness)

Accuracy and Completeness Timeliness

To determine the accuracy and completeness of processing employer contribution payments and recording deposit activities, a Program Review will be conducted to determine the existence of necessary internal controls and to determine whether or not such controls are functioning properly. To assess the promptness with which the State deposits contribution payments into the clearing account, an Estimation Sample will be conducted. (Timeliness of the transfer of monies from the clearing account into the UTF

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 2 R 04/03

CASHIERING INTRODUCTION

will be gauged through another vehicle and will not be assessed through TPS)

REVIEW METHODOLOGIES Because accuracy of posting of contribution payments will be evident through the Account Maintenance Acceptance Samples for Contribution Report Processing, Debits/Billings and Credits/Refunds, no Acceptance Sampling is required for the Cashiering function. Program Review The Program Review for Cashiering has two components: a Systems Review and an Estimation Sample.

The Systems Review covers the following:

Recorded Information and Instructions

Training

Recording of Transactions and Events

Execution by Authorized Individuals

Systems to Assure Execution of Events

Review of Completed Work

Review UI Cashiering activities conducted by Non-State Entities (other State Agency or Lockbox)

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 3 R 04/03

CASHIERING INTRODUCTION

REVIEW METHODOLOGIES The Systems Review will identify the internal controls and quality assurance systems necessary for an effective Cashiering operation, and indicate if such controls are in place. Most questions in the Systems Review require a Verification Source (VS). However, because of the significance of the Cashiering function, some review questions require small, stringent tests to confirm the presence and effectiveness of the internal controls. Verification Test (VT) instructions are provided when a verification test is needed. If a VT fails, the reviewer must draw the conclusion that a risk exists in that area. (VTs that fail must be repeated the following year.) In addition to the review of the State Cashiering operation, a section has been designed for the States that employ non-State, State Agencies (e.g. State Departments of Revenue) or banks (lockboxes) to perform Cashiering activities. For States that employ either a non-State agency or a bank lockbox for Cashiering activities, BOTH SYSTEMS REVIEWS ARE NECESSARY because:

Rarely can all contribution payments and documents received at a non-State cashiering site be processed exclusively at the site, and

The State Cashiering Systems Review includes questions dealing with recording

deposit information for which States have responsibility. All references to Non-State State Agencies and Bank Lockbox Operations will be generically referred to as Non-State Entities on all subsequent pages. NOTE: If NO contribution payments are received by the State, some questions in the State Cashiering Systems Review may not be applicable to your State's operations. The reviewer should carefully examine each question in the State Cashiering Systems Review, document the reason specific questions are not applicable and request Regional Office approval to record N/A answers for those questions.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 4 R 04/03

CASHIERING INTRODUCTION

REVIEW METHODOLOGIES The Estimation Sample for Cashiering examines :

Employer Contribution Payments In addition to the Systems Review, a sample of employer contribution payments will be examined to measure the timeliness in which contribution payments are deposited into the State's clearing account. The Estimation Sample will be selected from daily mail receipts during the review period.

PROGRAM REVIEW COMPONENTS SYSTEMS REVIEWS

State

Non-State Entities

ESTIMATION SAMPLES

State

Non-State Entities

SYSTEMS REVIEWS

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 9 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW INTERVIEW SHEET

Function

Reviewer

Persons Interviewed

Documents Reviewed

Date

Name:

Title:

Title:

Form#:

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 10 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Recorded Information and Instructions In the State Cashiering operations, procedures should be set forth for receiving employer contribution payments, preparing contribution payments for deposit, depositing contributions into the clearing account, recording deposit activity, posting contribution payments to the employers' accounts and transferring monies to the UTF.

The reviewer should examine recorded information, instructions and procedures available to the staff and compare them to the laws and written policies of the State to determine if they are current, accurate, and complete. The reviewer should also observe the Cashiering process and talk with employees to learn if the recorded information, instructions and procedures are available to staff.. The operations of a non-State entity to process contribution payments for the State, will not be included in this section of the review (See the Non-State Entities Systems Review for a review of non-State State Agencies and bank lockbox operations). However, residual work done by the State will be included, e.g., procedures for sending and receiving work to and from the non-State entity. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If there are no recorded instructions, describe in the narrative how the staff becomes aware of the proper procedures to perform the tasks of the Cashiering function.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 11 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State have recorded information and instructions to assist employees to perform

Cashiering functions in accordance with State laws and policies?

Yes No __ 2. If yes, are all recorded information and instructions: Yes No

a. Current? ..................................................................................................................... b. Accurate? ................................................................................................................... c. Complete? .................................................................................................................. d. Readily available to staff?..........................................................................................

VS:(Questions 1 and 2 ) 3. If any of the preceding evaluative questions are answered "no", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS:(Question 3 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 13 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A" and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 15 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Training The State needs to have systems and procedures to identify training needs and deliver training to employees who perform duties within the Cashiering function. New employees need to learn the procedures for processing and posting employer contribution payments. Experienced employees benefit from periodic refresher courses and additional training when procedures change and/or defects in quality occur at an unacceptably high rate.

The reviewer should become familiar with the methods and procedures the State uses to identify and meet the training needs of employees involved in cashiering activities. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If there is no formal training program, then describe how the staff learns of the laws and written policies and the proper procedures to perform the Cashiering duties.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 17 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State have methods or procedures to provide training for newly hired

employees? Yes No __

*If yes, identify the type of training: Yes No

a. *Formal Classroom Training? ................................................................................... b. *On the Job Training?................................................................................................ c. *One-on-One Training? ............................................................................................. d. *Individual Self-guided Training?............................................................................. e. *Other?.......................................................................................................................

Describe the type and frequency of training in the narrative.

2. Does the State have methods or procedures to provide refresher training for experienced

employees?

Yes No __

*If yes, identify the type of training: Yes No

a. *Formal Classroom (e.g., refresher courses)? ........................................................... b. *On the Job Training?................................................................................................ c. *One-on-One Training? ............................................................................................. d. *Individual Self-guided Training? . .......................................................................... e. *Other?........................................................................ . . . . .

Describe the type and frequency of training in the narrative.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 18 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 3. Does the State provide training when there are: Yes No N/A

a. State law changes? ..................................................................................................... b. Policy/procedure changes? ........................................................................................ c. Needs identified from review of finished work

(e.g., supervision, quality assurance review)? ........................................................... d. Hardware/software changes? ..................................................................................... e. Peak processing periods? ........................................................................................... f. *Other?.......................................................................................................................

4. Does the State have processes (e.g., back-up training or organizational flexibility) to

assure that staff absences will not disrupt operations? Yes No __

If yes, describe in the narrative following these questions. VS: (Questions 1-4 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 19 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 5. *In the opinion of the supervisor or manager, does the training meet the needs of the

Yes No __ 6. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions VS:(Question 6 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 21 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 23 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Recording of Transactions and Events The Cashiering function should have procedures and controls to assure that employer contribution payments are accurately accounted for and that bank deposits are accurate and reconciled. Whether the State system is automated or manual, an audit trail should lead from source documents to State accounting records of receipts and to the transfer of monies into the UI Trust Fund.

The reviewer must determine whether there are systems to assure that records of receipt and processing of employer contribution payments are kept accurately, completely, and up-to-date. An audit trail should be in place leading to support documentation. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If there is no recording or reconciliation of the General Ledger Account, then explain how the State is assured that the accounts are accurate.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 25 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State maintain an audit trail for the following types of transactions: Yes No N/A

a. Receipt of employer contribution payments? . . . . . . . b. Preparation of contribution payments for deposit? . . . c. Deposits to the clearing account? . . . . . . . . . . . . . . ... d. Deposit discrepancies? . . . . . . . . . . . . . . . . . . . . . .... e. Posting to employer accounts? . . . . . . . . . . . . . . . . . f. Transfer monies to the UI Trust Fund? . . . . . . . . . . g. Balancing of contribution payments? . . . . . . . . . . . . h. Information received via electronic media . . . . . . . i. Dishonored contribution payments (NSFs)? . . . . . .

2. Does the State have a means to identify the source of discrepancies? Yes No __

*If yes, which are used: Yes No

a. *Deposit list/calculator tapes? ................................................................................... b. *Batch lists/batch reconciliation? .............................................................................. c. *Bank statements? ..................................................................................................... d. *Debit or credit notices from bank? (Dishonored checks

or discrepancies) ....................................................................................................... e. *Bank Statement Trial Balance?................................................................................ f. *State Treasurer's Report? ......................................................................................... g. *Other?.......................................................................................................................

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 26 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 3. Are the information sources retained and accessible for State use? Yes No __ VS:(Questions 1 – 3 ) 4. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS:(Question 4 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 27 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 29 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Execution by Authorized Individuals The Cashiering unit handles negotiable items and cash. Access to these contribution payments should be limited to authorized, assigned staff. This requirement provides security for the contribution payments and assures that the cashiering functions are performed by authorized, assigned individuals only.

The reviewer must examine the flow of contribution payments through the State and identify the internal controls limiting access to and providing accountability for the contribution payments. The reviewer must also examine the authorizations and procedures governing the flow of contribution payments from field offices and other sources to the Central Cashiering unit. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 31 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State have the following controls to assure that the processing of contribution

payments is limited to assigned staff in the Central Office:

a. Specific individual(s) assigned to assure that all mail is picked up or delivered daily?

Yes No __

b. Specific individual(s) assigned to open and handle checks?

Yes No __

c. Area for opening and handling checks restricted to assigned individuals? Yes No __

d. Specific individual(s) assigned to receive and prepare contribution payments for deposit?

Yes No __

e. Area for preparing contribution payments for deposit restricted to assigned individuals?

Yes No __

f. Specific individual(s) assigned to account for and forward contribution payments to bank for deposit?

Yes No __

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 32 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. g. Area for accounting of contribution payments to forward to the bank for deposit

restricted to assigned individual(s)? Yes No __

h. Specific individual(s) assigned to deliver contribution payments to bank? Yes No __

i. * Controls for receiving and depositing contribution payments other than those listed above? (If yes, describe in the narrative).

