17 CHAPTER IV DATA COLLECTION AND ANALYSIS 4.1 Brief Description of Bank X 4.1.1 Company Profile of Bank X Bank X was formed on 1990’s, as part of the Government of Indonesia’s bank restructuring program. Since the establishment, Bank X embarked on a comprehensive process of consolidation. Most visibly, Bank X closed 194 overlapping branches and reduced Bank X’s combined workforce from 26,600 to 17,620. Bank X’s single brand was rolled out throughout Bank X’s network and across all of Bank X’s advertising and promotional activities. One of Bank X’s most significant achievements has been the complete replacement of Bank X’s technology platform. Bank X inherited a total of nine different core banking systems from Bank X’s four legacy banks. After an initial investment to immediately consolidate Bank X’s systems around the strongest inherited platform, Bank X undertook a three-year, US$200 million, program to replace Bank X’s score banking platform with one specifically geared toward consumer banking. Today, Bank X’s IT infrastructure provides straight-through processing and a unified interface for customers. Bank X corporate customer base still represents the core of the Indonesia economy. By sector, it is well diversified and particularly active in food and beverage manufacturing, agriculture, construction, chemicals and textiles. Credit approvals and monitoring are subject to a highly structured ‘four eyes’ approval process, in which credit approval decisions are separated from the marketing activities of Bank X’s business units. From its founding, Bank X has worked to create a strong, professional management team operating under internationally recognized principles of corporate governance, control and compliance. The Bank is supervised by a Board of Commissioners appointed by the Ministry of State-Owned Enterprise from respected members of the financial community. The highest level of executive management is the Board of

Transcript

17

CHAPTER IV

DATA COLLECTION AND ANALYSIS

4.1 Brief Description of Bank X

4.1.1 Company Profile of Bank X

Bank X was formed on 1990’s, as part of the Government of Indonesia’s bank

restructuring program. Since the establishment, Bank X embarked on a comprehensive

process of consolidation. Most visibly, Bank X closed 194 overlapping branches and

reduced Bank X’s combined workforce from 26,600 to 17,620. Bank X’s single brand

was rolled out throughout Bank X’s network and across all of Bank X’s advertising and

promotional activities.

One of Bank X’s most significant achievements has been the complete replacement of

Bank X’s technology platform. Bank X inherited a total of nine different core banking

systems from Bank X’s four legacy banks. After an initial investment to immediately

consolidate Bank X’s systems around the strongest inherited platform, Bank X

undertook a three-year, US$200 million, program to replace Bank X’s score banking

platform with one specifically geared toward consumer banking. Today, Bank X’s IT

infrastructure provides straight-through processing and a unified interface for

customers.

Bank X corporate customer base still represents the core of the Indonesia economy. By

sector, it is well diversified and particularly active in food and beverage manufacturing,

agriculture, construction, chemicals and textiles. Credit approvals and monitoring are

subject to a highly structured ‘four eyes’ approval process, in which credit approval

decisions are separated from the marketing activities of Bank X’s business units.

From its founding, Bank X has worked to create a strong, professional management

team operating under internationally recognized principles of corporate governance,

control and compliance. The Bank is supervised by a Board of Commissioners

appointed by the Ministry of State-Owned Enterprise from respected members of the

financial community. The highest level of executive management is the Board of

18

Directors, headed by a President Director.Bank X’sBoard of Directors includes bankers

drawn from the legacy banks as well as independent outside directors. In addition, Bank

X maintains independent Offices of Compliances, Audit and the Corporate Secretary,

and is under regular scrutiny from external auditors representing Bank Indonesia and the

Supreme Audit Agency (BPK), as well as international auditing firms. AsiaMoney

magazine had recognized Bank X’s commitment toward GCG principles by awarding

Corporate Governance Award for category Best Overall for Corporate Governance in

Indonesia and Best for Disclosure and Transparency.

With assets that have grown to more than Rp 319 trillion today, and more than 21

thousand employees spread among 956 domestic branch offices and 6 overseas

branches and representatives Bank X has committed to delivering excellence in banking

services and to provide wide-ranging financial solutions in investment and sharia’

products as well as bancassurance forBank X’sprivate and state-owned corporate,

commercial, small business and micro customers in addition to Bank X’s consumer

clients. This commitment had been recognized through the top ranking in Banking

Service Excellence Award 2007 of Infobank magazine.

