99 CHAPTER IV Asset pricing model should predict its price correctly as that of the market and the residuals / error shoul systematic pattern with any of its variables / parameters that ar changes systematically with the change in variables then it is known as bias of the model. The residuals should be distributed normally. This chapter explains the predictability of the model and behaviour of th ption towards its variables li , of returns of the stock, exercise price, and risk-free interest rate. The findings of the study are explained in depth. Part research study was published in the book “ Manage t Pra Polic Princ [105], by The Allied Publishers Private Limited, New Delhi, after edited by a faculty of Indian Inst agem dore xure 4.2 EARL DIE Bla stat mar s of tions “t differ in certain sys ys” fr val by model tions with less than hs to tion optio are ei eep in or out of the rton ates est all pri r deep in the money dee f th opt less t e market prices. M and Mervil 4] op deep mone ons have model prices those are lower than market prices, whereas deep out of money options PREDICTABILITY OF THE BS MODEL IN INDIAN OPTION MARKET 4.1 INTRODUCTION d not have any e used to predict the price. If the error e call o prices ke stock price and life of the option and the parameters like volatility of this Business men ctices, ies and iples” itute of Man ent, In . (Anne I) IER STU S ck [21, 23] es that ket price call op end to tematic wa om the ues given the BS for op three mont expira and for ns that ther d money. Me [98] st that BS imated c ces fo as well as p out o e money ions are han th acbeth le [9 ine that in the y opti have model prices that are higher. These conflicts may perhaps be

Transcript

99

CHAPTER IV

Asset pricing model should predict its price correctly as that of the

market and the residuals / error shoul systematic pattern with

any of its variables / parameters that ar

changes systematically with the change in variables then it is known as bias of

the model. The residuals should be distributed normally. This chapter explains

the predictability of the model and behaviour of th ption towards its

variables li ,

of returns of the stock, exercise price, and risk-free interest rate. The findings of

the study are explained in depth. Part research study was published in

the book “ Manage t Pra Polic Princ [105], by

The Allied Publishers Private Limited, New Delhi, after edited by a faculty of

Indian Inst agem dore xure

4.2 EARL DIE Bla stat mar s of tions “t differ in

certain sys ys” fr val by model tions with

less than hs to tion optio are ei eep in or

out of the rton ates est all pri r deep in

the money dee f th opt less t e market

prices. M and Mervil 4] op deep mone ons have

model prices those are lower than market prices, whereas deep out of money

options

PREDICTABILITY OF THE BS MODEL IN INDIAN OPTION MARKET

4.1 INTRODUCTION

d not have any

e used to predict the price. If the error

e call o prices

ke stock price and life of the option and the parameters like volatility

of this

Business men ctices, ies and iples”

itute of Man ent, In . (Anne I)

IER STU S

ck [21, 23] es that ket price call op end to

tematic wa om the ues given the BS for op

three mont expira and for ns that ther d

money. Me [98] st that BS imated c ces fo

as well as p out o e money ions are han th

acbeth le [9 ine that in the y opti

have model prices that are higher. These conflicts may perhaps be

100

reconciled by the fact that the studies examined market prices at different points

in time and these systematic biases vary with time (Rubinstein [41,118]).

4.3 DEFINITIONS

Based on the above studies, this research tries to find the truth about

the predictability of the BS Model and pricing biases, if any, in the Indian option

market. The Mean Absolute Errors (MAE) calculated with the following formula

for various moneyness and various lives of the options are tabulated in the

Table 4.1.

Σ ׀ PO – PT׀ Mean Absolute Error = ------------------- Σ PO

where PT is the call option price theoretically calculated using BS model and PO

is the observed call option prices in the market.

Moneyness is defined as S0 / X and the values ranging 0.99 to 1.01 are

taken as at-the-money options, values les ed as out-of-

the-money options and above 1.01 as in-the-money options. As the number is

increasing the mo

Mean percentage errors are calculated using the following formula.

[{(PO – PT) / P ] Mean Percentage Er -------------- n

where n is the sample

The percentage he formu O – PT) / PO} x100] in

each of the options taken in the sample. Then, the sum of the percentage errors

is calculated and result is divided by the number of data “n”.

s than 0.99 is consider

neyness is also increasing.

Σror = -----------------

O} x100

size.

error is found using t la [{(P

101

Though the mean percentage error is misrepresenting in the cases of

very low option prices, it gives irection of the err enlighten us whether,

the BS model is overpricing or under-pricing the options. Thus it is considered

the research studies abroad are not

considering the deep out-of-the-money options and deep in-the-money options,

ut, they have so little data that they

cannot predict the market price correctly. If the data volume is not sufficient

the d or. It

as an important measure and used in the research.