Yes No __

VS:(Question 1 ) 2. Does the State have the following internal controls to provide accountability for all

employer contribution payments received in other units in the Central Office and/or the field:

a. Specific individual(s) assigned and responsible for receiving and accounting for

contribution payments? Yes No __

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 33 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS

b. Procedures for controlling and forwarding contribution payments from collections

units, field units or other similar units to the Central Cashiering Unit? Yes No __

c. Procedures to verify that contribution payments forwarded from collections units, field units or other similar units were received by Central Cashiering Unit?

Yes No __ VS: (Question 2 ) 3. Does the State have the following internal controls providing accountability for handling

currency (actual cash) received:

a. Pre-numbered receipt books? Yes No __

(1) If yes, is an internal audit (e.g., verifies who assigns the books, who

possesses them, that the proper number sequence is used, etc.) performed? Yes No __

(2) *If yes to (1) above, indicate frequency of audit by checking all that apply:

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 34 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS VT: (Verification Test) Conduct the following test and annotate your findings in the space below. Pull either the completed receipt books from the last four quarters or the records of completed receipts for the last four quarters. Verify and track the use of pre-numbered receipt books, correct numbering of the receipt books and that the receipts are used in sequence from the books. Verify that the currency received was deposited and accurately posted to the employer

account for 12 receipts. If the total number of receipts written is less than 12, verify the deposit activity and accuracy of posting to the employer's account for all of them.

NOTE: If no receipt books were issued and/or no receipts were written during the review period, contact your Regional Office for instructions. 4. Are specific individual(s) assigned to transfer monies from the clearing account to the

UTF? Yes No __ VS:(Question 4 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 35 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS

5. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS:(Question 5 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 37 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 39 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Systems to Assure Execution of Events For Cashiering, controls are needed to reconcile balances of transactions and to identify areas where exceptions are encountered.

The reviewer will determine if such controls have been built into the Cashiering operations. It is beyond the scope of TPS to actually validate balances in the general accounting system. The reviewers will only verify that the State maintains a general accounting system and performs reconciliations of all accounts (i.e., Accounts Receivables, Clearing, Solvency Fund, Penalty and Interest). A section has been designed for States that employ the services of Non-State Entities to perform cashiering activities. Both sections must be completed by States that use the services of Non-State Entities because not all cashiering activities can be processed through the Non-State Entities' operation. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 41 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State verify that the amount shown on the daily deposit records agrees with the

amount credited by the bank? Yes No __ 2. Does the State verify that the amount credited by the bank agrees with the amount

recorded in the State's accounting system (i.e., general ledger account)? Yes No __ 3. Does the State have internal controls in place to assure that discrepancies between its

deposit records and bank deposit records are routinely reconciled? Yes No __ 4. Does the State have internal controls that assure that adjustments are made to the

accounting system to reflect discrepancies reported by the bank? Yes No __ 5. Does the State have internal controls that assure that adjustments are made to employer

accounts to reflect the discrepancies reported by the bank? Yes No __

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 42 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 6. Does the state have internal controls to assure that the State accounting system is

adjusted to reflect dishonored-check contribution payments? Yes No __ 7. Does the state have internal controls to assure that the employer's account is adjusted to

reflect dishonored-check contribution payments? Yes No __ VT: (Verification Test) For each bank used by the state, select a bank reconciliation statement(s) (or statement from comptroller's office citing state banking activities) for one month from the past 12 months. Track all entries (e.g., deposits, debit for dishonored checks, credit memorandums resulting from coding errors, or other adjustments to deposits) back to the deposit record to assure that all appropriate action was taken. Exclude from this test transfer of funds, employer refund activity or any benefit payment activity. NOTE If the state does not receive a traditional bank statement, determine the means by which it acquires a record of banking transactions. Consult with the Regional Office to develop an approach to conducting the VT using the documents available.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 43 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 8. Does the State have procedures to assure timely deposit of all contribution payments? Yes No __ VS:(Question 8 ) 9. *Does the State sort contribution payments and source documents as follows?

Yes No

a. *Timely reports.......................................................................................................... b. *Untimely reports ...................................................................................................... c. *Reports with liability reported, payment enclosed .................................................. d. *Reports with liability reported, no payment enclosed ............................................. e. *Reports with no wages, no liability due................................................................... f. *Reports with excess wage only, no liability due...................................................... g. *Other items that can not be processed immediately

(e.g., Correspondence, etc.) ....................................................................................... 10. *Does the State have procedures to give priority to depositing high dollar contribution

payments? Yes No __

If yes, describe in the narrative at the end of this section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 44 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 11. Does the State have a procedure for problem items that require special handling (e.g.,

reports received with no employer account number, irregular contribution payments, etc.), that assures prompt follow-up and deposit of payments? (Example: process to place items in a suspense account/exception file for follow-up).

Yes No __

a. If yes, does the State have procedures to assure that items placed in the above accounts/files are ultimately handled and posted as appropriate?

Yes No __ VT: (Verification Test) Conduct the following test and note your findings in the space below. At the beginning of the quarter, identify 12-15 employer contribution payments in the "suspense account/exception file". At the end of the quarter, review the records to determine the disposition of the items. If an item has not yet been cleared, determine whether or not procedures have been

followed thus far. For items that have been cleared, determine if procedures were followed correctly and

timely (e.g., payments were posted to the proper employers' accounts within the time frame required by the State, or money was correctly refunded or transferred to the proper State agency).

NOTE: Reviewers who cannot conduct this test because the State does not use exception files/suspense accounts must contact their Regional Office for further instructions.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 45 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 12. Does the State have a procedure to assure prompt transfer of monies from the Clearing

Account into the UTF? Yes No __ VS: (Question 12 ) 13. *Does the State accept Electronic Fund Transfers (EFT) for contribution payments?

Yes No __ 14. Does the State have system procedures or internal controls to assure that employer

accounts are properly posted to reflect: Yes No N/A

a. Payments received in paper form (checks/cash)? ...................................................... b. Payments received via EFT?......................................................................................

(N/A is only appropriate if Question #13 is answered "No"). VS: (Question 14 ) 15. *What is the estimated average time to credit (apply) monies to the appropriate employer

account? Number of days ______

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 46 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 16. If procedures are automated, is a systems check performed every time a program is changed?

Yes __ No __

17. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS: (Question 16 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 47 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 49 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW Review of Completed Work For Cashiering function, the State should be conducting systematic reviews of completed work to assure accuracy and timeliness. The review should include contribution payments posted to employer accounts as well as deposit activity.

The reviewer will consider the kind of supervisory program and/or quality assurance review the State uses to assess the Cashiering function. The review procedure may differ for new employees. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If there is no supervisory and/or quality assurance review, describe how quality is assured in the Cashiering unit.

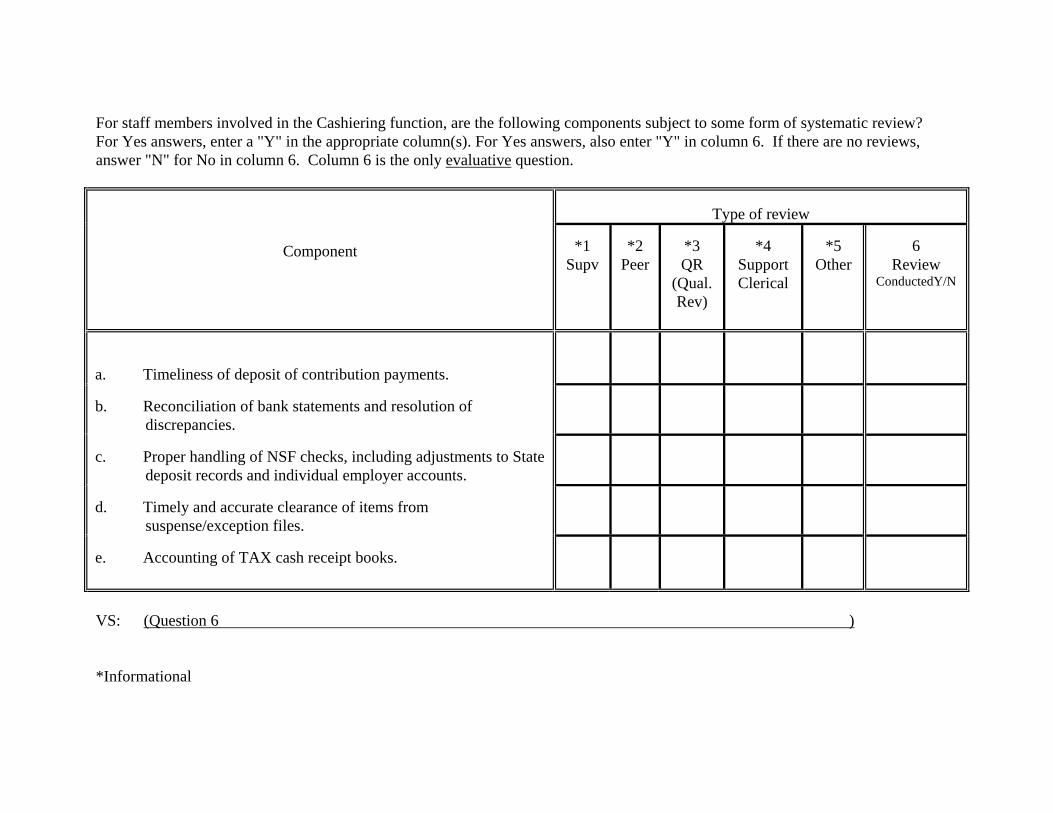

For staff members involved in the Cashiering function, are the following components subject to some form of systematic review? For Yes answers, enter a "Y" in the appropriate column(s). For Yes answers, also enter "Y" in column 6. If there are no reviews, answer "N" for No in column 6. Column 6 is the only evaluative question.

Type of review

Component

*1 Supv

*2

Peer

*3 QR

(Qual.Rev)

*4

Support Clerical

*5

Other

6

Review ConductedY/N

a. Timeliness of deposit of contribution payments.

b. Reconciliation of bank statements and resolution of

discrepancies.

c. Proper handling of NSF checks, including adjustments to State

deposit records and individual employer accounts.

d. Timely and accurate clearance of items from

suspense/exception files.

e. Accounting of TAX cash receipt books.