Below is the organization stucture of Bank X:

19

Consumer Finance

Change Mngt Office

Internal Audit

Deputy President Director

Corporate Banking

Commercial Banking

Macro and Retail Bankng

Treasury and Int Bank

Spc Asset Mngt

Compliance and HC

Risk Management

Finance and Strategy

Technology and Operation

Corp Sec, Legal, and Consumer

Care

Jakarta Network

Regional Network

Micro Business

Mass and E- Bankng

Wealth Mngt

BBB X Fin Svc

Bank Z Bali

Jkt Com Sales

Reg Com Sales I

Reg Com Sales II

Wholesale Prdct Mgt

Small Business I

Small Business II

Syaria Bank X

Corporate Banking I

Corporate Banking II

Corporate Banking III

Syndct and Strctd Finance

Plantation Specialist

Bank X Securities

Int bnk and CM serv

Treasury

Bank X Europe Ltd

Credit Recovery I

Credit Rec II

Asset Mngt

Consumer Cards

Consumer Loans

Tunas Finance

Compliance

HC Service

HC Strtgy & Plcy

Learning Center

Market & Opr Risk

Credit Risk and

Corporate Risk

Commercial Risk

Retail and Consumer

Risk

IT Business Solution and Application

Services

IT Operation

Planning, Plcy,

Procedures, Arch

Credit Operations

Central Operations

e-channel operations

Corporate Secretary

Legal

Customer Care

Culture and

Service Spc.

Figure 4.1 Head Office Organizational Chart

Investor Relation

Strategy and Perf

Accounting

Procurement and FA

Chief Economist

Board of Commissioners President Director

20

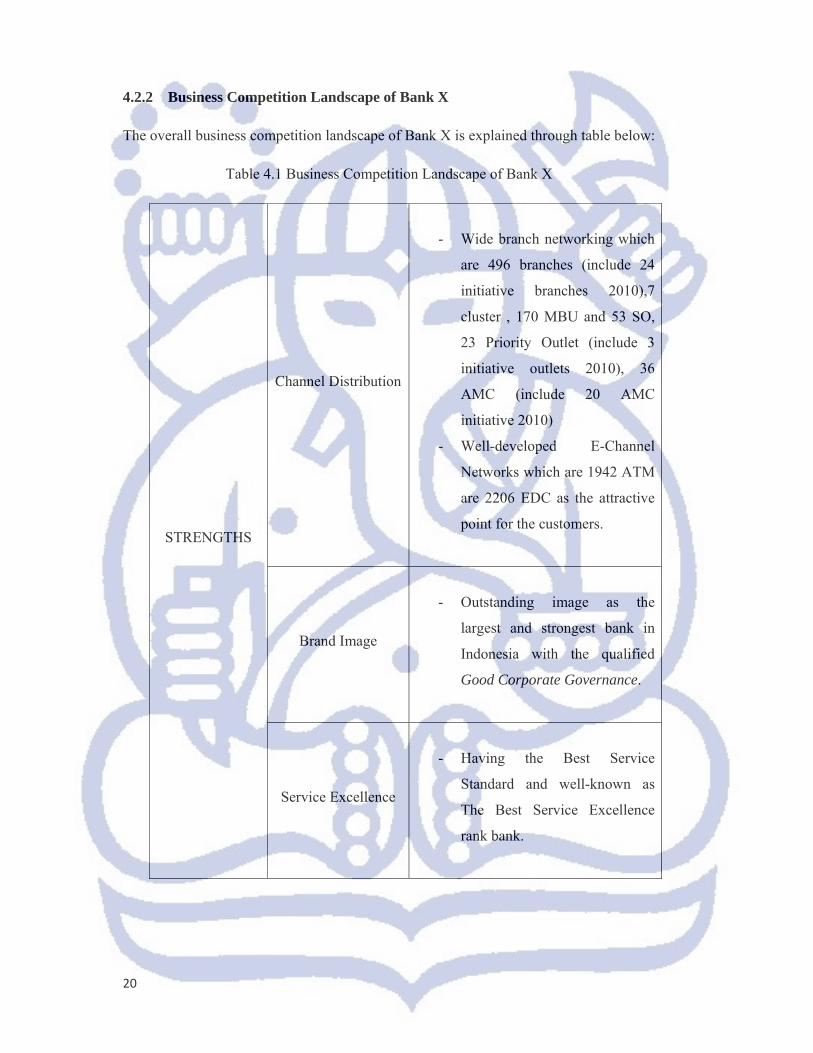

4.2.2 Business Competition Landscape of Bank X

The overall business competition landscape of Bank X is explained through table below:

Table 4.1 Business Competition Landscape of Bank X

STRENGTHS

Channel Distribution

- Wide branch networking which

are 496 branches (include 24

initiative branches 2010),7

cluster , 170 MBU and 53 SO,

23 Priority Outlet (include 3

initiative outlets 2010), 36

AMC (include 20 AMC

initiative 2010)

- Well-developed E-Channel

Networks which are 1942 ATM

are 2206 EDC as the attractive

point for the customers.