4.4 CLASSIFICATION OF DATA

First, the call options that are offered by NSE were collected, analyzed

and the traded options were segregated from the non-traded ones. Then, using

the ex-dividend dates and dates of board meetings related to dividend

decisions, the options related to cum-dividend stocks during the life of the

options were eliminated. Lastly, the data are classified into fourteen groups of

moneyness each having three consecutive classes of moneyness. The

definition of moneyness is So / X. The classifications started from 0.83 to 1.20.

The classification is made in a way that ATM options of 1.00 lies at the center of

the classification (0.99 to 1.01). Though,

they have also studied in Indian context. B

enough they are not considered for making conclusion. The details are given in

Table no. 4.1

102

TABLE 4.1

DETAILS OF CALL OPTION TAKEN AS SAMPLE AS PER MONEYNESS

the final sample size is 95,956. Box-Plot analysis is used to identify the outliers,

whi exp in detail at chapter 6. The call options with moneyness

between 0.93 and 1.10 are having a reason

related to deep in-the-money and deep ou the

very little number of traded options, for which the market may not correctly price

e options. The distribution of the call options looks like a normal curve, but

Ou f the a e call on dat 21 out s have elimi ted and

ch is lained

able number of data. The other data

t-of- -money options are having

th

having fat tail.

103

CHART 4.1

DISTRIBUTION OF CALL OPTION DATA FOR VARIOUS MONEYNESS

DISTRIBUTION OF CALL OPTIONS

0

5,000

10,000

15,000

20,000

25,000

< 0.

83

0.84

-0.8

6

0.87

-0.8

9

0.90

-0.9

2

0.93

-0.9

5

0.96

-0.9

8

0.99

-1.0

1

1.02

-1.0

4

1.05

-1.0

7

1.08

-1.1

0

1.11

-1.1

3

1.14

-1.1

6

1.17

-1.1

9

> 1.

20

MONEYNESS

NO

. OF

CA

LL O

PTIO

NS

4.5 PREDICTABILITY OF THE MODEL

The main objective of this empirical study is the predictability of the

model. The predictability of the model is verified through mean absolute errors,

ross various

determinants of the call option price.

4.5.1 M

mean percentage error and the distribution of these errors ac

EAN ABSOLUTE ERRORS

The options were classified with different categories of moneyness,

processed and the option prices were calculated using BS model. The actual

markets prices of call options taken from the NSE website [68] were compared

104

with the respective predicted prices by the model and the MAE thus calculated

are summarized and shown in the table no. 4.2.