VS: (Question 6 )

*Informational

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 53 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 7. If any of the preceding evaluative questions are answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS: (Question 7 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 55 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 57 R 04/03

CASHIERING PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS Additional Controls 1. *Does the State have internal controls or quality assurance systems in the Cashiering

function which this review failed to identify? Yes No __

If yes, describe below. 2. * Are there any exemplary practices for the Cashiering function? Yes No __

If yes, describe below.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 59 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

Review of Non-State Cashiering Activities

(Bank Lockbox or non-State Agency) *THE STATE USES A BANK LOCKBOX OR NON-STATE AGENCY TO PERFORM CASHIERING ACTIVITIES: YES NO ___ If yes, continue to the next page. If no, this concludes the Systems Review. SYSTEMS REVIEW Recorded Information and Instructions The State should have a contract with the bank or non-State agency that performs its Cashiering activities. The contract should specify all the procedures and controls that are needed to assure that contribution payments are processed timely and accurately, that information and unprocessed contribution payments and documents are forwarded to the State, that deposits are made to the Clearing Account in a timely manner, and that transfers are made to the UTF timely. The State should also have methods to verify that the contractual requirements are being met. The reviewer should review the contract and visit the location(s) where the Cashiering activity takes place (bank or other agency) to determine that the operation is fulfilling the contract requirements. The reviewer should also review the process to assure that contribution payments are being processed timely and accurately and that information, unprocessed contribution payments and documents are forwarded to the State. In the Narrative Section following the questions, explain "Other" responses and "Compensating Controls". Identify the question being explained by referencing the number and section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 60 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 61 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. *Cashiering activities are performed by:

a. * Bank ....................................................................................................................... b. * Non-State AGENCY (e.g., Dept. of Revenue) .......................................................

2. Does the Contract and/or related document(s) that detail services to be provided, contain

provisions for the following: Yes No a. Frequency of deposit? ................................................................................................

b. Security? .................................................................................................................... c. Accuracy of data provided to State? .......................................................................... d. Promptness of data provided to State?....................................................................... e. Accessibility of records?............................................................................................ f. On-site review by State? ............................................................................................ g. Frequency of mail pick-up? ....................................................................................... h. *Disaster Recovery? ..................................................................................................

VS: (Question 2 ) 3. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions VS:(Question 3 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 63 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A" and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 65 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW Recording of Transactions and Events The contract should specify procedures and controls to assure that employer contribution payments are accurately accounted for and that bank deposits are accurate and reconciled. Whether the Non-State Entity system is automated or manual, it should provide an audit trail that leads from source documents to records of receipts and to the deposit of monies into the UTF.

The reviewer must determine whether there are systems to assure that records of receipt and processing of employer contribution payments are accurately and promptly recorded. An audit trail should be in place leading to support documentation. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If the Non-State Entity does not provide a record of monies received by employers and a record of deposit activities, explain how the State is assured that the accounts are accurately maintained and how the State is assured that the Non-State Entity is adhering to the contract requirements.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 67 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the Non-State Entity have a method to prove untimely employer reporting, such as

retaining untimely envelopes or filming/imaging of the envelopes to document untimely reports and payments?

Yes No __

VS: (Question 1 ) 2. Does the State have procedures to verify that items forwarded to the State from the Non-

State Entity are received? Yes No __ VS: (Question 2 ) 3. Does the endorsement or other documentation on the checks contain information that

assists State staff with an audit trail for payments? Yes No __ VS: (Question 3 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 68 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 4. Are copies of the contribution payments available to the State staff? Yes No __ VS: (Question 4 ) 5. Are controls in place to assure the accuracy of report and payment data? Yes No __

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 69 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 6. *Does State receive magnetic media output of information from the Non-State Entity?

Yes No __

a. If yes, does the State have a method to verify the accuracy of the information? Yes No __ VS: (Question 6a .) 7. *If the State permits contribution payments via EFT, is the associated contribution report

required to be submitted to the Non-State Entity?

Yes No __

a. If yes, is there a written procedure to properly credit the employer's account with the payment?

Yes No __

If yes, describe the procedure in the narrative. VS: (Question 7a. )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 70 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 8. *Does the Non-State Entity process contribution report data submitted:

Yes No

a. *On diskette? ............................................................................................................. b. *On magnetic tape .................................................................................................... c. *Via Electronic Data Interchange (EDI)?..................................................................

9. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions VS:(Question 9 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 71 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 73 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW Execution by Authorized Individuals Since the Cashiering function requires the handling of negotiable items and cash, access to these items should be limited to authorized, assigned staff. This requirement provides security for the contribution payments and assures that the cashiering functions are performed only by authorized individuals.

The reviewer should examine the contract and the handling of contribution payments by the Non-State Entity to identify the internal controls limiting access to and providing accountability for the contribution payments. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 75 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

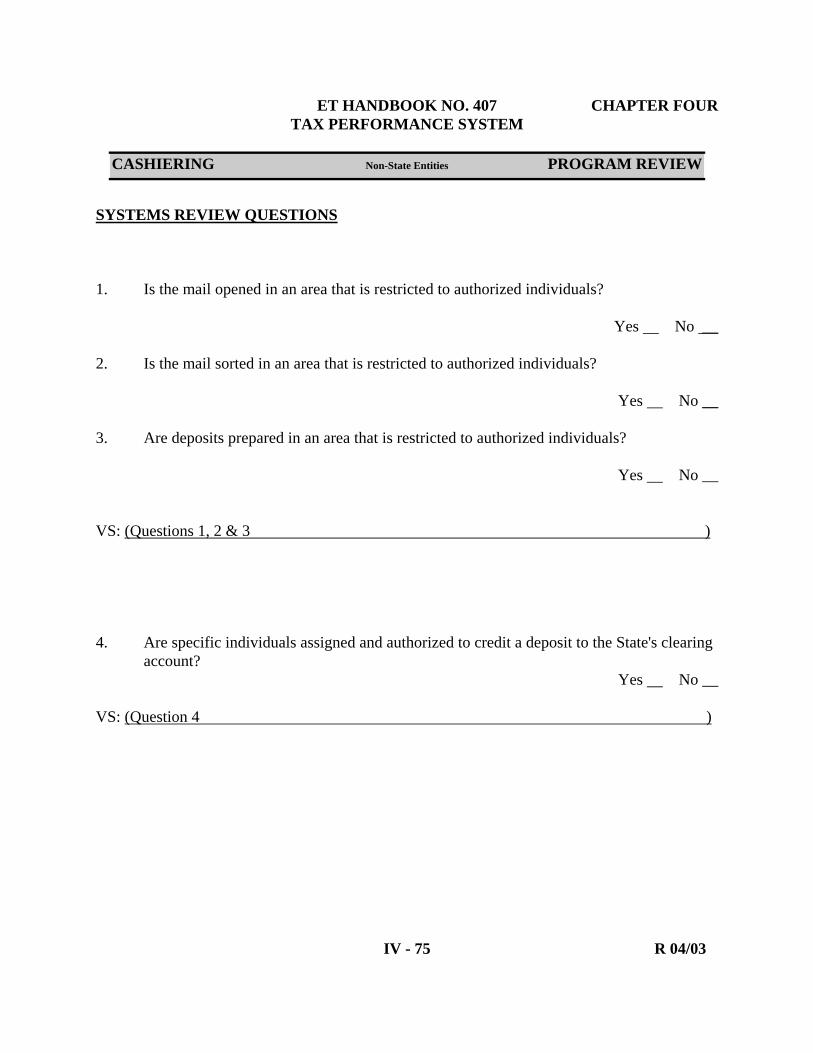

SYSTEMS REVIEW QUESTIONS 1. Is the mail opened in an area that is restricted to authorized individuals?

Yes No __ 2. Is the mail sorted in an area that is restricted to authorized individuals? Yes No __ 3. Are deposits prepared in an area that is restricted to authorized individuals? Yes No __ VS: (Questions 1, 2 & 3 ) 4. Are specific individuals assigned and authorized to credit a deposit to the State's clearing

account? Yes No __ VS: (Question 4 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 76 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 5. Are specific individuals assigned and authorized to make adjustments to the State's

account (e.g., debit and credit memoranda, encoding errors and dishonored contribution payments)?

Yes No __ VS: (Question 5 )

6. *Does the contract authorize bank or non-State personnel to transfer funds to the UTF?

Yes No __

If yes, are specific individuals authorized to make the transfer of money to the UTF?

Yes No __

VS: (Question 6a. )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 77 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 7. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions VS:(Question 7 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 79 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 81 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW Systems to Assure Execution of Events For Cashiering, controls are needed to assure that the Non-State Entity provides the services detailed in the contract and that specific instructions are followed.