Brand Image

- Outstanding image as the

largest and strongest bank in

Indonesia with the qualified

Good Corporate Governance.

Service Excellence

- Having the Best Service

Standard and well-known as

The Best Service Excellence

rank bank.

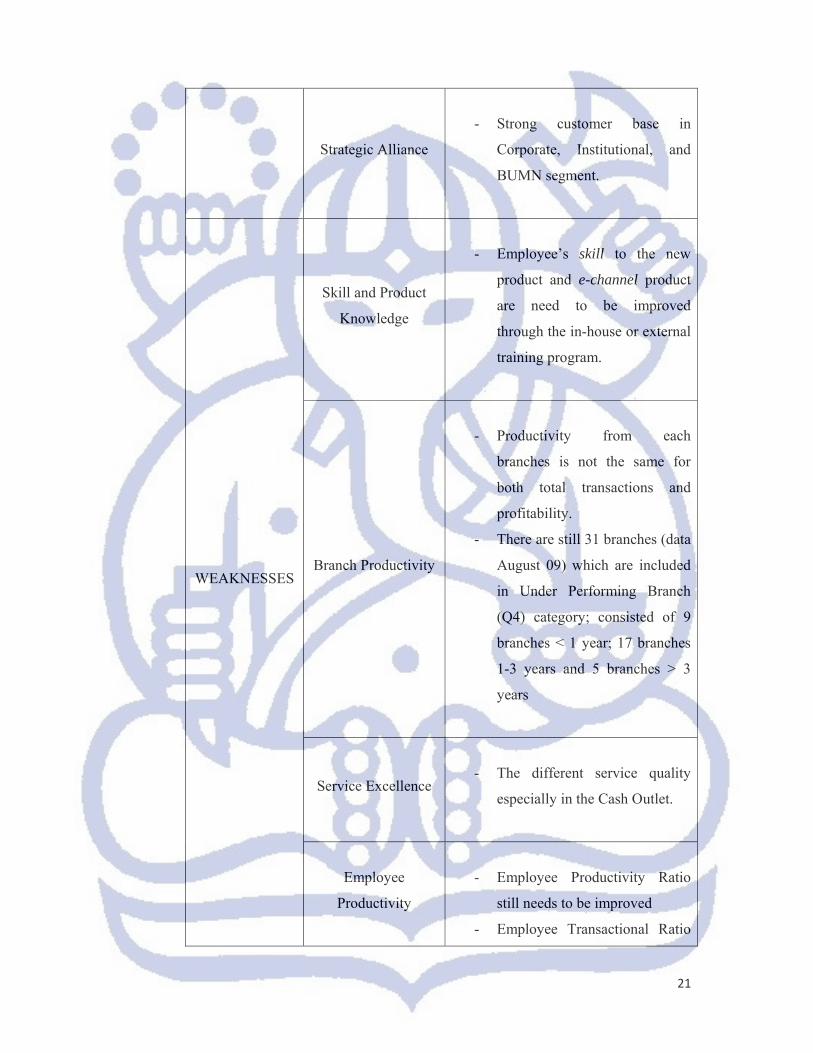

21

Strategic Alliance

- Strong customer base in

Corporate, Institutional, and

BUMN segment.

WEAKNESSES

Skill and Product

Knowledge

- Employee’s skill to the new

product and e-channel product

are need to be improved

through the in-house or external

training program.

Branch Productivity

- Productivity from each

branches is not the same for

both total transactions and

profitability.

- There are still 31 branches (data

August 09) which are included

in Under Performing Branch

(Q4) category; consisted of 9

branches < 1 year; 17 branches

1-3 years and 5 branches > 3

years

Service Excellence

- The different service quality

especially in the Cash Outlet.

Employee

Productivity

- Employee Productivity Ratio

still needs to be improved

- Employee Transactional Ratio

22

and CM Ratio are not the same

in each branch and cash outlet

OPPORTUNITY

Macro and Micro

Economic Condition

- The return of macro economic

condition that goes along with

the restructuring in real sector

and capital market

- Recovery from the stagnancy of

the economic will go together

with the increasing of inflation

rate in 2010, therefore those

become funding opportunity in

order to get the bigger spread.

Market Potential

- The big market potential in

micro, small, and consumer

segment

- Potential development in

business cluster

- In accordance with the new

government’s programs, the

potential opportunity in

transportation sector (harbour)

and government’s purchasing

Value Chain and

Alliances

- Potential value chain from

business sectors which give

biggest contribution to GDP,

that are private consumption,

infrastructure & contractors,

cement industries

23

E-Channel

Development and

Improvement

- More various e-channel

services as the network-

alternatives for distribution

- Global education and

information level that push the

using of e-channel

THREATS

Competition

- The numbers of competitors,

especially foreign owned bank

which is focused on consumer,

small, and micro segments

- Competitors are more

aggressive to open new

branches

Consolidation and

Acquisition

- The continuing banking

consolidation where the banks

from merger can be strong

competitors today

Economic Condition

- Recovery of capital market will

be followed by the

movement/switching of funds

from the banking sector to the

capital market

Other Financial

Institution

- Various products from direct

investment, pawnshop

(“pegadaian”), multifinance

and insurance.