TE ERRORS OF OPTIONS WITH VARIOUS MONEYNESS

TABLE 4.2 MEAN ABSOLU

Moneyness No. Of data

Total Observed

Price

Total Absolute

Error

Mean Absolute

Error

< 0.83 187 4,130 1,635 0.40

0.84-0.86 370 7,265 3,720 0.51

0.87-0.89 1,005 17,501 9,349 0.53

0.90-0.92 3,163 54,356 28,077 0.52

0.93-0.95 8,671 155,569 66,442 0.43

0.96-0.98 17,112 383,157 127,623 0.33

0.99-1.01 21,984 624,996 154,049 0.25

1.02-1.04 17,643 660,766 114,602 0.17

1.05-1.07 11,191 542,341 70,111 0.13

1.08-1.10 6,550 378,344 45,151 0.12

1.11-1.13 3,854 251,920 26,870 0.11

1.14-1.16 2,328 164,207 16,709 0.10

1.17-1.19 1,383 101,157 11,043 0.11

> 1.20 515 62,963 7,688 0.12

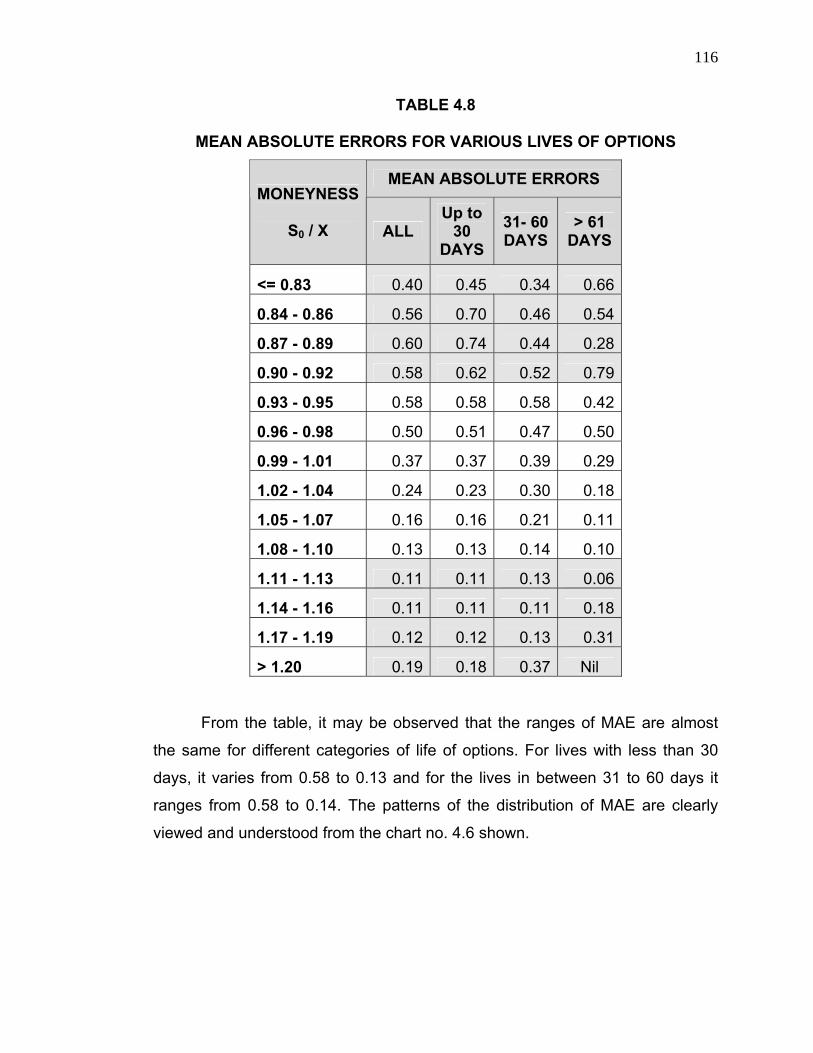

It may be observed from the above table, the MAE are as high as about

0.52 for the deep out-of-the-money options having moneyness 0.80 to 0.92.

Then it starts decreasing at a faster rate. For the moneyness of 0.93-0.95, it

dropped down by about 17% to 0.43 and for the next classification of 0.96-0.98,

it reduced by 23% to 0.33. Then, MAE are reduced by 24%, 32%, 23% and 7%

for next four moneynesses. At the end, it is almost flat.

105

The options that are having number of trades very less during the entire

period of five years and ten months (1716 working days) are illiquid and may

not reflect the correct price of the market. If we neglect the data related to

number of options less th ing the of study7; the MAE vary

from 0.12 to 0.43, with a m The clas tions of data with less than

5000 are shown in shades d not be considered for the conclusion

and are given only for the academic purpose. The mean predictability of the

model is around 76%. Mean is not a resistant summary of statistics and is

drastically influenced by th alues. Because of this, the predictability

of the model is low and the . For th ata without categories the

mean absolute error is 0.25 only. Let us also consider the resistant summary of

median based statistics. sorted in the ascending order. The

percentiles are calculated using SAS; values at t responding percentages

are given in the table no.4.3.

TABLE 4.3

an 5000 dur period

ean of 0.24. sifica

, which nee

e extreme v

error is high e full d

MAE are

he cor

PERCENTILES OF MEAN ABSOLUTE ERRORS

PERCENTILE ABSOLUTE ERRORS

100% 625.0199% 69.5195% 25.390% 15.62

Upper Quartile 75% 7.03Median 50% 3.12

Lower Quar 1.27tile 25%10% 0.475% 0.231% 0.050% 0

-------------------------------------------------------------------------------------------------------7Gurdip Bakshi, Charles Cao, and Zhiwu Chen in their study [10] considered data with

more than 4500 only during the period of 3 years.

106

A percentile8 is the value of a variable below which a certain percent of

observations fall. So the 20th percentile is the value (or score) below which 20

percent of the observations may be found. Fifty percentages of the options are

having MAE less than 3.12. The next 25% of the sample are having MAEs

within 3.12 to 7.03. The next 15%of the options are having errors from 7.03 to

15.62. It means, that the BS model predicted the call option prices with a

minimum accuracy of 84.38% for ninety percentages (86,360 options) of the

sample of 95,956. A very small portion of the options are having higher errors.

Thus, it may be inferred that the BS model is good as far as MAE are

considered. The median based statistics give better picture of the error

n the mean, which is influenced by the extreme values.

rs are considered to nullify the effect of positive and