The reviewer will determine if such controls have been built into the contract and if the Non-State Entity is adhering to the conditions of the contract. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 83 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

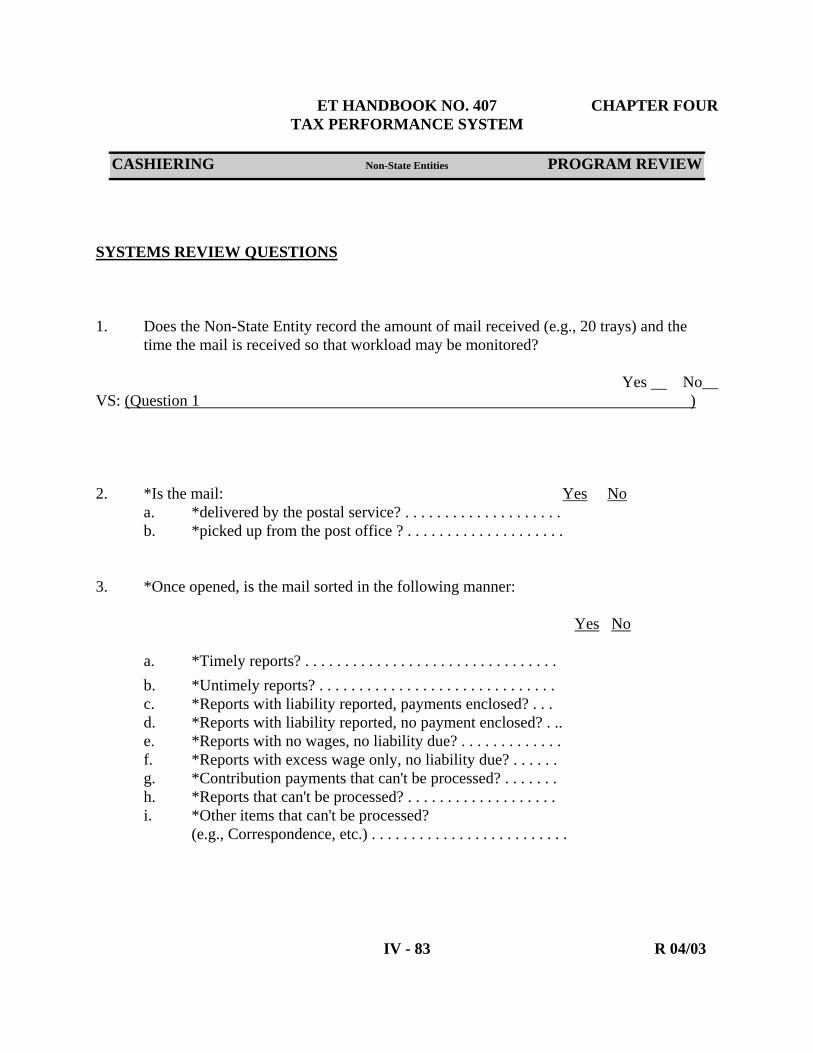

SYSTEMS REVIEW QUESTIONS 1. Does the Non-State Entity record the amount of mail received (e.g., 20 trays) and the

time the mail is received so that workload may be monitored? Yes No__ VS: (Question 1 ) 2. *Is the mail: Yes No

a. *delivered by the postal service? . . . . . . . . . . . . . . . . . . . . b. *picked up from the post office ? . . . . . . . . . . . . . . . . . . . .

3. *Once opened, is the mail sorted in the following manner:

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 84 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

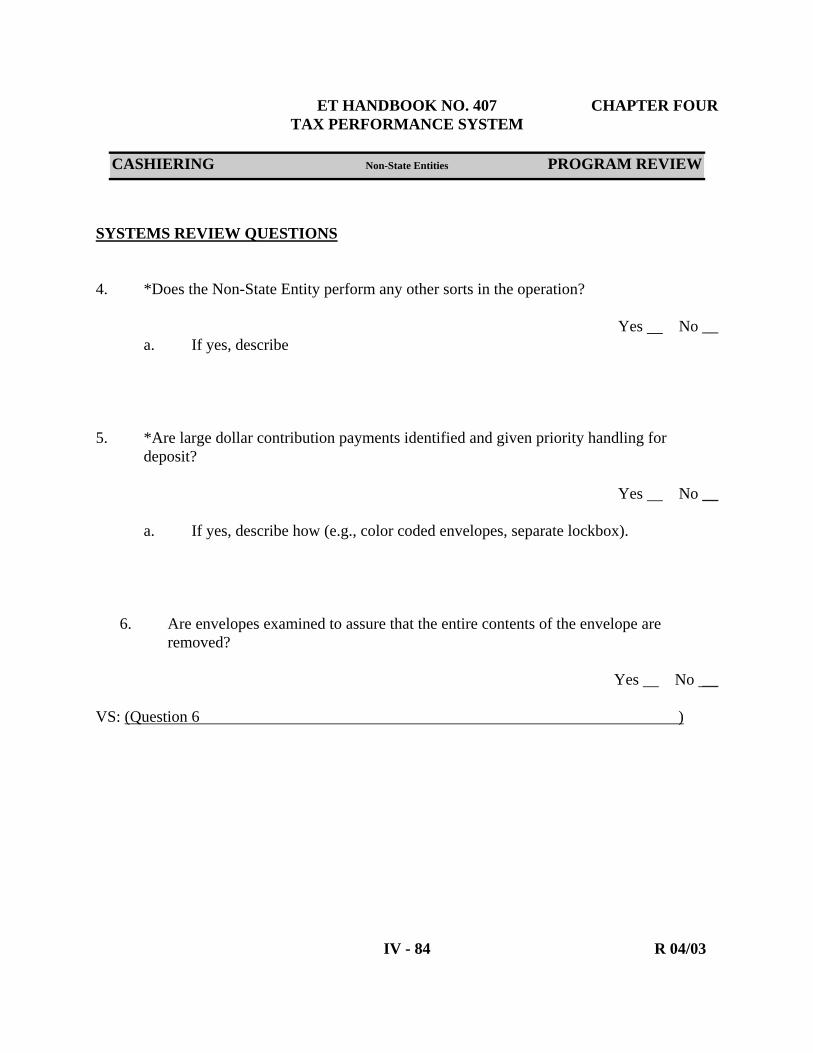

SYSTEMS REVIEW QUESTIONS 4. *Does the Non-State Entity perform any other sorts in the operation? Yes No __

a. If yes, describe

5. *Are large dollar contribution payments identified and given priority handling for

deposit? Yes No __

a. If yes, describe how (e.g., color coded envelopes, separate lockbox).

6. Are envelopes examined to assure that the entire contents of the envelope are

removed?

Yes No __ VS: (Question 6 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 85 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

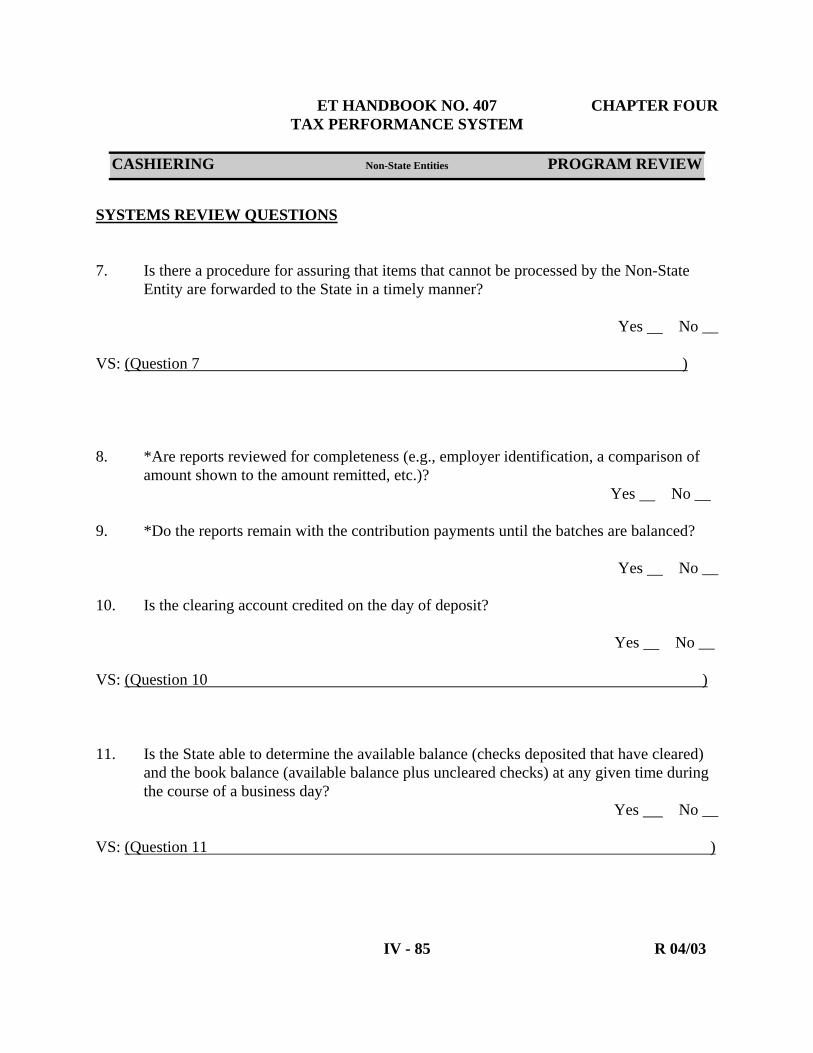

SYSTEMS REVIEW QUESTIONS 7. Is there a procedure for assuring that items that cannot be processed by the Non-State

Entity are forwarded to the State in a timely manner? Yes No __ VS: (Question 7 ) 8. *Are reports reviewed for completeness (e.g., employer identification, a comparison of

amount shown to the amount remitted, etc.)? Yes No __

9. *Do the reports remain with the contribution payments until the batches are balanced? Yes No __ 10. Is the clearing account credited on the day of deposit?

Yes No __

VS: (Question 10 ) 11. Is the State able to determine the available balance (checks deposited that have cleared)

and the book balance (available balance plus uncleared checks) at any given time during the course of a business day?