24

4.2 Data Collection

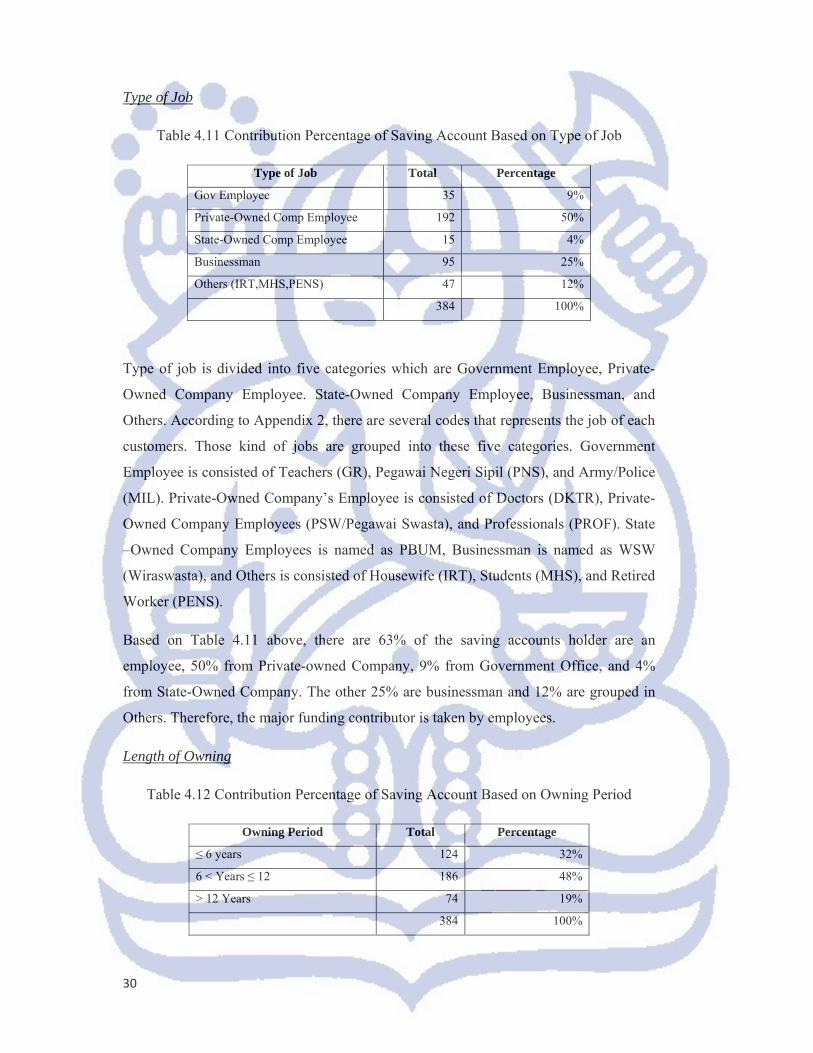

4.2.1 Number of Samples1

The number of samples is one of the important aspect in conducting the quantitative

research. Based on Roscoe from the book Research Methods For Business (1992 : 253),

there are suggestion about the sample size as follows:

1) Reasonable sample size used in the research is between 30 to 500

2) When samples are divided into categories, meaning the number of samples in

each category is at least 30

3) The research conducted with a multivariant analysis (correlation or regression),

then the minimum members of the sample is 10 times the number of variable

observed

4) For research experiments that are simple, which use experimental groups and

controls, the number of members of each sample must be 10 to 20.

Since the West Java Regional Office has 4 (four) areas, which are Surapati, Asia Afrika,

Braga, and Cirebon Area, the sample size must be representing each area. The number

of observation for Deposit is 19,081, then 81,230 for Saving Accounts and 4259 for

Current Account (only amount of fund which is equal to or greater than IDR 10

million). Therefore, based on Table 4.2, this research uses 377 number of samples for

analyzing the Deposit, 384 number of samples for analyzing the Saving Accounts

(Tabungan), and 354 number of samples for analyzing Current Account (Giro).