Yes No __ VS: (Question 11 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 86 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

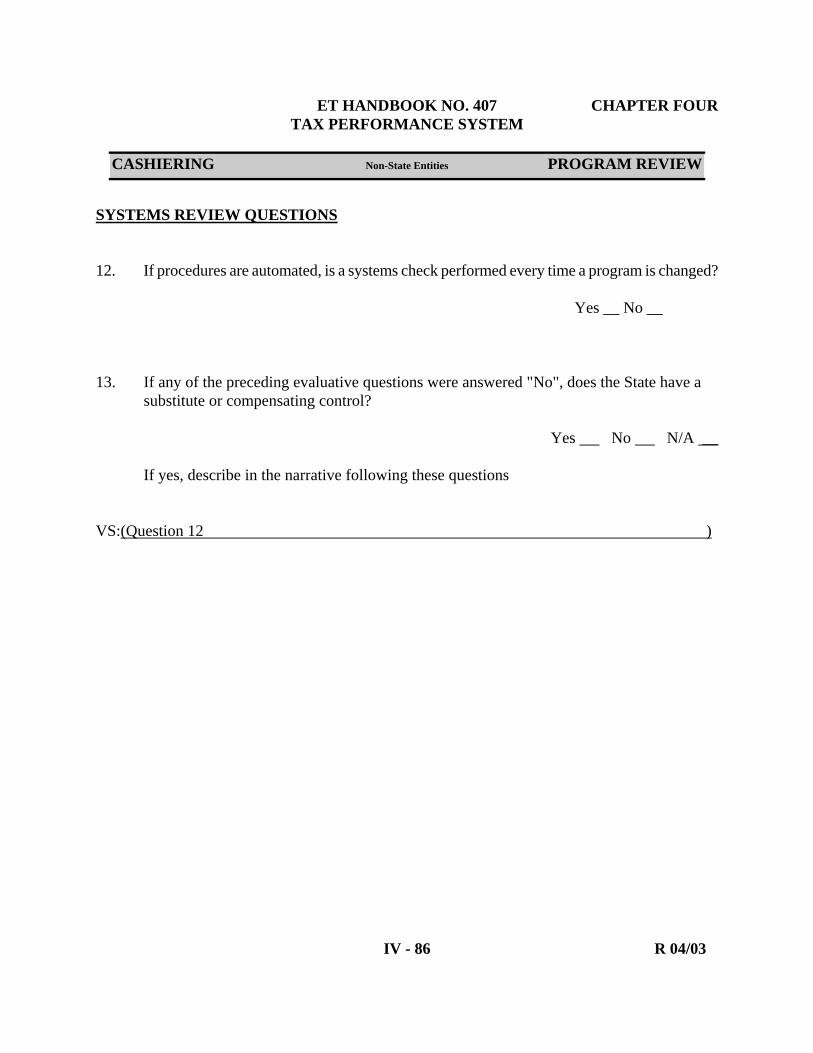

SYSTEMS REVIEW QUESTIONS 12. If procedures are automated, is a systems check performed every time a program is changed?

Yes __ No __

13. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions VS:(Question 12 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 87 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 88 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 89 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

Review of Completed Work For States that use the services of Non-State Entities to perform Cashiering functions, a review of completed work would include monitoring contract provisions. The State should conduct systematic reviews of completed work by the Non-State Entity to assure accuracy and timeliness of the information. The contract should specify the quality of work expected by the State.

The reviewer will consider the kind of quality assurance review the State uses to assess the quality of work completed for it by the Non-State Entity. In the Narrative Section following the questions, explain "Other" responses, and describe "Compensating Controls". Identify the question being explained by referencing the number and section. If there is no quality assurance review, describe how quality is assured by the State in the Cashiering function.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 91 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 1. Does the State monitor the performance of the contract?

Yes No __

a. *If yes, identify which provisions are monitored in the narrative following these questions.

VS: (Question 1 ) 2. *Does State management consider the provisions of the contract adequate for the State's

payment processing needs?

Yes No __

a. *If No, how is the contract deficient?

3. *Is the contract procured through a competitive bid process?

Yes No __

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 92 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS 4. If any of the preceding evaluative questions were answered "No", does the State have a

substitute or compensating control? Yes No N/A __

If yes, describe in the narrative following these questions. VS:(Question 4 )

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 93 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW NARRATIVE Question Explanation of "N/A", and "Compensating Controls" Number (when deemed necessary) Question Answers to "If yes, describe" and "Other": Number

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 94 R 04/03

CASHIERING Non-State Entities PROGRAM REVIEW

SYSTEMS REVIEW QUESTIONS Additional Controls 1. *Are there additional internal controls or quality assurance systems exercised by the

Non-State Entity that this review failed to identify? Yes No __

If yes, describe below. 2. * Are there any exemplary practices by the Non-State Entity or by the State in the dealing

with the Non-State Entity? Yes No __

If yes, describe below.

ESTIMATION SAMPLE

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 97 R 04/03

CASHIERING PROGRAM REVIEW

DEPOSIT PROMPTNESS OF CONTRIBUTION PAYMENTS ESTIMATION SAMPLE INSTRUCTIONS Purpose/Intent To measure the timeliness in which States deposit

contribution payments into the Clearing Account. Scope The scope of the review will be the contribution payments

received during the second quarter review period. Universe The universe for the Estimation Sample should include all

paper payments (e.g., cash, checks) received during the review period. A sample will be drawn from the universe of paper payments to determine deposit promptness. A sample size GOAL of 500 payments (see the Sampling Table on page 111) will be selected from the paper payment universe and listed on the TPS Cashiering Sample Coding Sheet.

NOTE: In States that accept ELECTRONIC FUND TRANSFERS (EFTs), the reviewer must determine the percent of contributions received via EFT. Sampling the EFT universe is not necessary since all EFTs are deposited timely. A formula has been developed that combines the measurements from the Estimation Sample (paper payment sample) and the entire EFT universe to reflect overall deposit promptness (see Step 11).

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 98 R 04/03

CASHIERING PROGRAM REVIEW

ESTIMATION SAMPLE INSTRUCTIONS

Timing/Frequency The sample will be selected once per calendar year.

The sample selection period will cover the time during which the state receives the "peak" or "bulk" mail for the second quarter reports. (Typically, reports and payments will be due on or around July 31).

Sampling Procedures The following are steps for selecting sample items.

STEP 1. * The reviewer will estimate the time period during which 90% of the receipts for the quarter are anticipated. This could be as long as five weeks in some states. From that time period, the reviewer should determine the five days during which the greatest amount of mail receipt is anticipated. The five days selected should be based on historical mail receipt data and the reporting due date. Reviewers must be able to support their decision. Sample items are to be selected from each of these five days. The samples may be chosen from five consecutive days or from five days chosen at random over the course of the mail receipt period. If the cashiering function is performed at a lock box, or other agency site, or located one or more hours from the state agency, the number of sampling days may be reduced to three days (with RO approval). The sample size will remain at 500 items, increasing the number of sample items to be selected each day to 167 items. (Although this modification will be accepted, it is not preferable because it reduces the representativeness of the sample items.) Note: If 90% or more of the receipts for the quarter are expected to arrive within five days or less, samples must be taken each day.

* Please refer to last page of Estimation Sample Instructions if lockbox is used.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

Reviewers must inform the Regional Office of the days selected for sampling and provide information to support the selection, including an estimate of the percentage of total dollar amount that will be received during the selected period. STEP 3. Determine if mail is presorted. Determine if checks are sorted for special handling prior to opening the envelopes based on predetermined indicators such as color coded envelopes or a separate mailing address for large employers.

Reviewers must insure that the overall sample is representative of the population of all payment items in terms of these large employers.

For example: if 10 percent of the payment items are from these large employers, 10 percent of the total sample must come from them as well. To manage this 10 percent, 50 items (10% of the total of 500) must be selected from the large employer group. The remaining 450 sample items will be taken from the "regular" flow of contribution items.

Estimate the number of projected items in each of the two groups. Using the example and assuming 10 percent are large employers, there would be 5,000 large employers and 45,000 "regular" employers. Fifty (10%) items should be selected from the large employer group and 450 from the remainder. Calculate the Check Interval Number and Random Starting Number using the same method. The same or a different Random Number can be used for the two groups.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 100 R 06/10

CASHIERING PROGRAM REVIEW

ESTIMATION SAMPLE INSTRUCTIONS Sampling Procedures contd. STEP 4. Determine which sample selection method will be used . The state may use either one of the following sampling

methodologies: a. Check Interval, b. Mail Tray. For either method, the goal is to select 500 sample items in total for the 5 days. This requires the reviewer to estimate the amount of mail or number of mail trays to be received for the 5 day period and then to establish a sample interval, or to establish the number of sample items to be selected from each tray. Either method can be used for selecting samples; however, the Mail Tray Method may be easiest to estimate. Once a method is selected, it should be used for all of the 5 days. Do not switch back and forth between methods. In some state agencies, mail is received round the clock or is received before or after the reviewer is on site. Under these circumstances, the reviewer must make a “best guess” of how much mail will be received while he or she is available and select an appropriate number of sample items from mail incoming during that time period. For example, the reviewer is on site 7:00 AM to 4:00 PM, and the total number of mail trays for the five day period between the hours the reviewer is on site is expected to be 45. Since the sample is set at 500 items, divide 500 by 45. The result is 11.1 therefore the reviewer would randomly select 11 items from each mail tray delivered between 7:00 AM to 4:00 PM for each of the five days. To use the Check Interval Method: (1) Project the total number of contribution payments (less EFT payments) to be received during the designated time frame by one of

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

the following methods and enter the number in the appropriate place on the Summary Sheet.

(a) Use last year’s total number of receipts (items) for the

second quarter, OR (b) Use the number of employers expected to report during

the sample period. (Total number of active employers minus anticipated number of late filers).

(2) Divide the projected number of contribution payments (items) y

500 to determine the Check Interval Number (Nth number).

(3) Determine the Random Starting Number for the sample. (See instructions in Appendix A, TPS Handbook). This will be the first sample item selected.

(4) From the Random Starting Number, count the envelopes until

the Nth item is selected. Each successive item to be selected is determined by adding the Nth number to the number of the most recently selected item. (NOTE: It is permissible to measure the distance between the random start number item and the Nth item within a mail tray to select each subsequent sample item.)

To use the Mail Tray Method:

(1) Estimate the number of mail trays to be received during the peak period using historical data from the Cashiering Unit and/or the Mail Room.

(2) Determine the number of sample items to be selected from each tray by dividing 500 by the number of trays that you expect to receive.

EXAMPLE: If forty (40) trays of mail are expected during the sampling time frame, divide 500 by 40. The result is 12.5 contribution payments per tray. Alternately, make a

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

random selection of 12 items from the first tray and 13 from the next tray during the course of the sample selection time frame.

STEP 5. Select sample contribution payments.

On each of the days of the sampling time frame, the TPS reviewer (or alternate) will go to the area where the mail is received, opened (by machine) and transferred to mail trays. The samples for the day will be selected from these trays by the method selected.

NOTE: It is more important to maintain a consistent sampling technique than it is to pull exactly 500 items. Once the sampling technique is established, do not alter it. Example: if you are pulling every 10th item and the 20th item contains no payment, do not record that account as part of the sample, but continue to count to the 30th item which will be the next item recorded as part of the sample. The sampling table on page 113 will adjust the percentage needed to determine the value-to-pass.