Below is the table of sample size of certain population with confidence level of 95%

based on Krejcie and Morgan (1970):

1 Sugiono. Statistika untuk Penelitian. Bandung : Alfabeta.

25

Table 4.2 Krejcie and Morgan Sample Size

4.2.2 Sampling Technique

This research is using Simple Random Sampling, which is the basic sampling technique

where selecting a group of subjects (a sample) for study from a larger group (a

population). Each individual is chosen entirely by chance and each member of the

population has an equal chance of being included in the sample. Every possible sample

of a given size has the same chance of selection.2 It is used simple random sampling

technique since the population has an equal chance of being included in the sample.

Beside that, the simple random sampling is the best for the situation which there is less

available information about the population and data collection can be efficiently

conducted on randomly distributed items.

4.3 Data Analysis

2 Valerie J. Easton and John H McColl. Statistic Glossary (http://stat.yale.edu/Courses/1997‐98/101/sample.htm)

(N) (s) (N) (s) (N) (s)Jumlah Jumlah Jumlah Jumlah Jumlah Jumlah Anggota Anggota Anggota Anggota Anggota AnggotaPopulasi Sampel Populasi Sampel Populasi Sampel

Dependent Variable: NTR Method: ML - Binary Logit (Quadratic hill climbing) Date: 07/05/10 Time: 23:06 Sample: 1 384 Included observations: 384 Convergence achieved after 5 iterations WARNING: Singular covariance - coefficients are not unique Covariance matrix computed using second derivatives

Variable Coefficient Std. Error z-Statistic Prob.

C 0.683323 NA NA NAMAT 0.683323 NA NA NA

RELIGION 0.383188 NA NA NAJOB 0.091682 NA NA NAAGE 0.470278 NA NA NA

McFadden R-squared 0.012602 Mean dependent var 0.872396S.D. dependent var 0.334084 S.E. of regression 0.334139Akaike info criterion 0.780032 Sum squared resid 42.31492Schwarz criterion 0.831473 Log likelihood -144.7661Hannan-Quinn criter. 0.800435 Deviance 289.5322Restr. deviance 293.2276 Restr. log likelihood -146.6138LR statistic 3.695400 Avg. log likelihood -0.376995Prob(LR statistic) 0.448795

Dependent Variable: NTR Method: ML - Binary Logit (Quadratic hill climbing) Date: 07/07/10 Time: 11:08 Sample: 1 384 Included observations: 384 Convergence achieved after 4 iterations Covariance matrix computed using second derivatives

Variable Coefficient Std. Error z-Statistic Prob.

C 1.366645 0.362366 3.771449 0.0002 RELIGION 0.383188 0.347798 1.101752 0.2706

JOB 0.091682 0.319711 0.286765 0.7743 AGE 0.470278 0.314913 1.493357 0.1353

McFadden R-squared 0.012602 Mean dependent var 0.872396 S.D. dependent var 0.334084 S.E. of regression 0.333699 Akaike info criterion 0.774824 Sum squared resid 42.31492 Schwarz criterion 0.815976 Log likelihood -144.7661 Hannan-Quinn criter. 0.791146 Deviance 289.5322 Restr. deviance 293.2276 Restr. log likelihood -146.6138 LR statistic 3.695400 Avg. log likelihood -0.376995 Prob(LR statistic) 0.296290

Obs with Dep=0 49 Total obs 384 Obs with Dep=1 335

43

From the EViews 7 output in Table 4.19, the constant and coefficients from each

variables are known which are maturoty date, job, religion, and age. The equation will

be as follows

. . . .

.

On the other hand, since the maturity date seems constant, maturity date affects the

calculation of standard deviation, Z-test, and probability to be Not Applicable (NA) in

the calculation. Therefore, by eliminating the maturity date as variable and joining the

maturity date into constant, the Logit Model will be more make sense.

From the EViews 7 output in Table 4.20, for constant and coefficients from each

variables are known which are job, religion, and age. The equation will be as follows

. . . .