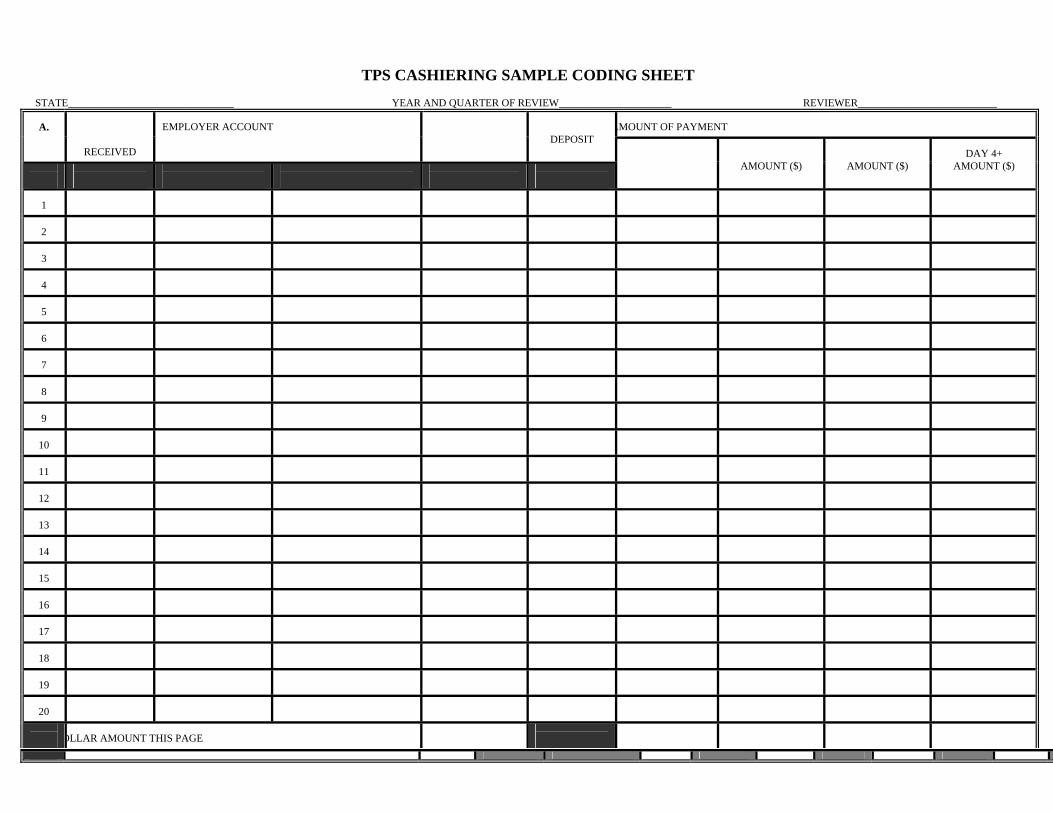

STEP 6. Record identifying information for each sampled payment. For each sample contribution payment, complete Columns B, C, and D on Coding Sheet as follows.

a. Column B: Enter the date that the mail was received by the State

or Non-State Entity. b. Column C:

Enter the employer account number assigned by the State. If an account number is not available, enter the employer's name or business name as shown on the report or payment.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

NOTE: Even when the account number is available, it may

be useful to record the employer's name to assure accurate identification. This column may also be used at the discretion of the reviewer to record any other information that would be helpful in identifying the account or tracking the payment.

c. Column D: Enter the amount of the payment. STEP 7. Replace sample item.

Return each payment to approximately the same spot from which it was removed. There should be nothing that would indicate which payments are part of the sample except the information recorded on the Coding sheet. STEP 8. Determine the review date.

Determine the date it is reasonable to assume that all contribution payments received during the selection period are deposited and the information is posted to the employers file. Enter the date in the appropriate blank on the Summary Sheet. Hold the list of sample contribution payments until the sample review date.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

Each sample payment listed on the Coding Sheet will be reviewed for timeliness of deposit.

Review appropriate records to determine the date that all payments listed were deposited (e.g., deposit slips, batch listings, cash transmittal log, employer's record, etc.). STEP 10. Complete Coding Sheet.

For each sample contribution payment, complete the Coding Sheet as follows:

a. Column E: Enter the date that each payment listed was

deposited. b. Columns F, G, H and I:

For each payment listed, complete the appropriate column (Columns F through I), using the following process.

(1) Determine the number of banking days between date the payment was received and the date the payment was deposited (do not include weekends and holidays). NOTE: Payments received one day and deposited the next day are considered to be deposited within one day, regardless of the TIME of day received or the TIME of day deposited.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

(2) Based on the number of days between receipt and the date of deposit, enter the dollar amount of the sample payment either column F, G, H, or I, as follows: Column F represents within 1 day for deposit. Column G represents within 2 days for deposit.

Column H represents within 3 days for deposit.

Column I represents within 4 or more days for deposit.

c. For each page of the coding sheet, total amounts of each column and enter the total amount of the column on, Total Dollar This Page (line 21). The total amount of Columns F, G, H, and I should equal the total of column D. d. For each page of coding sheet, count the number of items in each column and enter total on, Total Items This Page (line 22). The Total items of each column should equal the total number of completed lines of the Coding Sheet (cannot exceed 20 per sheet). Complete the coding sheet for all sample items.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

e. Complete Part II of the Summary page of the Coding Sheet as follows:

(1) Total amounts of Columns D, F, G, H and I from coding sheets used in sample selection. (2) Enter column total amount on corresponding columns of Summary Coding Sheet on line 1, columns D, F, G, H and I. (Total amounts of columns F, G, H, and I should equal total of line 1, column D). (3) Total items for columns D, F, G, H and I for all coding sheets used in the sample selection. (4) Enter column total items on corresponding columns of Summary Coding Sheet on line 2, columns D, F, G, H and I.

(Total number of items for column F, G, H and I should equal total of line 2, column D).

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

f. Complete Part III of the Summary Page. This will give the percentage for timeliness and amounts deposited.

(1) To compute the percent of amounts deposited: Divide the total dollar amounts of each column (F through I) from Part II, line 1 by the total dollars column D, line 1, then Multiply the result by 100 and round to the nearest, one decimal place.

(2) Enter the percentages in Part III, line 3, in corresponding column (F, G, H or I).

(3) To compute the percentage of items deposited: Divide the total item count of each column (F through I) from Part II, line 2 by the total item count from column D, line 2, then Multiply the result by 100 and round to the nearest, one decimal place.

(4) Enter the percentages in Part III, line 4, in corresponding column (F, G, H and I).

NOTE: The percentages of items deposited (f (3) & f (4) above) are only to aid the reviewer and State management in analyzing the level of effort in the deposit activity (items vs. dollars). No Federal requirements pertain to the number of items deposited. Federal requirements relate to dollar amounts only.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

g. Complete Part IV, Summary Recap of the Summary Page. This will demonstrate the percentage of dollars deposited by day.

(1) From Part III, line 3 enter the percentages from the corresponding columns into the percentage line. (2) From Part II, line 1, columns F, G, H, and I, enter amounts into corresponding column in Part IV. (3) Add the percentages and amounts deposited within 3 days (lines 5, 6, and 7 of Summary Recap) and enter on line 8. (4) Total percent column and amount column. Percentage total should be 100%. Total of amount should balance with Part II line 1, Column D total.

h. Enter the actual number of contribution payments received during the designated time frame in the appropriate blank of Part I on the Summary. i. Subtract the projected number of payments (or trays) from the actual number of payments (or trays) and enter the difference on the designated line in Part I of the Summary Sheet.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

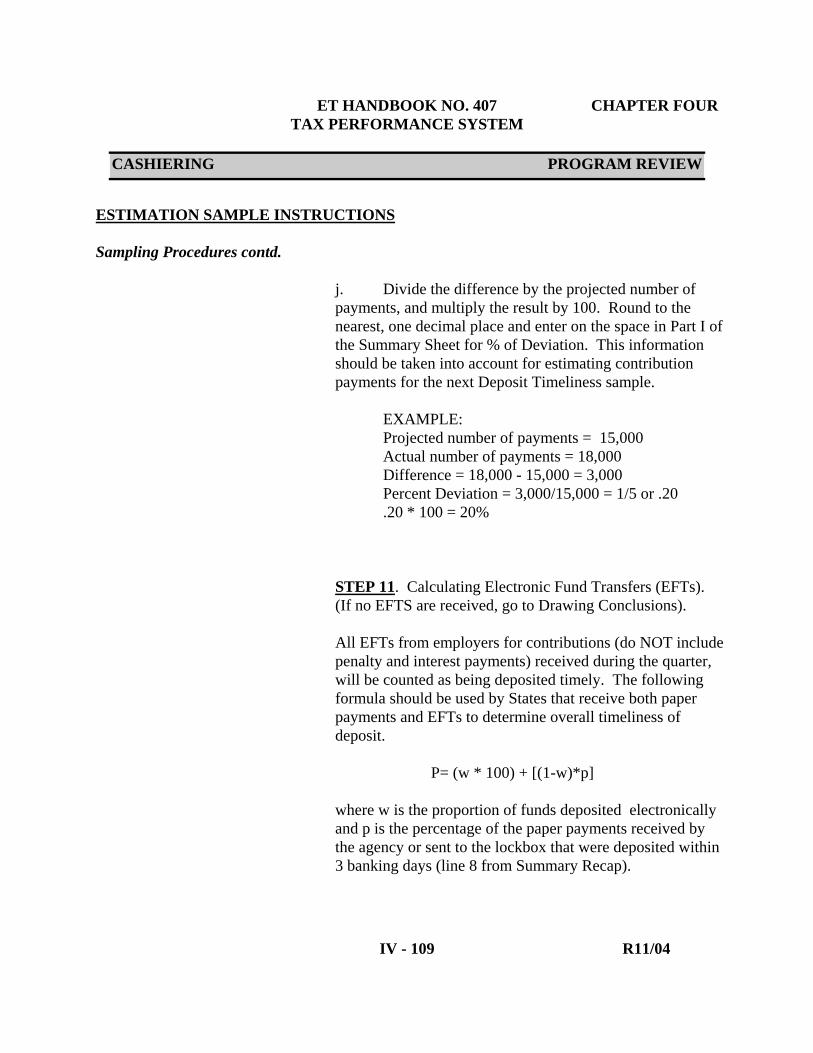

j. Divide the difference by the projected number of payments, and multiply the result by 100. Round to the nearest, one decimal place and enter on the space in Part I of the Summary Sheet for % of Deviation. This information should be taken into account for estimating contribution payments for the next Deposit Timeliness sample.

EXAMPLE: Projected number of payments = 15,000 Actual number of payments = 18,000 Difference = 18,000 - 15,000 = 3,000 Percent Deviation = 3,000/15,000 = 1/5 or .20 .20 * 100 = 20%

STEP 11. Calculating Electronic Fund Transfers (EFTs). (If no EFTS are received, go to Drawing Conclusions).

All EFTs from employers for contributions (do NOT include penalty and interest payments) received during the quarter, will be counted as being deposited timely. The following formula should be used by States that receive both paper payments and EFTs to determine overall timeliness of deposit.

P= (w * 100) + [(1-w)*p]

where w is the proportion of funds deposited electronically and p is the percentage of the paper payments received by the agency or sent to the lockbox that were deposited within 3 banking days (line 8 from Summary Recap).

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

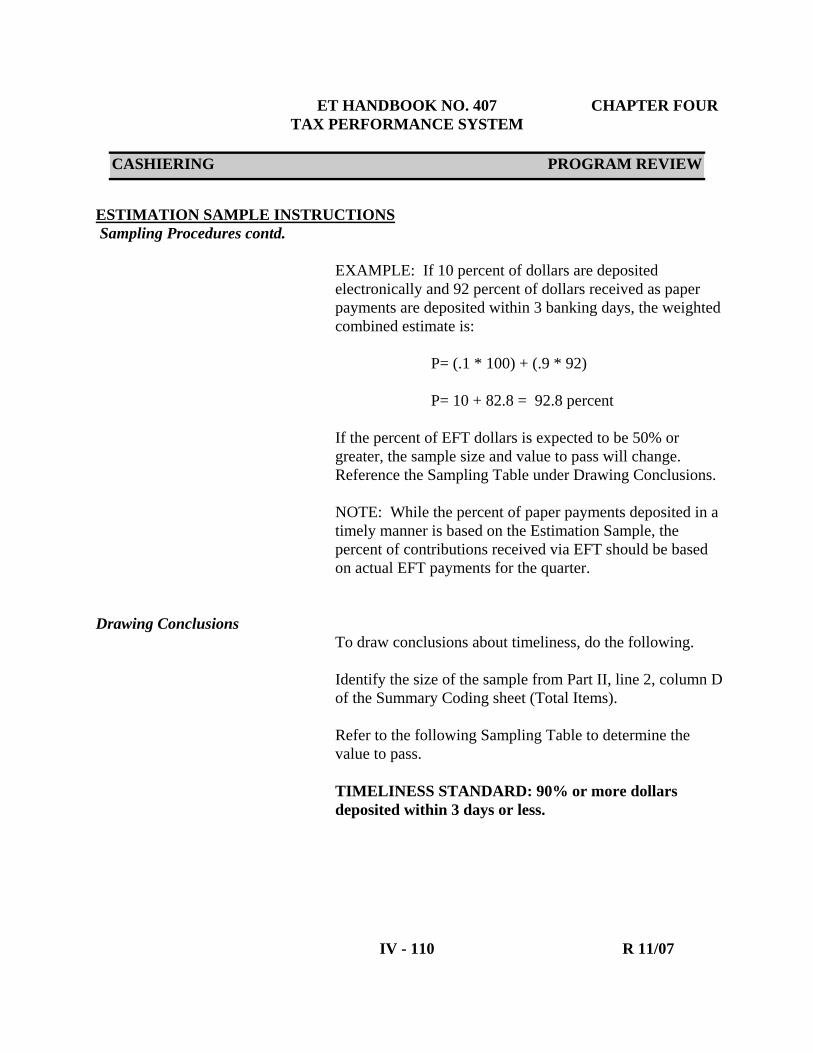

EXAMPLE: If 10 percent of dollars are deposited electronically and 92 percent of dollars received as paper payments are deposited within 3 banking days, the weighted combined estimate is:

If the percent of EFT dollars is expected to be 50% or greater, the sample size and value to pass will change. Reference the Sampling Table under Drawing Conclusions. NOTE: While the percent of paper payments deposited in a timely manner is based on the Estimation Sample, the percent of contributions received via EFT should be based on actual EFT payments for the quarter.

Drawing Conclusions To draw conclusions about timeliness, do the following. Identify the size of the sample from Part II, line 2, column D of the Summary Coding sheet (Total Items). Refer to the following Sampling Table to determine the value to pass. TIMELINESS STANDARD: 90% or more dollars deposited within 3 days or less.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

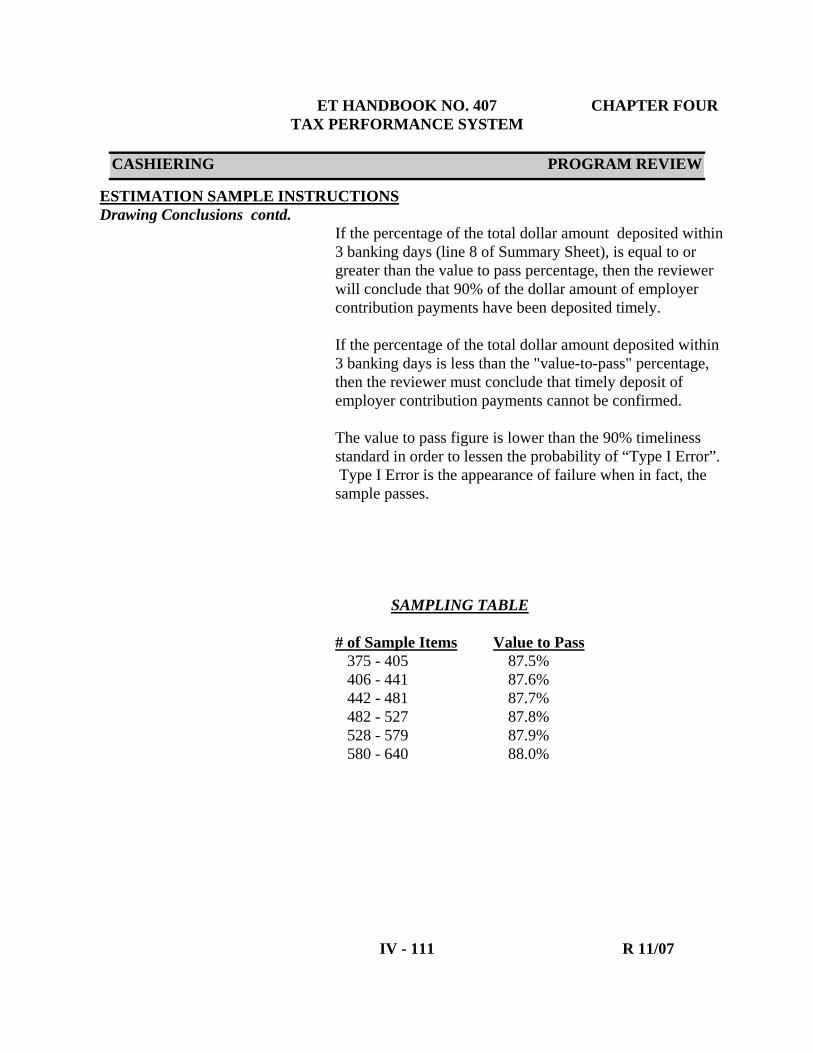

If the percentage of the total dollar amount deposited within 3 banking days (line 8 of Summary Sheet), is equal to or greater than the value to pass percentage, then the reviewer will conclude that 90% of the dollar amount of employer contribution payments have been deposited timely. If the percentage of the total dollar amount deposited within 3 banking days is less than the "value-to-pass" percentage, then the reviewer must conclude that timely deposit of employer contribution payments cannot be confirmed. The value to pass figure is lower than the 90% timeliness standard in order to lessen the probability of “Type I Error”. Type I Error is the appearance of failure when in fact, the sample passes.