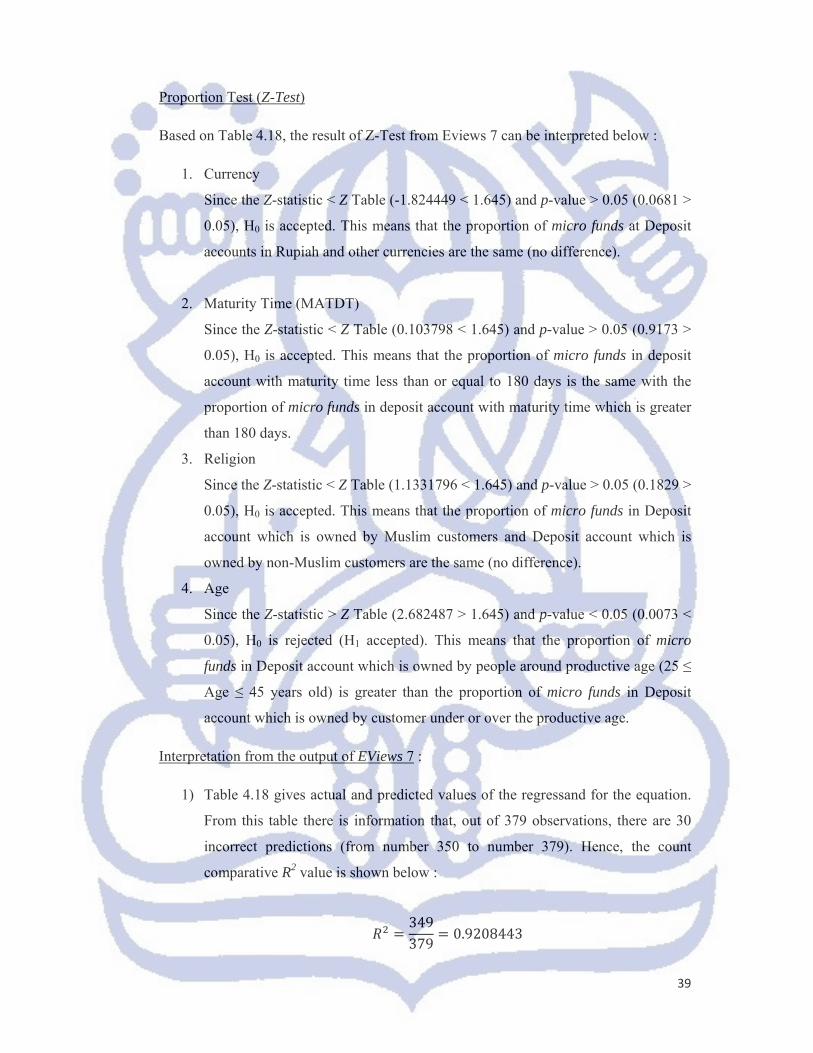

Proportion Test (Z-Test)

Based on Table 4.19, the result of Z-Test from Eviews 7 can be interpreted below :

1. Maturity Date (MATDT)

The input of Maturity Time in EViews 7 as variable on Table 4.19 makes the

result of standard error, z-statistic, and probability become Not-Applicable

(NA). Compared to Table 4.20, if the maturity time is not input, there are clear

information about the standard error, z-statistic, and probability for all

variables, except Maturity Time.

2. Religion

Since the Z-statistic < Z Table (1.101752 < 1.645) and p-value > 0.05 (0.2706 >

0.05), H0 is accepted. This means that the proportion of micro funds in saving

accounts which are owned by Muslim customers and the proportion of micro

funds in saving account which are owned by non-Muslim customers are the

same (no difference).

3. Job

Since the Z-statistic < Z Table 0.286765 < 1.645) and p-value > 0.05 (0.7743 >

0.05), H0 is accepted. This means that the proportion of micro funds in saving

44

accounts which are owned by employees (government office employee, state-

owned company employee, and private-owned company employee) and the

proportion of micro funds in saving accounts which are owned by other kind of

job (businessman, students, housewife, etc) are the same (no difference).

4. Age

Since the Z-statistic < Z Table (1.493357 < 1.645) and p-value > 0.05 (0.1353 >

0.05), H0 is accepted. This means that the proportion of micro funds in saving

account which are owned by people around productive age (25 ≤ Age ≤ 45 years

old) and the proportion of micro funds in saving account which are owned by

people under or over the productive age are the same (no difference).

Interpretation from the output of EViews 7:

1) Table 4.19 an 4.20 gives actual and predicted values of the regressand for the

equation. From this table there is information that, out of 384 observations, there

are 49 incorrect predictions (from number 336 to number 384). Hence, the count

comparative R2 value is shown below :

335384 0.8723958

Whereas McFadden R2 value from EViews 7 output is 0.012602. These two

values are not directly comparable. Based on the McFadden R2 value, type of

job, maturity time, age, and religion are represent and explain only 1.26% of the

whole factors that may affect the funding contribution from third party which is

a very small percentage. Meanwhile, there are 98.74% which are influenced by

other factors that are not stated in this research.

2) From the estimated Likelihood Ratio (LR) statistic, there is clear information

that four variables are statistically significant at about 44.87 percent level. Since

the using of 5 percent significance level, then these variables are not statistically

significant. So, all regressors have very low significant impact on the NTR

Value, as the LR statistic is 3.6954.

45

3) The positive sign of maturity date, religion, job and age are interpreted below.

1. Since the coefficient value of Job is 0.091682, job becomes the least

factor that influences the composition of micro funding at Bank X West

Java Regional Area. If the Job rate goes up by 1 percentage point, the

logit goes up by about 0.09162, holding other variable constant. Taking

the anti-log of 0.091682 (e0.091682), then the result is 1.0960. This means

that the saving accounts which is categorized as micro fund is 1.0960

times mostly owned by employee (government office employee, state-

owned company employee, and private-owned company employee) than

other kind of job (businessman, students, housewife, etc).

2. If the increment Maturity Date (MATDT) increased by 1 percentage

point, the logit also goes up by about 0.683323, holding other variable

constant.

Based on Table 4.19, Maturity Date has the highest coefficient than

others, which is 0.683323, Maturity Date has the biggest correlation to

the funding composition based on variety of funds saved. The coefficient

value of maturity date is the same with constant and all saving accounts

have the same maturity time which is 1 day. Therefore, no matter the

segment of its source, whether it is from micro, small, or commercial

funding, the maturity date is always 1 day because the customers have

right to withdraw their money in saving account anytime.

3. Since the coefficient value of Religion is 0.383188, religion becomes the

third biggest factor that influence the composition of micro funding at

Bank X West Java Regional Area. If the Religion rate goes up by 1

percentage point, the logit goes up by about 0.383188, holding other

variable constant. Counting anti-log of 0.383188 (e0.383188), then the

result is 1.467. This means that micro funds in saving accounts is 1.467

times more owned by Muslim than customers with other type of religion.

46

4. Since the coefficient value of Age is 0.470278, age becomes the second

biggest factor that influence the composition of micro funding at Bank X

West Java Regional Area. If the Age rate goes up by 1 percentage point,

the logit goes up by about 0.470278, holding other variable constant.

Taking anti-log of 0.470278 (e0.470278), then the result is 1.6. This means

that micro funds in saving accounts are 1.6 times more owned by

customers around productive age.

4.3.3.3 Current Account Logit Model Analysis

Table 4.21 Eviews 7 Output for Current Account (Including Maturity Date)

Dependent Variable: NTR Method: ML - Binary Logit (Quadratic hill climbing) Date: 07/20/10 Time: 20:11 Sample: 1 354 Included observations: 354 Convergence achieved after 5 iterations WARNING: Singular covariance - coefficients are not unique Covariance matrix computed using second derivatives

Variable Coefficient Std. Error z-Statistic Prob.

C 0.878795 NA NA NA MAT 0.878795 NA NA NA JOB -0.938705 NA NA NA

RELIGION 0.568316 NA NA NA AGE 0.711274 NA NA NA

McFadden R-squared 0.060314 Mean dependent var 0.864407 S.D. dependent var 0.342841 S.E. of regression 0.336947 Akaike info criterion 0.774138 Sum squared resid 39.62305 Schwarz criterion 0.828790 Log likelihood -132.0225 Hannan-Quinn criter. 0.795882 Deviance 264.0450 Restr. deviance 280.9928 Restr. log likelihood -140.4964 LR statistic 16.94783 Avg. log likelihood -0.372945 Prob(LR statistic) 0.001979

Obs with Dep=0 48 Total obs 354 Obs with Dep=1 306

47

Table 4.22 Eviews 7 Output for Current Account (Without Maturity Date)

Dependent Variable: NTR Method: ML - Binary Logit (Quadratic hill climbing) Date: 07/20/10 Time: 20:13 Sample: 1 354 Included observations: 354 Convergence achieved after 4 iterations Covariance matrix computed using second derivatives

Variable Coefficient Std. Error z-Statistic Prob.

C 1.757591 0.377521 4.655616 0.0000 JOB -0.938705 0.343244 -2.734800 0.0062

RELIGION 0.568316 0.353405 1.608116 0.1078 AGE 0.711274 0.370556 1.919481 0.0549

McFadden R-squared 0.060314 Mean dependent var 0.864407 S.D. dependent var 0.342841 S.E. of regression 0.336465 Akaike info criterion 0.768489 Sum squared resid 39.62305 Schwarz criterion 0.812210 Log likelihood -132.0225 Hannan-Quinn criter. 0.785884 Deviance 264.0450 Restr. deviance 280.9928 Restr. log likelihood -140.4964 LR statistic 16.94783 Avg. log likelihood -0.372945 Prob(LR statistic) 0.000724

Obs with Dep=0 48 Total obs 354 Obs with Dep=1 306

From the EViews 7 output in Table 4.21, the constant and coefficients from each

variables are known which are maturity date, job, religion, and age. The equation will

be as follows

. . . . .

On the other hand, since the maturity date seems constant, maturity date affects the

calculation of standard deviation, Z-test, and probability to be Not Applicable (NA) in

the calculation. Therefore, by eliminating the maturity date as variable and joining the

maturity date into constant, the Logit Model will be more make sense.