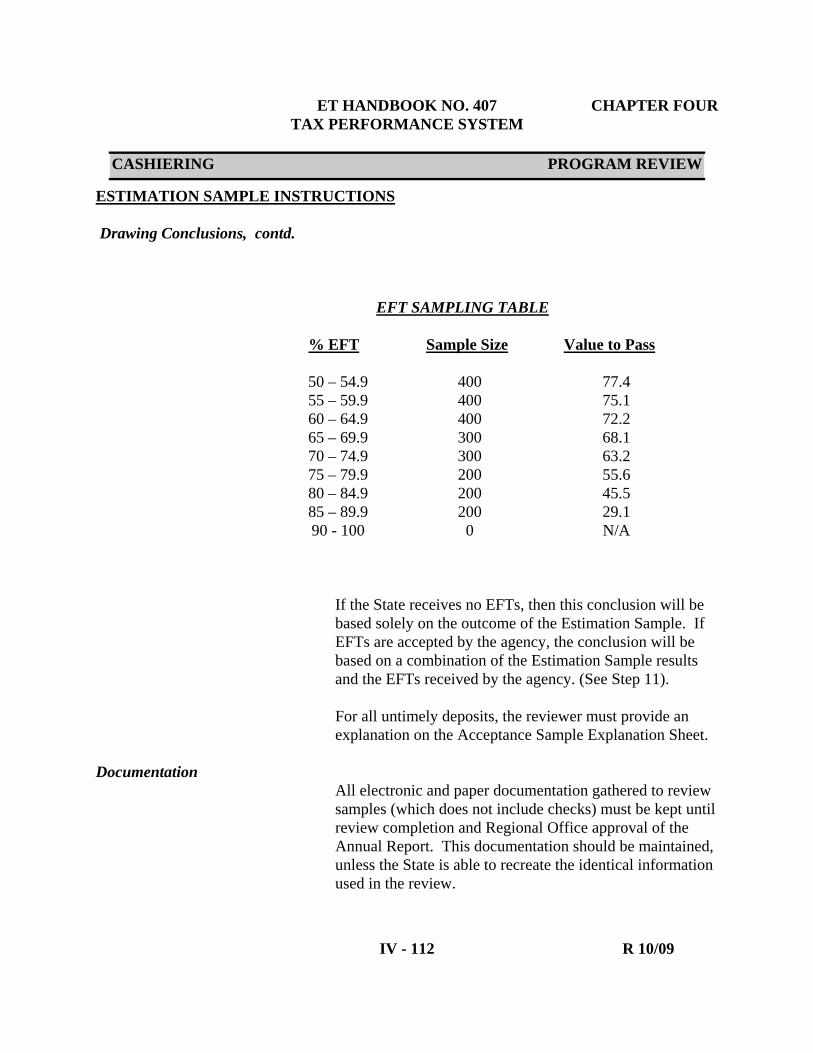

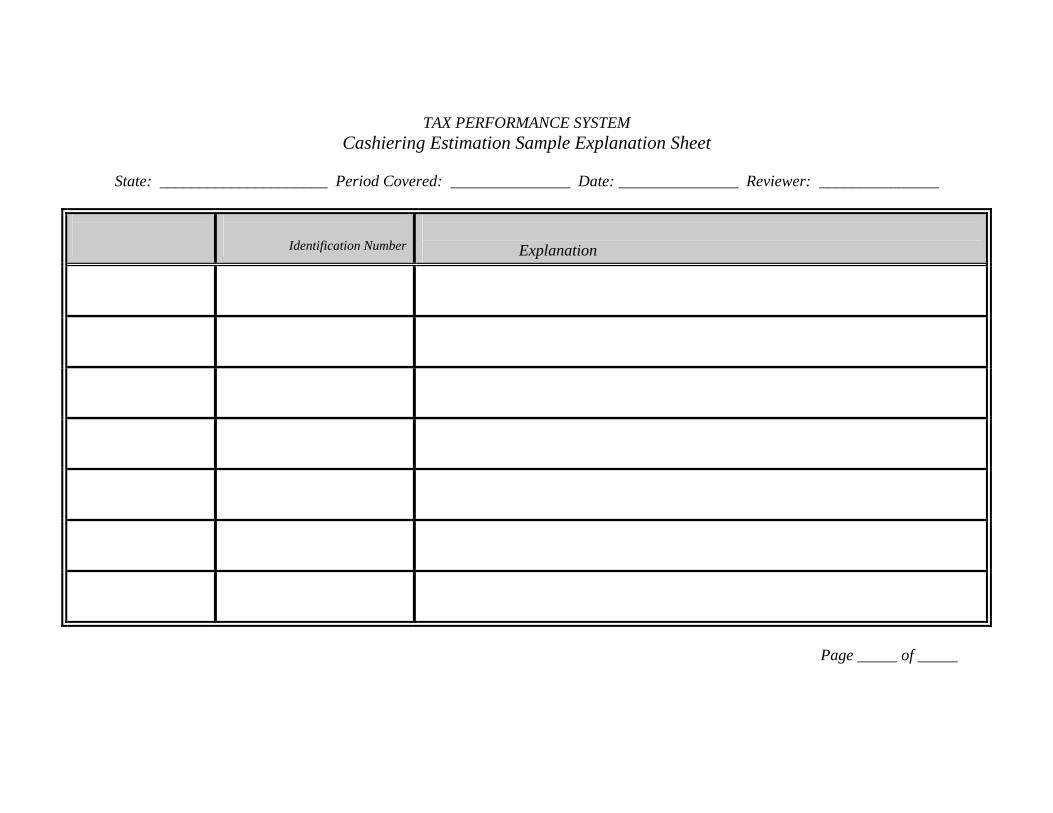

If the State receives no EFTs, then this conclusion will be based solely on the outcome of the Estimation Sample. If EFTs are accepted by the agency, the conclusion will be based on a combination of the Estimation Sample results and the EFTs received by the agency. (See Step 11). For all untimely deposits, the reviewer must provide an explanation on the Acceptance Sample Explanation Sheet.

Documentation

All electronic and paper documentation gathered to review samples (which does not include checks) must be kept until review completion and Regional Office approval of the Annual Report. This documentation should be maintained, unless the State is able to recreate the identical information used in the review.

ET HANDBOOK NO. 407 CHAPTER FOUR TAX PERFORMANCE SYSTEM

IV - 113 R 04/03

CASHIERING PROGRAM REVIEW

ESTIMATION SAMPLE INSTRUCTIONS Lockboxes

All States should make all reasonable attempts to follow the above instructions. If, however, lockboxes are not in the same geographical location as the reviewer AND it is not possible for the reviewer (or alternate) to pull the sample for the entire "peak" period, OR there are other circumstances that make it impossible to follow the instructions (i.e., around the clock processing), a modified sampling methodology may be used with the advance approval through the Regional Office. The State must request approval through the Regional Office and give the reason for the request. Based on the information provided, the Regional Office and National Office will develop a modified sampling methodology for the State.

TAX PERFORMANCE SYSTEM Cashiering Estimation Sample Explanation Sheet

State: _____________________ Period Covered: _______________ Date: _______________ Reviewer: _______________

Identification Number

Explanation

Page _____ of _____

TPS CASHIERING SAMPLE CODING SHEET STATE_______________________________ YEAR AND QUARTER OF REVIEW_____________________ REVIEWER__________________________

AMOUNT OF PAYMENT

A.

RECEIVED

EMPLOYER ACCOUNT

DEPOSIT

AMOUNT ($)

AMOUNT ($)

DAY 4+

AMOUNT ($)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

OLLAR AMOUNT THIS PAGE

TOTAL ITEMS THIS PAGE

*Payments received one day and deposited the same day or any time the next day, are considered to be deposited within one day.

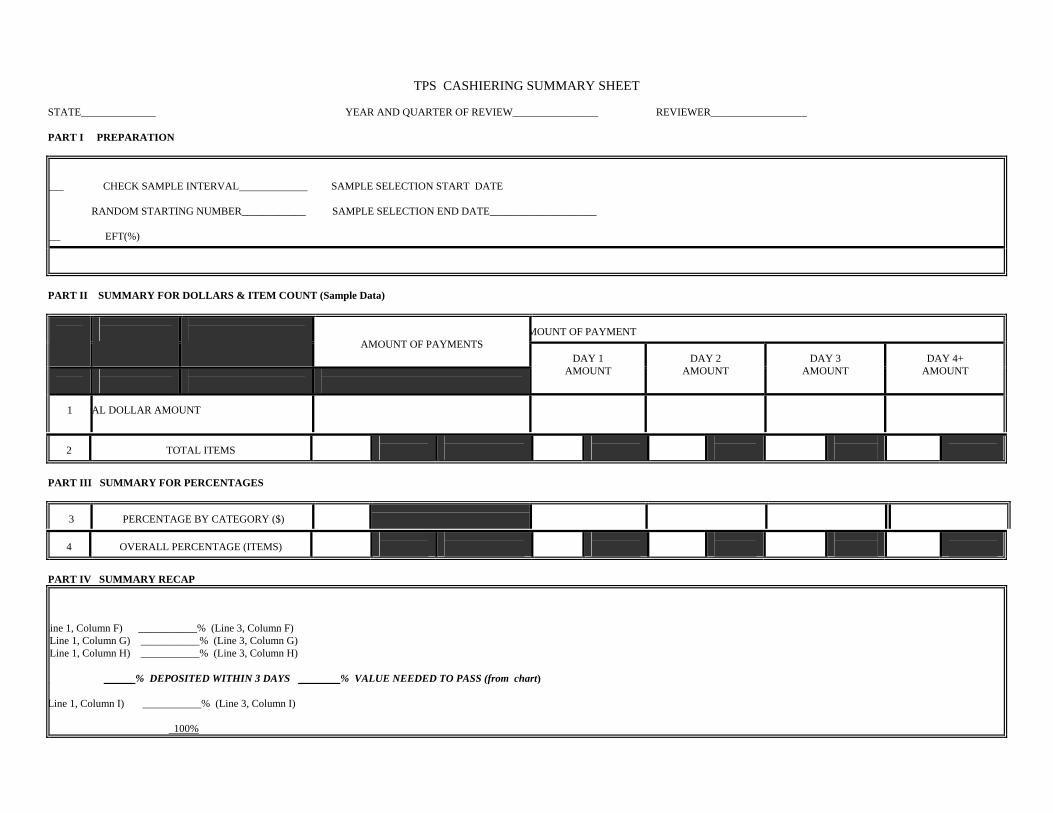

TPS CASHIERING SUMMARY SHEET STATE______________ YEAR AND QUARTER OF REVIEW________________ REVIEWER__________________ PART I PREPARATION

___ CHECK SAMPLE INTERVAL SAMPLE SELECTION START DATE

RANDOM STARTING NUMBER____________ SAMPLE SELECTION END DATE____________________

___ EFT(%)

PART II SUMMARY FOR DOLLARS & ITEM COUNT (Sample Data)

MOUNT OF PAYMENT

AMOUNT OF PAYMENTS

DAY 1

AMOUNT

DAY 2

AMOUNT

DAY 3

AMOUNT

DAY 4+

AMOUNT

1

AL DOLLAR AMOUNT

2

TOTAL ITEMS

PART III SUMMARY FOR PERCENTAGES

3

PERCENTAGE BY CATEGORY ($)

4

OVERALL PERCENTAGE (ITEMS)

PART IV SUMMARY RECAP

Line 1, Column F) ___________% (Line 3, Column F) Line 1, Column G) ___________% (Line 3, Column G) Line 1, Column H) ___________% (Line 3, Column H)

% DEPOSITED WITHIN 3 DAYS % VALUE NEEDED TO PASS (from chart)