From the EViews 7 output in Table 4.22, for constant and coefficients from each

variables are known which are job, religion, and age. The equation will be as follows

. . . .

48

Proportion Test (Z-Test)

Based on Table 4.21, the result of Z-Test from Eviews 7 can be interpreted below :

1. Maturity Date (MATDT)

The input of Maturity Date in EViews 7 as variable on Table 4.21 makes the

result of standard error, z-statistic, and probability become Not-Applicable

(NA). Compared to Table 4.22, if the maturity date is not input, there are clear

information about the standard error, z-statistic, and probability for all

variables, except Maturity Date.

2. Religion

Since the Z-statistic < Z Table (1.608116 < 1.645) and p-value > 0.05 (0.1078 >

0.05), H0 is accepted. This means that the proportion of current accounts in form

of micro funds which are owned by Muslim customers and current accounts in

form of micro funds which are owned by non-Muslim customers are the same

(no difference).

3. Job

Since the Z-statistic < Z Table -2.734800 < 1.645 and p-value < 0.05 (0.0062 <

0.05), H0 is rejected (H1 accepted). This means that the proportion of current

accounts in form of micro funds which are owned by employees (government

office employee, state-owned company employee, and private-owned company

employee) are greater than the proportion of current accounts in form of micro

funds which are owned by other kind of job (businessman, students, housewife,

etc) are the same (no difference).

4. Age

Since the Z-statistic > Z Table (1.919481 > 1.645) and p-value > 0.05 (0.0549 >

0.05), H0 is rejected (H1 accepted). This means that the proportion of micro

funds in current account which is owned by people around productive age (25 ≤

Age ≤ 45 years old) is greater than the proportion of micro funds in current

accounts which are owned by people under or over the productive age.

49

Interpretation from the output of EViews 7:

1) Table 4.21 an 4.22 gives actual and predicted values of the regressand for the

equation. From this table there is information that, out of 384 observations, there

are 46 incorrect predictions (from number 307 to number 354). Hence, the count

comparative R2 value is shown below :

306354 0.864407

Whereas McFadden R2 value from EViews 7 output is 0.060314. These two

values are not directly comparable. Based on the McFadden R2 value, type of

job, maturity time, age, and religion are represent and explain only 6.0314% of

the whole factors that may affect the funding contribution from third party which

is a very small percentage. Meanwhile, there are 93.97% which are influenced

by other factors that are not stated in this research.

2) From the estimated Likelihood Ratio (LR) statistic, there is clear information

that four variables are statistically significant at about 0.0724 percent level.

Since the using of 5 percent significance level, then these variables are

statistically significant. So, all regressors have high impact on the NTR Value, as

the LR statistic is 16.94783.

3) The negative sign of job and positive sign of maturity date, religion, and age are

interpreted below.

1. Since the coefficient value of Job is -0.938705, job becomes the most

influencing factor to the composition of micro funding in current account at

Bank X West Java Regional Area. If the job rate goes up by 1 percentage

point, the logit goes down by about 0.938705, holding other variable

constant. Taking the anti-log of -0.938705 (e-0.938705), then the result is

0.3911. This means that 39.11% of funds in current accounts which are

owned by employee (government office employee, state-owned company

employee, and private-owned company employee) from micro funds.

50

2. If the increment Maturity Date (MATDT) increased by 1 percentage point,

the logit also goes up by about 0.878795, holding other variable constant.

Based on Table 4.21, Maturity Date has the second highest coefficient than

others, which is 0.878795. The coefficient value of maturity date is the same

with constant and all current accounts have the same maturity time which is

1 day. Therefore, no matter the segment of its source, whether it is from

micro, small, or commercial funding, the maturity date is always 1 day

because the customers have right to withdraw their money in current account

anytime and this makes the coefficient of maturity date grouped with the

constant to be 1.757591.

3. Since the coefficient value of Age is 0.711274, age becomes the third biggest

factor that influence the composition of micro funding in current account at

Bank X West Java Regional Area. If the Age rate goes up by 1 percentage

point, the logit goes up by about 0.711274, holding other variable constant.

Taking anti-log of 0.711274 (e0.711274), then the result is 2.0366. This means

that micro funds in saving accounts are 2.0366 times more owned by

customers around productive age.

4. Since the coefficient value of Religion is 0.568316, religion becomes the

least influencing factor to the composition of micro funding in current

account at Bank X West Java Regional Area. If the Religion rate goes up by

1 percentage point, the logit goes up by about 0.568316, holding other

variable constant. Counting anti-log of 0.568316 (e0.568316), then the result is

1.7653. This means that micro funds in current accounts is 1.7653 times

more owned by Muslim than customers with other type of religion.